Management Accounting Report: Connectta Ltd Costing System Analysis

VerifiedAdded on 2022/12/27

|10

|2258

|27

Report

AI Summary

This report provides a comprehensive analysis of Connectta Ltd's management accounting practices. It begins by examining the application of the job costing system used by the company, emphasizing its role in cost estimation and control. The report then delves into the computation of work-in-progress inventory and finished goods costs, providing detailed calculations and explanations. Furthermore, it addresses the treatment of over-applied and under-applied overheads, discussing their implications and the appropriate accounting procedures. The report also explores the activity-based costing (ABC) system, highlighting its benefits and advantages over traditional costing methods, particularly in terms of accuracy and decision-making support. Finally, the report recommends that Connectta Ltd adopt ABC costing techniques to improve cost identification and management, providing a valuable resource for students on Desklib.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note

Management Accounting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGEMENT ACCOUNTING

Table of Contents

Introduction...............................................................................................................................2

Discussion..................................................................................................................................3

Application of Job Costing System.......................................................................................3

Work in Progress Inventory Account....................................................................................4

Computation of Costs of Finished goods..............................................................................4

Over Applied and Under Applied Overhead of the Business................................................5

Treatment of Under or Over Applied Overheads of the business.........................................5

Activity Based Costing System and its Application..............................................................6

Conclusion.................................................................................................................................8

Reference...................................................................................................................................9

MANAGEMENT ACCOUNTING

Table of Contents

Introduction...............................................................................................................................2

Discussion..................................................................................................................................3

Application of Job Costing System.......................................................................................3

Work in Progress Inventory Account....................................................................................4

Computation of Costs of Finished goods..............................................................................4

Over Applied and Under Applied Overhead of the Business................................................5

Treatment of Under or Over Applied Overheads of the business.........................................5

Activity Based Costing System and its Application..............................................................6

Conclusion.................................................................................................................................8

Reference...................................................................................................................................9

2

MANAGEMENT ACCOUNTING

Introduction

The main purpose of the assessment is to analyze the operations and costing system

which is followed by Connectta Ltd. The management of the company follows Job costing

system for appropriately representing the costs of the business. The assessment would be

focusing on the costing methods which is available to the business and how improvements can

be brought about in the same. The assessment also includes computations of different costs for

Connectta Ltd. In addition to this, the assessment would be showing alternative treatments of

overhead costs and impact of the same on total costs. The analysis would be conducted for under

and over applied overhead costs and how the same is to be treated from the perspective of

costing accounting. The assessment would also be determining the role of activity-based costing

system and how the same helps the management of the company in taking decisions for the

future of the company. The assessment would also be going into details regarding the benefits

which are associated with the Activity based costing techniques and how the same manages the

deficiencies which are present in traditional costing system.

Discussion

Application of Job Costing System

The assessment would be discussing different aspects of the reporting framework of cost

accounting along with the reporting framework which is followed by Connectta Ltd. In a current

market, it is very essential for a business to determine the appropriate costs of the business for

not only estimating the profits which can be earned but also for the purpose of estimating the

price of the product which is to be offered to the customers (Özkan and Karaibrahimoğlu 2013).

Job Costing is a system which is used by the company for the purpose of fulfilling the orders of

the client. In a business job costing technique are applied by the management of the company for

MANAGEMENT ACCOUNTING

Introduction

The main purpose of the assessment is to analyze the operations and costing system

which is followed by Connectta Ltd. The management of the company follows Job costing

system for appropriately representing the costs of the business. The assessment would be

focusing on the costing methods which is available to the business and how improvements can

be brought about in the same. The assessment also includes computations of different costs for

Connectta Ltd. In addition to this, the assessment would be showing alternative treatments of

overhead costs and impact of the same on total costs. The analysis would be conducted for under

and over applied overhead costs and how the same is to be treated from the perspective of

costing accounting. The assessment would also be determining the role of activity-based costing

system and how the same helps the management of the company in taking decisions for the

future of the company. The assessment would also be going into details regarding the benefits

which are associated with the Activity based costing techniques and how the same manages the

deficiencies which are present in traditional costing system.

Discussion

Application of Job Costing System

The assessment would be discussing different aspects of the reporting framework of cost

accounting along with the reporting framework which is followed by Connectta Ltd. In a current

market, it is very essential for a business to determine the appropriate costs of the business for

not only estimating the profits which can be earned but also for the purpose of estimating the

price of the product which is to be offered to the customers (Özkan and Karaibrahimoğlu 2013).

Job Costing is a system which is used by the company for the purpose of fulfilling the orders of

the client. In a business job costing technique are applied by the management of the company for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGEMENT ACCOUNTING

controlling the usage of raw materials. The companies which effectively considers the order of

the consumers for the purpose of meeting the demand of the consumers. Considering the core

activities of the company, the management of a company has a variety of options regarding

appropriate costing technique which needs to be applied by the management of the company. Job

costing techniques are used for the purpose of estimating the total costa of manufacturing

concerns and in entities which relies more on customers’ orders for meeting the production

requirements and generating sales revenue from operations (Walther and Skousen 2017).

The job costing system is appropriate for companies which are engaged in

manufacturing sector and such companies reports the costs in costing reports which are prepared

according to the job costing system. There are certain companies which utilizes job costing

system for effective presentation of the costs of the business are hospitals, manufacturing

concerns and other business operations.

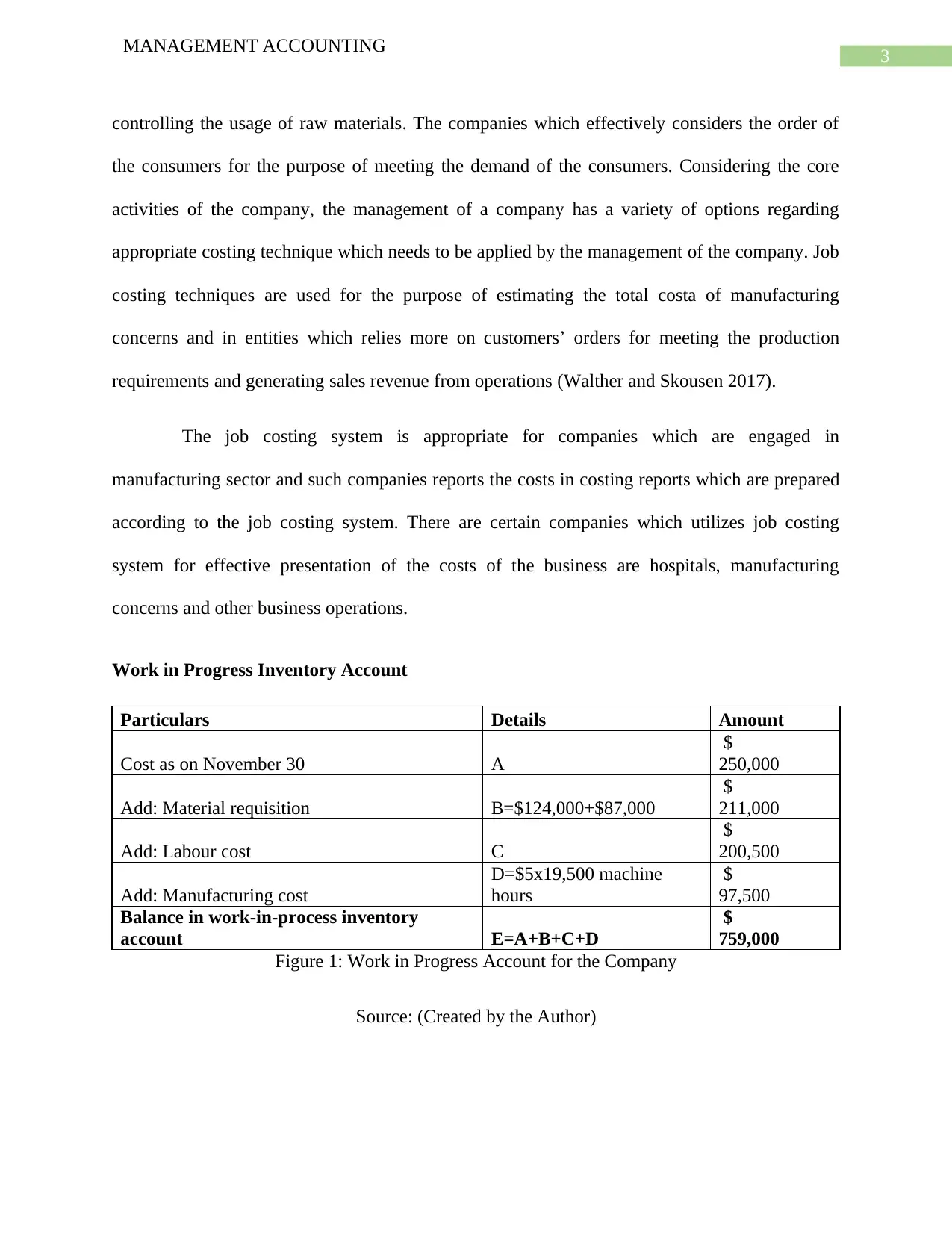

Work in Progress Inventory Account

Particulars Details Amount

Cost as on November 30 A

$

250,000

Add: Material requisition B=$124,000+$87,000

$

211,000

Add: Labour cost C

$

200,500

Add: Manufacturing cost

D=$5x19,500 machine

hours

$

97,500

Balance in work-in-process inventory

account E=A+B+C+D

$

759,000

Figure 1: Work in Progress Account for the Company

Source: (Created by the Author)

MANAGEMENT ACCOUNTING

controlling the usage of raw materials. The companies which effectively considers the order of

the consumers for the purpose of meeting the demand of the consumers. Considering the core

activities of the company, the management of a company has a variety of options regarding

appropriate costing technique which needs to be applied by the management of the company. Job

costing techniques are used for the purpose of estimating the total costa of manufacturing

concerns and in entities which relies more on customers’ orders for meeting the production

requirements and generating sales revenue from operations (Walther and Skousen 2017).

The job costing system is appropriate for companies which are engaged in

manufacturing sector and such companies reports the costs in costing reports which are prepared

according to the job costing system. There are certain companies which utilizes job costing

system for effective presentation of the costs of the business are hospitals, manufacturing

concerns and other business operations.

Work in Progress Inventory Account

Particulars Details Amount

Cost as on November 30 A

$

250,000

Add: Material requisition B=$124,000+$87,000

$

211,000

Add: Labour cost C

$

200,500

Add: Manufacturing cost

D=$5x19,500 machine

hours

$

97,500

Balance in work-in-process inventory

account E=A+B+C+D

$

759,000

Figure 1: Work in Progress Account for the Company

Source: (Created by the Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGEMENT ACCOUNTING

The above table effectively shows computation of the work in progress account balances

for Connectta Ltd. by considering material requisition, labour costs and manufacturing costs of

the business. The balance which is shown in the work in progress account for inventory is shown

to be $ 759,000. The computation of work in inventory cost is considered to be important as the

same is related to the production process and the closing balance of Work in progress is always

considered to be important from the perspective of taking important decisions regarding

operatons.

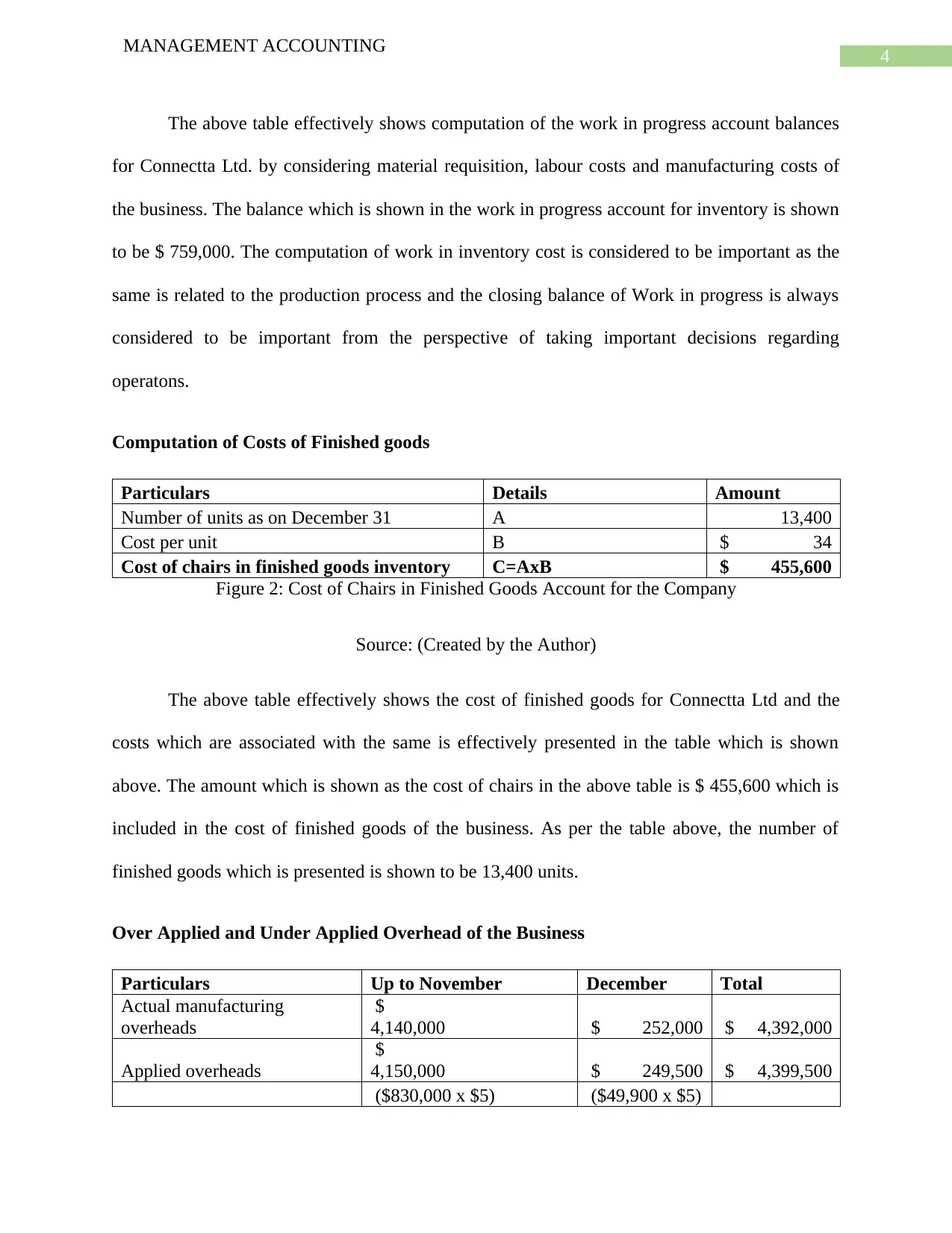

Computation of Costs of Finished goods

Particulars Details Amount

Number of units as on December 31 A 13,400

Cost per unit B $ 34

Cost of chairs in finished goods inventory C=AxB $ 455,600

Figure 2: Cost of Chairs in Finished Goods Account for the Company

Source: (Created by the Author)

The above table effectively shows the cost of finished goods for Connectta Ltd and the

costs which are associated with the same is effectively presented in the table which is shown

above. The amount which is shown as the cost of chairs in the above table is $ 455,600 which is

included in the cost of finished goods of the business. As per the table above, the number of

finished goods which is presented is shown to be 13,400 units.

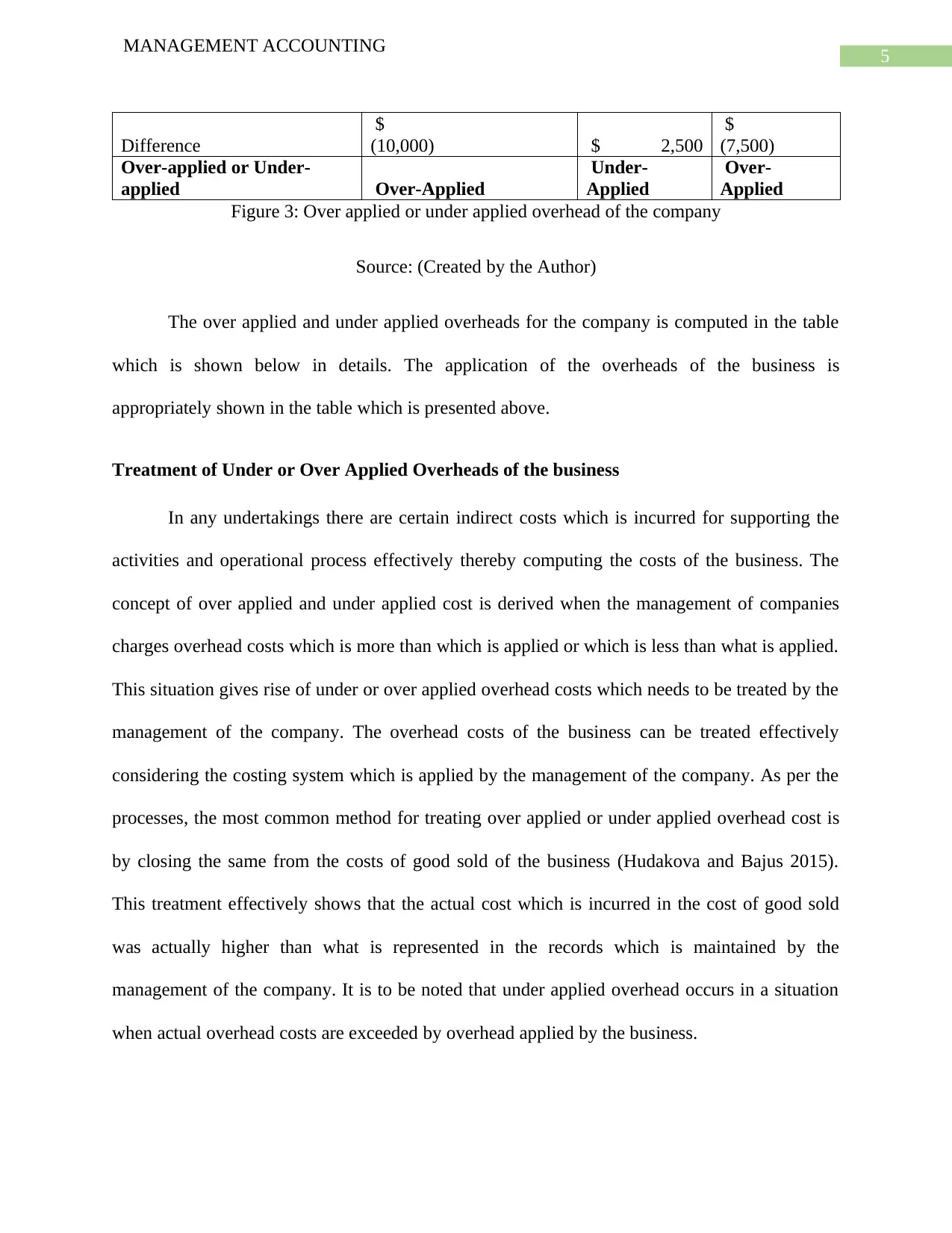

Over Applied and Under Applied Overhead of the Business

Particulars Up to November December Total

Actual manufacturing

overheads

$

4,140,000 $ 252,000 $ 4,392,000

Applied overheads

$

4,150,000 $ 249,500 $ 4,399,500

($830,000 x $5) ($49,900 x $5)

MANAGEMENT ACCOUNTING

The above table effectively shows computation of the work in progress account balances

for Connectta Ltd. by considering material requisition, labour costs and manufacturing costs of

the business. The balance which is shown in the work in progress account for inventory is shown

to be $ 759,000. The computation of work in inventory cost is considered to be important as the

same is related to the production process and the closing balance of Work in progress is always

considered to be important from the perspective of taking important decisions regarding

operatons.

Computation of Costs of Finished goods

Particulars Details Amount

Number of units as on December 31 A 13,400

Cost per unit B $ 34

Cost of chairs in finished goods inventory C=AxB $ 455,600

Figure 2: Cost of Chairs in Finished Goods Account for the Company

Source: (Created by the Author)

The above table effectively shows the cost of finished goods for Connectta Ltd and the

costs which are associated with the same is effectively presented in the table which is shown

above. The amount which is shown as the cost of chairs in the above table is $ 455,600 which is

included in the cost of finished goods of the business. As per the table above, the number of

finished goods which is presented is shown to be 13,400 units.

Over Applied and Under Applied Overhead of the Business

Particulars Up to November December Total

Actual manufacturing

overheads

$

4,140,000 $ 252,000 $ 4,392,000

Applied overheads

$

4,150,000 $ 249,500 $ 4,399,500

($830,000 x $5) ($49,900 x $5)

5

MANAGEMENT ACCOUNTING

Difference

$

(10,000) $ 2,500

$

(7,500)

Over-applied or Under-

applied Over-Applied

Under-

Applied

Over-

Applied

Figure 3: Over applied or under applied overhead of the company

Source: (Created by the Author)

The over applied and under applied overheads for the company is computed in the table

which is shown below in details. The application of the overheads of the business is

appropriately shown in the table which is presented above.

Treatment of Under or Over Applied Overheads of the business

In any undertakings there are certain indirect costs which is incurred for supporting the

activities and operational process effectively thereby computing the costs of the business. The

concept of over applied and under applied cost is derived when the management of companies

charges overhead costs which is more than which is applied or which is less than what is applied.

This situation gives rise of under or over applied overhead costs which needs to be treated by the

management of the company. The overhead costs of the business can be treated effectively

considering the costing system which is applied by the management of the company. As per the

processes, the most common method for treating over applied or under applied overhead cost is

by closing the same from the costs of good sold of the business (Hudakova and Bajus 2015).

This treatment effectively shows that the actual cost which is incurred in the cost of good sold

was actually higher than what is represented in the records which is maintained by the

management of the company. It is to be noted that under applied overhead occurs in a situation

when actual overhead costs are exceeded by overhead applied by the business.

MANAGEMENT ACCOUNTING

Difference

$

(10,000) $ 2,500

$

(7,500)

Over-applied or Under-

applied Over-Applied

Under-

Applied

Over-

Applied

Figure 3: Over applied or under applied overhead of the company

Source: (Created by the Author)

The over applied and under applied overheads for the company is computed in the table

which is shown below in details. The application of the overheads of the business is

appropriately shown in the table which is presented above.

Treatment of Under or Over Applied Overheads of the business

In any undertakings there are certain indirect costs which is incurred for supporting the

activities and operational process effectively thereby computing the costs of the business. The

concept of over applied and under applied cost is derived when the management of companies

charges overhead costs which is more than which is applied or which is less than what is applied.

This situation gives rise of under or over applied overhead costs which needs to be treated by the

management of the company. The overhead costs of the business can be treated effectively

considering the costing system which is applied by the management of the company. As per the

processes, the most common method for treating over applied or under applied overhead cost is

by closing the same from the costs of good sold of the business (Hudakova and Bajus 2015).

This treatment effectively shows that the actual cost which is incurred in the cost of good sold

was actually higher than what is represented in the records which is maintained by the

management of the company. It is to be noted that under applied overhead occurs in a situation

when actual overhead costs are exceeded by overhead applied by the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGEMENT ACCOUNTING

In other words, it can be said that if an overhead cost of an entity is under applied or over

applied and if the same is insignificant in nature than the same is treated as period costs and

closed with the cost of goods sold account of the entity. In case the amount of under applied or

over applied costs of the business is significant than the same is prorated over the relevant

accounts. The relevant accounts which would be considered is from the perspective of costing

system of the company.

Activity Based Costing System and its Application

Activity based costing techniques is an accounting method which is used by the

management of the company which effectively identifies costs related to the operations and

assigns the same to overhead costs appropriately (Tsai et al. 2014). An activity-based costing

system recognises the relationship between costs, overhead activities and the products which is

manufactured by the business. The costing method is regarded to be the most popular method in

business as the same effectively identifies the costs and relates the same to the activities which

are associated with the same. The overhead costs of the business effectively assign indirect costs

of the business more effectively in comparisons to traditional methods.

Activity-based costing methods is mostly used in manufacturing concerns since it

enhances the reliability of the cost data and thereby provides an appropriate presentation of the

costs of the business. This help the management of the company in taking appropriate decisions

regarding the cost element of the entity. It is to be noted that ABC system of costing is

effectively related with the transactions or event which is considered for the purpose of costing

which is known as the cost drivers of the business. The process of activity-based costing is more

preferred by most of the businesses due to the advantages which are brought about by the process

in comparison to traditional costing methods. Activity based costing techniques considers the

MANAGEMENT ACCOUNTING

In other words, it can be said that if an overhead cost of an entity is under applied or over

applied and if the same is insignificant in nature than the same is treated as period costs and

closed with the cost of goods sold account of the entity. In case the amount of under applied or

over applied costs of the business is significant than the same is prorated over the relevant

accounts. The relevant accounts which would be considered is from the perspective of costing

system of the company.

Activity Based Costing System and its Application

Activity based costing techniques is an accounting method which is used by the

management of the company which effectively identifies costs related to the operations and

assigns the same to overhead costs appropriately (Tsai et al. 2014). An activity-based costing

system recognises the relationship between costs, overhead activities and the products which is

manufactured by the business. The costing method is regarded to be the most popular method in

business as the same effectively identifies the costs and relates the same to the activities which

are associated with the same. The overhead costs of the business effectively assign indirect costs

of the business more effectively in comparisons to traditional methods.

Activity-based costing methods is mostly used in manufacturing concerns since it

enhances the reliability of the cost data and thereby provides an appropriate presentation of the

costs of the business. This help the management of the company in taking appropriate decisions

regarding the cost element of the entity. It is to be noted that ABC system of costing is

effectively related with the transactions or event which is considered for the purpose of costing

which is known as the cost drivers of the business. The process of activity-based costing is more

preferred by most of the businesses due to the advantages which are brought about by the process

in comparison to traditional costing methods. Activity based costing techniques considers the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING

same cost drivers as traditional costing techniques for the purpose of identifying the costs of the

business and appropriately treating the same.

In terms of comparison between the traditional and ABC costing method, it can be said

that both the methods apply a similar approach in identification of the indirect costs of the

business and the same is done on the basis of the cost drivers of the business (Monroy, Nasiri

and Peláez 2014). The difference which can be identified between the tow method lies in the

accuracy and complexity between the two methods. The method of traditional costing has a more

simplistic approach and can be considered to be less accurate in comparisons to ABC costing

techniques (Tibesku et al.2013). The traditional costing system applies an arbitrary rate for the

purpose of assigning the indirect cost of the business. This is a deficiency which is effectively

covered by ABC costing system. The process of ABC costing system first applies the cost to the

activity which the cost is actually associated with and then the cost is assigned to the cost of the

product on the basis of the usage of the product. It is to be noted that Activity based costing

system is more accurate than traditional costing system and it effectively portrays the breakdown

of the indirect costs of the business. Therefore, it can be said that the ABC costing system

effectively represents the cost information of a business and helps the management of the

company to take important decisions regarding a business.

Conclusion

The analysis of the above situation shows that the management of Connectta Ltd is

applying job costing techniques for the purpose of estimating the costs of the business. The

above discussion also shows computation of work in progress and finished goods inventory costs

which would be included in total costs of the business. The discussion also reveals that the

treatment of over applied and under applied costs of the business in costing terms and how the

MANAGEMENT ACCOUNTING

same cost drivers as traditional costing techniques for the purpose of identifying the costs of the

business and appropriately treating the same.

In terms of comparison between the traditional and ABC costing method, it can be said

that both the methods apply a similar approach in identification of the indirect costs of the

business and the same is done on the basis of the cost drivers of the business (Monroy, Nasiri

and Peláez 2014). The difference which can be identified between the tow method lies in the

accuracy and complexity between the two methods. The method of traditional costing has a more

simplistic approach and can be considered to be less accurate in comparisons to ABC costing

techniques (Tibesku et al.2013). The traditional costing system applies an arbitrary rate for the

purpose of assigning the indirect cost of the business. This is a deficiency which is effectively

covered by ABC costing system. The process of ABC costing system first applies the cost to the

activity which the cost is actually associated with and then the cost is assigned to the cost of the

product on the basis of the usage of the product. It is to be noted that Activity based costing

system is more accurate than traditional costing system and it effectively portrays the breakdown

of the indirect costs of the business. Therefore, it can be said that the ABC costing system

effectively represents the cost information of a business and helps the management of the

company to take important decisions regarding a business.

Conclusion

The analysis of the above situation shows that the management of Connectta Ltd is

applying job costing techniques for the purpose of estimating the costs of the business. The

above discussion also shows computation of work in progress and finished goods inventory costs

which would be included in total costs of the business. The discussion also reveals that the

treatment of over applied and under applied costs of the business in costing terms and how the

8

MANAGEMENT ACCOUNTING

same would impact the total costs of the business. In addition to this, the discussion also reveals

the benefits which are associated with ABC costing techniques in comparison to traditional

costing techniques of the business. Therefore, it is recommended to the management of

Connectta Ltd that they should start following ABC costing techniques for the purpose of

effectively identifying the costs of the business.

MANAGEMENT ACCOUNTING

same would impact the total costs of the business. In addition to this, the discussion also reveals

the benefits which are associated with ABC costing techniques in comparison to traditional

costing techniques of the business. Therefore, it is recommended to the management of

Connectta Ltd that they should start following ABC costing techniques for the purpose of

effectively identifying the costs of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGEMENT ACCOUNTING

Reference

Hudakova, S.L. and Bajus, R., 2015. Cost management using activity-based costing

model. Актуальні проблеми економіки, (2), pp.373-386.

Monroy, C.R., Nasiri, A. and Peláez, M.Á., 2014. Activity Based Costing, Time-Driven Activity

Based Costing and Lean Accounting: Differences among three accounting systems’ approach to

manufacturing. In Annals of Industrial Engineering 2012 (pp. 11-17). Springer, London.

Özkan, S. and Karaibrahimoğlu, Y.Z., 2013. Activity-based costing approach in the

measurement of cost of quality in SMEs: a case study. Total Quality Management & Business

Excellence, 24(3-4), pp.420-431.

Tibesku, C.O., Hofer, P., Portegies, W., Ruys, C.J.M. and Fennema, P., 2013. Benefits of using

customized instrumentation in total knee arthroplasty: results from an activity-based costing

model. Archives of orthopaedic and trauma surgery, 133(3), pp.405-411.

Tsai, W.H., Yang, C.H., Chang, J.C. and Lee, H.L., 2014. An activity-based costing decision

model for life cycle assessment in green building projects. European Journal of Operational

Research, 238(2), pp.607-619.

Walther, L.M. and Skousen, C.J., 2017. Introduction to Managerial Accounting. Bookboon.

MANAGEMENT ACCOUNTING

Reference

Hudakova, S.L. and Bajus, R., 2015. Cost management using activity-based costing

model. Актуальні проблеми економіки, (2), pp.373-386.

Monroy, C.R., Nasiri, A. and Peláez, M.Á., 2014. Activity Based Costing, Time-Driven Activity

Based Costing and Lean Accounting: Differences among three accounting systems’ approach to

manufacturing. In Annals of Industrial Engineering 2012 (pp. 11-17). Springer, London.

Özkan, S. and Karaibrahimoğlu, Y.Z., 2013. Activity-based costing approach in the

measurement of cost of quality in SMEs: a case study. Total Quality Management & Business

Excellence, 24(3-4), pp.420-431.

Tibesku, C.O., Hofer, P., Portegies, W., Ruys, C.J.M. and Fennema, P., 2013. Benefits of using

customized instrumentation in total knee arthroplasty: results from an activity-based costing

model. Archives of orthopaedic and trauma surgery, 133(3), pp.405-411.

Tsai, W.H., Yang, C.H., Chang, J.C. and Lee, H.L., 2014. An activity-based costing decision

model for life cycle assessment in green building projects. European Journal of Operational

Research, 238(2), pp.607-619.

Walther, L.M. and Skousen, C.J., 2017. Introduction to Managerial Accounting. Bookboon.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.