Management Accounting Systems: Cost Analysis and Budgetary Tools

VerifiedAdded on 2024/05/20

|17

|4078

|354

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems, techniques, and their application within an organizational context, specifically focusing on Zylla. It explains management accounting and its essential requirements, covering job accounting, price optimizing, cost accounting, and inventory management systems. Different methods used for management accounting reporting, such as budget reports, cost reports, inventory management reports, and sales reports, are also discussed. The report evaluates the benefits of management accounting systems in reducing expenses, increasing profitability, enhancing decision-making, and improving productivity. It also explains the advantages and disadvantages of various planning tools used in budgetary control, including financial budgets, non-monetary budgets, and operational budgets, and analyzes their application for preparing and forecasting budgets. The report calculates costs using marginal and absorption costing techniques to prepare an income statement and compares how organizations adapt management accounting systems to respond to financial problems, ultimately analyzing how management accounting can lead organizations to sustainable success.

Unit 5 Management accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction................................................................................................................................3

P1 Explain management accounting and give the essential requirements of different types of

management accounting.............................................................................................................4

P2 Explain different methods used for management accounting reporting...............................5

M1 Evaluate the benefits of management accounting systems and their application within an

organisational context................................................................................................................6

P4 Explain the advantages and disadvantages of different types of planning tools used in

budgetary control...................................................................................................................7

M3 Analyse the use of different planning tools and their application for preparing and

forecasting budgets.............................................................................................................9

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costing....................................................................10

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems....................................................................................................................13

M4 Analyse how, responding to financial problems, management accounting can lead

organisations to sustainable success.........................................................................................14

Conclusion................................................................................................................................15

References................................................................................................................................16

2

Introduction................................................................................................................................3

P1 Explain management accounting and give the essential requirements of different types of

management accounting.............................................................................................................4

P2 Explain different methods used for management accounting reporting...............................5

M1 Evaluate the benefits of management accounting systems and their application within an

organisational context................................................................................................................6

P4 Explain the advantages and disadvantages of different types of planning tools used in

budgetary control...................................................................................................................7

M3 Analyse the use of different planning tools and their application for preparing and

forecasting budgets.............................................................................................................9

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costing....................................................................10

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems....................................................................................................................13

M4 Analyse how, responding to financial problems, management accounting can lead

organisations to sustainable success.........................................................................................14

Conclusion................................................................................................................................15

References................................................................................................................................16

2

Introduction:

In complex and competitive scenario, management accounting has become essential and

useful for decision making and simplifying complex situation. Zylla is an organisation, which

has gone through number of changes and the directors are of the view that the existing

systems need to go through changes and more appropriate system need to be installed which

are in accordance with the changing requirements of the system. Management accounting

systems provides large interface for keeping organisation data and designing activities in

appropriate manner. Thus, this management accounting report will make analyses of

management systems and management accounting techniques and there will also be analyses

of financial tools for responding financial issues. There will also be practical examples of

costing to show understanding about the varied accounting techniques.

3

In complex and competitive scenario, management accounting has become essential and

useful for decision making and simplifying complex situation. Zylla is an organisation, which

has gone through number of changes and the directors are of the view that the existing

systems need to go through changes and more appropriate system need to be installed which

are in accordance with the changing requirements of the system. Management accounting

systems provides large interface for keeping organisation data and designing activities in

appropriate manner. Thus, this management accounting report will make analyses of

management systems and management accounting techniques and there will also be analyses

of financial tools for responding financial issues. There will also be practical examples of

costing to show understanding about the varied accounting techniques.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P1 Explain management accounting and give the essential requirements for different

types of management accounting.

Management accounting can be defined as a mechanism whereby data are collected,

recorded, and interpreted for relevant decision making. The origin of management accounting

was initiated from 18th century itself and with the increase in working complexities; there was

huge development in management models, theories and systems. There are large management

accounting systems such as cost accounting system, job accounting system, price optimising

system and inventory management system and their essential requirements are discussed here

below:

Job accounting system: This system is formulated with a view to estimate the costing for

specific jobs or batch systems. Different specific batches have their own costing criteria and

batches have to be costs accordingly. The most essential requirement of this system is that it

aids in assessing costing for units, it aids in inventory valuation, profitability measures and

also useful in comparing one batch costing with another batch costing(Guga, & Musa, 2015).

Price optimising system: This system can be defined as a system which is used for

estimating prices for different set of products. This system is mainly used for estimating

people reactions at different pricing and optimum pricing policy is used for estimating

product’s pricing. Optimum pricing strategy aid organisation in reaching its products to wide

range of consumers and making huge sales. Increasing sales is always one of the crucial

agenda for any organisation (Guga, & Musa, 2015).

Cost accounting system: This is a system which is used for estimating different set of costs

such as variable cost and fixed costs and other overheads costing, analyses of inventory

valuation and profitability analysis. Assigning costs to products manufactured is a critical job

which has to be done so as to assess the profitability portion and the productive capacity of a

concern.

Inventory management system: This system is implemented for analysing the inventory

level, re-order level, re-order capacity, productive capacity, EOQ level etc. Inventory can be

effectively managed through this system. For a manufacturing concern, it is highly useful that

investment in inventories is done appropriately and with due to attention so as to not invest

large funds into inventory mechanism. Thus, the major essential are that it eliminates

4

types of management accounting.

Management accounting can be defined as a mechanism whereby data are collected,

recorded, and interpreted for relevant decision making. The origin of management accounting

was initiated from 18th century itself and with the increase in working complexities; there was

huge development in management models, theories and systems. There are large management

accounting systems such as cost accounting system, job accounting system, price optimising

system and inventory management system and their essential requirements are discussed here

below:

Job accounting system: This system is formulated with a view to estimate the costing for

specific jobs or batch systems. Different specific batches have their own costing criteria and

batches have to be costs accordingly. The most essential requirement of this system is that it

aids in assessing costing for units, it aids in inventory valuation, profitability measures and

also useful in comparing one batch costing with another batch costing(Guga, & Musa, 2015).

Price optimising system: This system can be defined as a system which is used for

estimating prices for different set of products. This system is mainly used for estimating

people reactions at different pricing and optimum pricing policy is used for estimating

product’s pricing. Optimum pricing strategy aid organisation in reaching its products to wide

range of consumers and making huge sales. Increasing sales is always one of the crucial

agenda for any organisation (Guga, & Musa, 2015).

Cost accounting system: This is a system which is used for estimating different set of costs

such as variable cost and fixed costs and other overheads costing, analyses of inventory

valuation and profitability analysis. Assigning costs to products manufactured is a critical job

which has to be done so as to assess the profitability portion and the productive capacity of a

concern.

Inventory management system: This system is implemented for analysing the inventory

level, re-order level, re-order capacity, productive capacity, EOQ level etc. Inventory can be

effectively managed through this system. For a manufacturing concern, it is highly useful that

investment in inventories is done appropriately and with due to attention so as to not invest

large funds into inventory mechanism. Thus, the major essential are that it eliminates

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

excessive implementation of funds, shortage or crisis of inventory, and maintains smooth

flow of inventory into organisation processes (Guga, & Musa, 2015).

P2 Explain different methods used for management accounting reporting.

Management accounting reporting is done so that information interpreted and concluded into

systems can be recorded and analyzed thoroughly. This reporting are further used for making

communications with specific personnel and their aids them with future decision making and

relevant opportunities. The different methods used for management accounting reporting are

a budget report, cost report, inventory management report, sales report etc.

Budget report: This budget report is formulated for making budgeting figures regarding

sales, production, financial budget etc. These reports are formulated with a view to make a

thorough interpretation of the budgeted figures. Budget reports are made for production,

sales, inventories, cash budget, financial budget etc. The budget report makes analyses about

the effectiveness of budgeting figures and budgeting assumptions (Isaac, et. al.,2015).

Inventory management report: This report considers inventory valuation and analyses the

level at which inventory must be purchased and keep a complete record of maintenance of

inventory level. This report is quite essential as it defines the blockage of funds into

inventories and also about the inventory level which must be maintained so as to make the

uninterrupted flow of inventories channel.

Sales report: this report defines the number of units and recognizes the revenue. This report

is prepared on the basis of a different set of periods i.e. quarterly, monthly, yearly etc. This

report will provide answer related to existing sales and sales forecasting as well. Varied

operational tools are implemented over the sales figures for making a further interpretation to

be used for future reference (Isaac, et. al., 2015).

Cost report: This report defines costing calculation of a different set of products produced by

companies. It is a useful report which provides a guide for future costing, profitability

analysis, and ascertaining liquidity of the company. Costing directly affects various factors

such as expenses, revenues, administration, profitability etc. and thus, is useful for the

organization productivity.

5

flow of inventory into organisation processes (Guga, & Musa, 2015).

P2 Explain different methods used for management accounting reporting.

Management accounting reporting is done so that information interpreted and concluded into

systems can be recorded and analyzed thoroughly. This reporting are further used for making

communications with specific personnel and their aids them with future decision making and

relevant opportunities. The different methods used for management accounting reporting are

a budget report, cost report, inventory management report, sales report etc.

Budget report: This budget report is formulated for making budgeting figures regarding

sales, production, financial budget etc. These reports are formulated with a view to make a

thorough interpretation of the budgeted figures. Budget reports are made for production,

sales, inventories, cash budget, financial budget etc. The budget report makes analyses about

the effectiveness of budgeting figures and budgeting assumptions (Isaac, et. al.,2015).

Inventory management report: This report considers inventory valuation and analyses the

level at which inventory must be purchased and keep a complete record of maintenance of

inventory level. This report is quite essential as it defines the blockage of funds into

inventories and also about the inventory level which must be maintained so as to make the

uninterrupted flow of inventories channel.

Sales report: this report defines the number of units and recognizes the revenue. This report

is prepared on the basis of a different set of periods i.e. quarterly, monthly, yearly etc. This

report will provide answer related to existing sales and sales forecasting as well. Varied

operational tools are implemented over the sales figures for making a further interpretation to

be used for future reference (Isaac, et. al., 2015).

Cost report: This report defines costing calculation of a different set of products produced by

companies. It is a useful report which provides a guide for future costing, profitability

analysis, and ascertaining liquidity of the company. Costing directly affects various factors

such as expenses, revenues, administration, profitability etc. and thus, is useful for the

organization productivity.

5

M1 Evaluate the benefits of management accounting systems and their application

within an organisational context.

Management accounting systems are highly beneficial in relation to resolving financial issues

and resolving decision-making issues. The following are the benefits of management

accounting systems:

Reduces expenses: Management systems are used for the purpose of reducing expenses.

These systems are produced with a view to eliminating duplication of activities, controls

costing, evaluate profitability etc. Thus, systems are produced with a view to eliminating

any form of costing (Legaspi, 2014).

Increases profitability: These systems are evaluated with a view to collect and interpret

data at one place. All the data are collected at a single place and are used for increasing

profitability for all.

Decision-making processing: Managers requires a large set of information for different

decision processes. Costing and pricing systems are used for interpreting different

information and or evaluating costing and pricing of products (Legaspi, 2014).

Enhances productivity: the management systems techniques are also highly useful for

enhancing organization productivity. The management processes get improvised through

management systems as it measures the most effective process and measures variances

accordingly (Aduda, and Ndaita, 2017).

In an organization context and specifically in a manufacturing concern like Zylla, various

manufacturing processes continue which can take the benefits of management systems. The

systems would be useful in estimating costs for different batches and analyses the

profitability accordingly. The inventory management also analyses the costs of inventory

level and estimate cost of products, accordingly. Thus, all the systems are highly useful and

beneficial.

6

within an organisational context.

Management accounting systems are highly beneficial in relation to resolving financial issues

and resolving decision-making issues. The following are the benefits of management

accounting systems:

Reduces expenses: Management systems are used for the purpose of reducing expenses.

These systems are produced with a view to eliminating duplication of activities, controls

costing, evaluate profitability etc. Thus, systems are produced with a view to eliminating

any form of costing (Legaspi, 2014).

Increases profitability: These systems are evaluated with a view to collect and interpret

data at one place. All the data are collected at a single place and are used for increasing

profitability for all.

Decision-making processing: Managers requires a large set of information for different

decision processes. Costing and pricing systems are used for interpreting different

information and or evaluating costing and pricing of products (Legaspi, 2014).

Enhances productivity: the management systems techniques are also highly useful for

enhancing organization productivity. The management processes get improvised through

management systems as it measures the most effective process and measures variances

accordingly (Aduda, and Ndaita, 2017).

In an organization context and specifically in a manufacturing concern like Zylla, various

manufacturing processes continue which can take the benefits of management systems. The

systems would be useful in estimating costs for different batches and analyses the

profitability accordingly. The inventory management also analyses the costs of inventory

level and estimate cost of products, accordingly. Thus, all the systems are highly useful and

beneficial.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

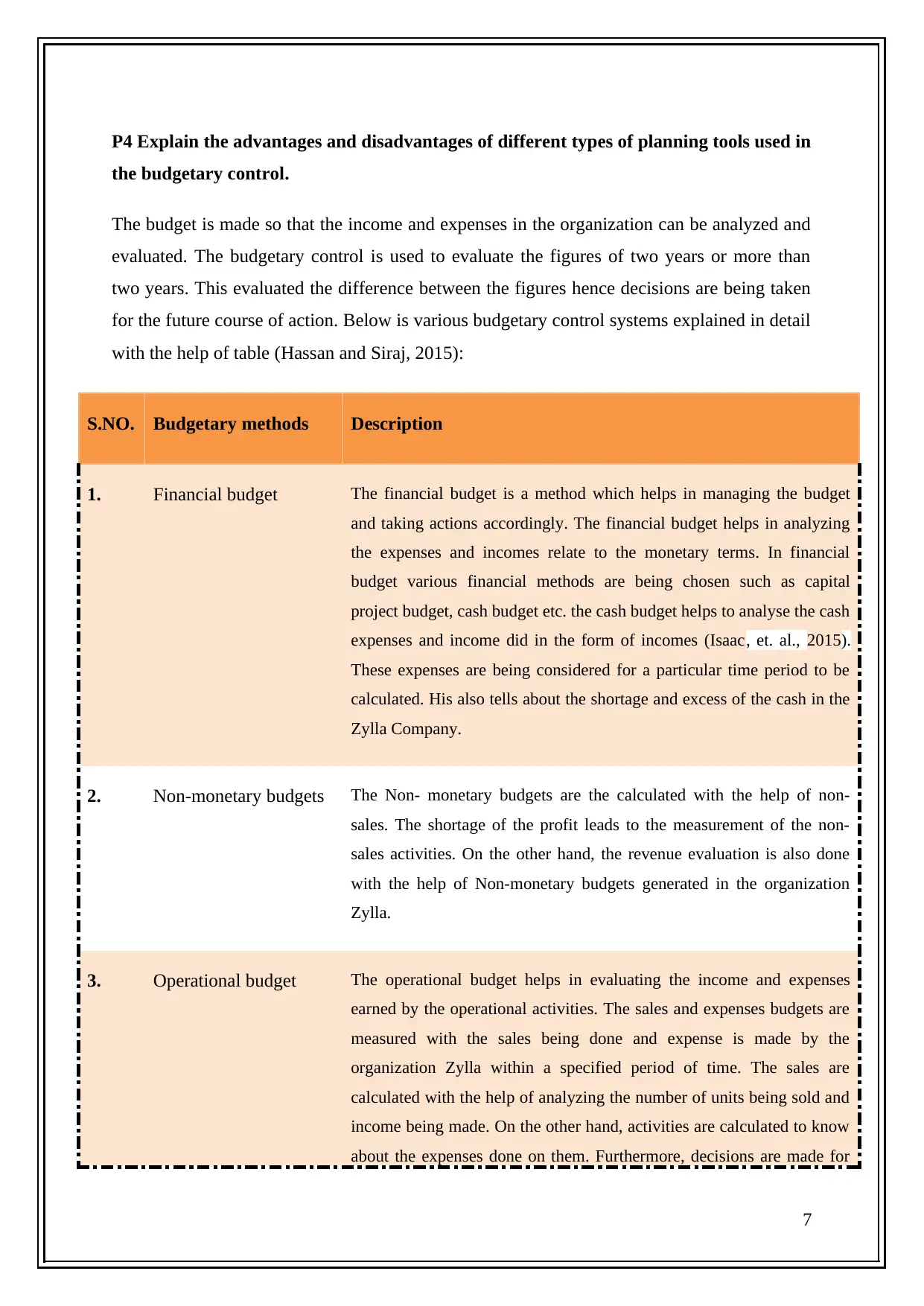

P4 Explain the advantages and disadvantages of different types of planning tools used in

the budgetary control.

The budget is made so that the income and expenses in the organization can be analyzed and

evaluated. The budgetary control is used to evaluate the figures of two years or more than

two years. This evaluated the difference between the figures hence decisions are being taken

for the future course of action. Below is various budgetary control systems explained in detail

with the help of table (Hassan and Siraj, 2015):

S.NO. Budgetary methods Description

1. Financial budget The financial budget is a method which helps in managing the budget

and taking actions accordingly. The financial budget helps in analyzing

the expenses and incomes relate to the monetary terms. In financial

budget various financial methods are being chosen such as capital

project budget, cash budget etc. the cash budget helps to analyse the cash

expenses and income did in the form of incomes (Isaac, et. al., 2015).

These expenses are being considered for a particular time period to be

calculated. His also tells about the shortage and excess of the cash in the

Zylla Company.

2. Non-monetary budgets The Non- monetary budgets are the calculated with the help of non-

sales. The shortage of the profit leads to the measurement of the non-

sales activities. On the other hand, the revenue evaluation is also done

with the help of Non-monetary budgets generated in the organization

Zylla.

3. Operational budget The operational budget helps in evaluating the income and expenses

earned by the operational activities. The sales and expenses budgets are

measured with the sales being done and expense is made by the

organization Zylla within a specified period of time. The sales are

calculated with the help of analyzing the number of units being sold and

income being made. On the other hand, activities are calculated to know

about the expenses done on them. Furthermore, decisions are made for

7

the budgetary control.

The budget is made so that the income and expenses in the organization can be analyzed and

evaluated. The budgetary control is used to evaluate the figures of two years or more than

two years. This evaluated the difference between the figures hence decisions are being taken

for the future course of action. Below is various budgetary control systems explained in detail

with the help of table (Hassan and Siraj, 2015):

S.NO. Budgetary methods Description

1. Financial budget The financial budget is a method which helps in managing the budget

and taking actions accordingly. The financial budget helps in analyzing

the expenses and incomes relate to the monetary terms. In financial

budget various financial methods are being chosen such as capital

project budget, cash budget etc. the cash budget helps to analyse the cash

expenses and income did in the form of incomes (Isaac, et. al., 2015).

These expenses are being considered for a particular time period to be

calculated. His also tells about the shortage and excess of the cash in the

Zylla Company.

2. Non-monetary budgets The Non- monetary budgets are the calculated with the help of non-

sales. The shortage of the profit leads to the measurement of the non-

sales activities. On the other hand, the revenue evaluation is also done

with the help of Non-monetary budgets generated in the organization

Zylla.

3. Operational budget The operational budget helps in evaluating the income and expenses

earned by the operational activities. The sales and expenses budgets are

measured with the sales being done and expense is made by the

organization Zylla within a specified period of time. The sales are

calculated with the help of analyzing the number of units being sold and

income being made. On the other hand, activities are calculated to know

about the expenses done on them. Furthermore, decisions are made for

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

future by analyzing the expenses and income at a specifies amount of

time

8

time

8

M3 Analyse the use of different planning tools and their application for preparing and

forecasting budgets.

Planning tools helps in making planning about various budgets in the organization Zylla. The

planning tools help in preparing for the future and implementing those decisions. Various

budgets are used as a tool such as capital budgets, cash budgets, and operational budgets etc.

(De Toni, et. al., 2017).

These uses of different planning tool are and their applications for forecast situations and

implementing the decisions accordingly. These uses are explained below in brief:

Decision making: The planning tool helps in taking effective decisions in the organization

Zylla. The decisions must be taken by analyzing each of the factors which negatively affects

the decision. Strategies are made so that control can be made on these factors (Isaac, et. al.,

2015). Some standards are set so that evaluation of the implementation of the actions can be

done and the outcome can be received according to the planning (De Toni, et. al., 2017).

Future Forecasting: The decisions are being made in such a manner so that future can be

predicted and actions are being taken accordingly. This future forecast helps in saving the

resources and using them in an appropriate manner. Moreover, it also helps in preparing a

budget and applying the resources after evaluation of the percentage of income, expenditure,

and revenues (De Toni, et. al., 2017).

9

forecasting budgets.

Planning tools helps in making planning about various budgets in the organization Zylla. The

planning tools help in preparing for the future and implementing those decisions. Various

budgets are used as a tool such as capital budgets, cash budgets, and operational budgets etc.

(De Toni, et. al., 2017).

These uses of different planning tool are and their applications for forecast situations and

implementing the decisions accordingly. These uses are explained below in brief:

Decision making: The planning tool helps in taking effective decisions in the organization

Zylla. The decisions must be taken by analyzing each of the factors which negatively affects

the decision. Strategies are made so that control can be made on these factors (Isaac, et. al.,

2015). Some standards are set so that evaluation of the implementation of the actions can be

done and the outcome can be received according to the planning (De Toni, et. al., 2017).

Future Forecasting: The decisions are being made in such a manner so that future can be

predicted and actions are being taken accordingly. This future forecast helps in saving the

resources and using them in an appropriate manner. Moreover, it also helps in preparing a

budget and applying the resources after evaluation of the percentage of income, expenditure,

and revenues (De Toni, et. al., 2017).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

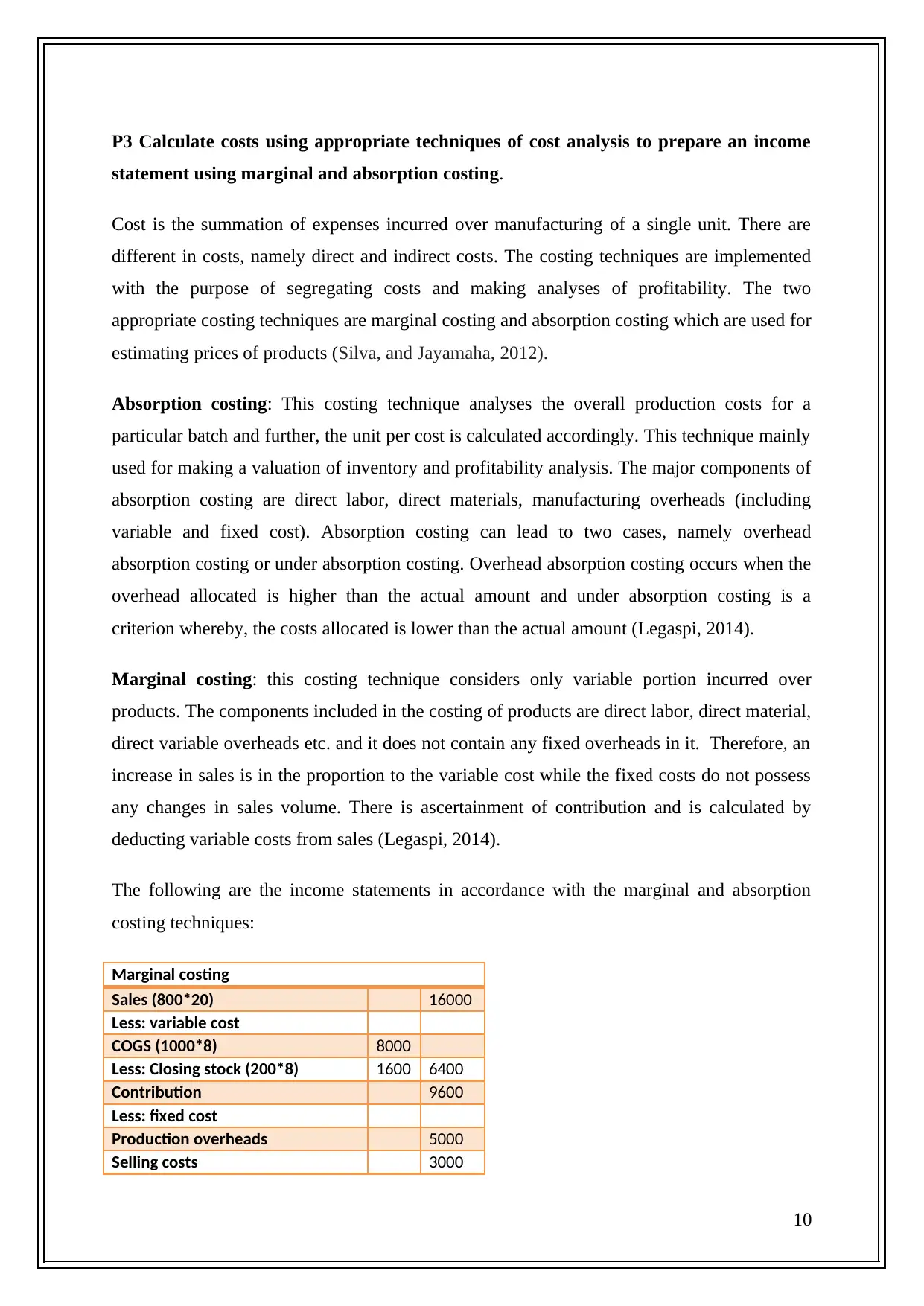

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costing.

Cost is the summation of expenses incurred over manufacturing of a single unit. There are

different in costs, namely direct and indirect costs. The costing techniques are implemented

with the purpose of segregating costs and making analyses of profitability. The two

appropriate costing techniques are marginal costing and absorption costing which are used for

estimating prices of products (Silva, and Jayamaha, 2012).

Absorption costing: This costing technique analyses the overall production costs for a

particular batch and further, the unit per cost is calculated accordingly. This technique mainly

used for making a valuation of inventory and profitability analysis. The major components of

absorption costing are direct labor, direct materials, manufacturing overheads (including

variable and fixed cost). Absorption costing can lead to two cases, namely overhead

absorption costing or under absorption costing. Overhead absorption costing occurs when the

overhead allocated is higher than the actual amount and under absorption costing is a

criterion whereby, the costs allocated is lower than the actual amount (Legaspi, 2014).

Marginal costing: this costing technique considers only variable portion incurred over

products. The components included in the costing of products are direct labor, direct material,

direct variable overheads etc. and it does not contain any fixed overheads in it. Therefore, an

increase in sales is in the proportion to the variable cost while the fixed costs do not possess

any changes in sales volume. There is ascertainment of contribution and is calculated by

deducting variable costs from sales (Legaspi, 2014).

The following are the income statements in accordance with the marginal and absorption

costing techniques:

Marginal costing

Sales (800*20) 16000

Less: variable cost

COGS (1000*8) 8000

Less: Closing stock (200*8) 1600 6400

Contribution 9600

Less: fixed cost

Production overheads 5000

Selling costs 3000

10

statement using marginal and absorption costing.

Cost is the summation of expenses incurred over manufacturing of a single unit. There are

different in costs, namely direct and indirect costs. The costing techniques are implemented

with the purpose of segregating costs and making analyses of profitability. The two

appropriate costing techniques are marginal costing and absorption costing which are used for

estimating prices of products (Silva, and Jayamaha, 2012).

Absorption costing: This costing technique analyses the overall production costs for a

particular batch and further, the unit per cost is calculated accordingly. This technique mainly

used for making a valuation of inventory and profitability analysis. The major components of

absorption costing are direct labor, direct materials, manufacturing overheads (including

variable and fixed cost). Absorption costing can lead to two cases, namely overhead

absorption costing or under absorption costing. Overhead absorption costing occurs when the

overhead allocated is higher than the actual amount and under absorption costing is a

criterion whereby, the costs allocated is lower than the actual amount (Legaspi, 2014).

Marginal costing: this costing technique considers only variable portion incurred over

products. The components included in the costing of products are direct labor, direct material,

direct variable overheads etc. and it does not contain any fixed overheads in it. Therefore, an

increase in sales is in the proportion to the variable cost while the fixed costs do not possess

any changes in sales volume. There is ascertainment of contribution and is calculated by

deducting variable costs from sales (Legaspi, 2014).

The following are the income statements in accordance with the marginal and absorption

costing techniques:

Marginal costing

Sales (800*20) 16000

Less: variable cost

COGS (1000*8) 8000

Less: Closing stock (200*8) 1600 6400

Contribution 9600

Less: fixed cost

Production overheads 5000

Selling costs 3000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

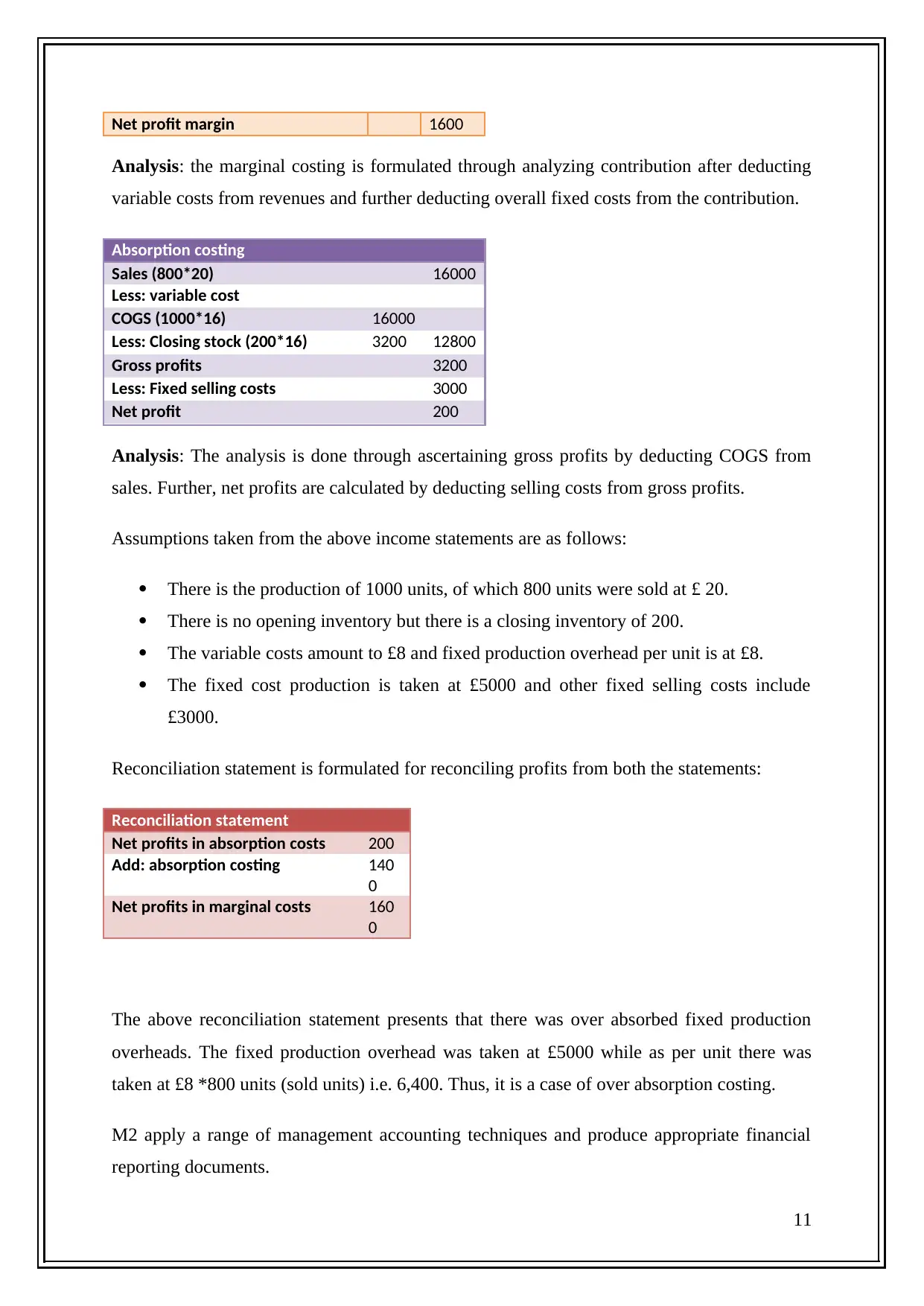

Net profit margin 1600

Analysis: the marginal costing is formulated through analyzing contribution after deducting

variable costs from revenues and further deducting overall fixed costs from the contribution.

Absorption costing

Sales (800*20) 16000

Less: variable cost

COGS (1000*16) 16000

Less: Closing stock (200*16) 3200 12800

Gross profits 3200

Less: Fixed selling costs 3000

Net profit 200

Analysis: The analysis is done through ascertaining gross profits by deducting COGS from

sales. Further, net profits are calculated by deducting selling costs from gross profits.

Assumptions taken from the above income statements are as follows:

There is the production of 1000 units, of which 800 units were sold at £ 20.

There is no opening inventory but there is a closing inventory of 200.

The variable costs amount to £8 and fixed production overhead per unit is at £8.

The fixed cost production is taken at £5000 and other fixed selling costs include

£3000.

Reconciliation statement is formulated for reconciling profits from both the statements:

Reconciliation statement

Net profits in absorption costs 200

Add: absorption costing 140

0

Net profits in marginal costs 160

0

The above reconciliation statement presents that there was over absorbed fixed production

overheads. The fixed production overhead was taken at £5000 while as per unit there was

taken at £8 *800 units (sold units) i.e. 6,400. Thus, it is a case of over absorption costing.

M2 apply a range of management accounting techniques and produce appropriate financial

reporting documents.

11

Analysis: the marginal costing is formulated through analyzing contribution after deducting

variable costs from revenues and further deducting overall fixed costs from the contribution.

Absorption costing

Sales (800*20) 16000

Less: variable cost

COGS (1000*16) 16000

Less: Closing stock (200*16) 3200 12800

Gross profits 3200

Less: Fixed selling costs 3000

Net profit 200

Analysis: The analysis is done through ascertaining gross profits by deducting COGS from

sales. Further, net profits are calculated by deducting selling costs from gross profits.

Assumptions taken from the above income statements are as follows:

There is the production of 1000 units, of which 800 units were sold at £ 20.

There is no opening inventory but there is a closing inventory of 200.

The variable costs amount to £8 and fixed production overhead per unit is at £8.

The fixed cost production is taken at £5000 and other fixed selling costs include

£3000.

Reconciliation statement is formulated for reconciling profits from both the statements:

Reconciliation statement

Net profits in absorption costs 200

Add: absorption costing 140

0

Net profits in marginal costs 160

0

The above reconciliation statement presents that there was over absorbed fixed production

overheads. The fixed production overhead was taken at £5000 while as per unit there was

taken at £8 *800 units (sold units) i.e. 6,400. Thus, it is a case of over absorption costing.

M2 apply a range of management accounting techniques and produce appropriate financial

reporting documents.

11

The two techniques namely, absorption and marginal costing are implemented. Both

techniques have a different set of assumptions and produce a different set of income

statements. In the above, income statements are based on both the techniques and the

difference in their figures is due to mainly following reasons:

The inventory valuation is different in both the concept and it is mainly due to the

ascertainment of fixed cost. The fixed cost in marginal costs is not taken into

consideration while assessing the valuable contribution and only variable component

is taken into consideration. On the other hand, in absorption costing, both the variable

and fixed component is taken into consideration.

The difference in the net profit margins is due to over-absorption of fixed cost

element in the absorption costing by 1400 (6400 (800*8) – 5000). The actual

production costs were only £5000 while the costing was done £ 8 per unit of 800 units

sold. The reporting documents are described as above and the assumptions are made

accordingly (Aruomoaghe, & Agbo, 2013).

12

techniques have a different set of assumptions and produce a different set of income

statements. In the above, income statements are based on both the techniques and the

difference in their figures is due to mainly following reasons:

The inventory valuation is different in both the concept and it is mainly due to the

ascertainment of fixed cost. The fixed cost in marginal costs is not taken into

consideration while assessing the valuable contribution and only variable component

is taken into consideration. On the other hand, in absorption costing, both the variable

and fixed component is taken into consideration.

The difference in the net profit margins is due to over-absorption of fixed cost

element in the absorption costing by 1400 (6400 (800*8) – 5000). The actual

production costs were only £5000 while the costing was done £ 8 per unit of 800 units

sold. The reporting documents are described as above and the assumptions are made

accordingly (Aruomoaghe, & Agbo, 2013).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.