Analysis of Management Accounting Systems for Sustainable Business

VerifiedAdded on 2023/01/19

|19

|5360

|41

Report

AI Summary

This report delves into the principles and practices of management accounting, using CORUS, a steel manufacturing company, as a case study. It examines the core concepts of management accounting, including planning, decision-making, and control, highlighting the differences between management and financial accounting. The report explores various management accounting systems, such as inventory management and cost accounting, detailing their benefits and applications. It then analyzes different reporting methods like budget reports, accounts receivables ageing reports, cost reports, and inventory reports, emphasizing their roles in decision-making and operational efficiency. Furthermore, the report reflects on income statement preparation using marginal and absorption costing, evaluates planning tools in budgetary control, and showcases how management accounting techniques help address financial problems and achieve sustainable success within CORUS. The analysis covers the importance of inventory management, cost accounting systems, and the use of price optimization to enhance business outcomes. The report concludes by summarizing the significance of management accounting in guiding business operations and fostering financial stability.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................4

MAIN BODY...................................................................................................................................4

LO 1.................................................................................................................................................4

P1 Understanding management accounting and management accounting systems...............4

P2 Different methods used for management accounting reporting........................................6

M1. Evaluating the benefits of different management accounting systems...........................8

LO2..................................................................................................................................................9

P3. Reflecting income statement as per marginal and absorption costing.............................9

LO3................................................................................................................................................10

P 4 Advantages and disadvantages of different types of planning tools in budgetary control10

M 3 Use of different planning tools and their application....................................................12

LO4................................................................................................................................................12

P 5 Management accounting system to respond to financial problems................................12

M 4 Management accounting helps in gaining sustainable success.....................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

MAIN BODY...................................................................................................................................4

LO 1.................................................................................................................................................4

P1 Understanding management accounting and management accounting systems...............4

P2 Different methods used for management accounting reporting........................................6

M1. Evaluating the benefits of different management accounting systems...........................8

LO2..................................................................................................................................................9

P3. Reflecting income statement as per marginal and absorption costing.............................9

LO3................................................................................................................................................10

P 4 Advantages and disadvantages of different types of planning tools in budgetary control10

M 3 Use of different planning tools and their application....................................................12

LO4................................................................................................................................................12

P 5 Management accounting system to respond to financial problems................................12

M 4 Management accounting helps in gaining sustainable success.....................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting refers to the practice of analysing, presenting and interpreting an

accounting information that is been gathered with help of financial accounting and the cost

accounting for the purpose of assisting the management in decision making process, creating

policy, making routine operations for an organization, The main objective of MA is to measure

the performance, assessing risk, allocating the resources and presenting the final reports to

management which helps them in preparing budget, forecasting success and also helps in taking

corrective measures in respect of dealing with any kind of the financial problem. This study is

based on CORUS, a manufacturing company that deals producing steel and distributes its

products like cold and hot rolled, packaging, tubes, bars, electro-plated, metallic coated,

developing components. Its business operations are been spread across the whole world and is

headquartered in United Kingdom. Furthermore, the report provides a deeper insight towards

importance of MA systems and different methods that can be adopted for reporting with benefits

of each system that helps the firm in running its business operations smoothly. Moreover, the

report reflects framing of income statement as per marginal and absorption costing method along

with the evaluation of different panning tools and their use in solving the financial problem.

Several MA techniques are also been highlighted that CORUS is using for avoiding any type of

financial problem and uncertainty in the future.

MAIN BODY

LO 1

P1 Understanding management accounting and management accounting systems

Management Accounting is defined as a process through which the organisations

simplify the entire process of recording the transactions and facilitating activities related to

operational activities of the company (Sands, Lee and Gunarathne, 2015).. This technique assists

the managers and accountants working in an organisation in determining the operational costs

incurred in the business and also help to control and minimise such costs by reducing the

unnecessary expenditure avenues of the company. Overall, management accounting is a great

tool which facilitates the decision making of the managers of the company. However, financial

accounting must not be confused with management accounting since there is a very fine line

Management accounting refers to the practice of analysing, presenting and interpreting an

accounting information that is been gathered with help of financial accounting and the cost

accounting for the purpose of assisting the management in decision making process, creating

policy, making routine operations for an organization, The main objective of MA is to measure

the performance, assessing risk, allocating the resources and presenting the final reports to

management which helps them in preparing budget, forecasting success and also helps in taking

corrective measures in respect of dealing with any kind of the financial problem. This study is

based on CORUS, a manufacturing company that deals producing steel and distributes its

products like cold and hot rolled, packaging, tubes, bars, electro-plated, metallic coated,

developing components. Its business operations are been spread across the whole world and is

headquartered in United Kingdom. Furthermore, the report provides a deeper insight towards

importance of MA systems and different methods that can be adopted for reporting with benefits

of each system that helps the firm in running its business operations smoothly. Moreover, the

report reflects framing of income statement as per marginal and absorption costing method along

with the evaluation of different panning tools and their use in solving the financial problem.

Several MA techniques are also been highlighted that CORUS is using for avoiding any type of

financial problem and uncertainty in the future.

MAIN BODY

LO 1

P1 Understanding management accounting and management accounting systems

Management Accounting is defined as a process through which the organisations

simplify the entire process of recording the transactions and facilitating activities related to

operational activities of the company (Sands, Lee and Gunarathne, 2015).. This technique assists

the managers and accountants working in an organisation in determining the operational costs

incurred in the business and also help to control and minimise such costs by reducing the

unnecessary expenditure avenues of the company. Overall, management accounting is a great

tool which facilitates the decision making of the managers of the company. However, financial

accounting must not be confused with management accounting since there is a very fine line

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

between both the modes of accounting. At Corus Group as well, the financial management and

financial managers assist in preparation of financial statement that helps in attracting the external

parties and investors of the company and management accounting is prepared for the internal

purpose i.e. for determining what will be their budgeted costs and how it can be minimised or to

compare such budgeted costs with the actual ones (Kaplan and Atkinson, 2015). Management

accounting plays a major role in the operation of Tata Corus and this can be ascertained through

following points:

Planning: Management Accounting is a major step in the planning done in the organisation due

to the various accounting tools that are being used which helps in determining the estimated

resource usage or the estimated cost that might be incurred in the company. Therefore it assists

in preplanning of the company.

Decision-Making: Management Accounting helps the mangers in formulating various

interpretations regarding the current resources, expenditures and income sources of the company.

Therefore, the company can be assisted in formulating various decisions related to the company

in a simplified manner.

Controlling: Management accounting also assists in regularly monitoring and evaluation of the

processes and techniques that are being implemented in the company. This helps the managers in

determining what is going wrong and right so that the managers are able to determine whatever

deviations that might be incurred between the estimated and actual costs.

In order to implement the management accounting systems, there are a variety of tools

that can be used and these can be categorised as follows:

Inventory Management System: Inventory Management System assists in maintaining and

keeping control of the stock levels in the company that are being used and ensuring that there are

no excess stocks in the company i.e. the cost incurred in maintaining the stock in the company

does not exceed too much or falls too low (Otley, 2016). There are various systems through

which inventory levels can be managed i.e. LIFO, FIFO etc. While LIFO is related to “Last In

First Out” under which the stock that has entered last is used first and the older stock is used later

on; in FIFO method which is “First In First Out”, the stock that entered earlier is used first and

the stock that entered later is used after that. Both of these inventory systems are used in the

management of the stock in the company so that the working capital of the company does not

gets blocked. Further, this system assists the management accountants in determining the

financial managers assist in preparation of financial statement that helps in attracting the external

parties and investors of the company and management accounting is prepared for the internal

purpose i.e. for determining what will be their budgeted costs and how it can be minimised or to

compare such budgeted costs with the actual ones (Kaplan and Atkinson, 2015). Management

accounting plays a major role in the operation of Tata Corus and this can be ascertained through

following points:

Planning: Management Accounting is a major step in the planning done in the organisation due

to the various accounting tools that are being used which helps in determining the estimated

resource usage or the estimated cost that might be incurred in the company. Therefore it assists

in preplanning of the company.

Decision-Making: Management Accounting helps the mangers in formulating various

interpretations regarding the current resources, expenditures and income sources of the company.

Therefore, the company can be assisted in formulating various decisions related to the company

in a simplified manner.

Controlling: Management accounting also assists in regularly monitoring and evaluation of the

processes and techniques that are being implemented in the company. This helps the managers in

determining what is going wrong and right so that the managers are able to determine whatever

deviations that might be incurred between the estimated and actual costs.

In order to implement the management accounting systems, there are a variety of tools

that can be used and these can be categorised as follows:

Inventory Management System: Inventory Management System assists in maintaining and

keeping control of the stock levels in the company that are being used and ensuring that there are

no excess stocks in the company i.e. the cost incurred in maintaining the stock in the company

does not exceed too much or falls too low (Otley, 2016). There are various systems through

which inventory levels can be managed i.e. LIFO, FIFO etc. While LIFO is related to “Last In

First Out” under which the stock that has entered last is used first and the older stock is used later

on; in FIFO method which is “First In First Out”, the stock that entered earlier is used first and

the stock that entered later is used after that. Both of these inventory systems are used in the

management of the stock in the company so that the working capital of the company does not

gets blocked. Further, this system assists the management accountants in determining the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

duration for which the company needs to maintain the reorder quantity of stock i.e. that level at

which the company order for next batch of goods thus assisting the management in maintain the

costs incurred in the business operations.

Cost Accounting System: The meaning of cost accounting systems can be defined as a means

through which the company can ascertain the costs that might get incurred in manufacturing of

the products and also goes a step further by analysing the profitability of the company and

predicting so that later it can be compared with actual. Job Costing, Standard Costing and

process costing are some of the strategies through which this can be implemented. Job costing

techniques is used when the cost of a particular product’s manufacturing or a particular job needs

to be ascertained rather than that of the entire company. Process Costing can also be defined as

that technique which assists the management in determining the costs related to the entire

manufacturing or production process of the company and therefore, assists the management in

formulate the pocket friendly and budget friendly targets in the company (Morse, 2015).

Therefore such costing systems help the management in estimating the total cost that might get

incurred.

P2 Different methods used for management accounting reporting

Management accounting reporting comprises of the various documents that are prepared

under the accounting in the entire process. Some of these can be classified as:

Budget report: This kind of report assists the managers in taking decisions that are related to the

cost aspect in the business i.e. it helps in allocating and ascertaining the resources that might be

required and these are then compared to the resources which were actually consumed thus

improving the efficiency of the organisation. When the deviation or variance that exists between

the estimated and actual costs, the managers are able to determine what are the reasons behind

such inconsistencies and this are then removed from the company thus overall, making it a very

important tool in the organisations. These also help in ensuring that the company is allocating its

resources in a proper manner and there are no over expenditure or under expenditure. These are

usually prepared between fixed time intervals that are usually ranging from a period of 1 year to

a quarterly basis, however there is no specific bondation i.e. it can be prepared as per the need of

the management i.e. as and when required by them.

Accounts Receivables Ageing Report: This report is prepared by the managers when they want

to easily categorize and segregate the receivables of the company. The managers try to balance

which the company order for next batch of goods thus assisting the management in maintain the

costs incurred in the business operations.

Cost Accounting System: The meaning of cost accounting systems can be defined as a means

through which the company can ascertain the costs that might get incurred in manufacturing of

the products and also goes a step further by analysing the profitability of the company and

predicting so that later it can be compared with actual. Job Costing, Standard Costing and

process costing are some of the strategies through which this can be implemented. Job costing

techniques is used when the cost of a particular product’s manufacturing or a particular job needs

to be ascertained rather than that of the entire company. Process Costing can also be defined as

that technique which assists the management in determining the costs related to the entire

manufacturing or production process of the company and therefore, assists the management in

formulate the pocket friendly and budget friendly targets in the company (Morse, 2015).

Therefore such costing systems help the management in estimating the total cost that might get

incurred.

P2 Different methods used for management accounting reporting

Management accounting reporting comprises of the various documents that are prepared

under the accounting in the entire process. Some of these can be classified as:

Budget report: This kind of report assists the managers in taking decisions that are related to the

cost aspect in the business i.e. it helps in allocating and ascertaining the resources that might be

required and these are then compared to the resources which were actually consumed thus

improving the efficiency of the organisation. When the deviation or variance that exists between

the estimated and actual costs, the managers are able to determine what are the reasons behind

such inconsistencies and this are then removed from the company thus overall, making it a very

important tool in the organisations. These also help in ensuring that the company is allocating its

resources in a proper manner and there are no over expenditure or under expenditure. These are

usually prepared between fixed time intervals that are usually ranging from a period of 1 year to

a quarterly basis, however there is no specific bondation i.e. it can be prepared as per the need of

the management i.e. as and when required by them.

Accounts Receivables Ageing Report: This report is prepared by the managers when they want

to easily categorize and segregate the receivables of the company. The managers try to balance

the receivables in a perfect ratio trying to ensure that it is not too high and not too low thus

protecting the company against any probable bad debts (Agrawal and Cooper, 2017). The report

ultimately helps in determining a particular limit or amount up to which the companies should

allow goods to be sold on the credit so that the risk of bad debts does not get too high and neither

does the cash gets blocked unnecessarily or is available in too much excess. Thus in management

accounting, the ageing report helps in regular monitoring and evaluation of the credit that is

being given in the business entity ensuring that the company is trading in a balanced manner and

therefore can be stated as an important and comprehensive part in the decision making ability of

the managers of a company.

Cost report: This kind of managerial report helps in depicting and ascertaining the cost that will

be involved in the various stages in production of the product (Bobryshev and et.al., 2015). A

comparison is made between the previous and current cost and the causes for increase or

decrease in the cost are determined and analysed accordingly. This assists in determining that

whether the current cost levels of the company are in control or not and whether any policies

need to be adopted in the entire procedure. Job costing also comprises of costing reports in the

manner such as by determining cost associated with individual jobs and these are usually

beneficial in companies like event management ones where the cost can be allocated to a

particular job or task but in manufacturing industries like Corus, it is a difficult task and

therefore, it is not of much use to the company.

Inventory report: this kind of report is prepared to keep track of the incoming and consumption

of the raw material that is being used by the manufacturing unit. This helps in determining what

the current inventory level is and whether it is blocking working capital unnecessarily or is

acting towards loss of production of the goods. It also details what would be the additional

requirement of the raw material in future. Therefore, the management accounting is assisted by

the inventory report that is being prepared and hence assists in ensuring that appropriate stock

levels are maintained in the company (Chiarini and Vagnoni, 2015). It is a major tool in the

entire decision making process for the managers and acts as a basis for the company in

formulating various budgets so that revenue as well as cost can be predicted.

Therefore, it can be concluded that apart from the reports mentioned above, there are

many additional reports also which are prepared by the managerial accountants like executive

protecting the company against any probable bad debts (Agrawal and Cooper, 2017). The report

ultimately helps in determining a particular limit or amount up to which the companies should

allow goods to be sold on the credit so that the risk of bad debts does not get too high and neither

does the cash gets blocked unnecessarily or is available in too much excess. Thus in management

accounting, the ageing report helps in regular monitoring and evaluation of the credit that is

being given in the business entity ensuring that the company is trading in a balanced manner and

therefore can be stated as an important and comprehensive part in the decision making ability of

the managers of a company.

Cost report: This kind of managerial report helps in depicting and ascertaining the cost that will

be involved in the various stages in production of the product (Bobryshev and et.al., 2015). A

comparison is made between the previous and current cost and the causes for increase or

decrease in the cost are determined and analysed accordingly. This assists in determining that

whether the current cost levels of the company are in control or not and whether any policies

need to be adopted in the entire procedure. Job costing also comprises of costing reports in the

manner such as by determining cost associated with individual jobs and these are usually

beneficial in companies like event management ones where the cost can be allocated to a

particular job or task but in manufacturing industries like Corus, it is a difficult task and

therefore, it is not of much use to the company.

Inventory report: this kind of report is prepared to keep track of the incoming and consumption

of the raw material that is being used by the manufacturing unit. This helps in determining what

the current inventory level is and whether it is blocking working capital unnecessarily or is

acting towards loss of production of the goods. It also details what would be the additional

requirement of the raw material in future. Therefore, the management accounting is assisted by

the inventory report that is being prepared and hence assists in ensuring that appropriate stock

levels are maintained in the company (Chiarini and Vagnoni, 2015). It is a major tool in the

entire decision making process for the managers and acts as a basis for the company in

formulating various budgets so that revenue as well as cost can be predicted.

Therefore, it can be concluded that apart from the reports mentioned above, there are

many additional reports also which are prepared by the managerial accountants like executive

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

report which helps in determining what it the time scale and resource scale in determining how

the much is time expectancy rate of the project intended to be carried out.

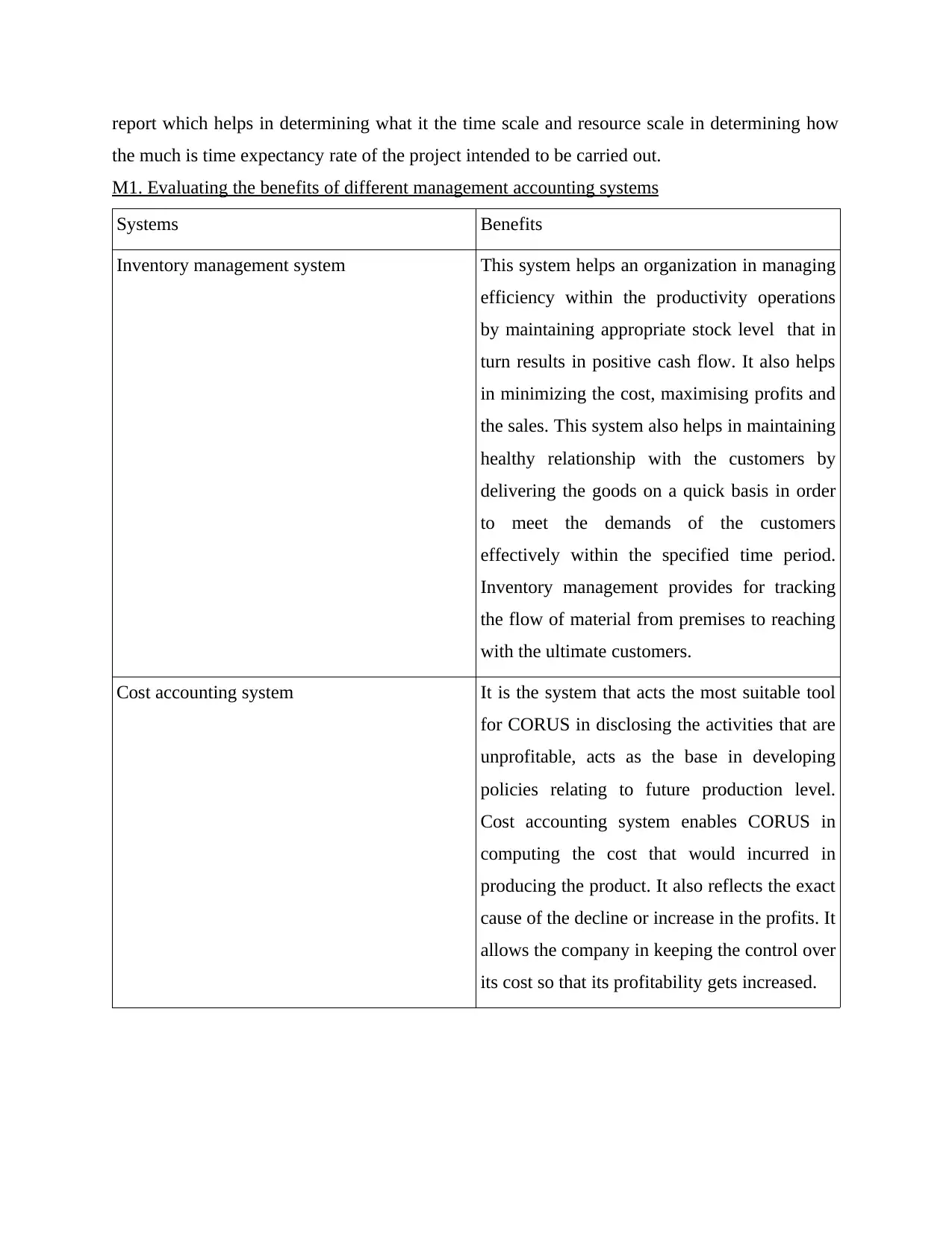

M1. Evaluating the benefits of different management accounting systems

Systems Benefits

Inventory management system This system helps an organization in managing

efficiency within the productivity operations

by maintaining appropriate stock level that in

turn results in positive cash flow. It also helps

in minimizing the cost, maximising profits and

the sales. This system also helps in maintaining

healthy relationship with the customers by

delivering the goods on a quick basis in order

to meet the demands of the customers

effectively within the specified time period.

Inventory management provides for tracking

the flow of material from premises to reaching

with the ultimate customers.

Cost accounting system It is the system that acts the most suitable tool

for CORUS in disclosing the activities that are

unprofitable, acts as the base in developing

policies relating to future production level.

Cost accounting system enables CORUS in

computing the cost that would incurred in

producing the product. It also reflects the exact

cause of the decline or increase in the profits. It

allows the company in keeping the control over

its cost so that its profitability gets increased.

the much is time expectancy rate of the project intended to be carried out.

M1. Evaluating the benefits of different management accounting systems

Systems Benefits

Inventory management system This system helps an organization in managing

efficiency within the productivity operations

by maintaining appropriate stock level that in

turn results in positive cash flow. It also helps

in minimizing the cost, maximising profits and

the sales. This system also helps in maintaining

healthy relationship with the customers by

delivering the goods on a quick basis in order

to meet the demands of the customers

effectively within the specified time period.

Inventory management provides for tracking

the flow of material from premises to reaching

with the ultimate customers.

Cost accounting system It is the system that acts the most suitable tool

for CORUS in disclosing the activities that are

unprofitable, acts as the base in developing

policies relating to future production level.

Cost accounting system enables CORUS in

computing the cost that would incurred in

producing the product. It also reflects the exact

cause of the decline or increase in the profits. It

allows the company in keeping the control over

its cost so that its profitability gets increased.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

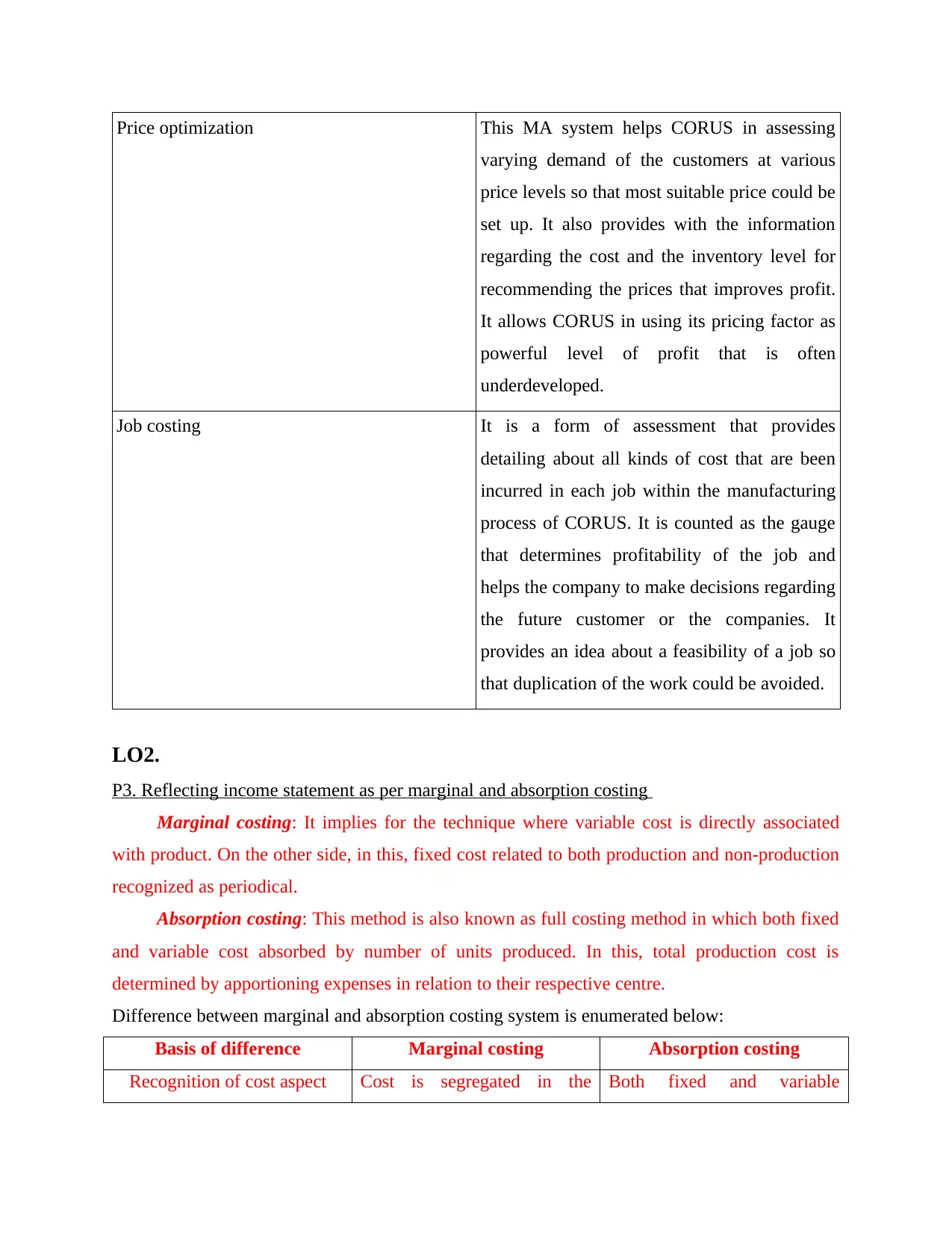

Price optimization This MA system helps CORUS in assessing

varying demand of the customers at various

price levels so that most suitable price could be

set up. It also provides with the information

regarding the cost and the inventory level for

recommending the prices that improves profit.

It allows CORUS in using its pricing factor as

powerful level of profit that is often

underdeveloped.

Job costing It is a form of assessment that provides

detailing about all kinds of cost that are been

incurred in each job within the manufacturing

process of CORUS. It is counted as the gauge

that determines profitability of the job and

helps the company to make decisions regarding

the future customer or the companies. It

provides an idea about a feasibility of a job so

that duplication of the work could be avoided.

LO2.

P3. Reflecting income statement as per marginal and absorption costing

Marginal costing: It implies for the technique where variable cost is directly associated

with product. On the other side, in this, fixed cost related to both production and non-production

recognized as periodical.

Absorption costing: This method is also known as full costing method in which both fixed

and variable cost absorbed by number of units produced. In this, total production cost is

determined by apportioning expenses in relation to their respective centre.

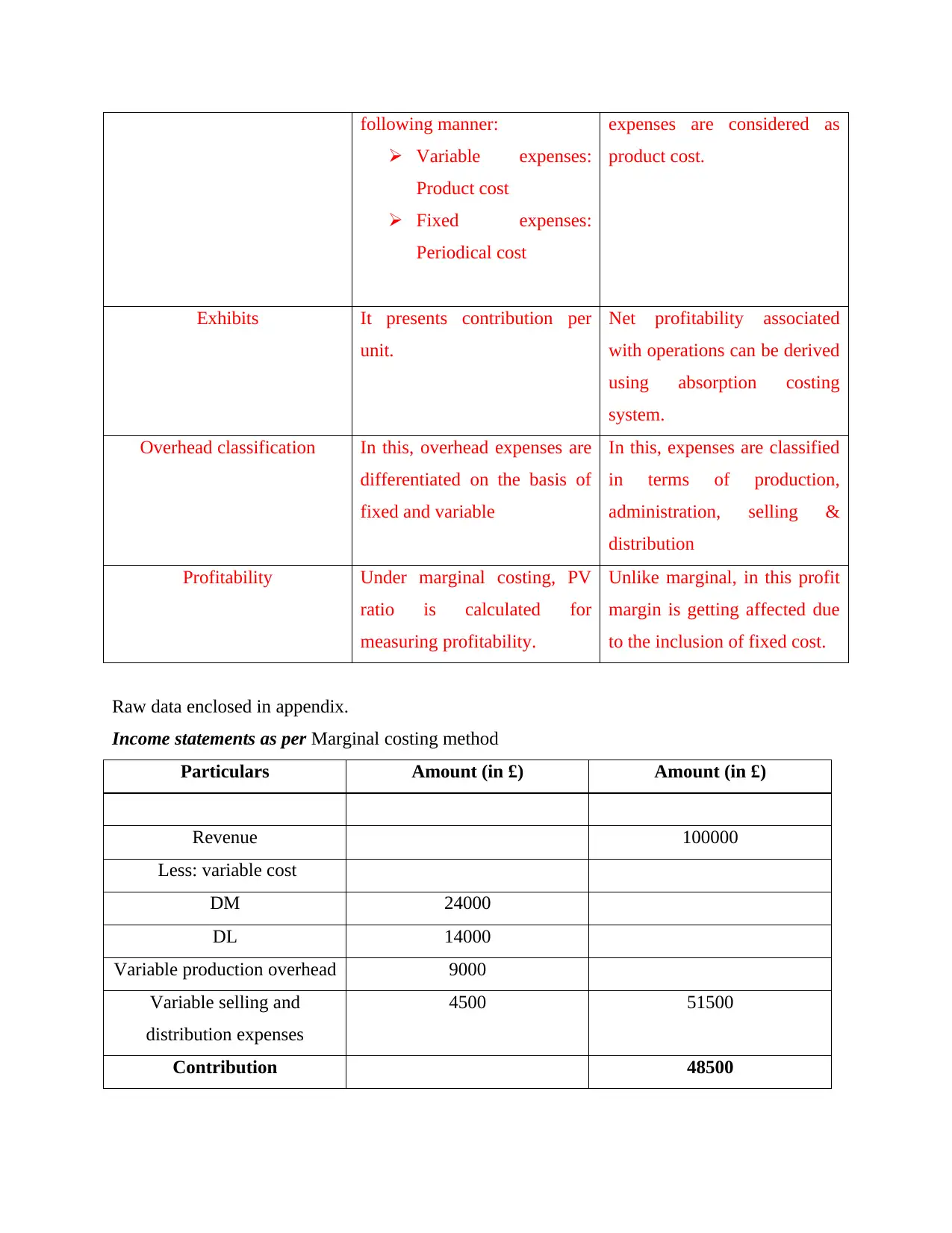

Difference between marginal and absorption costing system is enumerated below:

Basis of difference Marginal costing Absorption costing

Recognition of cost aspect Cost is segregated in the Both fixed and variable

varying demand of the customers at various

price levels so that most suitable price could be

set up. It also provides with the information

regarding the cost and the inventory level for

recommending the prices that improves profit.

It allows CORUS in using its pricing factor as

powerful level of profit that is often

underdeveloped.

Job costing It is a form of assessment that provides

detailing about all kinds of cost that are been

incurred in each job within the manufacturing

process of CORUS. It is counted as the gauge

that determines profitability of the job and

helps the company to make decisions regarding

the future customer or the companies. It

provides an idea about a feasibility of a job so

that duplication of the work could be avoided.

LO2.

P3. Reflecting income statement as per marginal and absorption costing

Marginal costing: It implies for the technique where variable cost is directly associated

with product. On the other side, in this, fixed cost related to both production and non-production

recognized as periodical.

Absorption costing: This method is also known as full costing method in which both fixed

and variable cost absorbed by number of units produced. In this, total production cost is

determined by apportioning expenses in relation to their respective centre.

Difference between marginal and absorption costing system is enumerated below:

Basis of difference Marginal costing Absorption costing

Recognition of cost aspect Cost is segregated in the Both fixed and variable

following manner:

Variable expenses:

Product cost

Fixed expenses:

Periodical cost

expenses are considered as

product cost.

Exhibits It presents contribution per

unit.

Net profitability associated

with operations can be derived

using absorption costing

system.

Overhead classification In this, overhead expenses are

differentiated on the basis of

fixed and variable

In this, expenses are classified

in terms of production,

administration, selling &

distribution

Profitability Under marginal costing, PV

ratio is calculated for

measuring profitability.

Unlike marginal, in this profit

margin is getting affected due

to the inclusion of fixed cost.

Raw data enclosed in appendix.

Income statements as per Marginal costing method

Particulars Amount (in £) Amount (in £)

Revenue 100000

Less: variable cost

DM 24000

DL 14000

Variable production overhead 9000

Variable selling and

distribution expenses

4500 51500

Contribution 48500

Variable expenses:

Product cost

Fixed expenses:

Periodical cost

expenses are considered as

product cost.

Exhibits It presents contribution per

unit.

Net profitability associated

with operations can be derived

using absorption costing

system.

Overhead classification In this, overhead expenses are

differentiated on the basis of

fixed and variable

In this, expenses are classified

in terms of production,

administration, selling &

distribution

Profitability Under marginal costing, PV

ratio is calculated for

measuring profitability.

Unlike marginal, in this profit

margin is getting affected due

to the inclusion of fixed cost.

Raw data enclosed in appendix.

Income statements as per Marginal costing method

Particulars Amount (in £) Amount (in £)

Revenue 100000

Less: variable cost

DM 24000

DL 14000

Variable production overhead 9000

Variable selling and

distribution expenses

4500 51500

Contribution 48500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

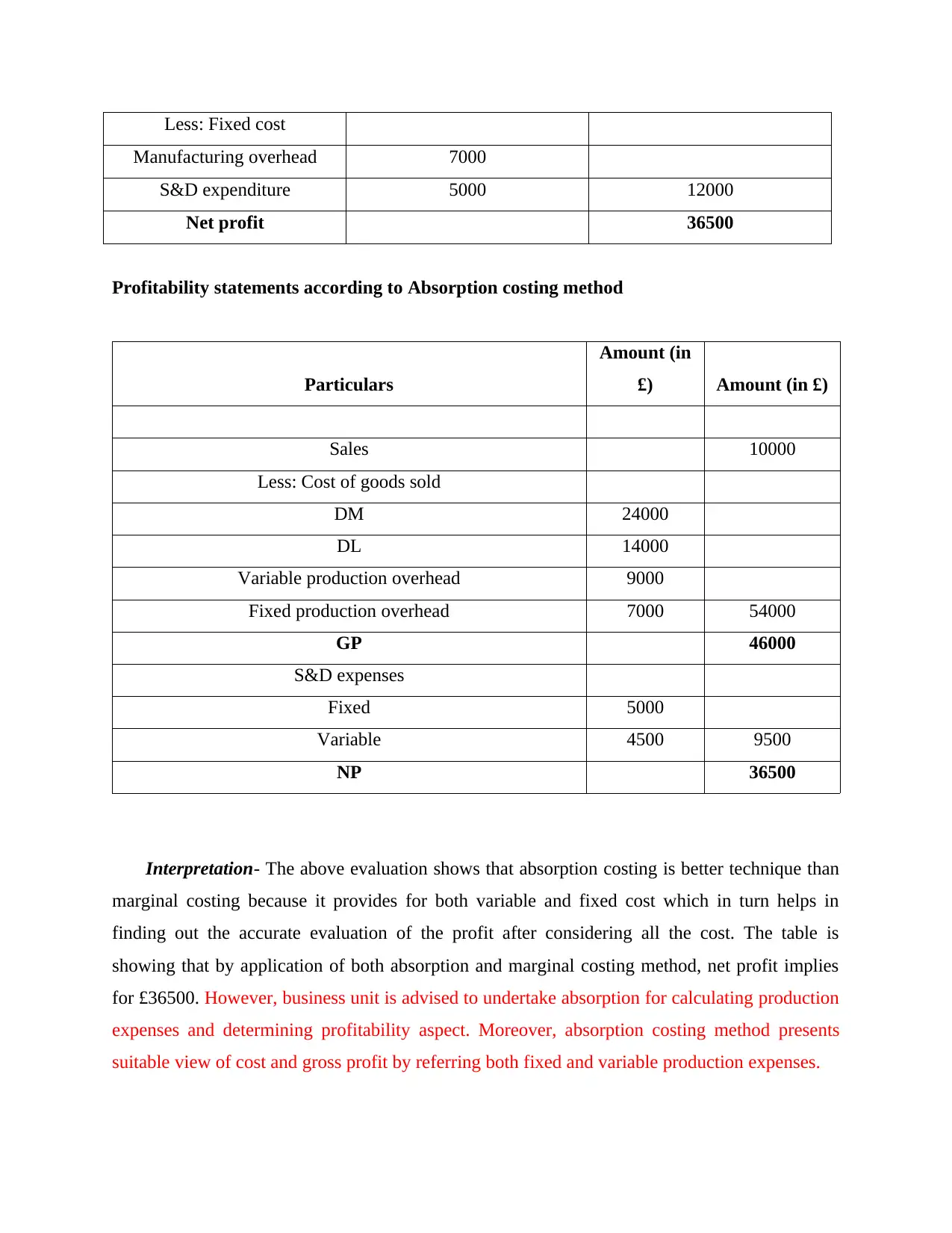

Less: Fixed cost

Manufacturing overhead 7000

S&D expenditure 5000 12000

Net profit 36500

Profitability statements according to Absorption costing method

Particulars

Amount (in

£) Amount (in £)

Sales 10000

Less: Cost of goods sold

DM 24000

DL 14000

Variable production overhead 9000

Fixed production overhead 7000 54000

GP 46000

S&D expenses

Fixed 5000

Variable 4500 9500

NP 36500

Interpretation- The above evaluation shows that absorption costing is better technique than

marginal costing because it provides for both variable and fixed cost which in turn helps in

finding out the accurate evaluation of the profit after considering all the cost. The table is

showing that by application of both absorption and marginal costing method, net profit implies

for £36500. However, business unit is advised to undertake absorption for calculating production

expenses and determining profitability aspect. Moreover, absorption costing method presents

suitable view of cost and gross profit by referring both fixed and variable production expenses.

Manufacturing overhead 7000

S&D expenditure 5000 12000

Net profit 36500

Profitability statements according to Absorption costing method

Particulars

Amount (in

£) Amount (in £)

Sales 10000

Less: Cost of goods sold

DM 24000

DL 14000

Variable production overhead 9000

Fixed production overhead 7000 54000

GP 46000

S&D expenses

Fixed 5000

Variable 4500 9500

NP 36500

Interpretation- The above evaluation shows that absorption costing is better technique than

marginal costing because it provides for both variable and fixed cost which in turn helps in

finding out the accurate evaluation of the profit after considering all the cost. The table is

showing that by application of both absorption and marginal costing method, net profit implies

for £36500. However, business unit is advised to undertake absorption for calculating production

expenses and determining profitability aspect. Moreover, absorption costing method presents

suitable view of cost and gross profit by referring both fixed and variable production expenses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO3.

P 4 Advantages and disadvantages of different types of planning tools in budgetary control

The planning tools are the tools that are used in order to plan for the managing the work

of the company and to manage the accounts of the company. The budget is the estimate of the

future income and expenses which may occur because of running of business (Maas, Schaltegger

and Crutzen, 2016). The budgetary control is the process of setting up of goals relating to

performance and objectives so that the actual work can be compared with the standard work to

find the deviation between both. There are different types of planning tools which are used under

the budgetary control these tools are discussed in the adjoining points connected below-

Zero base budgeting- this is a type of budgeting within which the process of budget making

starts form the initial or zero level. This includes the process of making the budget without using

the last year’s budget or any past record. Here the company starts from the scratch and the

company overlooks every aspect of the business or the different departments and their sources of

income and application of the expenses.

Advantages

This system of budgeting helps the company in systematically evaluate all the

information and facts relating to the income and expenses. This is because of the reason

that this type of budgeting helps the company in analysing all the resources thoroughly

and then allocate the resources to the different departments within the company. Another advantage is that it takes into consideration all the new changes and

development within the working environment. This is because of the reason that this

budget does not take into consideration the past records. Therefore, the latest budget

made is of with new and updated changes.

Disadvantages

Since this type of budget is not based on the past records thus, it might not be appropriate

(Cooper, Ezzamel and Qu, 2017). This is because of the reason that the planner will not

have any clue relating to the past trends then how they will make the budgets. Another major drawback is that it takes a lot of time to prepare this type of budget. This

is because of the reason that the maker of budget has to start from the starting and this

consumes a lot of time in researching and then developing the budget.

P 4 Advantages and disadvantages of different types of planning tools in budgetary control

The planning tools are the tools that are used in order to plan for the managing the work

of the company and to manage the accounts of the company. The budget is the estimate of the

future income and expenses which may occur because of running of business (Maas, Schaltegger

and Crutzen, 2016). The budgetary control is the process of setting up of goals relating to

performance and objectives so that the actual work can be compared with the standard work to

find the deviation between both. There are different types of planning tools which are used under

the budgetary control these tools are discussed in the adjoining points connected below-

Zero base budgeting- this is a type of budgeting within which the process of budget making

starts form the initial or zero level. This includes the process of making the budget without using

the last year’s budget or any past record. Here the company starts from the scratch and the

company overlooks every aspect of the business or the different departments and their sources of

income and application of the expenses.

Advantages

This system of budgeting helps the company in systematically evaluate all the

information and facts relating to the income and expenses. This is because of the reason

that this type of budgeting helps the company in analysing all the resources thoroughly

and then allocate the resources to the different departments within the company. Another advantage is that it takes into consideration all the new changes and

development within the working environment. This is because of the reason that this

budget does not take into consideration the past records. Therefore, the latest budget

made is of with new and updated changes.

Disadvantages

Since this type of budget is not based on the past records thus, it might not be appropriate

(Cooper, Ezzamel and Qu, 2017). This is because of the reason that the planner will not

have any clue relating to the past trends then how they will make the budgets. Another major drawback is that it takes a lot of time to prepare this type of budget. This

is because of the reason that the maker of budget has to start from the starting and this

consumes a lot of time in researching and then developing the budget.

Flexible budgeting- this is a type of budget which is made with flexibility. It is a type of budget

which adjust itself in accordance with the changes taking place in the activity of work or the

volume of the work. this budget is also referred to as the variable budget (Endrikat, Hartmann

and Schreck, 2017). This is because of the reason that in variable budget the cost of anything

varies in accordance with the changes taking place.

Advantages

The major advantage of this type of budget is that it is very easy for the company to

compare the actual budget with the standard budget. This is because of the reason that

these budgets are made with keeping the past records in mind and this helps the company

in setting the standard and then for knowing the profitability the comparison can be done. The other advantage is that this budget is based on the knowledge of the person making

the budget. Therefore, they know well that which principle is applicable in which

situation.

Disadvantage

The major disadvantage is that for making these budgets the company y has to hire some

of the experts who have specialized knowledge and understanding of the fact.

Another disadvantage is that the planning process under this type of budget is that it

needs more of planning for tracking the different expenses which can be incurred within

the business.

Variance analysis: This tool of MA is highly significant which helps in developing

competent strategic and policy framework for the near future. On the basis of this, by doing

comparison of actual expenses in against to the standards firm can assess deviations. Referring

the causes associated with it organization can take corrective measure for improvement.

Advantages:

Highlights inefficient operational areas and gives indication for taking action for the

same.

Facilitates cost control and profit maximization

Disadvantages:

Time-intensive exercise

High deviation derived due to inappropriate standards may result into lack of employee

demotivation

which adjust itself in accordance with the changes taking place in the activity of work or the

volume of the work. this budget is also referred to as the variable budget (Endrikat, Hartmann

and Schreck, 2017). This is because of the reason that in variable budget the cost of anything

varies in accordance with the changes taking place.

Advantages

The major advantage of this type of budget is that it is very easy for the company to

compare the actual budget with the standard budget. This is because of the reason that

these budgets are made with keeping the past records in mind and this helps the company

in setting the standard and then for knowing the profitability the comparison can be done. The other advantage is that this budget is based on the knowledge of the person making

the budget. Therefore, they know well that which principle is applicable in which

situation.

Disadvantage

The major disadvantage is that for making these budgets the company y has to hire some

of the experts who have specialized knowledge and understanding of the fact.

Another disadvantage is that the planning process under this type of budget is that it

needs more of planning for tracking the different expenses which can be incurred within

the business.

Variance analysis: This tool of MA is highly significant which helps in developing

competent strategic and policy framework for the near future. On the basis of this, by doing

comparison of actual expenses in against to the standards firm can assess deviations. Referring

the causes associated with it organization can take corrective measure for improvement.

Advantages:

Highlights inefficient operational areas and gives indication for taking action for the

same.

Facilitates cost control and profit maximization

Disadvantages:

Time-intensive exercise

High deviation derived due to inappropriate standards may result into lack of employee

demotivation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.