Management Accounting Report: Techniques and Organizational Processes

VerifiedAdded on 2022/12/28

|19

|4588

|43

Report

AI Summary

This report delves into the core concepts of management accounting, focusing on its role in aiding business decision-making and resource allocation. It examines essential requirements for different management accounting systems, emphasizing their benefits and applications within an organizational context. The report explores various reporting methods, including budgeting and variance analysis, and evaluates their integration within organizational processes, using Connect Catering Services as a case study. Furthermore, it covers cost analysis techniques such as marginal and absorption costing, with practical application in preparing income statements. The report also analyzes different planning tools used for budgetary control, outlining their advantages and disadvantages. Finally, it includes financial reports, such as break-even analysis and variance analysis, to demonstrate the application of management accounting techniques in real-world scenarios.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management Accounting refers to provision of financial information that assist a company in

using its resources, making decisions also to develop and expand its business operations. It is

made up of two words that is management and accounting that focuses on increasing efficiency

in business processes and facilitates in providing information that is necessary for management

committee of the organization (Armitage, 2020). As per Cost and Management Accounts,

London, Management Accounting is based on presenting professional information and capability

of showcasing knowledge related to accounting, which assists the managing committee in

formulating policies, plans and in controlling for undertakings. It deals with preparation of

reports that helps internal management of the company in evaluating their performance and

taking decisions accordingly.

This report is based on Connect catering Services, one of the best catering brands

established in UK, having its headquarters in Oxfordshire, UK. It has initiated its operations in

the year 1989, by John Herring.

TASK 1

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.

Management accounting also referred as managerial accounting facilitates in achieving

goals and objectives of the organisation with the use of measuring, classifying, evaluating and

communicating information related to commercial activities of a company (Kurdestani, 2020) .

It provides a clear picture about statical data and info of company’s activities that have a

financial impact over the company. The purpose of it is to make workforce more targeted and

goal oriented by evaluating their performance and motivating them to increase their productivity.

It helps in setting standard performance, comparing it with actual performance, finding

deviations and overcoming such performance gaps.

Management Accounting refers to provision of financial information that assist a company in

using its resources, making decisions also to develop and expand its business operations. It is

made up of two words that is management and accounting that focuses on increasing efficiency

in business processes and facilitates in providing information that is necessary for management

committee of the organization (Armitage, 2020). As per Cost and Management Accounts,

London, Management Accounting is based on presenting professional information and capability

of showcasing knowledge related to accounting, which assists the managing committee in

formulating policies, plans and in controlling for undertakings. It deals with preparation of

reports that helps internal management of the company in evaluating their performance and

taking decisions accordingly.

This report is based on Connect catering Services, one of the best catering brands

established in UK, having its headquarters in Oxfordshire, UK. It has initiated its operations in

the year 1989, by John Herring.

TASK 1

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.

Management accounting also referred as managerial accounting facilitates in achieving

goals and objectives of the organisation with the use of measuring, classifying, evaluating and

communicating information related to commercial activities of a company (Kurdestani, 2020) .

It provides a clear picture about statical data and info of company’s activities that have a

financial impact over the company. The purpose of it is to make workforce more targeted and

goal oriented by evaluating their performance and motivating them to increase their productivity.

It helps in setting standard performance, comparing it with actual performance, finding

deviations and overcoming such performance gaps.

• Measurement of presentation: It helps an organisation to evaluate and implement the

completion of worker’s activity. This helps in managing acute and effective plan of action used

for developing an effective plan.

• Categorisation of risk: Another advantage of management accounting or managerial

accounting is recognising the risk element for the company.

• Allotment of resources: Company will face problem in is sufficiently capable to

achieve the utilisation of resources with efficiency that helps the various sections to

have the distinct point of view for every section and figures in the organisation (Loy,

2020.). It also includes the summarizing, analysing and coverage the resources that

supervise the financial information.

P2 Explain different methods used for management accounting reporting.

Management accounting is the process for communicating with information related to

statistics and finance. This is involved in serving the complexities of organization effectively and

managing audit and accounting.

Budget: This is known as the total of income and cost and according to the concept of

macroeconomics, it is known as the interval which is followed by governing bodies,

administrative body and list. This method starts with assuming the success of future.

There is need to implement effective financing so that project can be completed

efficiently.

Variance analysis: It is the part of fund control activity in which a budget for income,

revenue and expenses is differentiate with the actual report of the enterprise and the

statement usually carry forward to classify the enterprise presentation in respect of the

plan and policies that ensures by the management.

M1 Evaluate the benefits of management accounting systems and their application within an

organizational context.

Management accounting is a process to determine, examine and conveys all important

information to managers which is helpful to make decisions and having knowledge about the

cost of accounting to achieve goals of organization in effective manner. Management accounting

is beneficial for every organization to plan all activities sequentially for effective operations.

completion of worker’s activity. This helps in managing acute and effective plan of action used

for developing an effective plan.

• Categorisation of risk: Another advantage of management accounting or managerial

accounting is recognising the risk element for the company.

• Allotment of resources: Company will face problem in is sufficiently capable to

achieve the utilisation of resources with efficiency that helps the various sections to

have the distinct point of view for every section and figures in the organisation (Loy,

2020.). It also includes the summarizing, analysing and coverage the resources that

supervise the financial information.

P2 Explain different methods used for management accounting reporting.

Management accounting is the process for communicating with information related to

statistics and finance. This is involved in serving the complexities of organization effectively and

managing audit and accounting.

Budget: This is known as the total of income and cost and according to the concept of

macroeconomics, it is known as the interval which is followed by governing bodies,

administrative body and list. This method starts with assuming the success of future.

There is need to implement effective financing so that project can be completed

efficiently.

Variance analysis: It is the part of fund control activity in which a budget for income,

revenue and expenses is differentiate with the actual report of the enterprise and the

statement usually carry forward to classify the enterprise presentation in respect of the

plan and policies that ensures by the management.

M1 Evaluate the benefits of management accounting systems and their application within an

organizational context.

Management accounting is a process to determine, examine and conveys all important

information to managers which is helpful to make decisions and having knowledge about the

cost of accounting to achieve goals of organization in effective manner. Management accounting

is beneficial for every organization to plan all activities sequentially for effective operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There are various type budgets and accounts are prepared which are divided in various form such

as department and product. Actual performance is compared with standard set and if there are

some variances raised mangers find out reasons behind and take actions to solve them.

Management accounting explains responsibilities of executives and their area of working so

there is no confusion regarding work; everything is done in well-organized manner. It Manages

and coordinate all finance, production, and personal activities of an organization to achieve

objectives. It also removes all wastage and unnecessary activities which saves time to perform

activities and also improves efficiency of organization.

D1 Critically evaluate how management accounting systems and management accounting

reporting is integrated within organizational processes.

Management accounting refers to process of quantifying, measuring and evaluating

results to judge performance of a company. It facilitates decision making in an organization and

provides information relating to its operational and financial efficiency in terms of projects

undertaken. Cost management process in an organization is vital for regular improvement in its

business operations so as to focus on minimizing cost of production and increasing efficiency in

its processes.

Report Type Integration of report with organizational process

Budget Reports This report helps connect catering services in setting up goals

and targets and provide it the direction for its achievement in

most optimum way.

Job Cost Reports This report facilitates connect catering services in minimizing

their production cost and provides the path for setting of

prices and fulfilling their cost objectives.

Performance Reports This report assist connect catering services in evaluating their

performance with past experiences and to manage their future

plans of production for enhancing profitability by minimizing

cost.

Order Information Reports This report helps connect catering services in keeping a track

of sales made and analyzes information that relates to

fulfilling customer orders in an effective manner and on given

as department and product. Actual performance is compared with standard set and if there are

some variances raised mangers find out reasons behind and take actions to solve them.

Management accounting explains responsibilities of executives and their area of working so

there is no confusion regarding work; everything is done in well-organized manner. It Manages

and coordinate all finance, production, and personal activities of an organization to achieve

objectives. It also removes all wastage and unnecessary activities which saves time to perform

activities and also improves efficiency of organization.

D1 Critically evaluate how management accounting systems and management accounting

reporting is integrated within organizational processes.

Management accounting refers to process of quantifying, measuring and evaluating

results to judge performance of a company. It facilitates decision making in an organization and

provides information relating to its operational and financial efficiency in terms of projects

undertaken. Cost management process in an organization is vital for regular improvement in its

business operations so as to focus on minimizing cost of production and increasing efficiency in

its processes.

Report Type Integration of report with organizational process

Budget Reports This report helps connect catering services in setting up goals

and targets and provide it the direction for its achievement in

most optimum way.

Job Cost Reports This report facilitates connect catering services in minimizing

their production cost and provides the path for setting of

prices and fulfilling their cost objectives.

Performance Reports This report assist connect catering services in evaluating their

performance with past experiences and to manage their future

plans of production for enhancing profitability by minimizing

cost.

Order Information Reports This report helps connect catering services in keeping a track

of sales made and analyzes information that relates to

fulfilling customer orders in an effective manner and on given

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

time.

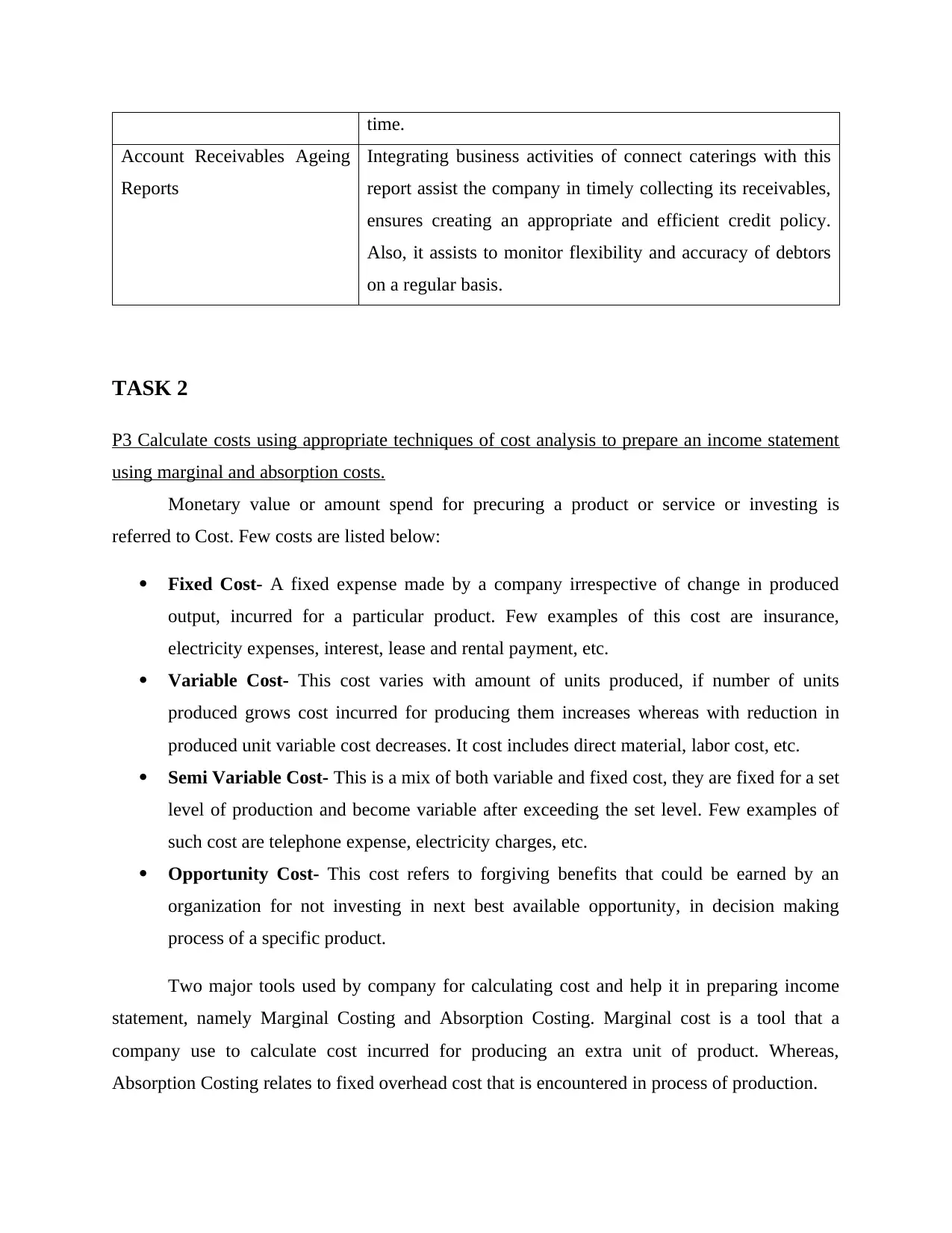

Account Receivables Ageing

Reports

Integrating business activities of connect caterings with this

report assist the company in timely collecting its receivables,

ensures creating an appropriate and efficient credit policy.

Also, it assists to monitor flexibility and accuracy of debtors

on a regular basis.

TASK 2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

Monetary value or amount spend for precuring a product or service or investing is

referred to Cost. Few costs are listed below:

Fixed Cost- A fixed expense made by a company irrespective of change in produced

output, incurred for a particular product. Few examples of this cost are insurance,

electricity expenses, interest, lease and rental payment, etc.

Variable Cost- This cost varies with amount of units produced, if number of units

produced grows cost incurred for producing them increases whereas with reduction in

produced unit variable cost decreases. It cost includes direct material, labor cost, etc.

Semi Variable Cost- This is a mix of both variable and fixed cost, they are fixed for a set

level of production and become variable after exceeding the set level. Few examples of

such cost are telephone expense, electricity charges, etc.

Opportunity Cost- This cost refers to forgiving benefits that could be earned by an

organization for not investing in next best available opportunity, in decision making

process of a specific product.

Two major tools used by company for calculating cost and help it in preparing income

statement, namely Marginal Costing and Absorption Costing. Marginal cost is a tool that a

company use to calculate cost incurred for producing an extra unit of product. Whereas,

Absorption Costing relates to fixed overhead cost that is encountered in process of production.

Account Receivables Ageing

Reports

Integrating business activities of connect caterings with this

report assist the company in timely collecting its receivables,

ensures creating an appropriate and efficient credit policy.

Also, it assists to monitor flexibility and accuracy of debtors

on a regular basis.

TASK 2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

Monetary value or amount spend for precuring a product or service or investing is

referred to Cost. Few costs are listed below:

Fixed Cost- A fixed expense made by a company irrespective of change in produced

output, incurred for a particular product. Few examples of this cost are insurance,

electricity expenses, interest, lease and rental payment, etc.

Variable Cost- This cost varies with amount of units produced, if number of units

produced grows cost incurred for producing them increases whereas with reduction in

produced unit variable cost decreases. It cost includes direct material, labor cost, etc.

Semi Variable Cost- This is a mix of both variable and fixed cost, they are fixed for a set

level of production and become variable after exceeding the set level. Few examples of

such cost are telephone expense, electricity charges, etc.

Opportunity Cost- This cost refers to forgiving benefits that could be earned by an

organization for not investing in next best available opportunity, in decision making

process of a specific product.

Two major tools used by company for calculating cost and help it in preparing income

statement, namely Marginal Costing and Absorption Costing. Marginal cost is a tool that a

company use to calculate cost incurred for producing an extra unit of product. Whereas,

Absorption Costing relates to fixed overhead cost that is encountered in process of production.

M2 Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents.

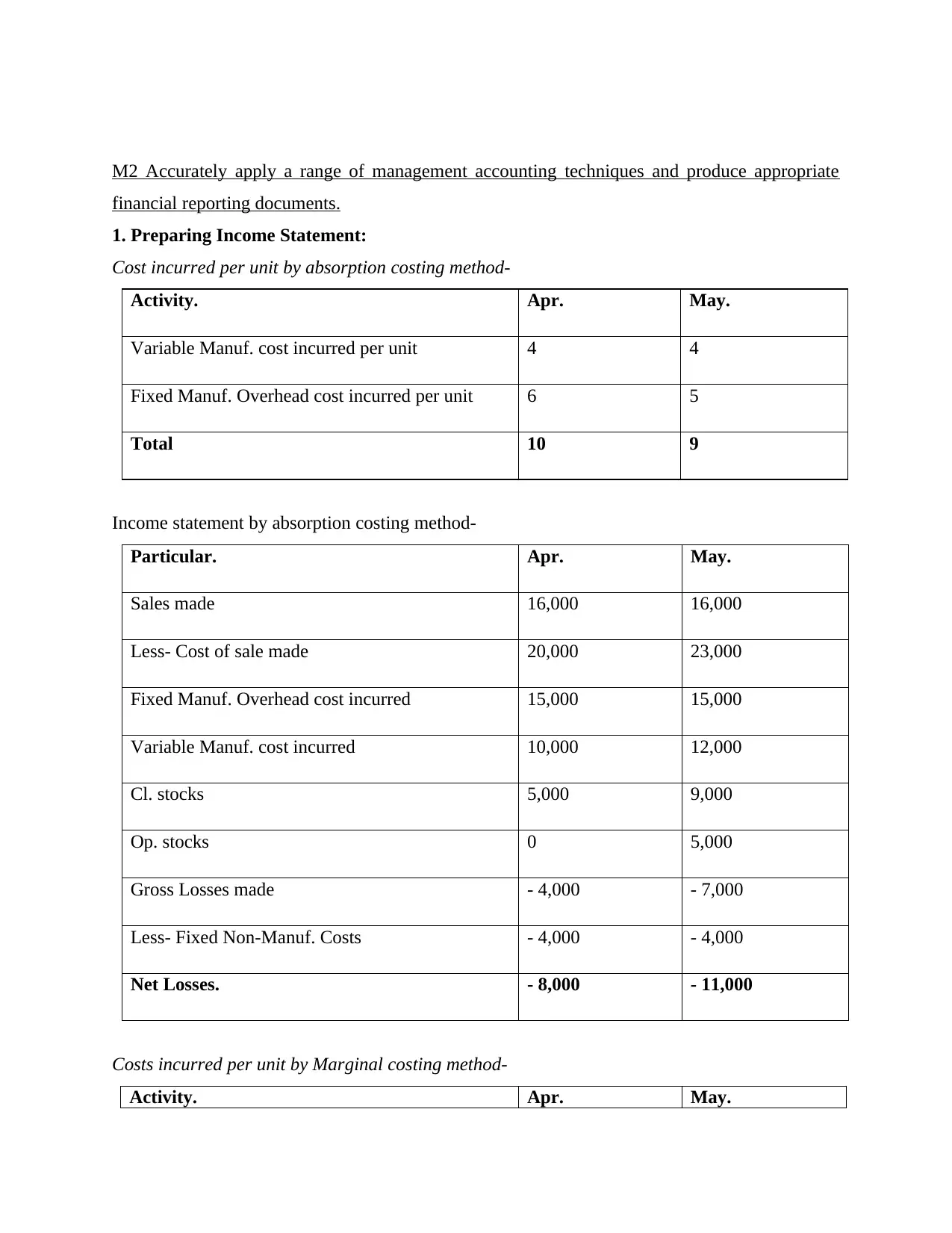

1. Preparing Income Statement:

Cost incurred per unit by absorption costing method-

Activity. Apr. May.

Variable Manuf. cost incurred per unit 4 4

Fixed Manuf. Overhead cost incurred per unit 6 5

Total 10 9

Income statement by absorption costing method-

Particular. Apr. May.

Sales made 16,000 16,000

Less- Cost of sale made 20,000 23,000

Fixed Manuf. Overhead cost incurred 15,000 15,000

Variable Manuf. cost incurred 10,000 12,000

Cl. stocks 5,000 9,000

Op. stocks 0 5,000

Gross Losses made - 4,000 - 7,000

Less- Fixed Non-Manuf. Costs - 4,000 - 4,000

Net Losses. - 8,000 - 11,000

Costs incurred per unit by Marginal costing method-

Activity. Apr. May.

financial reporting documents.

1. Preparing Income Statement:

Cost incurred per unit by absorption costing method-

Activity. Apr. May.

Variable Manuf. cost incurred per unit 4 4

Fixed Manuf. Overhead cost incurred per unit 6 5

Total 10 9

Income statement by absorption costing method-

Particular. Apr. May.

Sales made 16,000 16,000

Less- Cost of sale made 20,000 23,000

Fixed Manuf. Overhead cost incurred 15,000 15,000

Variable Manuf. cost incurred 10,000 12,000

Cl. stocks 5,000 9,000

Op. stocks 0 5,000

Gross Losses made - 4,000 - 7,000

Less- Fixed Non-Manuf. Costs - 4,000 - 4,000

Net Losses. - 8,000 - 11,000

Costs incurred per unit by Marginal costing method-

Activity. Apr. May.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable Manuf. costs per unit 4 4

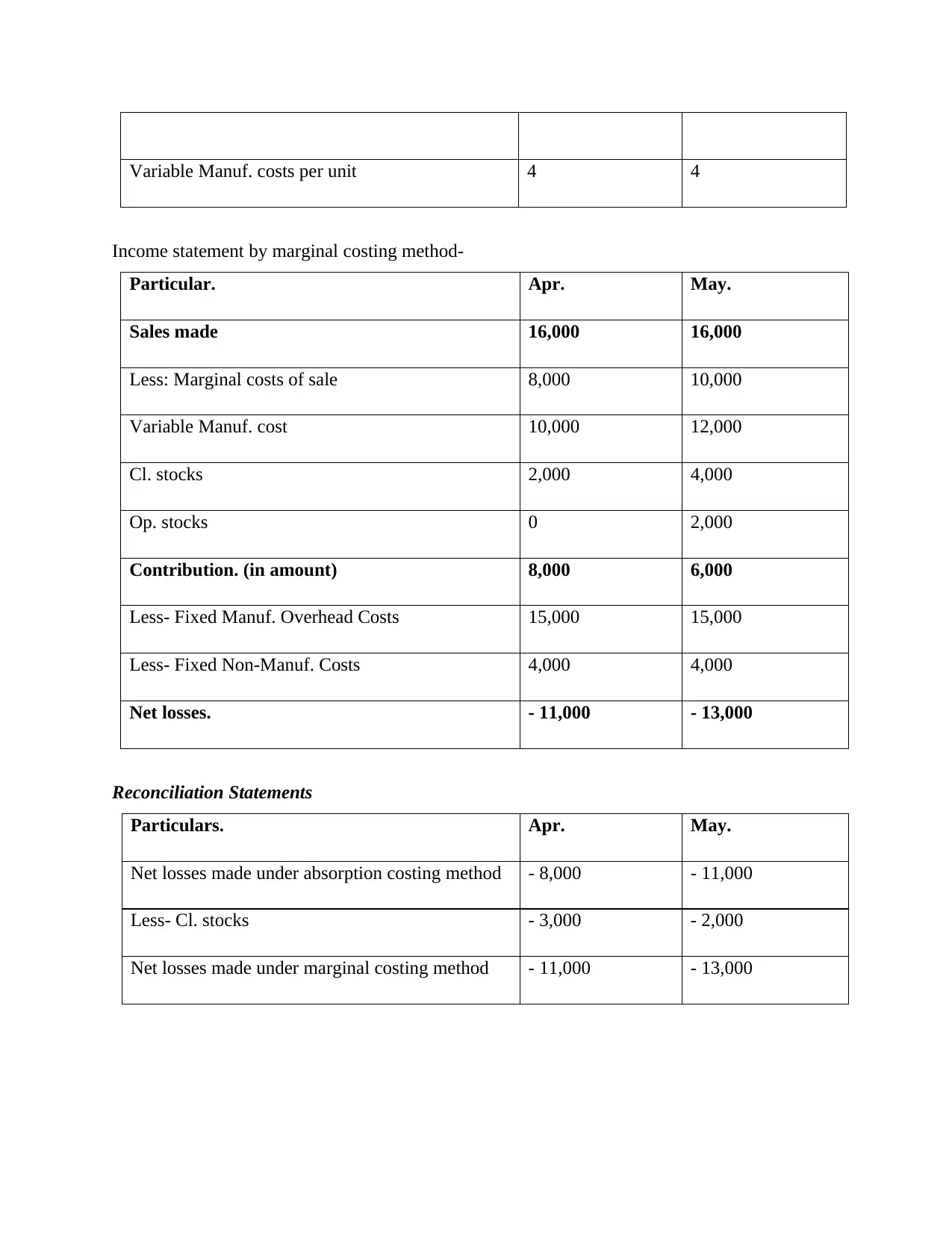

Income statement by marginal costing method-

Particular. Apr. May.

Sales made 16,000 16,000

Less: Marginal costs of sale 8,000 10,000

Variable Manuf. cost 10,000 12,000

Cl. stocks 2,000 4,000

Op. stocks 0 2,000

Contribution. (in amount) 8,000 6,000

Less- Fixed Manuf. Overhead Costs 15,000 15,000

Less- Fixed Non-Manuf. Costs 4,000 4,000

Net losses. - 11,000 - 13,000

Reconciliation Statements

Particulars. Apr. May.

Net losses made under absorption costing method - 8,000 - 11,000

Less- Cl. stocks - 3,000 - 2,000

Net losses made under marginal costing method - 11,000 - 13,000

Income statement by marginal costing method-

Particular. Apr. May.

Sales made 16,000 16,000

Less: Marginal costs of sale 8,000 10,000

Variable Manuf. cost 10,000 12,000

Cl. stocks 2,000 4,000

Op. stocks 0 2,000

Contribution. (in amount) 8,000 6,000

Less- Fixed Manuf. Overhead Costs 15,000 15,000

Less- Fixed Non-Manuf. Costs 4,000 4,000

Net losses. - 11,000 - 13,000

Reconciliation Statements

Particulars. Apr. May.

Net losses made under absorption costing method - 8,000 - 11,000

Less- Cl. stocks - 3,000 - 2,000

Net losses made under marginal costing method - 11,000 - 13,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D2 Produce financial reports that accurately apply and interpret data for a range of business

activities.

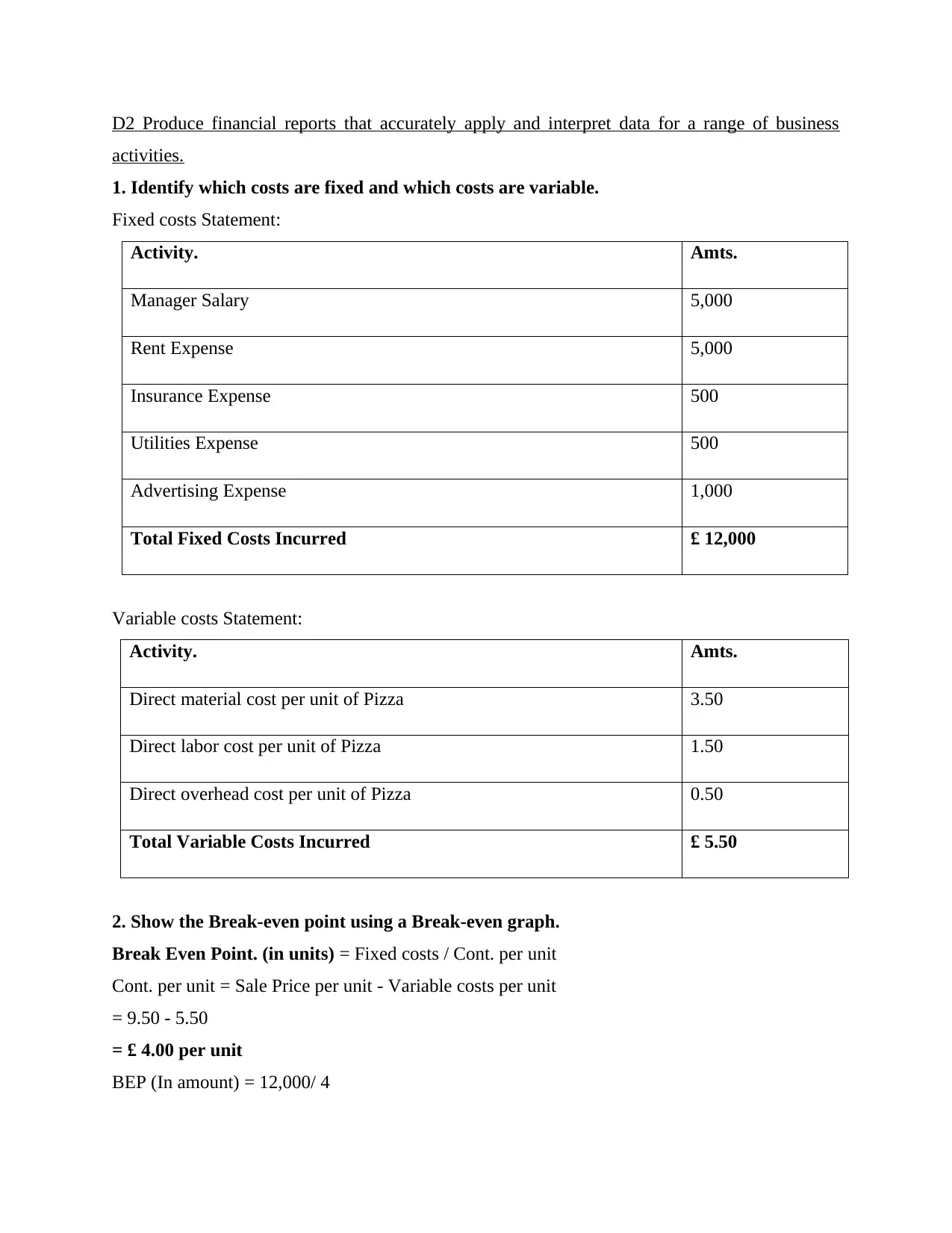

1. Identify which costs are fixed and which costs are variable.

Fixed costs Statement:

Activity. Amts.

Manager Salary 5,000

Rent Expense 5,000

Insurance Expense 500

Utilities Expense 500

Advertising Expense 1,000

Total Fixed Costs Incurred £ 12,000

Variable costs Statement:

Activity. Amts.

Direct material cost per unit of Pizza 3.50

Direct labor cost per unit of Pizza 1.50

Direct overhead cost per unit of Pizza 0.50

Total Variable Costs Incurred £ 5.50

2. Show the Break-even point using a Break-even graph.

Break Even Point. (in units) = Fixed costs / Cont. per unit

Cont. per unit = Sale Price per unit - Variable costs per unit

= 9.50 - 5.50

= £ 4.00 per unit

BEP (In amount) = 12,000/ 4

activities.

1. Identify which costs are fixed and which costs are variable.

Fixed costs Statement:

Activity. Amts.

Manager Salary 5,000

Rent Expense 5,000

Insurance Expense 500

Utilities Expense 500

Advertising Expense 1,000

Total Fixed Costs Incurred £ 12,000

Variable costs Statement:

Activity. Amts.

Direct material cost per unit of Pizza 3.50

Direct labor cost per unit of Pizza 1.50

Direct overhead cost per unit of Pizza 0.50

Total Variable Costs Incurred £ 5.50

2. Show the Break-even point using a Break-even graph.

Break Even Point. (in units) = Fixed costs / Cont. per unit

Cont. per unit = Sale Price per unit - Variable costs per unit

= 9.50 - 5.50

= £ 4.00 per unit

BEP (In amount) = 12,000/ 4

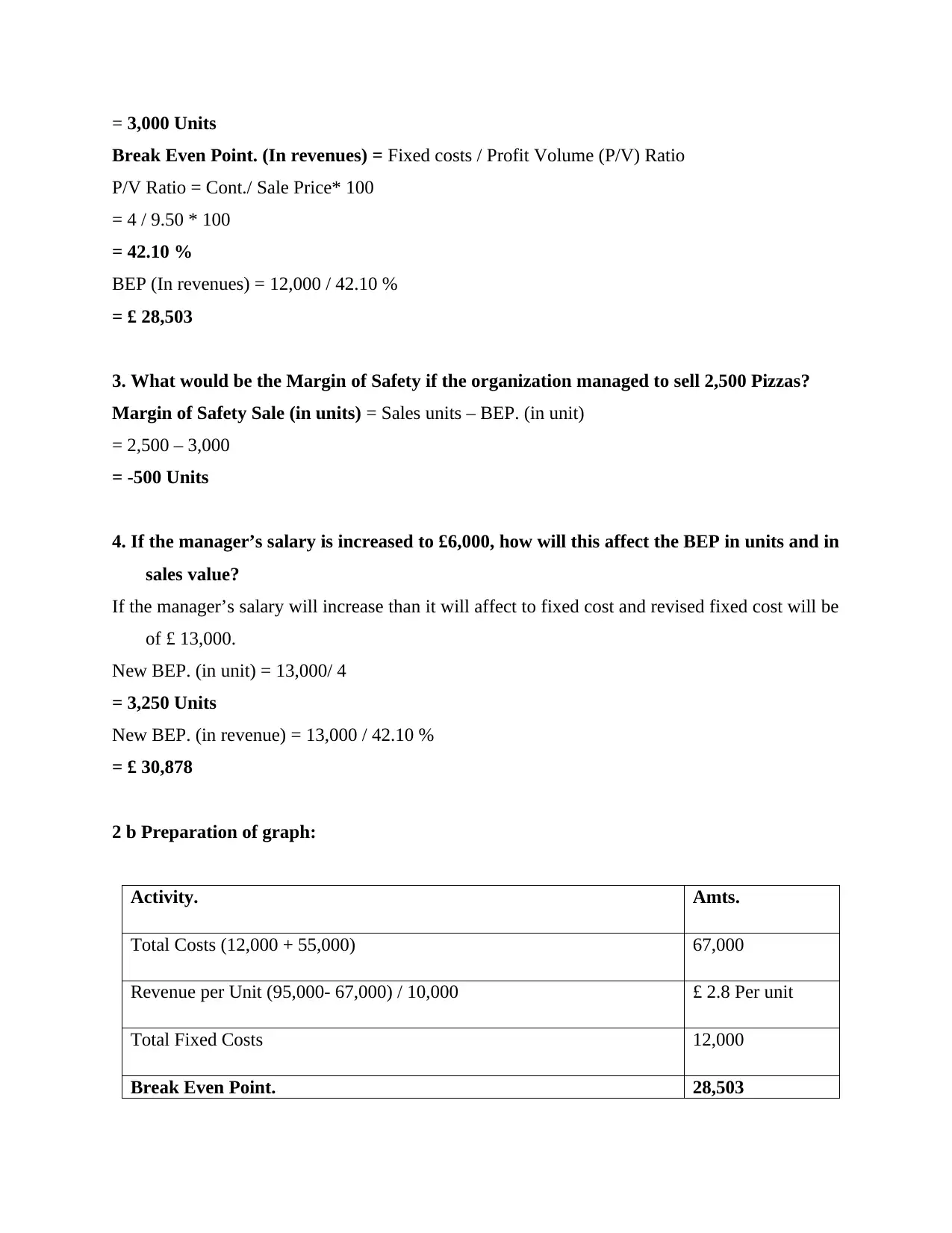

= 3,000 Units

Break Even Point. (In revenues) = Fixed costs / Profit Volume (P/V) Ratio

P/V Ratio = Cont./ Sale Price* 100

= 4 / 9.50 * 100

= 42.10 %

BEP (In revenues) = 12,000 / 42.10 %

= £ 28,503

3. What would be the Margin of Safety if the organization managed to sell 2,500 Pizzas?

Margin of Safety Sale (in units) = Sales units – BEP. (in unit)

= 2,500 – 3,000

= -500 Units

4. If the manager’s salary is increased to £6,000, how will this affect the BEP in units and in

sales value?

If the manager’s salary will increase than it will affect to fixed cost and revised fixed cost will be

of £ 13,000.

New BEP. (in unit) = 13,000/ 4

= 3,250 Units

New BEP. (in revenue) = 13,000 / 42.10 %

= £ 30,878

2 b Preparation of graph:

Activity. Amts.

Total Costs (12,000 + 55,000) 67,000

Revenue per Unit (95,000- 67,000) / 10,000 £ 2.8 Per unit

Total Fixed Costs 12,000

Break Even Point. 28,503

Break Even Point. (In revenues) = Fixed costs / Profit Volume (P/V) Ratio

P/V Ratio = Cont./ Sale Price* 100

= 4 / 9.50 * 100

= 42.10 %

BEP (In revenues) = 12,000 / 42.10 %

= £ 28,503

3. What would be the Margin of Safety if the organization managed to sell 2,500 Pizzas?

Margin of Safety Sale (in units) = Sales units – BEP. (in unit)

= 2,500 – 3,000

= -500 Units

4. If the manager’s salary is increased to £6,000, how will this affect the BEP in units and in

sales value?

If the manager’s salary will increase than it will affect to fixed cost and revised fixed cost will be

of £ 13,000.

New BEP. (in unit) = 13,000/ 4

= 3,250 Units

New BEP. (in revenue) = 13,000 / 42.10 %

= £ 30,878

2 b Preparation of graph:

Activity. Amts.

Total Costs (12,000 + 55,000) 67,000

Revenue per Unit (95,000- 67,000) / 10,000 £ 2.8 Per unit

Total Fixed Costs 12,000

Break Even Point. 28,503

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variance analysis report:

Actual units sold = 12,000 Units

Budgeted units to be sold = 10,000 Units

Budgeted price per unit = £ 9.50

Sale Volume Variance= (Actual unit sold- Budgeted unit sold) x Budgeted price per unit

= (12,000 – 10,000) * 9.50

= 2,000 * 9.50

= 19,000 Favorable Position

Flexible budget

Items Actual Budgeted Variance

Sale price per unit 10 9.50 0.50 Favorable.

No. of Units sold 12,000 10,000 2,000 Favorable.

Actual units sold = 12,000 Units

Budgeted units to be sold = 10,000 Units

Budgeted price per unit = £ 9.50

Sale Volume Variance= (Actual unit sold- Budgeted unit sold) x Budgeted price per unit

= (12,000 – 10,000) * 9.50

= 2,000 * 9.50

= 19,000 Favorable Position

Flexible budget

Items Actual Budgeted Variance

Sale price per unit 10 9.50 0.50 Favorable.

No. of Units sold 12,000 10,000 2,000 Favorable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Revenue earned 1,20,000 95,000 25,000 Favorable.

Fixed costs 15,000 12,000 3,000 Adverse.

Variable costs 5 5.50 0.50 Favorable.

TASK 3

P4 Advantages and disadvantages of different types of planning tools used for budgetary control

Budgetary control is a method of determining the difference between actual result and

budgeted/standard results for an organization. In this, an organisation set a standard

figure for future and then compare with actual figure to calculate various variances

(Bakhtiari, 2020)

. This method considered the difference of standard and actual performs in figures. It will help

the organisation to increase the profitability ratio to achieve organizational goals.

Advantages of planning tools used for budgetary control:

Planning tools are essential elements, which helps the organisation to monitor various

activity, strategy, variances, performance at different level of output. Theses are the important

planning tools in management accounting- strategic planning, budgets, price strategies etc. Main

object to use strategic planning and budgets as a planning tool is to achieve the targets in given

time period with applicable policies and capabilities.

Budget define as, an estimation of expenses and income for a particular time period of

future. It helps an organisation to manage expenses according to income. Strategic plan also

related with the growth of an organisation, in this manner company can compare the past

strategical programme with the present strategies and try to implement the changes in

organisation on the basis of profitability.

Disadvantages of planning tools used for budgetary control:

Fixed costs 15,000 12,000 3,000 Adverse.

Variable costs 5 5.50 0.50 Favorable.

TASK 3

P4 Advantages and disadvantages of different types of planning tools used for budgetary control

Budgetary control is a method of determining the difference between actual result and

budgeted/standard results for an organization. In this, an organisation set a standard

figure for future and then compare with actual figure to calculate various variances

(Bakhtiari, 2020)

. This method considered the difference of standard and actual performs in figures. It will help

the organisation to increase the profitability ratio to achieve organizational goals.

Advantages of planning tools used for budgetary control:

Planning tools are essential elements, which helps the organisation to monitor various

activity, strategy, variances, performance at different level of output. Theses are the important

planning tools in management accounting- strategic planning, budgets, price strategies etc. Main

object to use strategic planning and budgets as a planning tool is to achieve the targets in given

time period with applicable policies and capabilities.

Budget define as, an estimation of expenses and income for a particular time period of

future. It helps an organisation to manage expenses according to income. Strategic plan also

related with the growth of an organisation, in this manner company can compare the past

strategical programme with the present strategies and try to implement the changes in

organisation on the basis of profitability.

Disadvantages of planning tools used for budgetary control:

In budgetary control, budget is the important tool, which find out the difference between

actual and standard performance. It can be said that, budgetary control refers to prepare budgets

for future and compare with present performance. There are many disadvantages of planning

tools, which is used in budgetary control these are:

Heavy cost: It is very difficult to prepare a budget in inflationary situations, in this a

heavy cost spent by organisation, which is not affordable by small scale enterprises.

Basically, Budget prepared for future on the basis of present and past data but future is

uncertain, so it can not be possible to make correct every time.

Time taking procedure: It is also a time taking procedure, in this an organisation have to collect

the data related with present and past conditions to make this (Farazdaghi, 2020. So it

is not possible to waste time in collecting the past data every time for an organisation.

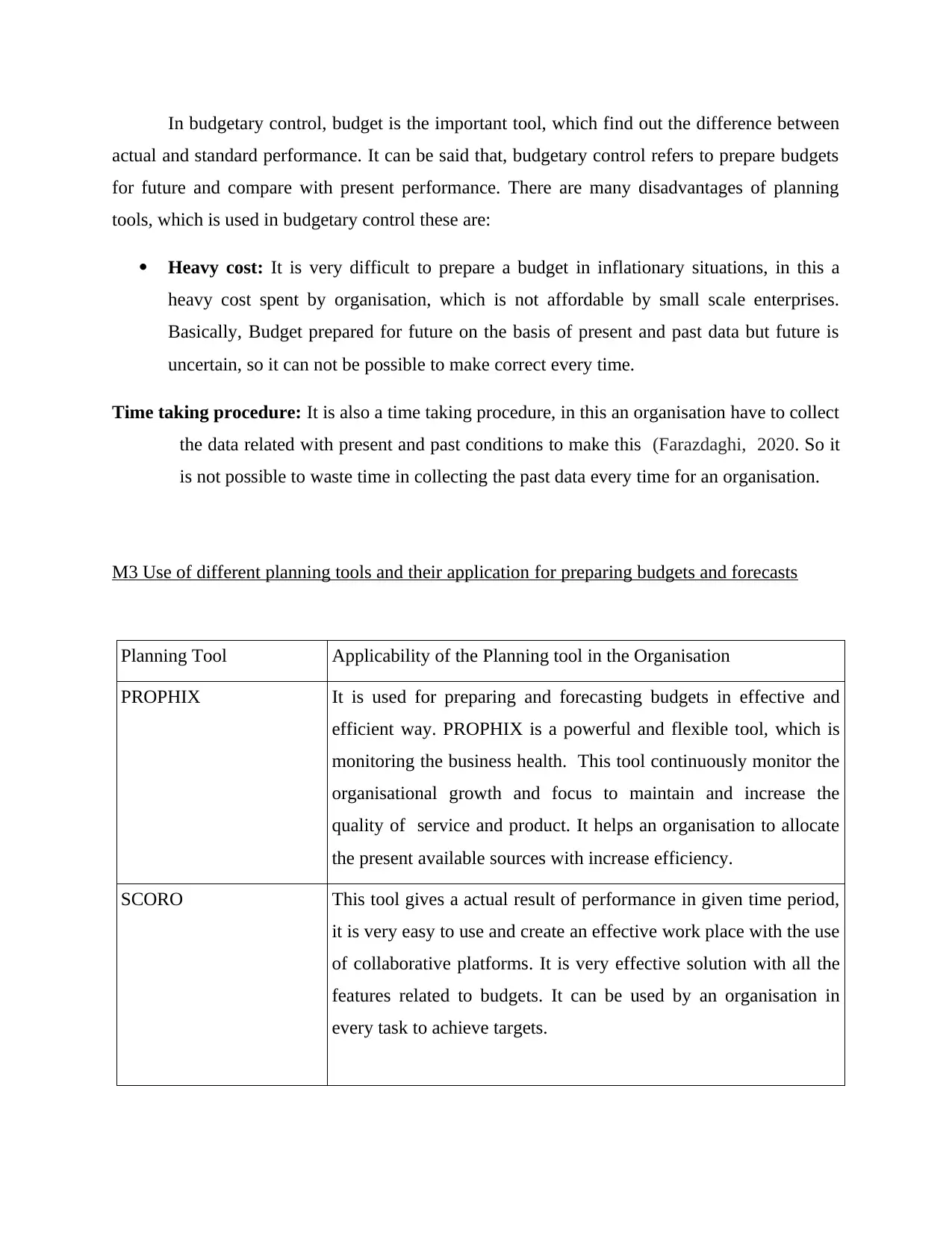

M3 Use of different planning tools and their application for preparing budgets and forecasts

Planning Tool Applicability of the Planning tool in the Organisation

PROPHIX It is used for preparing and forecasting budgets in effective and

efficient way. PROPHIX is a powerful and flexible tool, which is

monitoring the business health. This tool continuously monitor the

organisational growth and focus to maintain and increase the

quality of service and product. It helps an organisation to allocate

the present available sources with increase efficiency.

SCORO This tool gives a actual result of performance in given time period,

it is very easy to use and create an effective work place with the use

of collaborative platforms. It is very effective solution with all the

features related to budgets. It can be used by an organisation in

every task to achieve targets.

actual and standard performance. It can be said that, budgetary control refers to prepare budgets

for future and compare with present performance. There are many disadvantages of planning

tools, which is used in budgetary control these are:

Heavy cost: It is very difficult to prepare a budget in inflationary situations, in this a

heavy cost spent by organisation, which is not affordable by small scale enterprises.

Basically, Budget prepared for future on the basis of present and past data but future is

uncertain, so it can not be possible to make correct every time.

Time taking procedure: It is also a time taking procedure, in this an organisation have to collect

the data related with present and past conditions to make this (Farazdaghi, 2020. So it

is not possible to waste time in collecting the past data every time for an organisation.

M3 Use of different planning tools and their application for preparing budgets and forecasts

Planning Tool Applicability of the Planning tool in the Organisation

PROPHIX It is used for preparing and forecasting budgets in effective and

efficient way. PROPHIX is a powerful and flexible tool, which is

monitoring the business health. This tool continuously monitor the

organisational growth and focus to maintain and increase the

quality of service and product. It helps an organisation to allocate

the present available sources with increase efficiency.

SCORO This tool gives a actual result of performance in given time period,

it is very easy to use and create an effective work place with the use

of collaborative platforms. It is very effective solution with all the

features related to budgets. It can be used by an organisation in

every task to achieve targets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.