Management Accounting Report: Evaluating Systems for Financial Success

VerifiedAdded on 2023/01/03

|20

|4862

|26

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within Capital Joinery Ltd, a medium-scale business in the UK. The report begins by defining management accounting and outlining the requirements of various systems, including inventory management, cost accounting, job costing, and price optimization systems. It then explores different methods of management accounting reporting, such as budget reports, account receivable aging reports, cost managerial accounting reports, performance reports, and job cost reports, evaluating their benefits. The report further delves into cost analysis techniques, distinguishing between fixed, variable, sunk, explicit, and implicit costs, and their application in preparing income statements using marginal and absorption costing. It also examines various planning tools used in budgetary control, discussing their advantages and disadvantages. Finally, the report analyzes how management accounting systems are adopted to address financial problems, leading to sustainable success. The report concludes with an evaluation of the role of planning tools in resolving financial issues and promoting business success.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explaining management accounting and providing some essential requirements of various

types of management accounting systems:..................................................................................1

P2 Explaining different methods used for reporting of management accounting:......................2

M1 Evaluating benefits that management accounting systems persist as well as their

application within business:.........................................................................................................4

D1 Critical evaluation of management accounting systems and reports in integration with an

organization:................................................................................................................................4

TASK 2............................................................................................................................................5

P3 Calculating costs with the utilisation of appropriate techniques of cost analysis and

preparing income statement by using marginal as well as absorption costs:...............................5

M2 Accurate application of management accounting techniques and production of financial

reporting documents:...................................................................................................................8

D2 Producing financial reports which accurately applies and interprets data for activities of

business:.......................................................................................................................................8

TASK 3............................................................................................................................................9

P4 Explaining advantages and disadvantages in relation to different types of planning tools

that is used in budgetary control:.................................................................................................9

M3 Analysing uses of different planning tools along with their application for preparation of

budget:........................................................................................................................................11

TASK 4..........................................................................................................................................11

P5 Comparison of ways in which management accounting systems are adopted as a response

to financial problems:................................................................................................................11

M4 Analysing how management accounting leads to solution of financial problems in an

organization which lead to sustainable success:........................................................................13

D3 Evaluation of planning tools as a response to solution of financial problems for success of

business:.....................................................................................................................................13

CONCLUSION..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explaining management accounting and providing some essential requirements of various

types of management accounting systems:..................................................................................1

P2 Explaining different methods used for reporting of management accounting:......................2

M1 Evaluating benefits that management accounting systems persist as well as their

application within business:.........................................................................................................4

D1 Critical evaluation of management accounting systems and reports in integration with an

organization:................................................................................................................................4

TASK 2............................................................................................................................................5

P3 Calculating costs with the utilisation of appropriate techniques of cost analysis and

preparing income statement by using marginal as well as absorption costs:...............................5

M2 Accurate application of management accounting techniques and production of financial

reporting documents:...................................................................................................................8

D2 Producing financial reports which accurately applies and interprets data for activities of

business:.......................................................................................................................................8

TASK 3............................................................................................................................................9

P4 Explaining advantages and disadvantages in relation to different types of planning tools

that is used in budgetary control:.................................................................................................9

M3 Analysing uses of different planning tools along with their application for preparation of

budget:........................................................................................................................................11

TASK 4..........................................................................................................................................11

P5 Comparison of ways in which management accounting systems are adopted as a response

to financial problems:................................................................................................................11

M4 Analysing how management accounting leads to solution of financial problems in an

organization which lead to sustainable success:........................................................................13

D3 Evaluation of planning tools as a response to solution of financial problems for success of

business:.....................................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES:.............................................................................................................................14

.......................................................................................................................................................14

.......................................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The term Management Accounting is refers about procedure of keeping record that

enhance to internal information which effectively information about company is having strategic

decision through betterment for stabilise organisation which is formulated (Abdusalomova,

2019). Through helps whee the internal stakeholder are enhance their work responsibility to

commence for internal manager, employees, executives are better mapping all facts and figure

towards performance in market. It also helps towards external effective determine through actual

status of the enterprise in effective manner. The major objective of preparing management

accounting that to better maintain overall financial structure towards better consultancy firm in

making established towards United Kingdom.

As per this report, it is taken company such as Capital Joinery Ltd. It is a medium scale

business which is having where they tend to provide better services of financial products as well

as consulting towards furniture made to optimum quality that get to attain more competitive

advantages by following United Kingdom legislation by reducing bills. They ensure as their

every furniture to allow better traditional modern look alike. In this report the topics are covering

about requirement for different types of management accounting system. Different method in

assort in accounting report. Cost using appropriate technique for costing analysis for prepare an

income statement, to elaborate about advantages and disadvantages types of planning tools used

for budgetary control. By adapting management accounting system to better respond to financial

problem.

TASK 1

P1 Explaining management accounting and providing some essential requirements of various

types of management accounting systems:

Management accounting is the procedure of examining and communicating company's

data with managers, so firm can observe the performance from plan of action and enhance it.

Management accounting system enables managers to Capital Joinery to adequately monitor

business operations and improvise decision making by management. Mentioned below different

type of management accounting system along with its essential requirement:

Inventory management system: This technique helps in tracking position of inventory

in an organization. It keeps record of entire procedure of Capital Joinery from its

1

The term Management Accounting is refers about procedure of keeping record that

enhance to internal information which effectively information about company is having strategic

decision through betterment for stabilise organisation which is formulated (Abdusalomova,

2019). Through helps whee the internal stakeholder are enhance their work responsibility to

commence for internal manager, employees, executives are better mapping all facts and figure

towards performance in market. It also helps towards external effective determine through actual

status of the enterprise in effective manner. The major objective of preparing management

accounting that to better maintain overall financial structure towards better consultancy firm in

making established towards United Kingdom.

As per this report, it is taken company such as Capital Joinery Ltd. It is a medium scale

business which is having where they tend to provide better services of financial products as well

as consulting towards furniture made to optimum quality that get to attain more competitive

advantages by following United Kingdom legislation by reducing bills. They ensure as their

every furniture to allow better traditional modern look alike. In this report the topics are covering

about requirement for different types of management accounting system. Different method in

assort in accounting report. Cost using appropriate technique for costing analysis for prepare an

income statement, to elaborate about advantages and disadvantages types of planning tools used

for budgetary control. By adapting management accounting system to better respond to financial

problem.

TASK 1

P1 Explaining management accounting and providing some essential requirements of various

types of management accounting systems:

Management accounting is the procedure of examining and communicating company's

data with managers, so firm can observe the performance from plan of action and enhance it.

Management accounting system enables managers to Capital Joinery to adequately monitor

business operations and improvise decision making by management. Mentioned below different

type of management accounting system along with its essential requirement:

Inventory management system: This technique helps in tracking position of inventory

in an organization. It keeps record of entire procedure of Capital Joinery from its

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

purchase of raw materials, supply chain, production to sales of finished product

(Alsharari and Youssef, 2017).

Essential requirement: This system simplifies management of inventory in business and

reduces risk of over stocking or under stocking. Reason is that over stocking can cause increment

in cost of maintenance while under stocking hampers daily operations of an organization.

Cost accounting system: It is a platform where management of company records costs

incurred in an enterprise. In other words, this system records expenses that comprised in

various activities of business.

Essential requirement: Cost accounting system is an effective framework as it provides

platform to management of Capital Joinery for adequately monitor expenditure that incurs in

business. It helps in identification of unnecessary costs, by eliminating which company can

improve its profitability.

Job costing system: It enables company to accumulate information regarding costs that

is associated with each job or process of an organization. Therefore, expense of Capital

Joinery in relation to specific job can be determined with job costing system.

Essential requirement: Job costing system monitors expenditure associated with each process

of manufacturing activities of Capital Joinery. It provides flexibility to management of company

to identify productivity of process of an entity so that firm can imply cost control activities in

accordance to information gained. It improves efficiency of Capital Joinery.

Price optimisation system: This system keep tracks of variations in demand in

accordance to changing levels of product prices (Alborov and et. al , 2017). It provides

platform for efficient analysis of results consisted with changing prices.

Essential requirement: Price optimisation system helps Capital Joinery to align prices of its

product with expectations of customers. This leads to increment in satisfaction level of customer

and helps company in attracting large number of customers.

P2 Explaining different methods used for reporting of management accounting:

Management Accounting Reporting is defined as the formulation of reports in context

of managers or chief executive officer associated with the various business operations related

with the total quality management, logistics, human resources. Information technology, research

and development, marketing and many more operations as per the company requirements (Ax

and Greve, 2017). Reports on all such operations helps the managers and CEO of an organization

2

(Alsharari and Youssef, 2017).

Essential requirement: This system simplifies management of inventory in business and

reduces risk of over stocking or under stocking. Reason is that over stocking can cause increment

in cost of maintenance while under stocking hampers daily operations of an organization.

Cost accounting system: It is a platform where management of company records costs

incurred in an enterprise. In other words, this system records expenses that comprised in

various activities of business.

Essential requirement: Cost accounting system is an effective framework as it provides

platform to management of Capital Joinery for adequately monitor expenditure that incurs in

business. It helps in identification of unnecessary costs, by eliminating which company can

improve its profitability.

Job costing system: It enables company to accumulate information regarding costs that

is associated with each job or process of an organization. Therefore, expense of Capital

Joinery in relation to specific job can be determined with job costing system.

Essential requirement: Job costing system monitors expenditure associated with each process

of manufacturing activities of Capital Joinery. It provides flexibility to management of company

to identify productivity of process of an entity so that firm can imply cost control activities in

accordance to information gained. It improves efficiency of Capital Joinery.

Price optimisation system: This system keep tracks of variations in demand in

accordance to changing levels of product prices (Alborov and et. al , 2017). It provides

platform for efficient analysis of results consisted with changing prices.

Essential requirement: Price optimisation system helps Capital Joinery to align prices of its

product with expectations of customers. This leads to increment in satisfaction level of customer

and helps company in attracting large number of customers.

P2 Explaining different methods used for reporting of management accounting:

Management Accounting Reporting is defined as the formulation of reports in context

of managers or chief executive officer associated with the various business operations related

with the total quality management, logistics, human resources. Information technology, research

and development, marketing and many more operations as per the company requirements (Ax

and Greve, 2017). Reports on all such operations helps the managers and CEO of an organization

2

in functions of the management like planning, organizing, staffing, directing and controlling.

They used to analyse and interpret such reports in order to forecast and predict the

implementation of new ideas within the budget and report structure. Observation these

management accounting reports helps the firm in gaining the desired sales and objectives goals

for an organization.

Methods

Budget reports enables budgetary control of each and every operation or department of

the firm. It basically consist that how much budget is set for the research and

development department or marketing department (Cooper, Ezzamel and Qu, 2017).

Within the funds set to spend, at that limit only, team member of each department can

spend their money accordingly.

Account Receivable Ageing Reports is a type of report where all the receiving money is

calculated and stated by the finance department. It mentions all the invoices by the

customers, suppliers, internal and external stakeholders of an organization. It is important

measure such report because it helps in analysing the future budget or funding in an

organization.

Cost Managerial Accounting Reports ensures that costs and expenses are recorded and

calculated by the finance team of an organization (Drury, 2018). It mentions all the cost

which are occurred in raw materials, production purposes, marketing expenses, employee

expenses, electricity and many more cost which overall business has to bear is stated in

this type of report.

Performance Reports is a type of report where all the performances are measures in

terms of monetary basis. It mentions the comparison between the planned budget and

outcome of investing of such funds from the business. It helps the company in comparing

the cost which was estimated and which was actually being spend.

Job Cost Reports provides platform for evaluation of ongoing cost are measure and

stated in this type of report (Hiebl and Richter, 2018). It mentions the everyday expenses

which are being bear by the company which are occurred in a regular business operations

in an organization. This helps the firm in getting the day to day report of the expenses in

a company.

Benefits:

3

They used to analyse and interpret such reports in order to forecast and predict the

implementation of new ideas within the budget and report structure. Observation these

management accounting reports helps the firm in gaining the desired sales and objectives goals

for an organization.

Methods

Budget reports enables budgetary control of each and every operation or department of

the firm. It basically consist that how much budget is set for the research and

development department or marketing department (Cooper, Ezzamel and Qu, 2017).

Within the funds set to spend, at that limit only, team member of each department can

spend their money accordingly.

Account Receivable Ageing Reports is a type of report where all the receiving money is

calculated and stated by the finance department. It mentions all the invoices by the

customers, suppliers, internal and external stakeholders of an organization. It is important

measure such report because it helps in analysing the future budget or funding in an

organization.

Cost Managerial Accounting Reports ensures that costs and expenses are recorded and

calculated by the finance team of an organization (Drury, 2018). It mentions all the cost

which are occurred in raw materials, production purposes, marketing expenses, employee

expenses, electricity and many more cost which overall business has to bear is stated in

this type of report.

Performance Reports is a type of report where all the performances are measures in

terms of monetary basis. It mentions the comparison between the planned budget and

outcome of investing of such funds from the business. It helps the company in comparing

the cost which was estimated and which was actually being spend.

Job Cost Reports provides platform for evaluation of ongoing cost are measure and

stated in this type of report (Hiebl and Richter, 2018). It mentions the everyday expenses

which are being bear by the company which are occurred in a regular business operations

in an organization. This helps the firm in getting the day to day report of the expenses in

a company.

Benefits:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Improvement in profits: Using such reports in a company help the firm in improving

the profits and revenues. Because these reports assist the company in observing and

analysing the reports which gives them the direction that where they can cut the expenses

and where they can increase the prices for the products and services of an organization.

Future planning: Management accounting reports supports the firm in forecasting and

prediction in upcoming cost and expenses so it basically it also helps in future planning in

terms of investments and funding regarding the salary of employees and many more as

per the business needs and requirements.

Regulation to activities: By analysing the cost of the company, it becomes more easy for

the organization to regulate their activities accordingly in terms of each and every

function or department of the firm (Langfield-Smith, Thorne and Hilton, 2018). If

company already knows that how much they have to spend in every operations of the

company then the regulation of the activities can be automatically performed.

M1 Evaluating benefits that management accounting systems persist as well as their application

within business:

Management accounting system tracks financial information of an organization which

enhances its strategic formulation and improves productivity.

Inventory management system helps in reducing risk of high cost or hindrance in

business activity due to mismanagement of inventory.

Cost accounting system records expenses of Capital Joinery which helps in

implementation of cost control activities.

Job costing system keeps track of expenditures incurred in each jobs of company.

Price optimisation system provides platform for setting optimum price of products.

D1 Critical evaluation of management accounting systems and reports in integration with an

organization:

Management accounting systems and report improves monitoring or management

activities of Capital Joinery. Cost accounting and job costing system helps in cost reduction

whereas price optimisation leads to high profit generation with effective price setting. Inventory

management system improves efficiency of company. Budgetary reports estimates revenues and

expenditure of an organization.

4

the profits and revenues. Because these reports assist the company in observing and

analysing the reports which gives them the direction that where they can cut the expenses

and where they can increase the prices for the products and services of an organization.

Future planning: Management accounting reports supports the firm in forecasting and

prediction in upcoming cost and expenses so it basically it also helps in future planning in

terms of investments and funding regarding the salary of employees and many more as

per the business needs and requirements.

Regulation to activities: By analysing the cost of the company, it becomes more easy for

the organization to regulate their activities accordingly in terms of each and every

function or department of the firm (Langfield-Smith, Thorne and Hilton, 2018). If

company already knows that how much they have to spend in every operations of the

company then the regulation of the activities can be automatically performed.

M1 Evaluating benefits that management accounting systems persist as well as their application

within business:

Management accounting system tracks financial information of an organization which

enhances its strategic formulation and improves productivity.

Inventory management system helps in reducing risk of high cost or hindrance in

business activity due to mismanagement of inventory.

Cost accounting system records expenses of Capital Joinery which helps in

implementation of cost control activities.

Job costing system keeps track of expenditures incurred in each jobs of company.

Price optimisation system provides platform for setting optimum price of products.

D1 Critical evaluation of management accounting systems and reports in integration with an

organization:

Management accounting systems and report improves monitoring or management

activities of Capital Joinery. Cost accounting and job costing system helps in cost reduction

whereas price optimisation leads to high profit generation with effective price setting. Inventory

management system improves efficiency of company. Budgetary reports estimates revenues and

expenditure of an organization.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

P3 Calculating costs with the utilisation of appropriate techniques of cost analysis and preparing

income statement by using marginal as well as absorption costs:

It is defined as the expenses occurred in the operations of the company. These expenses

includes the basic like electricity, water, facilities and many expenses, Heavy expenses includes

the raw materials cost, expenses in marketing, HR, IT, R&D and many more departments.

Expenses on assets like machinery, building and other assets of the firm.

Types of cost: Fixed cost: It evaluates costs incurred either every day, week, month or year. Like salary

of the employees, machinery depreciation cost, building cost, rent cost and many more

cost which are to be fixed by the firm and which cannot be changed in any way. That is

why it is known as the fixed cost. Variable cost: It is type of cost which are incurred on variable basis like sudden cost.

Like electricity bill, damage of machinery cost, raw materials cost, technology cost and

many more cost which changes from time to time and can occur on a sudden basis. That

is why it is known as the variable cost. Sunk cost: This cost incurs if any recovery of loan or non repayment is not dome by the

external or internal stakeholders (Lindholm Laine and Suomala, 2017). It is the cost

which are non recoverable and cannot be recovered at any cost by the company. That is

why it is known as the sunk cost. Explicit cost: It is a type of cost which are incurred externally from the company. Like

wages, rents, raw materials and many more. These are those cost which are directly bear

by the company and either fixed or variable cost in terms of monetary amount. It is also

known as the external cost which are generally shown in the books of accounts. That is

why it is known as the explicit cost.

Implicit cost: It is a type of cost which are incurred as an opportunity cost which are not

actually paid by the firm directly. It uses the resources directly of the company which are

already owned by an organization. It is also known as the internal cost which are

generally not shown in the books of accounts. That is why it is known as the implicit

cost.

Cost analysis

5

P3 Calculating costs with the utilisation of appropriate techniques of cost analysis and preparing

income statement by using marginal as well as absorption costs:

It is defined as the expenses occurred in the operations of the company. These expenses

includes the basic like electricity, water, facilities and many expenses, Heavy expenses includes

the raw materials cost, expenses in marketing, HR, IT, R&D and many more departments.

Expenses on assets like machinery, building and other assets of the firm.

Types of cost: Fixed cost: It evaluates costs incurred either every day, week, month or year. Like salary

of the employees, machinery depreciation cost, building cost, rent cost and many more

cost which are to be fixed by the firm and which cannot be changed in any way. That is

why it is known as the fixed cost. Variable cost: It is type of cost which are incurred on variable basis like sudden cost.

Like electricity bill, damage of machinery cost, raw materials cost, technology cost and

many more cost which changes from time to time and can occur on a sudden basis. That

is why it is known as the variable cost. Sunk cost: This cost incurs if any recovery of loan or non repayment is not dome by the

external or internal stakeholders (Lindholm Laine and Suomala, 2017). It is the cost

which are non recoverable and cannot be recovered at any cost by the company. That is

why it is known as the sunk cost. Explicit cost: It is a type of cost which are incurred externally from the company. Like

wages, rents, raw materials and many more. These are those cost which are directly bear

by the company and either fixed or variable cost in terms of monetary amount. It is also

known as the external cost which are generally shown in the books of accounts. That is

why it is known as the explicit cost.

Implicit cost: It is a type of cost which are incurred as an opportunity cost which are not

actually paid by the firm directly. It uses the resources directly of the company which are

already owned by an organization. It is also known as the internal cost which are

generally not shown in the books of accounts. That is why it is known as the implicit

cost.

Cost analysis

5

It is defined as the analysis which are done on the cost of an organization. Each and every

type of cost requires the analysis for the better functioning of the company and so that the

company can improve it's operations in every department of the firm and can meet their goals

and objectives of the company. Analysis includes the forecasting, interpreting and observing the

various cost which are to be bear by the company.

Types of cost analysis: Life cycle cost analysis: It is the type of analysis which is done according to the life cycle

of the company. For example, life cycle from purchasing of raw materials to the selling

of the products and services with the maximum return in terms if profits and revenues.

Cost benefit analysis: It is the type of analysis which is done for the extra benefit of the

company that means more than the assumptions or expected return by the firm (Malina

ed., 2017). This analysis finds out the best approach to generate more benefit to the firm.

6

type of cost requires the analysis for the better functioning of the company and so that the

company can improve it's operations in every department of the firm and can meet their goals

and objectives of the company. Analysis includes the forecasting, interpreting and observing the

various cost which are to be bear by the company.

Types of cost analysis: Life cycle cost analysis: It is the type of analysis which is done according to the life cycle

of the company. For example, life cycle from purchasing of raw materials to the selling

of the products and services with the maximum return in terms if profits and revenues.

Cost benefit analysis: It is the type of analysis which is done for the extra benefit of the

company that means more than the assumptions or expected return by the firm (Malina

ed., 2017). This analysis finds out the best approach to generate more benefit to the firm.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

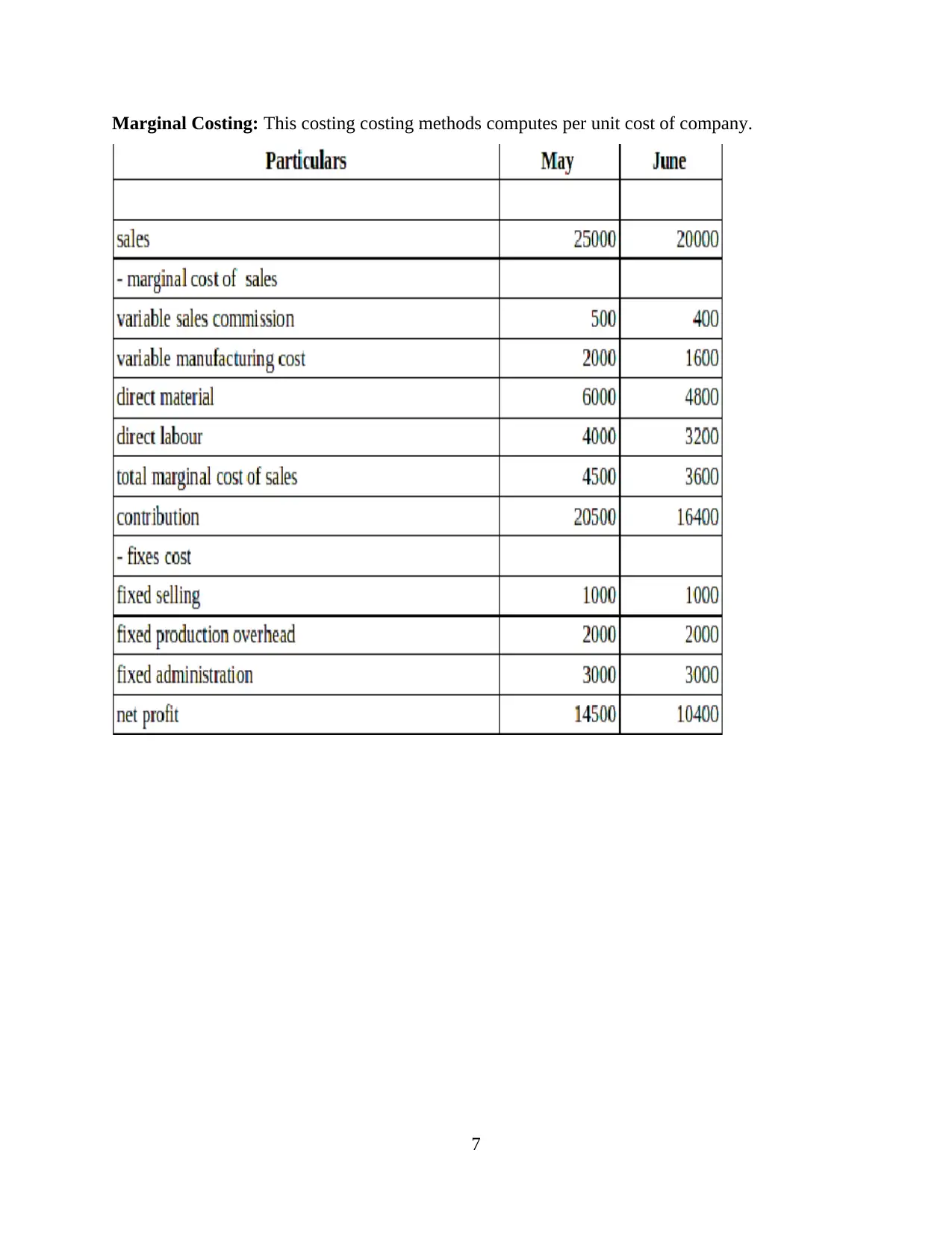

Marginal Costing: This costing costing methods computes per unit cost of company.

7

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

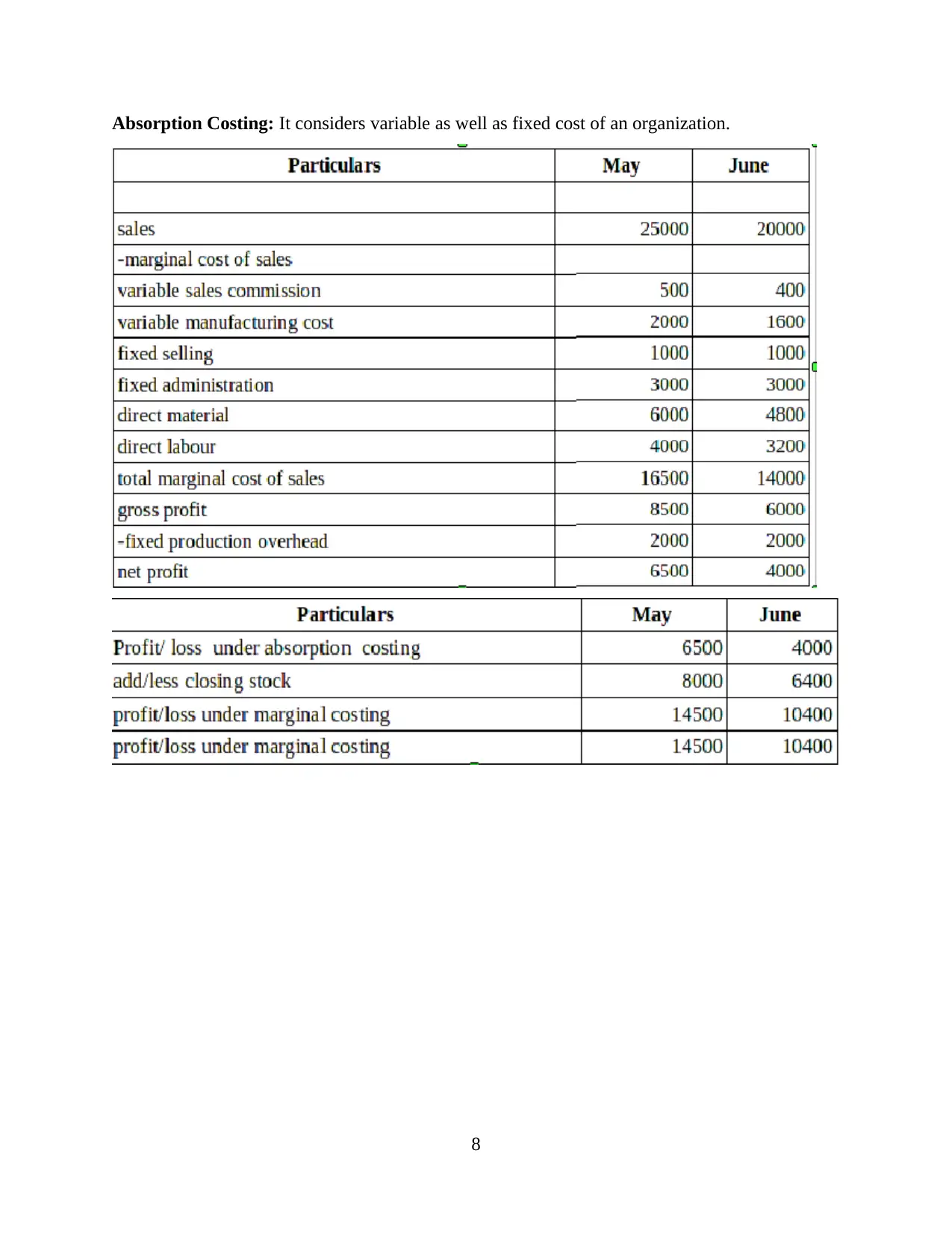

Absorption Costing: It considers variable as well as fixed cost of an organization.

8

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.