Budgeting in Management Accounting: Executive Summary and Analysis

VerifiedAdded on 2020/10/22

|15

|3717

|483

Report

AI Summary

This report provides an executive summary of budgeting within the context of management accounting. It explores the significance of budgeting in maintaining financial balance and efficiency, detailing various approaches like top-down and bottom-up methods, along with their respective advantages and disadvantages. The study further analyzes two scholarly articles focusing on budgeting's role in sponsorship decision-making processes. The first study highlights the crucial role of budgeting in performance evaluation, while the second emphasizes its function as an authorization tool. The report concludes that effective budgeting is essential for achieving success and efficiency in management accounting, offering valuable insights for management accountants. The report also touches upon the role of accounting personnel involvement in the sponsorship management.

MANAGERIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Budgeting is termed as very important concept in management accounting. It helps to

keep appropriate balance in its income and expenses in efficient aspect. The present study is

discussing about budgeting with context of management accounting. It will provide detailed

information associated to budgeting with its type of approaches. These approaches are

described with its merits and demerits in management accounting. Further, there is selection of

two scholarly articles which are based on budgeting with management accounting in

sponsorship decision making process. From study 1, its major finding is of significant budgetary

role for evaluating performance and from study 2 it reflects active budgetary role as

authorisation. Further it could be summed up by stating that budgeting helps in attaining

success in efficient aspect.

Budgeting is termed as very important concept in management accounting. It helps to

keep appropriate balance in its income and expenses in efficient aspect. The present study is

discussing about budgeting with context of management accounting. It will provide detailed

information associated to budgeting with its type of approaches. These approaches are

described with its merits and demerits in management accounting. Further, there is selection of

two scholarly articles which are based on budgeting with management accounting in

sponsorship decision making process. From study 1, its major finding is of significant budgetary

role for evaluating performance and from study 2 it reflects active budgetary role as

authorisation. Further it could be summed up by stating that budgeting helps in attaining

success in efficient aspect.

TABLE OF CONTENTS

INTRODUCTION..............................................................................................................................1

MAIN BODY ................................................................................................................................... 1

Explanation of Budgeting.......................................................................................................... 1

Explanation about question and purpose of study ...................................................................4

Discussion about both study with its findings...........................................................................5

Specific lessons and outcome from two studies which are useful for management

accountants...............................................................................................................................8

CONCLUSION................................................................................................................................10

REFERENCES................................................................................................................................. 11

INTRODUCTION..............................................................................................................................1

MAIN BODY ................................................................................................................................... 1

Explanation of Budgeting.......................................................................................................... 1

Explanation about question and purpose of study ...................................................................4

Discussion about both study with its findings...........................................................................5

Specific lessons and outcome from two studies which are useful for management

accountants...............................................................................................................................8

CONCLUSION................................................................................................................................10

REFERENCES................................................................................................................................. 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Managerial accounting is also referred as cost accounting with process of interpreting,

analysing, communicating, identifying and measuring information to managers with context of

objectives of business entity. Budgeting refers to process of framing plan for spending money as

this expenditure plan is known as budget. It helps to keep appropriate balance in its income and

expenses in efficient aspect. The present study is discussing about budgeting with context of

management accounting. It will provide detailed information associated to budgeting with its

type of approaches. These approaches are described with its merits and demerits in

management accounting. Further, there is selection of two scholarly articles which are based on

budgeting with management accounting in sponsorship decision making process. The other

scholarly article which will be chosen will show budgetary role with context of sponsorship

management as contingency perspective. It had provided explanation of purpose of both study

with its method which is used for exploring topic. In the same series, it had been discussed

contrasting aspect of both study with its outcome which are important for management

accountants.

MAIN BODY

Explanation of Budgeting

Budgeting refers to process for creating plan for spending money. The plan of spending

is known as budget. In simple words, the creation of this spending plan helps for allowing for

identify in advance about presence of sufficient money to perform activity according to need.

Generally, it balances expenses with its income. If there is high spending as compared to

income, then it creates problem. If spending or budget plan is followed in appropriate manner

then it will help for keeping free from debt (Cowton, 2018). The basic principles of budgeting

are:

Planning annual operations

Setting coordination in work of different parts of business

Communicating plans to managers

Motivating manager for attaining goals

1

Managerial accounting is also referred as cost accounting with process of interpreting,

analysing, communicating, identifying and measuring information to managers with context of

objectives of business entity. Budgeting refers to process of framing plan for spending money as

this expenditure plan is known as budget. It helps to keep appropriate balance in its income and

expenses in efficient aspect. The present study is discussing about budgeting with context of

management accounting. It will provide detailed information associated to budgeting with its

type of approaches. These approaches are described with its merits and demerits in

management accounting. Further, there is selection of two scholarly articles which are based on

budgeting with management accounting in sponsorship decision making process. The other

scholarly article which will be chosen will show budgetary role with context of sponsorship

management as contingency perspective. It had provided explanation of purpose of both study

with its method which is used for exploring topic. In the same series, it had been discussed

contrasting aspect of both study with its outcome which are important for management

accountants.

MAIN BODY

Explanation of Budgeting

Budgeting refers to process for creating plan for spending money. The plan of spending

is known as budget. In simple words, the creation of this spending plan helps for allowing for

identify in advance about presence of sufficient money to perform activity according to need.

Generally, it balances expenses with its income. If there is high spending as compared to

income, then it creates problem. If spending or budget plan is followed in appropriate manner

then it will help for keeping free from debt (Cowton, 2018). The basic principles of budgeting

are:

Planning annual operations

Setting coordination in work of different parts of business

Communicating plans to managers

Motivating manager for attaining goals

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Controlling activities

Evaluation of managers performance

Planning annual operation: Usually, business will frame plans for long term perspective.

Business could not be switched over night and it is difficult to account long term plan while

dealing with regular operations. The managers must be ensured through annual budget and

planning for future by manager as they transform long term plan to manageable steps.

Setting coordination in work of different parts of business: In business, there are

various departments so it is difficult to ensure about performing its operation in appropriate

aspect. Budget also helps in ensuring about work of each department which is directly directed

according to attaining about best feature for business.

Communicating plans to managers: Budget communicates operation of each

department for attaining objective of organization. In the same series, it reflects about activity

for performing and how it fit to other departments.

Motivating manager for attaining goals: Planned outcome had been provided through

budget. Generally, it depends on environment as it breaks its results for shorter duration.

Controlling activities: Various business operation as management by exception, as they

use reporting system which reflects about not attaining budgeted activity (Hiebl, 2018).

Evaluation of manager’s performance: The manager knows about what activity they

have to perform with its measure. They provide appropriate basis for identifying quality of

manager for performing their job.

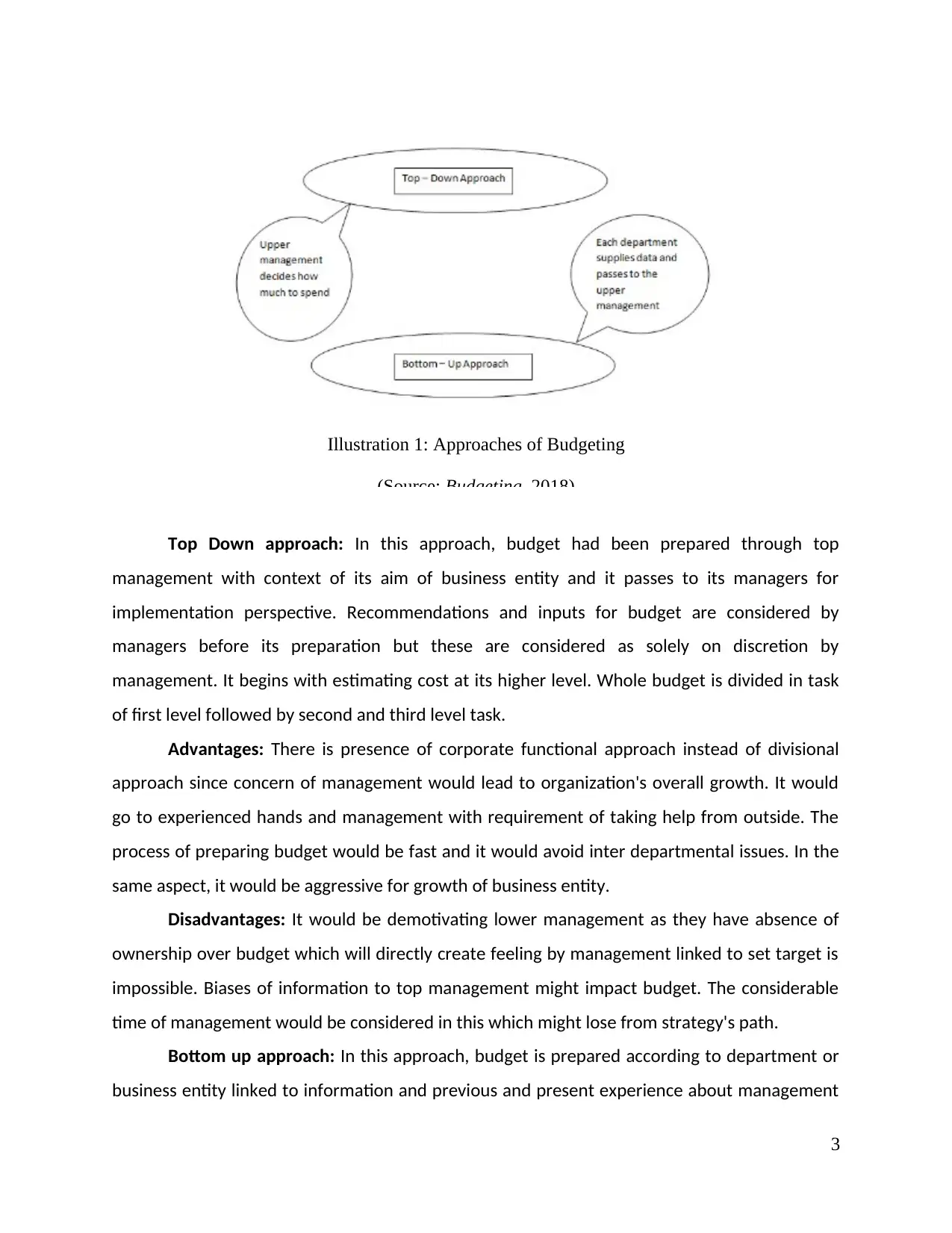

Approaches of Budgeting

There are two approaches of budgeting which are stated below:

Top Down approach

Bottom Up approach

2

Evaluation of managers performance

Planning annual operation: Usually, business will frame plans for long term perspective.

Business could not be switched over night and it is difficult to account long term plan while

dealing with regular operations. The managers must be ensured through annual budget and

planning for future by manager as they transform long term plan to manageable steps.

Setting coordination in work of different parts of business: In business, there are

various departments so it is difficult to ensure about performing its operation in appropriate

aspect. Budget also helps in ensuring about work of each department which is directly directed

according to attaining about best feature for business.

Communicating plans to managers: Budget communicates operation of each

department for attaining objective of organization. In the same series, it reflects about activity

for performing and how it fit to other departments.

Motivating manager for attaining goals: Planned outcome had been provided through

budget. Generally, it depends on environment as it breaks its results for shorter duration.

Controlling activities: Various business operation as management by exception, as they

use reporting system which reflects about not attaining budgeted activity (Hiebl, 2018).

Evaluation of manager’s performance: The manager knows about what activity they

have to perform with its measure. They provide appropriate basis for identifying quality of

manager for performing their job.

Approaches of Budgeting

There are two approaches of budgeting which are stated below:

Top Down approach

Bottom Up approach

2

Illustration 1: Approaches of Budgeting

(Source: Budgeting, 2018)

Top Down approach: In this approach, budget had been prepared through top

management with context of its aim of business entity and it passes to its managers for

implementation perspective. Recommendations and inputs for budget are considered by

managers before its preparation but these are considered as solely on discretion by

management. It begins with estimating cost at its higher level. Whole budget is divided in task

of first level followed by second and third level task.

Advantages: There is presence of corporate functional approach instead of divisional

approach since concern of management would lead to organization's overall growth. It would

go to experienced hands and management with requirement of taking help from outside. The

process of preparing budget would be fast and it would avoid inter departmental issues. In the

same aspect, it would be aggressive for growth of business entity.

Disadvantages: It would be demotivating lower management as they have absence of

ownership over budget which will directly create feeling by management linked to set target is

impossible. Biases of information to top management might impact budget. The considerable

time of management would be considered in this which might lose from strategy's path.

Bottom up approach: In this approach, budget is prepared according to department or

business entity linked to information and previous and present experience about management

3

(Source: Budgeting, 2018)

Top Down approach: In this approach, budget had been prepared through top

management with context of its aim of business entity and it passes to its managers for

implementation perspective. Recommendations and inputs for budget are considered by

managers before its preparation but these are considered as solely on discretion by

management. It begins with estimating cost at its higher level. Whole budget is divided in task

of first level followed by second and third level task.

Advantages: There is presence of corporate functional approach instead of divisional

approach since concern of management would lead to organization's overall growth. It would

go to experienced hands and management with requirement of taking help from outside. The

process of preparing budget would be fast and it would avoid inter departmental issues. In the

same aspect, it would be aggressive for growth of business entity.

Disadvantages: It would be demotivating lower management as they have absence of

ownership over budget which will directly create feeling by management linked to set target is

impossible. Biases of information to top management might impact budget. The considerable

time of management would be considered in this which might lose from strategy's path.

Bottom up approach: In this approach, budget is prepared according to department or

business entity linked to information and previous and present experience about management

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

for approval and input. It directly begins by determining various task and operation performed

through firm. Every unit has to disclose about its required funds and resources in its individual

budget.

Advantages: Managers are motivated and committed to organization because of

budget's ownership with them. The presence of better knowledge related to organization's

operation. Overall business strategy would be concentrated by senior management instead of

unit wise business. It could be quite more accurate for individual task as it provides overall

accuracy to its whole budget.

Disadvantages: It might not be par with its full objective of organization as it is prepared

through managers at business unit level. The process of preparing budget would be slow and

create dispute among inter department. Control can be lost by management for forecasting of

organization. Target could be set through managers which are easy to attain for decreasing

pressure (Su, 2018).

Explanation about question and purpose of study

Study 1: [In search of management accounting in sponsorship decision making

process]

In this study, it is about role and functions of budgeting and accounting in sponsorship

management. The potential associated to accounting procedure has to be directly invoked in

management and there is considerable control on sponsorship. It had reflected this study with

context of budgetary processes via senior management. In simple words, it had shown role of

budget in sponsorship decision making process (Delaney and Guilding, 2010).

Study 2: [An examination of budgetary roles in context of sponsorship management: A

contingency perspective]

In this study, budgetary roles are examined with reference to sponsorship management

and factors had been identified with its significance. In simple words, they had extracted

importance of budgeting with decision making process in sponsorship management Delaney,

(Delaney and Guilding, 2011).

Questions set out for exploring topic

Study 1

4

through firm. Every unit has to disclose about its required funds and resources in its individual

budget.

Advantages: Managers are motivated and committed to organization because of

budget's ownership with them. The presence of better knowledge related to organization's

operation. Overall business strategy would be concentrated by senior management instead of

unit wise business. It could be quite more accurate for individual task as it provides overall

accuracy to its whole budget.

Disadvantages: It might not be par with its full objective of organization as it is prepared

through managers at business unit level. The process of preparing budget would be slow and

create dispute among inter department. Control can be lost by management for forecasting of

organization. Target could be set through managers which are easy to attain for decreasing

pressure (Su, 2018).

Explanation about question and purpose of study

Study 1: [In search of management accounting in sponsorship decision making

process]

In this study, it is about role and functions of budgeting and accounting in sponsorship

management. The potential associated to accounting procedure has to be directly invoked in

management and there is considerable control on sponsorship. It had reflected this study with

context of budgetary processes via senior management. In simple words, it had shown role of

budget in sponsorship decision making process (Delaney and Guilding, 2010).

Study 2: [An examination of budgetary roles in context of sponsorship management: A

contingency perspective]

In this study, budgetary roles are examined with reference to sponsorship management

and factors had been identified with its significance. In simple words, they had extracted

importance of budgeting with decision making process in sponsorship management Delaney,

(Delaney and Guilding, 2011).

Questions set out for exploring topic

Study 1

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

What are the main roles of budget in context of sponsorship decision making?

What is importance of following budgetary role?

Is a formal budgeting and analysis of project had undertaken? Is so, by whom and how it

is extensive?

Study 2

Examine importance and nature of role of budget associated to sponsorship investment

decision making?

Identify the factors which affects importance of budgetary role in sponsorship context?

Discussion about both study with its findings

Findings of study 1

Its findings are classified in three categories related to:

Sponsorship Decision making procedure

Role of budget in sponsorship management

Degree of accounting personnel involvement related to sponsorship management

Sponsorship Decision making procedure: It is very important for considering

institution's sponsorship allocation of budgetary process, which could be comprised in three

different phases. The first phase directly deals with decision on university-wide with proportion

of total university investment has to be allocated to activities of sponsorship. The followed

phase is directly related to method of investing on campus based in its Australian university.

Both the decision making phases could be observed as located with level of chief executive

officer in hierarchy linked to university. So, third phase for decision making incur at campus

level.

Role of budget in sponsorship management: It had provided awareness among

requirement of budgeting linked to sponsorship management which was apparent with

manager's discussion. The importance placed with application of budget associated to

sponsorship management was directly viewed with connection to campus's manager oversight

of expenditure of sponsorship. It does not signify active budgetary role played thorough any

5

What is importance of following budgetary role?

Is a formal budgeting and analysis of project had undertaken? Is so, by whom and how it

is extensive?

Study 2

Examine importance and nature of role of budget associated to sponsorship investment

decision making?

Identify the factors which affects importance of budgetary role in sponsorship context?

Discussion about both study with its findings

Findings of study 1

Its findings are classified in three categories related to:

Sponsorship Decision making procedure

Role of budget in sponsorship management

Degree of accounting personnel involvement related to sponsorship management

Sponsorship Decision making procedure: It is very important for considering

institution's sponsorship allocation of budgetary process, which could be comprised in three

different phases. The first phase directly deals with decision on university-wide with proportion

of total university investment has to be allocated to activities of sponsorship. The followed

phase is directly related to method of investing on campus based in its Australian university.

Both the decision making phases could be observed as located with level of chief executive

officer in hierarchy linked to university. So, third phase for decision making incur at campus

level.

Role of budget in sponsorship management: It had provided awareness among

requirement of budgeting linked to sponsorship management which was apparent with

manager's discussion. The importance placed with application of budget associated to

sponsorship management was directly viewed with connection to campus's manager oversight

of expenditure of sponsorship. It does not signify active budgetary role played thorough any

5

particular accounting personnel. Initially, it was anticipated before this study that appearance

of predominant function of budget in concern of sponsorship management with identification

of amount could be expended. It is referred as authorisation role.

The literature of this study had conceived budgetary monetary function as outcome for

identification of maximising sales or for striving cost minimisation target. It is ensuring about

way of spending with underscore the method as sponsorship budget does not represent any

specific target to strive. For this concern, motivation was referred through one manager with

connection to budget of sponsorship, as it appears better for interpreting comment of manager

which signify same.

In the similar aspect, budgetary role as promoting cross organizational coordination and

communication had been referred. It had been directly appeared about level of sponsorship

budget and carried implication for extent. It had formed communication among campus

managers which had raised sponsorship budgets and provided increment in cross campus

discussion on proper method to expend budget. The managers did not observe increment of

cross organizational coordination and particular form through process of sponsorship budgetary

process.

Further, it had extracted other significant budgetary role which is directly concerned for

performance evaluation. It is accepted on wide aspect about potential of role would be muted

with context to discretionary expenditure where result of financial quantification of

expenditure is problematic. It had directly supported this aspect, but managers had

acknowledged performance evaluation as huge importance.

Degree of accounting personnel involvement in sponsorship management: The

accounting personnel of Australian university were not performing with appropriate active roles

with association of sponsorship management. It had observed procedure of formal budgeting

and conducted appropriate analysis. Generally, it is stated that no senior manager is

responsible for budget of sponsorship with qualifications of formal accounting.

Findings of study 2

It had been extracted that motivation is considered as second highest role of scoring

budget. It had provided insight about significance of budgetary role associated with

6

of predominant function of budget in concern of sponsorship management with identification

of amount could be expended. It is referred as authorisation role.

The literature of this study had conceived budgetary monetary function as outcome for

identification of maximising sales or for striving cost minimisation target. It is ensuring about

way of spending with underscore the method as sponsorship budget does not represent any

specific target to strive. For this concern, motivation was referred through one manager with

connection to budget of sponsorship, as it appears better for interpreting comment of manager

which signify same.

In the similar aspect, budgetary role as promoting cross organizational coordination and

communication had been referred. It had been directly appeared about level of sponsorship

budget and carried implication for extent. It had formed communication among campus

managers which had raised sponsorship budgets and provided increment in cross campus

discussion on proper method to expend budget. The managers did not observe increment of

cross organizational coordination and particular form through process of sponsorship budgetary

process.

Further, it had extracted other significant budgetary role which is directly concerned for

performance evaluation. It is accepted on wide aspect about potential of role would be muted

with context to discretionary expenditure where result of financial quantification of

expenditure is problematic. It had directly supported this aspect, but managers had

acknowledged performance evaluation as huge importance.

Degree of accounting personnel involvement in sponsorship management: The

accounting personnel of Australian university were not performing with appropriate active roles

with association of sponsorship management. It had observed procedure of formal budgeting

and conducted appropriate analysis. Generally, it is stated that no senior manager is

responsible for budget of sponsorship with qualifications of formal accounting.

Findings of study 2

It had been extracted that motivation is considered as second highest role of scoring

budget. It had provided insight about significance of budgetary role associated with

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

sponsorship management. With reference to its findings, it had given strong recommendation

about expenditure authorisation which is significant function in sponsorship management. It is

suggested that other role of budget had exhibited degree of importance associated to various

budgetary roles as it had original set of measure which could be applicable or adapted in future

work by laying special emphasis on appraising these budgetary roles on generic or specific

context. The role of performance evaluation was stated as very less important as it provides

support for widely held budget which in not used for measuring performance of discretionary

expenditure.

Insights for industry practice had been provided in its findings which appears on

inconsistent aspect with its academic literature which supports for marketing. The financial

terms are used by sponsorship managers for optimising instruments through budget for

control, planning and performance evaluation. Limited importance had been extracted for

authorisation budgetary role in this conducted study. Its observation is in-congruent with this

study.

In its finding sponsorship is directly regarded with archetypal form related to

discretionary expenditure as budgets are used predominantly with authorisation of sponsorship

expenditure. It directly carries intuitive merit on considerable aspect. The assertions are not

qualified with context of function of budgetary in such manner which considers relative

importance on direct base with enquiry on contingency model. It has recognition of various

budgetary usage among different industries, functional and organizational setting in its

organizations. In the same series, it had directed specifically for tracing formulation of

sponsorship budget.

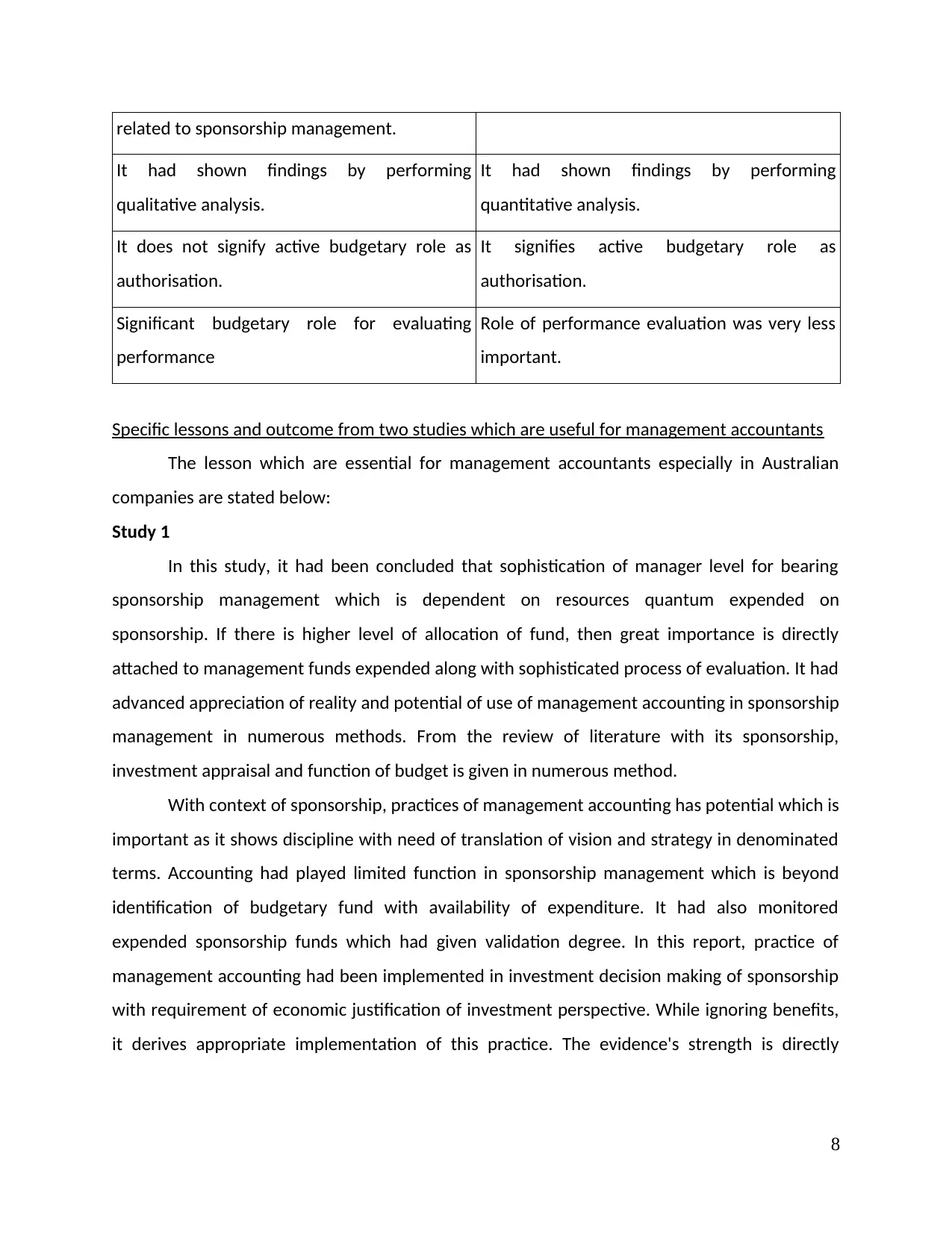

Study 1 Study 2

It is based on management accounting in

sponsorship decision making process.

It is based on Budgetary roles in context of

sponsorship management.

Its findings are classified in three categories as

Sponsorship Decision making procedure, role

of budget in sponsorship management and

Degree of accounting personnel involvement

It has provided finding on basis of importance

of budgetary role in sponsorship management.

7

about expenditure authorisation which is significant function in sponsorship management. It is

suggested that other role of budget had exhibited degree of importance associated to various

budgetary roles as it had original set of measure which could be applicable or adapted in future

work by laying special emphasis on appraising these budgetary roles on generic or specific

context. The role of performance evaluation was stated as very less important as it provides

support for widely held budget which in not used for measuring performance of discretionary

expenditure.

Insights for industry practice had been provided in its findings which appears on

inconsistent aspect with its academic literature which supports for marketing. The financial

terms are used by sponsorship managers for optimising instruments through budget for

control, planning and performance evaluation. Limited importance had been extracted for

authorisation budgetary role in this conducted study. Its observation is in-congruent with this

study.

In its finding sponsorship is directly regarded with archetypal form related to

discretionary expenditure as budgets are used predominantly with authorisation of sponsorship

expenditure. It directly carries intuitive merit on considerable aspect. The assertions are not

qualified with context of function of budgetary in such manner which considers relative

importance on direct base with enquiry on contingency model. It has recognition of various

budgetary usage among different industries, functional and organizational setting in its

organizations. In the same series, it had directed specifically for tracing formulation of

sponsorship budget.

Study 1 Study 2

It is based on management accounting in

sponsorship decision making process.

It is based on Budgetary roles in context of

sponsorship management.

Its findings are classified in three categories as

Sponsorship Decision making procedure, role

of budget in sponsorship management and

Degree of accounting personnel involvement

It has provided finding on basis of importance

of budgetary role in sponsorship management.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

related to sponsorship management.

It had shown findings by performing

qualitative analysis.

It had shown findings by performing

quantitative analysis.

It does not signify active budgetary role as

authorisation.

It signifies active budgetary role as

authorisation.

Significant budgetary role for evaluating

performance

Role of performance evaluation was very less

important.

Specific lessons and outcome from two studies which are useful for management accountants

The lesson which are essential for management accountants especially in Australian

companies are stated below:

Study 1

In this study, it had been concluded that sophistication of manager level for bearing

sponsorship management which is dependent on resources quantum expended on

sponsorship. If there is higher level of allocation of fund, then great importance is directly

attached to management funds expended along with sophisticated process of evaluation. It had

advanced appreciation of reality and potential of use of management accounting in sponsorship

management in numerous methods. From the review of literature with its sponsorship,

investment appraisal and function of budget is given in numerous method.

With context of sponsorship, practices of management accounting has potential which is

important as it shows discipline with need of translation of vision and strategy in denominated

terms. Accounting had played limited function in sponsorship management which is beyond

identification of budgetary fund with availability of expenditure. It had also monitored

expended sponsorship funds which had given validation degree. In this report, practice of

management accounting had been implemented in investment decision making of sponsorship

with requirement of economic justification of investment perspective. While ignoring benefits,

it derives appropriate implementation of this practice. The evidence's strength is directly

8

It had shown findings by performing

qualitative analysis.

It had shown findings by performing

quantitative analysis.

It does not signify active budgetary role as

authorisation.

It signifies active budgetary role as

authorisation.

Significant budgetary role for evaluating

performance

Role of performance evaluation was very less

important.

Specific lessons and outcome from two studies which are useful for management accountants

The lesson which are essential for management accountants especially in Australian

companies are stated below:

Study 1

In this study, it had been concluded that sophistication of manager level for bearing

sponsorship management which is dependent on resources quantum expended on

sponsorship. If there is higher level of allocation of fund, then great importance is directly

attached to management funds expended along with sophisticated process of evaluation. It had

advanced appreciation of reality and potential of use of management accounting in sponsorship

management in numerous methods. From the review of literature with its sponsorship,

investment appraisal and function of budget is given in numerous method.

With context of sponsorship, practices of management accounting has potential which is

important as it shows discipline with need of translation of vision and strategy in denominated

terms. Accounting had played limited function in sponsorship management which is beyond

identification of budgetary fund with availability of expenditure. It had also monitored

expended sponsorship funds which had given validation degree. In this report, practice of

management accounting had been implemented in investment decision making of sponsorship

with requirement of economic justification of investment perspective. While ignoring benefits,

it derives appropriate implementation of this practice. The evidence's strength is directly

8

concerned to authorisation function of budget as it beckons field work for exploring contextual

problems which directly impact manner of usage of budget.

The strong evidence had been given for involvement of limited accountant in process of

sponsorship management which would directly appear with scope of conduct. In the same

series, normative exploration of accounting techniques for drawing yield on great sophistication

in organization's range in sponsorship management. The sponsorship expenditure could be

observed for constituting particular discretionary expenditure form. It had also attempted for

building research initiative with alternative enquiry line for pursuing comparison of nature of

accounting control. It is applied to sponsorship management in such aspect accounting is

invoked in management with its kind of discretionary expenditure like training and advertising.

In its finding, it has been stated that degree of accounting linked to personnel

involvement in sponsorship management. Usually, managers infrequently draws expertise in

finance and marketing department to assess provision of project of value of money. It had given

appropriate exposure on accounting job with virtue of administrative nature of position in its

Australian university.

Study 2

According to this study, sponsors have huge demand of demonstrable return on

investment. If there is lack of financial discipline and credibility then it creates various issues.

The efficient manner where budget provides support to sponsorship management which could

be observes as particular interface of accounting facet. Budgets could be used for rational

model for measurement, identification, analysing and communicating information for

application of process of investment decision making. Sponsorship could be significant

expenditure for befitting over long term perspective as it could be constituted as investment

form. This development is posing various issues of accounting.

In the similar aspect, sponsorship could be directly viewed as investment as it might

anticipate deployment of accounting on basis of techniques of investment appraisal with

various other methodologies of management accounting with context of sponsorship process

of investment decision making. The findings had recommended various other role of budgetary

which had been given importance with reference to motivation, planning and forecasting.

9

problems which directly impact manner of usage of budget.

The strong evidence had been given for involvement of limited accountant in process of

sponsorship management which would directly appear with scope of conduct. In the same

series, normative exploration of accounting techniques for drawing yield on great sophistication

in organization's range in sponsorship management. The sponsorship expenditure could be

observed for constituting particular discretionary expenditure form. It had also attempted for

building research initiative with alternative enquiry line for pursuing comparison of nature of

accounting control. It is applied to sponsorship management in such aspect accounting is

invoked in management with its kind of discretionary expenditure like training and advertising.

In its finding, it has been stated that degree of accounting linked to personnel

involvement in sponsorship management. Usually, managers infrequently draws expertise in

finance and marketing department to assess provision of project of value of money. It had given

appropriate exposure on accounting job with virtue of administrative nature of position in its

Australian university.

Study 2

According to this study, sponsors have huge demand of demonstrable return on

investment. If there is lack of financial discipline and credibility then it creates various issues.

The efficient manner where budget provides support to sponsorship management which could

be observes as particular interface of accounting facet. Budgets could be used for rational

model for measurement, identification, analysing and communicating information for

application of process of investment decision making. Sponsorship could be significant

expenditure for befitting over long term perspective as it could be constituted as investment

form. This development is posing various issues of accounting.

In the similar aspect, sponsorship could be directly viewed as investment as it might

anticipate deployment of accounting on basis of techniques of investment appraisal with

various other methodologies of management accounting with context of sponsorship process

of investment decision making. The findings had recommended various other role of budgetary

which had been given importance with reference to motivation, planning and forecasting.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.