Management Accounting Assignment: Case Studies and Analysis Report

VerifiedAdded on 2020/04/01

|9

|1167

|51

Homework Assignment

AI Summary

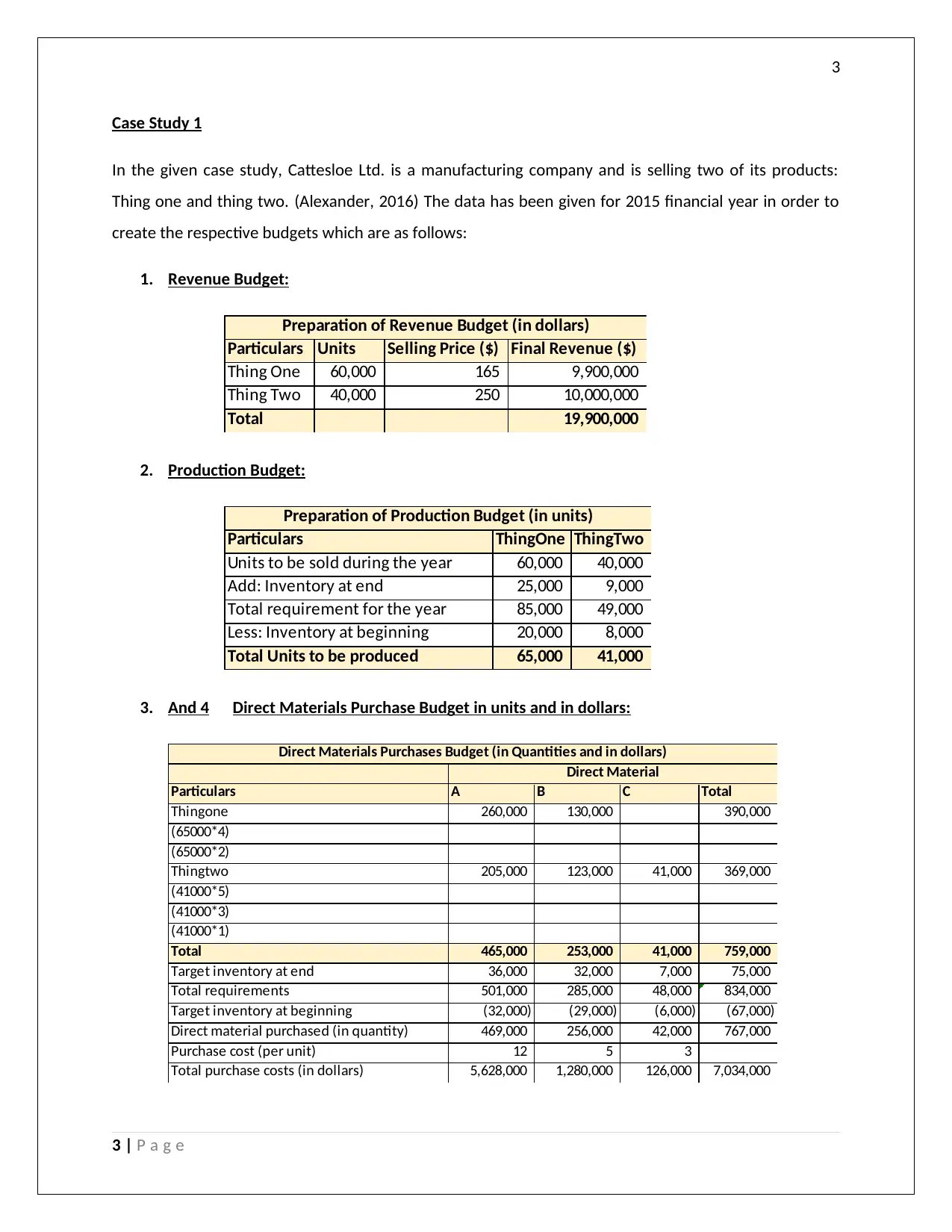

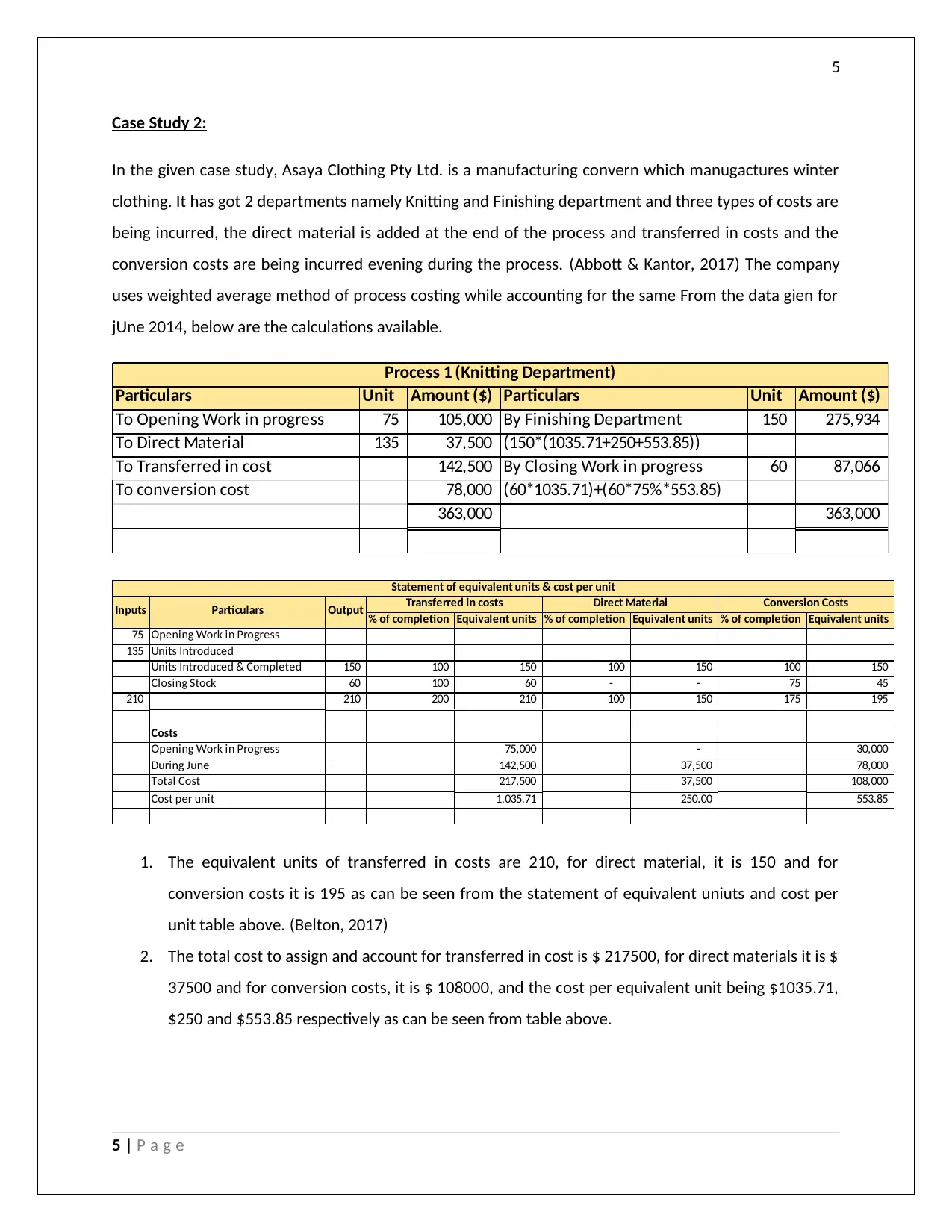

This management accounting assignment presents three case studies, providing practical applications of financial concepts. Case Study 1 focuses on creating revenue, production, and direct materials budgets for a manufacturing company. Case Study 2 delves into process costing using the weighted average method, calculating equivalent units and cost per unit in a knitting and finishing department. Finally, Case Study 3 analyzes a budget hotel, outlining goals, vision, mission, and strategies for success in the competitive hospitality industry, including revenue management, customer satisfaction, and cost control. The assignment includes references to relevant accounting literature.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.