Management Accounting Report: MAS, Costing, and Financial Statements

VerifiedAdded on 2023/01/19

|21

|5494

|49

Report

AI Summary

This management accounting report provides a comprehensive overview of the subject, focusing on the role of management accounting (MA) in business entities. The report examines various Management Accounting Systems (MAS) such as price optimization, inventory management, cost accounting, and job costing systems, illustrating their benefits and integration within organizational processes. It also explores different types of MA reports, including accounts receivable aging reports, stock reports, performance reports, and budget reports. Furthermore, the report delves into the preparation of income statements under absorption and marginal costing methods, providing detailed profit and loss statements for the London Clothing Works (Sel Ltd) for three months. The report concludes by evaluating how MAS and MA reports are integrated within the organizational processes of the company.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................7

TASK 3 .........................................................................................................................................12

TASK 4..........................................................................................................................................13

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

APPENDIX....................................................................................................................................18

...............................................................................................................................18

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................7

TASK 3 .........................................................................................................................................12

TASK 4..........................................................................................................................................13

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

APPENDIX....................................................................................................................................18

...............................................................................................................................18

INTRODUCTION

The term management accounting (MA) is a type of accounting that is associated with

process of collection of monetary and non monetary data of business entities in order to produce

internal managerial reports (Al-Qady and El-Helbawy, 2016). In this accounting, each aspect and

element of companies are covered in a detailed manner so that management department can take

suitable steps in an effective manner. The main objective of project report is to understanding

about MA and its role for businesses. For better understanding, a manufacturing company has

been chosen that is The London Clothing Works (Sel Ltd). The company is located in London,

United Kingdom and operates in production of vital range of cloths.

The project report covers about different types of management accounting systems

(MAS), vital range of MA reports as well as budgets. In addition, financial statements are also

prepared on the basis of monetary data on assumption basis. Further part of project report covers

about role of MAS in sorting monetary issues.

MAIN BODY

TASK 1

MA and its role of business entities.

Management accounting- As above stated, the term MA is an accounting that involves in a

systematic procedure of collection of detailed information regards to various kinds of business

transactions (Wnuk-Pel, 2016). The objective of gathering this detailed information about

quantitative and qualitatitive aspects is to produce internal reports that help to managers in taking

crucial decisions in different situations. This accounting plays a significant role for companies

that are as follows:

Helps in effective planning- This accounting plays an important role in the context of

making effective planning of different types of available resources. It becomes possible

because on the basis of gathered information, managers can analyse futuristic activities

that helps in better planning. Such as in the above London Clothing Works (Sel Ltd),

their managers of different departments make effective planning by produced internal

reports as accordance of this accounting.

The term management accounting (MA) is a type of accounting that is associated with

process of collection of monetary and non monetary data of business entities in order to produce

internal managerial reports (Al-Qady and El-Helbawy, 2016). In this accounting, each aspect and

element of companies are covered in a detailed manner so that management department can take

suitable steps in an effective manner. The main objective of project report is to understanding

about MA and its role for businesses. For better understanding, a manufacturing company has

been chosen that is The London Clothing Works (Sel Ltd). The company is located in London,

United Kingdom and operates in production of vital range of cloths.

The project report covers about different types of management accounting systems

(MAS), vital range of MA reports as well as budgets. In addition, financial statements are also

prepared on the basis of monetary data on assumption basis. Further part of project report covers

about role of MAS in sorting monetary issues.

MAIN BODY

TASK 1

MA and its role of business entities.

Management accounting- As above stated, the term MA is an accounting that involves in a

systematic procedure of collection of detailed information regards to various kinds of business

transactions (Wnuk-Pel, 2016). The objective of gathering this detailed information about

quantitative and qualitatitive aspects is to produce internal reports that help to managers in taking

crucial decisions in different situations. This accounting plays a significant role for companies

that are as follows:

Helps in effective planning- This accounting plays an important role in the context of

making effective planning of different types of available resources. It becomes possible

because on the basis of gathered information, managers can analyse futuristic activities

that helps in better planning. Such as in the above London Clothing Works (Sel Ltd),

their managers of different departments make effective planning by produced internal

reports as accordance of this accounting.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Helps in better controlling- In addition, MA is beneficial for companies in order to make

better control over different kinds of activities and operations. This is so because by

utilising key information from internal reports, managers become able to focus on those

activities that are leading lower profit or higher costs. Same as in the above London

Clothing Works (Sel Ltd), their managers control different aspects in an a better way by

help of this accounting.

Helps in better decision making- Another benefit of this accounting is that it is useful for

better decision making (Akroyd, Biswas and Chuang, 2016). Such as in the above

London Clothing Works (Sel Ltd) company, managers take corrective actions and

decisions by help of this accounting.

Types of MAS:

Price optimisation system- It is an accounting system that is aligned in a systematic

process of guiding companies for applying corrective pricing strategies. This becomes

possibel because under it, a proper research is done about customers' need, wants and

demand. On the basis of it, business entities become aware about what types of changes

are needed to be done in current pricing patterns. Thus, this accounting system is useful

for companies in order to set the prices at a level that can help in increasing total sales

revenues. Such as in the aspect of above London Clothing Works (Sel Ltd) company,

their sales department is using this accounting system in order to revise price of products

at a level that can help in increasing sales units.

Inventory management system- This can be defined as an accounting system that is

assigned in the tasks of keeping track record of all types of inventories that is purchased

or sold out by companies. The objective of this accounting system is to make possible

that effective utilisation of stored material is being done by business entities. In addition,

it is essential for companies in order to keep the cost of material below estimation. This

accounting system manage all types of activitis and operations regards to inventory

management on the basis of effective technique of inventory valuation such as LIFO,

FIFO and weighted average method. In the London Clothing Works (Sel Ltd) company,

their production department make effective management of raw material like cotton, fiber

etc. in an effective manner by help of this accounting.

better control over different kinds of activities and operations. This is so because by

utilising key information from internal reports, managers become able to focus on those

activities that are leading lower profit or higher costs. Same as in the above London

Clothing Works (Sel Ltd), their managers control different aspects in an a better way by

help of this accounting.

Helps in better decision making- Another benefit of this accounting is that it is useful for

better decision making (Akroyd, Biswas and Chuang, 2016). Such as in the above

London Clothing Works (Sel Ltd) company, managers take corrective actions and

decisions by help of this accounting.

Types of MAS:

Price optimisation system- It is an accounting system that is aligned in a systematic

process of guiding companies for applying corrective pricing strategies. This becomes

possibel because under it, a proper research is done about customers' need, wants and

demand. On the basis of it, business entities become aware about what types of changes

are needed to be done in current pricing patterns. Thus, this accounting system is useful

for companies in order to set the prices at a level that can help in increasing total sales

revenues. Such as in the aspect of above London Clothing Works (Sel Ltd) company,

their sales department is using this accounting system in order to revise price of products

at a level that can help in increasing sales units.

Inventory management system- This can be defined as an accounting system that is

assigned in the tasks of keeping track record of all types of inventories that is purchased

or sold out by companies. The objective of this accounting system is to make possible

that effective utilisation of stored material is being done by business entities. In addition,

it is essential for companies in order to keep the cost of material below estimation. This

accounting system manage all types of activitis and operations regards to inventory

management on the basis of effective technique of inventory valuation such as LIFO,

FIFO and weighted average method. In the London Clothing Works (Sel Ltd) company,

their production department make effective management of raw material like cotton, fiber

etc. in an effective manner by help of this accounting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost accounting system- It is an accounting system which is responsible for accurate

prediction and controlling of overall cost of various kinds of activities and operations

(van, Caperchione and Caruana, 2016). Under this accounting system, detailed record of

estimated cost and actual cost is included that helps to managers of companies in order to

keep cost lower of different operations. In the aspect of above London Clothing Works

(Sel Ltd) company, their finance department manage cost of various kinds of operations

and activities regards to productions by help of this accounting.

Job costing system- This is an accounting system that is related with assigning cost of

each particular unit by help of computing total job cost. It is mostly applied by those

buiness entities wherein wide range of products are produced. This is so because by help

of this accounting, the production department become aware about which products cost is

below expected cost and which ones is not. Like the above London Clothing Works (Sel

Ltd) company, is involved in production of different types of cloths and help of this

accounting their production department assess the cost of each individual unit of

produced cloth.

Difference between management accounting and financial accounting:

Basis Management accounting Financial accounting

Purpose The key purpose of this accounting is

to do effective management of

internal perspectives.

While this accounting's objective is to

produce financial statements at the end

of accounting period.

Information Under this accounting both monetary

and non monetary information is

included.

On the other hand, in this accounting

only financial information is included.

Necessary This is not necessary to implement it

in each year.

While this is necessary to apply this

accounting for companies.

prediction and controlling of overall cost of various kinds of activities and operations

(van, Caperchione and Caruana, 2016). Under this accounting system, detailed record of

estimated cost and actual cost is included that helps to managers of companies in order to

keep cost lower of different operations. In the aspect of above London Clothing Works

(Sel Ltd) company, their finance department manage cost of various kinds of operations

and activities regards to productions by help of this accounting.

Job costing system- This is an accounting system that is related with assigning cost of

each particular unit by help of computing total job cost. It is mostly applied by those

buiness entities wherein wide range of products are produced. This is so because by help

of this accounting, the production department become aware about which products cost is

below expected cost and which ones is not. Like the above London Clothing Works (Sel

Ltd) company, is involved in production of different types of cloths and help of this

accounting their production department assess the cost of each individual unit of

produced cloth.

Difference between management accounting and financial accounting:

Basis Management accounting Financial accounting

Purpose The key purpose of this accounting is

to do effective management of

internal perspectives.

While this accounting's objective is to

produce financial statements at the end

of accounting period.

Information Under this accounting both monetary

and non monetary information is

included.

On the other hand, in this accounting

only financial information is included.

Necessary This is not necessary to implement it

in each year.

While this is necessary to apply this

accounting for companies.

MA reports- These are kinds of reports that consists information about monetary transactions of

specific time period. The MA reports are useful for business entities in order to take corrective

steps for managing available resources. The above accountant of above London Clothing Works

(Sel Ltd) company produce below mentioned reports that are as follows:

Accounts receivable ageing report- This a kinds of report that consists information about

total debtors whose payment is not received even after the due date (Phan, Baird, 2017).

The report keeps systematic record about date on which transaction is done, total debt

amount as well as interest rates. By help of this report, managers can easily access

information about total debt amount which is required to collect. Such as in the above

London Clothing Works (Sel Ltd) company, their finance department collects debt

amount from their customers in less time period and cost. Due to this their receivable turn

over ratio also improves.

Stock report- It is a report, that contains information regards to quantity of all forms of

inventories such as raw material, work in progress and finished goods. Under this report,

information is included on the basis of proper valuation of inventories as accordance of

LIFO, FIFO and weighted average methods. It is beneficial for business entities in order

to control overall cost of storage. For example in the above London Clothing Works (Sel

Ltd) company, their production department utilise key information about raw material

and finished goods by help of this report.

Performance report- This is a type of report that includes information regards to

estimated and actual outcome of different kinds of activities and operations. On the basis

of it, managers of companies take suitable action regards to improving overall

performance. In the aspect of promotion of employees, information provided by this

report plays a significant role. This is so because managers assess each individual

employees performance so that their progress can be assured. In the context of above

business London Clothing Works (Sel Ltd), their employees are promoted to upper level

on the basis of key information utilising through this report.

Budget report- It is a report that includes information regards to estimated revenues and

expenses as well as actual outcome (Yigitbasioglu, 2017). Due to this, variance is

calculated of different activities that helps in taking corrective actions for futuristic time

specific time period. The MA reports are useful for business entities in order to take corrective

steps for managing available resources. The above accountant of above London Clothing Works

(Sel Ltd) company produce below mentioned reports that are as follows:

Accounts receivable ageing report- This a kinds of report that consists information about

total debtors whose payment is not received even after the due date (Phan, Baird, 2017).

The report keeps systematic record about date on which transaction is done, total debt

amount as well as interest rates. By help of this report, managers can easily access

information about total debt amount which is required to collect. Such as in the above

London Clothing Works (Sel Ltd) company, their finance department collects debt

amount from their customers in less time period and cost. Due to this their receivable turn

over ratio also improves.

Stock report- It is a report, that contains information regards to quantity of all forms of

inventories such as raw material, work in progress and finished goods. Under this report,

information is included on the basis of proper valuation of inventories as accordance of

LIFO, FIFO and weighted average methods. It is beneficial for business entities in order

to control overall cost of storage. For example in the above London Clothing Works (Sel

Ltd) company, their production department utilise key information about raw material

and finished goods by help of this report.

Performance report- This is a type of report that includes information regards to

estimated and actual outcome of different kinds of activities and operations. On the basis

of it, managers of companies take suitable action regards to improving overall

performance. In the aspect of promotion of employees, information provided by this

report plays a significant role. This is so because managers assess each individual

employees performance so that their progress can be assured. In the context of above

business London Clothing Works (Sel Ltd), their employees are promoted to upper level

on the basis of key information utilising through this report.

Budget report- It is a report that includes information regards to estimated revenues and

expenses as well as actual outcome (Yigitbasioglu, 2017). Due to this, variance is

calculated of different activities that helps in taking corrective actions for futuristic time

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

period. In the aspect of above London Clothing Works (Sel Ltd) company, their

accountant produce this report with an objective of managing their financial outcomes.

As well as for better utilisation of available financial and non financial resources.

Benefits of MAS:

MAS Benefits

Price optimisation

system

This accounting system is associated with process of revising and

setting the prices at a level that can help in increasing total sales

revenues. In the aspect of London Clothing Works (Sel Ltd), their

sales managers set the price of cloths by help of this accounting.

Inventory management

system

It is linked with proper management of stored inventories in an

effective manner. In the London Clothing Works (Sel Ltd) company,

their manufacturing department implement this accounting system in

order to make better utilisation of available inventories.

Cost accounting system This accounting system is related with proper management of cost and

expenses of various kinds of activities and operations. Such as in the

above business entity, their finance department analyse key

information through this accounting system and manage overall cost

of different operations and activities.

Job costing system It is linked with process of assigning cost of job in order to calculate

cost of each individual produced output. In the aspect of above

London Clothing Works (Sel Ltd) company, their managers

implement this accounting system in order to get information regards

to cost of each produced clothing item.

Evaluation about how MAS and MA reports are integrated within organisational process.

In the MA, vital range of accounting systems and reports are included that helps in order

to effective internal management of various kinds of aspects (Talbot and Boiral, 2018). For

example in the London Clothing Works (Sel Ltd) company, they are using different types of

accounting systems such as price optimisation system, cost accounting system etc. each of these

accountant produce this report with an objective of managing their financial outcomes.

As well as for better utilisation of available financial and non financial resources.

Benefits of MAS:

MAS Benefits

Price optimisation

system

This accounting system is associated with process of revising and

setting the prices at a level that can help in increasing total sales

revenues. In the aspect of London Clothing Works (Sel Ltd), their

sales managers set the price of cloths by help of this accounting.

Inventory management

system

It is linked with proper management of stored inventories in an

effective manner. In the London Clothing Works (Sel Ltd) company,

their manufacturing department implement this accounting system in

order to make better utilisation of available inventories.

Cost accounting system This accounting system is related with proper management of cost and

expenses of various kinds of activities and operations. Such as in the

above business entity, their finance department analyse key

information through this accounting system and manage overall cost

of different operations and activities.

Job costing system It is linked with process of assigning cost of job in order to calculate

cost of each individual produced output. In the aspect of above

London Clothing Works (Sel Ltd) company, their managers

implement this accounting system in order to get information regards

to cost of each produced clothing item.

Evaluation about how MAS and MA reports are integrated within organisational process.

In the MA, vital range of accounting systems and reports are included that helps in order

to effective internal management of various kinds of aspects (Talbot and Boiral, 2018). For

example in the London Clothing Works (Sel Ltd) company, they are using different types of

accounting systems such as price optimisation system, cost accounting system etc. each of these

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

system alignes with different departments. Like price optimisation system is integrated with sales

department as well as cost accounting system with finance department.

Along with the MA reports are also integrated within prcoess of above company. This is

so because accounts receivable report is linked with finance report and performance report with

human resource department. It indicates that MAS and MA reports are integrated within

organisational process of above London Clothing Works (Sel Ltd) company.

TASK 2

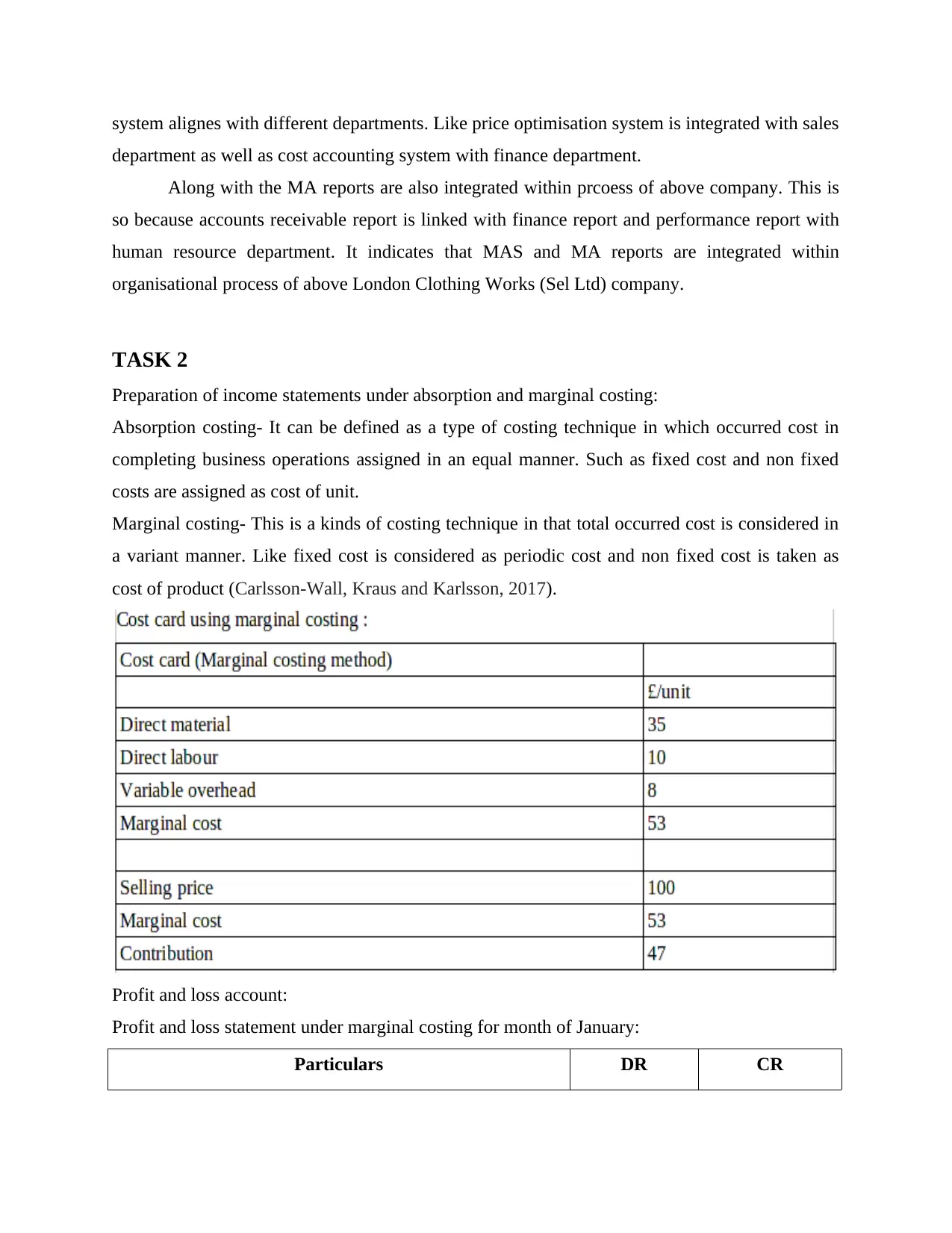

Preparation of income statements under absorption and marginal costing:

Absorption costing- It can be defined as a type of costing technique in which occurred cost in

completing business operations assigned in an equal manner. Such as fixed cost and non fixed

costs are assigned as cost of unit.

Marginal costing- This is a kinds of costing technique in that total occurred cost is considered in

a variant manner. Like fixed cost is considered as periodic cost and non fixed cost is taken as

cost of product (Carlsson-Wall, Kraus and Karlsson, 2017).

Profit and loss account:

Profit and loss statement under marginal costing for month of January:

Particulars DR CR

department as well as cost accounting system with finance department.

Along with the MA reports are also integrated within prcoess of above company. This is

so because accounts receivable report is linked with finance report and performance report with

human resource department. It indicates that MAS and MA reports are integrated within

organisational process of above London Clothing Works (Sel Ltd) company.

TASK 2

Preparation of income statements under absorption and marginal costing:

Absorption costing- It can be defined as a type of costing technique in which occurred cost in

completing business operations assigned in an equal manner. Such as fixed cost and non fixed

costs are assigned as cost of unit.

Marginal costing- This is a kinds of costing technique in that total occurred cost is considered in

a variant manner. Like fixed cost is considered as periodic cost and non fixed cost is taken as

cost of product (Carlsson-Wall, Kraus and Karlsson, 2017).

Profit and loss account:

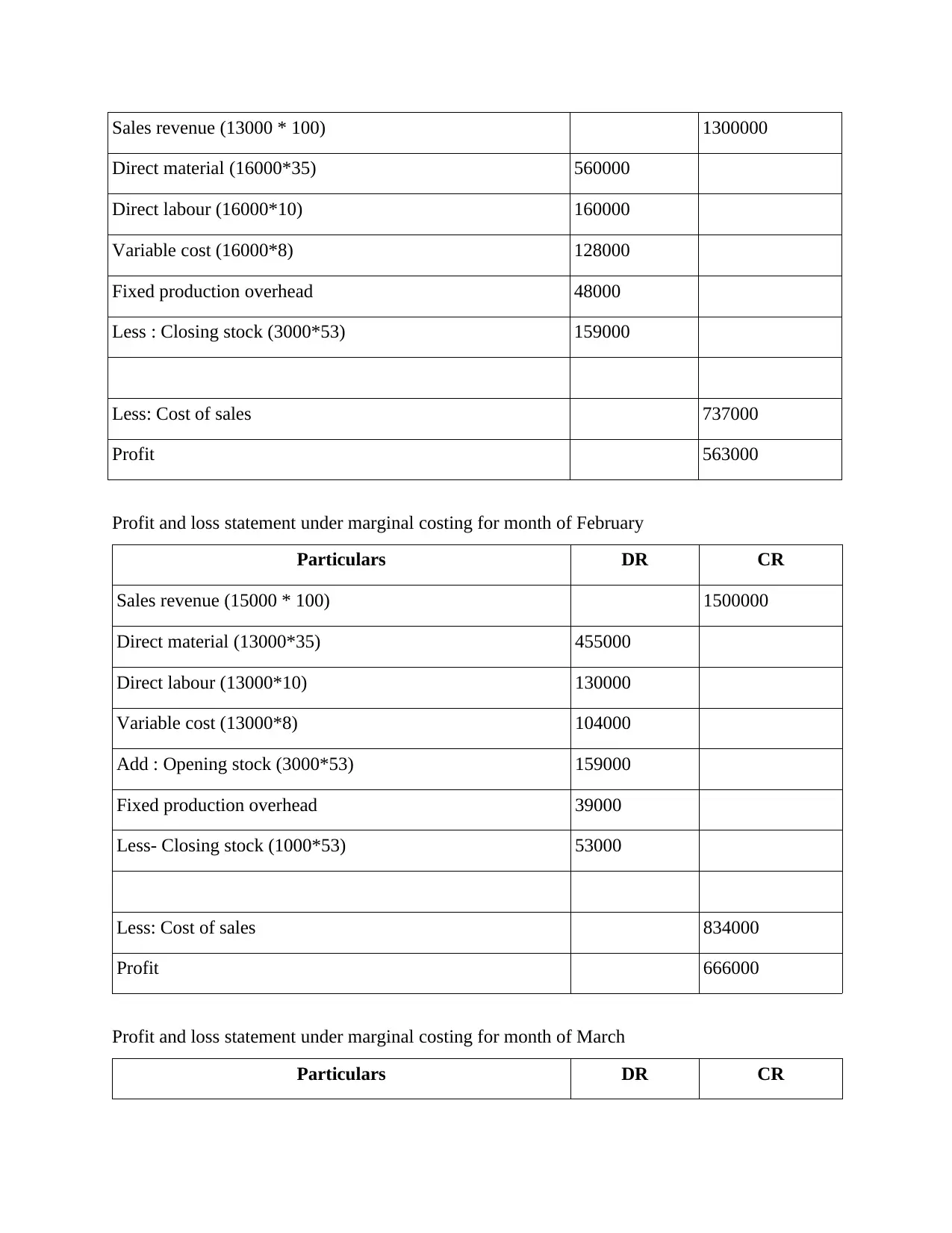

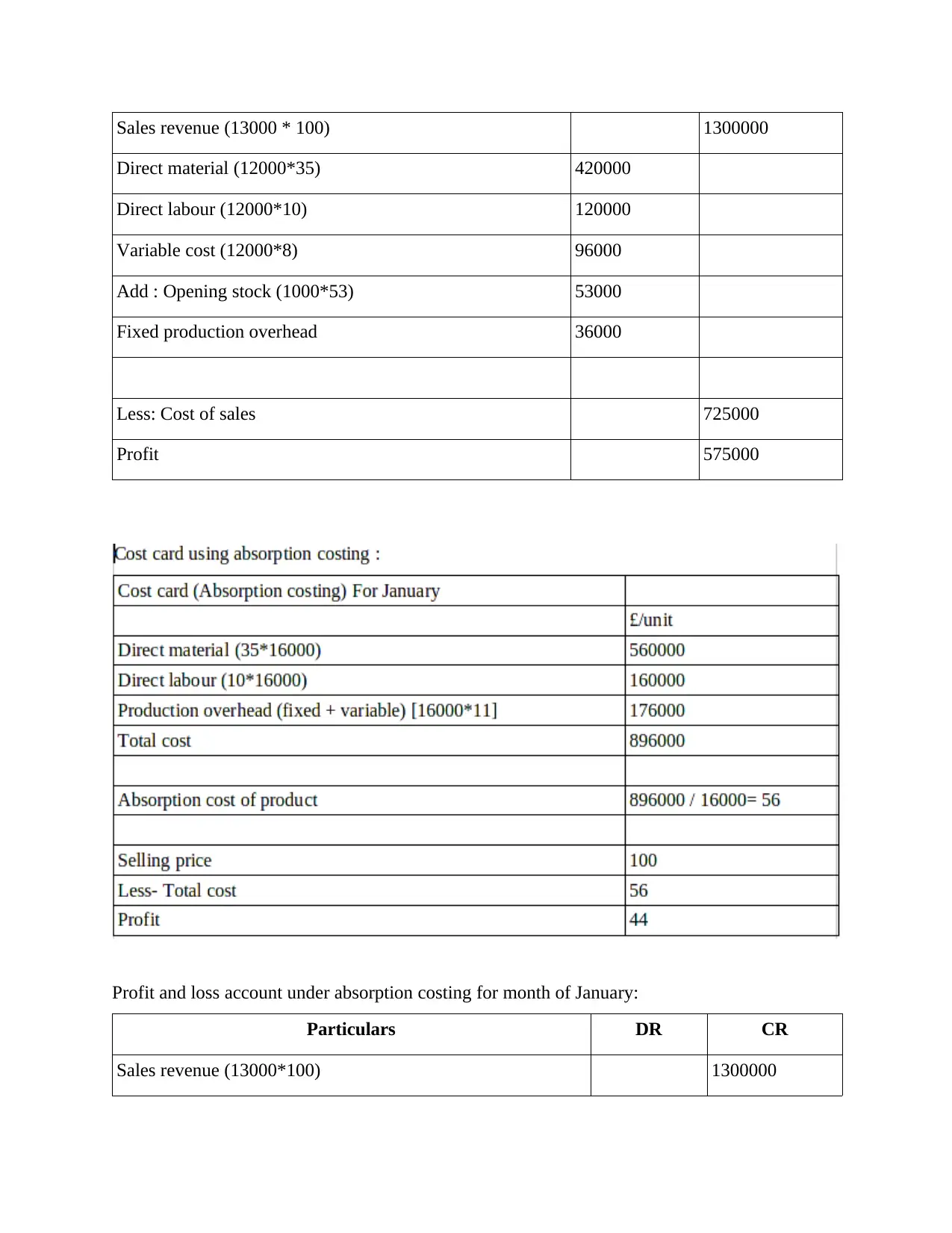

Profit and loss statement under marginal costing for month of January:

Particulars DR CR

Sales revenue (13000 * 100) 1300000

Direct material (16000*35) 560000

Direct labour (16000*10) 160000

Variable cost (16000*8) 128000

Fixed production overhead 48000

Less : Closing stock (3000*53) 159000

Less: Cost of sales 737000

Profit 563000

Profit and loss statement under marginal costing for month of February

Particulars DR CR

Sales revenue (15000 * 100) 1500000

Direct material (13000*35) 455000

Direct labour (13000*10) 130000

Variable cost (13000*8) 104000

Add : Opening stock (3000*53) 159000

Fixed production overhead 39000

Less- Closing stock (1000*53) 53000

Less: Cost of sales 834000

Profit 666000

Profit and loss statement under marginal costing for month of March

Particulars DR CR

Direct material (16000*35) 560000

Direct labour (16000*10) 160000

Variable cost (16000*8) 128000

Fixed production overhead 48000

Less : Closing stock (3000*53) 159000

Less: Cost of sales 737000

Profit 563000

Profit and loss statement under marginal costing for month of February

Particulars DR CR

Sales revenue (15000 * 100) 1500000

Direct material (13000*35) 455000

Direct labour (13000*10) 130000

Variable cost (13000*8) 104000

Add : Opening stock (3000*53) 159000

Fixed production overhead 39000

Less- Closing stock (1000*53) 53000

Less: Cost of sales 834000

Profit 666000

Profit and loss statement under marginal costing for month of March

Particulars DR CR

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales revenue (13000 * 100) 1300000

Direct material (12000*35) 420000

Direct labour (12000*10) 120000

Variable cost (12000*8) 96000

Add : Opening stock (1000*53) 53000

Fixed production overhead 36000

Less: Cost of sales 725000

Profit 575000

Profit and loss account under absorption costing for month of January:

Particulars DR CR

Sales revenue (13000*100) 1300000

Direct material (12000*35) 420000

Direct labour (12000*10) 120000

Variable cost (12000*8) 96000

Add : Opening stock (1000*53) 53000

Fixed production overhead 36000

Less: Cost of sales 725000

Profit 575000

Profit and loss account under absorption costing for month of January:

Particulars DR CR

Sales revenue (13000*100) 1300000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

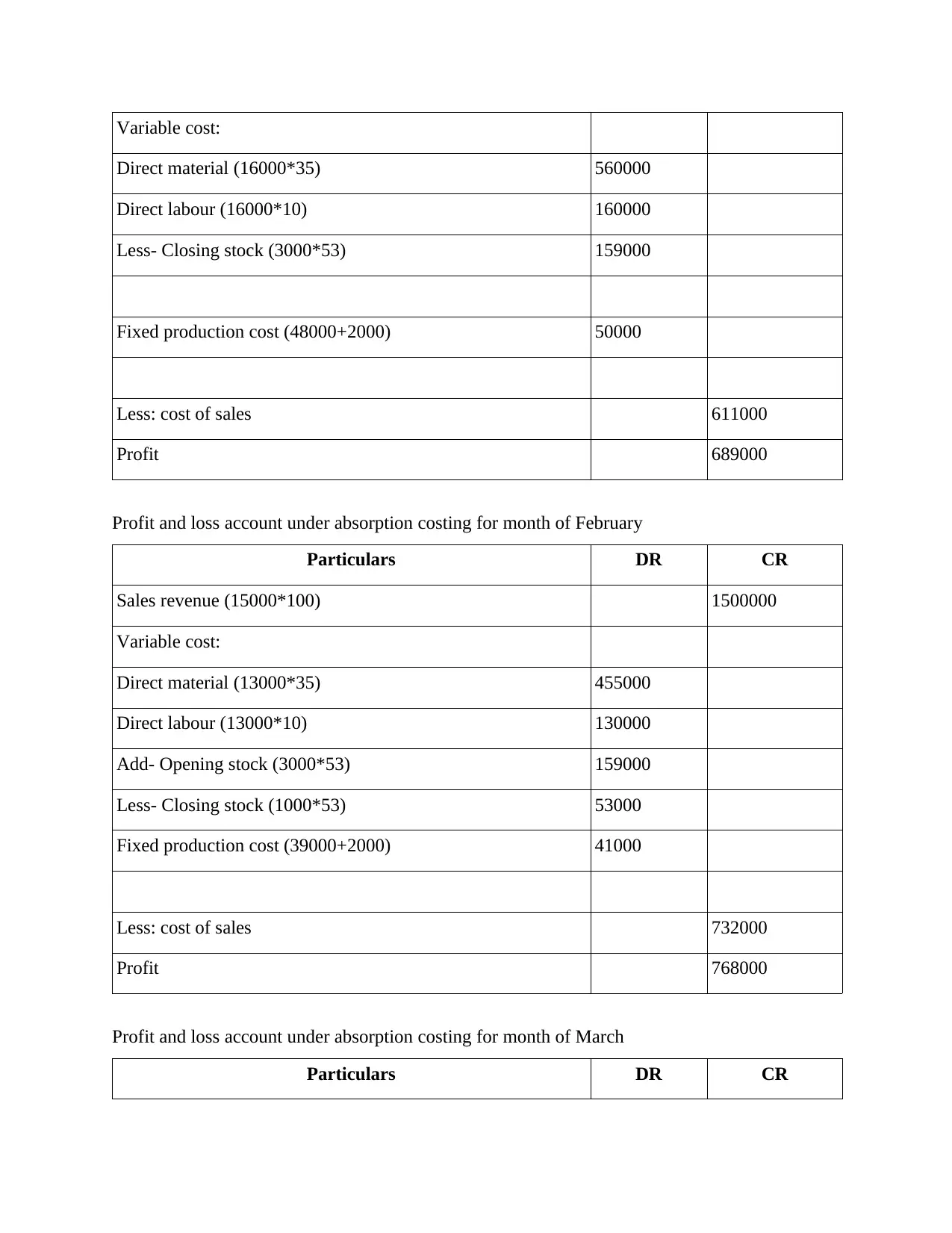

Variable cost:

Direct material (16000*35) 560000

Direct labour (16000*10) 160000

Less- Closing stock (3000*53) 159000

Fixed production cost (48000+2000) 50000

Less: cost of sales 611000

Profit 689000

Profit and loss account under absorption costing for month of February

Particulars DR CR

Sales revenue (15000*100) 1500000

Variable cost:

Direct material (13000*35) 455000

Direct labour (13000*10) 130000

Add- Opening stock (3000*53) 159000

Less- Closing stock (1000*53) 53000

Fixed production cost (39000+2000) 41000

Less: cost of sales 732000

Profit 768000

Profit and loss account under absorption costing for month of March

Particulars DR CR

Direct material (16000*35) 560000

Direct labour (16000*10) 160000

Less- Closing stock (3000*53) 159000

Fixed production cost (48000+2000) 50000

Less: cost of sales 611000

Profit 689000

Profit and loss account under absorption costing for month of February

Particulars DR CR

Sales revenue (15000*100) 1500000

Variable cost:

Direct material (13000*35) 455000

Direct labour (13000*10) 130000

Add- Opening stock (3000*53) 159000

Less- Closing stock (1000*53) 53000

Fixed production cost (39000+2000) 41000

Less: cost of sales 732000

Profit 768000

Profit and loss account under absorption costing for month of March

Particulars DR CR

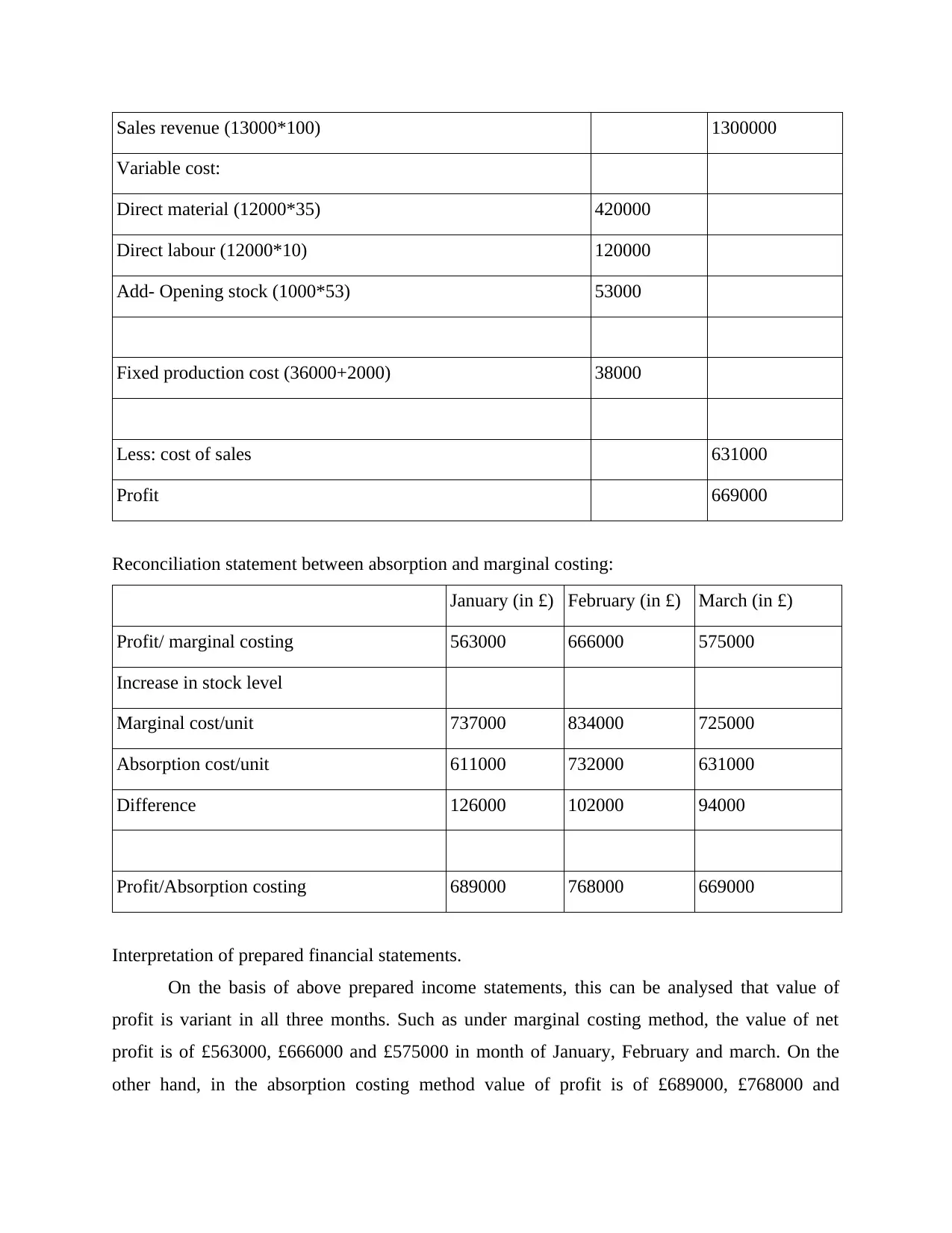

Sales revenue (13000*100) 1300000

Variable cost:

Direct material (12000*35) 420000

Direct labour (12000*10) 120000

Add- Opening stock (1000*53) 53000

Fixed production cost (36000+2000) 38000

Less: cost of sales 631000

Profit 669000

Reconciliation statement between absorption and marginal costing:

January (in £) February (in £) March (in £)

Profit/ marginal costing 563000 666000 575000

Increase in stock level

Marginal cost/unit 737000 834000 725000

Absorption cost/unit 611000 732000 631000

Difference 126000 102000 94000

Profit/Absorption costing 689000 768000 669000

Interpretation of prepared financial statements.

On the basis of above prepared income statements, this can be analysed that value of

profit is variant in all three months. Such as under marginal costing method, the value of net

profit is of £563000, £666000 and £575000 in month of January, February and march. On the

other hand, in the absorption costing method value of profit is of £689000, £768000 and

Variable cost:

Direct material (12000*35) 420000

Direct labour (12000*10) 120000

Add- Opening stock (1000*53) 53000

Fixed production cost (36000+2000) 38000

Less: cost of sales 631000

Profit 669000

Reconciliation statement between absorption and marginal costing:

January (in £) February (in £) March (in £)

Profit/ marginal costing 563000 666000 575000

Increase in stock level

Marginal cost/unit 737000 834000 725000

Absorption cost/unit 611000 732000 631000

Difference 126000 102000 94000

Profit/Absorption costing 689000 768000 669000

Interpretation of prepared financial statements.

On the basis of above prepared income statements, this can be analysed that value of

profit is variant in all three months. Such as under marginal costing method, the value of net

profit is of £563000, £666000 and £575000 in month of January, February and march. On the

other hand, in the absorption costing method value of profit is of £689000, £768000 and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.