ABC Ltd: Management Accounting Report and Analysis

VerifiedAdded on 2023/01/11

|15

|3754

|46

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within a business context, specifically using ABC Limited as a case study. It explores the core principles of management accounting, emphasizing its role in internal decision-making and organizational improvement. The report delves into various management accounting systems, including cost accounting, inventory management, job costing, and price optimization, highlighting their benefits and uses. Furthermore, it examines different types of management accounting reports, such as budget reports, performance reports, cost accounting reports, and accounts receivable reports, and their significance in planning, decision-making, and performance evaluation. The report also includes a practical application of costing methods, comparing and contrasting absorption and marginal costing through income statement preparation. Additionally, it analyzes planning tools, evaluating their advantages and disadvantages. Finally, it addresses how management accounting systems can respond to financial problems and offers recommendations for achieving sustainable business practices.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

LO1..................................................................................................................................................3

Explaining MA with its principles and role of it’s within the organization................................3

Stating different types of the MA reports....................................................................................5

Determining benefits and uses of MA systems...........................................................................7

Evaluating the way in which MA systems and reporting is integrated.......................................8

LO2..................................................................................................................................................8

Preparing income statement by making use of absorption and marginal costing methods.........8

TASK 2..........................................................................................................................................11

Compare and contrast planning tools with advantages and disadvantages of each planning tool.

...................................................................................................................................................11

Management accounting system to respond financial problems...............................................12

Conclusion and recommendation to company for applying method for achieve sustainable

business......................................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

TASK 1............................................................................................................................................3

LO1..................................................................................................................................................3

Explaining MA with its principles and role of it’s within the organization................................3

Stating different types of the MA reports....................................................................................5

Determining benefits and uses of MA systems...........................................................................7

Evaluating the way in which MA systems and reporting is integrated.......................................8

LO2..................................................................................................................................................8

Preparing income statement by making use of absorption and marginal costing methods.........8

TASK 2..........................................................................................................................................11

Compare and contrast planning tools with advantages and disadvantages of each planning tool.

...................................................................................................................................................11

Management accounting system to respond financial problems...............................................12

Conclusion and recommendation to company for applying method for achieve sustainable

business......................................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is concerned with the process of providing financial information

and resources to the managers for the purpose of better decision making in the context of

business. The main objective of management accounting is to improve the internal working of

the firm so that it can earn more profitability and achieve its goals and objectives in an effective

and efficient manner. This tool has helped the company in taking better decisions with regards to

proper controlling of business activities and development. The current study will focus on ABC

limited and the role of management accounting in the smooth functioning of the company’s

operations. Furthermore, it will also include a brief study on the management accounting tool

and its role in the business growth and its sustainability.

TASK 1

LO1.

Explaining MA with its principles and role of it’s within the organization

Principles of MA

Management accounting involves the presentation of analysis of business activities to the

internal management to promote better decision making. It is different from financial accounting

because financial accounting is concerned with preparation of financial statements for the

external parties whereas management accounting is done for the sake of internal purpose and to

improve the working of the organization.

MA systems

The systems associated with management accounting are as follows:

Cost accounting system- Cost accounting system is a framework used by the companies

to predict the cost of their products and services so that the firm can assess its profitability, value

the inventory and cost control (Ghasemi and et.al., 2016). The main objective of cost accounting

is to identify the cost of manufacturing a single product or service so that later on the firm can

add profit margin systematically. The importance of cost accounting is that it has help businesses

Management accounting is concerned with the process of providing financial information

and resources to the managers for the purpose of better decision making in the context of

business. The main objective of management accounting is to improve the internal working of

the firm so that it can earn more profitability and achieve its goals and objectives in an effective

and efficient manner. This tool has helped the company in taking better decisions with regards to

proper controlling of business activities and development. The current study will focus on ABC

limited and the role of management accounting in the smooth functioning of the company’s

operations. Furthermore, it will also include a brief study on the management accounting tool

and its role in the business growth and its sustainability.

TASK 1

LO1.

Explaining MA with its principles and role of it’s within the organization

Principles of MA

Management accounting involves the presentation of analysis of business activities to the

internal management to promote better decision making. It is different from financial accounting

because financial accounting is concerned with preparation of financial statements for the

external parties whereas management accounting is done for the sake of internal purpose and to

improve the working of the organization.

MA systems

The systems associated with management accounting are as follows:

Cost accounting system- Cost accounting system is a framework used by the companies

to predict the cost of their products and services so that the firm can assess its profitability, value

the inventory and cost control (Ghasemi and et.al., 2016). The main objective of cost accounting

is to identify the cost of manufacturing a single product or service so that later on the firm can

add profit margin systematically. The importance of cost accounting is that it has help businesses

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in lowering their cost of operations by eliminating irrelevant items which has ultimately led

towards the profit maximization.

Inventory management system- Inventory management system is a tool used by the

companies to monitor and control the stocked products like company assets, raw materials, or

finished products ready to be delivered to the customers. It is imperative for every manufacturing

company to have an inventory management system to keep record of the company’s resources

like increased transparency, improved delivery services and efficiency. Also, the company can

increase its inventory turnover by optimizing the value of goods and services by keeping fewer

items in hand and earning profitability. The most important use of this system is that it provides

better consumer satisfaction by providing faster shipping and delivery which helps in building

strong relationship with them.

Job costing system- Job costing is a system designed for the purpose of ascertaining and

accumulating manufacturing costs of a single unit or output. The job costing system is mainly

used when there are various items produced that differ from each other and have a significant

cost. This system serves as the subsidiary ledger for the producer’s work in progress inventory

and the finished goods inventory (Shevelev, Sheveleva and Gvozdev, 2017). The major benefit

of this system is that it helps the business managers in calculating profits on single jobs and

whether these are profitable enough to pursue in the near future. It is mainly used by construction

companies, consultants and contractors.

Price optimization system- Price optimization system is a tool of management accounting

that is used by the companies to forecast demand of their products & services at different price

levels and then combine the data relating to costs and inventory levels which further helps in

suggesting certain prices that can improve the profits. The system works on three elements like

pricing strategy, value of product for both buyer and seller and managing the elements of

profitability (Taylor and Scapens, 2016). It is of great importance because it provides financial

benefits like opportunities to increase the sales and consumer base through adequate optimization

of price which further can help in the growth and profitability of an enterprise.

towards the profit maximization.

Inventory management system- Inventory management system is a tool used by the

companies to monitor and control the stocked products like company assets, raw materials, or

finished products ready to be delivered to the customers. It is imperative for every manufacturing

company to have an inventory management system to keep record of the company’s resources

like increased transparency, improved delivery services and efficiency. Also, the company can

increase its inventory turnover by optimizing the value of goods and services by keeping fewer

items in hand and earning profitability. The most important use of this system is that it provides

better consumer satisfaction by providing faster shipping and delivery which helps in building

strong relationship with them.

Job costing system- Job costing is a system designed for the purpose of ascertaining and

accumulating manufacturing costs of a single unit or output. The job costing system is mainly

used when there are various items produced that differ from each other and have a significant

cost. This system serves as the subsidiary ledger for the producer’s work in progress inventory

and the finished goods inventory (Shevelev, Sheveleva and Gvozdev, 2017). The major benefit

of this system is that it helps the business managers in calculating profits on single jobs and

whether these are profitable enough to pursue in the near future. It is mainly used by construction

companies, consultants and contractors.

Price optimization system- Price optimization system is a tool of management accounting

that is used by the companies to forecast demand of their products & services at different price

levels and then combine the data relating to costs and inventory levels which further helps in

suggesting certain prices that can improve the profits. The system works on three elements like

pricing strategy, value of product for both buyer and seller and managing the elements of

profitability (Taylor and Scapens, 2016). It is of great importance because it provides financial

benefits like opportunities to increase the sales and consumer base through adequate optimization

of price which further can help in the growth and profitability of an enterprise.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stating different types of the MA reports

MA reports are mainly used for planning, decision making, regulating and in measuring

the performance. Such reports are been constantly generated throughout an accounting period

and helps in making crucial decisions depending on authenticity of such reports. Managers assess

such reports for highlighting certain patterns and thereafter converting it into the useful

information for the firm.

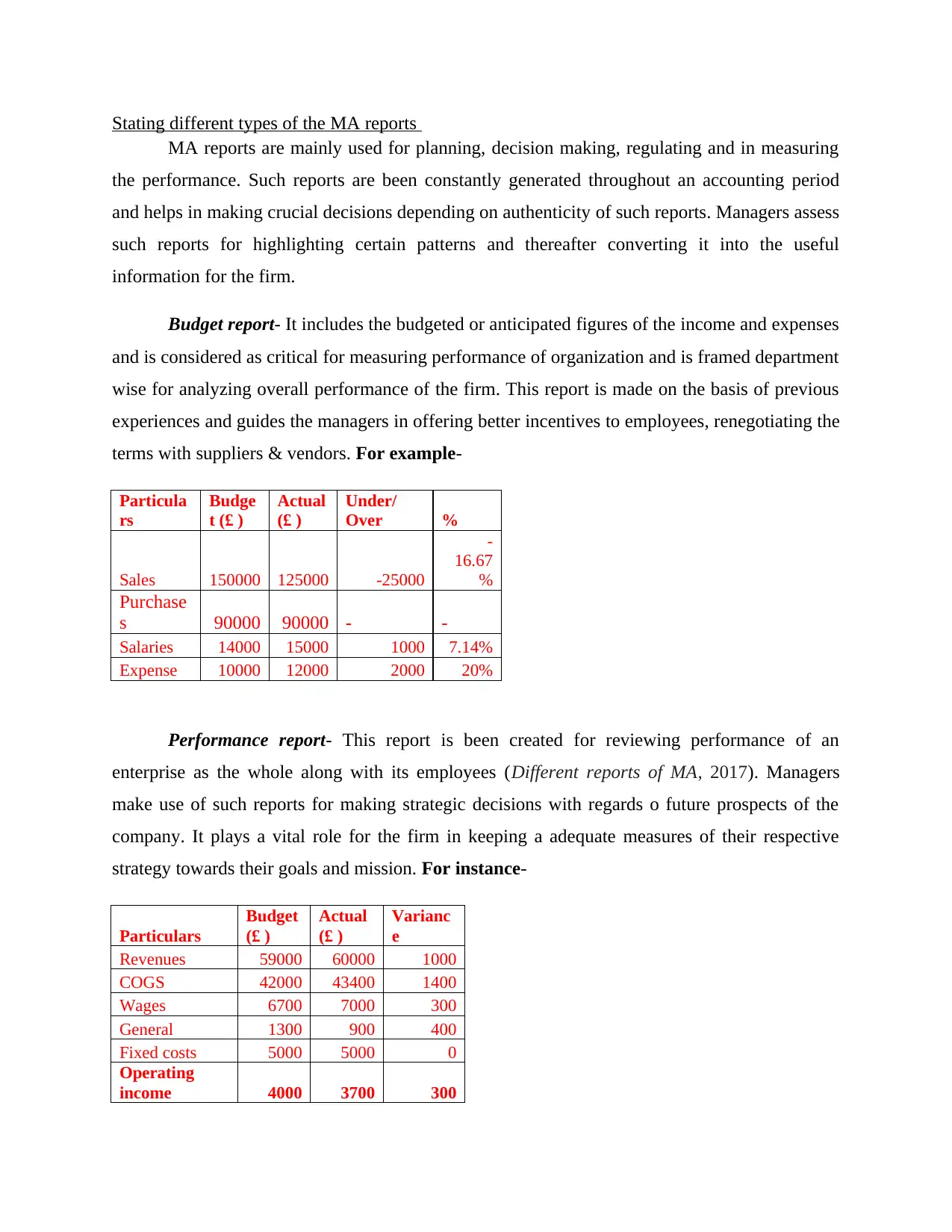

Budget report- It includes the budgeted or anticipated figures of the income and expenses

and is considered as critical for measuring performance of organization and is framed department

wise for analyzing overall performance of the firm. This report is made on the basis of previous

experiences and guides the managers in offering better incentives to employees, renegotiating the

terms with suppliers & vendors. For example-

Particula

rs

Budge

t (£ )

Actual

(£ )

Under/

Over %

Sales 150000 125000 -25000

-

16.67

%

Purchase

s 90000 90000 - -

Salaries 14000 15000 1000 7.14%

Expense 10000 12000 2000 20%

Performance report- This report is been created for reviewing performance of an

enterprise as the whole along with its employees (Different reports of MA, 2017). Managers

make use of such reports for making strategic decisions with regards o future prospects of the

company. It plays a vital role for the firm in keeping a adequate measures of their respective

strategy towards their goals and mission. For instance-

Particulars

Budget

(£ )

Actual

(£ )

Varianc

e

Revenues 59000 60000 1000

COGS 42000 43400 1400

Wages 6700 7000 300

General 1300 900 400

Fixed costs 5000 5000 0

Operating

income 4000 3700 300

MA reports are mainly used for planning, decision making, regulating and in measuring

the performance. Such reports are been constantly generated throughout an accounting period

and helps in making crucial decisions depending on authenticity of such reports. Managers assess

such reports for highlighting certain patterns and thereafter converting it into the useful

information for the firm.

Budget report- It includes the budgeted or anticipated figures of the income and expenses

and is considered as critical for measuring performance of organization and is framed department

wise for analyzing overall performance of the firm. This report is made on the basis of previous

experiences and guides the managers in offering better incentives to employees, renegotiating the

terms with suppliers & vendors. For example-

Particula

rs

Budge

t (£ )

Actual

(£ )

Under/

Over %

Sales 150000 125000 -25000

-

16.67

%

Purchase

s 90000 90000 - -

Salaries 14000 15000 1000 7.14%

Expense 10000 12000 2000 20%

Performance report- This report is been created for reviewing performance of an

enterprise as the whole along with its employees (Different reports of MA, 2017). Managers

make use of such reports for making strategic decisions with regards o future prospects of the

company. It plays a vital role for the firm in keeping a adequate measures of their respective

strategy towards their goals and mission. For instance-

Particulars

Budget

(£ )

Actual

(£ )

Varianc

e

Revenues 59000 60000 1000

COGS 42000 43400 1400

Wages 6700 7000 300

General 1300 900 400

Fixed costs 5000 5000 0

Operating

income 4000 3700 300

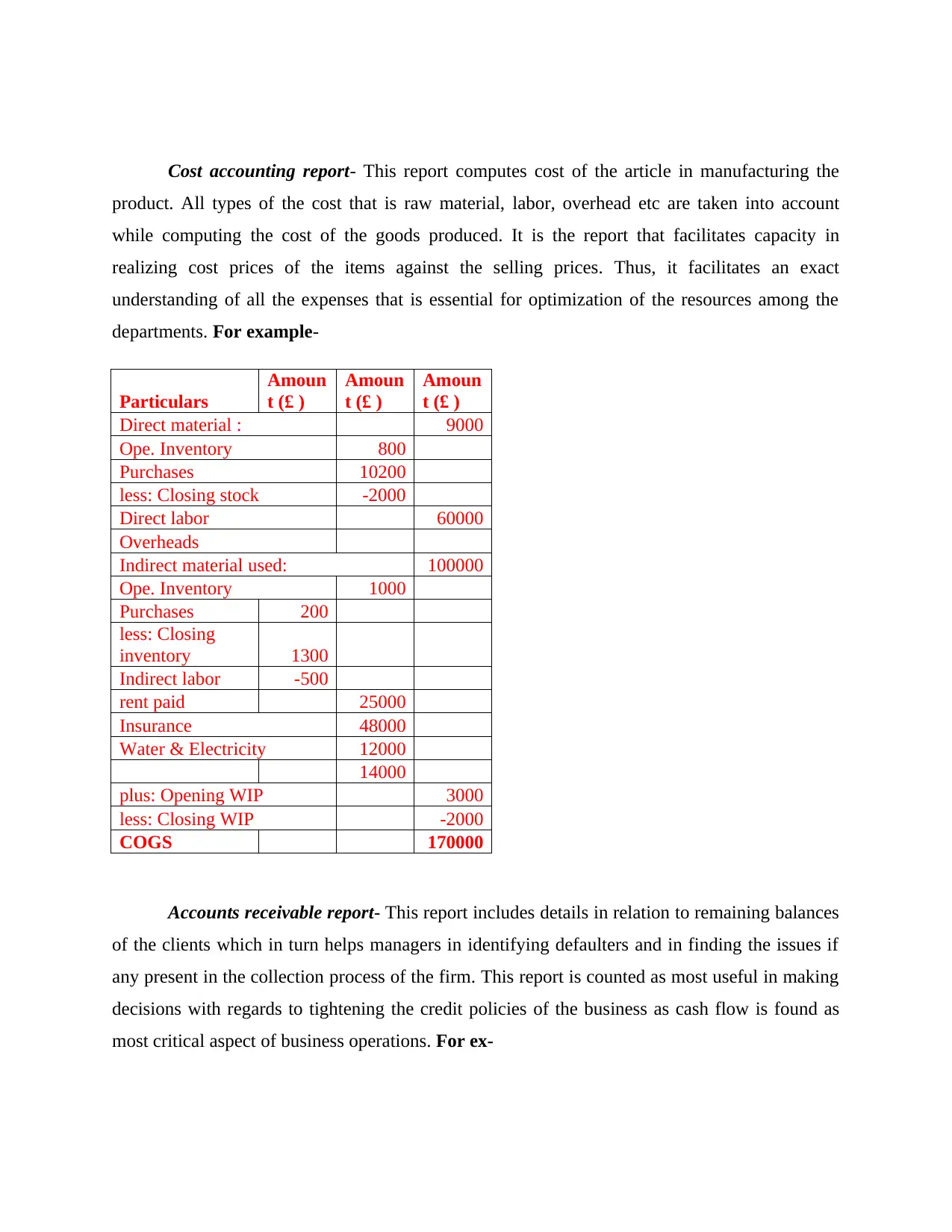

Cost accounting report- This report computes cost of the article in manufacturing the

product. All types of the cost that is raw material, labor, overhead etc are taken into account

while computing the cost of the goods produced. It is the report that facilitates capacity in

realizing cost prices of the items against the selling prices. Thus, it facilitates an exact

understanding of all the expenses that is essential for optimization of the resources among the

departments. For example-

Particulars

Amoun

t (£ )

Amoun

t (£ )

Amoun

t (£ )

Direct material : 9000

Ope. Inventory 800

Purchases 10200

less: Closing stock -2000

Direct labor 60000

Overheads

Indirect material used: 100000

Ope. Inventory 1000

Purchases 200

less: Closing

inventory 1300

Indirect labor -500

rent paid 25000

Insurance 48000

Water & Electricity 12000

14000

plus: Opening WIP 3000

less: Closing WIP -2000

COGS 170000

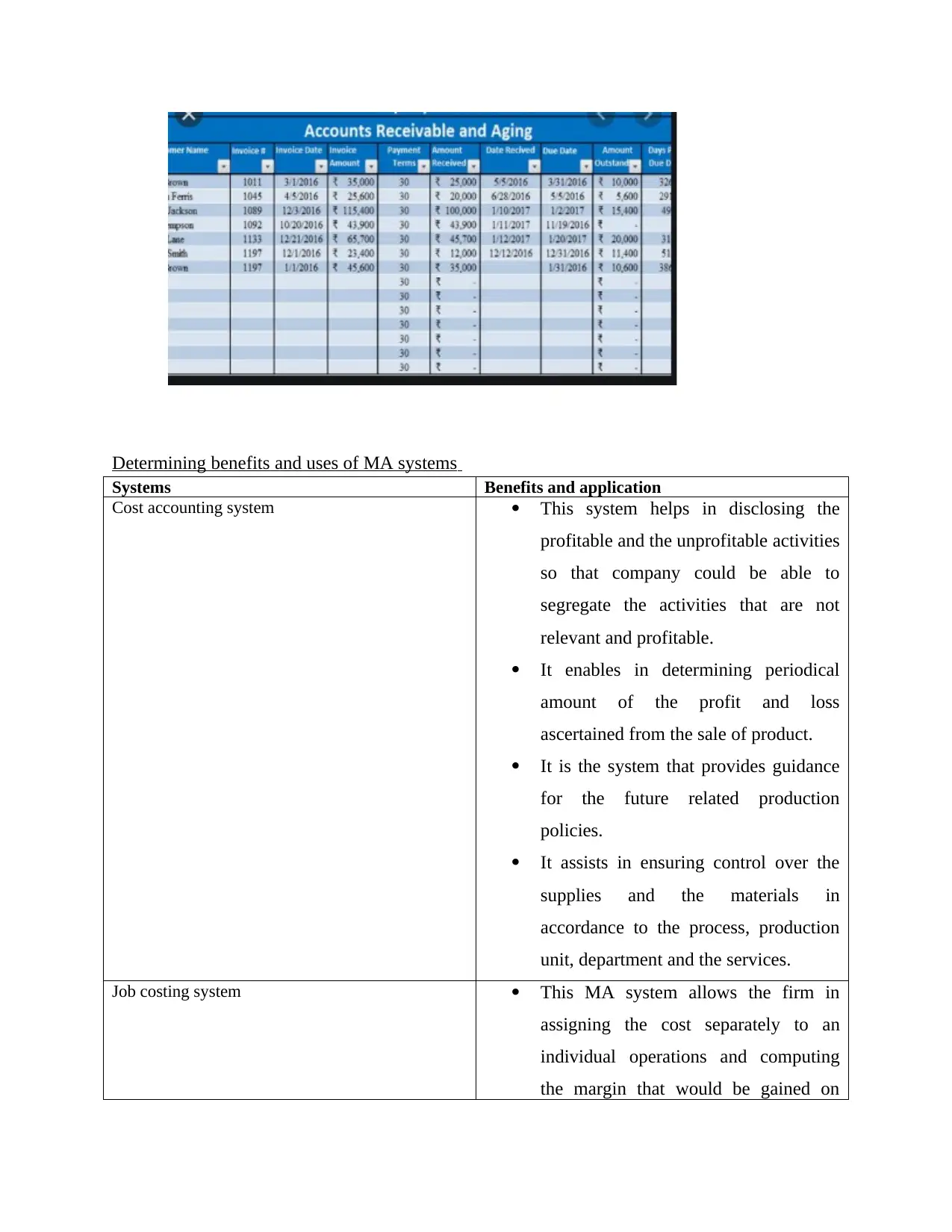

Accounts receivable report- This report includes details in relation to remaining balances

of the clients which in turn helps managers in identifying defaulters and in finding the issues if

any present in the collection process of the firm. This report is counted as most useful in making

decisions with regards to tightening the credit policies of the business as cash flow is found as

most critical aspect of business operations. For ex-

product. All types of the cost that is raw material, labor, overhead etc are taken into account

while computing the cost of the goods produced. It is the report that facilitates capacity in

realizing cost prices of the items against the selling prices. Thus, it facilitates an exact

understanding of all the expenses that is essential for optimization of the resources among the

departments. For example-

Particulars

Amoun

t (£ )

Amoun

t (£ )

Amoun

t (£ )

Direct material : 9000

Ope. Inventory 800

Purchases 10200

less: Closing stock -2000

Direct labor 60000

Overheads

Indirect material used: 100000

Ope. Inventory 1000

Purchases 200

less: Closing

inventory 1300

Indirect labor -500

rent paid 25000

Insurance 48000

Water & Electricity 12000

14000

plus: Opening WIP 3000

less: Closing WIP -2000

COGS 170000

Accounts receivable report- This report includes details in relation to remaining balances

of the clients which in turn helps managers in identifying defaulters and in finding the issues if

any present in the collection process of the firm. This report is counted as most useful in making

decisions with regards to tightening the credit policies of the business as cash flow is found as

most critical aspect of business operations. For ex-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Determining benefits and uses of MA systems

Systems Benefits and application

Cost accounting system This system helps in disclosing the

profitable and the unprofitable activities

so that company could be able to

segregate the activities that are not

relevant and profitable.

It enables in determining periodical

amount of the profit and loss

ascertained from the sale of product.

It is the system that provides guidance

for the future related production

policies.

It assists in ensuring control over the

supplies and the materials in

accordance to the process, production

unit, department and the services.

Job costing system This MA system allows the firm in

assigning the cost separately to an

individual operations and computing

the margin that would be gained on

Systems Benefits and application

Cost accounting system This system helps in disclosing the

profitable and the unprofitable activities

so that company could be able to

segregate the activities that are not

relevant and profitable.

It enables in determining periodical

amount of the profit and loss

ascertained from the sale of product.

It is the system that provides guidance

for the future related production

policies.

It assists in ensuring control over the

supplies and the materials in

accordance to the process, production

unit, department and the services.

Job costing system This MA system allows the firm in

assigning the cost separately to an

individual operations and computing

the margin that would be gained on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

each of the job.

It enables in assessing performance of

employees and also helps in identifying

employees who fails in meeting the

performance expectations.

It is the system that provides an access

to expenses that incurred on job even at

the time of manufacturing or

production process.

Inventory management system It helps in avoiding the problem of

stock outs and excess level of the stock

and tracks or manages the flow of

inventory optimally within the

business.

This system provides for invaluable

sales information that allows for more

of the data-driven decisions of

business.

This system saves greater amount of the

cost by eliminating an inventory cost

attached with the human error.

Through this system, company can

trace its product in a better and could

access the valuable data that in turn

allows or leads to potential or improved

negotiations with the suppliers.

Price optimization system It is the MA system that facilitates

consistency to the businesses in

providing a relevant and the optimized

data insights by reducing the possible

chances of errors.

It enables in assessing performance of

employees and also helps in identifying

employees who fails in meeting the

performance expectations.

It is the system that provides an access

to expenses that incurred on job even at

the time of manufacturing or

production process.

Inventory management system It helps in avoiding the problem of

stock outs and excess level of the stock

and tracks or manages the flow of

inventory optimally within the

business.

This system provides for invaluable

sales information that allows for more

of the data-driven decisions of

business.

This system saves greater amount of the

cost by eliminating an inventory cost

attached with the human error.

Through this system, company can

trace its product in a better and could

access the valuable data that in turn

allows or leads to potential or improved

negotiations with the suppliers.

Price optimization system It is the MA system that facilitates

consistency to the businesses in

providing a relevant and the optimized

data insights by reducing the possible

chances of errors.

It helps the company in analyzing and

emphasizing on the key or important

areas like sales margin and no. of

conversions.

Evaluating the way in which MA systems and reporting is integrated

MA is been integrated in each level of an enterprise as all types of the information that

relates to the company are included in it. MA is counted as very useful tool for an entity because

it affects the decision making of an enterprise which results organization success. Thus, there

present a direct link between MA and success or growth of an entity as enables in increasing

efficiency in the functioning of management and allows to fix appropriate target and the prices of

products.

LO2.

Preparing income statement by making use of absorption and marginal costing methods

Absorption costing- It means the method that is used for valuing an inventory which

includes all types of cost incurred in manufacturing the product that is fixed and the variable

costs (Ciuhureanu, 2018). It provides a more comprehensive and the accurate view on the cost

incurred for producing an inventory or the product.

Marginal costing- It means the costing method where marginal cost that is the variable

cost is been charged towards unit of the cost however fixed cost for a period is been completely

written off over contribution.

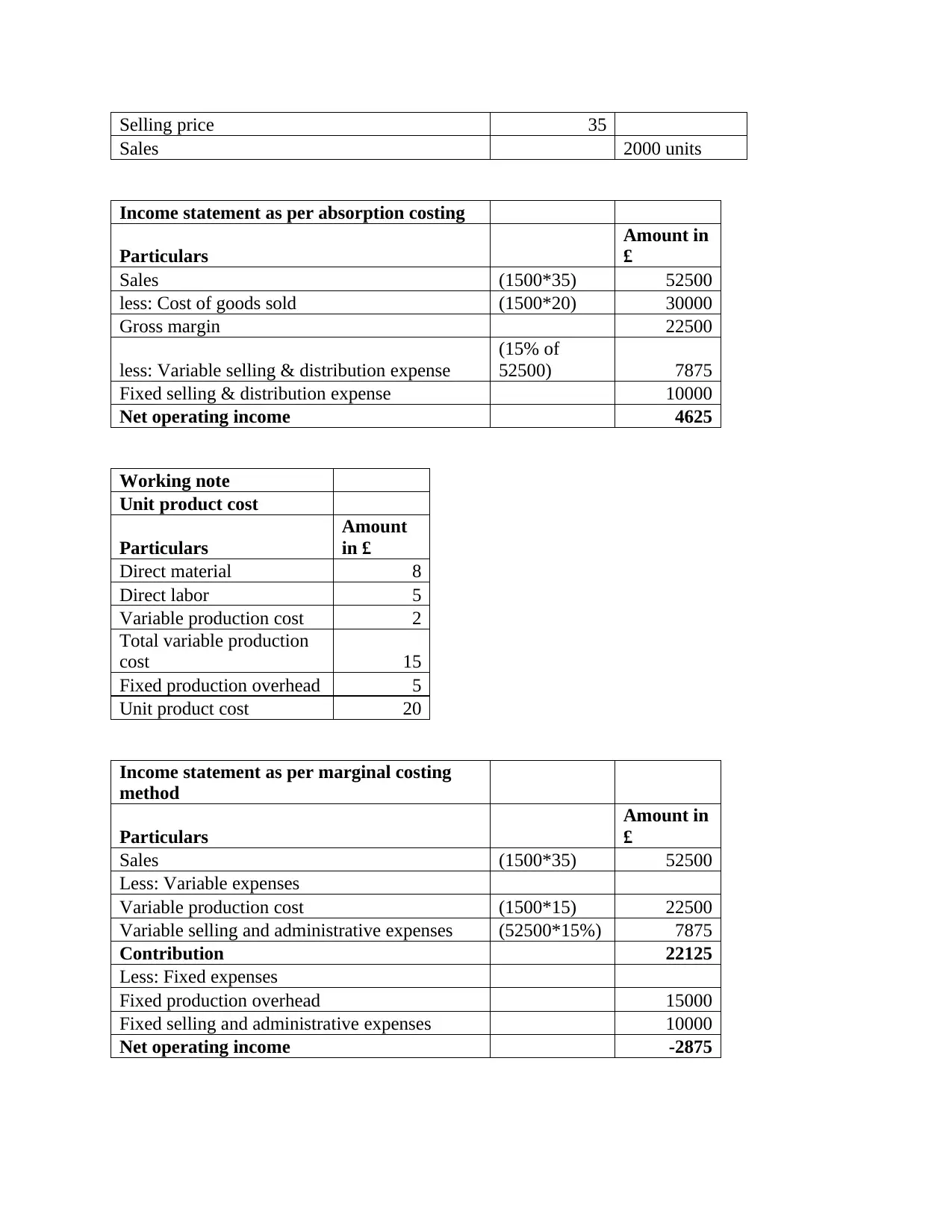

Particulars

Cost per unit

(£)

Direct material 8

Direct labor 5

Variable production cost 2

Fixed production overhead 5

Fixed production overhead incurred actually £15000

Fixed selling & distribution expense

£10000 per

month

Variable selling & distribution expense

15% of sales

value

emphasizing on the key or important

areas like sales margin and no. of

conversions.

Evaluating the way in which MA systems and reporting is integrated

MA is been integrated in each level of an enterprise as all types of the information that

relates to the company are included in it. MA is counted as very useful tool for an entity because

it affects the decision making of an enterprise which results organization success. Thus, there

present a direct link between MA and success or growth of an entity as enables in increasing

efficiency in the functioning of management and allows to fix appropriate target and the prices of

products.

LO2.

Preparing income statement by making use of absorption and marginal costing methods

Absorption costing- It means the method that is used for valuing an inventory which

includes all types of cost incurred in manufacturing the product that is fixed and the variable

costs (Ciuhureanu, 2018). It provides a more comprehensive and the accurate view on the cost

incurred for producing an inventory or the product.

Marginal costing- It means the costing method where marginal cost that is the variable

cost is been charged towards unit of the cost however fixed cost for a period is been completely

written off over contribution.

Particulars

Cost per unit

(£)

Direct material 8

Direct labor 5

Variable production cost 2

Fixed production overhead 5

Fixed production overhead incurred actually £15000

Fixed selling & distribution expense

£10000 per

month

Variable selling & distribution expense

15% of sales

value

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Selling price 35

Sales 2000 units

Income statement as per absorption costing

Particulars

Amount in

£

Sales (1500*35) 52500

less: Cost of goods sold (1500*20) 30000

Gross margin 22500

less: Variable selling & distribution expense

(15% of

52500) 7875

Fixed selling & distribution expense 10000

Net operating income 4625

Working note

Unit product cost

Particulars

Amount

in £

Direct material 8

Direct labor 5

Variable production cost 2

Total variable production

cost 15

Fixed production overhead 5

Unit product cost 20

Income statement as per marginal costing

method

Particulars

Amount in

£

Sales (1500*35) 52500

Less: Variable expenses

Variable production cost (1500*15) 22500

Variable selling and administrative expenses (52500*15%) 7875

Contribution 22125

Less: Fixed expenses

Fixed production overhead 15000

Fixed selling and administrative expenses 10000

Net operating income -2875

Sales 2000 units

Income statement as per absorption costing

Particulars

Amount in

£

Sales (1500*35) 52500

less: Cost of goods sold (1500*20) 30000

Gross margin 22500

less: Variable selling & distribution expense

(15% of

52500) 7875

Fixed selling & distribution expense 10000

Net operating income 4625

Working note

Unit product cost

Particulars

Amount

in £

Direct material 8

Direct labor 5

Variable production cost 2

Total variable production

cost 15

Fixed production overhead 5

Unit product cost 20

Income statement as per marginal costing

method

Particulars

Amount in

£

Sales (1500*35) 52500

Less: Variable expenses

Variable production cost (1500*15) 22500

Variable selling and administrative expenses (52500*15%) 7875

Contribution 22125

Less: Fixed expenses

Fixed production overhead 15000

Fixed selling and administrative expenses 10000

Net operating income -2875

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

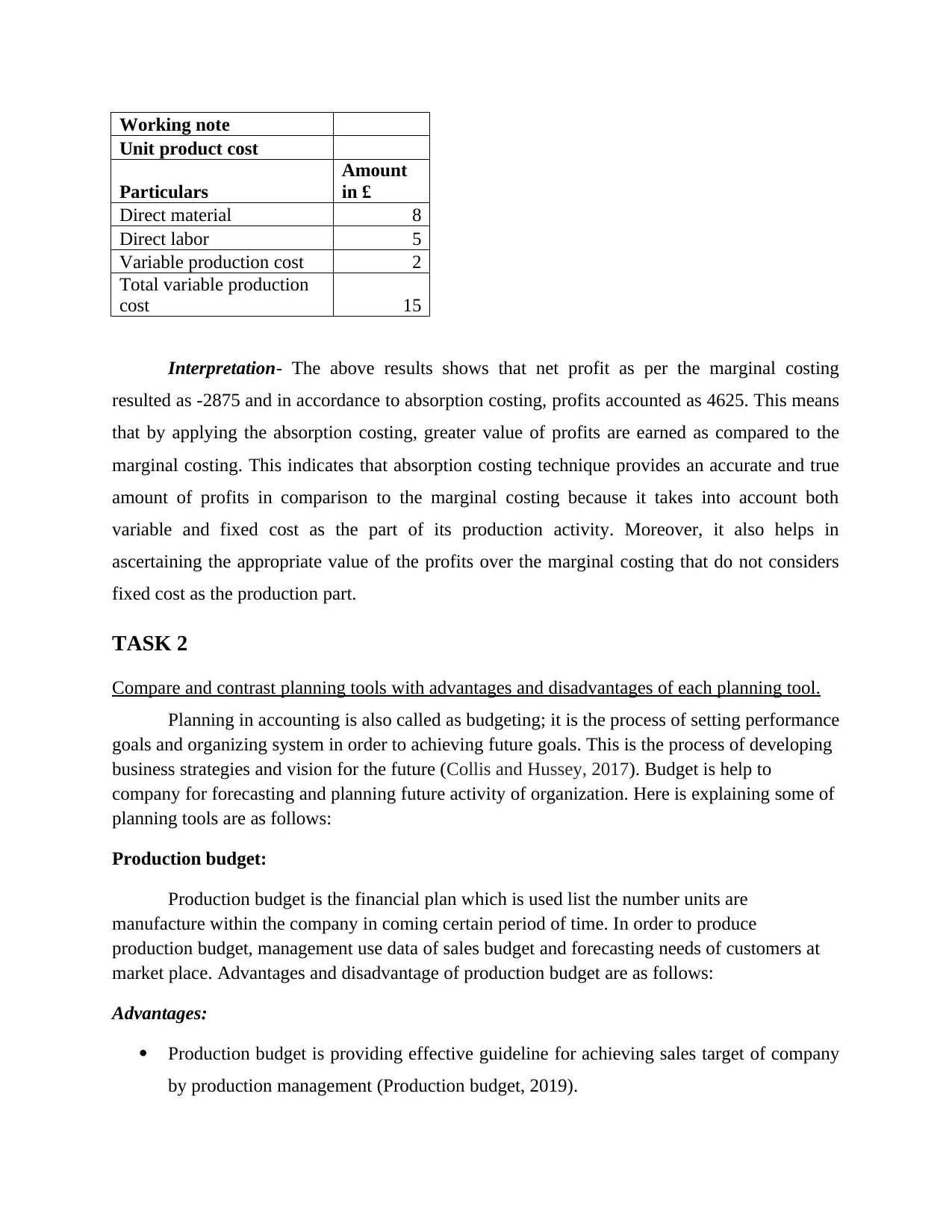

Working note

Unit product cost

Particulars

Amount

in £

Direct material 8

Direct labor 5

Variable production cost 2

Total variable production

cost 15

Interpretation- The above results shows that net profit as per the marginal costing

resulted as -2875 and in accordance to absorption costing, profits accounted as 4625. This means

that by applying the absorption costing, greater value of profits are earned as compared to the

marginal costing. This indicates that absorption costing technique provides an accurate and true

amount of profits in comparison to the marginal costing because it takes into account both

variable and fixed cost as the part of its production activity. Moreover, it also helps in

ascertaining the appropriate value of the profits over the marginal costing that do not considers

fixed cost as the production part.

TASK 2

Compare and contrast planning tools with advantages and disadvantages of each planning tool.

Planning in accounting is also called as budgeting; it is the process of setting performance

goals and organizing system in order to achieving future goals. This is the process of developing

business strategies and vision for the future (Collis and Hussey, 2017). Budget is help to

company for forecasting and planning future activity of organization. Here is explaining some of

planning tools are as follows:

Production budget:

Production budget is the financial plan which is used list the number units are

manufacture within the company in coming certain period of time. In order to produce

production budget, management use data of sales budget and forecasting needs of customers at

market place. Advantages and disadvantage of production budget are as follows:

Advantages:

Production budget is providing effective guideline for achieving sales target of company

by production management (Production budget, 2019).

Unit product cost

Particulars

Amount

in £

Direct material 8

Direct labor 5

Variable production cost 2

Total variable production

cost 15

Interpretation- The above results shows that net profit as per the marginal costing

resulted as -2875 and in accordance to absorption costing, profits accounted as 4625. This means

that by applying the absorption costing, greater value of profits are earned as compared to the

marginal costing. This indicates that absorption costing technique provides an accurate and true

amount of profits in comparison to the marginal costing because it takes into account both

variable and fixed cost as the part of its production activity. Moreover, it also helps in

ascertaining the appropriate value of the profits over the marginal costing that do not considers

fixed cost as the production part.

TASK 2

Compare and contrast planning tools with advantages and disadvantages of each planning tool.

Planning in accounting is also called as budgeting; it is the process of setting performance

goals and organizing system in order to achieving future goals. This is the process of developing

business strategies and vision for the future (Collis and Hussey, 2017). Budget is help to

company for forecasting and planning future activity of organization. Here is explaining some of

planning tools are as follows:

Production budget:

Production budget is the financial plan which is used list the number units are

manufacture within the company in coming certain period of time. In order to produce

production budget, management use data of sales budget and forecasting needs of customers at

market place. Advantages and disadvantage of production budget are as follows:

Advantages:

Production budget is providing effective guideline for achieving sales target of company

by production management (Production budget, 2019).

With the help of this budget company is able to maintain balance between inventory and

sales production of company.

Disadvantages:

Budget preparation is helpful for company it is take lots of time and efforts of

management.

Each person of management have own style to complete task, in this it is possible that all

employees not able to accept production budget prepared by management.

In the case of small plastic parts Ltd. Company is manufacture plastic parts. Management is

preparing production budget for the next quarter. As per production budget company estimate

that can sell higher units in last quarter. With this, management estimate to produce more items

as compare with sale of last quarter.

Zero base budgeting:

Zero base budgeting is also method of budgeting in this includes all the expenses which

justified for the each new time. This budgeting is started with zero level because every company

have need to analyse their cost and needs (Fleischman and McLean, 2020). There are various

advantages and disadvantages of zero base budgeting are as follows:

Advantages:

This budgeting is based on the decision making process as well as ignoring previous year

data for preparing budget.

Zero base budgeting have aim for analysing benefit of cost that is not make focus on

studying changes in expenses.

Disadvantages:

In this budget have a range of employee; take more time for making and turning delay in

result as well.

In this having chances of some fraud entries in which personal expenses include in this

budgeting.

In respect of Small plastic parts Ltd. Company, is prepare budget by taking better decision in

order to lead provide better communication between departments, employees and managers.

Management accounting system to respond financial problems.

Management of company is managing accounts of company as well as financial problems

which are generating within the organization (Hopper and Bui, 2016). The small plastic parts

sales production of company.

Disadvantages:

Budget preparation is helpful for company it is take lots of time and efforts of

management.

Each person of management have own style to complete task, in this it is possible that all

employees not able to accept production budget prepared by management.

In the case of small plastic parts Ltd. Company is manufacture plastic parts. Management is

preparing production budget for the next quarter. As per production budget company estimate

that can sell higher units in last quarter. With this, management estimate to produce more items

as compare with sale of last quarter.

Zero base budgeting:

Zero base budgeting is also method of budgeting in this includes all the expenses which

justified for the each new time. This budgeting is started with zero level because every company

have need to analyse their cost and needs (Fleischman and McLean, 2020). There are various

advantages and disadvantages of zero base budgeting are as follows:

Advantages:

This budgeting is based on the decision making process as well as ignoring previous year

data for preparing budget.

Zero base budgeting have aim for analysing benefit of cost that is not make focus on

studying changes in expenses.

Disadvantages:

In this budget have a range of employee; take more time for making and turning delay in

result as well.

In this having chances of some fraud entries in which personal expenses include in this

budgeting.

In respect of Small plastic parts Ltd. Company, is prepare budget by taking better decision in

order to lead provide better communication between departments, employees and managers.

Management accounting system to respond financial problems.

Management of company is managing accounts of company as well as financial problems

which are generating within the organization (Hopper and Bui, 2016). The small plastic parts

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.