University Report: Management Accounting and Control - PGBM 64

VerifiedAdded on 2022/10/19

|14

|4276

|255

Report

AI Summary

This report presents a comprehensive analysis of management accounting and control principles, addressing two specific questions from a university assignment. The first question focuses on production planning under resource constraints, including the allocation of fixed costs, the application of Economic Order Quantity (EOQ), and the interpretation of the margin of safety. It explores the use of a balanced scorecard for decision-making, considering financial, customer, internal process, and organizational capacity perspectives. The second question evaluates three investment proposals from different divisions (leather, wood, and steel) based on Return on Investment (ROI), residual income, and Economic Value Added (EVA). The report compares the viability of each proposal, considering the nature and timing of returns. The report provides detailed calculations in the appendices and supports its findings with relevant academic research.

Running head: MANAGEMENT ACCOUNTING AND CONTROL

MANAGEMENT ACCOUNTING AND CONTROL

Name of the Student

Name of the University

Author Note

MANAGEMENT ACCOUNTING AND CONTROL

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGEMENT ACCOUNTING AND CONTROL

Table of Contents

Answer to Question 1...................................................................................................................3

Answer to Question 2...................................................................................................................6

Bibliography...............................................................................................................................10

Appendix....................................................................................................................................12

MANAGEMENT ACCOUNTING AND CONTROL

Table of Contents

Answer to Question 1...................................................................................................................3

Answer to Question 2...................................................................................................................6

Bibliography...............................................................................................................................10

Appendix....................................................................................................................................12

2

MANAGEMENT ACCOUNTING AND CONTROL

Answer to Question 1

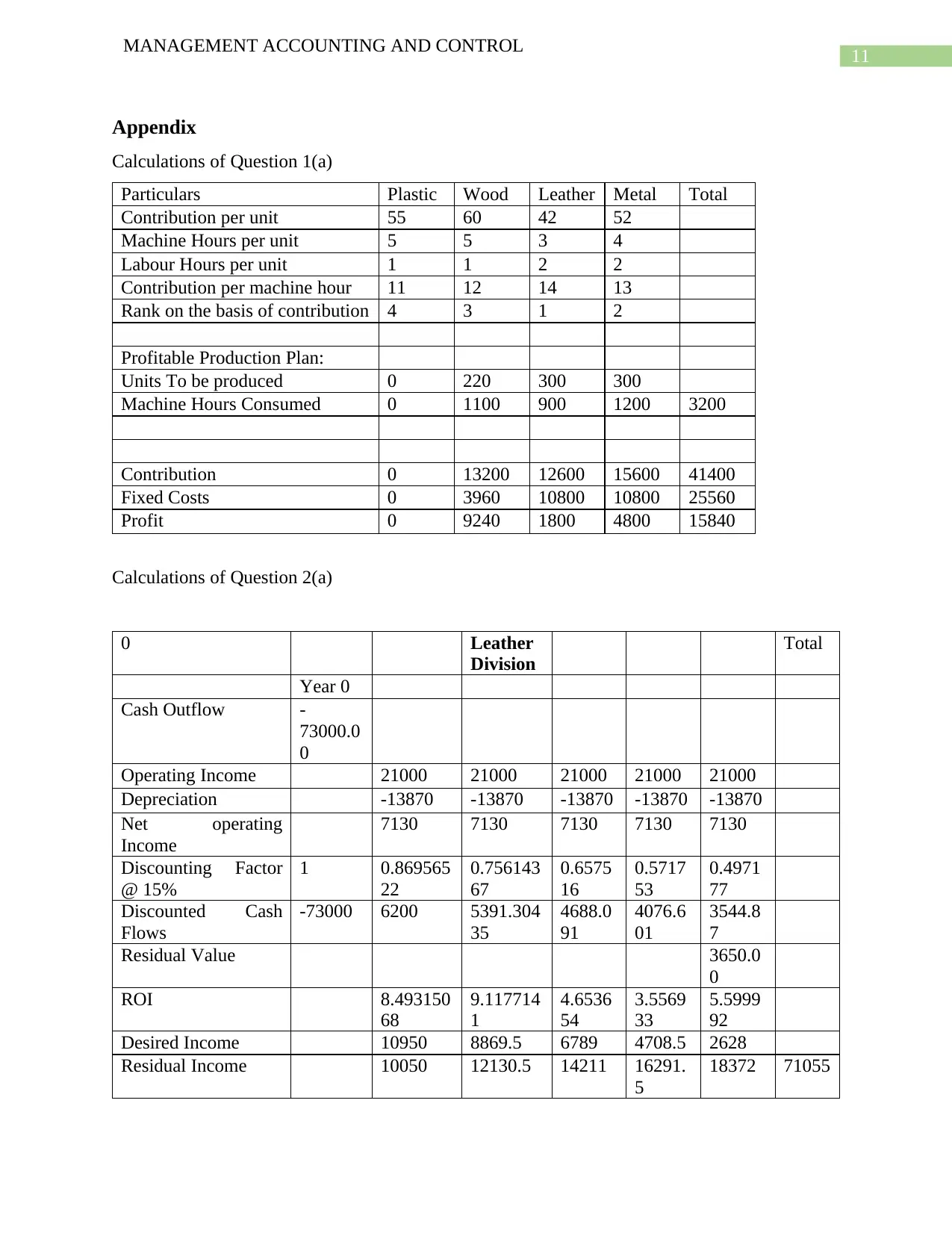

(a) In this situation, the production plan of the company has to be prepared by keeping the

constraint of machine hours in consideration. The absorbed fixed costs of the machine

hours should also be allocated to the products accordingly. When contribution is

calculated according to the constraint of machine hours in hand, the leather product

provides the highest amount of contribution. Fixed costs should also be allocated

according to the labour hours in hand (Novak and Popesko 2014). After calculating the

profit provided by a product on the basis of both the variable costs and labour costs, it has

been understood that producing 300 units each of the leather product and the metal

product along with 220 units of the wood product will turn out to be the most profitable

for the company as it provides a profit of 15840 after deducting all the costs. Plastic

chairs should not be produced at all as even though the profit earned from this type of

product is high, the product does not hold well under circumstances with restrictions on

the machine hours and the labour hours. After the allocation of the fixed costs, it is more

evident that the product is not at all profitable due to the high amount of machine hours it

consumes. Hence, after calculating the appropriate combination of products according to

the calculations made and ranking of the products, it has been found that the contribution

of the combination of the products is 41400 and the fixed costs are arrived at 25560.

(b) Economic order quantity (EOQ) is the appropriate amount of quantity that an entity

should procure at once while taking the cost of production, demand rate, holding costs

and other relevant variables into consideration (Sajtiprasert 2014). The main purpose of

applying EOQ is to reduce the costs associated with inventories. However, the theoretical

definition of EOQ is limited. It fails to consider the practical constraints faced by the

business. Utilising Sequential Quadratic Programming (SQP) is helpful in finding the

optimum quantity required for the buyer while taking constraints like budget, space,

ordering and procurement costs into consideration (Pasandideh, Niaki and Gharaei 2015).

This method has also been approved by conducting sensitivity analysis and its

comparison with other methods. In the given case, Lazy King Ltd. can apply the EOQ

model to order sufficient quantities of raw materials required for the manufacturing of the

profitable products in an efficient manner. It can altogether avoid the procurement of raw

MANAGEMENT ACCOUNTING AND CONTROL

Answer to Question 1

(a) In this situation, the production plan of the company has to be prepared by keeping the

constraint of machine hours in consideration. The absorbed fixed costs of the machine

hours should also be allocated to the products accordingly. When contribution is

calculated according to the constraint of machine hours in hand, the leather product

provides the highest amount of contribution. Fixed costs should also be allocated

according to the labour hours in hand (Novak and Popesko 2014). After calculating the

profit provided by a product on the basis of both the variable costs and labour costs, it has

been understood that producing 300 units each of the leather product and the metal

product along with 220 units of the wood product will turn out to be the most profitable

for the company as it provides a profit of 15840 after deducting all the costs. Plastic

chairs should not be produced at all as even though the profit earned from this type of

product is high, the product does not hold well under circumstances with restrictions on

the machine hours and the labour hours. After the allocation of the fixed costs, it is more

evident that the product is not at all profitable due to the high amount of machine hours it

consumes. Hence, after calculating the appropriate combination of products according to

the calculations made and ranking of the products, it has been found that the contribution

of the combination of the products is 41400 and the fixed costs are arrived at 25560.

(b) Economic order quantity (EOQ) is the appropriate amount of quantity that an entity

should procure at once while taking the cost of production, demand rate, holding costs

and other relevant variables into consideration (Sajtiprasert 2014). The main purpose of

applying EOQ is to reduce the costs associated with inventories. However, the theoretical

definition of EOQ is limited. It fails to consider the practical constraints faced by the

business. Utilising Sequential Quadratic Programming (SQP) is helpful in finding the

optimum quantity required for the buyer while taking constraints like budget, space,

ordering and procurement costs into consideration (Pasandideh, Niaki and Gharaei 2015).

This method has also been approved by conducting sensitivity analysis and its

comparison with other methods. In the given case, Lazy King Ltd. can apply the EOQ

model to order sufficient quantities of raw materials required for the manufacturing of the

profitable products in an efficient manner. It can altogether avoid the procurement of raw

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGEMENT ACCOUNTING AND CONTROL

materials of plastic chairs as the production of those chairs is totally unprofitable. Margin

of safety is a measure which is used to know the revenue that a company can earn over its

breakeven sales. This is calculated after the company meets both its fixed and variable

costs in a given financial year (Walther and Skousen 2017). A lower margin of safety

indicates that a company is likely to incur losses due to a slight change in fixed costs or a

decrease in the selling price. In the given case, the margin of safety of the entity is quite

high and the company can continue manufacturing its products at that level to be able to

maximise its profits under the given constraints (Caprice, Schlippenbach and Wey 2014).

In the given case, the company is not able to meet the entire demand for the wood chairs

and the plastic chairs. Apart from this, it has been found by many manufacturing

companies that lead time is a significant tool to differentiate themselves in the market and

is helpful in positioning themselves profitably. Hence, instead of increasing the labour

hours or providing special discounts to customers, the company can focus on improving

its efficiency by following a vendor-purchaser integrated production model (Vijayashree

and Uthayakumar 2014). These can lead to a decline in the costs incurred by the company

and increase the speed at which it delivers the products while also manufacturing them

quickly.

(c) The balanced scorecard is a financial tool that considers the performance of an entity

using four aspects. These are the financial perspective, customer/stakeholder perspective,

internal process related perspective and the organisational capacity. The main objective

of this tool is to provide the company with a strategy to satisfy all of the above mentioned

guidelines and to help in decision making (Tjader et al., 2014). When considering all of

the perspectives covered under a balanced scorecard and the scenarios faced by the entity,

it is evident that the tool can be used to guide the company in the process of making

decisions related to manufacturing specific products and outsourcing them. Although, the

limitation of the balanced scorecard has been found to be its inability to properly manage

the micro aspects of a business (Susilawati et al. 2013). This limitation is not completely

relevant in the present scenario as the company is not a very big organisation that

operates in a large number of business areas and produces a wide variety of range of

products. As the information about the company’s business and other perspectives is

quite clear, applying balanced scorecard in this case is more relevant (Sundharam,

MANAGEMENT ACCOUNTING AND CONTROL

materials of plastic chairs as the production of those chairs is totally unprofitable. Margin

of safety is a measure which is used to know the revenue that a company can earn over its

breakeven sales. This is calculated after the company meets both its fixed and variable

costs in a given financial year (Walther and Skousen 2017). A lower margin of safety

indicates that a company is likely to incur losses due to a slight change in fixed costs or a

decrease in the selling price. In the given case, the margin of safety of the entity is quite

high and the company can continue manufacturing its products at that level to be able to

maximise its profits under the given constraints (Caprice, Schlippenbach and Wey 2014).

In the given case, the company is not able to meet the entire demand for the wood chairs

and the plastic chairs. Apart from this, it has been found by many manufacturing

companies that lead time is a significant tool to differentiate themselves in the market and

is helpful in positioning themselves profitably. Hence, instead of increasing the labour

hours or providing special discounts to customers, the company can focus on improving

its efficiency by following a vendor-purchaser integrated production model (Vijayashree

and Uthayakumar 2014). These can lead to a decline in the costs incurred by the company

and increase the speed at which it delivers the products while also manufacturing them

quickly.

(c) The balanced scorecard is a financial tool that considers the performance of an entity

using four aspects. These are the financial perspective, customer/stakeholder perspective,

internal process related perspective and the organisational capacity. The main objective

of this tool is to provide the company with a strategy to satisfy all of the above mentioned

guidelines and to help in decision making (Tjader et al., 2014). When considering all of

the perspectives covered under a balanced scorecard and the scenarios faced by the entity,

it is evident that the tool can be used to guide the company in the process of making

decisions related to manufacturing specific products and outsourcing them. Although, the

limitation of the balanced scorecard has been found to be its inability to properly manage

the micro aspects of a business (Susilawati et al. 2013). This limitation is not completely

relevant in the present scenario as the company is not a very big organisation that

operates in a large number of business areas and produces a wide variety of range of

products. As the information about the company’s business and other perspectives is

quite clear, applying balanced scorecard in this case is more relevant (Sundharam,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGEMENT ACCOUNTING AND CONTROL

Sharma and Thangaiah 2013). From a financial perspective, the company should continue

its production in a manner which increases the overall profitability of its manufacturing

process. Hence, the company should consider following the production plan mentioned in

(a) to be able to maximise the profits earned by it. Apart from maximising the profits that

the company stands to earn in the given year, this plan also satisfies the various

perspectives measured by a balanced scorecard. Manufacturing only plastic chairs will

lead to a drastic decline in the profits of the company. Hence, it cannot be considered to

be a viable option as the company needs to generate profits to survive and thrive as a

business. This will also lead to the company not being able to meet its demand for other

products from the customers. Increasing the labour hours is good from a customer

perspective but it severely limits the capability of the company to generate high profits

from its manufacturing process. Not undertaking this measure also causes the business to

not meet the demands of its customers. Researchers suggest that the most important

aspect to consider when using balanced scorecard in the business is customer satisfaction.

In an ideal scenario, the main priority should be given to satisfying the customers in order

to satisfy and retain them. Hence, the company should consider accepting the outsourcing

offer as it leads to a reduction in the costs by a half. This will lead to the company to

meet the demand for its products in the market, while also avoiding the burdens caused

due to manufacturing the product itself (Leng et al., 2013). Other benefits that the

company can obtain from outsourcing the products are getting the time and resources to

focus on core activities, increasing the efficiency of the process of the business,

flexibility in staffing and gaining a competitive advantage over the competitors of the

business. This serves the purpose of ultimately leading to the development of the business

as a whole. However, apart from the financial and customer perspectives, there has been

an increasing demand from all stakeholders to consider environmental resources and

sustainability for the future generations into consideration. The usage of plastic has been

condemned by all the relevant authorities due to the negative effects caused by its usage.

There has been no support from the government authorities or the export countries. This

can also lead to a damage in the reputation of the company. Hence, in order to meet its

corporate social responsibility obligations and to make a good amount of profit on an

annual basis, the company should stop manufacturing the plastic chairs (Dinçer, Hacıoğlu

MANAGEMENT ACCOUNTING AND CONTROL

Sharma and Thangaiah 2013). From a financial perspective, the company should continue

its production in a manner which increases the overall profitability of its manufacturing

process. Hence, the company should consider following the production plan mentioned in

(a) to be able to maximise the profits earned by it. Apart from maximising the profits that

the company stands to earn in the given year, this plan also satisfies the various

perspectives measured by a balanced scorecard. Manufacturing only plastic chairs will

lead to a drastic decline in the profits of the company. Hence, it cannot be considered to

be a viable option as the company needs to generate profits to survive and thrive as a

business. This will also lead to the company not being able to meet its demand for other

products from the customers. Increasing the labour hours is good from a customer

perspective but it severely limits the capability of the company to generate high profits

from its manufacturing process. Not undertaking this measure also causes the business to

not meet the demands of its customers. Researchers suggest that the most important

aspect to consider when using balanced scorecard in the business is customer satisfaction.

In an ideal scenario, the main priority should be given to satisfying the customers in order

to satisfy and retain them. Hence, the company should consider accepting the outsourcing

offer as it leads to a reduction in the costs by a half. This will lead to the company to

meet the demand for its products in the market, while also avoiding the burdens caused

due to manufacturing the product itself (Leng et al., 2013). Other benefits that the

company can obtain from outsourcing the products are getting the time and resources to

focus on core activities, increasing the efficiency of the process of the business,

flexibility in staffing and gaining a competitive advantage over the competitors of the

business. This serves the purpose of ultimately leading to the development of the business

as a whole. However, apart from the financial and customer perspectives, there has been

an increasing demand from all stakeholders to consider environmental resources and

sustainability for the future generations into consideration. The usage of plastic has been

condemned by all the relevant authorities due to the negative effects caused by its usage.

There has been no support from the government authorities or the export countries. This

can also lead to a damage in the reputation of the company. Hence, in order to meet its

corporate social responsibility obligations and to make a good amount of profit on an

annual basis, the company should stop manufacturing the plastic chairs (Dinçer, Hacıoğlu

5

MANAGEMENT ACCOUNTING AND CONTROL

and Yüksel 2017). Although it is possible that the company may face the wrath of its

customers, this can be overcome by repositioning itself in the market as a company

manufacturing only environmental friendly products (Saeidi et al. 2015). A part of the

savings made in the costs by discontinuing the production can be invested in the

marketing of its products. For the remaining capacity of the wood chairs which it is not

able to produce currently, the company can choose to outsource the products as it can

earn a certain amount of profit by opting for the same.

Answer to Question 2

(a) In the given case, the three investment proposals of the three divisions called the leather

division, wood division and steel division vary from each other in terms of returns

provided on the investment, residual income provided and the economic value added by

each of the individual projects. While the return on investment of the proposal of the

leather division is positive throughout the lifetime of the asset, it never exceeds 9%

during the lifetime of the asset. The ROI of the proposal of the wood division is very high

and exceeds 10% in more than three years. The returns provided by this proposal are

fluctuating on a yearly basis and there is no guarantee of getting stable returns from this

proposal. The ROI of the investment proposed by the steel division is negative for the

first year but is increasing on a consistent basis from then on and provides extremely high

returns of around 69% in the final year of its lifetime. While all of the proposals have

their set of merits and demerits, it can be said that the proposals of the Steel Division and

Wood Division are viable as they provide similar returns on an average by the end of the

project. However, the company will have to survive initial losses to be able to implement

the Steel Division project. When considering residual income as a measure of the quality

of the investment proposal, the residual income provided by the proposal of the leather

division is higher than that of the wood division and the steel division (Havlíček,

Thalassinos and Berezkinova 2013). It is evident that leather division’s proposal is better

than the other two. In terms of economic value added to the organisation, the proposal of

the leather division is again considered to be more viable than that of the wood division

and steel division as the EVA of this proposal is more than that of the other two

proposals. It can be summarised that the investment proposals of the wood division and

MANAGEMENT ACCOUNTING AND CONTROL

and Yüksel 2017). Although it is possible that the company may face the wrath of its

customers, this can be overcome by repositioning itself in the market as a company

manufacturing only environmental friendly products (Saeidi et al. 2015). A part of the

savings made in the costs by discontinuing the production can be invested in the

marketing of its products. For the remaining capacity of the wood chairs which it is not

able to produce currently, the company can choose to outsource the products as it can

earn a certain amount of profit by opting for the same.

Answer to Question 2

(a) In the given case, the three investment proposals of the three divisions called the leather

division, wood division and steel division vary from each other in terms of returns

provided on the investment, residual income provided and the economic value added by

each of the individual projects. While the return on investment of the proposal of the

leather division is positive throughout the lifetime of the asset, it never exceeds 9%

during the lifetime of the asset. The ROI of the proposal of the wood division is very high

and exceeds 10% in more than three years. The returns provided by this proposal are

fluctuating on a yearly basis and there is no guarantee of getting stable returns from this

proposal. The ROI of the investment proposed by the steel division is negative for the

first year but is increasing on a consistent basis from then on and provides extremely high

returns of around 69% in the final year of its lifetime. While all of the proposals have

their set of merits and demerits, it can be said that the proposals of the Steel Division and

Wood Division are viable as they provide similar returns on an average by the end of the

project. However, the company will have to survive initial losses to be able to implement

the Steel Division project. When considering residual income as a measure of the quality

of the investment proposal, the residual income provided by the proposal of the leather

division is higher than that of the wood division and the steel division (Havlíček,

Thalassinos and Berezkinova 2013). It is evident that leather division’s proposal is better

than the other two. In terms of economic value added to the organisation, the proposal of

the leather division is again considered to be more viable than that of the wood division

and steel division as the EVA of this proposal is more than that of the other two

proposals. It can be summarised that the investment proposals of the wood division and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGEMENT ACCOUNTING AND CONTROL

the steel division are similar in nature in terms of the nature and timing of the returns,

economic value added and the residual income provided.

(b) Return on Investment (ROI) is the ratio between the net profit earned by an entity and the

cost of the investment made by it in a given year. It is used to indicate the percentage of

returns that an investor has been able to make over the amount he has invested in a given

financial year. The main benefits of using ROI as a measure of financial performance is

the better measurement of profitability along with the comparability between

investments. It also allows focusing on the performance of divisions where there is no

scope for much innovation and the major target is only to increase the profits (Auerbach,

Tulloch. and Possingham 2014). It is also convenient to use with the standard cost and

financial accounting systems followed on a worldwide basis. This measure suffers from

its own set of limitations despite the numerable benefits provided by it. While ROI

intends to measure the profit that an entity is earning on its investment, the profit that is

to be considered is not very clear in every case. There are many concepts of profit like

profit before tax, profit after tax and profit before depreciation and taxes and others. If a

company considers profit after tax for the measuring of ROI, a sudden increase in the tax

levels will reduce the ROI and make the investment seem unfavourable. Any unexpected

losses suffered by a company also play a part in reducing the ROI. While comparison of

ROIs is a benefit provided by this measure, differences arise due to the changes in

accounting policies followed by the divisions (Otley 2016). This results in making the

comparisons difficult. With regards to residual income, it is an effective concept as it

considers concepts like opportunity cost of capital in measuring the income. The concept

also considers the net operating assets used by the firm according to their updated value

and not the historical cost of the assets. This makes the results provided by it to be more

relevant. However, there are certain limitations in this model as well. In practical

application, a reliable measure of the opportunity cost of capital is difficult to arrive at

due to the nature of fluctuations in markets (McLellan 2014). Impairment of assets

without any proper evidence to back the same also leads to a decline in the value of the

residual income. This has been the case in many situations related to the measurement of

residual income. As residual income is an absolute measure, in order to compare the

performance of two divisions, one has to make sure that both the divisions are of the

MANAGEMENT ACCOUNTING AND CONTROL

the steel division are similar in nature in terms of the nature and timing of the returns,

economic value added and the residual income provided.

(b) Return on Investment (ROI) is the ratio between the net profit earned by an entity and the

cost of the investment made by it in a given year. It is used to indicate the percentage of

returns that an investor has been able to make over the amount he has invested in a given

financial year. The main benefits of using ROI as a measure of financial performance is

the better measurement of profitability along with the comparability between

investments. It also allows focusing on the performance of divisions where there is no

scope for much innovation and the major target is only to increase the profits (Auerbach,

Tulloch. and Possingham 2014). It is also convenient to use with the standard cost and

financial accounting systems followed on a worldwide basis. This measure suffers from

its own set of limitations despite the numerable benefits provided by it. While ROI

intends to measure the profit that an entity is earning on its investment, the profit that is

to be considered is not very clear in every case. There are many concepts of profit like

profit before tax, profit after tax and profit before depreciation and taxes and others. If a

company considers profit after tax for the measuring of ROI, a sudden increase in the tax

levels will reduce the ROI and make the investment seem unfavourable. Any unexpected

losses suffered by a company also play a part in reducing the ROI. While comparison of

ROIs is a benefit provided by this measure, differences arise due to the changes in

accounting policies followed by the divisions (Otley 2016). This results in making the

comparisons difficult. With regards to residual income, it is an effective concept as it

considers concepts like opportunity cost of capital in measuring the income. The concept

also considers the net operating assets used by the firm according to their updated value

and not the historical cost of the assets. This makes the results provided by it to be more

relevant. However, there are certain limitations in this model as well. In practical

application, a reliable measure of the opportunity cost of capital is difficult to arrive at

due to the nature of fluctuations in markets (McLellan 2014). Impairment of assets

without any proper evidence to back the same also leads to a decline in the value of the

residual income. This has been the case in many situations related to the measurement of

residual income. As residual income is an absolute measure, in order to compare the

performance of two divisions, one has to make sure that both the divisions are of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING AND CONTROL

same size and operate under similar conditions. Otherwise, it becomes quite evident that

this is not a suitable measure to compare the performances of two divisions. Economic

value added is defined as the value that an investment adds to the firm over the return

required by the shareholders. This is said to be a measure which quantifies the additional

economic benefits that a shareholder obtains due to investing in a specified investment

avenue. The main rationale of the EVA measure is highly acceptable as it is universally

accepted that the purpose of a business is to create value apart from providing returns to

the shareholders. It also acts as a good measure of the difference between the actual level

and the desired level of performance of a company. However, like the above mentioned

measures of performance, EVA becomes difficult to calculate and less reliable when the

aspects of measure keep changing on a constant basis. Whereas negative EVA is

considered not to be good, it has been proven that firms with negative EVA in the short

run provide extremely high returns in the short run (Ivanov, Leong and Zaima 2014).

This encourages investors to invest in such firms in the short run. Due to its nature of

relying heavily on the capital invested by a company, and being an absolute value of

measure, EVA tends to look much better for larger firms than for the smaller firms and

the start-ups. Hence, in case of companies which are heavy on intangible assets like

technology and service oriented companies, EVA cannot be used as a reliable source of

measure to know the value created by the firm. As in the case of Residual Income, EVA

remains relevant only to the period for which it is calculated and cannot be reliably used

to measure the future trends and forecasts of the company. It has been noted that correctly

calculating the EVA needs around 164 adjustments to be made to the calculated

accounting reports to remove the distortions caused by accounting rules and regulations.

In practice, accountants and firms do not use more than a dozen of these (Collier 2015).

(c) Short term financial measures have long been criticised by various research scholars and

users for their lack of completeness, neutrality, balance and their encouragement of

having a short term vision (Anon 2019). There is also no clarity about a standard measure

to measure the performance of a firm (Miller, Washburn and Glick 2013). While using

the short term measures of financial performance, the focus of the organisation remains

only on areas which are to be worked on to improve the immediate financial performance

of the company. However, they never fail to provide concrete solutions to sustaining the

MANAGEMENT ACCOUNTING AND CONTROL

same size and operate under similar conditions. Otherwise, it becomes quite evident that

this is not a suitable measure to compare the performances of two divisions. Economic

value added is defined as the value that an investment adds to the firm over the return

required by the shareholders. This is said to be a measure which quantifies the additional

economic benefits that a shareholder obtains due to investing in a specified investment

avenue. The main rationale of the EVA measure is highly acceptable as it is universally

accepted that the purpose of a business is to create value apart from providing returns to

the shareholders. It also acts as a good measure of the difference between the actual level

and the desired level of performance of a company. However, like the above mentioned

measures of performance, EVA becomes difficult to calculate and less reliable when the

aspects of measure keep changing on a constant basis. Whereas negative EVA is

considered not to be good, it has been proven that firms with negative EVA in the short

run provide extremely high returns in the short run (Ivanov, Leong and Zaima 2014).

This encourages investors to invest in such firms in the short run. Due to its nature of

relying heavily on the capital invested by a company, and being an absolute value of

measure, EVA tends to look much better for larger firms than for the smaller firms and

the start-ups. Hence, in case of companies which are heavy on intangible assets like

technology and service oriented companies, EVA cannot be used as a reliable source of

measure to know the value created by the firm. As in the case of Residual Income, EVA

remains relevant only to the period for which it is calculated and cannot be reliably used

to measure the future trends and forecasts of the company. It has been noted that correctly

calculating the EVA needs around 164 adjustments to be made to the calculated

accounting reports to remove the distortions caused by accounting rules and regulations.

In practice, accountants and firms do not use more than a dozen of these (Collier 2015).

(c) Short term financial measures have long been criticised by various research scholars and

users for their lack of completeness, neutrality, balance and their encouragement of

having a short term vision (Anon 2019). There is also no clarity about a standard measure

to measure the performance of a firm (Miller, Washburn and Glick 2013). While using

the short term measures of financial performance, the focus of the organisation remains

only on areas which are to be worked on to improve the immediate financial performance

of the company. However, they never fail to provide concrete solutions to sustaining the

8

MANAGEMENT ACCOUNTING AND CONTROL

performance in the long run or any information about the market conditions that may

exist in the future. Hence, to overcome these deficiencies, it becomes vital for KAdlex

PLC to adopt a more complete and long term performance measure which measures both

the financial and the non-financial factors which are likely to impact the business.

Balance scorecard has proven itself to be such a measure over the years since it was first

adopted (Akkermans and Van Oorschot 2018). Its focus remains on becoming a tool

which measures the performance of the firm as a whole and not just on improving the

profitability of the firm. Other factors like customer perspective, internal process, and

organisational capacity to learn and grow are all required to be considered while forming

the policies of an entity. This reduces the firm’s short term planning and helps it in

forming a business where the focus is on creating a sustainable and growth oriented

business for a long period of time. This aligns all the activities of the firm into a single

strategy and makes sure that everyone works towards achieving the vision and mission of

the organisation. This perspective is important as the firm should always strive to carry

on its business in the future and not wind itself up at the first available opportunity.

MANAGEMENT ACCOUNTING AND CONTROL

performance in the long run or any information about the market conditions that may

exist in the future. Hence, to overcome these deficiencies, it becomes vital for KAdlex

PLC to adopt a more complete and long term performance measure which measures both

the financial and the non-financial factors which are likely to impact the business.

Balance scorecard has proven itself to be such a measure over the years since it was first

adopted (Akkermans and Van Oorschot 2018). Its focus remains on becoming a tool

which measures the performance of the firm as a whole and not just on improving the

profitability of the firm. Other factors like customer perspective, internal process, and

organisational capacity to learn and grow are all required to be considered while forming

the policies of an entity. This reduces the firm’s short term planning and helps it in

forming a business where the focus is on creating a sustainable and growth oriented

business for a long period of time. This aligns all the activities of the firm into a single

strategy and makes sure that everyone works towards achieving the vision and mission of

the organisation. This perspective is important as the firm should always strive to carry

on its business in the future and not wind itself up at the first available opportunity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGEMENT ACCOUNTING AND CONTROL

Bibliography

Akkermans, H.A. and Van Oorschot, K.E., 2018. Relevance assumed: a case study of balanced

scorecard development using system dynamics. In System Dynamics (pp. 107-132). Palgrave

Macmillan, London.

Anon, (2019). [Online] Available at:

https://www.researchgate.net/publication/235320491_The_balanced_scorecard_Short-

term_guest_or_long-term_resident [Accessed 26 Jul. 2019].

Auerbach, N.A., Tulloch, A.I. and Possingham, H.P., 2014. Informed actions: where to cost

effectively manage multiple threats to species to maximize return on investment. Ecological

Applications, 24(6), pp.1357-1373.

Caprice, S., Schlippenbach, V.V. and Wey, C., 2014. Supplier Fixed Costs and Retail Market

Monopolization.

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for decision

making. John Wiley & Sons.

Dinçer, H., Hacıoğlu, Ü. and Yüksel, S., 2017. Balanced scorecard based performance

measurement of European airlines using a hybrid multicriteria decision making approach under

the fuzzy environment. Journal of Air Transport Management, 63, pp.17-33.

Havlíček, K., Thalassinos, I.E. and Berezkinova, L., 2013. Innovation management and

controlling in SMEs. European Research Studies Journal, 16(4), pp.57-70.

Ivanov, S.I., Leong, K. and Zaima, J.K., 2014. An empirical examination of negative economic

value added firms. The International Journal of Business and Finance Research, 8(1), pp.103-

112.

Leng, J.W., Jiang, P.Y., Zhang, F.Q. and Cao, W., 2013. Framework and key enabling

technologies for social manufacturing. In Applied Mechanics and Materials (Vol. 312, pp. 498-

501). Trans Tech Publications.

McLellan, J.D., 2014. Management Accounting Theory and Practice: Measuring the Gap in

United States Businesses. Journal of Accounting, Business & Management, 21(1).

Miller, C.C., Washburn, N.T. and Glick, W.H., 2013. Perspective— the myth of firm

performance. Organization Science, 24(3), pp.948-964.

MANAGEMENT ACCOUNTING AND CONTROL

Bibliography

Akkermans, H.A. and Van Oorschot, K.E., 2018. Relevance assumed: a case study of balanced

scorecard development using system dynamics. In System Dynamics (pp. 107-132). Palgrave

Macmillan, London.

Anon, (2019). [Online] Available at:

https://www.researchgate.net/publication/235320491_The_balanced_scorecard_Short-

term_guest_or_long-term_resident [Accessed 26 Jul. 2019].

Auerbach, N.A., Tulloch, A.I. and Possingham, H.P., 2014. Informed actions: where to cost

effectively manage multiple threats to species to maximize return on investment. Ecological

Applications, 24(6), pp.1357-1373.

Caprice, S., Schlippenbach, V.V. and Wey, C., 2014. Supplier Fixed Costs and Retail Market

Monopolization.

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for decision

making. John Wiley & Sons.

Dinçer, H., Hacıoğlu, Ü. and Yüksel, S., 2017. Balanced scorecard based performance

measurement of European airlines using a hybrid multicriteria decision making approach under

the fuzzy environment. Journal of Air Transport Management, 63, pp.17-33.

Havlíček, K., Thalassinos, I.E. and Berezkinova, L., 2013. Innovation management and

controlling in SMEs. European Research Studies Journal, 16(4), pp.57-70.

Ivanov, S.I., Leong, K. and Zaima, J.K., 2014. An empirical examination of negative economic

value added firms. The International Journal of Business and Finance Research, 8(1), pp.103-

112.

Leng, J.W., Jiang, P.Y., Zhang, F.Q. and Cao, W., 2013. Framework and key enabling

technologies for social manufacturing. In Applied Mechanics and Materials (Vol. 312, pp. 498-

501). Trans Tech Publications.

McLellan, J.D., 2014. Management Accounting Theory and Practice: Measuring the Gap in

United States Businesses. Journal of Accounting, Business & Management, 21(1).

Miller, C.C., Washburn, N.T. and Glick, W.H., 2013. Perspective— the myth of firm

performance. Organization Science, 24(3), pp.948-964.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGEMENT ACCOUNTING AND CONTROL

Novák, P. and Popesko, B., 2014. Cost variability and cost behaviour in manufacturing

enterprises. Economics and Sociology.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

Pasandideh, S.H.R., Niaki, S.T.A. and Gharaei, A., 2015. Optimization of a multiproduct

economic production quantity problem with stochastic constraints using sequential quadratic

programming. Knowledge-Based Systems, 84, pp.98-107.

Saeidi, S.P., Sofian, S., Saeidi, P., Saeidi, S.P. and Saaeidi, S.A., 2015. How does corporate

social responsibility contribute to firm financial performance? The mediating role of competitive

advantage, reputation, and customer satisfaction. Journal of business research, 68(2), pp.341-

350.

Sajtiprasert, W., 2014. Application of economic order quantity (EOQ) for inventory management

of a food ingredient importer.

Sundharam, V.N., Sharma, V. and Stephan Thangaiah, I.S., 2013. An integration of BSC and

AHP for sustainable growth of manufacturing industries. International Journal of Business

Excellence, 6(1), pp.77-92.

Susilawati, A., Tan, J., Bell, D. and Sarwar, M., 2013. Develop a framework of performance

measurement and improvement system for lean manufacturing activity. International Journal of

Lean Thinking, 4(1), pp.51-64.

Tjader, Y., May, J.H., Shang, J., Vargas, L.G. and Gao, N., 2014. Firm-level outsourcing

decision making: A balanced scorecard-based analytic network process model. International

Journal of Production Economics, 147, pp.614-623.

Vijayashree, M. and Uthayakumar, R., 2014. An integrated inventory model with controllable

lead time and setup cost reduction for defective and non-defective items. International Journal

of Supply and Operations Management, 1(2), p.190.

Walther, L.M. and Skousen, C.J., 2017. Cost Analysis. Bookboon.

MANAGEMENT ACCOUNTING AND CONTROL

Novák, P. and Popesko, B., 2014. Cost variability and cost behaviour in manufacturing

enterprises. Economics and Sociology.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

Pasandideh, S.H.R., Niaki, S.T.A. and Gharaei, A., 2015. Optimization of a multiproduct

economic production quantity problem with stochastic constraints using sequential quadratic

programming. Knowledge-Based Systems, 84, pp.98-107.

Saeidi, S.P., Sofian, S., Saeidi, P., Saeidi, S.P. and Saaeidi, S.A., 2015. How does corporate

social responsibility contribute to firm financial performance? The mediating role of competitive

advantage, reputation, and customer satisfaction. Journal of business research, 68(2), pp.341-

350.

Sajtiprasert, W., 2014. Application of economic order quantity (EOQ) for inventory management

of a food ingredient importer.

Sundharam, V.N., Sharma, V. and Stephan Thangaiah, I.S., 2013. An integration of BSC and

AHP for sustainable growth of manufacturing industries. International Journal of Business

Excellence, 6(1), pp.77-92.

Susilawati, A., Tan, J., Bell, D. and Sarwar, M., 2013. Develop a framework of performance

measurement and improvement system for lean manufacturing activity. International Journal of

Lean Thinking, 4(1), pp.51-64.

Tjader, Y., May, J.H., Shang, J., Vargas, L.G. and Gao, N., 2014. Firm-level outsourcing

decision making: A balanced scorecard-based analytic network process model. International

Journal of Production Economics, 147, pp.614-623.

Vijayashree, M. and Uthayakumar, R., 2014. An integrated inventory model with controllable

lead time and setup cost reduction for defective and non-defective items. International Journal

of Supply and Operations Management, 1(2), p.190.

Walther, L.M. and Skousen, C.J., 2017. Cost Analysis. Bookboon.

11

MANAGEMENT ACCOUNTING AND CONTROL

Appendix

Calculations of Question 1(a)

Particulars Plastic Wood Leather Metal Total

Contribution per unit 55 60 42 52

Machine Hours per unit 5 5 3 4

Labour Hours per unit 1 1 2 2

Contribution per machine hour 11 12 14 13

Rank on the basis of contribution 4 3 1 2

Profitable Production Plan:

Units To be produced 0 220 300 300

Machine Hours Consumed 0 1100 900 1200 3200

Contribution 0 13200 12600 15600 41400

Fixed Costs 0 3960 10800 10800 25560

Profit 0 9240 1800 4800 15840

Calculations of Question 2(a)

0 Leather

Division

Total

Year 0

Cash Outflow -

73000.0

0

Operating Income 21000 21000 21000 21000 21000

Depreciation -13870 -13870 -13870 -13870 -13870

Net operating

Income

7130 7130 7130 7130 7130

Discounting Factor

@ 15%

1 0.869565

22

0.756143

67

0.6575

16

0.5717

53

0.4971

77

Discounted Cash

Flows

-73000 6200 5391.304

35

4688.0

91

4076.6

01

3544.8

7

Residual Value 3650.0

0

ROI 8.493150

68

9.117714

1

4.6536

54

3.5569

33

5.5999

92

Desired Income 10950 8869.5 6789 4708.5 2628

Residual Income 10050 12130.5 14211 16291.

5

18372 71055

MANAGEMENT ACCOUNTING AND CONTROL

Appendix

Calculations of Question 1(a)

Particulars Plastic Wood Leather Metal Total

Contribution per unit 55 60 42 52

Machine Hours per unit 5 5 3 4

Labour Hours per unit 1 1 2 2

Contribution per machine hour 11 12 14 13

Rank on the basis of contribution 4 3 1 2

Profitable Production Plan:

Units To be produced 0 220 300 300

Machine Hours Consumed 0 1100 900 1200 3200

Contribution 0 13200 12600 15600 41400

Fixed Costs 0 3960 10800 10800 25560

Profit 0 9240 1800 4800 15840

Calculations of Question 2(a)

0 Leather

Division

Total

Year 0

Cash Outflow -

73000.0

0

Operating Income 21000 21000 21000 21000 21000

Depreciation -13870 -13870 -13870 -13870 -13870

Net operating

Income

7130 7130 7130 7130 7130

Discounting Factor

@ 15%

1 0.869565

22

0.756143

67

0.6575

16

0.5717

53

0.4971

77

Discounted Cash

Flows

-73000 6200 5391.304

35

4688.0

91

4076.6

01

3544.8

7

Residual Value 3650.0

0

ROI 8.493150

68

9.117714

1

4.6536

54

3.5569

33

5.5999

92

Desired Income 10950 8869.5 6789 4708.5 2628

Residual Income 10050 12130.5 14211 16291.

5

18372 71055

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.