Management Accounting Report: Costing and Overhead Analysis

VerifiedAdded on 2022/09/24

|8

|1368

|19

Report

AI Summary

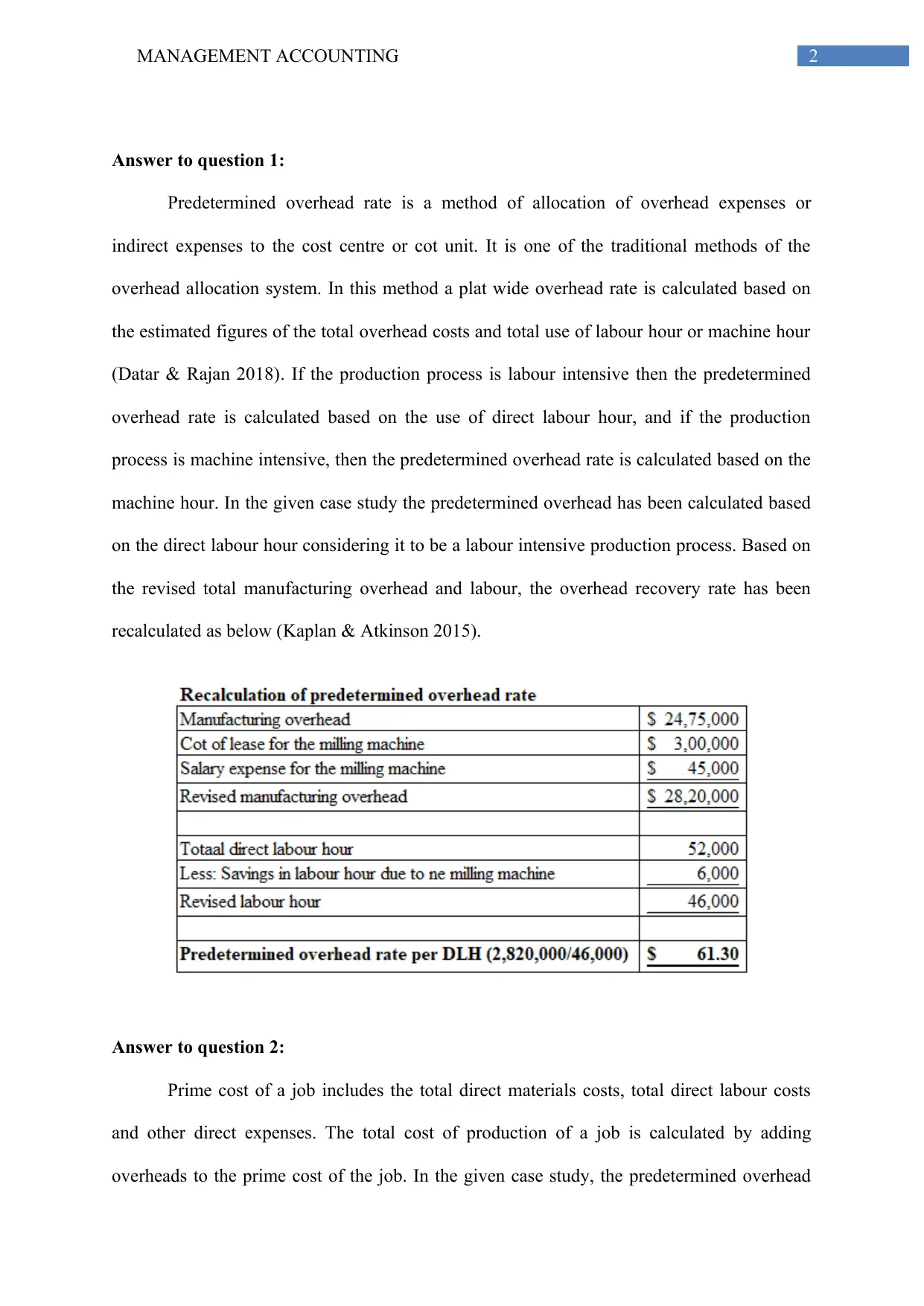

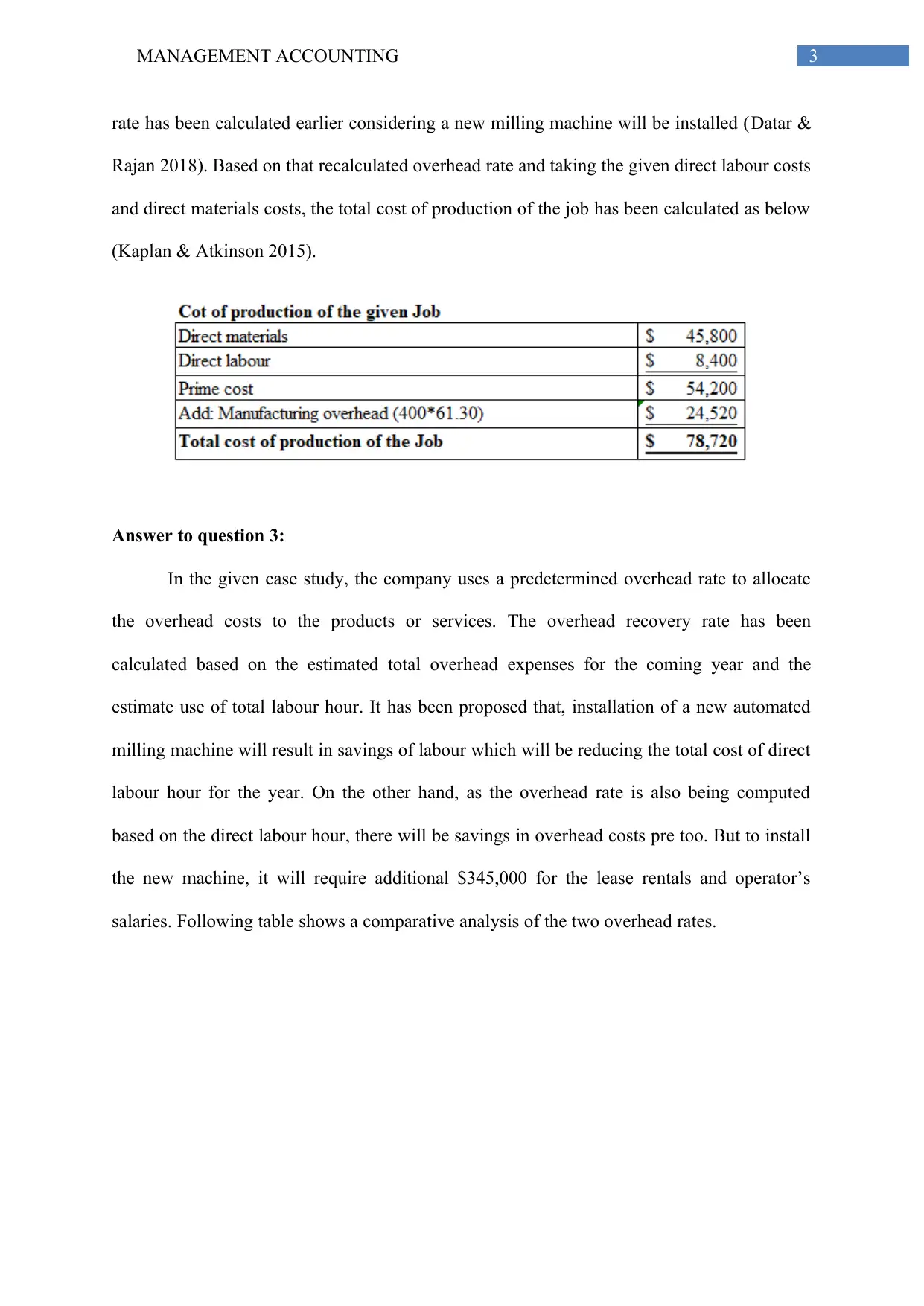

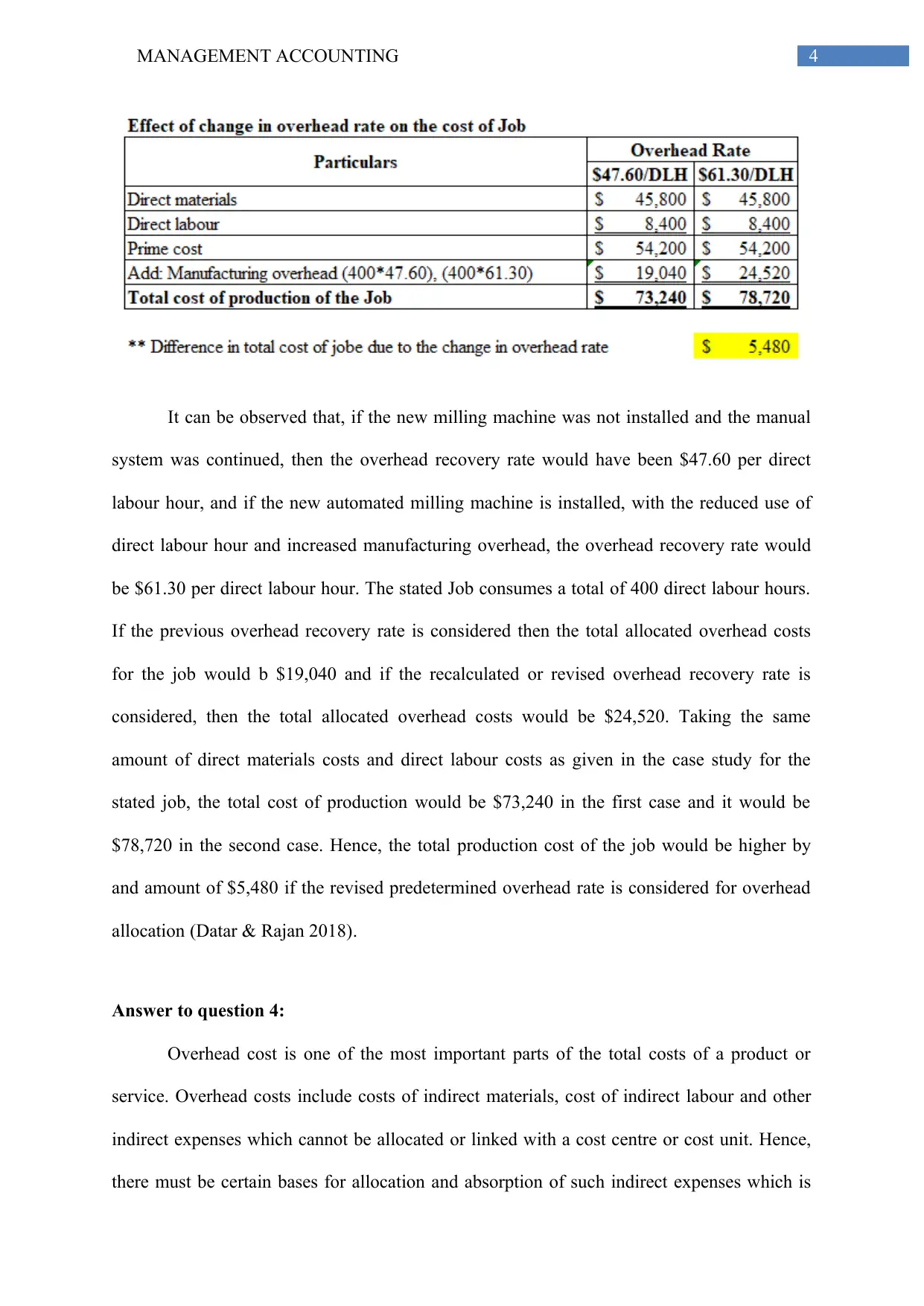

This report analyzes a management accounting case study involving Gibson Fabricators Corporation, which uses a job-order costing system. The report examines the calculation and application of a predetermined overhead rate based on direct labor hours. It explores the impact of installing a new automated milling machine on overhead costs, prime costs, and the total cost of production. The analysis includes a comparative assessment of overhead recovery rates before and after the machine installation, considering factors like direct labor savings and increased overhead expenses. The report emphasizes the importance of managing overhead costs for overall cost minimization and provides recommendations based on the feasibility and cost savings associated with the machine installation, considering scenarios with varying direct labor savings. The report also includes the calculation of prime costs, and the total cost of production of a job, with and without the automated milling machine, highlighting the impact of the overhead rate on the final cost. The report concludes with recommendations on whether to install the machine based on the potential labor savings.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.