Management Accounting Report: Financial Planning, Budgeting & Analysis

VerifiedAdded on 2024/05/16

|22

|3908

|355

Report

AI Summary

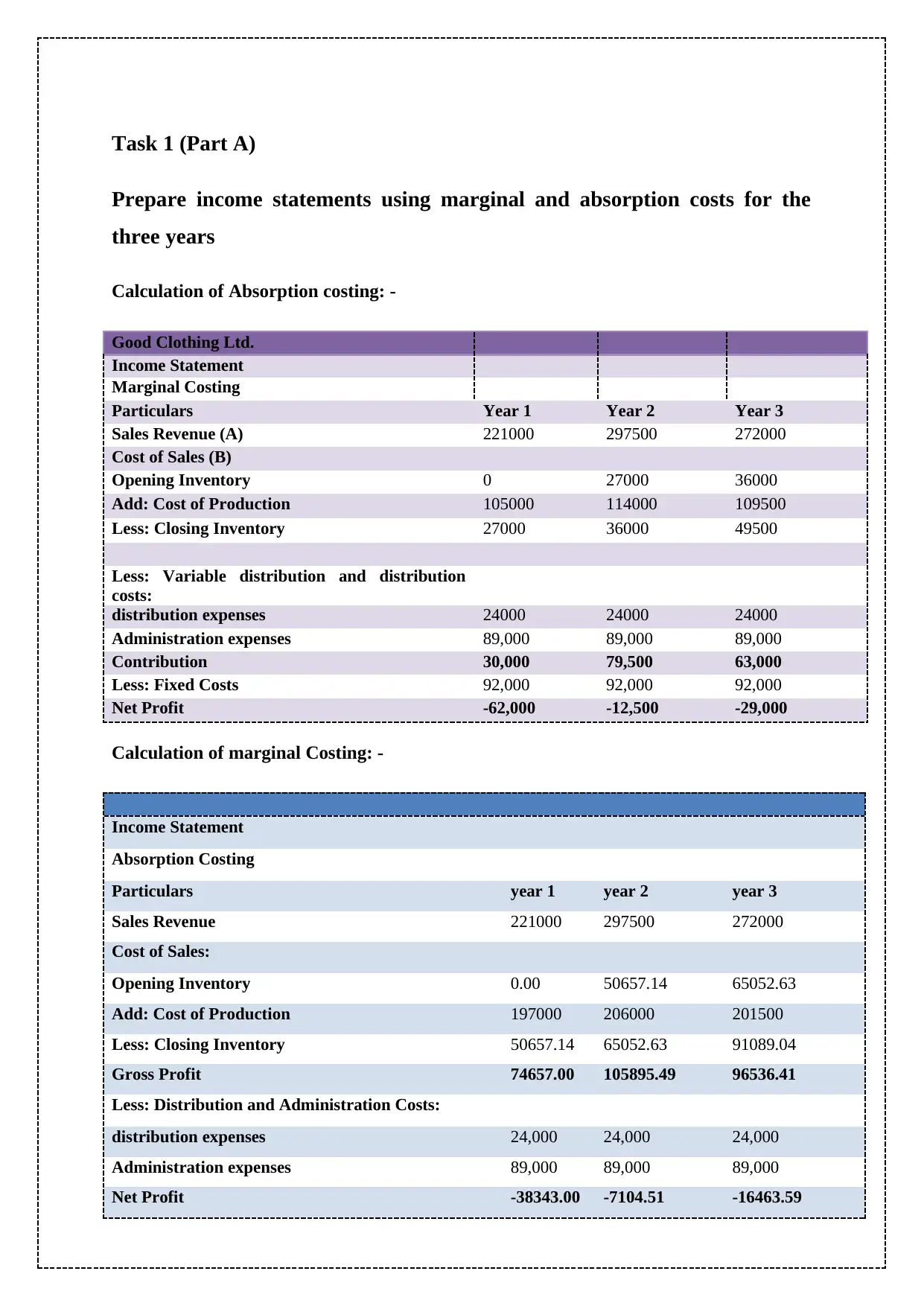

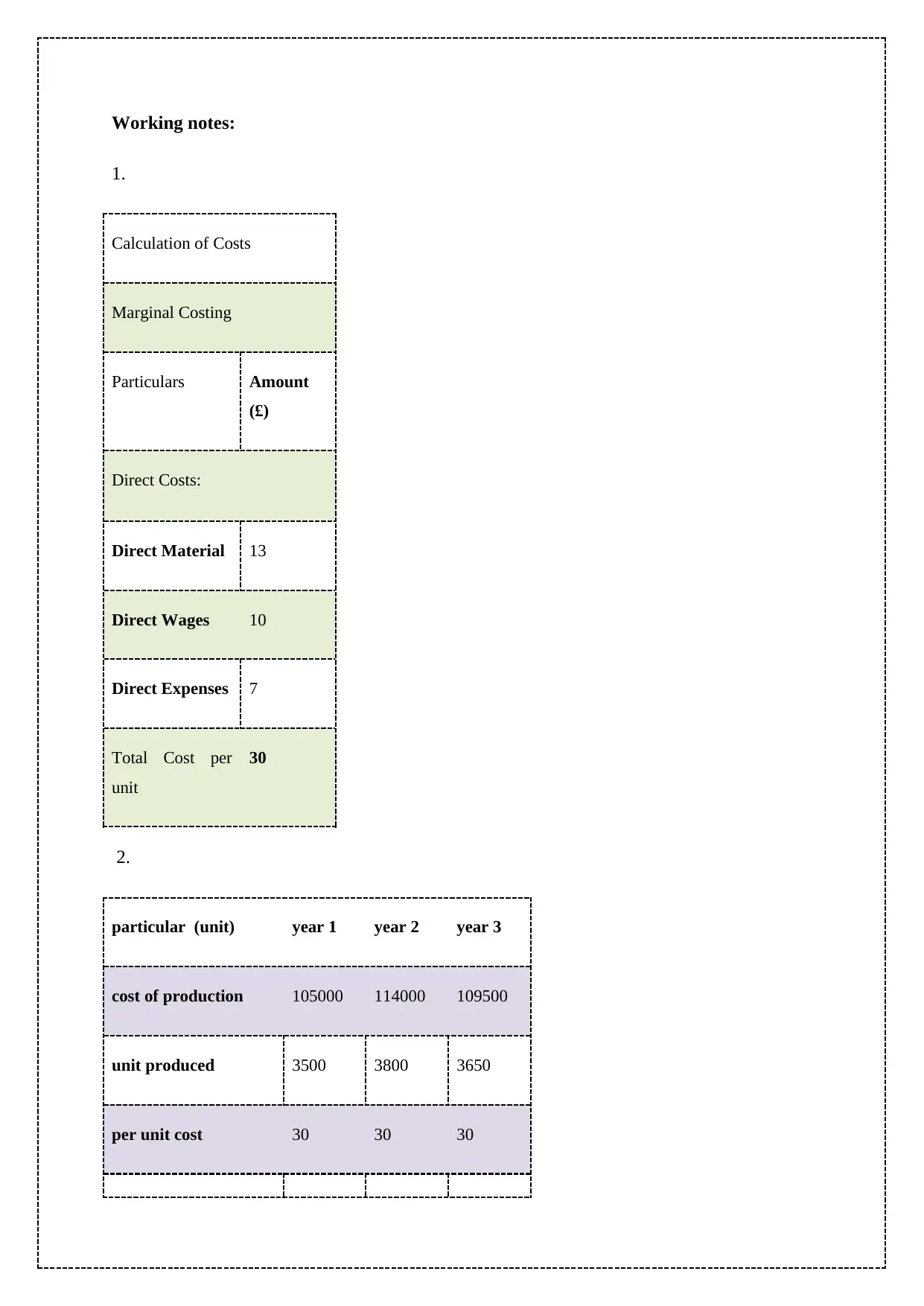

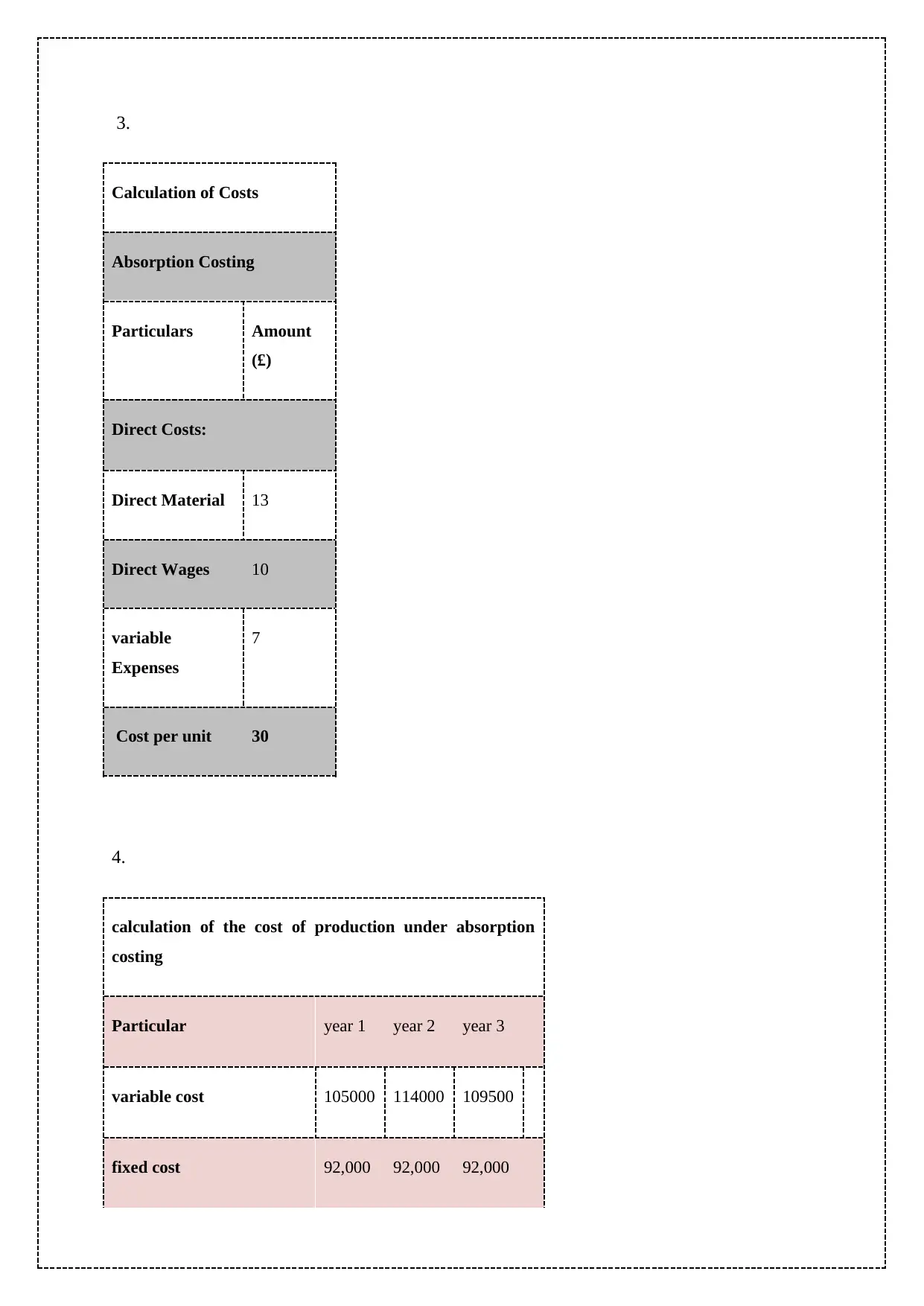

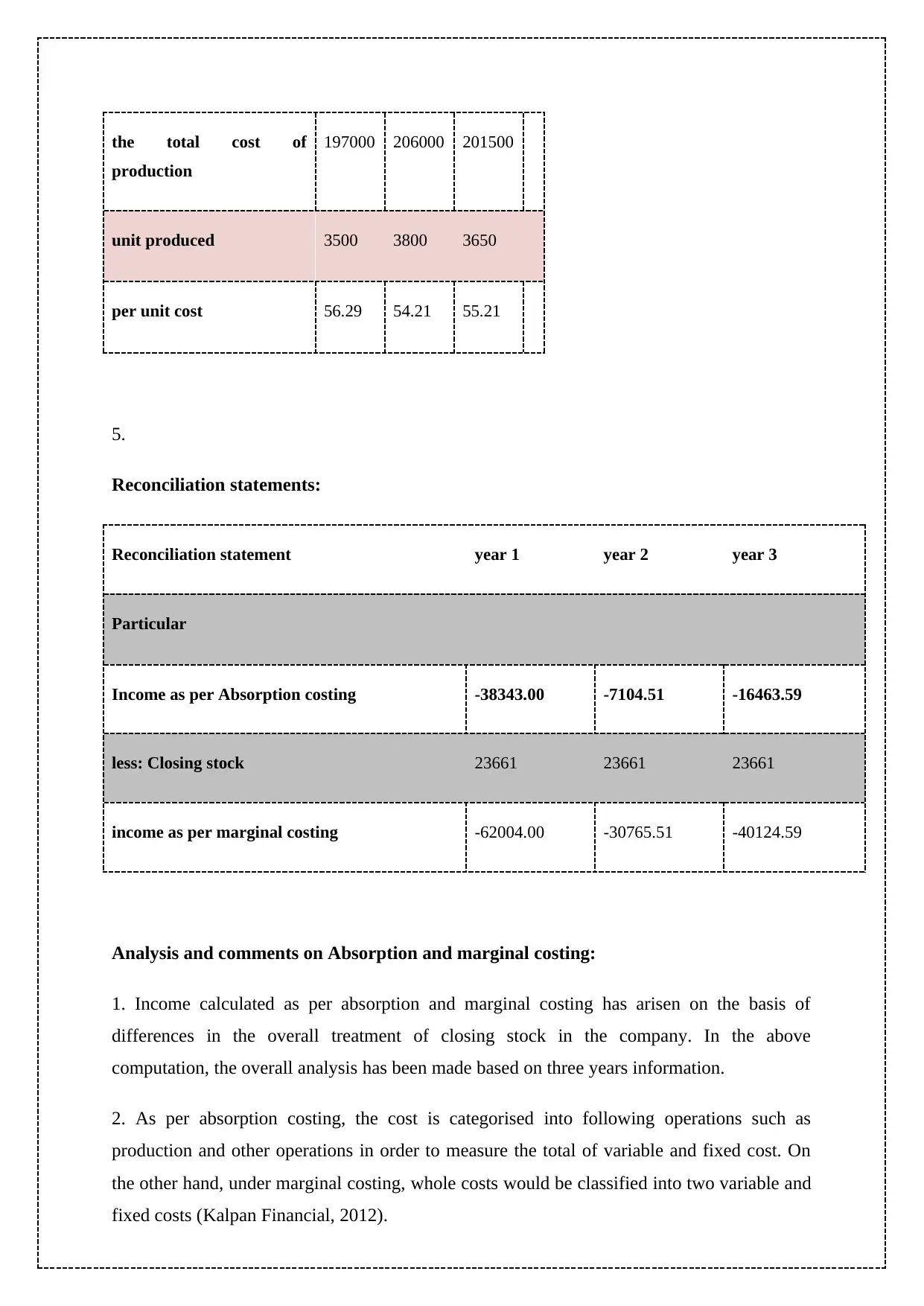

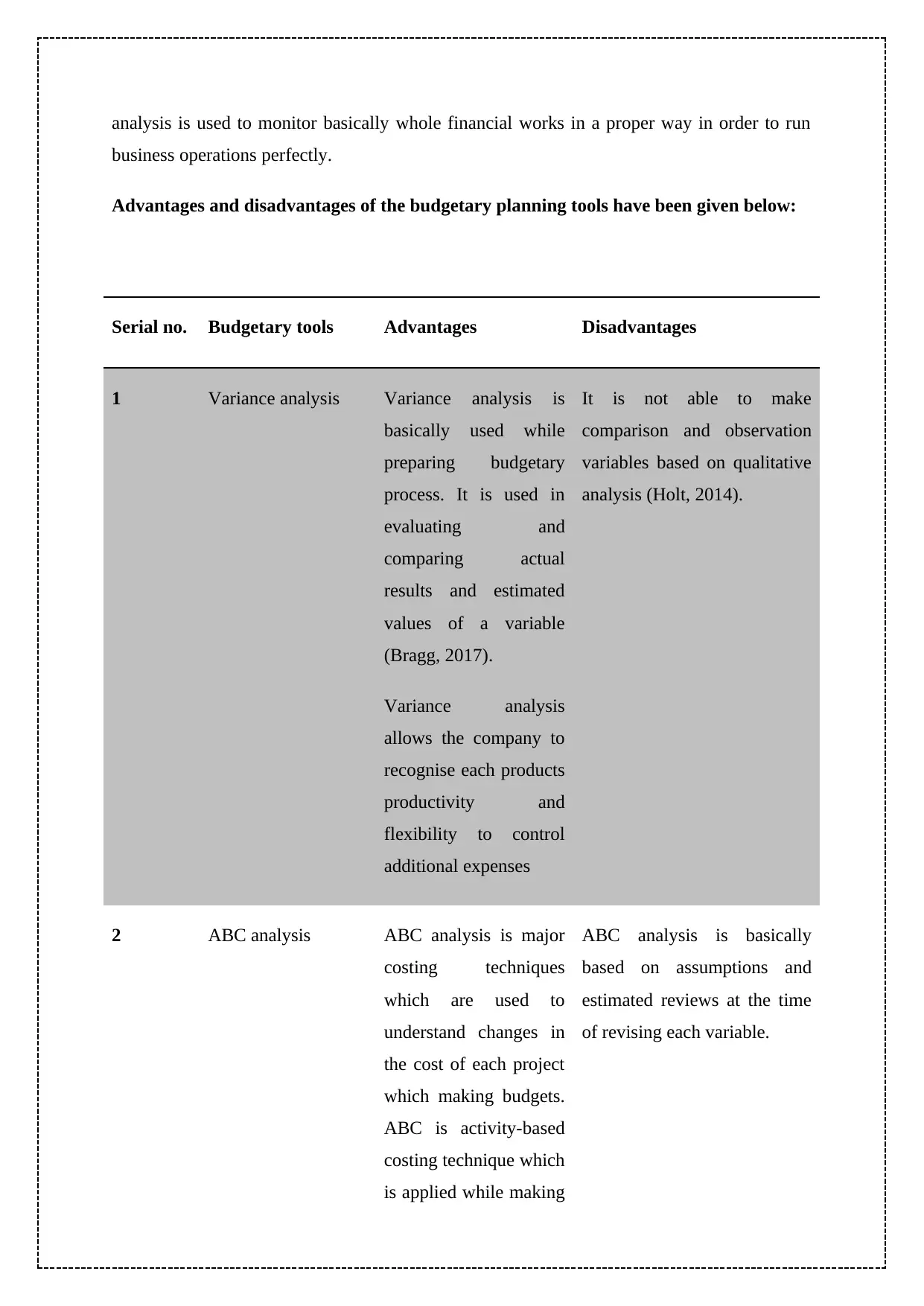

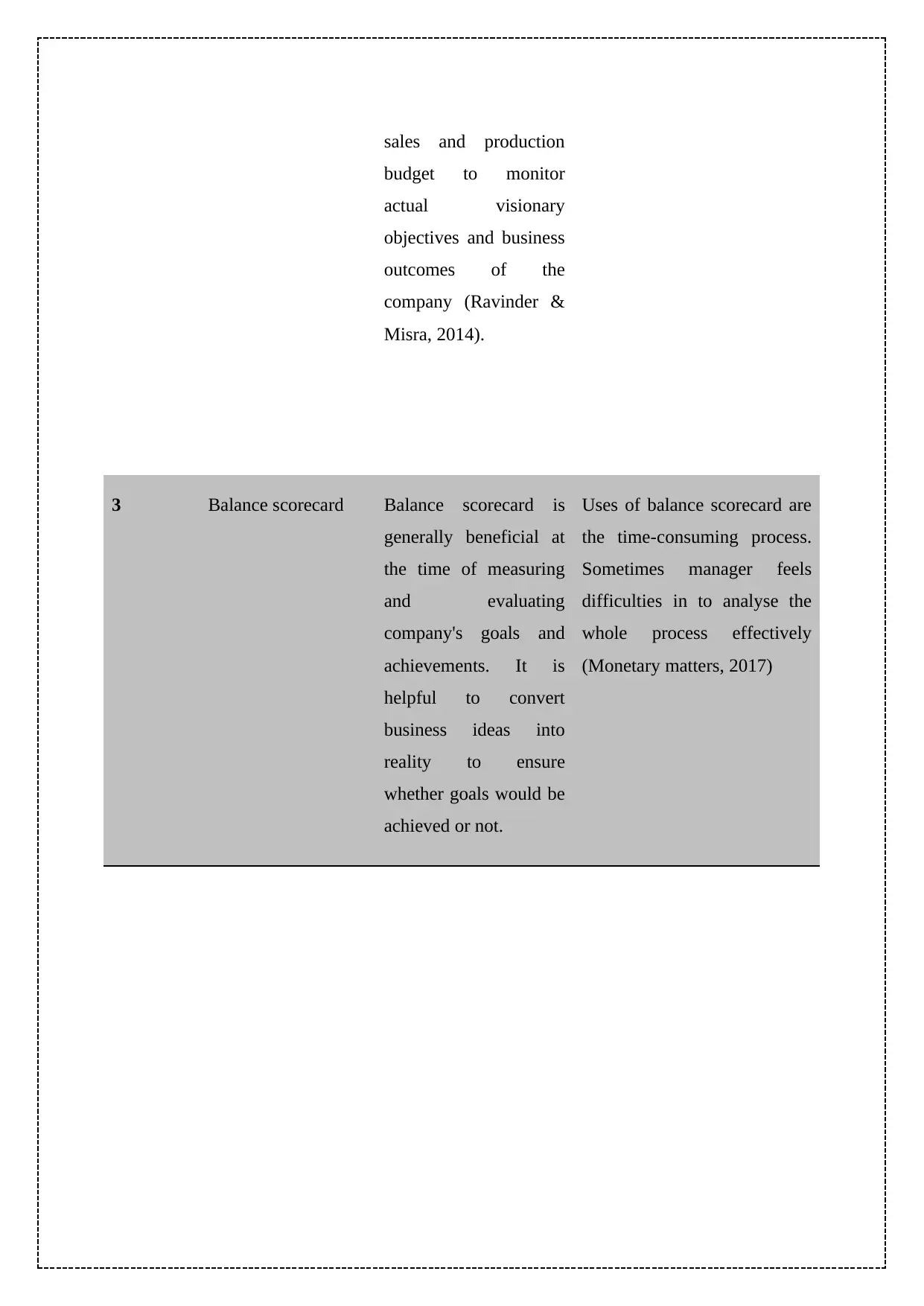

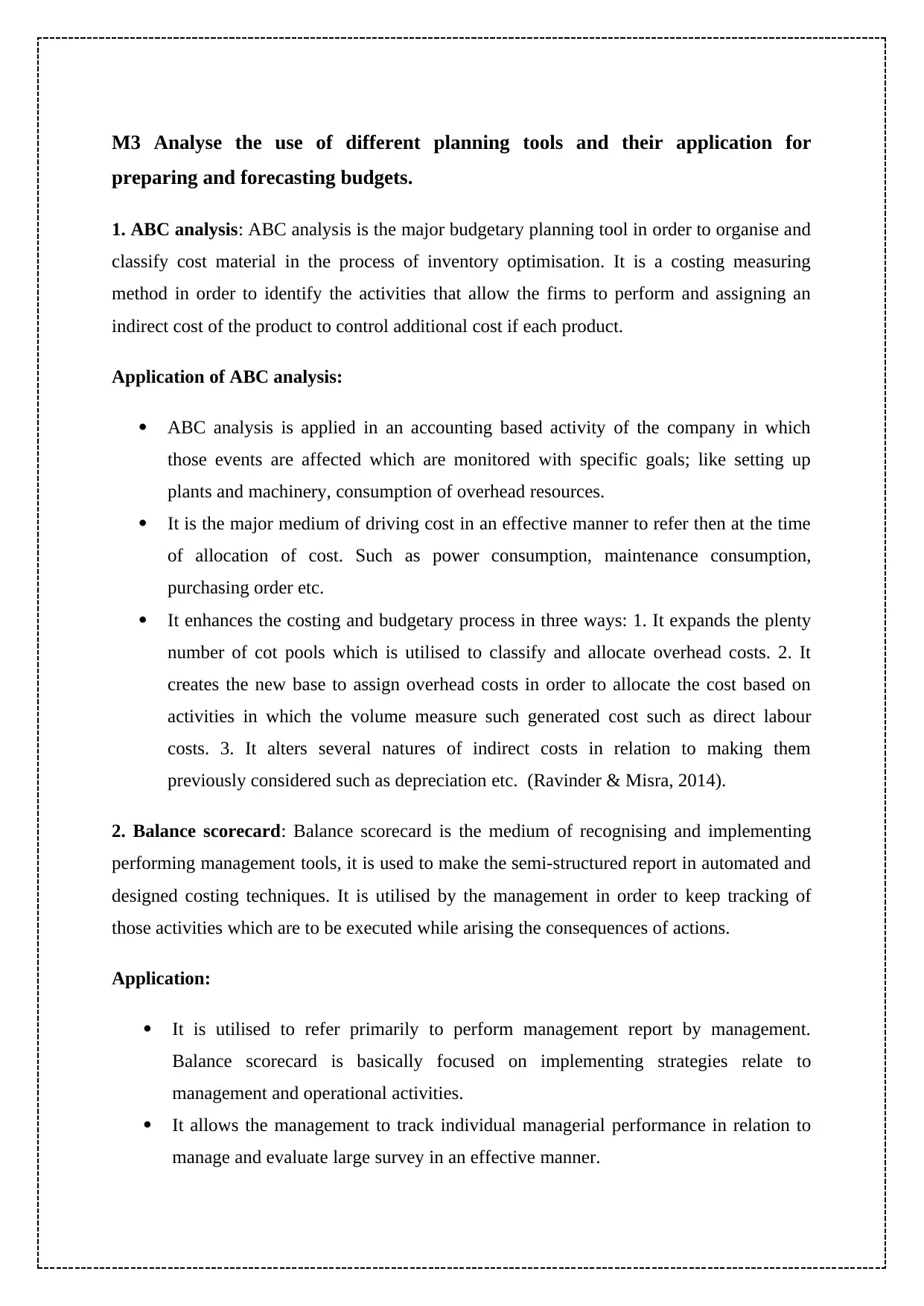

This management accounting report provides a detailed analysis of financial planning and budgetary control, utilizing both marginal and absorption costing methods to assess a company's financial performance over three years. It includes income statements, cost calculations, and reconciliation statements to highlight the differences between costing methodologies. The report further explains the advantages and disadvantages of various planning tools such as variance analysis, balance scorecards, and ABC costing, emphasizing their application in preparing and forecasting budgets. It evaluates how organizations adapt their management accounting systems to address financial challenges, focusing on financial planning, cost measurement, decision-making processes, and budgetary control. The analysis demonstrates how effective management accounting can lead organizations to sustainable success by improving financial stability and strategic decision-making. Desklib offers a range of similar solved assignments and study resources for students.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.