Detailed Management Accounting Report: HLW Case Study Analysis

VerifiedAdded on 2020/05/16

|15

|3328

|207

Report

AI Summary

This comprehensive report provides a detailed analysis of a management accounting case study, focusing on the financial performance of HLW. The report begins with an executive summary outlining the key objectives and findings, followed by a table of contents for easy navigation. Part A of the report delves into cost accounting, including activity-based costing, overhead cost analysis, and the distinction between direct and indirect costs. Part B examines HLW's revenue streams, comparing current and proposed membership plans, and assessing the impact on sales revenue and cash flow. The analysis includes detailed calculations of sales revenue under different scenarios, incorporating assumptions about court usage and membership uptake. The report concludes with a summary of findings, highlighting the benefits of implementing the new membership plans and their potential to improve financial performance. The report emphasizes the importance of management accounting in making informed financial decisions and projecting future profitability. The report provides an in-depth analysis of financial data, cost structures, and revenue strategies, offering valuable insights into the management accounting practices of the company.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Management Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Executive summary:

The concept of management accounting or the managerial accounting enables the managers

to make use of the provisions of accounting information to better obtain the information in

the betterment of the internal organization. The concept of management accounting helps in

serving as the internal control for the better performance of the management functions. One

of the important factors of management accounting is relating to the provision of financial

and non-financial decisions making procedure of the firm to provide the management with

the better information. The concept of management accounting enables the management

accountant to consider the events that takes during the normal course of business by taking

into the considerations the requirements of the business.

The primary objective of the management accounting is to help in projecting the future

anticipated profits and undertaking the necessary decisions of either making or purchasing.

The current case study takes into the considerations the explanation of the two methods

namely the management accounting and cost accounting by assessing the future cash flow

analysis from the implementation of the new plans. The initial phase of the study is

associated with the determination of the overhead costs and determining the product cost

thereafter. The later part of the case study is associated with the determination of the analysis

of the cash flow in order to determine the potential benefit of the new plans.

Executive summary:

The concept of management accounting or the managerial accounting enables the managers

to make use of the provisions of accounting information to better obtain the information in

the betterment of the internal organization. The concept of management accounting helps in

serving as the internal control for the better performance of the management functions. One

of the important factors of management accounting is relating to the provision of financial

and non-financial decisions making procedure of the firm to provide the management with

the better information. The concept of management accounting enables the management

accountant to consider the events that takes during the normal course of business by taking

into the considerations the requirements of the business.

The primary objective of the management accounting is to help in projecting the future

anticipated profits and undertaking the necessary decisions of either making or purchasing.

The current case study takes into the considerations the explanation of the two methods

namely the management accounting and cost accounting by assessing the future cash flow

analysis from the implementation of the new plans. The initial phase of the study is

associated with the determination of the overhead costs and determining the product cost

thereafter. The later part of the case study is associated with the determination of the analysis

of the cash flow in order to determine the potential benefit of the new plans.

2MANAGEMENT ACCOUNTING

Table of Contents

Answer to Part A:.......................................................................................................................3

Answer to requirement 1:...........................................................................................................3

Answer to requirement B:..........................................................................................................3

Answer to requirement C:..........................................................................................................4

Answer to Part B:.......................................................................................................................5

Answer to requirement A:..........................................................................................................5

Answer to requirement 2:...........................................................................................................6

Sales revenue in the present plan:..............................................................................................7

Sales revenue presented under the presented plans of membership:.........................................8

Answer to requirement 3:.........................................................................................................10

Conclusion:..............................................................................................................................11

Reference List:.........................................................................................................................13

Table of Contents

Answer to Part A:.......................................................................................................................3

Answer to requirement 1:...........................................................................................................3

Answer to requirement B:..........................................................................................................3

Answer to requirement C:..........................................................................................................4

Answer to Part B:.......................................................................................................................5

Answer to requirement A:..........................................................................................................5

Answer to requirement 2:...........................................................................................................6

Sales revenue in the present plan:..............................................................................................7

Sales revenue presented under the presented plans of membership:.........................................8

Answer to requirement 3:.........................................................................................................10

Conclusion:..............................................................................................................................11

Reference List:.........................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

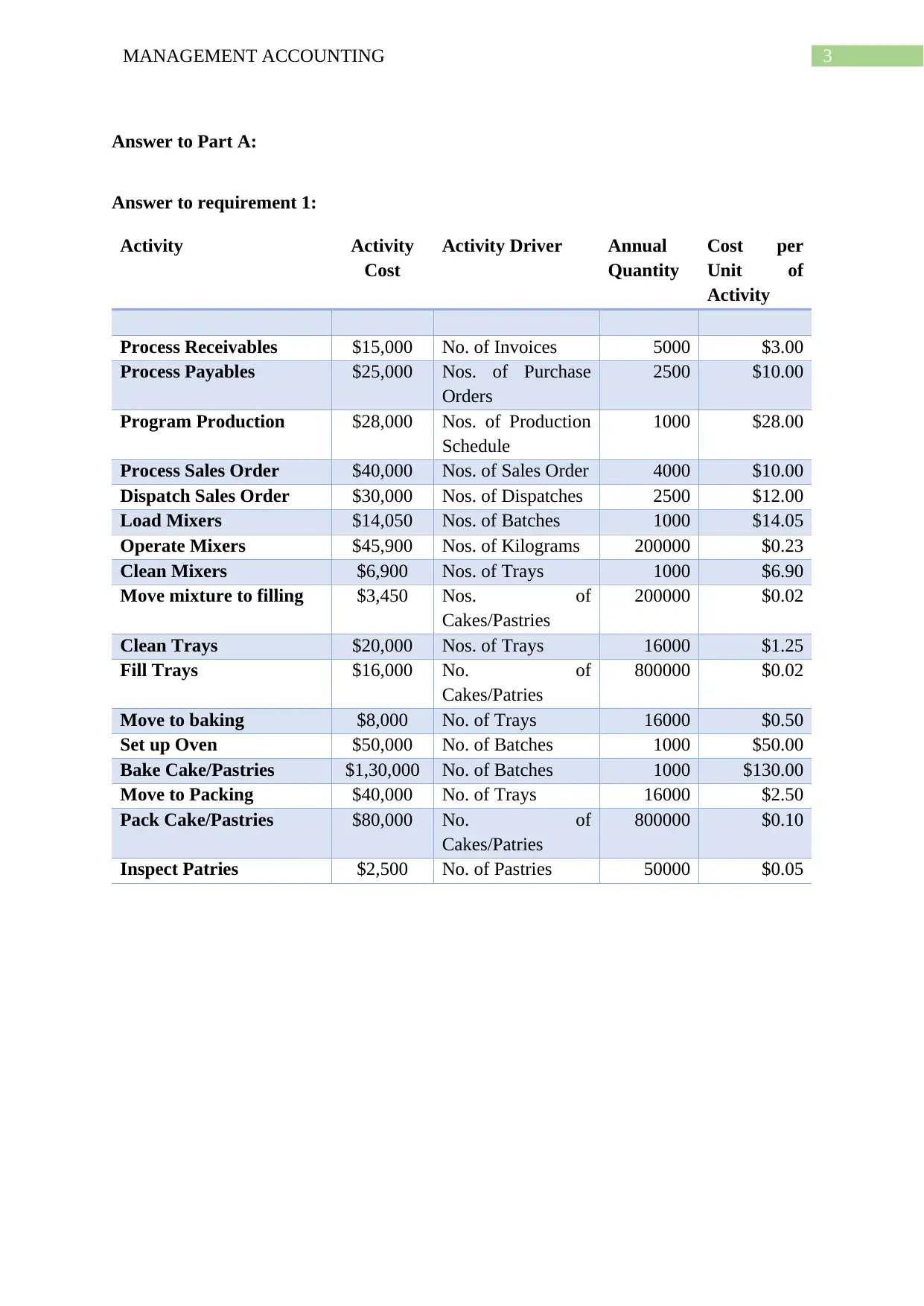

Answer to Part A:

Answer to requirement 1:

Activity Activity

Cost

Activity Driver Annual

Quantity

Cost per

Unit of

Activity

Process Receivables $15,000 No. of Invoices 5000 $3.00

Process Payables $25,000 Nos. of Purchase

Orders

2500 $10.00

Program Production $28,000 Nos. of Production

Schedule

1000 $28.00

Process Sales Order $40,000 Nos. of Sales Order 4000 $10.00

Dispatch Sales Order $30,000 Nos. of Dispatches 2500 $12.00

Load Mixers $14,050 Nos. of Batches 1000 $14.05

Operate Mixers $45,900 Nos. of Kilograms 200000 $0.23

Clean Mixers $6,900 Nos. of Trays 1000 $6.90

Move mixture to filling $3,450 Nos. of

Cakes/Pastries

200000 $0.02

Clean Trays $20,000 Nos. of Trays 16000 $1.25

Fill Trays $16,000 No. of

Cakes/Patries

800000 $0.02

Move to baking $8,000 No. of Trays 16000 $0.50

Set up Oven $50,000 No. of Batches 1000 $50.00

Bake Cake/Pastries $1,30,000 No. of Batches 1000 $130.00

Move to Packing $40,000 No. of Trays 16000 $2.50

Pack Cake/Pastries $80,000 No. of

Cakes/Patries

800000 $0.10

Inspect Patries $2,500 No. of Pastries 50000 $0.05

Answer to Part A:

Answer to requirement 1:

Activity Activity

Cost

Activity Driver Annual

Quantity

Cost per

Unit of

Activity

Process Receivables $15,000 No. of Invoices 5000 $3.00

Process Payables $25,000 Nos. of Purchase

Orders

2500 $10.00

Program Production $28,000 Nos. of Production

Schedule

1000 $28.00

Process Sales Order $40,000 Nos. of Sales Order 4000 $10.00

Dispatch Sales Order $30,000 Nos. of Dispatches 2500 $12.00

Load Mixers $14,050 Nos. of Batches 1000 $14.05

Operate Mixers $45,900 Nos. of Kilograms 200000 $0.23

Clean Mixers $6,900 Nos. of Trays 1000 $6.90

Move mixture to filling $3,450 Nos. of

Cakes/Pastries

200000 $0.02

Clean Trays $20,000 Nos. of Trays 16000 $1.25

Fill Trays $16,000 No. of

Cakes/Patries

800000 $0.02

Move to baking $8,000 No. of Trays 16000 $0.50

Set up Oven $50,000 No. of Batches 1000 $50.00

Bake Cake/Pastries $1,30,000 No. of Batches 1000 $130.00

Move to Packing $40,000 No. of Trays 16000 $2.50

Pack Cake/Pastries $80,000 No. of

Cakes/Patries

800000 $0.10

Inspect Patries $2,500 No. of Pastries 50000 $0.05

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

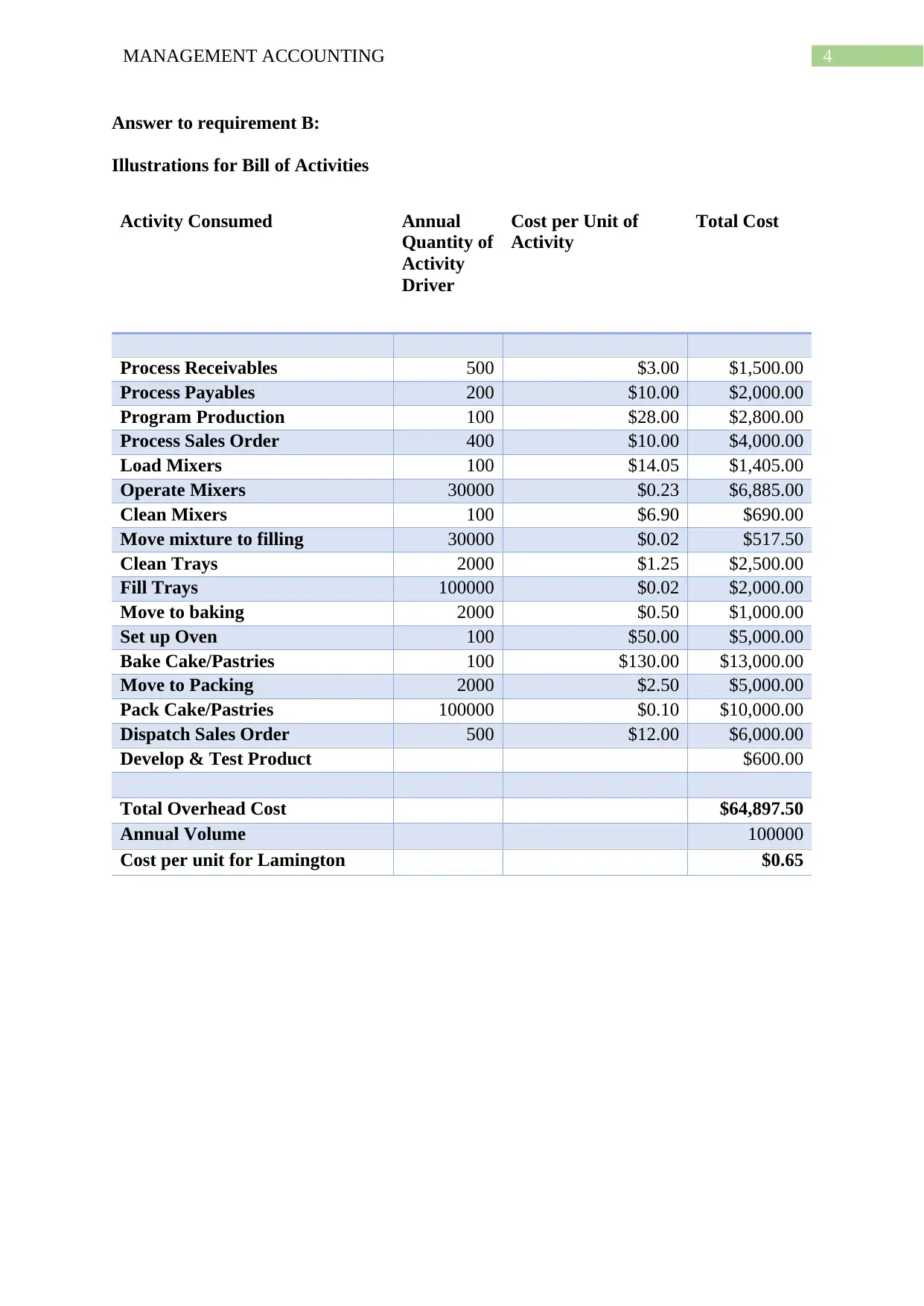

Answer to requirement B:

Illustrations for Bill of Activities

Activity Consumed Annual

Quantity of

Activity

Driver

Cost per Unit of

Activity

Total Cost

Process Receivables 500 $3.00 $1,500.00

Process Payables 200 $10.00 $2,000.00

Program Production 100 $28.00 $2,800.00

Process Sales Order 400 $10.00 $4,000.00

Load Mixers 100 $14.05 $1,405.00

Operate Mixers 30000 $0.23 $6,885.00

Clean Mixers 100 $6.90 $690.00

Move mixture to filling 30000 $0.02 $517.50

Clean Trays 2000 $1.25 $2,500.00

Fill Trays 100000 $0.02 $2,000.00

Move to baking 2000 $0.50 $1,000.00

Set up Oven 100 $50.00 $5,000.00

Bake Cake/Pastries 100 $130.00 $13,000.00

Move to Packing 2000 $2.50 $5,000.00

Pack Cake/Pastries 100000 $0.10 $10,000.00

Dispatch Sales Order 500 $12.00 $6,000.00

Develop & Test Product $600.00

Total Overhead Cost $64,897.50

Annual Volume 100000

Cost per unit for Lamington $0.65

Answer to requirement B:

Illustrations for Bill of Activities

Activity Consumed Annual

Quantity of

Activity

Driver

Cost per Unit of

Activity

Total Cost

Process Receivables 500 $3.00 $1,500.00

Process Payables 200 $10.00 $2,000.00

Program Production 100 $28.00 $2,800.00

Process Sales Order 400 $10.00 $4,000.00

Load Mixers 100 $14.05 $1,405.00

Operate Mixers 30000 $0.23 $6,885.00

Clean Mixers 100 $6.90 $690.00

Move mixture to filling 30000 $0.02 $517.50

Clean Trays 2000 $1.25 $2,500.00

Fill Trays 100000 $0.02 $2,000.00

Move to baking 2000 $0.50 $1,000.00

Set up Oven 100 $50.00 $5,000.00

Bake Cake/Pastries 100 $130.00 $13,000.00

Move to Packing 2000 $2.50 $5,000.00

Pack Cake/Pastries 100000 $0.10 $10,000.00

Dispatch Sales Order 500 $12.00 $6,000.00

Develop & Test Product $600.00

Total Overhead Cost $64,897.50

Annual Volume 100000

Cost per unit for Lamington $0.65

5MANAGEMENT ACCOUNTING

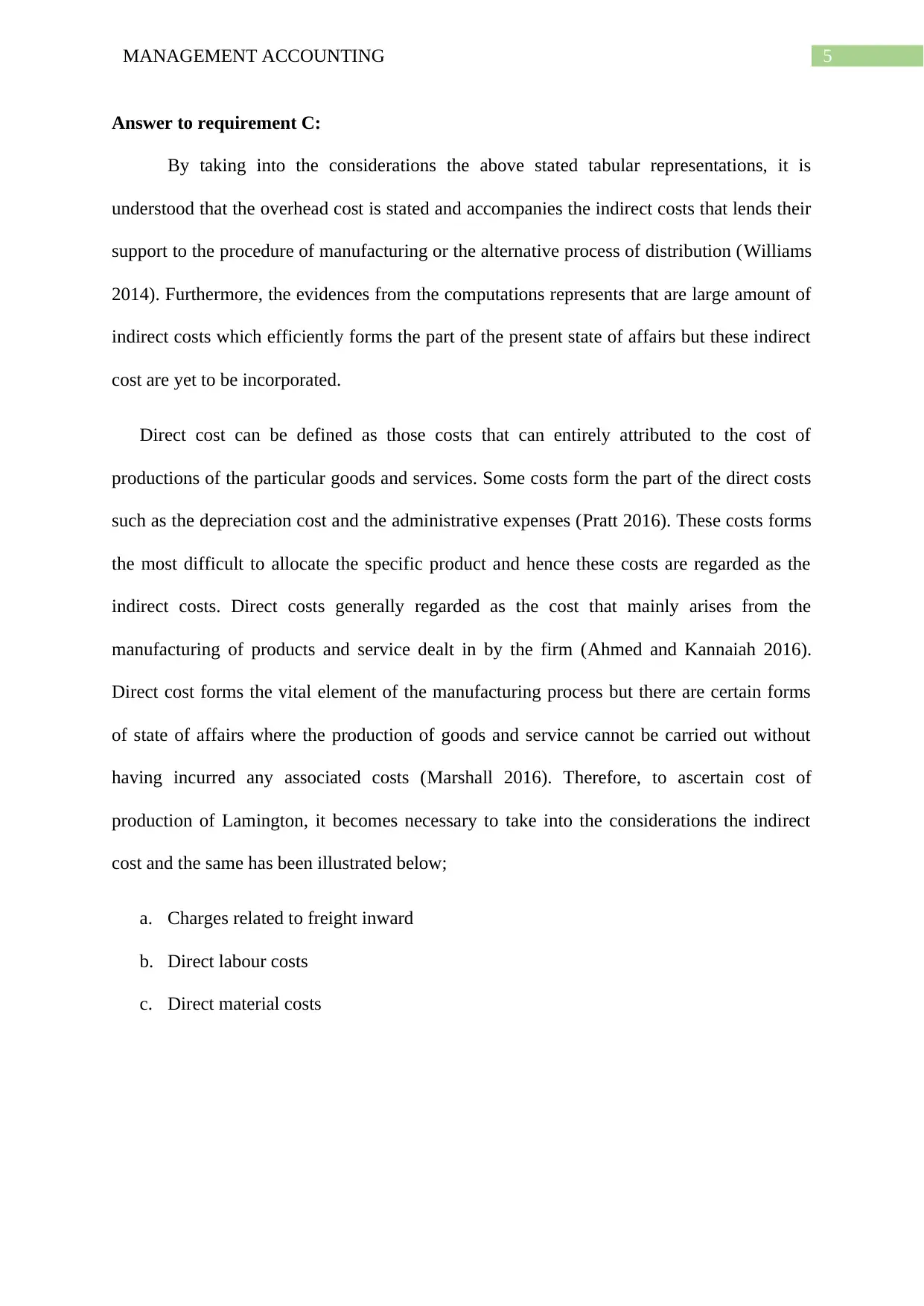

Answer to requirement C:

By taking into the considerations the above stated tabular representations, it is

understood that the overhead cost is stated and accompanies the indirect costs that lends their

support to the procedure of manufacturing or the alternative process of distribution (Williams

2014). Furthermore, the evidences from the computations represents that are large amount of

indirect costs which efficiently forms the part of the present state of affairs but these indirect

cost are yet to be incorporated.

Direct cost can be defined as those costs that can entirely attributed to the cost of

productions of the particular goods and services. Some costs form the part of the direct costs

such as the depreciation cost and the administrative expenses (Pratt 2016). These costs forms

the most difficult to allocate the specific product and hence these costs are regarded as the

indirect costs. Direct costs generally regarded as the cost that mainly arises from the

manufacturing of products and service dealt in by the firm (Ahmed and Kannaiah 2016).

Direct cost forms the vital element of the manufacturing process but there are certain forms

of state of affairs where the production of goods and service cannot be carried out without

having incurred any associated costs (Marshall 2016). Therefore, to ascertain cost of

production of Lamington, it becomes necessary to take into the considerations the indirect

cost and the same has been illustrated below;

a. Charges related to freight inward

b. Direct labour costs

c. Direct material costs

Answer to requirement C:

By taking into the considerations the above stated tabular representations, it is

understood that the overhead cost is stated and accompanies the indirect costs that lends their

support to the procedure of manufacturing or the alternative process of distribution (Williams

2014). Furthermore, the evidences from the computations represents that are large amount of

indirect costs which efficiently forms the part of the present state of affairs but these indirect

cost are yet to be incorporated.

Direct cost can be defined as those costs that can entirely attributed to the cost of

productions of the particular goods and services. Some costs form the part of the direct costs

such as the depreciation cost and the administrative expenses (Pratt 2016). These costs forms

the most difficult to allocate the specific product and hence these costs are regarded as the

indirect costs. Direct costs generally regarded as the cost that mainly arises from the

manufacturing of products and service dealt in by the firm (Ahmed and Kannaiah 2016).

Direct cost forms the vital element of the manufacturing process but there are certain forms

of state of affairs where the production of goods and service cannot be carried out without

having incurred any associated costs (Marshall 2016). Therefore, to ascertain cost of

production of Lamington, it becomes necessary to take into the considerations the indirect

cost and the same has been illustrated below;

a. Charges related to freight inward

b. Direct labour costs

c. Direct material costs

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

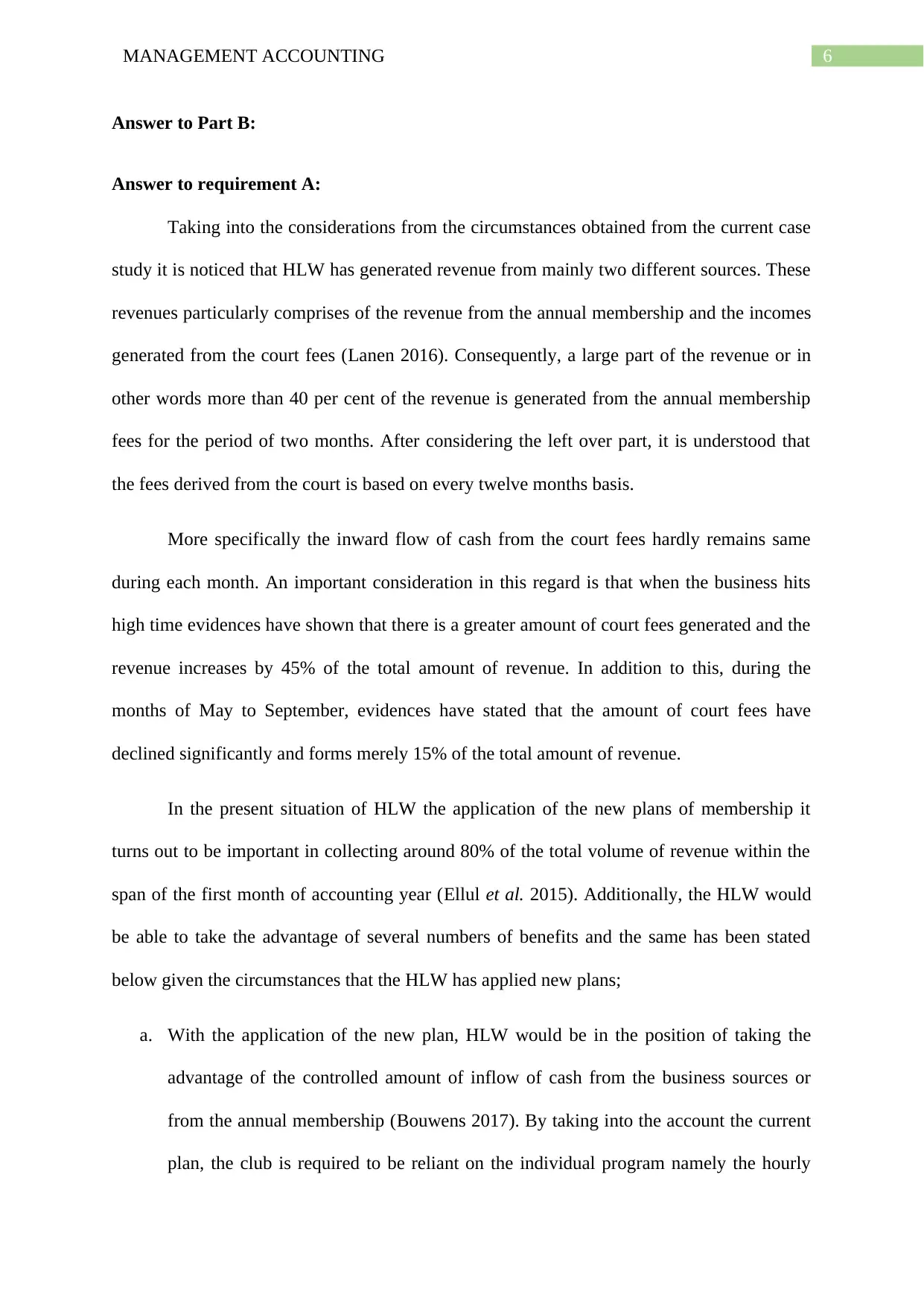

Answer to Part B:

Answer to requirement A:

Taking into the considerations from the circumstances obtained from the current case

study it is noticed that HLW has generated revenue from mainly two different sources. These

revenues particularly comprises of the revenue from the annual membership and the incomes

generated from the court fees (Lanen 2016). Consequently, a large part of the revenue or in

other words more than 40 per cent of the revenue is generated from the annual membership

fees for the period of two months. After considering the left over part, it is understood that

the fees derived from the court is based on every twelve months basis.

More specifically the inward flow of cash from the court fees hardly remains same

during each month. An important consideration in this regard is that when the business hits

high time evidences have shown that there is a greater amount of court fees generated and the

revenue increases by 45% of the total amount of revenue. In addition to this, during the

months of May to September, evidences have stated that the amount of court fees have

declined significantly and forms merely 15% of the total amount of revenue.

In the present situation of HLW the application of the new plans of membership it

turns out to be important in collecting around 80% of the total volume of revenue within the

span of the first month of accounting year (Ellul et al. 2015). Additionally, the HLW would

be able to take the advantage of several numbers of benefits and the same has been stated

below given the circumstances that the HLW has applied new plans;

a. With the application of the new plan, HLW would be in the position of taking the

advantage of the controlled amount of inflow of cash from the business sources or

from the annual membership (Bouwens 2017). By taking into the account the current

plan, the club is required to be reliant on the individual program namely the hourly

Answer to Part B:

Answer to requirement A:

Taking into the considerations from the circumstances obtained from the current case

study it is noticed that HLW has generated revenue from mainly two different sources. These

revenues particularly comprises of the revenue from the annual membership and the incomes

generated from the court fees (Lanen 2016). Consequently, a large part of the revenue or in

other words more than 40 per cent of the revenue is generated from the annual membership

fees for the period of two months. After considering the left over part, it is understood that

the fees derived from the court is based on every twelve months basis.

More specifically the inward flow of cash from the court fees hardly remains same

during each month. An important consideration in this regard is that when the business hits

high time evidences have shown that there is a greater amount of court fees generated and the

revenue increases by 45% of the total amount of revenue. In addition to this, during the

months of May to September, evidences have stated that the amount of court fees have

declined significantly and forms merely 15% of the total amount of revenue.

In the present situation of HLW the application of the new plans of membership it

turns out to be important in collecting around 80% of the total volume of revenue within the

span of the first month of accounting year (Ellul et al. 2015). Additionally, the HLW would

be able to take the advantage of several numbers of benefits and the same has been stated

below given the circumstances that the HLW has applied new plans;

a. With the application of the new plan, HLW would be in the position of taking the

advantage of the controlled amount of inflow of cash from the business sources or

from the annual membership (Bouwens 2017). By taking into the account the current

plan, the club is required to be reliant on the individual program namely the hourly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

fees charged by the court for generating greater than 50% of the total amount of

incomes.

b. With the implementation of the new plans, it would provide HLW would with the

greater amount of benefit for HLW. This is because it would provide HLW with the

preparation of platform that would assist the club in generating the stable amount of

inflow of cash during every of business operations (Angelopoulos and Pollalis 2017).

c. The application of new plan for the HLW would help in providing additional amount

of benefit because the management of the club is better able to accumulate revenue

which would be 80% greater than total amount of revenue derived during the early

phases of business operations (Schaltegger and Zvezdov 2015). The application of the

new plans ultimately lends the path for HLW in making an appropriate use of the

funds that is accumulated together with the considerations made for different forms of

financial decisions undertaken.

Answer to requirement 2:

Evidences obtained from the current case study suggest that there are several

highlighted issues and consequently there are some assumptions that is necessary required to

be made in getting the better understanding of the effect created from the new plans of

membership sales. There are certain listed assumptions in this regard and the same is stated

below;

a. The should be a full usage of court be made during the hours when the business hits

the peak time

b. Considerations should be made regarding 60% of the total usage capacity when the

business goes through the non-peak time

c. Additionally, it is necessary to make use of 40% of the total court during the lean time

fees charged by the court for generating greater than 50% of the total amount of

incomes.

b. With the implementation of the new plans, it would provide HLW would with the

greater amount of benefit for HLW. This is because it would provide HLW with the

preparation of platform that would assist the club in generating the stable amount of

inflow of cash during every of business operations (Angelopoulos and Pollalis 2017).

c. The application of new plan for the HLW would help in providing additional amount

of benefit because the management of the club is better able to accumulate revenue

which would be 80% greater than total amount of revenue derived during the early

phases of business operations (Schaltegger and Zvezdov 2015). The application of the

new plans ultimately lends the path for HLW in making an appropriate use of the

funds that is accumulated together with the considerations made for different forms of

financial decisions undertaken.

Answer to requirement 2:

Evidences obtained from the current case study suggest that there are several

highlighted issues and consequently there are some assumptions that is necessary required to

be made in getting the better understanding of the effect created from the new plans of

membership sales. There are certain listed assumptions in this regard and the same is stated

below;

a. The should be a full usage of court be made during the hours when the business hits

the peak time

b. Considerations should be made regarding 60% of the total usage capacity when the

business goes through the non-peak time

c. Additionally, it is necessary to make use of 40% of the total court during the lean time

8MANAGEMENT ACCOUNTING

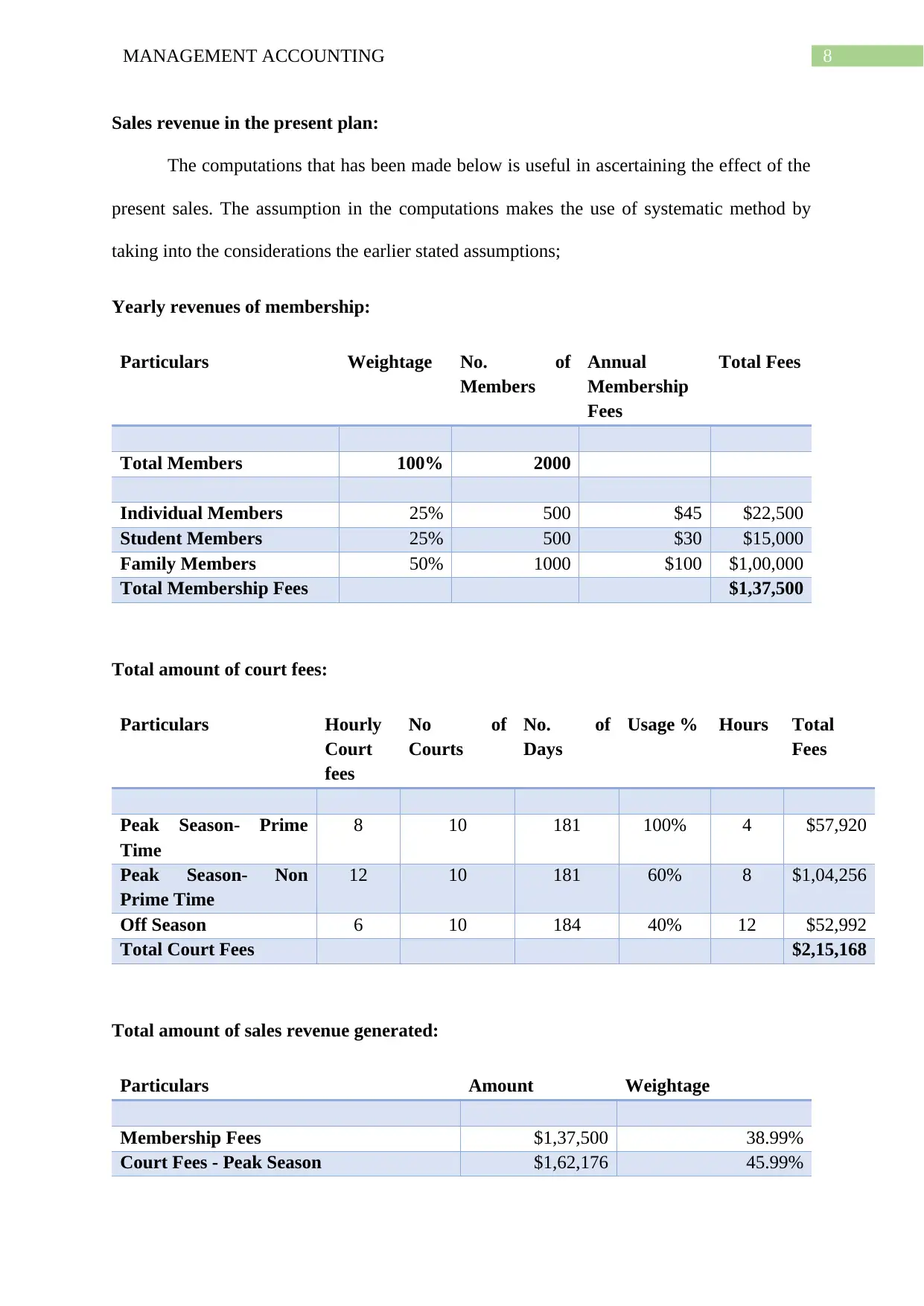

Sales revenue in the present plan:

The computations that has been made below is useful in ascertaining the effect of the

present sales. The assumption in the computations makes the use of systematic method by

taking into the considerations the earlier stated assumptions;

Yearly revenues of membership:

Particulars Weightage No. of

Members

Annual

Membership

Fees

Total Fees

Total Members 100% 2000

Individual Members 25% 500 $45 $22,500

Student Members 25% 500 $30 $15,000

Family Members 50% 1000 $100 $1,00,000

Total Membership Fees $1,37,500

Total amount of court fees:

Particulars Hourly

Court

fees

No of

Courts

No. of

Days

Usage % Hours Total

Fees

Peak Season- Prime

Time

8 10 181 100% 4 $57,920

Peak Season- Non

Prime Time

12 10 181 60% 8 $1,04,256

Off Season 6 10 184 40% 12 $52,992

Total Court Fees $2,15,168

Total amount of sales revenue generated:

Particulars Amount Weightage

Membership Fees $1,37,500 38.99%

Court Fees - Peak Season $1,62,176 45.99%

Sales revenue in the present plan:

The computations that has been made below is useful in ascertaining the effect of the

present sales. The assumption in the computations makes the use of systematic method by

taking into the considerations the earlier stated assumptions;

Yearly revenues of membership:

Particulars Weightage No. of

Members

Annual

Membership

Fees

Total Fees

Total Members 100% 2000

Individual Members 25% 500 $45 $22,500

Student Members 25% 500 $30 $15,000

Family Members 50% 1000 $100 $1,00,000

Total Membership Fees $1,37,500

Total amount of court fees:

Particulars Hourly

Court

fees

No of

Courts

No. of

Days

Usage % Hours Total

Fees

Peak Season- Prime

Time

8 10 181 100% 4 $57,920

Peak Season- Non

Prime Time

12 10 181 60% 8 $1,04,256

Off Season 6 10 184 40% 12 $52,992

Total Court Fees $2,15,168

Total amount of sales revenue generated:

Particulars Amount Weightage

Membership Fees $1,37,500 38.99%

Court Fees - Peak Season $1,62,176 45.99%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

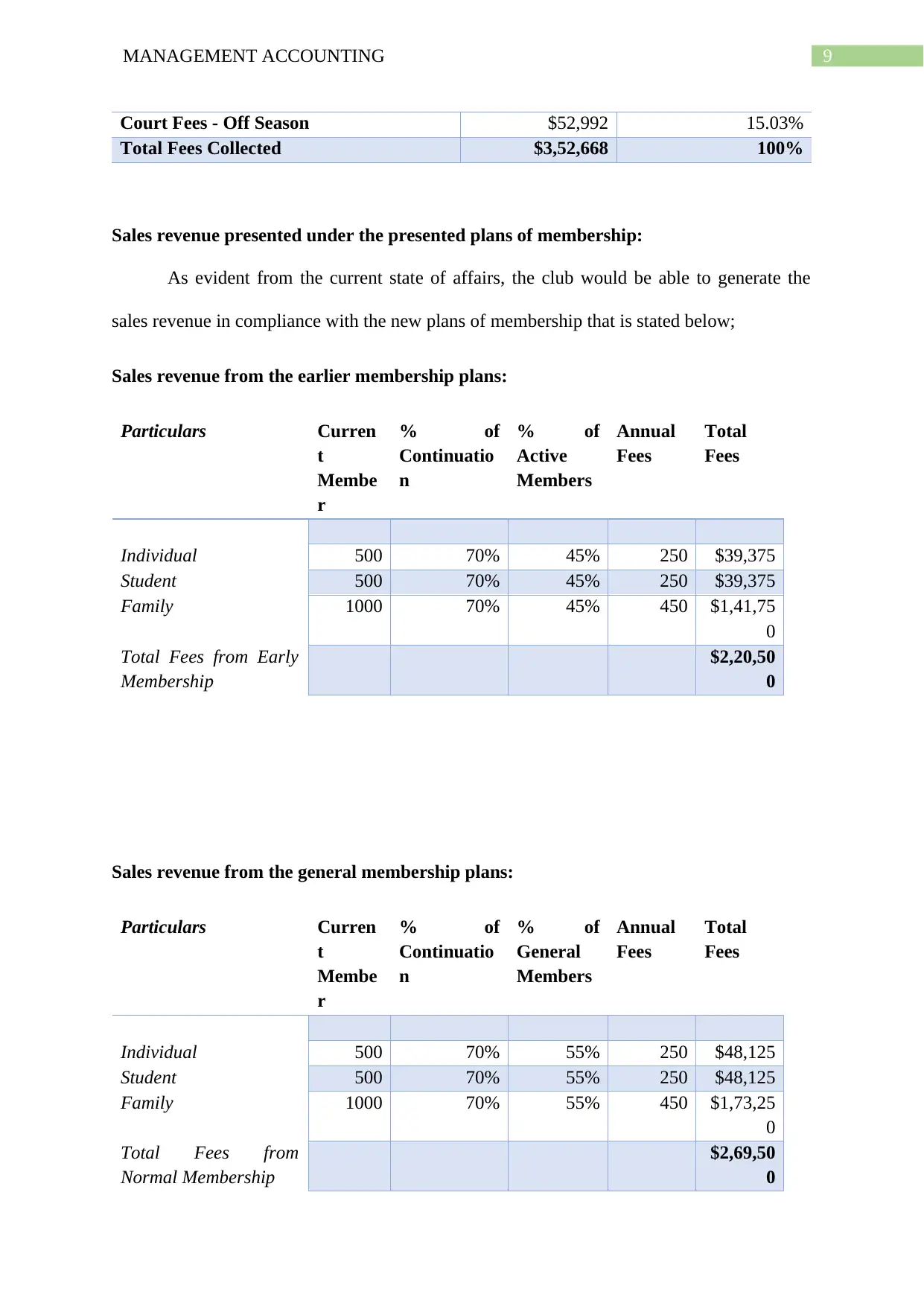

Court Fees - Off Season $52,992 15.03%

Total Fees Collected $3,52,668 100%

Sales revenue presented under the presented plans of membership:

As evident from the current state of affairs, the club would be able to generate the

sales revenue in compliance with the new plans of membership that is stated below;

Sales revenue from the earlier membership plans:

Particulars Curren

t

Membe

r

% of

Continuatio

n

% of

Active

Members

Annual

Fees

Total

Fees

Individual 500 70% 45% 250 $39,375

Student 500 70% 45% 250 $39,375

Family 1000 70% 45% 450 $1,41,75

0

Total Fees from Early

Membership

$2,20,50

0

Sales revenue from the general membership plans:

Particulars Curren

t

Membe

r

% of

Continuatio

n

% of

General

Members

Annual

Fees

Total

Fees

Individual 500 70% 55% 250 $48,125

Student 500 70% 55% 250 $48,125

Family 1000 70% 55% 450 $1,73,25

0

Total Fees from

Normal Membership

$2,69,50

0

Court Fees - Off Season $52,992 15.03%

Total Fees Collected $3,52,668 100%

Sales revenue presented under the presented plans of membership:

As evident from the current state of affairs, the club would be able to generate the

sales revenue in compliance with the new plans of membership that is stated below;

Sales revenue from the earlier membership plans:

Particulars Curren

t

Membe

r

% of

Continuatio

n

% of

Active

Members

Annual

Fees

Total

Fees

Individual 500 70% 45% 250 $39,375

Student 500 70% 45% 250 $39,375

Family 1000 70% 45% 450 $1,41,75

0

Total Fees from Early

Membership

$2,20,50

0

Sales revenue from the general membership plans:

Particulars Curren

t

Membe

r

% of

Continuatio

n

% of

General

Members

Annual

Fees

Total

Fees

Individual 500 70% 55% 250 $48,125

Student 500 70% 55% 250 $48,125

Family 1000 70% 55% 450 $1,73,25

0

Total Fees from

Normal Membership

$2,69,50

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

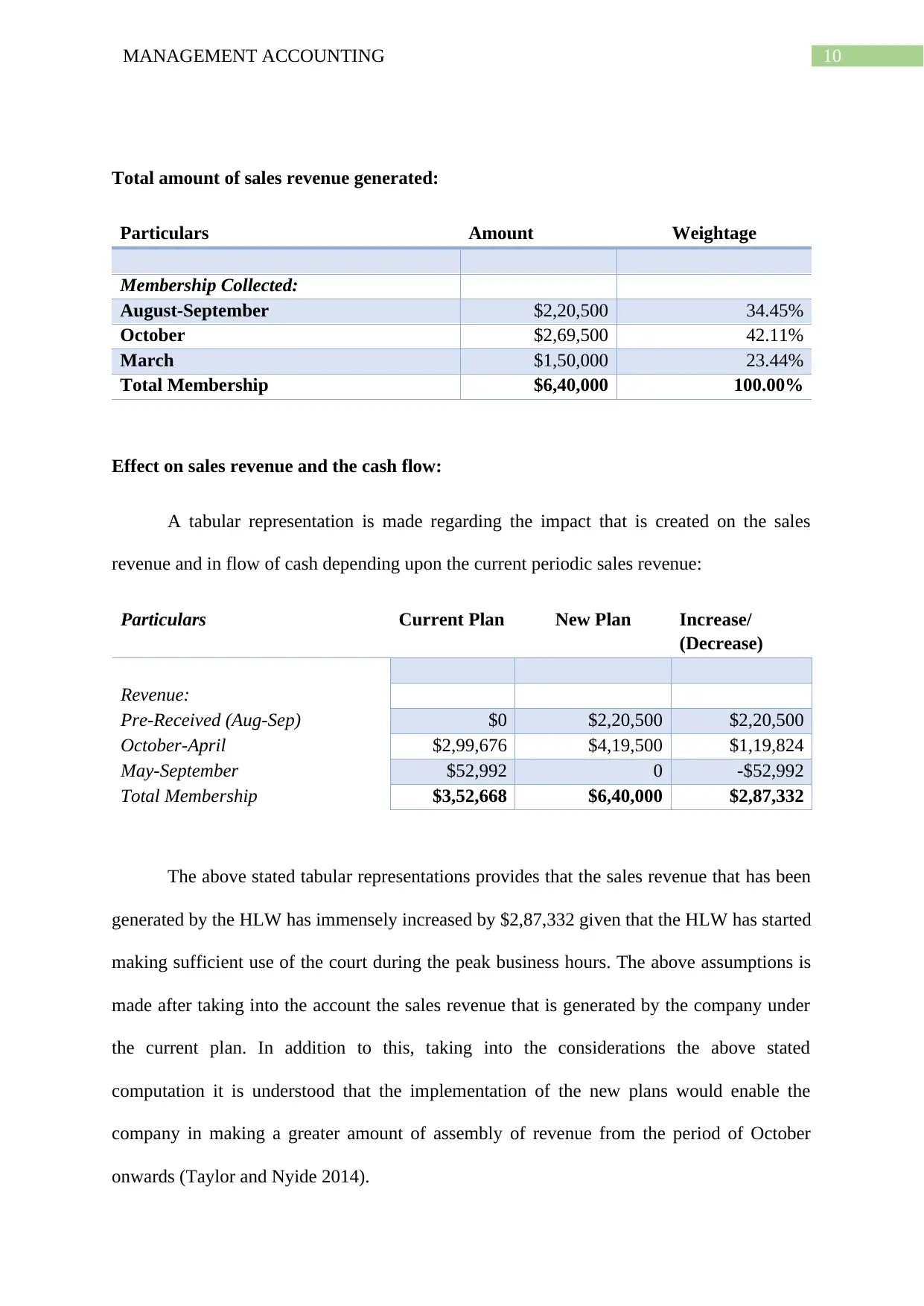

Total amount of sales revenue generated:

Particulars Amount Weightage

Membership Collected:

August-September $2,20,500 34.45%

October $2,69,500 42.11%

March $1,50,000 23.44%

Total Membership $6,40,000 100.00%

Effect on sales revenue and the cash flow:

A tabular representation is made regarding the impact that is created on the sales

revenue and in flow of cash depending upon the current periodic sales revenue:

Particulars Current Plan New Plan Increase/

(Decrease)

Revenue:

Pre-Received (Aug-Sep) $0 $2,20,500 $2,20,500

October-April $2,99,676 $4,19,500 $1,19,824

May-September $52,992 0 -$52,992

Total Membership $3,52,668 $6,40,000 $2,87,332

The above stated tabular representations provides that the sales revenue that has been

generated by the HLW has immensely increased by $2,87,332 given that the HLW has started

making sufficient use of the court during the peak business hours. The above assumptions is

made after taking into the account the sales revenue that is generated by the company under

the current plan. In addition to this, taking into the considerations the above stated

computation it is understood that the implementation of the new plans would enable the

company in making a greater amount of assembly of revenue from the period of October

onwards (Taylor and Nyide 2014).

Total amount of sales revenue generated:

Particulars Amount Weightage

Membership Collected:

August-September $2,20,500 34.45%

October $2,69,500 42.11%

March $1,50,000 23.44%

Total Membership $6,40,000 100.00%

Effect on sales revenue and the cash flow:

A tabular representation is made regarding the impact that is created on the sales

revenue and in flow of cash depending upon the current periodic sales revenue:

Particulars Current Plan New Plan Increase/

(Decrease)

Revenue:

Pre-Received (Aug-Sep) $0 $2,20,500 $2,20,500

October-April $2,99,676 $4,19,500 $1,19,824

May-September $52,992 0 -$52,992

Total Membership $3,52,668 $6,40,000 $2,87,332

The above stated tabular representations provides that the sales revenue that has been

generated by the HLW has immensely increased by $2,87,332 given that the HLW has started

making sufficient use of the court during the peak business hours. The above assumptions is

made after taking into the account the sales revenue that is generated by the company under

the current plan. In addition to this, taking into the considerations the above stated

computation it is understood that the implementation of the new plans would enable the

company in making a greater amount of assembly of revenue from the period of October

onwards (Taylor and Nyide 2014).

11MANAGEMENT ACCOUNTING

Answer to requirement 3:

One of the important considerations concerning the above stated proposed plan is that

the revenue that is generated from the new plans would yield HLW with greater amount of

revenue from the sales made in earlier instances. The primary reason for this is that there are

certainly large amount of factors that is required to be taken into the considerations when

implementing the new plans (Christ and Burritt 2015). Bearing in mind the above stated

assumptions made, the below stated factors have provided a sufficient amount of

explanations relating to the analysis that is made.

a. An important factor that is required to be considered is that the revenue that would be

generated from the new plans would be considerably greater than that of the fees that

is derived in the earlier instances (Rieckhof, Bergmann and Guenther 2015). Because

of this, there are expectations that there could be a loss of memberships after applying

the new plans of memberships. In other words there are also certain amount of

students that are not reliant based on financial terms and would be incapable of

affording greater amount of fees together with the renewal of the plans of membership

relating to the new structure of fees (Bierer et al. 2015). In addition to this, after

taking into account the present outcome, it becomes vital to assess the feedback that is

derived form the members.

b. On the application of the new plans of membership, the management is provided with

the advantage of making the collection of fees during the starting period of two or

three months. In such kind of circumstances, the administration would be better

position of reducing the cost of collecting the revenues that is generated from the

court fees (Kokubu and Kitada 2015). The management would be provided with

better opportunities of maintaining sufficient periodic records for the amount of

Answer to requirement 3:

One of the important considerations concerning the above stated proposed plan is that

the revenue that is generated from the new plans would yield HLW with greater amount of

revenue from the sales made in earlier instances. The primary reason for this is that there are

certainly large amount of factors that is required to be taken into the considerations when

implementing the new plans (Christ and Burritt 2015). Bearing in mind the above stated

assumptions made, the below stated factors have provided a sufficient amount of

explanations relating to the analysis that is made.

a. An important factor that is required to be considered is that the revenue that would be

generated from the new plans would be considerably greater than that of the fees that

is derived in the earlier instances (Rieckhof, Bergmann and Guenther 2015). Because

of this, there are expectations that there could be a loss of memberships after applying

the new plans of memberships. In other words there are also certain amount of

students that are not reliant based on financial terms and would be incapable of

affording greater amount of fees together with the renewal of the plans of membership

relating to the new structure of fees (Bierer et al. 2015). In addition to this, after

taking into account the present outcome, it becomes vital to assess the feedback that is

derived form the members.

b. On the application of the new plans of membership, the management is provided with

the advantage of making the collection of fees during the starting period of two or

three months. In such kind of circumstances, the administration would be better

position of reducing the cost of collecting the revenues that is generated from the

court fees (Kokubu and Kitada 2015). The management would be provided with

better opportunities of maintaining sufficient periodic records for the amount of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.