Management Accounting Report: Coffee Pound Business Analysis

VerifiedAdded on 2020/07/23

|19

|5534

|43

Report

AI Summary

This comprehensive management accounting report analyzes the financial performance of Coffee Pound, a small business in the restaurant industry. The report covers various aspects of management accounting, including its types, roles, and techniques. It explores inventory management, cost accounting, and price-optimizing systems. The report includes a detailed comparison between management and financial accounting. Furthermore, it presents income statements using both marginal and absorption costing methods, along with an explanation of the differences between the two. It also discusses various budgeting and pricing methods suitable for Coffee Pound, along with the application and advantages of a management accounting system. The report also evaluates the integration of the management accounting system within the organization, focusing on setting prices, providing cost centers, facilitating decision-making, and preparing budgets. Finally, the report outlines how the management accounting system can address financial problems, and discusses the benefits of planning tools for a sustainable organization.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and its types..................................................................................1

P2. Explaining methods used in management accounting reporting..........................................3

M1. Application and advantages of Management accounting system........................................4

D1. Evaluating integration of management accounting system within organisation..................5

TASK 2............................................................................................................................................5

P3. Income statement using different costing techniques...........................................................5

M2. Applying various management accounting techniques.......................................................7

D2. Interpreting financial reports................................................................................................8

TASK 3............................................................................................................................................8

P4. Advantages and disadvantages of budgetary control tools...................................................8

M3. Uses of different planning tools in forecasting budgets....................................................10

D3. Planning tools for solving financial problems...................................................................11

TASK 4..........................................................................................................................................12

P5 Use of management accounting system for responding financial problems........................12

M4. Sustainable organisation through responding financial problems.....................................13

D4. Benefits of planning tools in sustainable organisation.......................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and its types..................................................................................1

P2. Explaining methods used in management accounting reporting..........................................3

M1. Application and advantages of Management accounting system........................................4

D1. Evaluating integration of management accounting system within organisation..................5

TASK 2............................................................................................................................................5

P3. Income statement using different costing techniques...........................................................5

M2. Applying various management accounting techniques.......................................................7

D2. Interpreting financial reports................................................................................................8

TASK 3............................................................................................................................................8

P4. Advantages and disadvantages of budgetary control tools...................................................8

M3. Uses of different planning tools in forecasting budgets....................................................10

D3. Planning tools for solving financial problems...................................................................11

TASK 4..........................................................................................................................................12

P5 Use of management accounting system for responding financial problems........................12

M4. Sustainable organisation through responding financial problems.....................................13

D4. Benefits of planning tools in sustainable organisation.......................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is a managerial function. It includes tools that are used by

management in advising the company about the techniques and measures to be used in order to

develop and grow organisation. It facilitates provision making for financial data. Main purposes

of management accounting is to facilitate decision making process and to provide suggestions

and advices for effectual performance of organisation.

Coffee Pound has been considered as per the requirement of scenario that employees of

the company need to be less than 50. The present report explains the management accounting

system, its roles, uses, techniques and types in brief. The report is prepared in context with

Coffee Pound for the better understanding of management accounting system. Coffee Pound is

small business organisation under restaurant industry. The present report also includes

preparation of income statement using marginal costing and absorption costing along with

explaining difference between the two. The report also provides various budgeting and pricing

methods that can be used by Coffee Pound.

TASK 1

P1. Management accounting and its types

Management accounting is a tool that is used by the manager of an organisation for the

process of identifying, accumulating, analysing, preparing, interpreting and communicating the

information used by them. It tracks the allocation of cost to products and services of the

company. Management accounting system helps the internal user of the information in taking

future economic decisions. Managers using management accounting makes provisions for

various financial and non- financial decision regarding the organisation. It involves functions

like performance management system, management decision making, etc. along with helping the

management in preparing organisation strategy (Armstrong, 2014). It is used by the management

for making their day to day decision using various management reports. Management accounting

system comprises various element of accounting including report of incomes and expenses,

budget reports, investment reports, etc.

1

Management accounting is a managerial function. It includes tools that are used by

management in advising the company about the techniques and measures to be used in order to

develop and grow organisation. It facilitates provision making for financial data. Main purposes

of management accounting is to facilitate decision making process and to provide suggestions

and advices for effectual performance of organisation.

Coffee Pound has been considered as per the requirement of scenario that employees of

the company need to be less than 50. The present report explains the management accounting

system, its roles, uses, techniques and types in brief. The report is prepared in context with

Coffee Pound for the better understanding of management accounting system. Coffee Pound is

small business organisation under restaurant industry. The present report also includes

preparation of income statement using marginal costing and absorption costing along with

explaining difference between the two. The report also provides various budgeting and pricing

methods that can be used by Coffee Pound.

TASK 1

P1. Management accounting and its types

Management accounting is a tool that is used by the manager of an organisation for the

process of identifying, accumulating, analysing, preparing, interpreting and communicating the

information used by them. It tracks the allocation of cost to products and services of the

company. Management accounting system helps the internal user of the information in taking

future economic decisions. Managers using management accounting makes provisions for

various financial and non- financial decision regarding the organisation. It involves functions

like performance management system, management decision making, etc. along with helping the

management in preparing organisation strategy (Armstrong, 2014). It is used by the management

for making their day to day decision using various management reports. Management accounting

system comprises various element of accounting including report of incomes and expenses,

budget reports, investment reports, etc.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Various types of management accounting systems are:

Inventory management system: This system of management accounting helps management in

carrying off inventory into the organisation. Finished stock and raw material, both are managed

under this system. Nowadays, for managing inventory, various computer software's has been

developed therefore these software's have helped managers in reducing their work load (Bertz,

and Quinn, 2014). With the help of this software's it is easy to manage various functions of

inventory like, purchase, opening stock, closing stock etc.

Price- Optimising system: This system is used to calculate the differences between the demand

of products and services at different price level using mathematical models. Determined

differences are then analysed and combined with inventory level and cost information to

determine the prices of products and services for achieving best profit levels. The system also

identifies the best price that will meet the objectives of business. This technique can be

implemented various industries like hospitality, restaurant , manufacturing, etc.

Cost accounting system: This segment of management accounting system is used to estimate

the cost of various products and services produced by a business unit (Bodie, 2013). The main

purposes of cost accounting system is controlling cost, valuation of inventory and analysing the

profitability of company. It is typical to determine the accurate of cost if company is dealing in

wide range of products and services, hence the system of cost accounting is difficult to operate

and so requires an experienced and professional cost accountant.

Job-Costing system: The system helps in assigning variable manufacturing cost to various

products batches or individual products. This system of costing is mostly used when there is a

significant differences in manufactured good or services to be provided. For implementing this

system, identification of various types of expenses to different jobs is essential. It produces

profitability report of various jobs that includes overall profit and loss information about the

entity (Brandau, Endenich, Trapp and Hoffjan, 2013).

All these accounting systems can be used in Coffee Pound store, as it has various

functions. Inventory management can be used in managing the incoming and outgoing of

inventory, managing fresh and old stock by using various methods like FIFO or LIFO, etc. Cost

2

Inventory management system: This system of management accounting helps management in

carrying off inventory into the organisation. Finished stock and raw material, both are managed

under this system. Nowadays, for managing inventory, various computer software's has been

developed therefore these software's have helped managers in reducing their work load (Bertz,

and Quinn, 2014). With the help of this software's it is easy to manage various functions of

inventory like, purchase, opening stock, closing stock etc.

Price- Optimising system: This system is used to calculate the differences between the demand

of products and services at different price level using mathematical models. Determined

differences are then analysed and combined with inventory level and cost information to

determine the prices of products and services for achieving best profit levels. The system also

identifies the best price that will meet the objectives of business. This technique can be

implemented various industries like hospitality, restaurant , manufacturing, etc.

Cost accounting system: This segment of management accounting system is used to estimate

the cost of various products and services produced by a business unit (Bodie, 2013). The main

purposes of cost accounting system is controlling cost, valuation of inventory and analysing the

profitability of company. It is typical to determine the accurate of cost if company is dealing in

wide range of products and services, hence the system of cost accounting is difficult to operate

and so requires an experienced and professional cost accountant.

Job-Costing system: The system helps in assigning variable manufacturing cost to various

products batches or individual products. This system of costing is mostly used when there is a

significant differences in manufactured good or services to be provided. For implementing this

system, identification of various types of expenses to different jobs is essential. It produces

profitability report of various jobs that includes overall profit and loss information about the

entity (Brandau, Endenich, Trapp and Hoffjan, 2013).

All these accounting systems can be used in Coffee Pound store, as it has various

functions. Inventory management can be used in managing the incoming and outgoing of

inventory, managing fresh and old stock by using various methods like FIFO or LIFO, etc. Cost

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting system can be used in determining the cost of its various segments like administration

cost, purchasing cost, salary to staff etc.

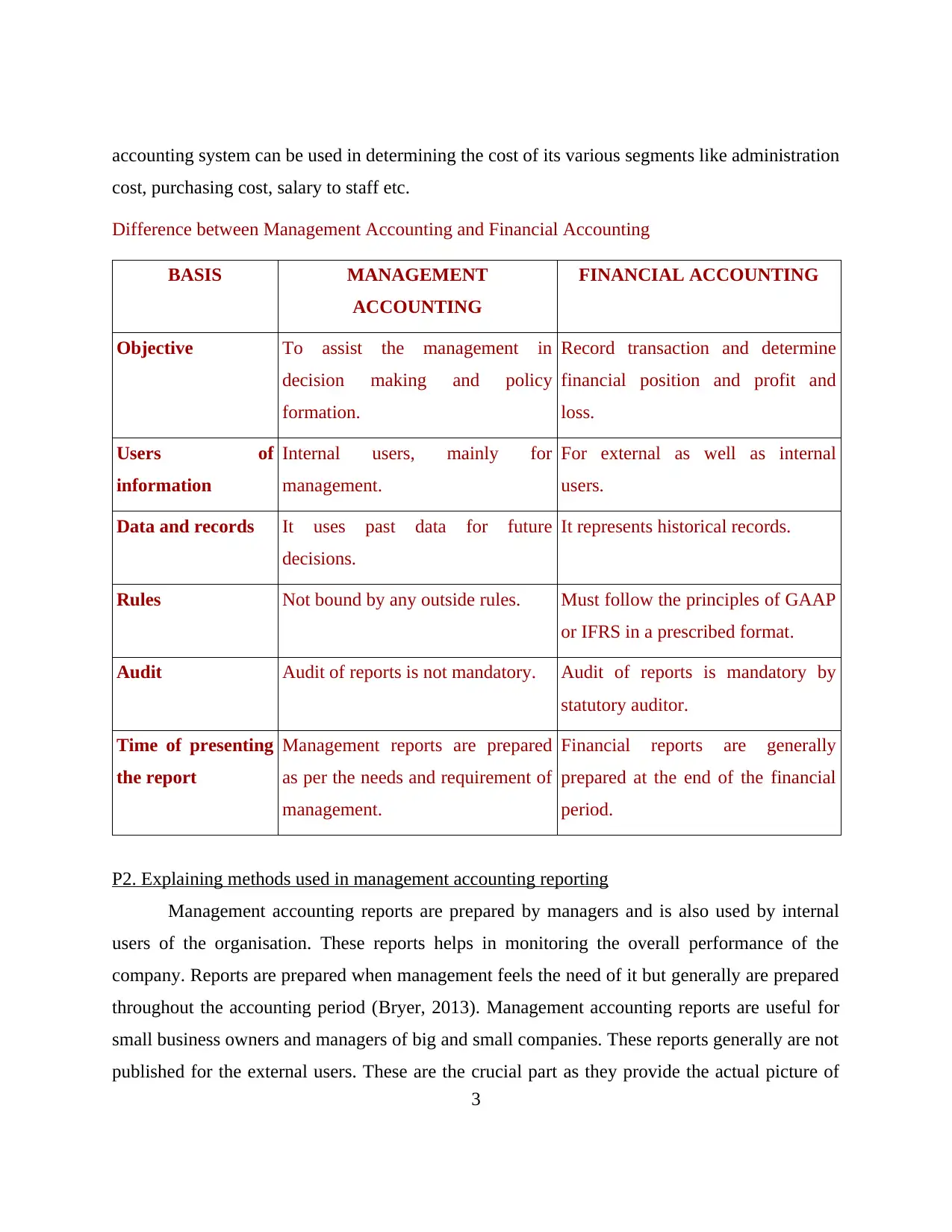

Difference between Management Accounting and Financial Accounting

BASIS MANAGEMENT

ACCOUNTING

FINANCIAL ACCOUNTING

Objective To assist the management in

decision making and policy

formation.

Record transaction and determine

financial position and profit and

loss.

Users of

information

Internal users, mainly for

management.

For external as well as internal

users.

Data and records It uses past data for future

decisions.

It represents historical records.

Rules Not bound by any outside rules. Must follow the principles of GAAP

or IFRS in a prescribed format.

Audit Audit of reports is not mandatory. Audit of reports is mandatory by

statutory auditor.

Time of presenting

the report

Management reports are prepared

as per the needs and requirement of

management.

Financial reports are generally

prepared at the end of the financial

period.

P2. Explaining methods used in management accounting reporting

Management accounting reports are prepared by managers and is also used by internal

users of the organisation. These reports helps in monitoring the overall performance of the

company. Reports are prepared when management feels the need of it but generally are prepared

throughout the accounting period (Bryer, 2013). Management accounting reports are useful for

small business owners and managers of big and small companies. These reports generally are not

published for the external users. These are the crucial part as they provide the actual picture of

3

cost, purchasing cost, salary to staff etc.

Difference between Management Accounting and Financial Accounting

BASIS MANAGEMENT

ACCOUNTING

FINANCIAL ACCOUNTING

Objective To assist the management in

decision making and policy

formation.

Record transaction and determine

financial position and profit and

loss.

Users of

information

Internal users, mainly for

management.

For external as well as internal

users.

Data and records It uses past data for future

decisions.

It represents historical records.

Rules Not bound by any outside rules. Must follow the principles of GAAP

or IFRS in a prescribed format.

Audit Audit of reports is not mandatory. Audit of reports is mandatory by

statutory auditor.

Time of presenting

the report

Management reports are prepared

as per the needs and requirement of

management.

Financial reports are generally

prepared at the end of the financial

period.

P2. Explaining methods used in management accounting reporting

Management accounting reports are prepared by managers and is also used by internal

users of the organisation. These reports helps in monitoring the overall performance of the

company. Reports are prepared when management feels the need of it but generally are prepared

throughout the accounting period (Bryer, 2013). Management accounting reports are useful for

small business owners and managers of big and small companies. These reports generally are not

published for the external users. These are the crucial part as they provide the actual picture of

3

the business (Types of managerial accounting report, 2017). Though these reports are prepared

when management feels the need of it, but generally the best practice is to prepare these reports

on quarterly basis. Health of the business is determined using these reports. Several types of

management accounting report that can be prepared by the management of Coffee Pound are:

Budget report: It is the most fundamental type of report that is used in management accounting.

It helps in identifying the cost controls across different segments of the enterprise (Cadez and

Guilding, 2012). The report is beneficial in all kinds of organisation whether organisation having

different segments or a unified entity. It is prepared for analysing the budgets of the current year

on the basis on facts and findings and actual cost of prior years. Budgets are prepared for cost

allocation, volume of sales of products and services, administration expenses, salary expenses,

revenues, etc. By preparing budgets it is possible for managers to identify the places to cut the

cost.

Job Cost report: The report is prepared for specific jobs and the actual cost accrued in specific

projects. This report compares the accrued cost of a project to actual revenue yielded from that

project. Through this comparison, it helps the management and owners of small businesses to

determine the most profitable segments of the organisation and also those segments which are

running in loss (Chan, 2015). This report is essential for Coffee Pound as it operates in various

segments of product. This will help the company in knowing which is the most profitable

segment of products it is dealing in and which products are causing loss.

Accounts receivable ageing report: This report is prepared by those business units who provide

their goods and services to their customers on credit basis. It is the most crucial and critical tool

of management reporting. It is prepared to determine the overall overview of actual credit

balances of different customers. Typically, this report provides credit balances which are 30, 60

and 90 days late. This report can help Coffee Pound in making estimated provisions for bad

debts and also in knowing the actual amount of goods that are given on credit.

Inventory and manufacturing report: This report is produced under inventory management

system. Companies that produce wide range of physical products with low fault tolerance

generally produce this report (DRURY, 2013). This is prepared to centralise data regarding

4

when management feels the need of it, but generally the best practice is to prepare these reports

on quarterly basis. Health of the business is determined using these reports. Several types of

management accounting report that can be prepared by the management of Coffee Pound are:

Budget report: It is the most fundamental type of report that is used in management accounting.

It helps in identifying the cost controls across different segments of the enterprise (Cadez and

Guilding, 2012). The report is beneficial in all kinds of organisation whether organisation having

different segments or a unified entity. It is prepared for analysing the budgets of the current year

on the basis on facts and findings and actual cost of prior years. Budgets are prepared for cost

allocation, volume of sales of products and services, administration expenses, salary expenses,

revenues, etc. By preparing budgets it is possible for managers to identify the places to cut the

cost.

Job Cost report: The report is prepared for specific jobs and the actual cost accrued in specific

projects. This report compares the accrued cost of a project to actual revenue yielded from that

project. Through this comparison, it helps the management and owners of small businesses to

determine the most profitable segments of the organisation and also those segments which are

running in loss (Chan, 2015). This report is essential for Coffee Pound as it operates in various

segments of product. This will help the company in knowing which is the most profitable

segment of products it is dealing in and which products are causing loss.

Accounts receivable ageing report: This report is prepared by those business units who provide

their goods and services to their customers on credit basis. It is the most crucial and critical tool

of management reporting. It is prepared to determine the overall overview of actual credit

balances of different customers. Typically, this report provides credit balances which are 30, 60

and 90 days late. This report can help Coffee Pound in making estimated provisions for bad

debts and also in knowing the actual amount of goods that are given on credit.

Inventory and manufacturing report: This report is produced under inventory management

system. Companies that produce wide range of physical products with low fault tolerance

generally produce this report (DRURY, 2013). This is prepared to centralise data regarding

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

labour, inventor cost, and additional overheads that are allocated in the process of production.

This report is also prepared by the organisations like Coffee Pound to manage the inventory.

Through this report management of Coffee Pound can identify the dead stock and can make

policies to rotate the same in the market.

M1. Application and advantages of Management accounting system

As discussed above various types of management accounting system and the types of

report, these can benefit Coffee Pound in number of ways:

This will help the management of Coffee Pound in estimating the cost of their products

and services and also those segment of products that are most profitable.

Management accounting system will help the management in making various future

economic decisions regarding the activities that need to be closed down and those that

need to be started (Fridson and Alvarez, 2011).

Use of management accounting system will help in forecasting the future trends through

management can prepare various policies accordingly.

Forecasting of future cash inflow and outflow is possible to determine and the impact of

the same to business unit.

Through this management can also determine the variations in forecasted budgets of cost

and sales and actual amount of expenses and sales volume.

This also helps in identifying the areas for future business expansions.

D1. Evaluating integration of management accounting system within organisation

As the need of management accounting has been discussed in the above report. The need

of its integration within the organisation also increases (Fullerton, Kennedy and Widener, 2013).

Before integrating management accounting management should identify the key areas that

require integration System of management accounting can be integrated in Coffee Pound by:

Setting the prices of different segments of products and services.

By providing cost centres of goods and services.

5

This report is also prepared by the organisations like Coffee Pound to manage the inventory.

Through this report management of Coffee Pound can identify the dead stock and can make

policies to rotate the same in the market.

M1. Application and advantages of Management accounting system

As discussed above various types of management accounting system and the types of

report, these can benefit Coffee Pound in number of ways:

This will help the management of Coffee Pound in estimating the cost of their products

and services and also those segment of products that are most profitable.

Management accounting system will help the management in making various future

economic decisions regarding the activities that need to be closed down and those that

need to be started (Fridson and Alvarez, 2011).

Use of management accounting system will help in forecasting the future trends through

management can prepare various policies accordingly.

Forecasting of future cash inflow and outflow is possible to determine and the impact of

the same to business unit.

Through this management can also determine the variations in forecasted budgets of cost

and sales and actual amount of expenses and sales volume.

This also helps in identifying the areas for future business expansions.

D1. Evaluating integration of management accounting system within organisation

As the need of management accounting has been discussed in the above report. The need

of its integration within the organisation also increases (Fullerton, Kennedy and Widener, 2013).

Before integrating management accounting management should identify the key areas that

require integration System of management accounting can be integrated in Coffee Pound by:

Setting the prices of different segments of products and services.

By providing cost centres of goods and services.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Facilitating decision making process.

Preparation of budgets for various activities in different departments.

Preparing centralised budget for the company as a whole.

By providing training to the management for using different management accounting

systems.

Developing budgets for staff development.

By conducting personal meetings and interview with key personnel of the organisation.

Identifying best practices that are required by the organisation.

By defining roles and responsibilities of the staff in clear and complete manner

Explaining purpose of integrating management system to the employees.

Qualitative characteristics of information includes:

Understandability: The information presented in the report must be in such a form that could be

understandable. A financial report having no understandability would be of no use to both

internal users and external users.

Reliability: The information must be reliable to the organisation and not hypothetical. Only

reliable information can present the actual view of the organisation. Information must be

represntational, verifiable and fair.

TASK 2

P3. Income statement using different costing techniques

Absorption costing method: It is used for calculating cost of product by taking into account

both indirect cost and direct cost (Groot and Selto, 2013). All the cost directly related to the

manufacturing of product like raw material, wages, etc. are accounted in direct cost and all other

cost that does not have direct connection with manufacturing of goods are accounted in indirect

cost. The method absorbs all the cost including fixed overheads as well.

6

Preparation of budgets for various activities in different departments.

Preparing centralised budget for the company as a whole.

By providing training to the management for using different management accounting

systems.

Developing budgets for staff development.

By conducting personal meetings and interview with key personnel of the organisation.

Identifying best practices that are required by the organisation.

By defining roles and responsibilities of the staff in clear and complete manner

Explaining purpose of integrating management system to the employees.

Qualitative characteristics of information includes:

Understandability: The information presented in the report must be in such a form that could be

understandable. A financial report having no understandability would be of no use to both

internal users and external users.

Reliability: The information must be reliable to the organisation and not hypothetical. Only

reliable information can present the actual view of the organisation. Information must be

represntational, verifiable and fair.

TASK 2

P3. Income statement using different costing techniques

Absorption costing method: It is used for calculating cost of product by taking into account

both indirect cost and direct cost (Groot and Selto, 2013). All the cost directly related to the

manufacturing of product like raw material, wages, etc. are accounted in direct cost and all other

cost that does not have direct connection with manufacturing of goods are accounted in indirect

cost. The method absorbs all the cost including fixed overheads as well.

6

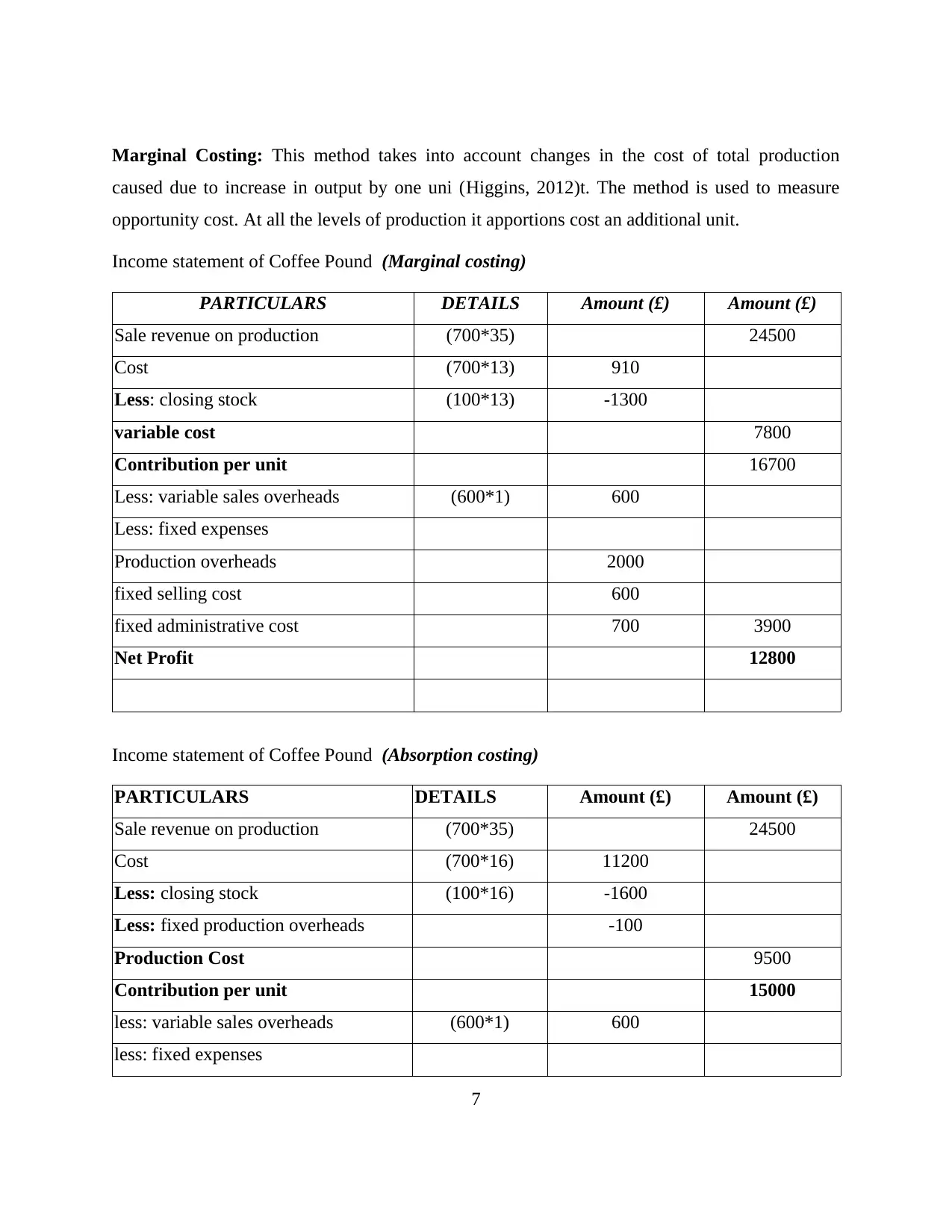

Marginal Costing: This method takes into account changes in the cost of total production

caused due to increase in output by one uni (Higgins, 2012)t. The method is used to measure

opportunity cost. At all the levels of production it apportions cost an additional unit.

Income statement of Coffee Pound (Marginal costing)

PARTICULARS DETAILS Amount (£) Amount (£)

Sale revenue on production (700*35) 24500

Cost (700*13) 910

Less: closing stock (100*13) -1300

variable cost 7800

Contribution per unit 16700

Less: variable sales overheads (600*1) 600

Less: fixed expenses

Production overheads 2000

fixed selling cost 600

fixed administrative cost 700 3900

Net Profit 12800

Income statement of Coffee Pound (Absorption costing)

PARTICULARS DETAILS Amount (£) Amount (£)

Sale revenue on production (700*35) 24500

Cost (700*16) 11200

Less: closing stock (100*16) -1600

Less: fixed production overheads -100

Production Cost 9500

Contribution per unit 15000

less: variable sales overheads (600*1) 600

less: fixed expenses

7

caused due to increase in output by one uni (Higgins, 2012)t. The method is used to measure

opportunity cost. At all the levels of production it apportions cost an additional unit.

Income statement of Coffee Pound (Marginal costing)

PARTICULARS DETAILS Amount (£) Amount (£)

Sale revenue on production (700*35) 24500

Cost (700*13) 910

Less: closing stock (100*13) -1300

variable cost 7800

Contribution per unit 16700

Less: variable sales overheads (600*1) 600

Less: fixed expenses

Production overheads 2000

fixed selling cost 600

fixed administrative cost 700 3900

Net Profit 12800

Income statement of Coffee Pound (Absorption costing)

PARTICULARS DETAILS Amount (£) Amount (£)

Sale revenue on production (700*35) 24500

Cost (700*16) 11200

Less: closing stock (100*16) -1600

Less: fixed production overheads -100

Production Cost 9500

Contribution per unit 15000

less: variable sales overheads (600*1) 600

less: fixed expenses

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

fixed selling cost 600

Fixed administrative cost 700 1900

Net Profit 13100

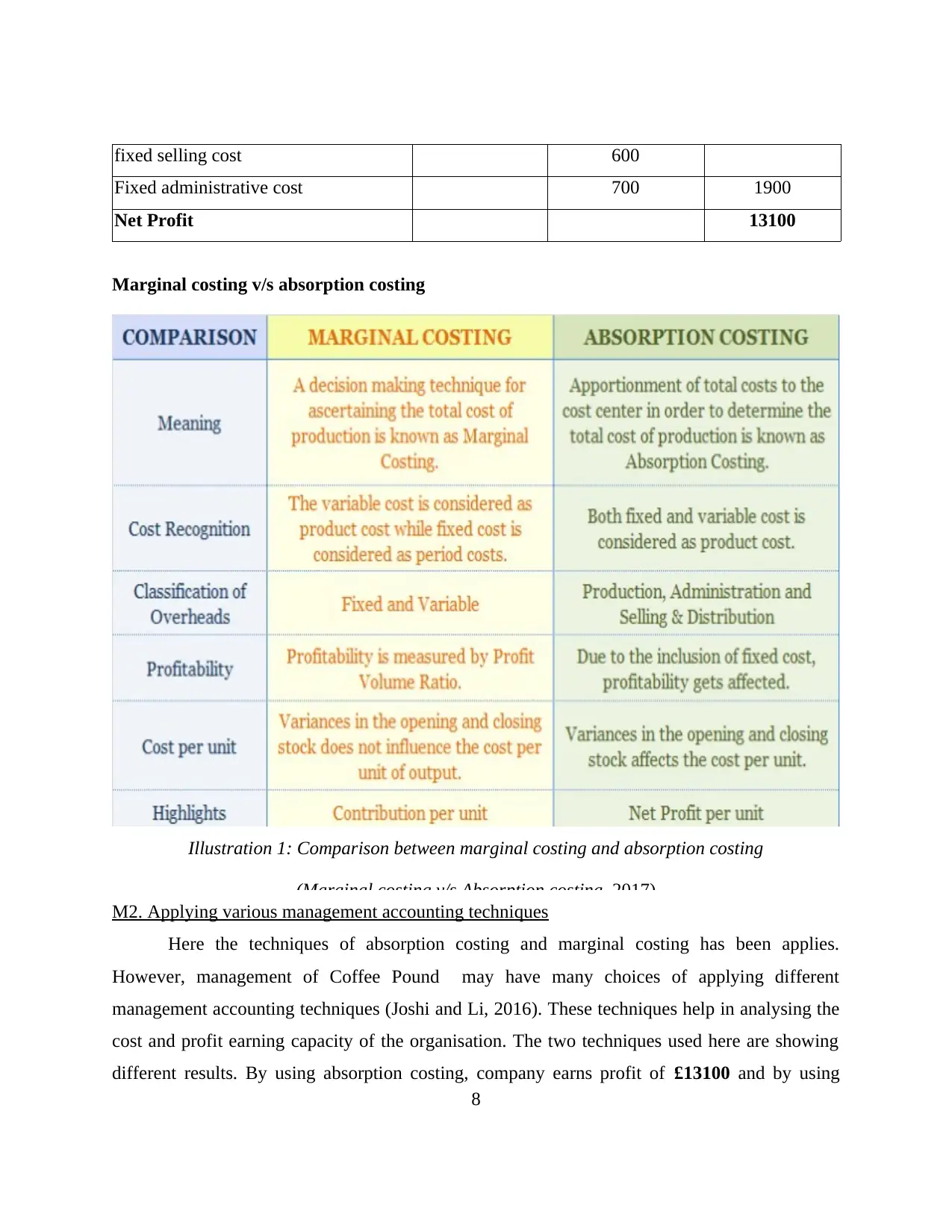

Marginal costing v/s absorption costing

Illustration 1: Comparison between marginal costing and absorption costing

(Marginal costing v/s Absorption costing, 2017)

M2. Applying various management accounting techniques

Here the techniques of absorption costing and marginal costing has been applies.

However, management of Coffee Pound may have many choices of applying different

management accounting techniques (Joshi and Li, 2016). These techniques help in analysing the

cost and profit earning capacity of the organisation. The two techniques used here are showing

different results. By using absorption costing, company earns profit of £13100 and by using

8

Fixed administrative cost 700 1900

Net Profit 13100

Marginal costing v/s absorption costing

Illustration 1: Comparison between marginal costing and absorption costing

(Marginal costing v/s Absorption costing, 2017)

M2. Applying various management accounting techniques

Here the techniques of absorption costing and marginal costing has been applies.

However, management of Coffee Pound may have many choices of applying different

management accounting techniques (Joshi and Li, 2016). These techniques help in analysing the

cost and profit earning capacity of the organisation. The two techniques used here are showing

different results. By using absorption costing, company earns profit of £13100 and by using

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

marginal costing, company earns profit of £12800. There is a significant difference of results in

both the techniques, this is because both the techniques uses different approaches to take into

account the cost of production. One uses all the expenses and another uses only variable

expenses of production as discussed above. Other techniques that Coffee Pound can use are

techniques of budgeting control, fund flow statement, cash flow statement, etc.

D2. Interpreting financial reports

To,

General Manager

Coffee Pound Store

Respected sir,

It is hereby to inform you that, income statement has been produced from both the

techniques i.e. absorption costing and marginal costing. From the analysis of both the income

statements we have reached to the conclusion that best results are shown by income statement

using absorption costing as it shows the profit of £13100 while marginal costing technique

shows profit of £12800. Therefore, it is advised to the company to use income statement using

absorption costing as it portrays better profit earning capacity of the firm. It will be fruitful to

attract more customers to the organisation and will also improve the financial performance of

the company.

With regards,

Management Accounting Officer

Coffee Pound Store

TASK 3

P4. Advantages and disadvantages of budgetary control tools

There are various types of budgetary control tools that can be used by the management of

Coffee Pound store following are the types of budgetary control tools and their advantages and

disadvantages:

9

both the techniques, this is because both the techniques uses different approaches to take into

account the cost of production. One uses all the expenses and another uses only variable

expenses of production as discussed above. Other techniques that Coffee Pound can use are

techniques of budgeting control, fund flow statement, cash flow statement, etc.

D2. Interpreting financial reports

To,

General Manager

Coffee Pound Store

Respected sir,

It is hereby to inform you that, income statement has been produced from both the

techniques i.e. absorption costing and marginal costing. From the analysis of both the income

statements we have reached to the conclusion that best results are shown by income statement

using absorption costing as it shows the profit of £13100 while marginal costing technique

shows profit of £12800. Therefore, it is advised to the company to use income statement using

absorption costing as it portrays better profit earning capacity of the firm. It will be fruitful to

attract more customers to the organisation and will also improve the financial performance of

the company.

With regards,

Management Accounting Officer

Coffee Pound Store

TASK 3

P4. Advantages and disadvantages of budgetary control tools

There are various types of budgetary control tools that can be used by the management of

Coffee Pound store following are the types of budgetary control tools and their advantages and

disadvantages:

9

Zero-based Budgeting: Under this method, budgets of prior years are not used instead,

this method assumes Zero budget as a base (Khodzytska and Ivchenko, 2014). Expenses

of past year are nit taken into account and budget for the present year are prepared on

taking prior year base as zero. Let say, if the administration expenses of past year of

Coffee Pound store were £6000, under this method of budgeting, management can not

ask for the same amount as the budget for present year.

Advantages:

This method facilitates Effective allocation of resources as it is based on the requirement

and need of the department.

Various ways of effective costing can be identified for better operations (Klemstine and

Maher, 2014). Increases communication and coordination in the organisation that increases transparency

among the employees and employer.

Disadvantages:

Difficult to obtain amount for budget.

Time consuming method as it starts with zero base. For the successful implementation it need to be clearly understood by the managers of all

level. Activity Based Budgeting: This method of budgeting takes into account the overhead

expenses of the business unit (Klychova and et.al., 2015). The budget is prepared by

identifying activities that requires high cost and the past year budget is not considered in

this method of budgeting. Outcomes are then identified and researched and on the basis

of this resources are then allocated.

Advantages:

This method helps in eliminating all the unnecessary and obsolete business activities

which in turns helps in saving cost.

10

this method assumes Zero budget as a base (Khodzytska and Ivchenko, 2014). Expenses

of past year are nit taken into account and budget for the present year are prepared on

taking prior year base as zero. Let say, if the administration expenses of past year of

Coffee Pound store were £6000, under this method of budgeting, management can not

ask for the same amount as the budget for present year.

Advantages:

This method facilitates Effective allocation of resources as it is based on the requirement

and need of the department.

Various ways of effective costing can be identified for better operations (Klemstine and

Maher, 2014). Increases communication and coordination in the organisation that increases transparency

among the employees and employer.

Disadvantages:

Difficult to obtain amount for budget.

Time consuming method as it starts with zero base. For the successful implementation it need to be clearly understood by the managers of all

level. Activity Based Budgeting: This method of budgeting takes into account the overhead

expenses of the business unit (Klychova and et.al., 2015). The budget is prepared by

identifying activities that requires high cost and the past year budget is not considered in

this method of budgeting. Outcomes are then identified and researched and on the basis

of this resources are then allocated.

Advantages:

This method helps in eliminating all the unnecessary and obsolete business activities

which in turns helps in saving cost.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.