Exploring the Role of Management Accounting in Business Efficiency

VerifiedAdded on 2020/10/22

|14

|3891

|278

AI Summary

The report emphasizes the pivotal role of management accounting in business decision-making processes, focusing on expense monitoring using various budgeting techniques such as static and flexible budgets. Highlighted is how these practices not only boost efficiency but also foster stronger relationships between management and shareholders at Sollatek (UK). The analysis confirms that cost accounting and job costing systems are particularly effective within the manufacturing sector, enhancing productivity and operational efficacy. Moreover, managerial accounting reports serve as essential tools for planning, budgeting, and performance measurement. To tackle financial challenges, the report advocates employing zero-based budgeting, ratio, variance analysis, KPIs, and benchmarking as robust planning strategies.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

P1 Explaining management accounting and essential requirements of types of systems...........1

P2 Explaining methods and techniques for management accounting reporting.........................2

M1 Evaluating benefits of systems with organizational context................................................4

P4 Explaining advantages and disadvantages of types of planning tools on basis of budgetary

control.........................................................................................................................................5

M3 Analysing use of planning tools and application to forecast and prepare budgets...............7

P5 Evaluating how business are adapting accounting system for responding financial

problems......................................................................................................................................8

M4 Analysing that while responding financial problems, management accounting lead

business for sustainable success..................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

P1 Explaining management accounting and essential requirements of types of systems...........1

P2 Explaining methods and techniques for management accounting reporting.........................2

M1 Evaluating benefits of systems with organizational context................................................4

P4 Explaining advantages and disadvantages of types of planning tools on basis of budgetary

control.........................................................................................................................................5

M3 Analysing use of planning tools and application to forecast and prepare budgets...............7

P5 Evaluating how business are adapting accounting system for responding financial

problems......................................................................................................................................8

M4 Analysing that while responding financial problems, management accounting lead

business for sustainable success..................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Management accounting is known as process to determine, analyse, tracing and reflecting

financial information which could be used internally through manager for purpose of planning,

decision making, planning and operational control. The present report will demonstrate

understanding of management accounting with their essential requirements and types. Similarly,

this would explain different methods of managerial accounting reports along with advantages

and disadvantages of planning tools with context to budgetary control. In the same series, there

will be analysis of these planning tools with application to forecast and prepare budgets. This

report would compare ways where organization could imply management accounting for

responding the financial issues. On basis of this report, each aspect would be described by

considering Sollatek (UK) as its line of business includes manufacturing of miscellaneous

fabricated products as comprised in industrial sector of manufactured goods.

P1 Explaining management accounting and essential requirements of types of systems

As per CIMA, management accounting is known as process of measurement,

identification, analysis, accumulation, preparation, communication and interpretation of

information used through management for planning, controlling and evaluating within business

and assuring appropriate application of accountability with context to resources (Cooper,

Ezzamel and Qu, 2017). The functions of management accounting with context to Sollatek (UK)

is formulation of financial strategies with application of sales forecast, job costing techniques,

budgets within managerial accounting tools. This would lead to elaborate financial consequences

of decisions as if senior leaders adjust capital structure of company, then with this help

ramifications related to financing of debt or equity.

Simultaneously it helps in monitoring expenses as with formation of static, flexible or

rolling budget with various other types, helps leader and head of the department for monitoring

expenses. The major function is to maintain profitability as there is presence of various tools for

keeping business profitable along with performing break even analysis.

Financial accounting lays special emphasis to prepare information with context to

external parties like public regulators, stakeholders and lenders. However, Management

accounting considers financial information of company along with developing reports for

confidential and internal use through managers for decision making and determining methods to

run company in efficient aspect.

1

Management accounting is known as process to determine, analyse, tracing and reflecting

financial information which could be used internally through manager for purpose of planning,

decision making, planning and operational control. The present report will demonstrate

understanding of management accounting with their essential requirements and types. Similarly,

this would explain different methods of managerial accounting reports along with advantages

and disadvantages of planning tools with context to budgetary control. In the same series, there

will be analysis of these planning tools with application to forecast and prepare budgets. This

report would compare ways where organization could imply management accounting for

responding the financial issues. On basis of this report, each aspect would be described by

considering Sollatek (UK) as its line of business includes manufacturing of miscellaneous

fabricated products as comprised in industrial sector of manufactured goods.

P1 Explaining management accounting and essential requirements of types of systems

As per CIMA, management accounting is known as process of measurement,

identification, analysis, accumulation, preparation, communication and interpretation of

information used through management for planning, controlling and evaluating within business

and assuring appropriate application of accountability with context to resources (Cooper,

Ezzamel and Qu, 2017). The functions of management accounting with context to Sollatek (UK)

is formulation of financial strategies with application of sales forecast, job costing techniques,

budgets within managerial accounting tools. This would lead to elaborate financial consequences

of decisions as if senior leaders adjust capital structure of company, then with this help

ramifications related to financing of debt or equity.

Simultaneously it helps in monitoring expenses as with formation of static, flexible or

rolling budget with various other types, helps leader and head of the department for monitoring

expenses. The major function is to maintain profitability as there is presence of various tools for

keeping business profitable along with performing break even analysis.

Financial accounting lays special emphasis to prepare information with context to

external parties like public regulators, stakeholders and lenders. However, Management

accounting considers financial information of company along with developing reports for

confidential and internal use through managers for decision making and determining methods to

run company in efficient aspect.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Significance of management accounting to integrate with organizations such as Sollatek

(UK) is stated below:

This leads to measure actual performance comparatively with budgets.

The activities of business are better managed through application both planning and

budgeting.

This helps management in such aspect that latter could maximise rate of return on capital

employed.

The businesses efficiency is increased and improves relation among labour and

management as well.

The types of management accounting system are detailed below: Cost accounting system: It is replicated as type of accounting system which evaluated

that how organization is doing and offers help to managers make decision on basis of cost

to do business. This approach is applicable to each kind of business as it trading or

manufacture products or delivering services. In simple words, this system is used through

manufacturers for tracing activities of production with application of perpetual inventory

system (Nitzl, 2018). This accounting system is framed especially for manufacturers

which traces inventory flow on continual aspect via different production stages.

Job Costing system: This system is distinctive method costing as form of particular order

costing which is directly adopted for executing work strictly as per specification of

customer. The process of production is highly dependent on number of orders received

through customers as production is not intermittent and standardised in nature. In simple

words, it is process to assign cost which incur a particular job to individual of business

involved with. It is referred as cost allocation to company's construction projects as it is

broadly used in construction industry.

P2 Explaining methods and techniques for management accounting reporting

Managerial accounting implies accounts for planning and budgeting objective to measure

company's performance. In this aspect, it considers creation of capital budget which states

investments and expenses that might undertake in the future. Similarly, other concept is

projected decision making as managers uses managerial accounting reports like accounts

receivable ageing report for tracing benefits of underlying receivables with their time duration. It

helps for long term decision making for multiple companies. Moreover, performance

2

(UK) is stated below:

This leads to measure actual performance comparatively with budgets.

The activities of business are better managed through application both planning and

budgeting.

This helps management in such aspect that latter could maximise rate of return on capital

employed.

The businesses efficiency is increased and improves relation among labour and

management as well.

The types of management accounting system are detailed below: Cost accounting system: It is replicated as type of accounting system which evaluated

that how organization is doing and offers help to managers make decision on basis of cost

to do business. This approach is applicable to each kind of business as it trading or

manufacture products or delivering services. In simple words, this system is used through

manufacturers for tracing activities of production with application of perpetual inventory

system (Nitzl, 2018). This accounting system is framed especially for manufacturers

which traces inventory flow on continual aspect via different production stages.

Job Costing system: This system is distinctive method costing as form of particular order

costing which is directly adopted for executing work strictly as per specification of

customer. The process of production is highly dependent on number of orders received

through customers as production is not intermittent and standardised in nature. In simple

words, it is process to assign cost which incur a particular job to individual of business

involved with. It is referred as cost allocation to company's construction projects as it is

broadly used in construction industry.

P2 Explaining methods and techniques for management accounting reporting

Managerial accounting implies accounts for planning and budgeting objective to measure

company's performance. In this aspect, it considers creation of capital budget which states

investments and expenses that might undertake in the future. Similarly, other concept is

projected decision making as managers uses managerial accounting reports like accounts

receivable ageing report for tracing benefits of underlying receivables with their time duration. It

helps for long term decision making for multiple companies. Moreover, performance

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

measurement is used for purpose of comparing actual outcome of operations with forecast made

in phase of planning and budgeting. The types of managerial accounting reports are stated below:

Accounts Receivable Aging report: This is replicated as critical tool for managing

business. The most factoring organizations request for these reports as contribution of

application package because it shows the best idea of portfolio of receivables. This lists gathers

all unpaid customer invoices along with unused credit memos through data ranges. This report is

useful because it gives snapshot of outstanding money and due by customers as clear sign on

underlying issue. However, slow payments does not indicate financial issues, it shows possible

misunderstanding or dispute. It has been observed that various organizations uses this report

when planning of collections calls and trying to predict their cash flow.

The aging report is used as particular tool to estimate potential bad debts, is used for

revising allowance for doubtful accounts. The usual method for performing to derive historical

percentage in every range that become a bad debt with application of percentage to total of

columns in recent aging report (Azudin and Mansor, 2018). This types of report is crucial for

business that offers credit to its customers. It gives overview of balance of credit as per age,

which includes different categories for items which are 30, 60 and 90 days late. This could help

for adjusting credit policies for aligning with repayment capabilities of consumers.

Budget report: It is an internal report which is used through management for comparing

estimated projections of budget with actual performance number attained during a period. In

simple words, budget report is designed for comparing that how close budgeted performance was

with actual performance of accounting period. Moreover, budgets are on basis of financial

objective with estimate along with future projections, they are often inaccurate and could differ

on large basis through company's actual financial performance. In accounting period, managers

often compare budgeted numbers that were prepared at initial stage of period of incur of actual

number. It serves for two objective as could correct problems occurring business for inlining

performance with financial objectives in budget. Secondly for evaluating how accurate and

realistic were predictions.

Job cost reports: This report reflects expense for particular project as usually matched

with estimate of revenue so Sollatek (UK) could evaluate profitability of job. It helps for

determining areas of higher earning of businesses so company could lay efforts there rather than

wasting time and money on jobs with less profit margin. These reports are also used for purpose

3

in phase of planning and budgeting. The types of managerial accounting reports are stated below:

Accounts Receivable Aging report: This is replicated as critical tool for managing

business. The most factoring organizations request for these reports as contribution of

application package because it shows the best idea of portfolio of receivables. This lists gathers

all unpaid customer invoices along with unused credit memos through data ranges. This report is

useful because it gives snapshot of outstanding money and due by customers as clear sign on

underlying issue. However, slow payments does not indicate financial issues, it shows possible

misunderstanding or dispute. It has been observed that various organizations uses this report

when planning of collections calls and trying to predict their cash flow.

The aging report is used as particular tool to estimate potential bad debts, is used for

revising allowance for doubtful accounts. The usual method for performing to derive historical

percentage in every range that become a bad debt with application of percentage to total of

columns in recent aging report (Azudin and Mansor, 2018). This types of report is crucial for

business that offers credit to its customers. It gives overview of balance of credit as per age,

which includes different categories for items which are 30, 60 and 90 days late. This could help

for adjusting credit policies for aligning with repayment capabilities of consumers.

Budget report: It is an internal report which is used through management for comparing

estimated projections of budget with actual performance number attained during a period. In

simple words, budget report is designed for comparing that how close budgeted performance was

with actual performance of accounting period. Moreover, budgets are on basis of financial

objective with estimate along with future projections, they are often inaccurate and could differ

on large basis through company's actual financial performance. In accounting period, managers

often compare budgeted numbers that were prepared at initial stage of period of incur of actual

number. It serves for two objective as could correct problems occurring business for inlining

performance with financial objectives in budget. Secondly for evaluating how accurate and

realistic were predictions.

Job cost reports: This report reflects expense for particular project as usually matched

with estimate of revenue so Sollatek (UK) could evaluate profitability of job. It helps for

determining areas of higher earning of businesses so company could lay efforts there rather than

wasting time and money on jobs with less profit margin. These reports are also used for purpose

3

of analysing expenses as project is in progress so managers could correct answers of waste prior

to cost escalate (Accounting reports, 2017).

M1 Evaluating benefits of systems with organizational context

Cost accounting system

Advantages

The cost accounting system would provide benefit to Sollatek (UK) with its application is

stated below:

This would lead to substitute wastes, loss and inefficiencies through fixing standard for

every aspect.

The innovative and improved method of production are appropriately followed with

reference to cost accounting system and lead to reduction in cost. It extracts reasons for increment or decrement in profit margin, so management could

undertake remedial action for maintaining profitability of concern. There is absence of

possibility for shutting any process or product or department.

Disadvantages

In order to cost accounting, which has also presence of downside with context to Sollatek

(UK) are stated below:

The cost of past year is not similar in succeeding year whereas data related to cost is not

useful. With context to cost accounting, cost are absorbed pertaining to pre-determined rate

which leads to under and over absorption of overheads.

Job costing system

Advantages

The Sollatek (UK) would adapt this system which would provide benefit are stated

below:

The cost might be earned with every job is known as job costing.

Management could directly estimate cost of job with reference to previous records.

This is suitable for cost plus contracts and facilitates pricing of every job. There is absence of under or over recovery of overheads.

Disadvantages

4

to cost escalate (Accounting reports, 2017).

M1 Evaluating benefits of systems with organizational context

Cost accounting system

Advantages

The cost accounting system would provide benefit to Sollatek (UK) with its application is

stated below:

This would lead to substitute wastes, loss and inefficiencies through fixing standard for

every aspect.

The innovative and improved method of production are appropriately followed with

reference to cost accounting system and lead to reduction in cost. It extracts reasons for increment or decrement in profit margin, so management could

undertake remedial action for maintaining profitability of concern. There is absence of

possibility for shutting any process or product or department.

Disadvantages

In order to cost accounting, which has also presence of downside with context to Sollatek

(UK) are stated below:

The cost of past year is not similar in succeeding year whereas data related to cost is not

useful. With context to cost accounting, cost are absorbed pertaining to pre-determined rate

which leads to under and over absorption of overheads.

Job costing system

Advantages

The Sollatek (UK) would adapt this system which would provide benefit are stated

below:

The cost might be earned with every job is known as job costing.

Management could directly estimate cost of job with reference to previous records.

This is suitable for cost plus contracts and facilitates pricing of every job. There is absence of under or over recovery of overheads.

Disadvantages

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This system is very expensive as absence of standardization in job costing. Although,

there is requirement of close supervision.

During inflation, comparison of job cost is use less .

There is absence of possibilities of corrective action, in case actual margin is lower

comparatively estimated job costing (Nishimura, 2019).

The price of job is fixed with reference to market condition but not related to past

records.

P4 Explaining advantages and disadvantages of types of planning tools on basis of budgetary

control

Budget is known estimation of expenses and revenue over given future period of time as

this is re-evaluated and compiled on periodic aspect. Budgetary control is a system of

management control where spending and actual income are compared with planned income and

spending ,so it is monitored that plan is being followed and if with need to be altered in order to

make profit margin. The types of planning tools are stated below with their merits and demerits:

Ratio analysis: It is referred to analysis and interpretation of figures reflecting in

financial statements such as profit and loss and balance sheet etc.

Advantages

The trend related to cost, profits, sales or other facts could be known through calculating

ratios of accounting figures of last few years. It would be help of ratios which might b

important to plan or predict business activities of the future.

This would lead to indication of overall profitability as management is highly concerned

with this aspect along with capability to attain both long and short term obligations to its

creditors for ensuring reasonable return to its owners and securing optimum utilisation of

firm's assets. It acts as aid to decision making such as supply of goods on credit of business or bank

loans would be made available and many more financial decisions.

Disadvantages

This tool is associated with only quantitative analysis whereas qualitative factors are

avoided.

On basis of ideal ratios, no fixed standards could be laid down.

5

there is requirement of close supervision.

During inflation, comparison of job cost is use less .

There is absence of possibilities of corrective action, in case actual margin is lower

comparatively estimated job costing (Nishimura, 2019).

The price of job is fixed with reference to market condition but not related to past

records.

P4 Explaining advantages and disadvantages of types of planning tools on basis of budgetary

control

Budget is known estimation of expenses and revenue over given future period of time as

this is re-evaluated and compiled on periodic aspect. Budgetary control is a system of

management control where spending and actual income are compared with planned income and

spending ,so it is monitored that plan is being followed and if with need to be altered in order to

make profit margin. The types of planning tools are stated below with their merits and demerits:

Ratio analysis: It is referred to analysis and interpretation of figures reflecting in

financial statements such as profit and loss and balance sheet etc.

Advantages

The trend related to cost, profits, sales or other facts could be known through calculating

ratios of accounting figures of last few years. It would be help of ratios which might b

important to plan or predict business activities of the future.

This would lead to indication of overall profitability as management is highly concerned

with this aspect along with capability to attain both long and short term obligations to its

creditors for ensuring reasonable return to its owners and securing optimum utilisation of

firm's assets. It acts as aid to decision making such as supply of goods on credit of business or bank

loans would be made available and many more financial decisions.

Disadvantages

This tool is associated with only quantitative analysis whereas qualitative factors are

avoided.

On basis of ideal ratios, no fixed standards could be laid down.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The financial statements offers historical information as it does not show current

conditions so it does not make sense for forecasting future.

Variance analysis: This term is used to identify areas where usually cost overrun and

determines that standard cost is established is reasonable.

Advantages

It helps in controlling cost.

The variances could be categorised as controllable and uncontrollable variances so , in

this aspect, controllable variances are used for consideration of further action.

The sub-division of this analysis directly discloses the relationship among other variances

(Variance Analysis, 2016). This creates cost consciousness in minds of each employee of business entity.

Disadvantages

It is on basis of financial outcome whose release is on later perspective.

The exercise of budgeting might be performed loosely which is bound for deviating

through actual number.

Zero based budget: There is less possibility of error because it allows business to initiate

with zero for each item with consideration of proper factors.

Advantages

It leads to accuracy as against daily methods of budgeting involves to make arbitrary

changes to budget or past year.

It helps for efficient allocation of resources and does not observe historical numbers

instead of actual numbers. Improvise communication and coordination within department and motivates employee

through engaging hem in decision making.

Disadvantages

There is requirement of high manpower as many departments does not have adequate

time and human resource.

There is lack of expertise as this budgeting objective to show true expenses incurred

through state or department (Zero Based Budgeting, 2018).

6

conditions so it does not make sense for forecasting future.

Variance analysis: This term is used to identify areas where usually cost overrun and

determines that standard cost is established is reasonable.

Advantages

It helps in controlling cost.

The variances could be categorised as controllable and uncontrollable variances so , in

this aspect, controllable variances are used for consideration of further action.

The sub-division of this analysis directly discloses the relationship among other variances

(Variance Analysis, 2016). This creates cost consciousness in minds of each employee of business entity.

Disadvantages

It is on basis of financial outcome whose release is on later perspective.

The exercise of budgeting might be performed loosely which is bound for deviating

through actual number.

Zero based budget: There is less possibility of error because it allows business to initiate

with zero for each item with consideration of proper factors.

Advantages

It leads to accuracy as against daily methods of budgeting involves to make arbitrary

changes to budget or past year.

It helps for efficient allocation of resources and does not observe historical numbers

instead of actual numbers. Improvise communication and coordination within department and motivates employee

through engaging hem in decision making.

Disadvantages

There is requirement of high manpower as many departments does not have adequate

time and human resource.

There is lack of expertise as this budgeting objective to show true expenses incurred

through state or department (Zero Based Budgeting, 2018).

6

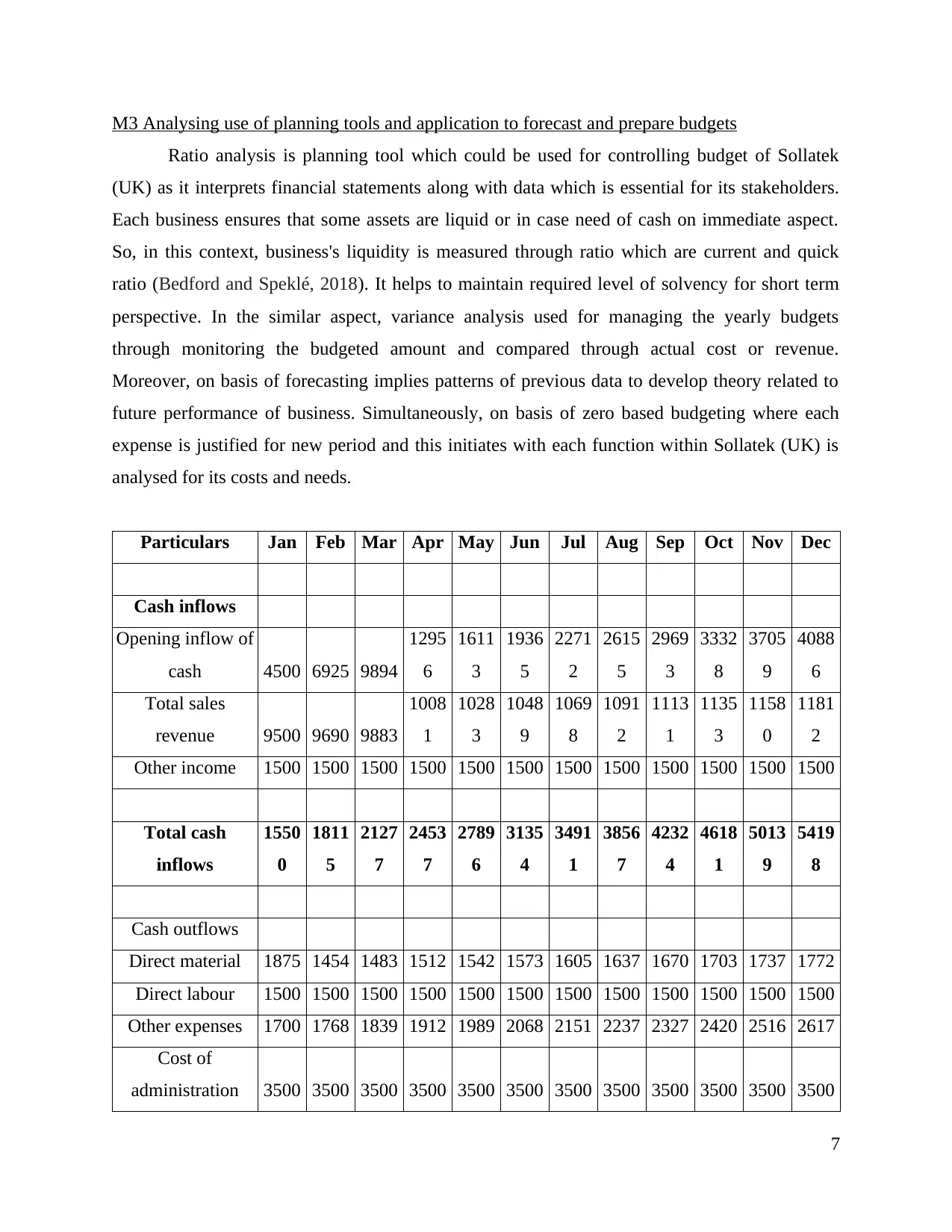

M3 Analysing use of planning tools and application to forecast and prepare budgets

Ratio analysis is planning tool which could be used for controlling budget of Sollatek

(UK) as it interprets financial statements along with data which is essential for its stakeholders.

Each business ensures that some assets are liquid or in case need of cash on immediate aspect.

So, in this context, business's liquidity is measured through ratio which are current and quick

ratio (Bedford and Speklé, 2018). It helps to maintain required level of solvency for short term

perspective. In the similar aspect, variance analysis used for managing the yearly budgets

through monitoring the budgeted amount and compared through actual cost or revenue.

Moreover, on basis of forecasting implies patterns of previous data to develop theory related to

future performance of business. Simultaneously, on basis of zero based budgeting where each

expense is justified for new period and this initiates with each function within Sollatek (UK) is

analysed for its costs and needs.

Particulars Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Cash inflows

Opening inflow of

cash 4500 6925 9894

1295

6

1611

3

1936

5

2271

2

2615

5

2969

3

3332

8

3705

9

4088

6

Total sales

revenue 9500 9690 9883

1008

1

1028

3

1048

9

1069

8

1091

2

1113

1

1135

3

1158

0

1181

2

Other income 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500

Total cash

inflows

1550

0

1811

5

2127

7

2453

7

2789

6

3135

4

3491

1

3856

7

4232

4

4618

1

5013

9

5419

8

Cash outflows

Direct material 1875 1454 1483 1512 1542 1573 1605 1637 1670 1703 1737 1772

Direct labour 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500

Other expenses 1700 1768 1839 1912 1989 2068 2151 2237 2327 2420 2516 2617

Cost of

administration 3500 3500 3500 3500 3500 3500 3500 3500 3500 3500 3500 3500

7

Ratio analysis is planning tool which could be used for controlling budget of Sollatek

(UK) as it interprets financial statements along with data which is essential for its stakeholders.

Each business ensures that some assets are liquid or in case need of cash on immediate aspect.

So, in this context, business's liquidity is measured through ratio which are current and quick

ratio (Bedford and Speklé, 2018). It helps to maintain required level of solvency for short term

perspective. In the similar aspect, variance analysis used for managing the yearly budgets

through monitoring the budgeted amount and compared through actual cost or revenue.

Moreover, on basis of forecasting implies patterns of previous data to develop theory related to

future performance of business. Simultaneously, on basis of zero based budgeting where each

expense is justified for new period and this initiates with each function within Sollatek (UK) is

analysed for its costs and needs.

Particulars Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Cash inflows

Opening inflow of

cash 4500 6925 9894

1295

6

1611

3

1936

5

2271

2

2615

5

2969

3

3332

8

3705

9

4088

6

Total sales

revenue 9500 9690 9883

1008

1

1028

3

1048

9

1069

8

1091

2

1113

1

1135

3

1158

0

1181

2

Other income 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500

Total cash

inflows

1550

0

1811

5

2127

7

2453

7

2789

6

3135

4

3491

1

3856

7

4232

4

4618

1

5013

9

5419

8

Cash outflows

Direct material 1875 1454 1483 1512 1542 1573 1605 1637 1670 1703 1737 1772

Direct labour 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500

Other expenses 1700 1768 1839 1912 1989 2068 2151 2237 2327 2420 2516 2617

Cost of

administration 3500 3500 3500 3500 3500 3500 3500 3500 3500 3500 3500 3500

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

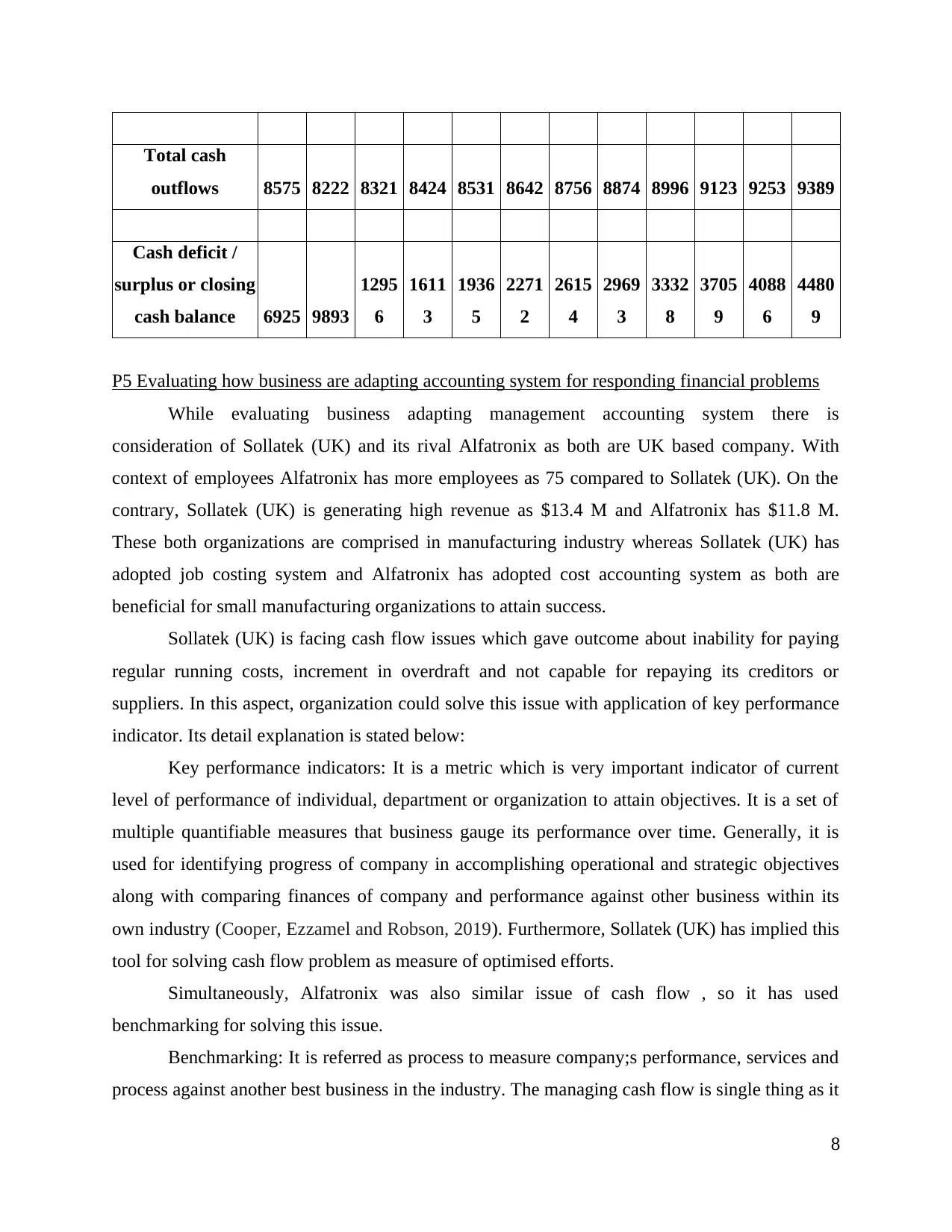

Total cash

outflows 8575 8222 8321 8424 8531 8642 8756 8874 8996 9123 9253 9389

Cash deficit /

surplus or closing

cash balance 6925 9893

1295

6

1611

3

1936

5

2271

2

2615

4

2969

3

3332

8

3705

9

4088

6

4480

9

P5 Evaluating how business are adapting accounting system for responding financial problems

While evaluating business adapting management accounting system there is

consideration of Sollatek (UK) and its rival Alfatronix as both are UK based company. With

context of employees Alfatronix has more employees as 75 compared to Sollatek (UK). On the

contrary, Sollatek (UK) is generating high revenue as $13.4 M and Alfatronix has $11.8 M.

These both organizations are comprised in manufacturing industry whereas Sollatek (UK) has

adopted job costing system and Alfatronix has adopted cost accounting system as both are

beneficial for small manufacturing organizations to attain success.

Sollatek (UK) is facing cash flow issues which gave outcome about inability for paying

regular running costs, increment in overdraft and not capable for repaying its creditors or

suppliers. In this aspect, organization could solve this issue with application of key performance

indicator. Its detail explanation is stated below:

Key performance indicators: It is a metric which is very important indicator of current

level of performance of individual, department or organization to attain objectives. It is a set of

multiple quantifiable measures that business gauge its performance over time. Generally, it is

used for identifying progress of company in accomplishing operational and strategic objectives

along with comparing finances of company and performance against other business within its

own industry (Cooper, Ezzamel and Robson, 2019). Furthermore, Sollatek (UK) has implied this

tool for solving cash flow problem as measure of optimised efforts.

Simultaneously, Alfatronix was also similar issue of cash flow , so it has used

benchmarking for solving this issue.

Benchmarking: It is referred as process to measure company;s performance, services and

process against another best business in the industry. The managing cash flow is single thing as it

8

outflows 8575 8222 8321 8424 8531 8642 8756 8874 8996 9123 9253 9389

Cash deficit /

surplus or closing

cash balance 6925 9893

1295

6

1611

3

1936

5

2271

2

2615

4

2969

3

3332

8

3705

9

4088

6

4480

9

P5 Evaluating how business are adapting accounting system for responding financial problems

While evaluating business adapting management accounting system there is

consideration of Sollatek (UK) and its rival Alfatronix as both are UK based company. With

context of employees Alfatronix has more employees as 75 compared to Sollatek (UK). On the

contrary, Sollatek (UK) is generating high revenue as $13.4 M and Alfatronix has $11.8 M.

These both organizations are comprised in manufacturing industry whereas Sollatek (UK) has

adopted job costing system and Alfatronix has adopted cost accounting system as both are

beneficial for small manufacturing organizations to attain success.

Sollatek (UK) is facing cash flow issues which gave outcome about inability for paying

regular running costs, increment in overdraft and not capable for repaying its creditors or

suppliers. In this aspect, organization could solve this issue with application of key performance

indicator. Its detail explanation is stated below:

Key performance indicators: It is a metric which is very important indicator of current

level of performance of individual, department or organization to attain objectives. It is a set of

multiple quantifiable measures that business gauge its performance over time. Generally, it is

used for identifying progress of company in accomplishing operational and strategic objectives

along with comparing finances of company and performance against other business within its

own industry (Cooper, Ezzamel and Robson, 2019). Furthermore, Sollatek (UK) has implied this

tool for solving cash flow problem as measure of optimised efforts.

Simultaneously, Alfatronix was also similar issue of cash flow , so it has used

benchmarking for solving this issue.

Benchmarking: It is referred as process to measure company;s performance, services and

process against another best business in the industry. The managing cash flow is single thing as it

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is significant, cash flow benchmarking is only attained via comparing own history but other

organization's attainments and history of failure for gaining insight and implementing innovative

plans. There must be implication of utilizing benchmarking cash flow for improving hoe to

manage cash and control, so try for connecting with competitors and utilise internet as tool of

research for reviewing websites. The cash flow management benchmarking could be directly

attained if situation is not ignored and implement ideas for making improvements.

M4 Analysing that while responding financial problems, management accounting lead business

for sustainable success

The basic objective of management accounting is to serve management for purpose of

decision making. On basis of financial issues, management is in requirement of information

relating to increment. Moreover, to establish strategies, practices and business models for

addressing social and environmental challenge for creating financial value and success for their

shareholders. In the present scenario, there are various organizations have presence of skills to

meet challenges and competing with sustainable economy as per Environmental management

and Assessment Institute (Horton and de Araujo Wanderley, 2018). On the contrary, there are

multiple indicators it initiates to alter and forecasts that 2-3rd of estimated forecasted growth over

coming 2 years for social and environmental data.

Simultaneously, cash flow forecast helps for predicting upcoming cash surpluses or

shortages lead to right decisions. This would lead to tax preparation, planning purchase of new

equipment or to determine about requirement of securing loans of small business. The

management accounts has reported in various aspects as firm could guide organization for

attaining success such as utilising tools of administrative accounting along techniques as natural

resource gain, carbon foot print and life cycle cost for assisting consolidating affairs in process of

decision making. Furthermore, determining social and environmental trends which influence

ability of company to produce value over time (Schaltegger, 2018).

CONCLUSION

From the above report it had been concluded that management accounting plays very

important role for business especially to management for decision making. This report has shown

that expense could be monitored by implementing static, flexible or any other type of budget. It

has articulated that it increases efficiency and improves relationship among its management and

9

organization's attainments and history of failure for gaining insight and implementing innovative

plans. There must be implication of utilizing benchmarking cash flow for improving hoe to

manage cash and control, so try for connecting with competitors and utilise internet as tool of

research for reviewing websites. The cash flow management benchmarking could be directly

attained if situation is not ignored and implement ideas for making improvements.

M4 Analysing that while responding financial problems, management accounting lead business

for sustainable success

The basic objective of management accounting is to serve management for purpose of

decision making. On basis of financial issues, management is in requirement of information

relating to increment. Moreover, to establish strategies, practices and business models for

addressing social and environmental challenge for creating financial value and success for their

shareholders. In the present scenario, there are various organizations have presence of skills to

meet challenges and competing with sustainable economy as per Environmental management

and Assessment Institute (Horton and de Araujo Wanderley, 2018). On the contrary, there are

multiple indicators it initiates to alter and forecasts that 2-3rd of estimated forecasted growth over

coming 2 years for social and environmental data.

Simultaneously, cash flow forecast helps for predicting upcoming cash surpluses or

shortages lead to right decisions. This would lead to tax preparation, planning purchase of new

equipment or to determine about requirement of securing loans of small business. The

management accounts has reported in various aspects as firm could guide organization for

attaining success such as utilising tools of administrative accounting along techniques as natural

resource gain, carbon foot print and life cycle cost for assisting consolidating affairs in process of

decision making. Furthermore, determining social and environmental trends which influence

ability of company to produce value over time (Schaltegger, 2018).

CONCLUSION

From the above report it had been concluded that management accounting plays very

important role for business especially to management for decision making. This report has shown

that expense could be monitored by implementing static, flexible or any other type of budget. It

has articulated that it increases efficiency and improves relationship among its management and

9

shareholders of Sollatek (UK). On basis of management accounting system, both cost accounting

and job costing system are appropriate for manufacturing industry which raises productivity and

efficiency as well. Furthermore, it has reflected that managerial accounting reports accounts for

objective of planning and budgeting for purpose of measuring performance of organization.

Henceforth, planning tools such as zero based budget, ratio and variance analysis are best

planning tool for responding financial problems with application of KPI and benchmarking.

10

and job costing system are appropriate for manufacturing industry which raises productivity and

efficiency as well. Furthermore, it has reflected that managerial accounting reports accounts for

objective of planning and budgeting for purpose of measuring performance of organization.

Henceforth, planning tools such as zero based budget, ratio and variance analysis are best

planning tool for responding financial problems with application of KPI and benchmarking.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.