2104AFE Management Accounting: Budgeting, Ethical Dilemmas & Solutions

VerifiedAdded on 2023/06/04

|9

|1976

|241

Report

AI Summary

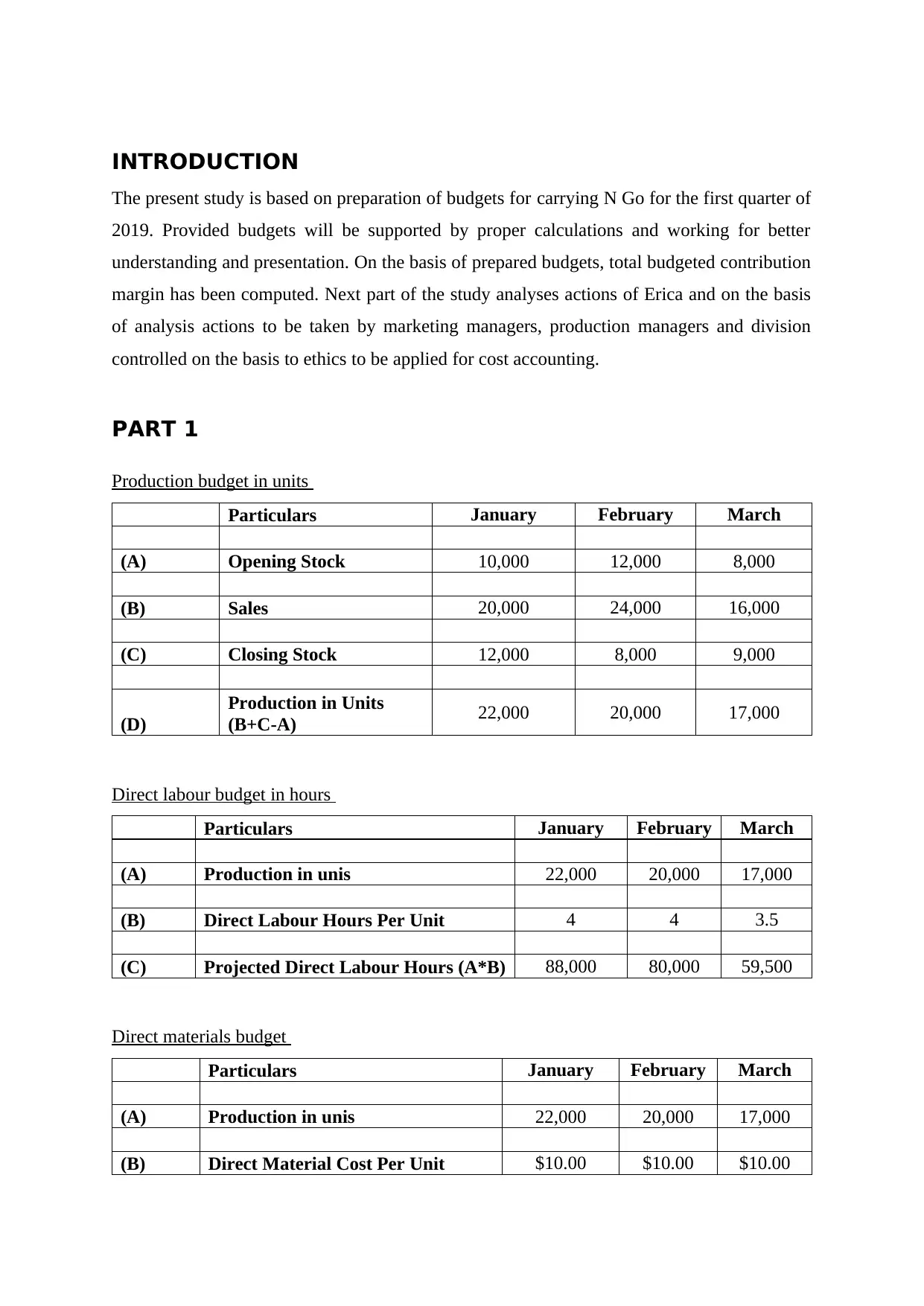

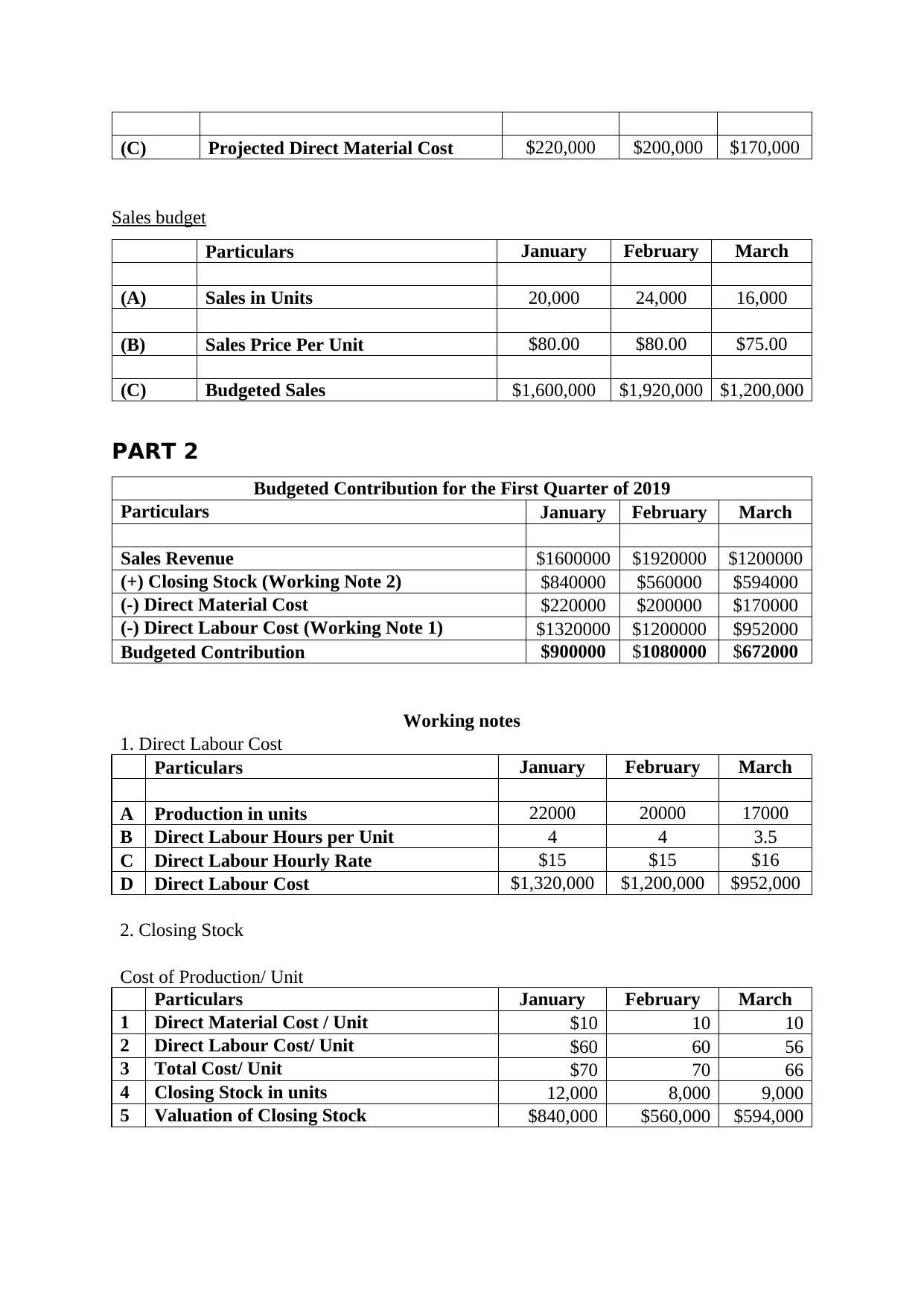

This report provides a comprehensive analysis of budgeting processes and ethical considerations within management accounting, specifically in the context of 'Carry N Go' division of Buffalo Corporation. It includes the preparation of various budgets such as production, direct labor, direct materials, and sales budgets for the first quarter of 2019. The report computes the budgeted contribution margin and delves into an ethical dilemma involving a division manager's actions to attain a bonus, discussing the implications and appropriate responses from marketing and production managers, as well as the division controller. The analysis incorporates ethical standards from APESB and proposes modifications to the bonus plan to ensure fairness and ethical conduct. The report concludes by emphasizing the importance of accurate cost recording and ethical practices in achieving sustainable business growth and profitability. Desklib offers more solved assignments for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.