Management Accounting for Decision Makers: Concepts and Techniques

VerifiedAdded on 2023/01/03

|14

|3748

|93

Report

AI Summary

This report provides an overview of management accounting concepts and techniques for decision-makers. It begins with an introduction to management accounting, emphasizing its role in internal financial reporting and decision-making. The main body is divided into parts. Part 1 explains the management accounting system, detailing various systems such as cost accounting, cost-volume-profit analysis, budgetary control, marginal costing, absorption costing, inventory management, job costing, and price optimization. It also discusses different methods used in management accounting, including cost reports, cash budgets, and performance reports. Part 2 compares how organizations adapt management accounting systems to address financial problems and discusses producing financial reports. The report also outlines the advantages and disadvantages of planning tools used for budgetary control, such as profit maximization and improved financial management, while acknowledging the uncertainty of the future. The report aims to equip students with the skills to present financial statements and assist senior managers in financial planning. The report underscores the significance of management accounting in monitoring company performance and aiding in effective financial decision-making.

MANAGEMENT ACCOUNTING

CONCEPTS AND TECHNIQUES

FOR DECISION MAKERS

CONCEPTS AND TECHNIQUES

FOR DECISION MAKERS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

PART 1............................................................................................................................................3

Understanding Management accounting system.........................................................................3

Advantage and disadvantage of planning tool used for budgetary control..................................6

Part 2................................................................................................................................................8

Comparing how organization are adapting management accounting system to respond to

financial problem.........................................................................................................................8

Producing financial report............................................................................................................9

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

PART 1............................................................................................................................................3

Understanding Management accounting system.........................................................................3

Advantage and disadvantage of planning tool used for budgetary control..................................6

Part 2................................................................................................................................................8

Comparing how organization are adapting management accounting system to respond to

financial problem.........................................................................................................................8

Producing financial report............................................................................................................9

INTRODUCTION

Management accounting is process of making report of the business activity operation

that help the mangers to make short term and long term decision by identifying, measuring, and

analysis the information by the mangers (Amara, Benelifa, 2017). This report highlight the

management accounting fundamentals that involve the business environment and their operation

in the environment. The report of how management accounting applies financial information and

data ton assist in planning decision, monitoring the finance of the company. By successful

completion, students shall ready to present the financial statement and help the senior manager

involve in financial planning. Whereas, they also learn the fundamental skills and knowledge in

the field. Management accounting assist the manager and owner to monitor the company's

performance and prepared throughout the year. Manager or owner can also request report for

weekly, monthly or quarterly depends on the nature of the company.

MAIN BODY

PART 1

Understanding Management accounting system.

It is also known as the managerial accounting system. Management accounting helps in

to provide the financial information and data to managers of the company for the decision-

making purpose. Its only involved the internal management team of the firm which make it

different from the financial accounting. Management accounting gives the financial data to

assist, monitors, planning and decision-making and manages the financial management of the

firm. Management accounting is a process where measures the data, identify, interpret and

anglicizing the financial information of the data to achieve the target goal of the company

(Hamamura, 2019). The process of preparing the management accounts are offer on time,

accurate statistical financial information needed by the management to complete day to day task

of the firms. They show the report which are prepared to fulfil the requirements of the

management. Accounting shows the data which are measures, identify and interpreted the

economical data for the decision. Management accounting system applications varies in the data.

Every management accounting system gives various information based on the requirements of

the firm's management. There are various kinds of management accounting system with their

various objectives and functions where all the elements creates the standardized context of the

data to analysis and communicate the data in accounting system.

Management accounting is process of making report of the business activity operation

that help the mangers to make short term and long term decision by identifying, measuring, and

analysis the information by the mangers (Amara, Benelifa, 2017). This report highlight the

management accounting fundamentals that involve the business environment and their operation

in the environment. The report of how management accounting applies financial information and

data ton assist in planning decision, monitoring the finance of the company. By successful

completion, students shall ready to present the financial statement and help the senior manager

involve in financial planning. Whereas, they also learn the fundamental skills and knowledge in

the field. Management accounting assist the manager and owner to monitor the company's

performance and prepared throughout the year. Manager or owner can also request report for

weekly, monthly or quarterly depends on the nature of the company.

MAIN BODY

PART 1

Understanding Management accounting system.

It is also known as the managerial accounting system. Management accounting helps in

to provide the financial information and data to managers of the company for the decision-

making purpose. Its only involved the internal management team of the firm which make it

different from the financial accounting. Management accounting gives the financial data to

assist, monitors, planning and decision-making and manages the financial management of the

firm. Management accounting is a process where measures the data, identify, interpret and

anglicizing the financial information of the data to achieve the target goal of the company

(Hamamura, 2019). The process of preparing the management accounts are offer on time,

accurate statistical financial information needed by the management to complete day to day task

of the firms. They show the report which are prepared to fulfil the requirements of the

management. Accounting shows the data which are measures, identify and interpreted the

economical data for the decision. Management accounting system applications varies in the data.

Every management accounting system gives various information based on the requirements of

the firm's management. There are various kinds of management accounting system with their

various objectives and functions where all the elements creates the standardized context of the

data to analysis and communicate the data in accounting system.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost Accounting System: It is the costing system is a framework used by the various

companies to calculate the cost of their products and analysis the inventory valuation,

profit analysis and to control the cost of the firm. In this cost system cost is performed on

the basis of activity based costing system or by traditional costing system. It shows the

approximate actual cost of the product for the effective functioning. Cost accounting

system is an accounting system which focuses on the cost of production considering the

inputs cost occurring on every production step plus fixed cost occurring in the production

like equipment depreciation. Cost accounting Measure cost individually and record and

then comparing the actual input of production and output from the production to compare

the financial performance of the firm. It is key concept in the management accounting as

they provide analytical tool like budgetary control, standard costing, marginal costing,

operational costing and inventory control of the firm to manage and work in the

efficiently. Cost-volume-profit : It helps the management to understand the relation between cost,

sales, volume and profits. It is an effect which are made by the cost on the profits and the

activity of financial report. They also known as Break even analysis which determine the

break even pointy for different level of sales volume and cost occurring which is useful to

manage the short term decision-making. It assumes the various factors like sales price,

fixed cost , and variable cost remains the same. Budgetary control: It is the process where budgets are prepared for the future period and

can be compared to the actual performance to know the variances of the company and

can be taken correct steps. This comparison brings out the discrepancies and correct steps

can be taken to avoid the losses. Budgetary control is the continuous process for the

organization which help in to stick with the plan and coordinating with management. Marginal costing: It is costing technique where marginal cost is a variable cost and are

charged from the cost of unit and fixed cost is written off completely against the

contribution. It can be calculated by dividing the change into cost of production by

change in quantity of the product. (Nan, 2019). Absorption cost: Is the marginal accounting method for calculating all the cost related to

the manufacturing product either direct or indirect cost such as direct material, direct

companies to calculate the cost of their products and analysis the inventory valuation,

profit analysis and to control the cost of the firm. In this cost system cost is performed on

the basis of activity based costing system or by traditional costing system. It shows the

approximate actual cost of the product for the effective functioning. Cost accounting

system is an accounting system which focuses on the cost of production considering the

inputs cost occurring on every production step plus fixed cost occurring in the production

like equipment depreciation. Cost accounting Measure cost individually and record and

then comparing the actual input of production and output from the production to compare

the financial performance of the firm. It is key concept in the management accounting as

they provide analytical tool like budgetary control, standard costing, marginal costing,

operational costing and inventory control of the firm to manage and work in the

efficiently. Cost-volume-profit : It helps the management to understand the relation between cost,

sales, volume and profits. It is an effect which are made by the cost on the profits and the

activity of financial report. They also known as Break even analysis which determine the

break even pointy for different level of sales volume and cost occurring which is useful to

manage the short term decision-making. It assumes the various factors like sales price,

fixed cost , and variable cost remains the same. Budgetary control: It is the process where budgets are prepared for the future period and

can be compared to the actual performance to know the variances of the company and

can be taken correct steps. This comparison brings out the discrepancies and correct steps

can be taken to avoid the losses. Budgetary control is the continuous process for the

organization which help in to stick with the plan and coordinating with management. Marginal costing: It is costing technique where marginal cost is a variable cost and are

charged from the cost of unit and fixed cost is written off completely against the

contribution. It can be calculated by dividing the change into cost of production by

change in quantity of the product. (Nan, 2019). Absorption cost: Is the marginal accounting method for calculating all the cost related to

the manufacturing product either direct or indirect cost such as direct material, direct

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

labour, rent etc. it is used to valuing the inventory and also refers to as full costing.

Absorption costing helps the external financial reporting and for income tax report. Inventory Management: It is the method of control the use and storage of the inventory

which are used for the production of good they sell. The application which are included

in the inventory management system include the barcode scanner, desktop software,

mobile devices for the smooth working of inventory such as goods, stock and supplies.

Also, it controls and supervise the quantities of goods which are sold in the market. The

main objective of the inventory management is known the accurate present level of

inventory and maintain the balance stock by minimize overstock and under-stock of good

in the organization. Firm can track the quantities of the stock and manager can take

correct decision on the production process of the firm. Job Costing System: It shows the manufacturing cost of individual items and batches of

the products. It is done when the goods are proceeded when two goods are different from

one another. It is to determine the accuracy and the estimate cost that can be offered to

the customer with come reasonable income. The job costing involves the three primary

expenses which are: material, labour and overhead. Price optimization system: It refers to the application of mathematical analysis of the

company's to identify the reaction of consumer on the various prices of the goods and

services from different channel. It also determines the prices of the product and service

which a company determines their goal like maximize the sales revenue. Finding an

alternative with the Highest performance and cost effective manner to maximize the

desired target and minimize the undesired targets in the company.

Different methods which are used to calculate the management accounting system: Cost Report: It calculates the cost of manufacturing of goods. It includes items like raw

material, costs, labour, product overhead and any extra cost which are to be considered in

the cost of manufacturing. All the cost is recorded on the cost report which shows the

capability to see the cost of product and comparing with selling price of the product. This

helps the manager to control and make the profits (De Rijdt, 2018). Cash Budget: It is the key element of management accounting to prepare the budget.

Cash Budgets are set by applying the budget of previous year and adjust to forecast the

Absorption costing helps the external financial reporting and for income tax report. Inventory Management: It is the method of control the use and storage of the inventory

which are used for the production of good they sell. The application which are included

in the inventory management system include the barcode scanner, desktop software,

mobile devices for the smooth working of inventory such as goods, stock and supplies.

Also, it controls and supervise the quantities of goods which are sold in the market. The

main objective of the inventory management is known the accurate present level of

inventory and maintain the balance stock by minimize overstock and under-stock of good

in the organization. Firm can track the quantities of the stock and manager can take

correct decision on the production process of the firm. Job Costing System: It shows the manufacturing cost of individual items and batches of

the products. It is done when the goods are proceeded when two goods are different from

one another. It is to determine the accuracy and the estimate cost that can be offered to

the customer with come reasonable income. The job costing involves the three primary

expenses which are: material, labour and overhead. Price optimization system: It refers to the application of mathematical analysis of the

company's to identify the reaction of consumer on the various prices of the goods and

services from different channel. It also determines the prices of the product and service

which a company determines their goal like maximize the sales revenue. Finding an

alternative with the Highest performance and cost effective manner to maximize the

desired target and minimize the undesired targets in the company.

Different methods which are used to calculate the management accounting system: Cost Report: It calculates the cost of manufacturing of goods. It includes items like raw

material, costs, labour, product overhead and any extra cost which are to be considered in

the cost of manufacturing. All the cost is recorded on the cost report which shows the

capability to see the cost of product and comparing with selling price of the product. This

helps the manager to control and make the profits (De Rijdt, 2018). Cash Budget: It is the key element of management accounting to prepare the budget.

Cash Budgets are set by applying the budget of previous year and adjust to forecast the

future. This includes inflow and outflow of expenses and revenue source. It helps the

company to attain the objective goal within the budgeted amount of the company.

However, it is the estimation of future company's cash position

Performance report : budgets are made to compare the actual revenue and expenditure to

the budget amount. This report is calculated each year by quarterly and half-yearly that

help the manger to plan the future demand of the product and fulfil the demand of the

market.

Advantage and disadvantage of planning tool used for budgetary control

Planning tools are the guidance for the company in order to plan different financial

concerns of the organization. Budgetary control means the process where budgets are arranged

for the future and can be compared with the actual result to find out the variances. This

comparison with the actual amount will help the management to find out the variances and

correct steps are taken to overcome. In case of budgetary control planning tools are the

supporting factors that can lead the organization to conduct the best level of financial planning.

Advantages of planning tools

Following are the different advantages associated with the budgetary planning that can

lead towards the best level of financial planning in favour of the organization. All these points

indicate all different advantages entertained against the financial planning.

Maximization of profit: Profit maximization is a key factor that support the company in

form of budgetary control. Planning tool guide company to utilize its financial stability in

the best way possible. Profit maximization is also considered as among the key objective

part of the business functions entertained by the organization (Nasrin, 2016). Planning

tools guide company in direct direction where organization can deliver the bes use of

company's financial resources. This is the significant advantage planning tool provide in

the overall objectives of the organization to channelizes business functions.

Improve financial management: Budgetary control is about to assess the needs and

requirements of the specific functional activity to control the financial requirements of

the company. All the planning tools allow company to analysis the financial requirements

associated with the specific functional area in order to achieve the best level of financial

stability in favour of the organization. Financial management is the key advantage that

budgetary control tools allocate to the organization (Rizqi, 2018). All these tools guide

company to attain the objective goal within the budgeted amount of the company.

However, it is the estimation of future company's cash position

Performance report : budgets are made to compare the actual revenue and expenditure to

the budget amount. This report is calculated each year by quarterly and half-yearly that

help the manger to plan the future demand of the product and fulfil the demand of the

market.

Advantage and disadvantage of planning tool used for budgetary control

Planning tools are the guidance for the company in order to plan different financial

concerns of the organization. Budgetary control means the process where budgets are arranged

for the future and can be compared with the actual result to find out the variances. This

comparison with the actual amount will help the management to find out the variances and

correct steps are taken to overcome. In case of budgetary control planning tools are the

supporting factors that can lead the organization to conduct the best level of financial planning.

Advantages of planning tools

Following are the different advantages associated with the budgetary planning that can

lead towards the best level of financial planning in favour of the organization. All these points

indicate all different advantages entertained against the financial planning.

Maximization of profit: Profit maximization is a key factor that support the company in

form of budgetary control. Planning tool guide company to utilize its financial stability in

the best way possible. Profit maximization is also considered as among the key objective

part of the business functions entertained by the organization (Nasrin, 2016). Planning

tools guide company in direct direction where organization can deliver the bes use of

company's financial resources. This is the significant advantage planning tool provide in

the overall objectives of the organization to channelizes business functions.

Improve financial management: Budgetary control is about to assess the needs and

requirements of the specific functional activity to control the financial requirements of

the company. All the planning tools allow company to analysis the financial requirements

associated with the specific functional area in order to achieve the best level of financial

stability in favour of the organization. Financial management is the key advantage that

budgetary control tools allocate to the organization (Rizqi, 2018). All these tools guide

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company to only allocate the required funds for every single functional activity based on

the needs and demand of every single operation which resist on behalf of the company in

blocking company's financial resources in form of excessive allocation of financial

resources to company.

Reduces cost of operations: Planning tools used for budgetary control allow the

organization to reduce the overall cost involved in conducting operations. All these tools

also support the company in controlling overall cost required to deliver the specific

services. Cost controlling is among the significant advantage these planning tools deliver

to the company. These tools highlight all significant areas that containing extra cost

which further reduce the overall cost of delivering the function. Reducing cost of

operation further allow company to maximize its overall profitability in order to

channelize business operations of organization (Makrygiannak, Jack, 2016).

Profit maximization: Profit maximization is among the key benefit planning tool

provide to the company. All these tools guide company to control the cost of delivering

the functional activity. Profit maximization can only be done by controlling the overall

cost to allocate the functional activity of organization. These tools make the operations

economical that in long run maximizes the overall profitability involved in delivering the

business operations. The above mentioned points indicate about the key benefits

associated with the planning tool in order to utilize them for delivering the business

objective and to achieve the best level of financial management.

Disadvantage of planning tool

Following are the points demonstrate the disadvantages associated with the planning tools for

conducting financial management.

Future is uncertain: All the planning tools used for conducting financial management

contain limitation in form of uncertainty. All these planning tool assume the specific

certainty about the future. The critical analysis of these tools indicate that future is not

certain and situation can change any time that will directly influence the overall cost

required to deliver the operations. Due to the uncertainty results of these planing tool

mislead company in most of the time. Uncertainty in relation to future activity is a key

disadvantage associated with the planning tool as those uncertainties will completely

restricts the financial planing outcomes of company. Many times company and

the needs and demand of every single operation which resist on behalf of the company in

blocking company's financial resources in form of excessive allocation of financial

resources to company.

Reduces cost of operations: Planning tools used for budgetary control allow the

organization to reduce the overall cost involved in conducting operations. All these tools

also support the company in controlling overall cost required to deliver the specific

services. Cost controlling is among the significant advantage these planning tools deliver

to the company. These tools highlight all significant areas that containing extra cost

which further reduce the overall cost of delivering the function. Reducing cost of

operation further allow company to maximize its overall profitability in order to

channelize business operations of organization (Makrygiannak, Jack, 2016).

Profit maximization: Profit maximization is among the key benefit planning tool

provide to the company. All these tools guide company to control the cost of delivering

the functional activity. Profit maximization can only be done by controlling the overall

cost to allocate the functional activity of organization. These tools make the operations

economical that in long run maximizes the overall profitability involved in delivering the

business operations. The above mentioned points indicate about the key benefits

associated with the planning tool in order to utilize them for delivering the business

objective and to achieve the best level of financial management.

Disadvantage of planning tool

Following are the points demonstrate the disadvantages associated with the planning tools for

conducting financial management.

Future is uncertain: All the planning tools used for conducting financial management

contain limitation in form of uncertainty. All these planning tool assume the specific

certainty about the future. The critical analysis of these tools indicate that future is not

certain and situation can change any time that will directly influence the overall cost

required to deliver the operations. Due to the uncertainty results of these planing tool

mislead company in most of the time. Uncertainty in relation to future activity is a key

disadvantage associated with the planning tool as those uncertainties will completely

restricts the financial planing outcomes of company. Many times company and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management remain in certain delusion that the future activity will exactly the same as

company is expecting which is not a real fact in any situation.

Extra cost incurred: Budgetary control requires extra cost to be incurred in conduction

of planning for all the budgetary requirements of company. The planning process always

create extra financial pressure over the resources of company. IT also consume plenty of

time in analysing the financial requirements and to plan the same. Extra cost uncured

over the planning price make the practice more burdensome over the financial stability of

the organization.

The above mentioned disadvantages are the key barrier part of the budgetary tools and

planning. All the above mentioned points generate the specific limitations in respect to establish

financial stability in the organization.

Part 2

Comparing how organization are adapting management accounting system to respond to

financial problem.

Companies encourage how they adopt their business models, strategies to be used,

producer to be followed to respond the environment and social challenges and maintain the value

of their stakeholder and sound financially strong in the market. Few companies accept the

challenges and confident to accept with required skills in sustainable economy. Some companies

are missed out the valuable analysis and fails to take the advantage set by the management

accounting. It makes the business scenario to analysis and sustain the effect of social

environmental factors on the organization performance.

Following managerial accounting ways that can be used to respond to financial problems:

Identifying financial issues by using budgetary target, key performing indicators either

financial or can be non financial and benchmarking to know the problems and variances and

solve them on time without any delay to surfer lose (Kaluzi, 2017). Financial governance of the

company should have knowledge about the governance and prevent it from the financial issue.

Company can be used this as a monitoring strategy of financial governance. Manager and

company should have the effective and efficient managerial skills to avoid the grievances on

management accounting. Also, with skills they can apply to prevent or deal with grievances such

as misappropriation of resources which help the company to grow. Whereas, effective strategy

system for the development and strategies that take time and gives the effective reporting such as

company is expecting which is not a real fact in any situation.

Extra cost incurred: Budgetary control requires extra cost to be incurred in conduction

of planning for all the budgetary requirements of company. The planning process always

create extra financial pressure over the resources of company. IT also consume plenty of

time in analysing the financial requirements and to plan the same. Extra cost uncured

over the planning price make the practice more burdensome over the financial stability of

the organization.

The above mentioned disadvantages are the key barrier part of the budgetary tools and

planning. All the above mentioned points generate the specific limitations in respect to establish

financial stability in the organization.

Part 2

Comparing how organization are adapting management accounting system to respond to

financial problem.

Companies encourage how they adopt their business models, strategies to be used,

producer to be followed to respond the environment and social challenges and maintain the value

of their stakeholder and sound financially strong in the market. Few companies accept the

challenges and confident to accept with required skills in sustainable economy. Some companies

are missed out the valuable analysis and fails to take the advantage set by the management

accounting. It makes the business scenario to analysis and sustain the effect of social

environmental factors on the organization performance.

Following managerial accounting ways that can be used to respond to financial problems:

Identifying financial issues by using budgetary target, key performing indicators either

financial or can be non financial and benchmarking to know the problems and variances and

solve them on time without any delay to surfer lose (Kaluzi, 2017). Financial governance of the

company should have knowledge about the governance and prevent it from the financial issue.

Company can be used this as a monitoring strategy of financial governance. Manager and

company should have the effective and efficient managerial skills to avoid the grievances on

management accounting. Also, with skills they can apply to prevent or deal with grievances such

as misappropriation of resources which help the company to grow. Whereas, effective strategy

system for the development and strategies that take time and gives the effective reporting such as

full disclosure of finical statement which is owned and make by the companies. To sustain the

business management accountant may guide the company with the report:

Finding the social and environmental trend which will affect the company to maintain the

value over the time.

Preparing the report on the impact of sustainability issue with comparing how and when

they will affect the company in future and what are the consequences.

Relate with the sustainable challenges with the strategies of the companies, performance

outlook of the company and with business model.

Key performance indicator (KPI) is the critical indicator of the progress toward the set

goal by the company. KPI can be established in the comp0any to support the sustainable

and strategic goal of the company.

Management accounting tools and techniques can be applied like availability of natural

resources, life cycle costing to guide incorporate sustainability into the process of

decision-making.

Creating the report which will affect the sustainability on pricing and budgeting decision

and strategic planning and investment decision (Schmitz, 2020).

Implementing the reporting strategy which result in sustainability matter to ensure the

non financial and financial data revealed. Example: The international incorporated

reporting framework established by IIRC.

Producing financial report.

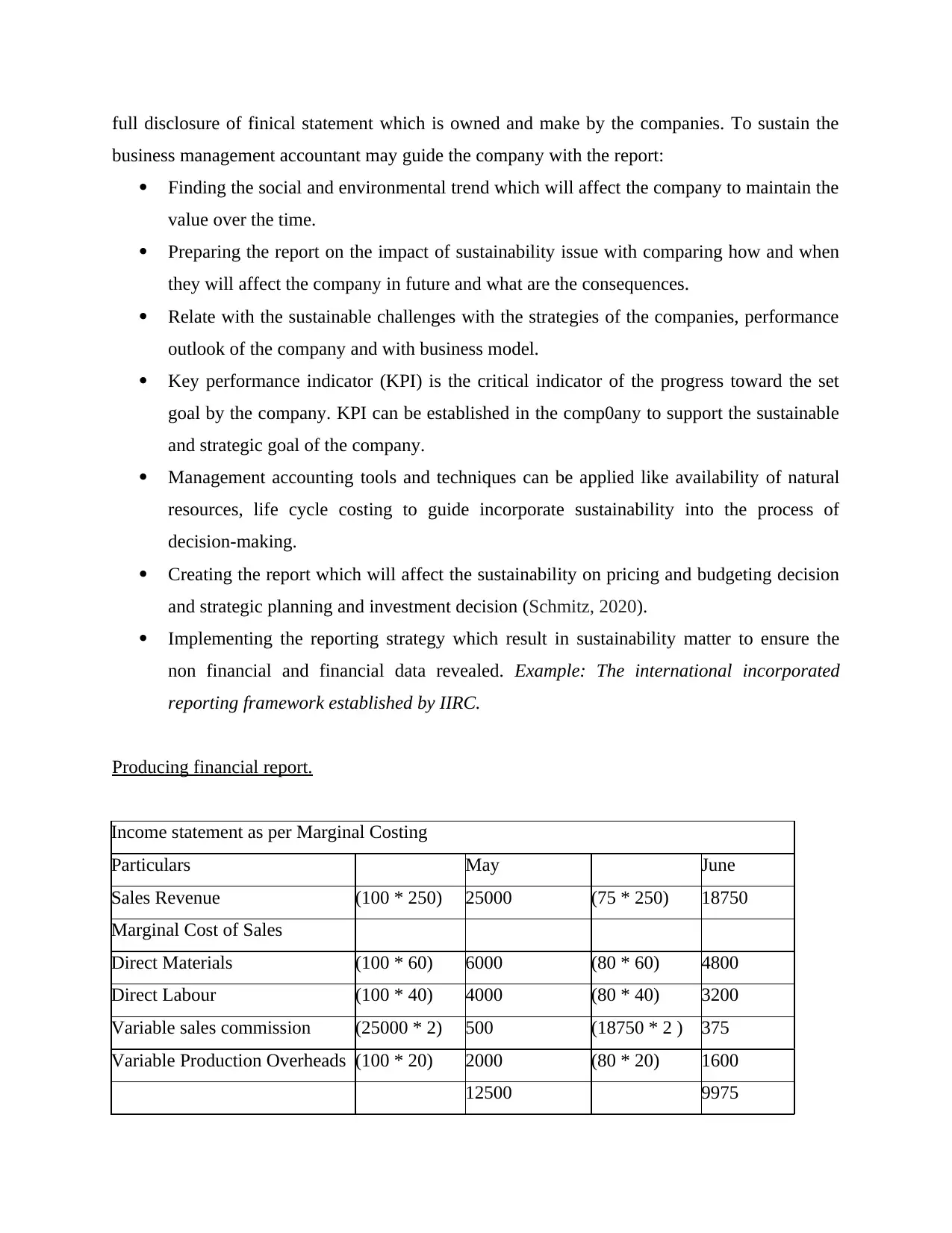

Income statement as per Marginal Costing

Particulars May June

Sales Revenue (100 * 250) 25000 (75 * 250) 18750

Marginal Cost of Sales

Direct Materials (100 * 60) 6000 (80 * 60) 4800

Direct Labour (100 * 40) 4000 (80 * 40) 3200

Variable sales commission (25000 * 2) 500 (18750 * 2 ) 375

Variable Production Overheads (100 * 20) 2000 (80 * 20) 1600

12500 9975

business management accountant may guide the company with the report:

Finding the social and environmental trend which will affect the company to maintain the

value over the time.

Preparing the report on the impact of sustainability issue with comparing how and when

they will affect the company in future and what are the consequences.

Relate with the sustainable challenges with the strategies of the companies, performance

outlook of the company and with business model.

Key performance indicator (KPI) is the critical indicator of the progress toward the set

goal by the company. KPI can be established in the comp0any to support the sustainable

and strategic goal of the company.

Management accounting tools and techniques can be applied like availability of natural

resources, life cycle costing to guide incorporate sustainability into the process of

decision-making.

Creating the report which will affect the sustainability on pricing and budgeting decision

and strategic planning and investment decision (Schmitz, 2020).

Implementing the reporting strategy which result in sustainability matter to ensure the

non financial and financial data revealed. Example: The international incorporated

reporting framework established by IIRC.

Producing financial report.

Income statement as per Marginal Costing

Particulars May June

Sales Revenue (100 * 250) 25000 (75 * 250) 18750

Marginal Cost of Sales

Direct Materials (100 * 60) 6000 (80 * 60) 4800

Direct Labour (100 * 40) 4000 (80 * 40) 3200

Variable sales commission (25000 * 2) 500 (18750 * 2 ) 375

Variable Production Overheads (100 * 20) 2000 (80 * 20) 1600

12500 9975

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

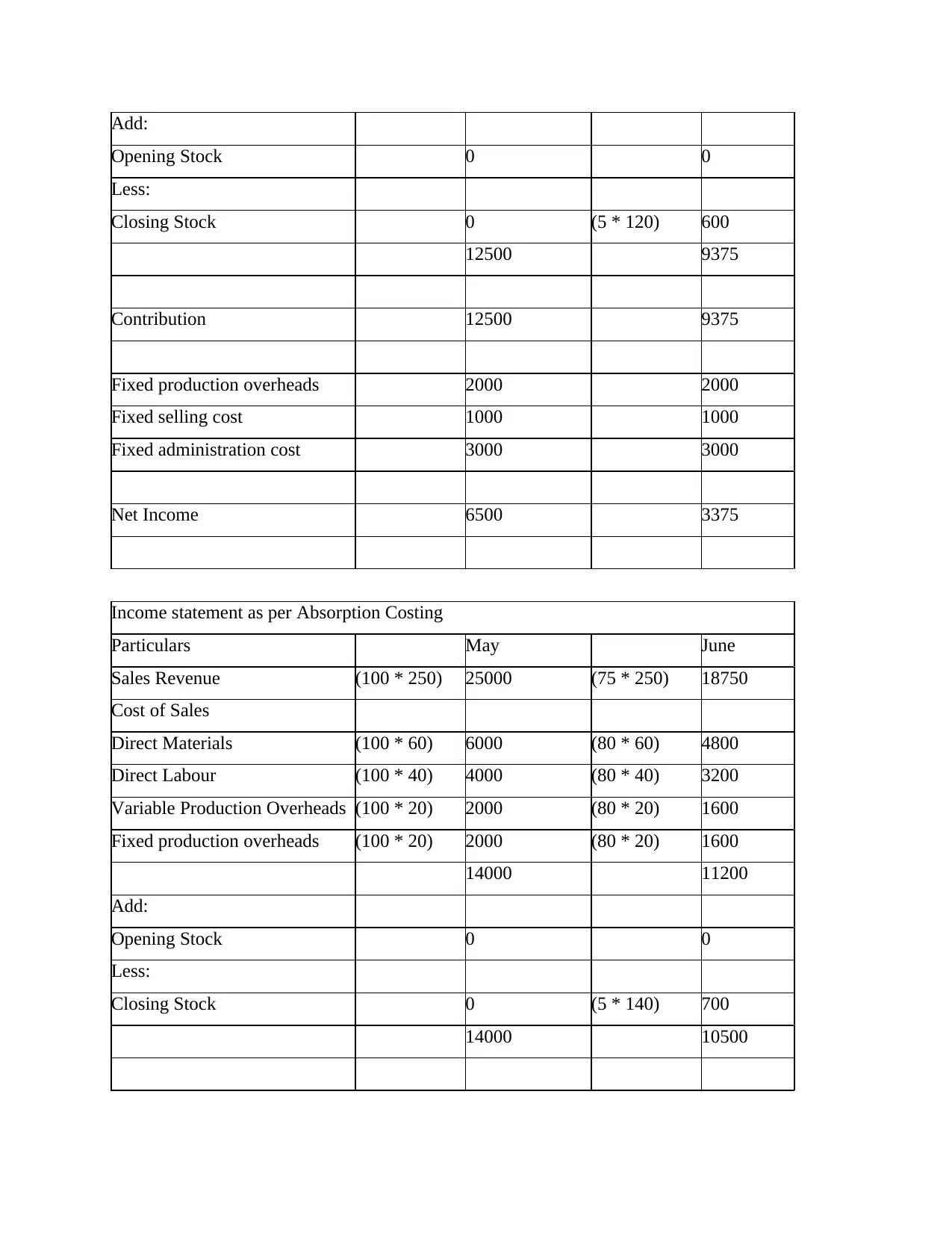

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5 * 120) 600

12500 9375

Contribution 12500 9375

Fixed production overheads 2000 2000

Fixed selling cost 1000 1000

Fixed administration cost 3000 3000

Net Income 6500 3375

Income statement as per Absorption Costing

Particulars May June

Sales Revenue (100 * 250) 25000 (75 * 250) 18750

Cost of Sales

Direct Materials (100 * 60) 6000 (80 * 60) 4800

Direct Labour (100 * 40) 4000 (80 * 40) 3200

Variable Production Overheads (100 * 20) 2000 (80 * 20) 1600

Fixed production overheads (100 * 20) 2000 (80 * 20) 1600

14000 11200

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5 * 140) 700

14000 10500

Opening Stock 0 0

Less:

Closing Stock 0 (5 * 120) 600

12500 9375

Contribution 12500 9375

Fixed production overheads 2000 2000

Fixed selling cost 1000 1000

Fixed administration cost 3000 3000

Net Income 6500 3375

Income statement as per Absorption Costing

Particulars May June

Sales Revenue (100 * 250) 25000 (75 * 250) 18750

Cost of Sales

Direct Materials (100 * 60) 6000 (80 * 60) 4800

Direct Labour (100 * 40) 4000 (80 * 40) 3200

Variable Production Overheads (100 * 20) 2000 (80 * 20) 1600

Fixed production overheads (100 * 20) 2000 (80 * 20) 1600

14000 11200

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5 * 140) 700

14000 10500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

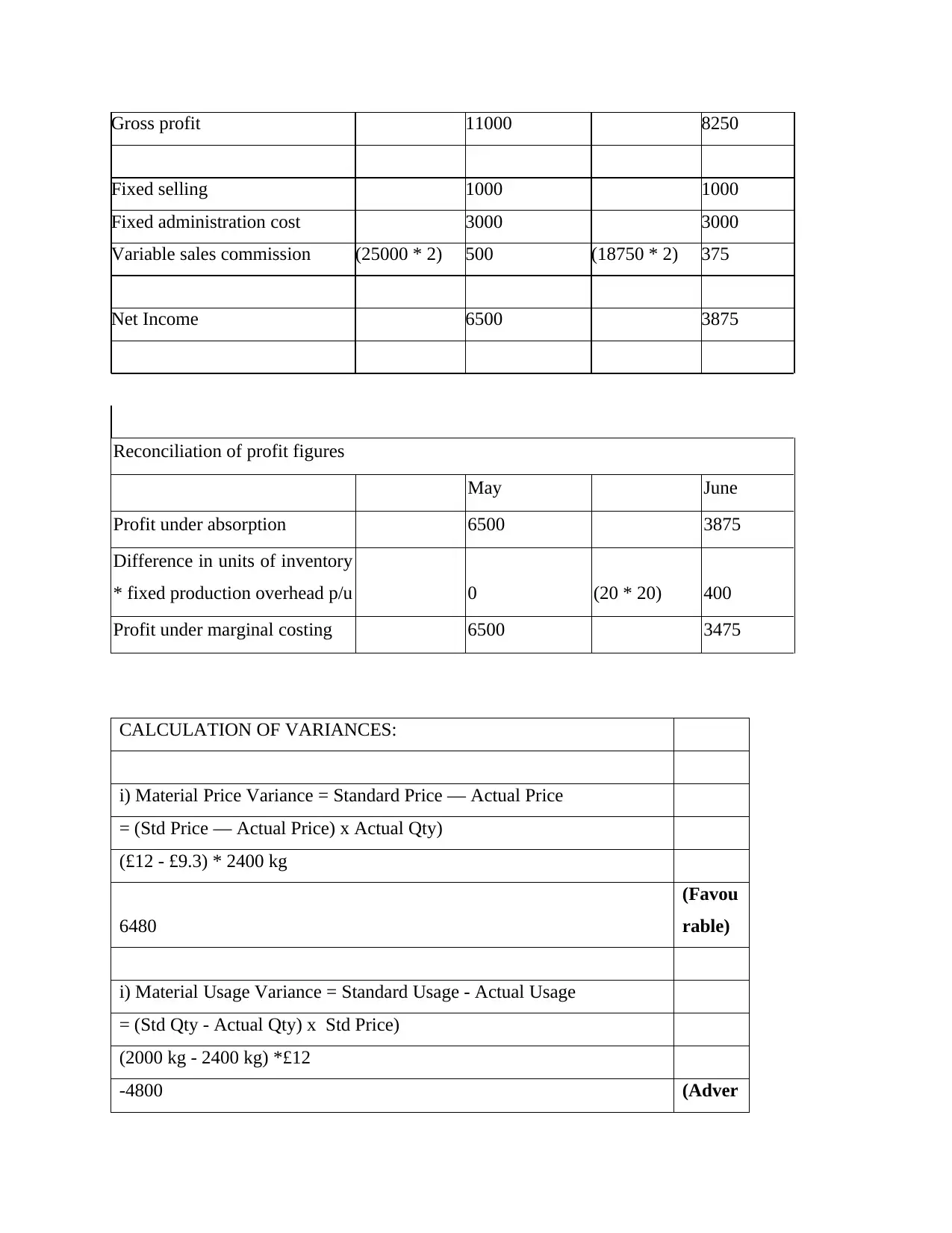

Gross profit 11000 8250

Fixed selling 1000 1000

Fixed administration cost 3000 3000

Variable sales commission (25000 * 2) 500 (18750 * 2) 375

Net Income 6500 3875

Reconciliation of profit figures

May June

Profit under absorption 6500 3875

Difference in units of inventory

* fixed production overhead p/u 0 (20 * 20) 400

Profit under marginal costing 6500 3475

CALCULATION OF VARIANCES:

i) Material Price Variance = Standard Price — Actual Price

= (Std Price — Actual Price) x Actual Qty)

(£12 - £9.3) * 2400 kg

6480

(Favou

rable)

i) Material Usage Variance = Standard Usage - Actual Usage

= (Std Qty - Actual Qty) x Std Price)

(2000 kg - 2400 kg) *£12

-4800 (Adver

Fixed selling 1000 1000

Fixed administration cost 3000 3000

Variable sales commission (25000 * 2) 500 (18750 * 2) 375

Net Income 6500 3875

Reconciliation of profit figures

May June

Profit under absorption 6500 3875

Difference in units of inventory

* fixed production overhead p/u 0 (20 * 20) 400

Profit under marginal costing 6500 3475

CALCULATION OF VARIANCES:

i) Material Price Variance = Standard Price — Actual Price

= (Std Price — Actual Price) x Actual Qty)

(£12 - £9.3) * 2400 kg

6480

(Favou

rable)

i) Material Usage Variance = Standard Usage - Actual Usage

= (Std Qty - Actual Qty) x Std Price)

(2000 kg - 2400 kg) *£12

-4800 (Adver

se)

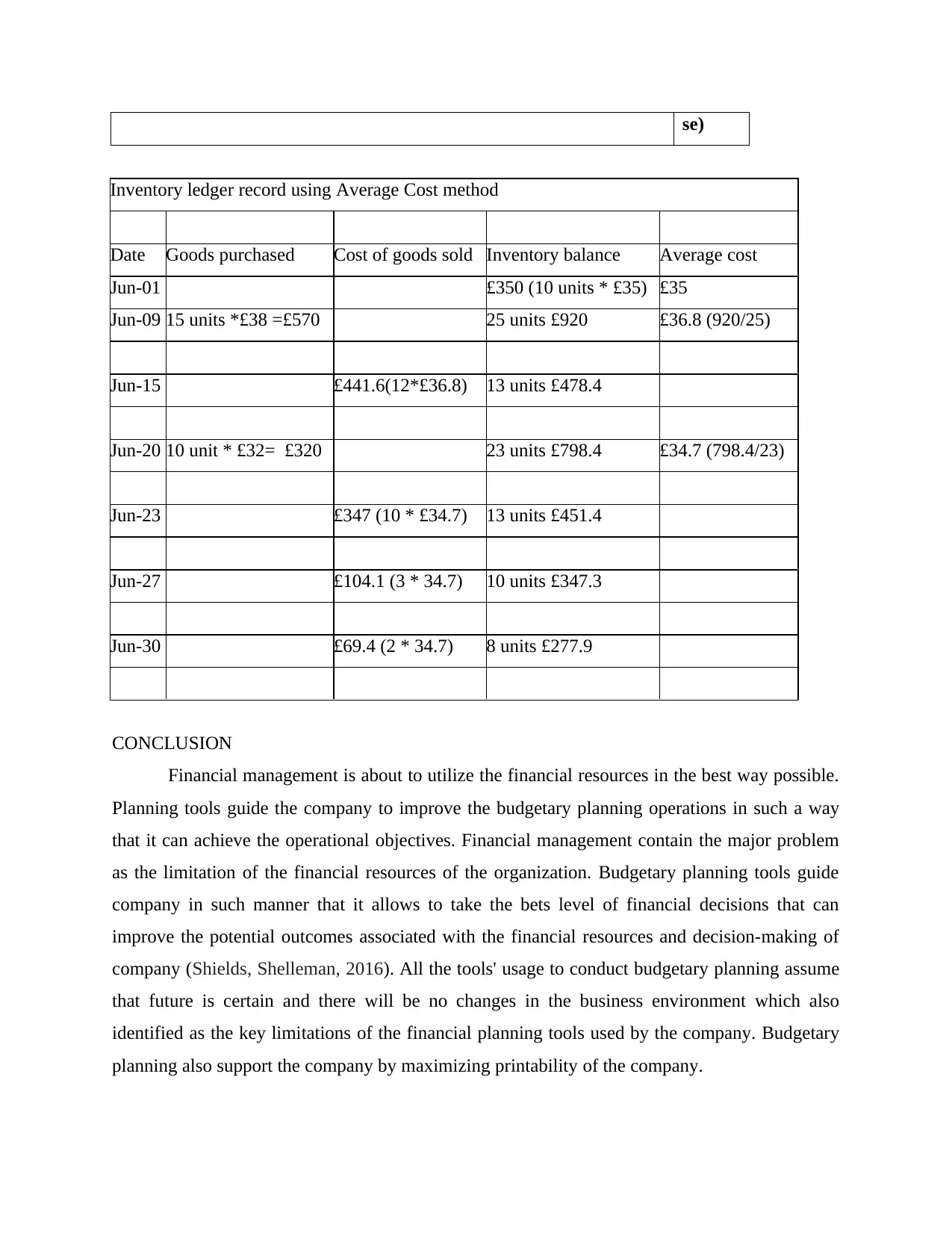

Inventory ledger record using Average Cost method

Date Goods purchased Cost of goods sold Inventory balance Average cost

Jun-01 £350 (10 units * £35) £35

Jun-09 15 units *£38 =£570 25 units £920 £36.8 (920/25)

Jun-15 £441.6(12*£36.8) 13 units £478.4

Jun-20 10 unit * £32= £320 23 units £798.4 £34.7 (798.4/23)

Jun-23 £347 (10 * £34.7) 13 units £451.4

Jun-27 £104.1 (3 * 34.7) 10 units £347.3

Jun-30 £69.4 (2 * 34.7) 8 units £277.9

CONCLUSION

Financial management is about to utilize the financial resources in the best way possible.

Planning tools guide the company to improve the budgetary planning operations in such a way

that it can achieve the operational objectives. Financial management contain the major problem

as the limitation of the financial resources of the organization. Budgetary planning tools guide

company in such manner that it allows to take the bets level of financial decisions that can

improve the potential outcomes associated with the financial resources and decision-making of

company (Shields, Shelleman, 2016). All the tools' usage to conduct budgetary planning assume

that future is certain and there will be no changes in the business environment which also

identified as the key limitations of the financial planning tools used by the company. Budgetary

planning also support the company by maximizing printability of the company.

Inventory ledger record using Average Cost method

Date Goods purchased Cost of goods sold Inventory balance Average cost

Jun-01 £350 (10 units * £35) £35

Jun-09 15 units *£38 =£570 25 units £920 £36.8 (920/25)

Jun-15 £441.6(12*£36.8) 13 units £478.4

Jun-20 10 unit * £32= £320 23 units £798.4 £34.7 (798.4/23)

Jun-23 £347 (10 * £34.7) 13 units £451.4

Jun-27 £104.1 (3 * 34.7) 10 units £347.3

Jun-30 £69.4 (2 * 34.7) 8 units £277.9

CONCLUSION

Financial management is about to utilize the financial resources in the best way possible.

Planning tools guide the company to improve the budgetary planning operations in such a way

that it can achieve the operational objectives. Financial management contain the major problem

as the limitation of the financial resources of the organization. Budgetary planning tools guide

company in such manner that it allows to take the bets level of financial decisions that can

improve the potential outcomes associated with the financial resources and decision-making of

company (Shields, Shelleman, 2016). All the tools' usage to conduct budgetary planning assume

that future is certain and there will be no changes in the business environment which also

identified as the key limitations of the financial planning tools used by the company. Budgetary

planning also support the company by maximizing printability of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.