Project Report: Management Accounting, Ethics, and Financial Analysis

VerifiedAdded on 2023/06/09

|13

|1778

|232

Project

AI Summary

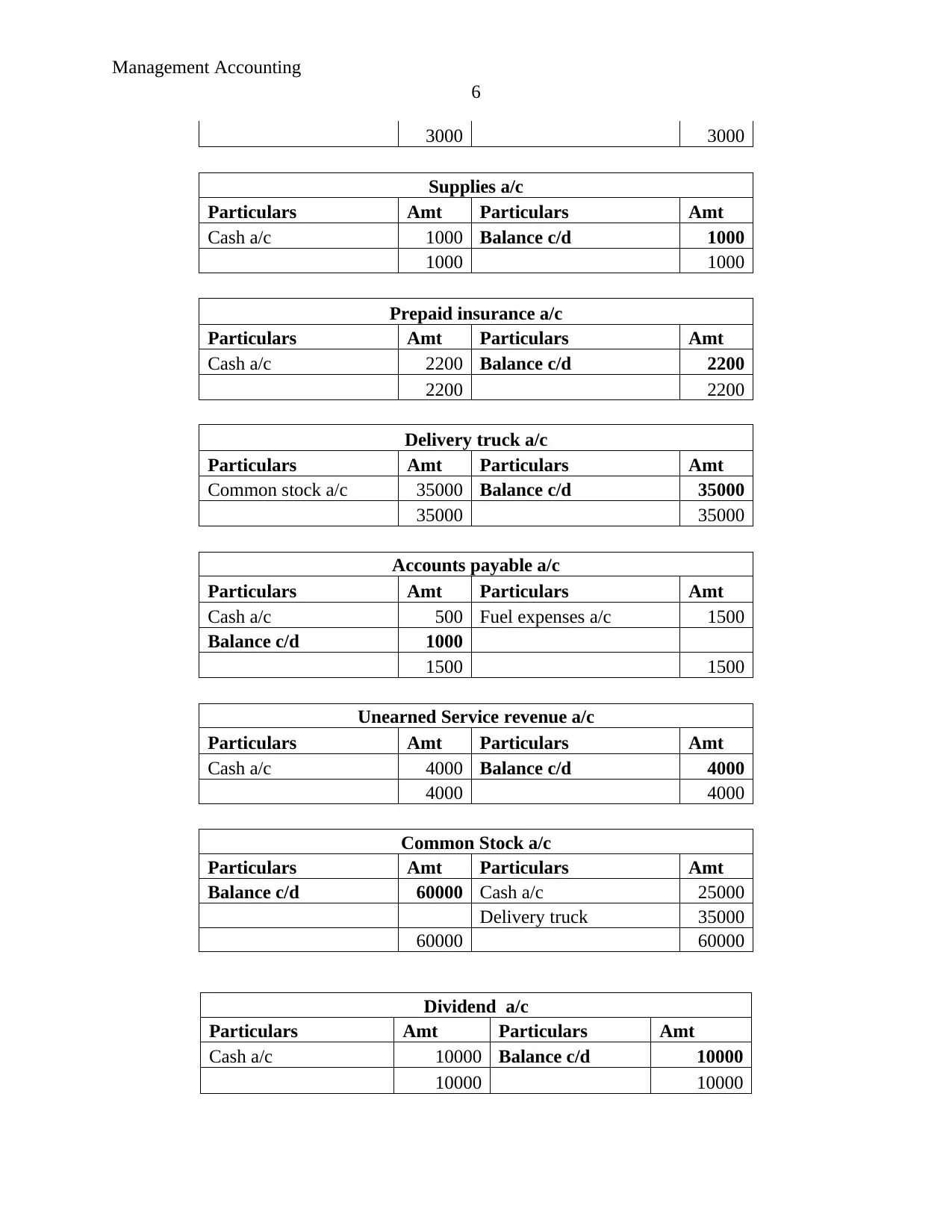

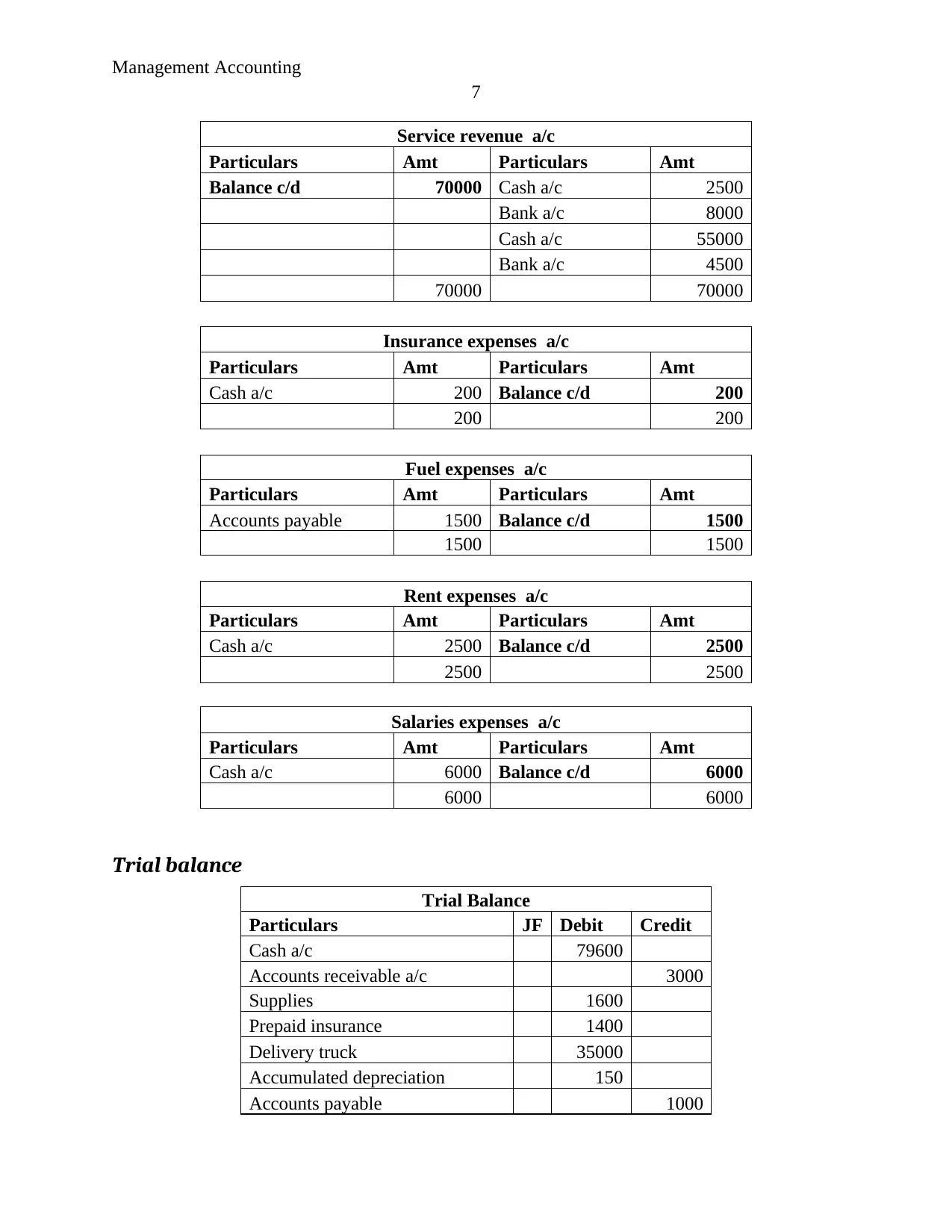

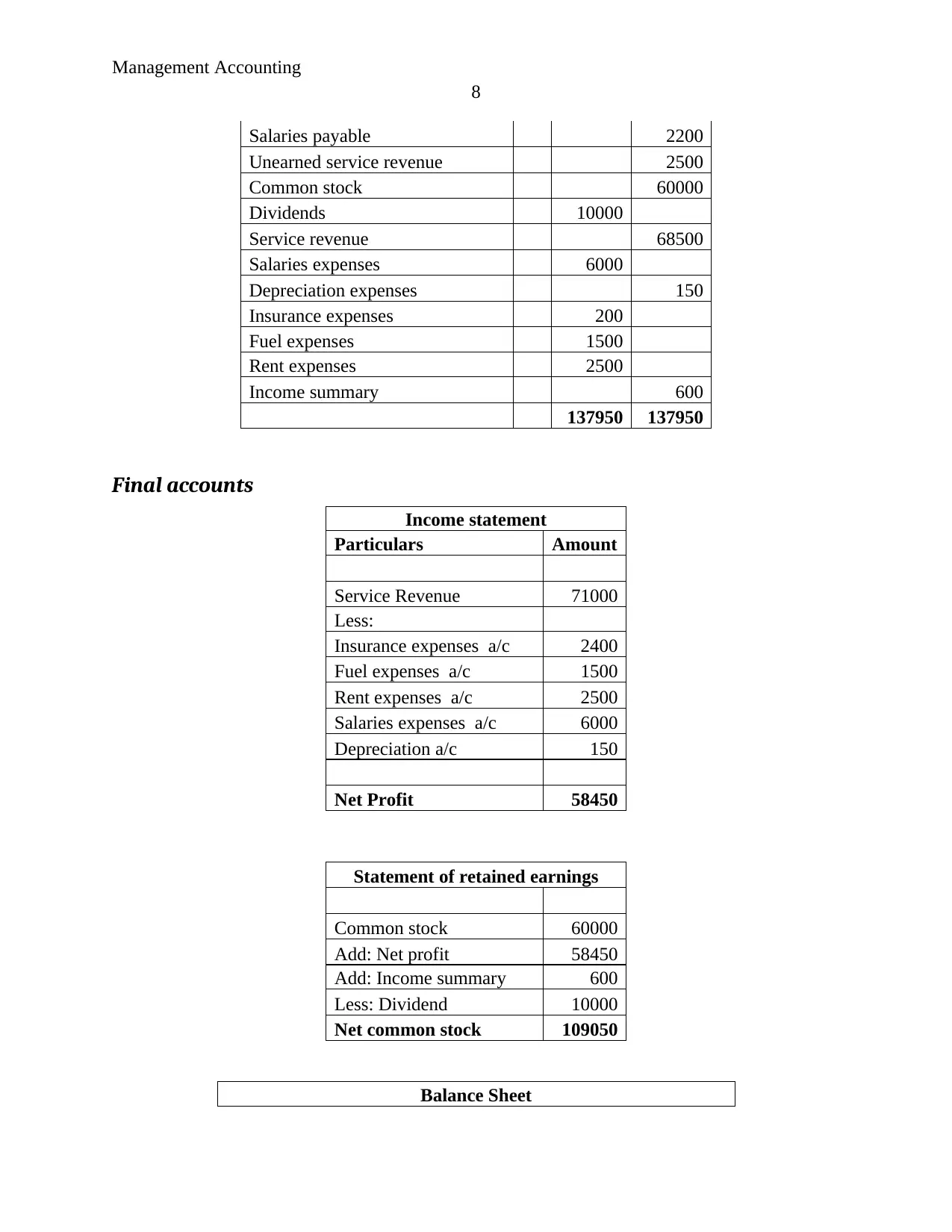

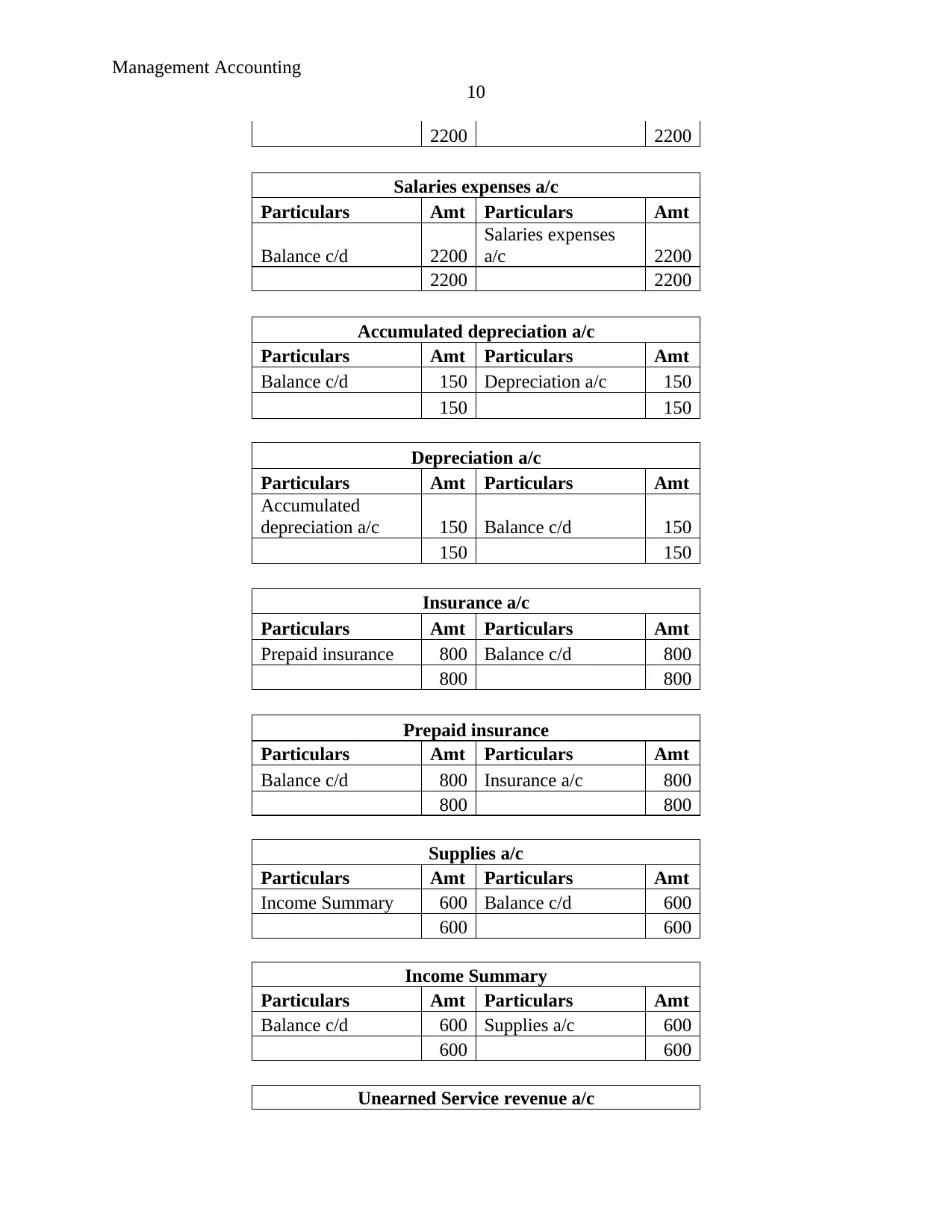

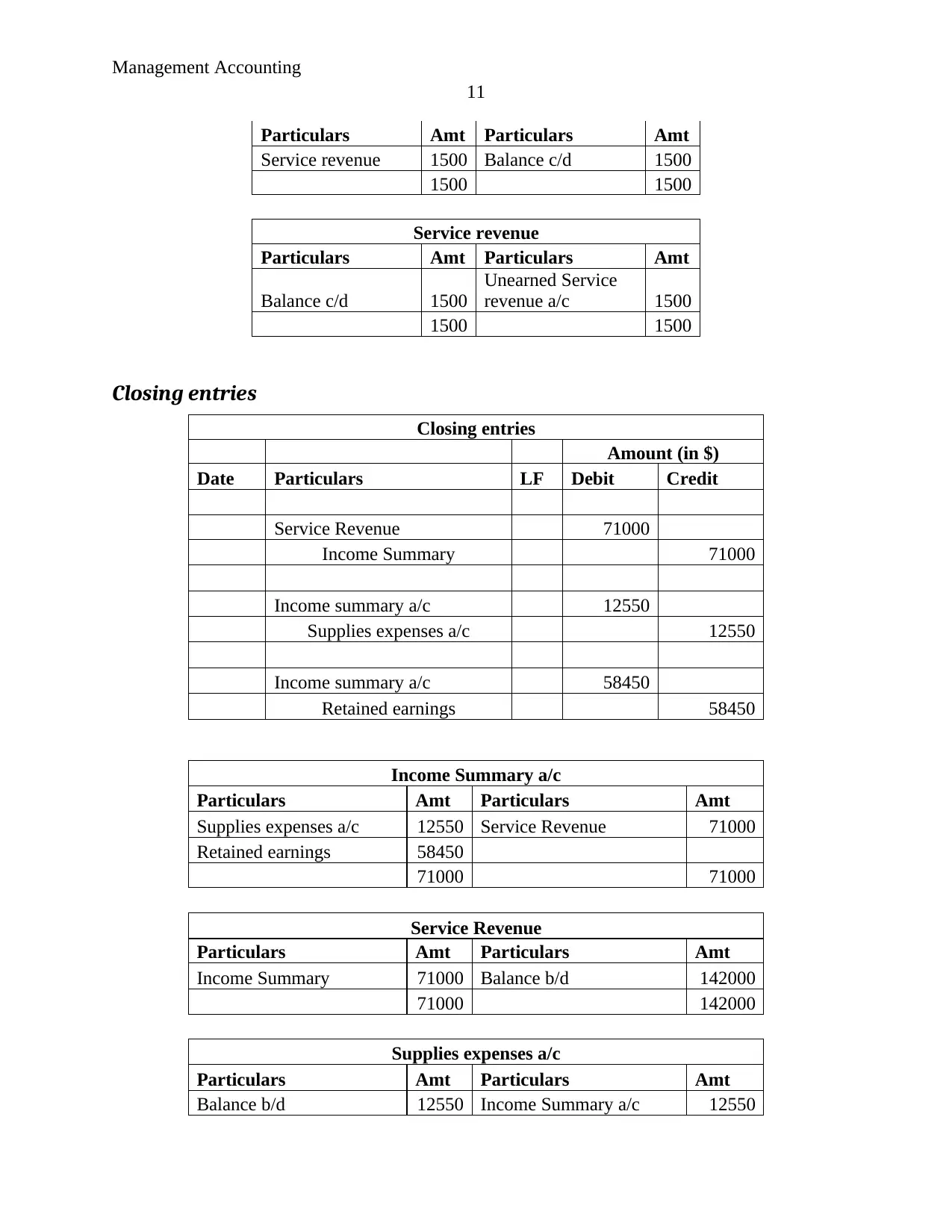

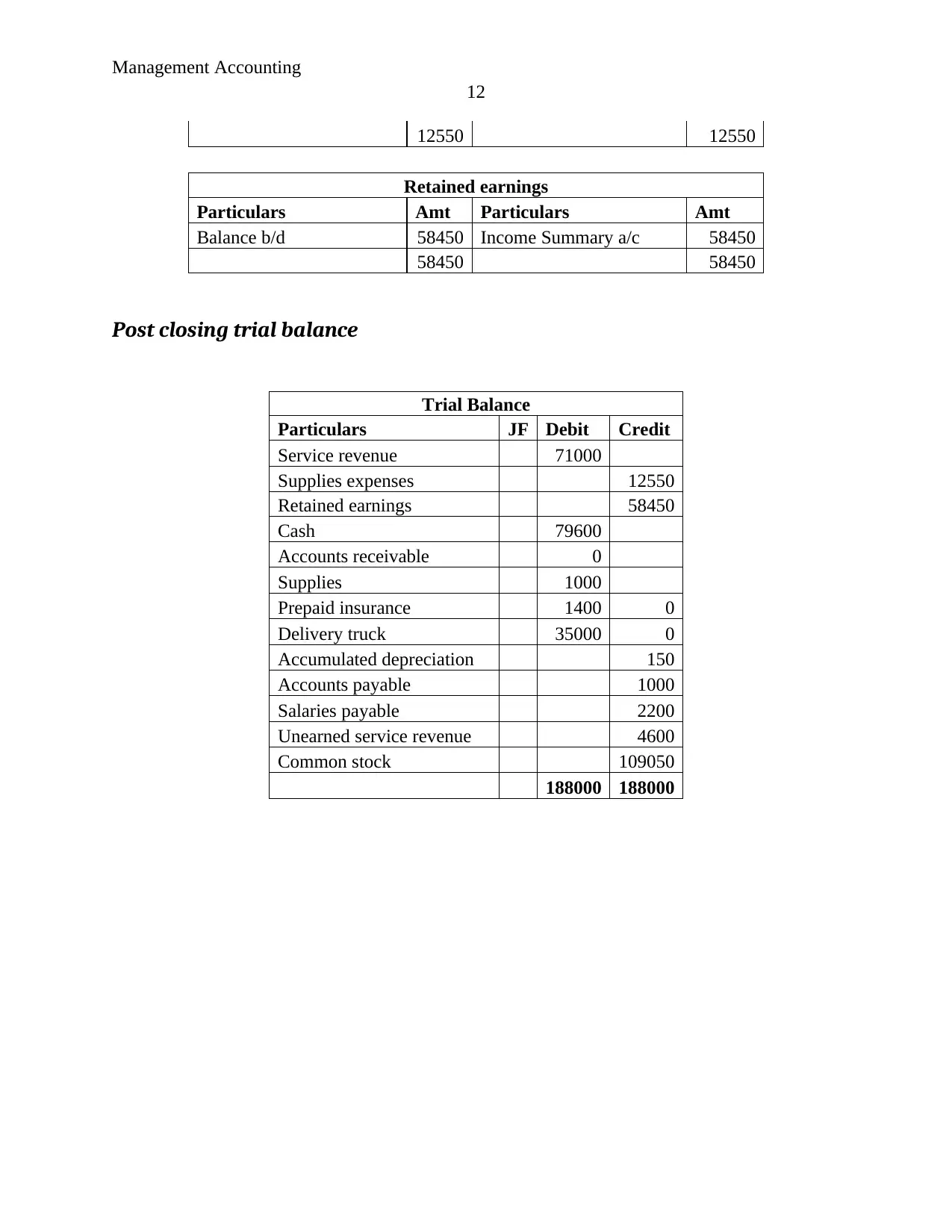

This management accounting project provides a comprehensive analysis of accrual accounting principles and their impact on financial statement usefulness. It includes a case study addressing ethical issues in financial reporting, focusing on the responsibilities of a controller in ensuring accurate financial information. The project also demonstrates the practical application of accounting principles through journal entries, ledger accounts, a trial balance, and the preparation of final accounts, including an income statement and balance sheet. Adjusting and closing entries are detailed, culminating in a post-closing trial balance, offering a complete overview of the accounting cycle. This resource is available for students seeking solved assignments and study materials on Desklib.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.