HI5017 Management Accounting Case Studies: Cost Analysis & Critique

VerifiedAdded on 2023/03/31

|11

|3347

|500

Case Study

AI Summary

This assignment presents a comprehensive analysis of a management accounting case study, focusing on cost concepts, relevant vs. irrelevant costs, and incremental cash flow analysis. It evaluates different alternatives for decision-making and provides a recommendation letter based on the analysis. Additionally, it includes a critique of a journal article, examining the role of managerial accounting in innovation management, specifically referencing Canon, Inc. and Apple Computer, Inc. The analysis covers the application of managerial accounting tools and techniques in enhancing decision-making processes and achieving business success. The assignment concludes by highlighting the importance of information sharing and collaboration in developing innovative products and ensuring cost-effectiveness.

Running head: MANAGEMENT ACCOUNTING CASE STUDIES

Management Accounting Case Studies

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Management Accounting Case Studies

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING CASE STUDIES

Table of Contents

Part A: Analysis of Case Study.....................................................................................2

Requirement 1:..........................................................................................................2

Requirement 2:..........................................................................................................2

Requirement 3..............................................................................................................3

Requirement 4...........................................................................................................3

Requirement 5:..........................................................................................................4

Part B: Critique of the journal article.............................................................................6

Requirement 1:..........................................................................................................6

Requirement 2:..........................................................................................................7

Requirement 3:..........................................................................................................7

References:................................................................................................................10

Table of Contents

Part A: Analysis of Case Study.....................................................................................2

Requirement 1:..........................................................................................................2

Requirement 2:..........................................................................................................2

Requirement 3..............................................................................................................3

Requirement 4...........................................................................................................3

Requirement 5:..........................................................................................................4

Part B: Critique of the journal article.............................................................................6

Requirement 1:..........................................................................................................6

Requirement 2:..........................................................................................................7

Requirement 3:..........................................................................................................7

References:................................................................................................................10

2MANAGEMENT ACCOUNTING CASE STUDIES

Part A: Analysis of Case Study

Requirement 1:

There were various costs which were included in the case study and the same

were in the form of fixed, variable, sunk and incremental costs. While evaluating the

financial viability of an investment or a project it is essential that sunk costs should

not be treated or taken into account. There are several costs like fixed cost which do

not change with the change in the level of business activity carried out by a

company. On the other hand variable costs are the one which do change with the

change in the level of activity and business operations undertaken by the company.

Increase in the business activity for a company sometimes often leads to increase in

the additional or incremental costs which are borne by the company. A key

illustration of the above described costs could be well described with the help of

examples given below:

Costs Illustrations

Fixed Cost Annual License Fees costing around $225 can be well related.

Variable Cost Amount gathered for child at a rate of $800 will be changing or

varying with the change in the number of students enrolling for the

same.

Incremental Cost Cost of Utilities and the increasing usage of the same due to increase

in the day factor can be well described as an incremental cost in

response to the increased usage of utilities.

Requirement 2:

There are various costs and factors applicable which may be relevant and

irrelevant while making the decision of purchasing the appliances. The key issues

which can be addressed in this situation are whether costs that would be incurred in

the view of future decision and can the costs be differentiated from the various

available alternatives. After specifying a certain criteria a cost is said to be relevant.

Thus a various factors and costs need to be accounted for while going for a

purchase consideration of a new appliance as:

Cost of the new appliance

Other Costs (Delivery and Installation Costs

Additional Utility Costs

While analysing the best alternative available for frank it is also equally important

to consider the various costs that are related with the purchase of appliances. Thus

few other costs might also be taken into account like:

Delivery and Pick up Charges Associated with the services rendered.

Self Service Costs like expenses related to laundry, detergent and

mileage.

Old Costs relating to the old equipment should not be further evaluated from the

various available options and must not be necessary to incorporate the same in the

future decisions. Costs that can be irrelevant while assessing the feasibility of

purchasing if new appliances could be as follows:

Old Appliance Expenses

Part A: Analysis of Case Study

Requirement 1:

There were various costs which were included in the case study and the same

were in the form of fixed, variable, sunk and incremental costs. While evaluating the

financial viability of an investment or a project it is essential that sunk costs should

not be treated or taken into account. There are several costs like fixed cost which do

not change with the change in the level of business activity carried out by a

company. On the other hand variable costs are the one which do change with the

change in the level of activity and business operations undertaken by the company.

Increase in the business activity for a company sometimes often leads to increase in

the additional or incremental costs which are borne by the company. A key

illustration of the above described costs could be well described with the help of

examples given below:

Costs Illustrations

Fixed Cost Annual License Fees costing around $225 can be well related.

Variable Cost Amount gathered for child at a rate of $800 will be changing or

varying with the change in the number of students enrolling for the

same.

Incremental Cost Cost of Utilities and the increasing usage of the same due to increase

in the day factor can be well described as an incremental cost in

response to the increased usage of utilities.

Requirement 2:

There are various costs and factors applicable which may be relevant and

irrelevant while making the decision of purchasing the appliances. The key issues

which can be addressed in this situation are whether costs that would be incurred in

the view of future decision and can the costs be differentiated from the various

available alternatives. After specifying a certain criteria a cost is said to be relevant.

Thus a various factors and costs need to be accounted for while going for a

purchase consideration of a new appliance as:

Cost of the new appliance

Other Costs (Delivery and Installation Costs

Additional Utility Costs

While analysing the best alternative available for frank it is also equally important

to consider the various costs that are related with the purchase of appliances. Thus

few other costs might also be taken into account like:

Delivery and Pick up Charges Associated with the services rendered.

Self Service Costs like expenses related to laundry, detergent and

mileage.

Old Costs relating to the old equipment should not be further evaluated from the

various available options and must not be necessary to incorporate the same in the

future decisions. Costs that can be irrelevant while assessing the feasibility of

purchasing if new appliances could be as follows:

Old Appliance Expenses

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING CASE STUDIES

Detergent Costs. This costs would not be consider material if delivery and

pick up services are not taken into account for the same.

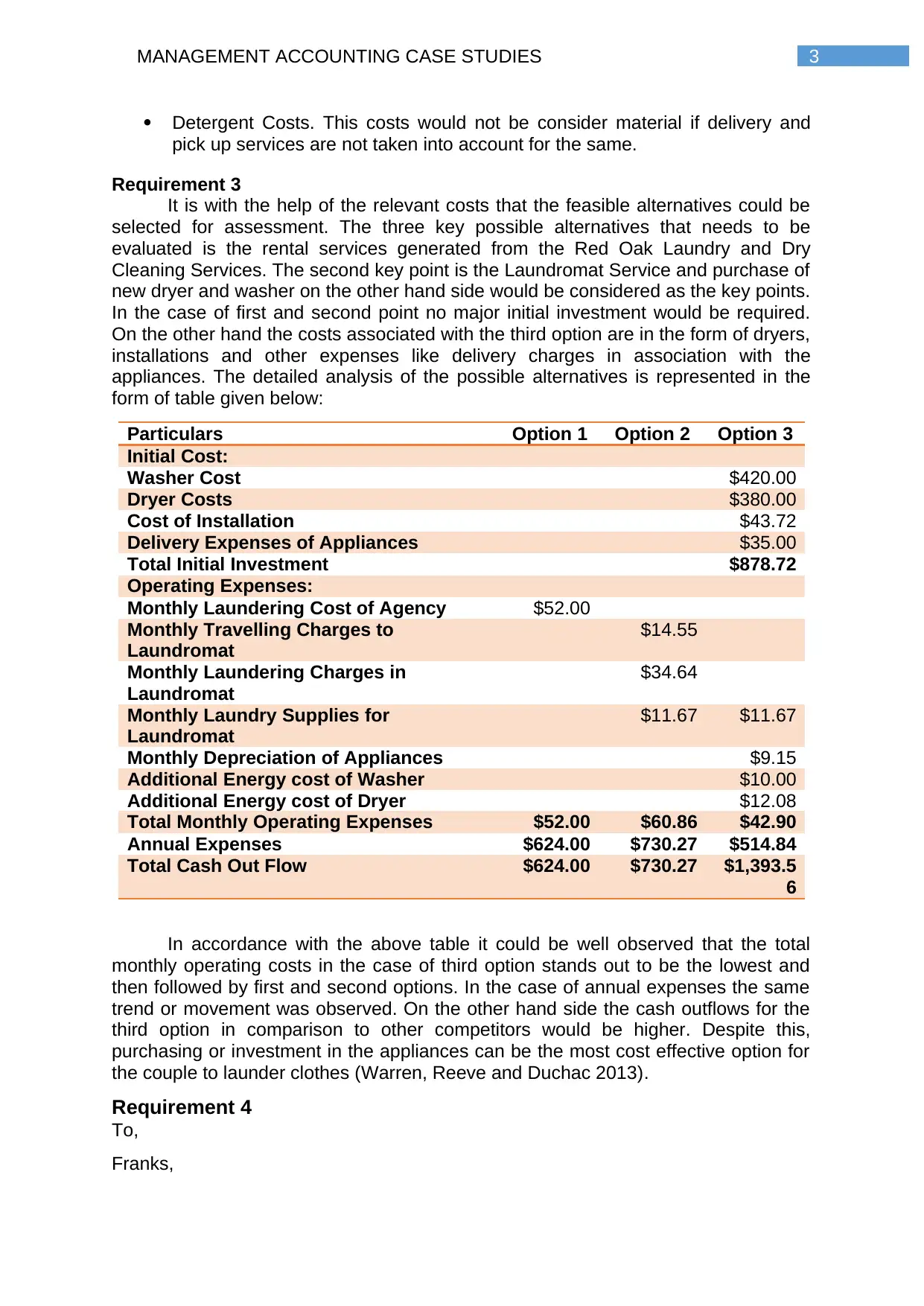

Requirement 3

It is with the help of the relevant costs that the feasible alternatives could be

selected for assessment. The three key possible alternatives that needs to be

evaluated is the rental services generated from the Red Oak Laundry and Dry

Cleaning Services. The second key point is the Laundromat Service and purchase of

new dryer and washer on the other hand side would be considered as the key points.

In the case of first and second point no major initial investment would be required.

On the other hand the costs associated with the third option are in the form of dryers,

installations and other expenses like delivery charges in association with the

appliances. The detailed analysis of the possible alternatives is represented in the

form of table given below:

Particulars Option 1 Option 2 Option 3

Initial Cost:

Washer Cost $420.00

Dryer Costs $380.00

Cost of Installation $43.72

Delivery Expenses of Appliances $35.00

Total Initial Investment $878.72

Operating Expenses:

Monthly Laundering Cost of Agency $52.00

Monthly Travelling Charges to

Laundromat

$14.55

Monthly Laundering Charges in

Laundromat

$34.64

Monthly Laundry Supplies for

Laundromat

$11.67 $11.67

Monthly Depreciation of Appliances $9.15

Additional Energy cost of Washer $10.00

Additional Energy cost of Dryer $12.08

Total Monthly Operating Expenses $52.00 $60.86 $42.90

Annual Expenses $624.00 $730.27 $514.84

Total Cash Out Flow $624.00 $730.27 $1,393.5

6

In accordance with the above table it could be well observed that the total

monthly operating costs in the case of third option stands out to be the lowest and

then followed by first and second options. In the case of annual expenses the same

trend or movement was observed. On the other hand side the cash outflows for the

third option in comparison to other competitors would be higher. Despite this,

purchasing or investment in the appliances can be the most cost effective option for

the couple to launder clothes (Warren, Reeve and Duchac 2013).

Requirement 4

To,

Franks,

Detergent Costs. This costs would not be consider material if delivery and

pick up services are not taken into account for the same.

Requirement 3

It is with the help of the relevant costs that the feasible alternatives could be

selected for assessment. The three key possible alternatives that needs to be

evaluated is the rental services generated from the Red Oak Laundry and Dry

Cleaning Services. The second key point is the Laundromat Service and purchase of

new dryer and washer on the other hand side would be considered as the key points.

In the case of first and second point no major initial investment would be required.

On the other hand the costs associated with the third option are in the form of dryers,

installations and other expenses like delivery charges in association with the

appliances. The detailed analysis of the possible alternatives is represented in the

form of table given below:

Particulars Option 1 Option 2 Option 3

Initial Cost:

Washer Cost $420.00

Dryer Costs $380.00

Cost of Installation $43.72

Delivery Expenses of Appliances $35.00

Total Initial Investment $878.72

Operating Expenses:

Monthly Laundering Cost of Agency $52.00

Monthly Travelling Charges to

Laundromat

$14.55

Monthly Laundering Charges in

Laundromat

$34.64

Monthly Laundry Supplies for

Laundromat

$11.67 $11.67

Monthly Depreciation of Appliances $9.15

Additional Energy cost of Washer $10.00

Additional Energy cost of Dryer $12.08

Total Monthly Operating Expenses $52.00 $60.86 $42.90

Annual Expenses $624.00 $730.27 $514.84

Total Cash Out Flow $624.00 $730.27 $1,393.5

6

In accordance with the above table it could be well observed that the total

monthly operating costs in the case of third option stands out to be the lowest and

then followed by first and second options. In the case of annual expenses the same

trend or movement was observed. On the other hand side the cash outflows for the

third option in comparison to other competitors would be higher. Despite this,

purchasing or investment in the appliances can be the most cost effective option for

the couple to launder clothes (Warren, Reeve and Duchac 2013).

Requirement 4

To,

Franks,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING CASE STUDIES

Date: 30th May 2019

Subject: Letter of recommendation

The situation provided to us needs to be analysed with the help of incremental

cash flows analysis. However, incremental costs in association with the case needs

to be well accounted in this case. Changes in the level of costs could be observed

due to incremental staffs introduced for feeding additional children. Every change in

the level of revenue needs to be well accounted. Incremental changes could be well

represented as given below:

Particulars Amount

Increased Number of Children 3

Revenue per Child $800

Incremental/Increased Revenue per Month $2,400

No. of employees 1

Labour Hour per week 40

Labour Charges per hour $9

Incremental Labour Charges per month $1,559

Food cost per day for each child $ 3.20

Number of days per week 5

Incremental food cost per month $208

Total Incremental cost $1,767

Incremental Profit per month $633

The incremental revenue, which is obtained by adding three children, would

be around $2400, which exceeds the costs that would be incurred in the form of

incremental food and additional staff where expenses amount to around $1767. A

total of $633 will be the benefit of Frank and the same can be achieved when the

option would be exercised.

Requirement 5:

There is a need for obtaining understanding on the issue that it has been

obtained for the management of the organisation in order to undertake decision

regarding the facility locations as well as enrolment decisions that needs overview

related to strategic objectives. The aspect would be highly useful for gaining an

overview of the effects of enrolment decision on the needed number of employees

along with excess food costs. For the two provided options, the monthly income

statements have to be computed. From the computation, it is apparent that an extra

employee is required for providing service to nine children. When the number of

children rises to 12, two staffs are needed and when the figure is 14, there would be

requirement of three additional staffs.

Staying in Current Location:-

Particulars 6 children 9 children

Revenue $ 4,800 $ 7,200

Expenses:

Date: 30th May 2019

Subject: Letter of recommendation

The situation provided to us needs to be analysed with the help of incremental

cash flows analysis. However, incremental costs in association with the case needs

to be well accounted in this case. Changes in the level of costs could be observed

due to incremental staffs introduced for feeding additional children. Every change in

the level of revenue needs to be well accounted. Incremental changes could be well

represented as given below:

Particulars Amount

Increased Number of Children 3

Revenue per Child $800

Incremental/Increased Revenue per Month $2,400

No. of employees 1

Labour Hour per week 40

Labour Charges per hour $9

Incremental Labour Charges per month $1,559

Food cost per day for each child $ 3.20

Number of days per week 5

Incremental food cost per month $208

Total Incremental cost $1,767

Incremental Profit per month $633

The incremental revenue, which is obtained by adding three children, would

be around $2400, which exceeds the costs that would be incurred in the form of

incremental food and additional staff where expenses amount to around $1767. A

total of $633 will be the benefit of Frank and the same can be achieved when the

option would be exercised.

Requirement 5:

There is a need for obtaining understanding on the issue that it has been

obtained for the management of the organisation in order to undertake decision

regarding the facility locations as well as enrolment decisions that needs overview

related to strategic objectives. The aspect would be highly useful for gaining an

overview of the effects of enrolment decision on the needed number of employees

along with excess food costs. For the two provided options, the monthly income

statements have to be computed. From the computation, it is apparent that an extra

employee is required for providing service to nine children. When the number of

children rises to 12, two staffs are needed and when the figure is 14, there would be

requirement of three additional staffs.

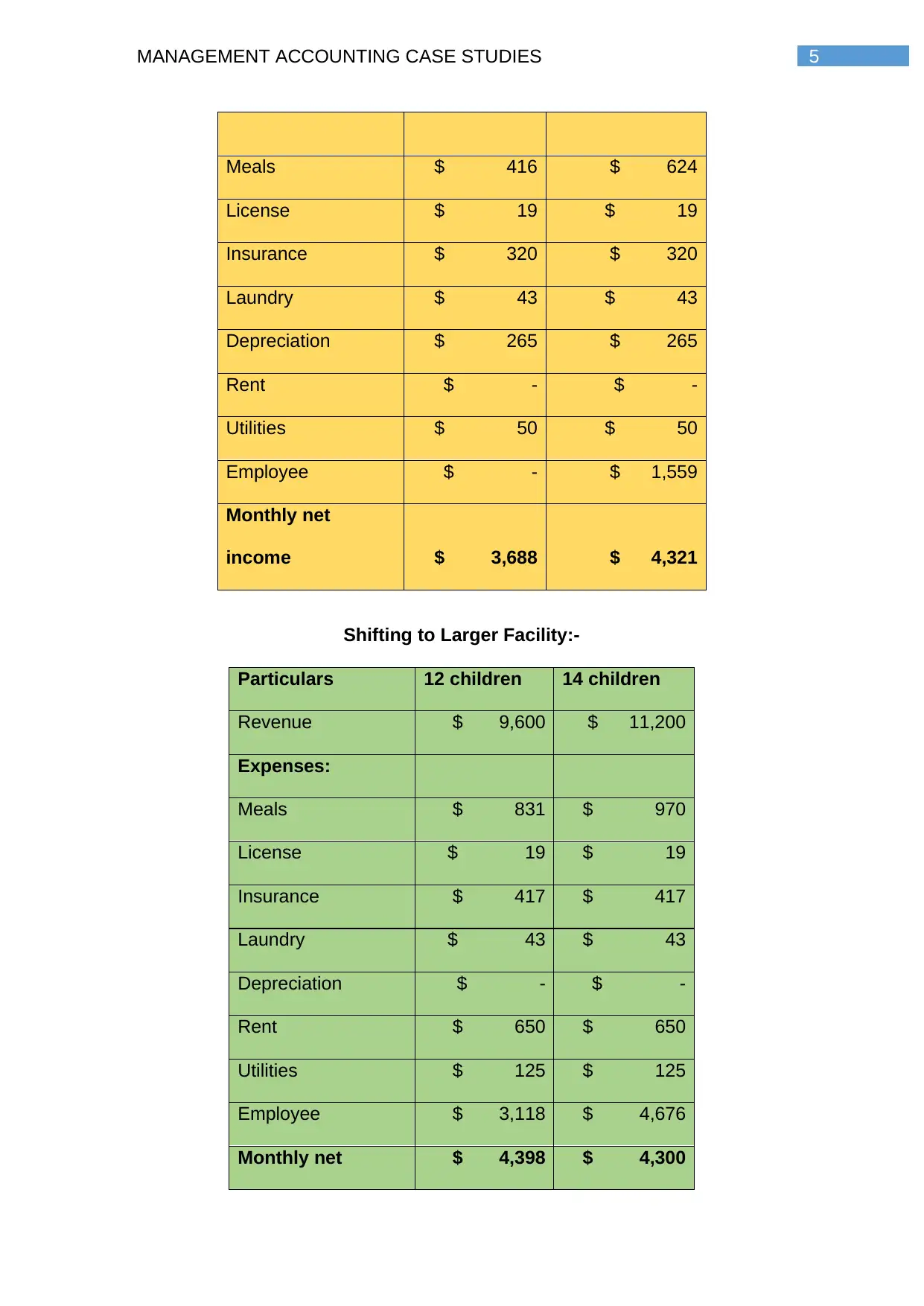

Staying in Current Location:-

Particulars 6 children 9 children

Revenue $ 4,800 $ 7,200

Expenses:

5MANAGEMENT ACCOUNTING CASE STUDIES

Meals $ 416 $ 624

License $ 19 $ 19

Insurance $ 320 $ 320

Laundry $ 43 $ 43

Depreciation $ 265 $ 265

Rent $ - $ -

Utilities $ 50 $ 50

Employee $ - $ 1,559

Monthly net

income $ 3,688 $ 4,321

Shifting to Larger Facility:-

Particulars 12 children 14 children

Revenue $ 9,600 $ 11,200

Expenses:

Meals $ 831 $ 970

License $ 19 $ 19

Insurance $ 417 $ 417

Laundry $ 43 $ 43

Depreciation $ - $ -

Rent $ 650 $ 650

Utilities $ 125 $ 125

Employee $ 3,118 $ 4,676

Monthly net $ 4,398 $ 4,300

Meals $ 416 $ 624

License $ 19 $ 19

Insurance $ 320 $ 320

Laundry $ 43 $ 43

Depreciation $ 265 $ 265

Rent $ - $ -

Utilities $ 50 $ 50

Employee $ - $ 1,559

Monthly net

income $ 3,688 $ 4,321

Shifting to Larger Facility:-

Particulars 12 children 14 children

Revenue $ 9,600 $ 11,200

Expenses:

Meals $ 831 $ 970

License $ 19 $ 19

Insurance $ 417 $ 417

Laundry $ 43 $ 43

Depreciation $ - $ -

Rent $ 650 $ 650

Utilities $ 125 $ 125

Employee $ 3,118 $ 4,676

Monthly net $ 4,398 $ 4,300

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING CASE STUDIES

income

Based on the above computation, it could be stated that the reasonable and

actionable course needs to be chosen. The result of the above computation denotes

that the most significant income would happen in the presence of six children. There

is no need to take into account the difference in income among 9, 12 and 14 children

when the future point is observed to be diminishing. If Frank undertakes the decision

of sifting to a bigger facility by accommodating 12 children, the expected monthly

income would be $4,397.72, which is greater in contrast to the other alternative.

Hence, by accepting this alternative, there would be greater monthly income for

Frank.

Part B: Critique of the journal article

Requirement 1:

Managerial accounting could be described as the mechanism of assessing

the cost of the organisations and financial data so that it could result in better

decisions. The big global entities are involved in the application of managerial

accounting concept in their decision-making processes (Mihăilă 2014). This

application could be witnessed in the journal named “Towards a new theory of

innovation management: A case study comparing Cannon, Inc. and Apple

Computer Inc”.

Apple Inc along with Canon Inc are observed to the leaders in the market in

their respective markets, which are photocopier sector and the premium computer

manufacturing sector. Success could be considered in the form a competitive

scenario having dependence on sound ground management along with different core

competencies of other firms. The companies have to generate innovation when they

offer products to the customers. Efficiency needs to be present in cost management

as well because of the massive technological changes. There is requirement for

sound management to combat with the market hurdles for maintaining superiority in

the industry. In the provided journal, it could be seen that the method of creation of

information and sharing have been provided significant emphasis due to the need of

managerial accounting. In the provided case of Canon, the firm is observed to carry

out feasibility study by including staffs working in different departments. The product

was new to be launched in the market, which is a mini-copier. The policy was to

undertake sound decision when the top executive team of each department is

present. The hard work of Steve Jobs is known to all along with the success

achieved by the individual. However, the major reason for the business success is

sound and effective management. As stated in the article, the management team of

Apple is highly efficient and continual interaction was maintained by them for

increasing the strength of the management. The application of sound tools of

management accounting as well as techniques related to the same have assisted

the firm to exploit the market opportunities for increasing the innovativeness of

products along with ensuring cost effectiveness (Narayanaswamy 2017). In addition,

it could be observed that the organisations have been working in combination with

their executives, managers and engineers to ensure full harmonisation for

developing innovative products in collaboration with the respective sectors.

income

Based on the above computation, it could be stated that the reasonable and

actionable course needs to be chosen. The result of the above computation denotes

that the most significant income would happen in the presence of six children. There

is no need to take into account the difference in income among 9, 12 and 14 children

when the future point is observed to be diminishing. If Frank undertakes the decision

of sifting to a bigger facility by accommodating 12 children, the expected monthly

income would be $4,397.72, which is greater in contrast to the other alternative.

Hence, by accepting this alternative, there would be greater monthly income for

Frank.

Part B: Critique of the journal article

Requirement 1:

Managerial accounting could be described as the mechanism of assessing

the cost of the organisations and financial data so that it could result in better

decisions. The big global entities are involved in the application of managerial

accounting concept in their decision-making processes (Mihăilă 2014). This

application could be witnessed in the journal named “Towards a new theory of

innovation management: A case study comparing Cannon, Inc. and Apple

Computer Inc”.

Apple Inc along with Canon Inc are observed to the leaders in the market in

their respective markets, which are photocopier sector and the premium computer

manufacturing sector. Success could be considered in the form a competitive

scenario having dependence on sound ground management along with different core

competencies of other firms. The companies have to generate innovation when they

offer products to the customers. Efficiency needs to be present in cost management

as well because of the massive technological changes. There is requirement for

sound management to combat with the market hurdles for maintaining superiority in

the industry. In the provided journal, it could be seen that the method of creation of

information and sharing have been provided significant emphasis due to the need of

managerial accounting. In the provided case of Canon, the firm is observed to carry

out feasibility study by including staffs working in different departments. The product

was new to be launched in the market, which is a mini-copier. The policy was to

undertake sound decision when the top executive team of each department is

present. The hard work of Steve Jobs is known to all along with the success

achieved by the individual. However, the major reason for the business success is

sound and effective management. As stated in the article, the management team of

Apple is highly efficient and continual interaction was maintained by them for

increasing the strength of the management. The application of sound tools of

management accounting as well as techniques related to the same have assisted

the firm to exploit the market opportunities for increasing the innovativeness of

products along with ensuring cost effectiveness (Narayanaswamy 2017). In addition,

it could be observed that the organisations have been working in combination with

their executives, managers and engineers to ensure full harmonisation for

developing innovative products in collaboration with the respective sectors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING CASE STUDIES

By analysing the above aspects, it could be said that efficient and effective

application of the tools and techniques of managerial accounting help the firms in

enhancing their decision-making process for entire business success.

Requirement 2:

Both managerial accounting and management accounting technique are

continual business processes, which help in bringing innovation to the management

systems for undertaking sound business decisions. The provided article provided a

summary of innovation in the management system of an organisation in the form of

the process of development of innovation and sound sharing of information. This is a

significant proposition owing to the presence of many firms, in which the analysis

and usage of financial and non-financial information could be witnessed in the

processes of the management. Hence, it could be stated that the management of an

entity develops and shares the valuable information for different purposes (Needles

and Crosson 2013).

The management executives remain on the top hierarchy of the organisational

structure and they are observed to be engaged in using both financial and non-

financial information so that analysis about different business activities could be

made and accordingly, decisions could be undertaken. Hence, when sound business

information is crucial for the organisation, sound decision-making depends on the

accurate usage of effective and crucial decision-making coupled with the innovation

related to management information system.

As per the journal article, significant amount of emphasis is placed on the

innovation pertaining to the information system. There has to be innovation in the

creation of information and sharing system owing to the usage of financial as well as

non-financial information by the management. From the provided case of Apple Inc,

it could be observed that the management executives of the firm worked in

collaboration for identifying managerial issues so that accurate decisions could be

undertaken. It is possible to bring innovation in the creation and sharing process of

information owing to the sound interrelation among the executives, managers and

engineers. They have received considerable assistance in solving managerial

accounting issues in the most effective fashion (Nonala and Kenney 1991). For

example, the management of Apple used their information creation and analysis

system in order to undertake decision at the time of developing Apple Mac Book.

The management of Canon Inc has used its management information system

for undertaking sound business decisions. They have been observed to bring

innovation in the managerial level related to creation of information. The

management approach of Canon Inc is seen to move forward to the business

problems and thus, difference could be observed in the process of decision-making

with Apple Inc. They have attempted in resolving the problems when all managerial

executives are present along with the help of efficiency information system. The

utilisation of various conventional management processes could be observed by

undertaking management decisions. For instance, the utilisation of various

conventional managerial techniques could be witnessed by the management of

Canon Inc coupled with innovative processes of technological develop for producing

the mini copier.

By analysing the above aspects, it could be said that efficient and effective

application of the tools and techniques of managerial accounting help the firms in

enhancing their decision-making process for entire business success.

Requirement 2:

Both managerial accounting and management accounting technique are

continual business processes, which help in bringing innovation to the management

systems for undertaking sound business decisions. The provided article provided a

summary of innovation in the management system of an organisation in the form of

the process of development of innovation and sound sharing of information. This is a

significant proposition owing to the presence of many firms, in which the analysis

and usage of financial and non-financial information could be witnessed in the

processes of the management. Hence, it could be stated that the management of an

entity develops and shares the valuable information for different purposes (Needles

and Crosson 2013).

The management executives remain on the top hierarchy of the organisational

structure and they are observed to be engaged in using both financial and non-

financial information so that analysis about different business activities could be

made and accordingly, decisions could be undertaken. Hence, when sound business

information is crucial for the organisation, sound decision-making depends on the

accurate usage of effective and crucial decision-making coupled with the innovation

related to management information system.

As per the journal article, significant amount of emphasis is placed on the

innovation pertaining to the information system. There has to be innovation in the

creation of information and sharing system owing to the usage of financial as well as

non-financial information by the management. From the provided case of Apple Inc,

it could be observed that the management executives of the firm worked in

collaboration for identifying managerial issues so that accurate decisions could be

undertaken. It is possible to bring innovation in the creation and sharing process of

information owing to the sound interrelation among the executives, managers and

engineers. They have received considerable assistance in solving managerial

accounting issues in the most effective fashion (Nonala and Kenney 1991). For

example, the management of Apple used their information creation and analysis

system in order to undertake decision at the time of developing Apple Mac Book.

The management of Canon Inc has used its management information system

for undertaking sound business decisions. They have been observed to bring

innovation in the managerial level related to creation of information. The

management approach of Canon Inc is seen to move forward to the business

problems and thus, difference could be observed in the process of decision-making

with Apple Inc. They have attempted in resolving the problems when all managerial

executives are present along with the help of efficiency information system. The

utilisation of various conventional management processes could be observed by

undertaking management decisions. For instance, the utilisation of various

conventional managerial techniques could be witnessed by the management of

Canon Inc coupled with innovative processes of technological develop for producing

the mini copier.

8MANAGEMENT ACCOUNTING CASE STUDIES

Requirement 3:

One of the crucial backbones of any business is deemed to be the

management, since it helps in organising the crucial components for smooth

conduction of business operations. This is made through sound usage of the existing

resources in order to accomplish the entire business goals. In order to undertake

decisions for sound management of business resources, it is necessary to ensure

proper management functions. The perspective of sound decision-making is deemed

to be the major pillar for ensuring the success of the entity. When innovation is

present in products and services, the firms are assisted to compete with their rivals

in the increasingly competitive markets (Weygandt et al. 2018). One of the significant

parts of business entities includes the management, which always undertakes efforts

for accomplishing both short-term and long-term business aims and objectives.

The importance of information that the management information system

provides could not be ignored, as this is crucial to make sound business decisions.

The sound management of the entities immensely contribute to the success of the

decision-making technique of the firms in order to enable the firm in fulfilling its short-

term and long-term business objectives. The various kinds of managerial tools and

decision-making processes could be observed within the firms for solving different

types of business and managerial issues (Needles, Powers and Crosson 2013).

According to the journal article, it is possible to contrast the case studies of

the two firms, which include Canon Inc and Apple Inc. Both the firms are identified to

be operating in the technological sector. Owing to the continual technological

variations resulting in various kinds of innovation, the business entities are observed

to be entering the market with innovative services and products on all time; thereby,

intensifying the competition to a greater extent. For assuring survival in the market

along with ensuring business success, all organisations have to ensure the adoption

of activities, which would help them to bring new products in the market. Therefore,

competition analysis needs to be conducted by them for making decision in order to

combat with the tough challenge (Otley and Emmanuel 2013).

As a result, it is necessary to assure that information creation and sharing of

the same is present in the decision-making process of the firm. The innovation in the

creation process of information denotes the development of highly significant

financial as well as non-financial information for sound decision-making. Along with

this, the sharing system of information denotes the process of ensuring the

availability of all managerial information to the top level executives engaged in

undertaking decisions and implementation of decisions. The sharing system of

information comprises of the process of accumulating information from various

departments and segments of the companies in order to undertake sound

contribution towards the process of making decision (Songini, Gnan and Malmi

2013).

From the above discussion, it is not adequate for the entities to possess

management information system for undertaking decision until innovation is present

in the information creation processes and sharing of information efficiently. Hence,

with the help of enhanced and effective management information system, it becomes

possible for the organisations to undertake sound decisions.

Therefore, it could be stated that There is requirement for sound management

to combat with the market hurdles for maintaining superiority in the industry. In the

Requirement 3:

One of the crucial backbones of any business is deemed to be the

management, since it helps in organising the crucial components for smooth

conduction of business operations. This is made through sound usage of the existing

resources in order to accomplish the entire business goals. In order to undertake

decisions for sound management of business resources, it is necessary to ensure

proper management functions. The perspective of sound decision-making is deemed

to be the major pillar for ensuring the success of the entity. When innovation is

present in products and services, the firms are assisted to compete with their rivals

in the increasingly competitive markets (Weygandt et al. 2018). One of the significant

parts of business entities includes the management, which always undertakes efforts

for accomplishing both short-term and long-term business aims and objectives.

The importance of information that the management information system

provides could not be ignored, as this is crucial to make sound business decisions.

The sound management of the entities immensely contribute to the success of the

decision-making technique of the firms in order to enable the firm in fulfilling its short-

term and long-term business objectives. The various kinds of managerial tools and

decision-making processes could be observed within the firms for solving different

types of business and managerial issues (Needles, Powers and Crosson 2013).

According to the journal article, it is possible to contrast the case studies of

the two firms, which include Canon Inc and Apple Inc. Both the firms are identified to

be operating in the technological sector. Owing to the continual technological

variations resulting in various kinds of innovation, the business entities are observed

to be entering the market with innovative services and products on all time; thereby,

intensifying the competition to a greater extent. For assuring survival in the market

along with ensuring business success, all organisations have to ensure the adoption

of activities, which would help them to bring new products in the market. Therefore,

competition analysis needs to be conducted by them for making decision in order to

combat with the tough challenge (Otley and Emmanuel 2013).

As a result, it is necessary to assure that information creation and sharing of

the same is present in the decision-making process of the firm. The innovation in the

creation process of information denotes the development of highly significant

financial as well as non-financial information for sound decision-making. Along with

this, the sharing system of information denotes the process of ensuring the

availability of all managerial information to the top level executives engaged in

undertaking decisions and implementation of decisions. The sharing system of

information comprises of the process of accumulating information from various

departments and segments of the companies in order to undertake sound

contribution towards the process of making decision (Songini, Gnan and Malmi

2013).

From the above discussion, it is not adequate for the entities to possess

management information system for undertaking decision until innovation is present

in the information creation processes and sharing of information efficiently. Hence,

with the help of enhanced and effective management information system, it becomes

possible for the organisations to undertake sound decisions.

Therefore, it could be stated that There is requirement for sound management

to combat with the market hurdles for maintaining superiority in the industry. In the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING CASE STUDIES

provided journal, it could be seen that the method of creation of information and

sharing have been provided significant emphasis due to the need of managerial

accounting. In the provided case of Canon, the firm is observed to carry out

feasibility study by including staffs working in different departments. The product was

new to be launched in the market, which is a mini-copier. The policy was to

undertake sound decision when the top executive team of each department is

present. The hard work of Steve Jobs is known to all along with the success

achieved by the individual. However, the major reason for the business success is

sound and effective management. As stated in the article, the management team of

Apple is highly efficient and continual interaction was maintained by them for

increasing the strength of the management. The application of sound tools of

management accounting as well as techniques related to the same have assisted

the firm to exploit the market opportunities for increasing the innovativeness of

products along with ensuring cost effectiveness. In addition, it could be observed that

the organisations have been working in combination with their executives, managers

and engineers to ensure full harmonisation for developing innovative products in

collaboration with the respective sectors.

provided journal, it could be seen that the method of creation of information and

sharing have been provided significant emphasis due to the need of managerial

accounting. In the provided case of Canon, the firm is observed to carry out

feasibility study by including staffs working in different departments. The product was

new to be launched in the market, which is a mini-copier. The policy was to

undertake sound decision when the top executive team of each department is

present. The hard work of Steve Jobs is known to all along with the success

achieved by the individual. However, the major reason for the business success is

sound and effective management. As stated in the article, the management team of

Apple is highly efficient and continual interaction was maintained by them for

increasing the strength of the management. The application of sound tools of

management accounting as well as techniques related to the same have assisted

the firm to exploit the market opportunities for increasing the innovativeness of

products along with ensuring cost effectiveness. In addition, it could be observed that

the organisations have been working in combination with their executives, managers

and engineers to ensure full harmonisation for developing innovative products in

collaboration with the respective sectors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING CASE STUDIES

References:

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and

medium-sized enterprises: current knowledge and avenues for further

research. Journal of Management Accounting Research, 27(1), pp.81-119.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and

firm performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), pp.414-428.

Krstevski, D. and Mancheski, G., 2016. Managerial accounting: Modeling customer

lifetime value-An application in the telecommunication industry. European Journal of

Business and Social Sciences, 5(01), pp.64-77.

Mihăilă, M., 2014. Managerial accounting and decision making, in energy

industry. Procedia-Social and Behavioral Sciences, 109, pp.1199-1202.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI

Learning Pvt. Ltd..

Needles, B. and Crosson, S., 2013. Managerial accounting. Cengage Learning.

Needles, B.E., Powers, M. and Crosson, S.V., 2013. Financial and managerial

accounting. Nelson Education.

Nonala, I. and Kenney, M., 1991. Towards a new theory of innovation management:

A case study comparing Canon, Inc. and Apple Computer, Inc. Journal of

Engineering and Technology Management, 8(1), pp.67-83.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management

control. Springer.

Songini, L., Gnan, L. and Malmi, T., 2013. The role and impact of accounting in

family business. Journal of Family Business Strategy, 4(2), pp.71-83.

Warren, C., Reeve, J.M. and Duchac, J., 2013. Financial & managerial accounting.

Cengage Learning.

Weygandt, J.J., Kieso, D.E., Kimmel, P.D. and Aly, I.M., 2018. Managerial

Accounting: Tools for Business Decision-making. John Wiley & Sons Canada,

Limited.

References:

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and

medium-sized enterprises: current knowledge and avenues for further

research. Journal of Management Accounting Research, 27(1), pp.81-119.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and

firm performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), pp.414-428.

Krstevski, D. and Mancheski, G., 2016. Managerial accounting: Modeling customer

lifetime value-An application in the telecommunication industry. European Journal of

Business and Social Sciences, 5(01), pp.64-77.

Mihăilă, M., 2014. Managerial accounting and decision making, in energy

industry. Procedia-Social and Behavioral Sciences, 109, pp.1199-1202.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI

Learning Pvt. Ltd..

Needles, B. and Crosson, S., 2013. Managerial accounting. Cengage Learning.

Needles, B.E., Powers, M. and Crosson, S.V., 2013. Financial and managerial

accounting. Nelson Education.

Nonala, I. and Kenney, M., 1991. Towards a new theory of innovation management:

A case study comparing Canon, Inc. and Apple Computer, Inc. Journal of

Engineering and Technology Management, 8(1), pp.67-83.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management

control. Springer.

Songini, L., Gnan, L. and Malmi, T., 2013. The role and impact of accounting in

family business. Journal of Family Business Strategy, 4(2), pp.71-83.

Warren, C., Reeve, J.M. and Duchac, J., 2013. Financial & managerial accounting.

Cengage Learning.

Weygandt, J.J., Kieso, D.E., Kimmel, P.D. and Aly, I.M., 2018. Managerial

Accounting: Tools for Business Decision-making. John Wiley & Sons Canada,

Limited.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.