Management Accounting Report: Analyzing Costs for Jeffery & Sons

VerifiedAdded on 2020/01/15

|25

|6901

|101

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, using the case of Jeffery & Sons. It begins by classifying different types of costs, calculates unit and total job costs for a specific job (Job 444), and applies absorption costing techniques to determine the cost of Exquisite products. The report then delves into cost data analysis, including the allocation and apportionment of overhead costs across production departments. Furthermore, it includes the preparation of a cost report with variance analysis, performance indicators, and recommendations for cost reduction and quality enhancement. The report also covers the budgeting process, including the preparation of production, material purchase, and cash budgets. Finally, it addresses variance calculations, corrective measures, and the preparation of an operating statement to reconcile budgeted and actual results, along with a discussion of responsibility centers.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Classifying the different types of cost..............................................................................1

1.2 Calculating the unit cost and total job cost for job 444....................................................3

1.3 Calculating the cost of Exquisite by using absorption costing technique........................4

1.4 Analyzing the cost data of Exquisite by using appropriate techniques............................6

TASK 2............................................................................................................................................7

2.1 Preparation of the cost report by analyzing the variances................................................7

2.2 Using performance indicator to assess the areas for potential improvements..................8

2.3 Recommending ways to reduce costs, enhance value and quality...................................9

TASK 3............................................................................................................................................9

3.1 Stating the purpose and nature of the budgeting process to the budget holders of Jeffery &

Son's........................................................................................................................................9

3.2 Opt the suitable budgeting method for the company along with its needs.....................10

3.3 Preparation of the production and material purchase budget.........................................10

3.4 Preparation of cash budget.............................................................................................12

TASK 4..........................................................................................................................................12

4.1 Calculating variances, assessment of causes and recommending the corrective measures

..............................................................................................................................................12

4.2 Preparing the operating statement which reconcile both the budgeted and actual results14

4.3 Responsibility centers.....................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Classifying the different types of cost..............................................................................1

1.2 Calculating the unit cost and total job cost for job 444....................................................3

1.3 Calculating the cost of Exquisite by using absorption costing technique........................4

1.4 Analyzing the cost data of Exquisite by using appropriate techniques............................6

TASK 2............................................................................................................................................7

2.1 Preparation of the cost report by analyzing the variances................................................7

2.2 Using performance indicator to assess the areas for potential improvements..................8

2.3 Recommending ways to reduce costs, enhance value and quality...................................9

TASK 3............................................................................................................................................9

3.1 Stating the purpose and nature of the budgeting process to the budget holders of Jeffery &

Son's........................................................................................................................................9

3.2 Opt the suitable budgeting method for the company along with its needs.....................10

3.3 Preparation of the production and material purchase budget.........................................10

3.4 Preparation of cash budget.............................................................................................12

TASK 4..........................................................................................................................................12

4.1 Calculating variances, assessment of causes and recommending the corrective measures

..............................................................................................................................................12

4.2 Preparing the operating statement which reconcile both the budgeted and actual results14

4.3 Responsibility centers.....................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting may be defined as a systematic record of business transactions

and activities which are made during the accounting year. Management accounting helps finance

manager in making effective decisions (Mongiello, 2015). It provides an idea to an organization

about their financial and statistical performance. Through this, company is able to undertake

effective measures which facilitate control over the costs that are incurred by an organization. It

helps organization in enhancing the productivity and profitability of an organization.

This project report is based upon the case scenario of Jeffery & Sons. It is most popular

manufacturing company who produces popular and branded products which are termed as

Exquisite. The present report will develop understanding about the different types of costs as

well as the use of different types of costing methods. Besides this, it will shed light on the ways

through which one can prepare or analyze the cost reports. Further, it depicts the nature and

purpose of budgeting process in the business organization.

TASK 1

1.1 Classifying the different types of cost

Cost refers to the summation of several expenses which are incurred by an organization

in order to manufacture the products or services (Alaa-Aldin, 2007).

Classification of the cost: Jeffery & Son's can classify on the different basis which are

enumerated blow:

On the basis of nature

Costs Features

Material

It consists of the cost which organization

incurs to access raw material for the production

of finished goods.

Labor

Labor cost refers to those which are highly

associated with the human resources of an

organization (Gibassier and Schaltegger,

2015). It includes the wages of worker, tax

benefits and their insurance.

1 | P a g e

Management accounting may be defined as a systematic record of business transactions

and activities which are made during the accounting year. Management accounting helps finance

manager in making effective decisions (Mongiello, 2015). It provides an idea to an organization

about their financial and statistical performance. Through this, company is able to undertake

effective measures which facilitate control over the costs that are incurred by an organization. It

helps organization in enhancing the productivity and profitability of an organization.

This project report is based upon the case scenario of Jeffery & Sons. It is most popular

manufacturing company who produces popular and branded products which are termed as

Exquisite. The present report will develop understanding about the different types of costs as

well as the use of different types of costing methods. Besides this, it will shed light on the ways

through which one can prepare or analyze the cost reports. Further, it depicts the nature and

purpose of budgeting process in the business organization.

TASK 1

1.1 Classifying the different types of cost

Cost refers to the summation of several expenses which are incurred by an organization

in order to manufacture the products or services (Alaa-Aldin, 2007).

Classification of the cost: Jeffery & Son's can classify on the different basis which are

enumerated blow:

On the basis of nature

Costs Features

Material

It consists of the cost which organization

incurs to access raw material for the production

of finished goods.

Labor

Labor cost refers to those which are highly

associated with the human resources of an

organization (Gibassier and Schaltegger,

2015). It includes the wages of worker, tax

benefits and their insurance.

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Overhead

These costs are also termed as operating cost

which is incurred by an organization to run

business activities and functions.

On the basis of changes take place in activity or volume

Costs Features

Fixed cost

It may defined as those which remain

unchanged as changes take place in the number

of unit produced. For instance: factory rent,

salary of the workers.

Semi-variable cost

In this, cost of the output remains fixed to the

certain level of production. Besides this, such

cost becomes variable when predetermined

level of output exceeds (Chan and Chan,

2004). For instance: Wages of workers,

advertisement expenses etc.

Variable cost

It refers to those which increase or decrease as

changes take place in the level of output

produced. It includes electricity expenses etc.

On the basis of functions

Costs Features

Production cost

It represents the cost which is incurred by

Jeffery & Son's in manufacturing of product.

Commercial cost Commercial cost includes administration as

well as selling and distribution cost. Such cost

refers to the operational expenses which firm

has to incur in order to run business operations

and functions in an effective manner (McLean,

2 | P a g e

These costs are also termed as operating cost

which is incurred by an organization to run

business activities and functions.

On the basis of changes take place in activity or volume

Costs Features

Fixed cost

It may defined as those which remain

unchanged as changes take place in the number

of unit produced. For instance: factory rent,

salary of the workers.

Semi-variable cost

In this, cost of the output remains fixed to the

certain level of production. Besides this, such

cost becomes variable when predetermined

level of output exceeds (Chan and Chan,

2004). For instance: Wages of workers,

advertisement expenses etc.

Variable cost

It refers to those which increase or decrease as

changes take place in the level of output

produced. It includes electricity expenses etc.

On the basis of functions

Costs Features

Production cost

It represents the cost which is incurred by

Jeffery & Son's in manufacturing of product.

Commercial cost Commercial cost includes administration as

well as selling and distribution cost. Such cost

refers to the operational expenses which firm

has to incur in order to run business operations

and functions in an effective manner (McLean,

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

McGovern and Davie, 2015).

1.2 Calculating the unit cost and total job cost for job 444

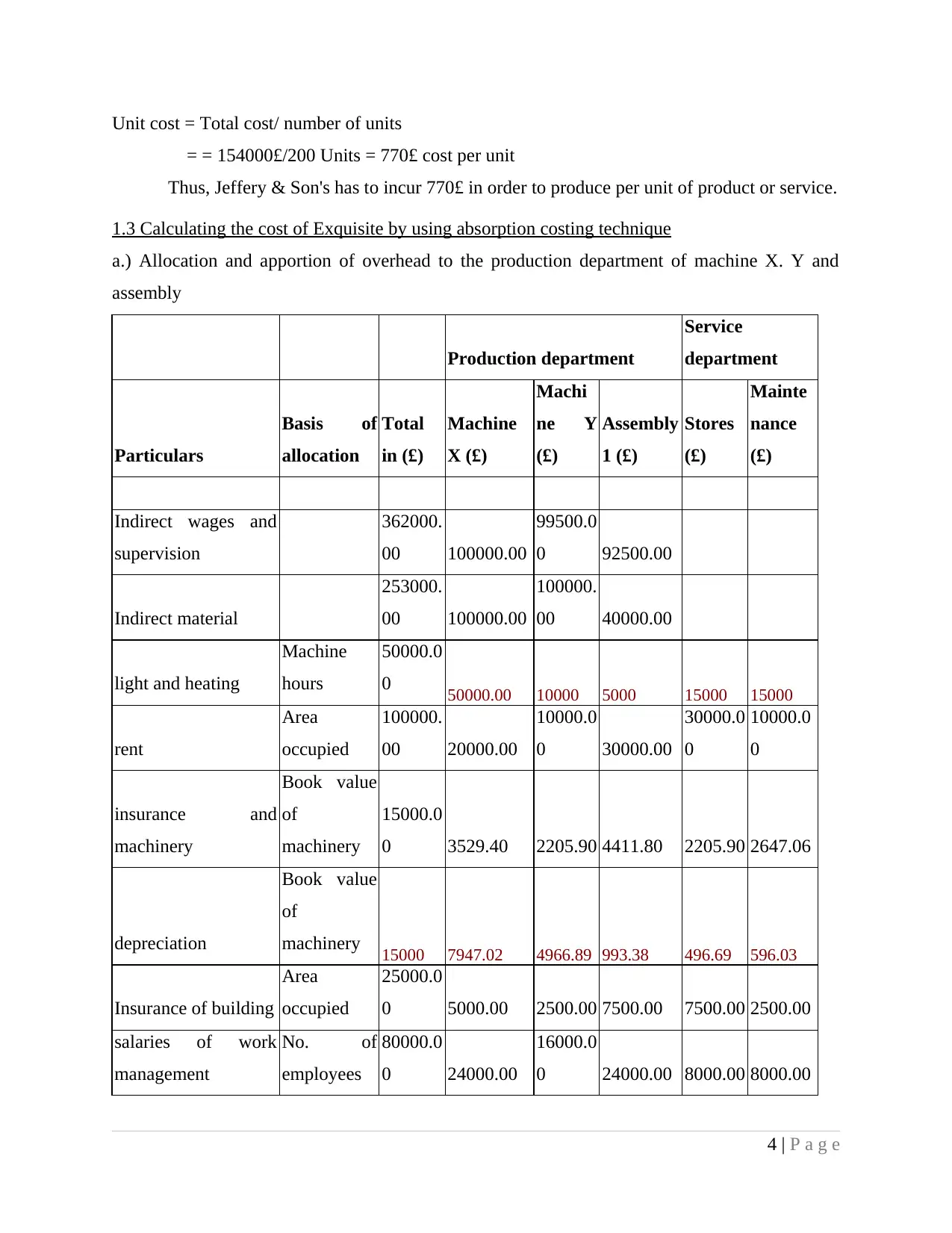

Cost sheet and unit cost: Cost sheet is the document which provides deeper insight to the

manager about the cost which they require to incur on the different types of projects. Along with

it, job costing may be defined as a process in which producer assigns manufacturing cost to an an

individual product. Besides this, unit cost refers to the cost which is incurred by Jeffery & Son's

in order to produce one unit of product or service.

Job cost sheet for Job no. 444

Particulars Total cost

Direct material 40000

Direct Labor 54000

Fixed production overhead 24000

variable production overhead 36000

Total cost 154000

Unit cost 770

Working note:

Direct material cost

Material cost = Quantity * price per kg.

= 50kg* 4£ per kg.*200 units= 400000£

Direct labor cost

Labor cost = Total working hours * rate per hour

Labor hours = 30 hours per unit*200 Units = 6000 Hours

Overhead

Fixed overhead = Total fixed production overhead/Total budgeted labor hours*Labor hours for

job

Fixed overhead = = 80000£/20000 hours* 6000 hours

= 24000£

Variable production overhead = Total hours* rate per hour

Variable overhead = = 6£ per hour * 6000 hours

= 36000£

3 | P a g e

1.2 Calculating the unit cost and total job cost for job 444

Cost sheet and unit cost: Cost sheet is the document which provides deeper insight to the

manager about the cost which they require to incur on the different types of projects. Along with

it, job costing may be defined as a process in which producer assigns manufacturing cost to an an

individual product. Besides this, unit cost refers to the cost which is incurred by Jeffery & Son's

in order to produce one unit of product or service.

Job cost sheet for Job no. 444

Particulars Total cost

Direct material 40000

Direct Labor 54000

Fixed production overhead 24000

variable production overhead 36000

Total cost 154000

Unit cost 770

Working note:

Direct material cost

Material cost = Quantity * price per kg.

= 50kg* 4£ per kg.*200 units= 400000£

Direct labor cost

Labor cost = Total working hours * rate per hour

Labor hours = 30 hours per unit*200 Units = 6000 Hours

Overhead

Fixed overhead = Total fixed production overhead/Total budgeted labor hours*Labor hours for

job

Fixed overhead = = 80000£/20000 hours* 6000 hours

= 24000£

Variable production overhead = Total hours* rate per hour

Variable overhead = = 6£ per hour * 6000 hours

= 36000£

3 | P a g e

Unit cost = Total cost/ number of units

= = 154000£/200 Units = 770£ cost per unit

Thus, Jeffery & Son's has to incur 770£ in order to produce per unit of product or service.

1.3 Calculating the cost of Exquisite by using absorption costing technique

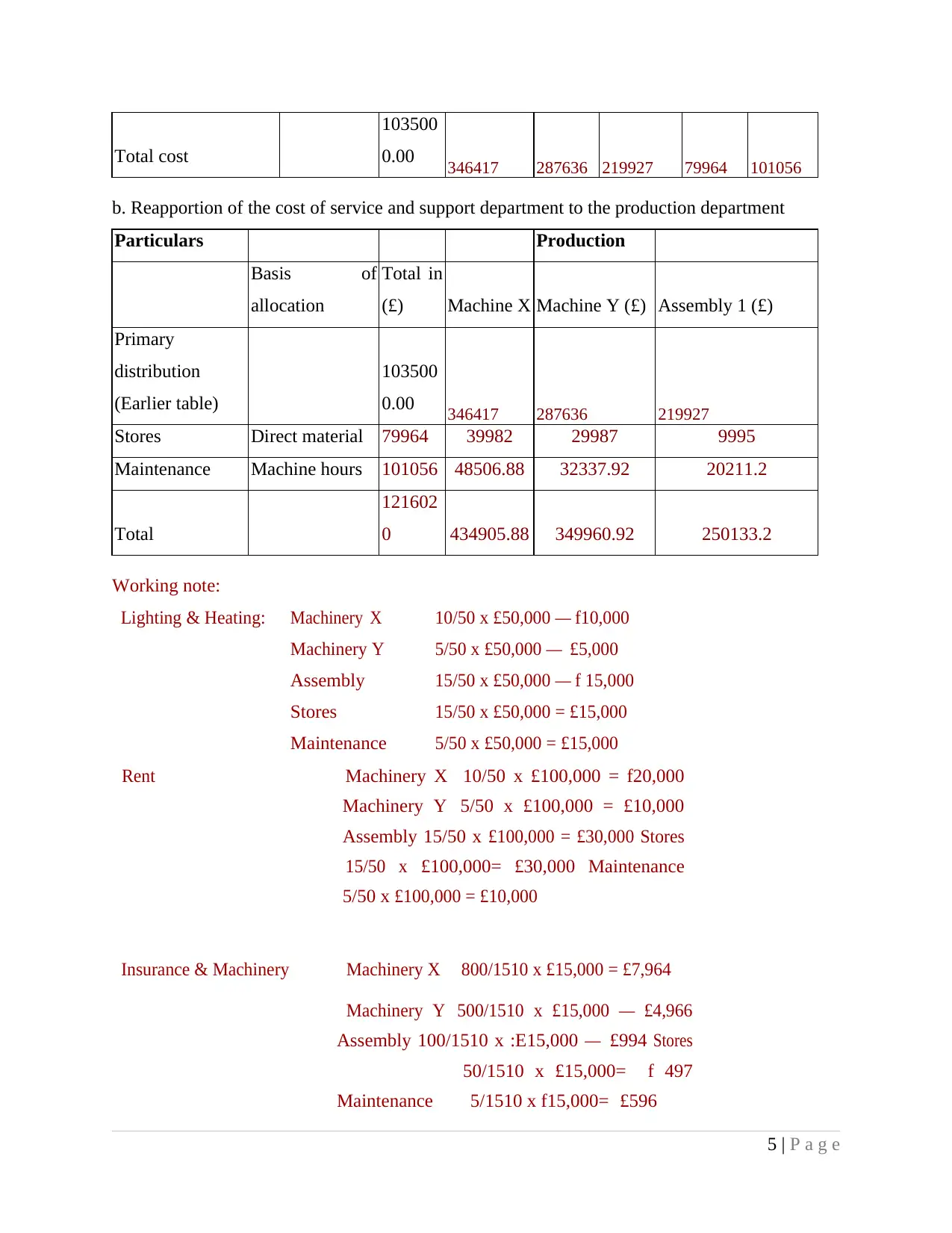

a.) Allocation and apportion of overhead to the production department of machine X. Y and

assembly

Production department

Service

department

Particulars

Basis of

allocation

Total

in (£)

Machine

X (£)

Machi

ne Y

(£)

Assembly

1 (£)

Stores

(£)

Mainte

nance

(£)

Indirect wages and

supervision

362000.

00 100000.00

99500.0

0 92500.00

Indirect material

253000.

00 100000.00

100000.

00 40000.00

light and heating

Machine

hours

50000.0

0 50000.00 10000 5000 15000 15000

rent

Area

occupied

100000.

00 20000.00

10000.0

0 30000.00

30000.0

0

10000.0

0

insurance and

machinery

Book value

of

machinery

15000.0

0 3529.40 2205.90 4411.80 2205.90 2647.06

depreciation

Book value

of

machinery 15000 7947.02 4966.89 993.38 496.69 596.03

Insurance of building

Area

occupied

25000.0

0 5000.00 2500.00 7500.00 7500.00 2500.00

salaries of work

management

No. of

employees

80000.0

0 24000.00

16000.0

0 24000.00 8000.00 8000.00

4 | P a g e

= = 154000£/200 Units = 770£ cost per unit

Thus, Jeffery & Son's has to incur 770£ in order to produce per unit of product or service.

1.3 Calculating the cost of Exquisite by using absorption costing technique

a.) Allocation and apportion of overhead to the production department of machine X. Y and

assembly

Production department

Service

department

Particulars

Basis of

allocation

Total

in (£)

Machine

X (£)

Machi

ne Y

(£)

Assembly

1 (£)

Stores

(£)

Mainte

nance

(£)

Indirect wages and

supervision

362000.

00 100000.00

99500.0

0 92500.00

Indirect material

253000.

00 100000.00

100000.

00 40000.00

light and heating

Machine

hours

50000.0

0 50000.00 10000 5000 15000 15000

rent

Area

occupied

100000.

00 20000.00

10000.0

0 30000.00

30000.0

0

10000.0

0

insurance and

machinery

Book value

of

machinery

15000.0

0 3529.40 2205.90 4411.80 2205.90 2647.06

depreciation

Book value

of

machinery 15000 7947.02 4966.89 993.38 496.69 596.03

Insurance of building

Area

occupied

25000.0

0 5000.00 2500.00 7500.00 7500.00 2500.00

salaries of work

management

No. of

employees

80000.0

0 24000.00

16000.0

0 24000.00 8000.00 8000.00

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total cost

103500

0.00 346417 287636 219927 79964 101056

b. Reapportion of the cost of service and support department to the production department

Particulars Production

Basis of

allocation

Total in

(£) Machine X Machine Y (£) Assembly 1 (£)

Primary

distribution

(Earlier table)

103500

0.00 346417 287636 219927

Stores Direct material 79964 39982 29987 9995

Maintenance Machine hours 101056 48506.88 32337.92 20211.2

Total

121602

0 434905.88 349960.92 250133.2

Working note:

Lighting & Heating: Machinery X 10/50 x £50,000 — f10,000

Machinery Y 5/50 x £50,000 — £5,000

Assembly 15/50 x £50,000 — f 15,000

Stores 15/50 x £50,000 = £15,000

Maintenance 5/50 x £50,000 = £15,000

Rent Machinery X 10/50 x £100,000 = f20,000

Machinery Y 5/50 x £100,000 = £10,000

Assembly 15/50 x £100,000 = £30,000 Stores

15/50 x £100,000= £30,000 Maintenance

5/50 x £100,000 = £10,000

Insurance & Machinery Machinery X 800/1510 x £15,000 = £7,964

Machinery Y 500/1510 x £15,000 — £4,966

Assembly 100/1510 x :E15,000 — £994 Stores

50/1510 x £15,000= f 497

Maintenance 5/1510 x f15,000= £596

5 | P a g e

103500

0.00 346417 287636 219927 79964 101056

b. Reapportion of the cost of service and support department to the production department

Particulars Production

Basis of

allocation

Total in

(£) Machine X Machine Y (£) Assembly 1 (£)

Primary

distribution

(Earlier table)

103500

0.00 346417 287636 219927

Stores Direct material 79964 39982 29987 9995

Maintenance Machine hours 101056 48506.88 32337.92 20211.2

Total

121602

0 434905.88 349960.92 250133.2

Working note:

Lighting & Heating: Machinery X 10/50 x £50,000 — f10,000

Machinery Y 5/50 x £50,000 — £5,000

Assembly 15/50 x £50,000 — f 15,000

Stores 15/50 x £50,000 = £15,000

Maintenance 5/50 x £50,000 = £15,000

Rent Machinery X 10/50 x £100,000 = f20,000

Machinery Y 5/50 x £100,000 = £10,000

Assembly 15/50 x £100,000 = £30,000 Stores

15/50 x £100,000= £30,000 Maintenance

5/50 x £100,000 = £10,000

Insurance & Machinery Machinery X 800/1510 x £15,000 = £7,964

Machinery Y 500/1510 x £15,000 — £4,966

Assembly 100/1510 x :E15,000 — £994 Stores

50/1510 x £15,000= f 497

Maintenance 5/1510 x f15,000= £596

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Depreciation of Machinery

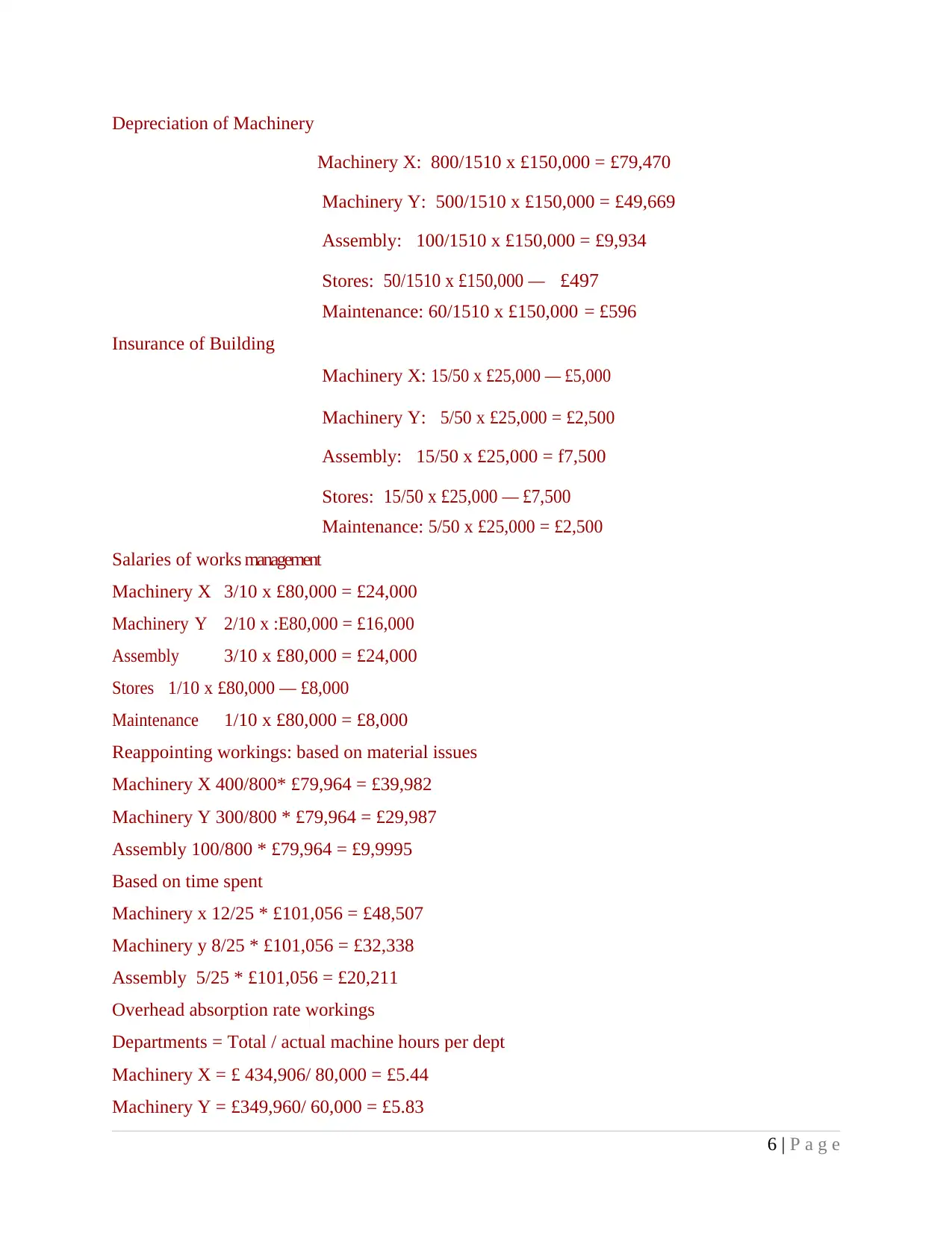

Machinery X: 800/1510 x £150,000 = £79,470

Machinery Y: 500/1510 x £150,000 = £49,669

Assembly: 100/1510 x £150,000 = £9,934

Stores: 50/1510 x £150,000 — £497

Maintenance: 60/1510 x £150,000 = £596

Insurance of Building

Machinery X: 15/50 x £25,000 — £5,000

Machinery Y: 5/50 x £25,000 = £2,500

Assembly: 15/50 x £25,000 = f7,500

Stores: 15/50 x £25,000 — £7,500

Maintenance: 5/50 x £25,000 = £2,500

Salaries of works management

Machinery X 3/10 x £80,000 = £24,000

Machinery Y 2/10 x :E80,000 = £16,000

Assembly 3/10 x £80,000 = £24,000

Stores 1/10 x £80,000 — £8,000

Maintenance 1/10 x £80,000 = £8,000

Reappointing workings: based on material issues

Machinery X 400/800* £79,964 = £39,982

Machinery Y 300/800 * £79,964 = £29,987

Assembly 100/800 * £79,964 = £9,9995

Based on time spent

Machinery x 12/25 * £101,056 = £48,507

Machinery y 8/25 * £101,056 = £32,338

Assembly 5/25 * £101,056 = £20,211

Overhead absorption rate workings

Departments = Total / actual machine hours per dept

Machinery X = £ 434,906/ 80,000 = £5.44

Machinery Y = £349,960/ 60,000 = £5.83

6 | P a g e

Machinery X: 800/1510 x £150,000 = £79,470

Machinery Y: 500/1510 x £150,000 = £49,669

Assembly: 100/1510 x £150,000 = £9,934

Stores: 50/1510 x £150,000 — £497

Maintenance: 60/1510 x £150,000 = £596

Insurance of Building

Machinery X: 15/50 x £25,000 — £5,000

Machinery Y: 5/50 x £25,000 = £2,500

Assembly: 15/50 x £25,000 = f7,500

Stores: 15/50 x £25,000 — £7,500

Maintenance: 5/50 x £25,000 = £2,500

Salaries of works management

Machinery X 3/10 x £80,000 = £24,000

Machinery Y 2/10 x :E80,000 = £16,000

Assembly 3/10 x £80,000 = £24,000

Stores 1/10 x £80,000 — £8,000

Maintenance 1/10 x £80,000 = £8,000

Reappointing workings: based on material issues

Machinery X 400/800* £79,964 = £39,982

Machinery Y 300/800 * £79,964 = £29,987

Assembly 100/800 * £79,964 = £9,9995

Based on time spent

Machinery x 12/25 * £101,056 = £48,507

Machinery y 8/25 * £101,056 = £32,338

Assembly 5/25 * £101,056 = £20,211

Overhead absorption rate workings

Departments = Total / actual machine hours per dept

Machinery X = £ 434,906/ 80,000 = £5.44

Machinery Y = £349,960/ 60,000 = £5.83

6 | P a g e

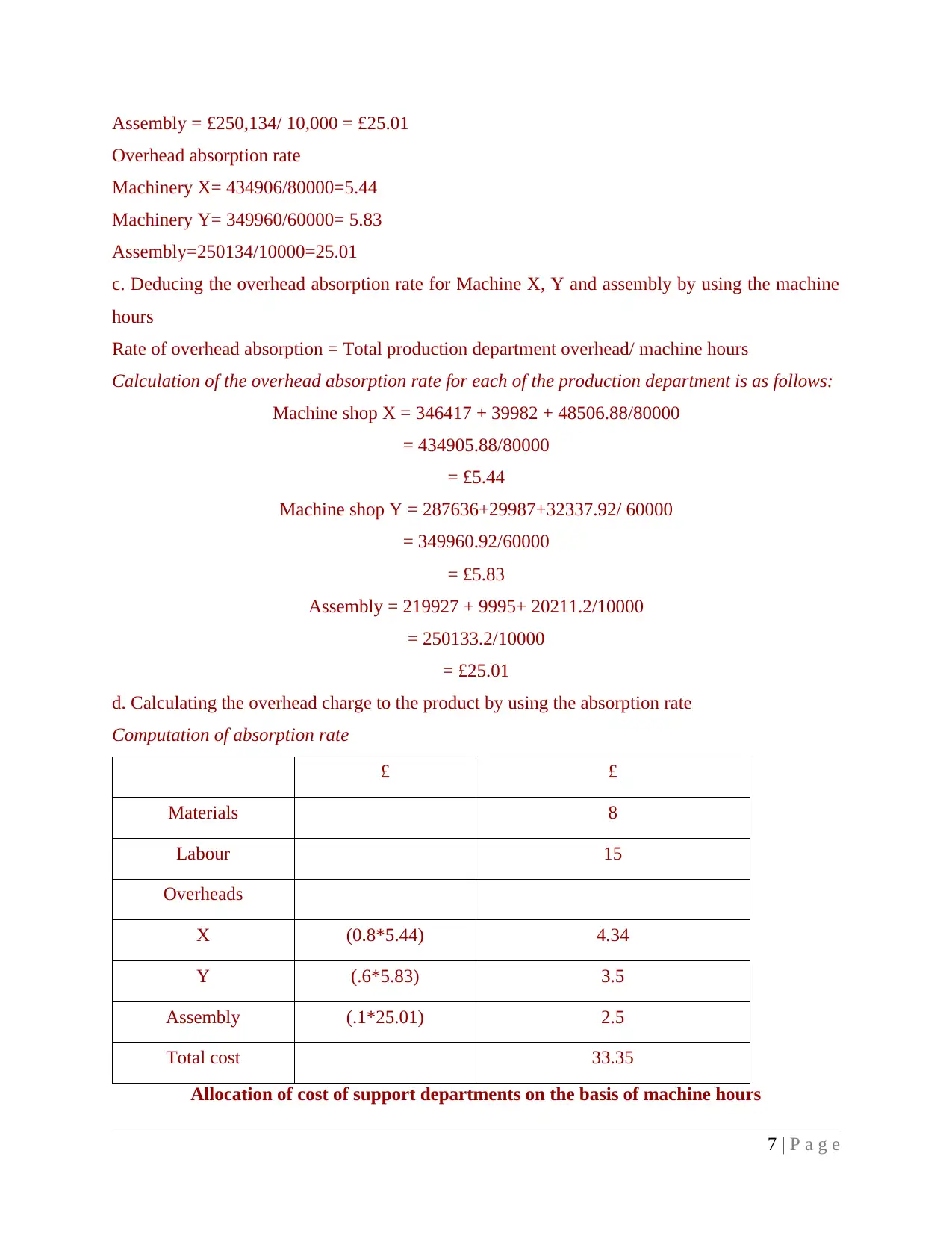

Assembly = £250,134/ 10,000 = £25.01

Overhead absorption rate

Machinery X= 434906/80000=5.44

Machinery Y= 349960/60000= 5.83

Assembly=250134/10000=25.01

c. Deducing the overhead absorption rate for Machine X, Y and assembly by using the machine

hours

Rate of overhead absorption = Total production department overhead/ machine hours

Calculation of the overhead absorption rate for each of the production department is as follows:

Machine shop X = 346417 + 39982 + 48506.88/80000

= 434905.88/80000

= £5.44

Machine shop Y = 287636+29987+32337.92/ 60000

= 349960.92/60000

= £5.83

Assembly = 219927 + 9995+ 20211.2/10000

= 250133.2/10000

= £25.01

d. Calculating the overhead charge to the product by using the absorption rate

Computation of absorption rate

£ £

Materials 8

Labour 15

Overheads

X (0.8*5.44) 4.34

Y (.6*5.83) 3.5

Assembly (.1*25.01) 2.5

Total cost 33.35

Allocation of cost of support departments on the basis of machine hours

7 | P a g e

Overhead absorption rate

Machinery X= 434906/80000=5.44

Machinery Y= 349960/60000= 5.83

Assembly=250134/10000=25.01

c. Deducing the overhead absorption rate for Machine X, Y and assembly by using the machine

hours

Rate of overhead absorption = Total production department overhead/ machine hours

Calculation of the overhead absorption rate for each of the production department is as follows:

Machine shop X = 346417 + 39982 + 48506.88/80000

= 434905.88/80000

= £5.44

Machine shop Y = 287636+29987+32337.92/ 60000

= 349960.92/60000

= £5.83

Assembly = 219927 + 9995+ 20211.2/10000

= 250133.2/10000

= £25.01

d. Calculating the overhead charge to the product by using the absorption rate

Computation of absorption rate

£ £

Materials 8

Labour 15

Overheads

X (0.8*5.44) 4.34

Y (.6*5.83) 3.5

Assembly (.1*25.01) 2.5

Total cost 33.35

Allocation of cost of support departments on the basis of machine hours

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

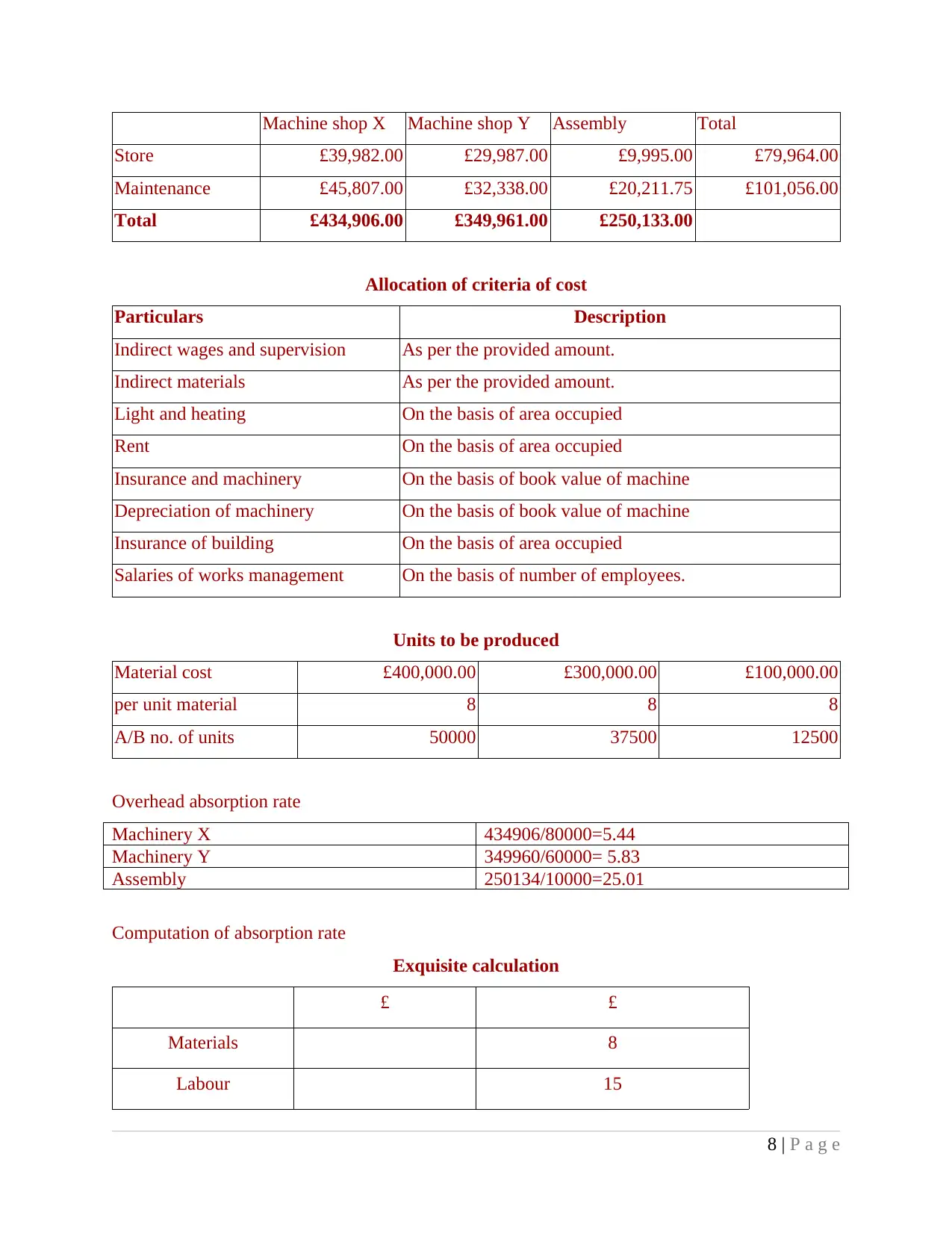

Machine shop X Machine shop Y Assembly Total

Store £39,982.00 £29,987.00 £9,995.00 £79,964.00

Maintenance £45,807.00 £32,338.00 £20,211.75 £101,056.00

Total £434,906.00 £349,961.00 £250,133.00

Allocation of criteria of cost

Particulars Description

Indirect wages and supervision As per the provided amount.

Indirect materials As per the provided amount.

Light and heating On the basis of area occupied

Rent On the basis of area occupied

Insurance and machinery On the basis of book value of machine

Depreciation of machinery On the basis of book value of machine

Insurance of building On the basis of area occupied

Salaries of works management On the basis of number of employees.

Units to be produced

Material cost £400,000.00 £300,000.00 £100,000.00

per unit material 8 8 8

A/B no. of units 50000 37500 12500

Overhead absorption rate

Machinery X 434906/80000=5.44

Machinery Y 349960/60000= 5.83

Assembly 250134/10000=25.01

Computation of absorption rate

Exquisite calculation

£ £

Materials 8

Labour 15

8 | P a g e

Store £39,982.00 £29,987.00 £9,995.00 £79,964.00

Maintenance £45,807.00 £32,338.00 £20,211.75 £101,056.00

Total £434,906.00 £349,961.00 £250,133.00

Allocation of criteria of cost

Particulars Description

Indirect wages and supervision As per the provided amount.

Indirect materials As per the provided amount.

Light and heating On the basis of area occupied

Rent On the basis of area occupied

Insurance and machinery On the basis of book value of machine

Depreciation of machinery On the basis of book value of machine

Insurance of building On the basis of area occupied

Salaries of works management On the basis of number of employees.

Units to be produced

Material cost £400,000.00 £300,000.00 £100,000.00

per unit material 8 8 8

A/B no. of units 50000 37500 12500

Overhead absorption rate

Machinery X 434906/80000=5.44

Machinery Y 349960/60000= 5.83

Assembly 250134/10000=25.01

Computation of absorption rate

Exquisite calculation

£ £

Materials 8

Labour 15

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

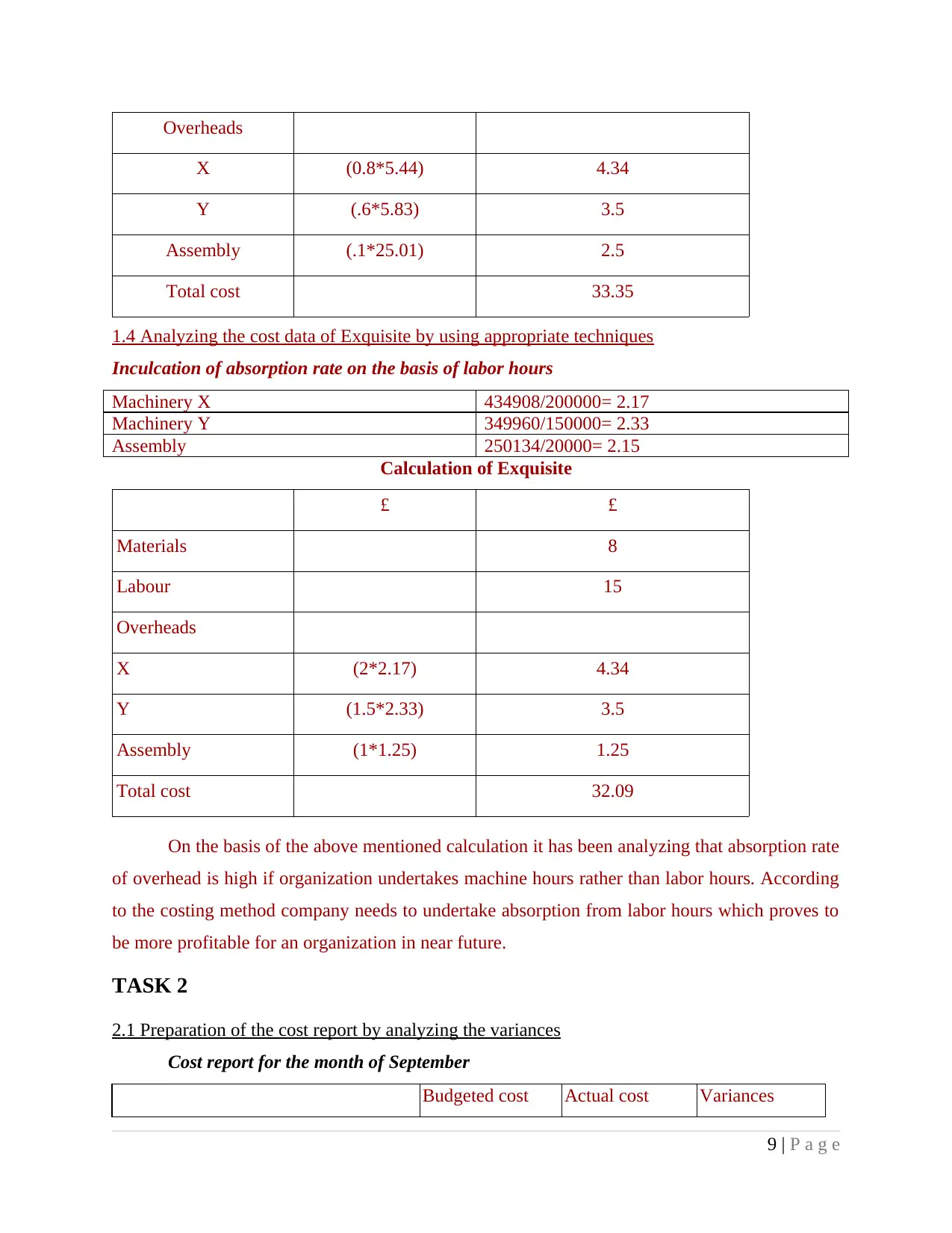

Overheads

X (0.8*5.44) 4.34

Y (.6*5.83) 3.5

Assembly (.1*25.01) 2.5

Total cost 33.35

1.4 Analyzing the cost data of Exquisite by using appropriate techniques

Inculcation of absorption rate on the basis of labor hours

Machinery X 434908/200000= 2.17

Machinery Y 349960/150000= 2.33

Assembly 250134/20000= 2.15

Calculation of Exquisite

£ £

Materials 8

Labour 15

Overheads

X (2*2.17) 4.34

Y (1.5*2.33) 3.5

Assembly (1*1.25) 1.25

Total cost 32.09

On the basis of the above mentioned calculation it has been analyzing that absorption rate

of overhead is high if organization undertakes machine hours rather than labor hours. According

to the costing method company needs to undertake absorption from labor hours which proves to

be more profitable for an organization in near future.

TASK 2

2.1 Preparation of the cost report by analyzing the variances

Cost report for the month of September

Budgeted cost Actual cost Variances

9 | P a g e

X (0.8*5.44) 4.34

Y (.6*5.83) 3.5

Assembly (.1*25.01) 2.5

Total cost 33.35

1.4 Analyzing the cost data of Exquisite by using appropriate techniques

Inculcation of absorption rate on the basis of labor hours

Machinery X 434908/200000= 2.17

Machinery Y 349960/150000= 2.33

Assembly 250134/20000= 2.15

Calculation of Exquisite

£ £

Materials 8

Labour 15

Overheads

X (2*2.17) 4.34

Y (1.5*2.33) 3.5

Assembly (1*1.25) 1.25

Total cost 32.09

On the basis of the above mentioned calculation it has been analyzing that absorption rate

of overhead is high if organization undertakes machine hours rather than labor hours. According

to the costing method company needs to undertake absorption from labor hours which proves to

be more profitable for an organization in near future.

TASK 2

2.1 Preparation of the cost report by analyzing the variances

Cost report for the month of September

Budgeted cost Actual cost Variances

9 | P a g e

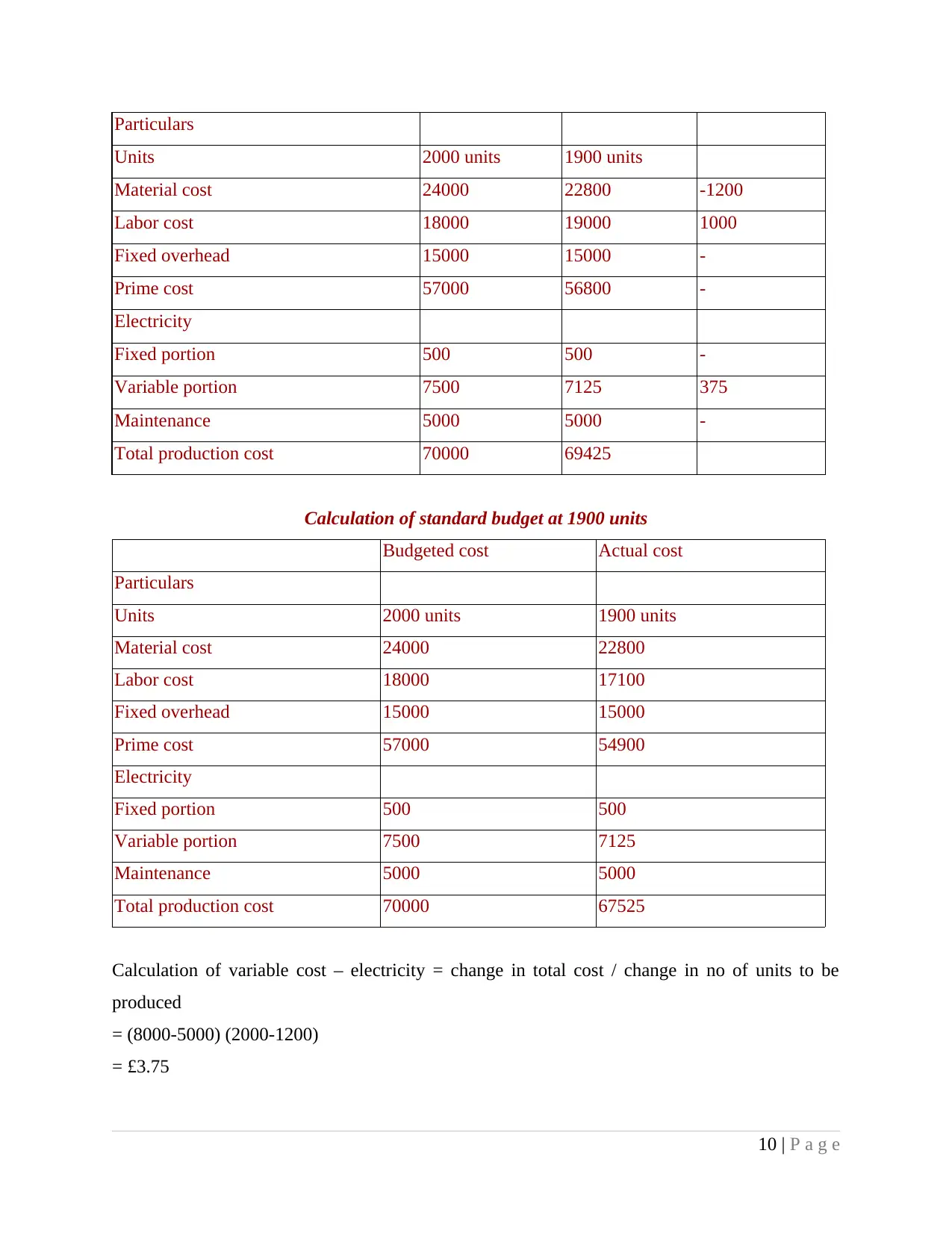

Particulars

Units 2000 units 1900 units

Material cost 24000 22800 -1200

Labor cost 18000 19000 1000

Fixed overhead 15000 15000 -

Prime cost 57000 56800 -

Electricity

Fixed portion 500 500 -

Variable portion 7500 7125 375

Maintenance 5000 5000 -

Total production cost 70000 69425

Calculation of standard budget at 1900 units

Budgeted cost Actual cost

Particulars

Units 2000 units 1900 units

Material cost 24000 22800

Labor cost 18000 17100

Fixed overhead 15000 15000

Prime cost 57000 54900

Electricity

Fixed portion 500 500

Variable portion 7500 7125

Maintenance 5000 5000

Total production cost 70000 67525

Calculation of variable cost – electricity = change in total cost / change in no of units to be

produced

= (8000-5000) (2000-1200)

= £3.75

10 | P a g e

Units 2000 units 1900 units

Material cost 24000 22800 -1200

Labor cost 18000 19000 1000

Fixed overhead 15000 15000 -

Prime cost 57000 56800 -

Electricity

Fixed portion 500 500 -

Variable portion 7500 7125 375

Maintenance 5000 5000 -

Total production cost 70000 69425

Calculation of standard budget at 1900 units

Budgeted cost Actual cost

Particulars

Units 2000 units 1900 units

Material cost 24000 22800

Labor cost 18000 17100

Fixed overhead 15000 15000

Prime cost 57000 54900

Electricity

Fixed portion 500 500

Variable portion 7500 7125

Maintenance 5000 5000

Total production cost 70000 67525

Calculation of variable cost – electricity = change in total cost / change in no of units to be

produced

= (8000-5000) (2000-1200)

= £3.75

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.