Management Accounting Case Study: Earl's Gyms, Galactia & MJA Eng

VerifiedAdded on 2023/06/12

|11

|1371

|144

Case Study

AI Summary

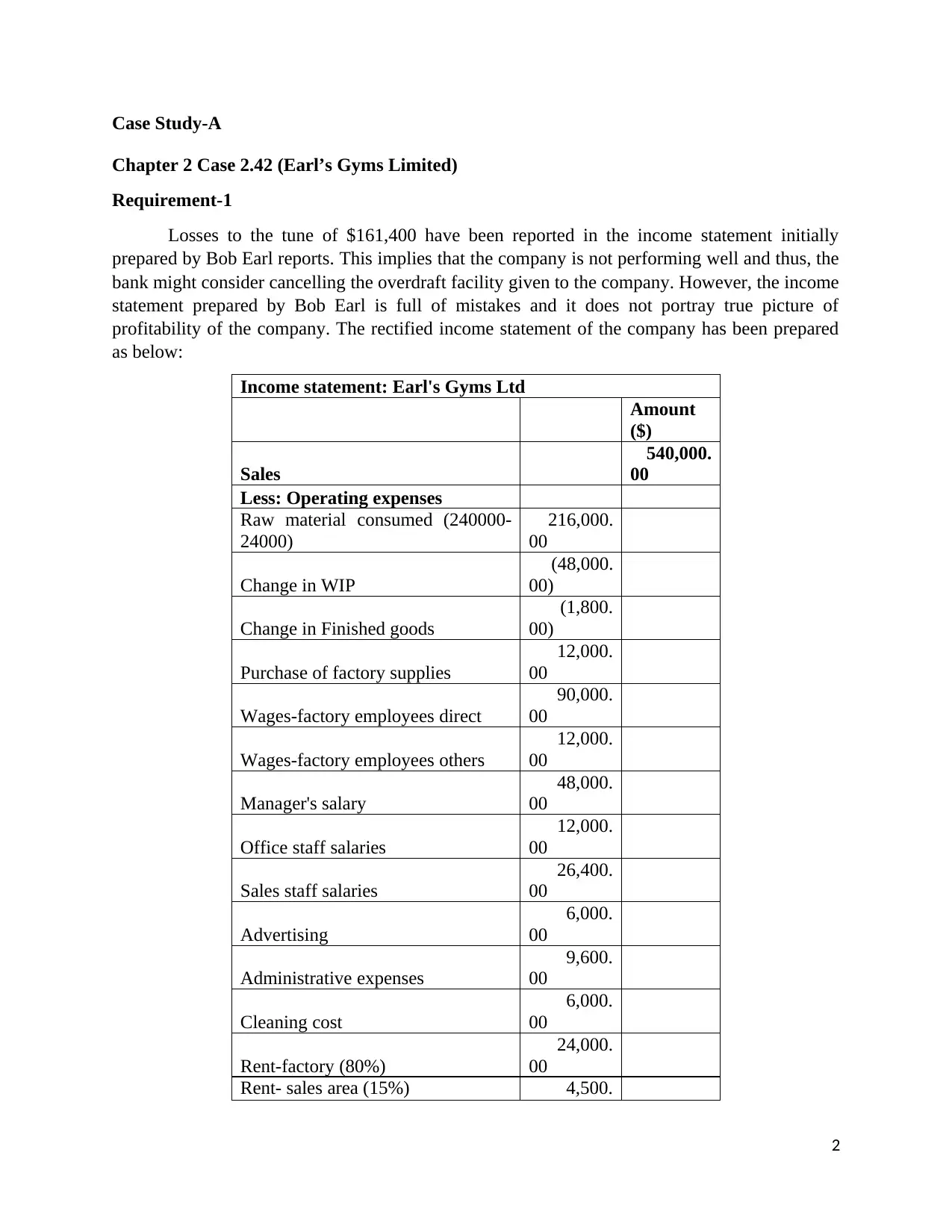

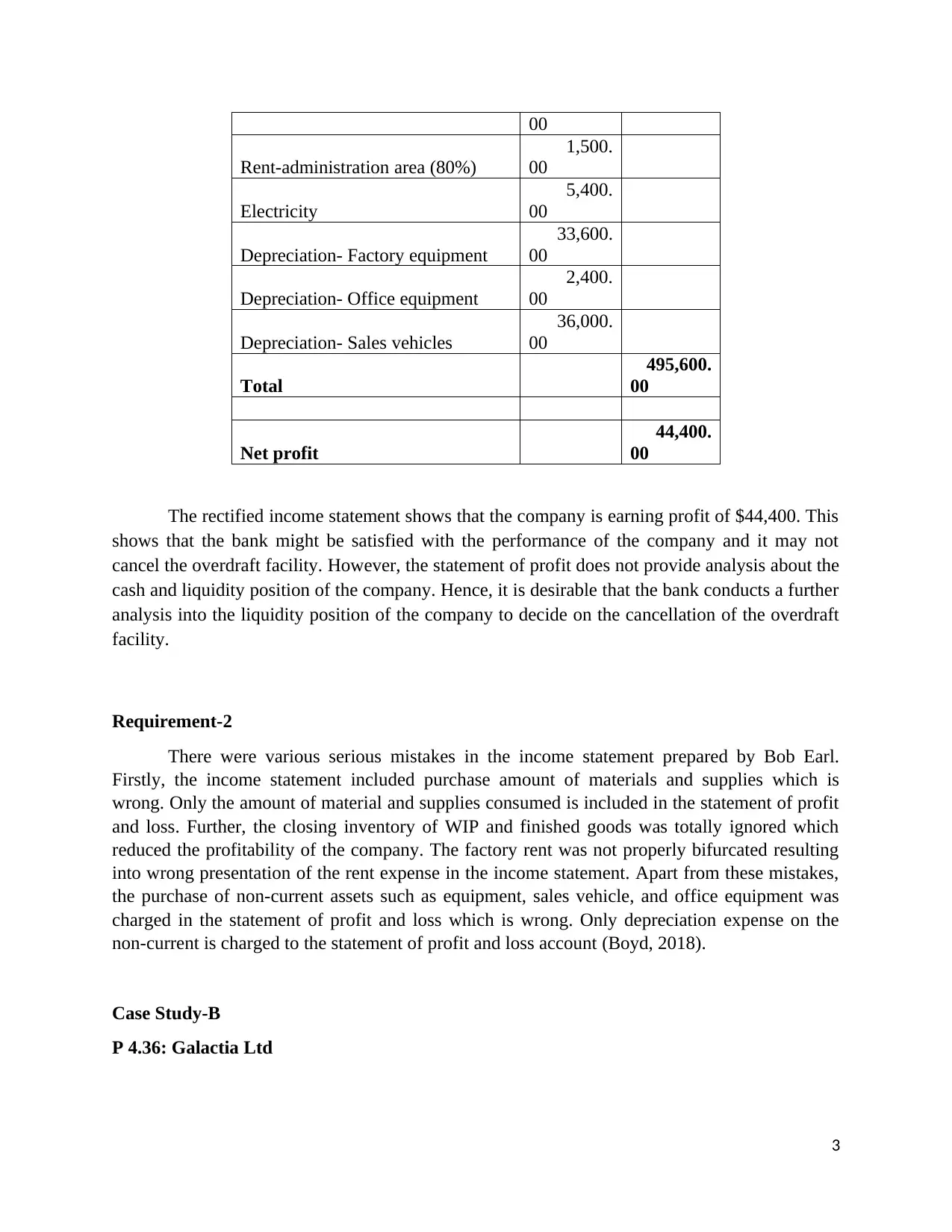

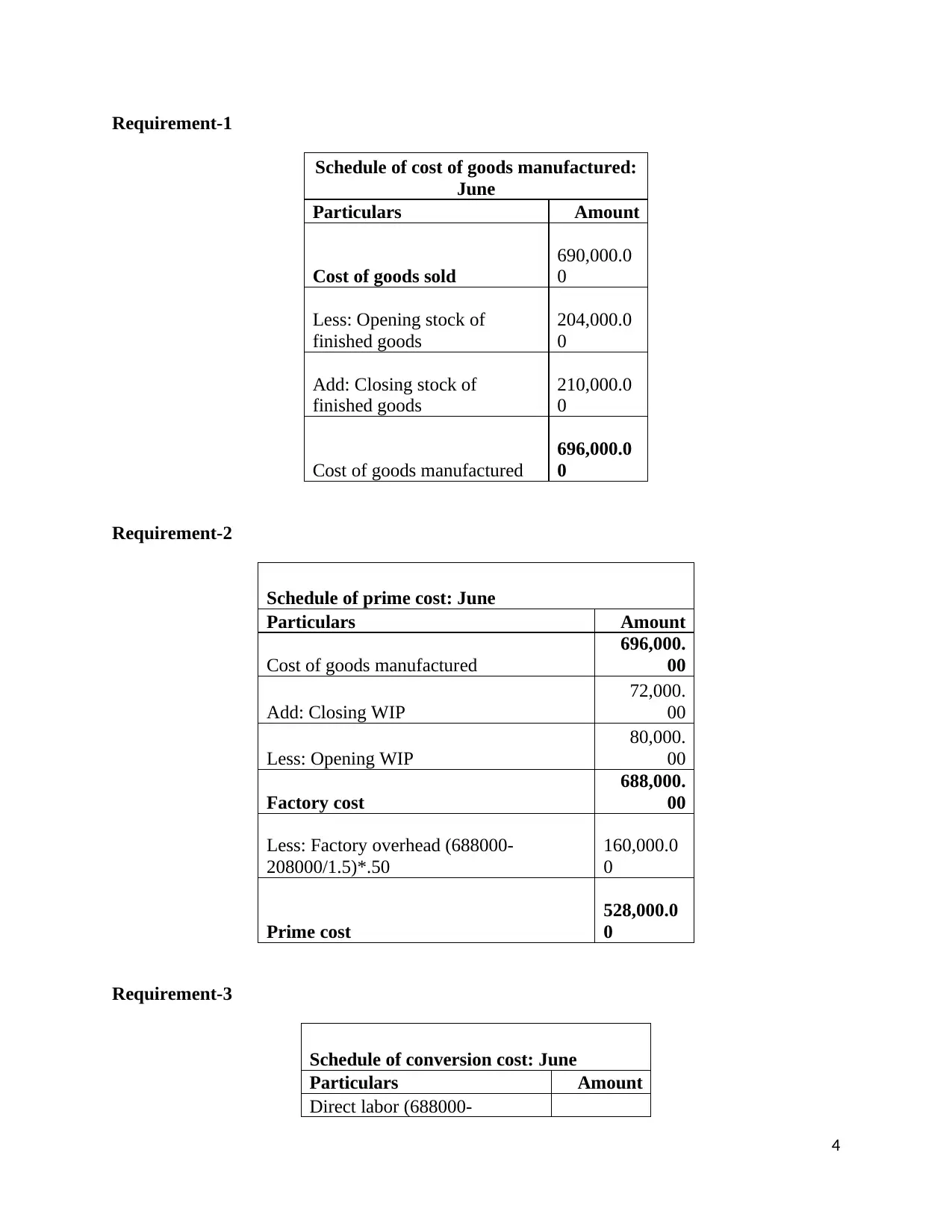

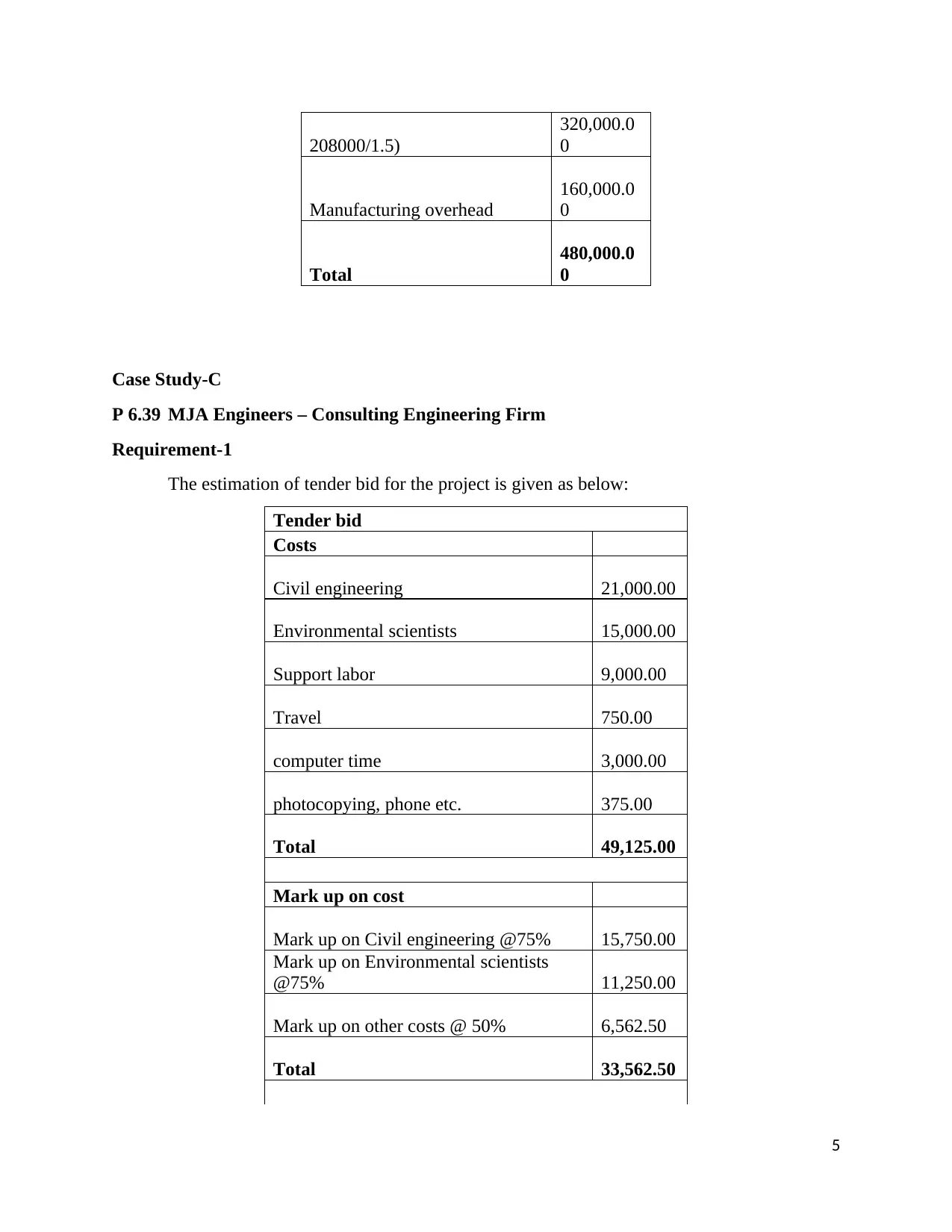

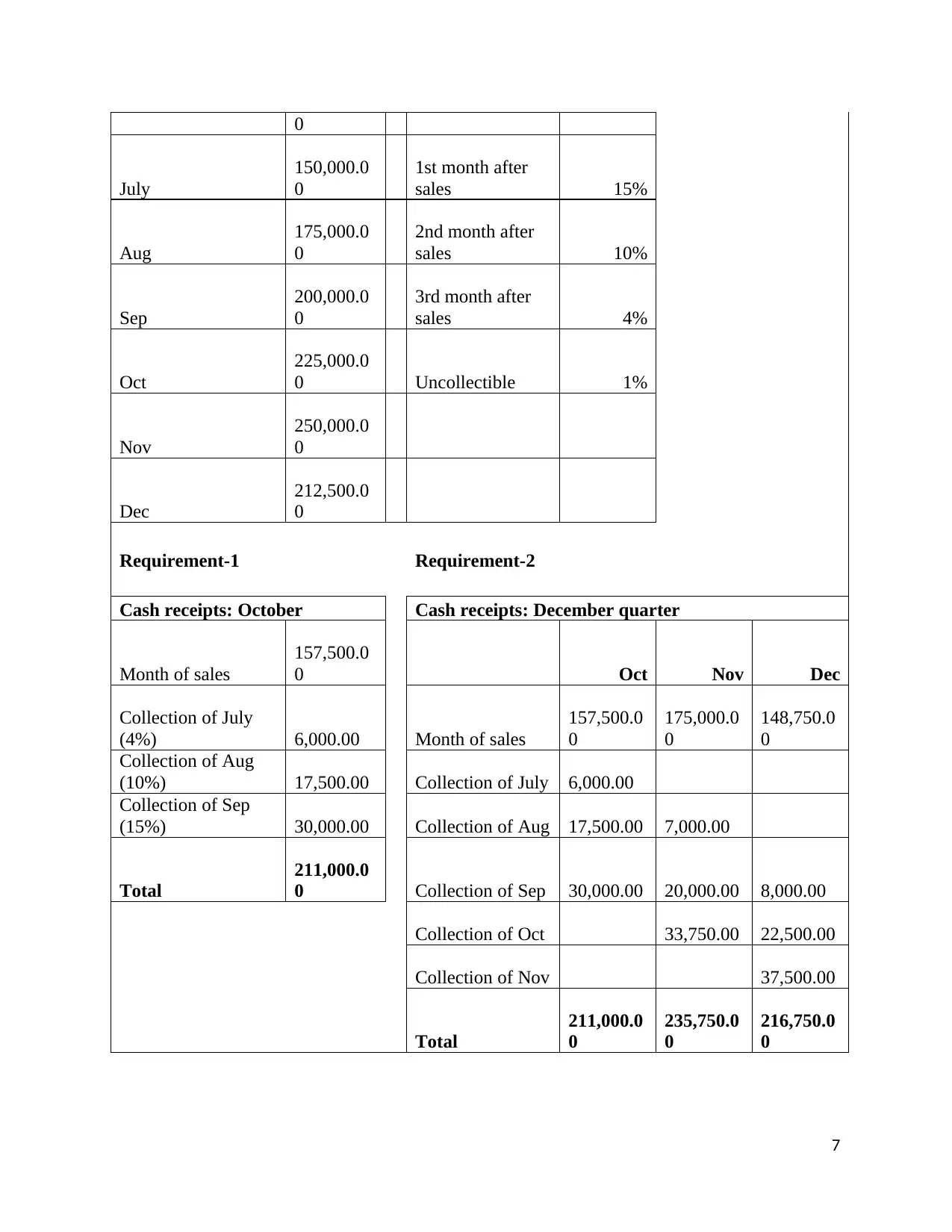

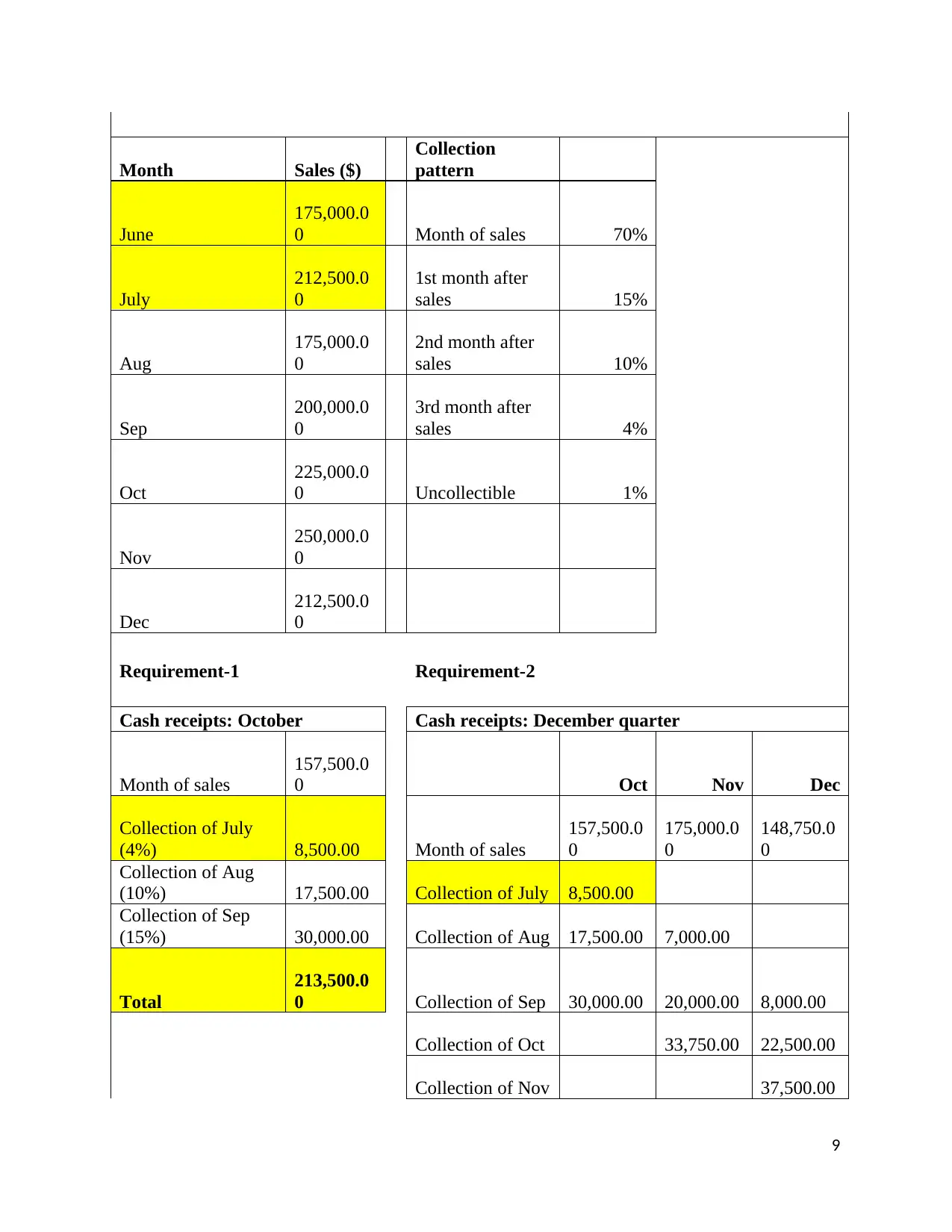

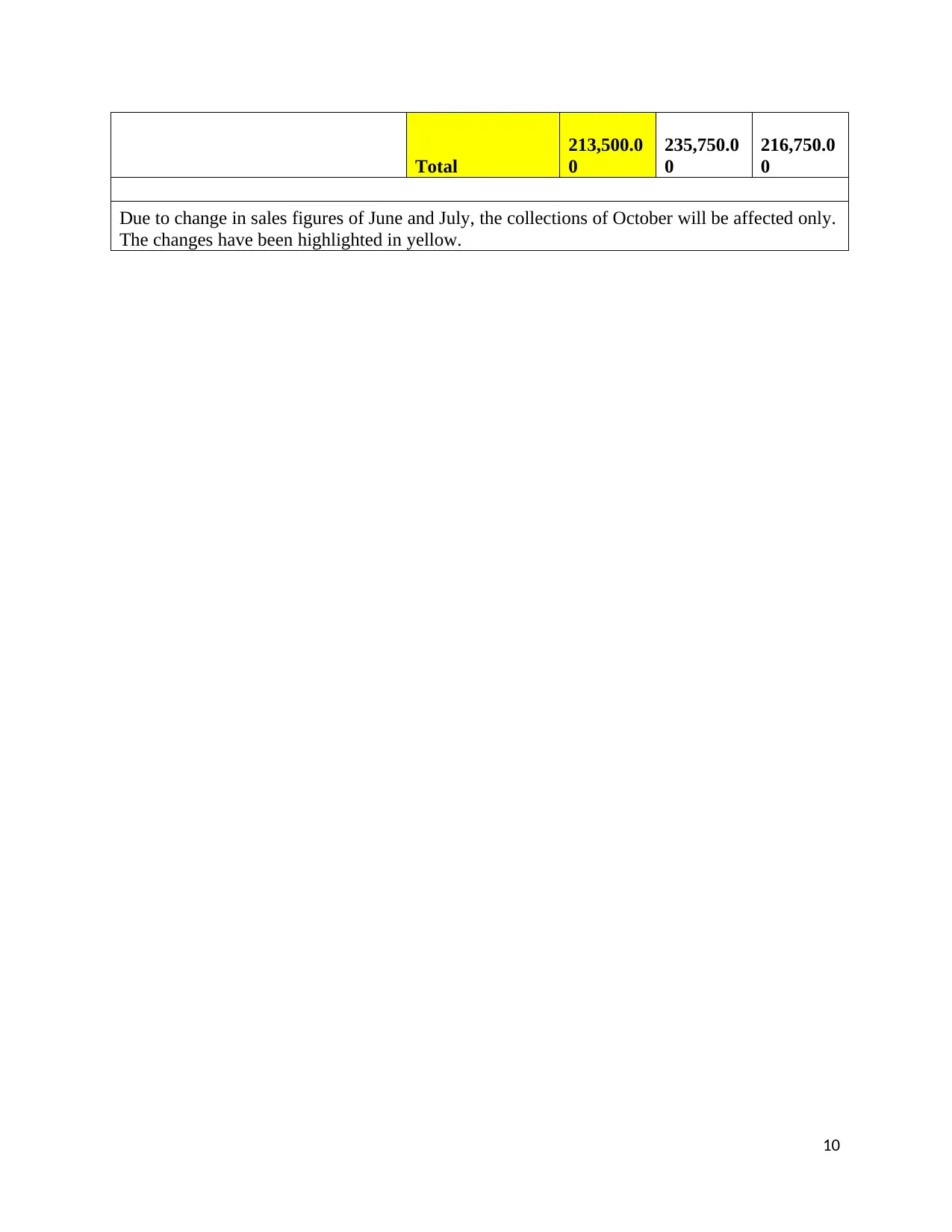

This document presents solutions to several management accounting case studies. It includes a rectified income statement for Earl's Gyms Ltd, demonstrating a profit contrary to initial reports, and analyzes mistakes in the original statement. It also provides schedules for cost of goods manufactured, prime cost, and conversion cost for Galactia Ltd. Furthermore, the document estimates a tender bid for MJA Engineers, highlighting the importance of direct cost tracking. Finally, it addresses cash receipts for a retailer, calculating collections for October and the December quarter. Desklib offers more solved assignments and past papers for students.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.