Coca-Cola Cost Analysis: A Comprehensive Management Accounting Report

VerifiedAdded on 2023/06/10

|14

|1920

|419

Report

AI Summary

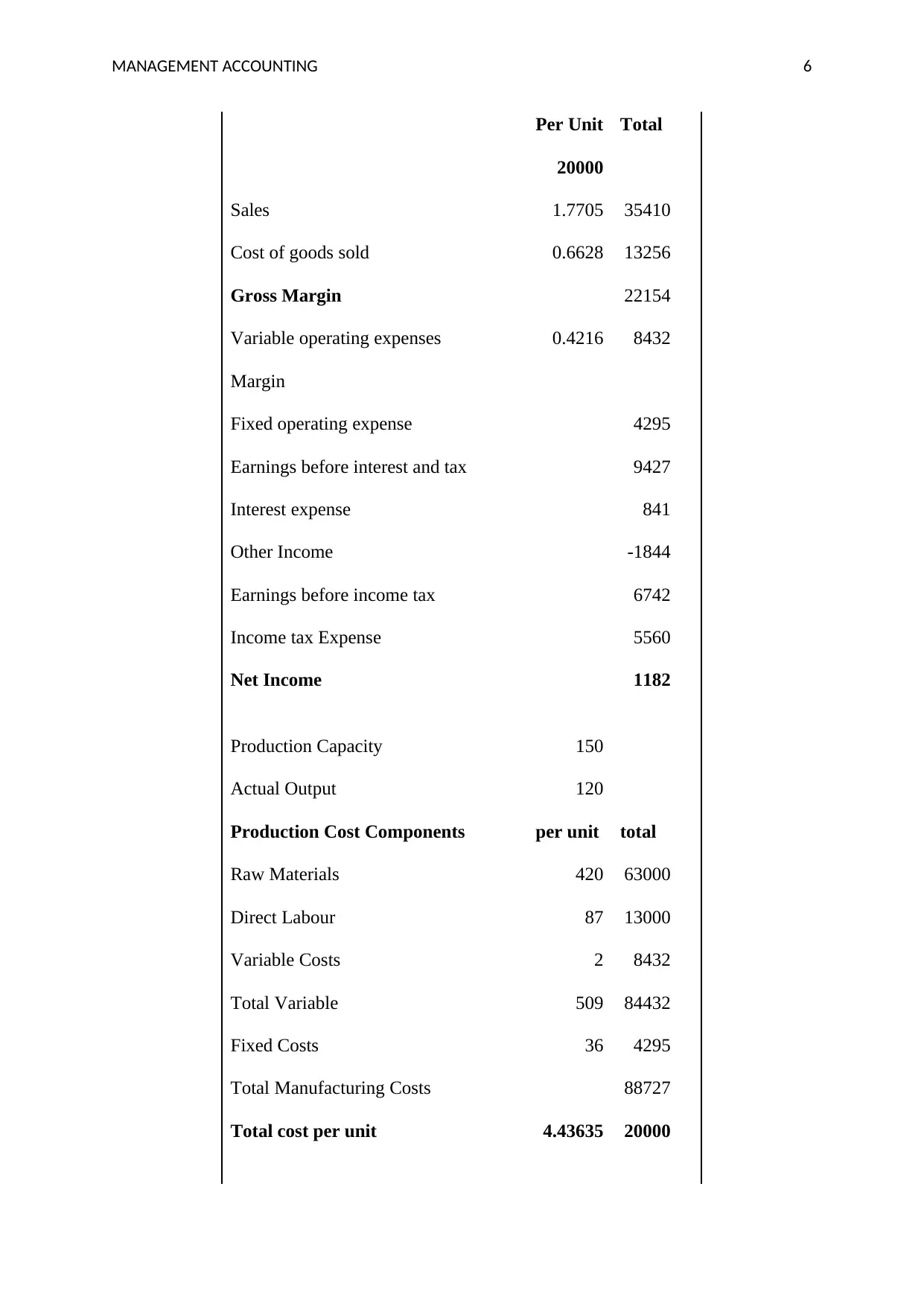

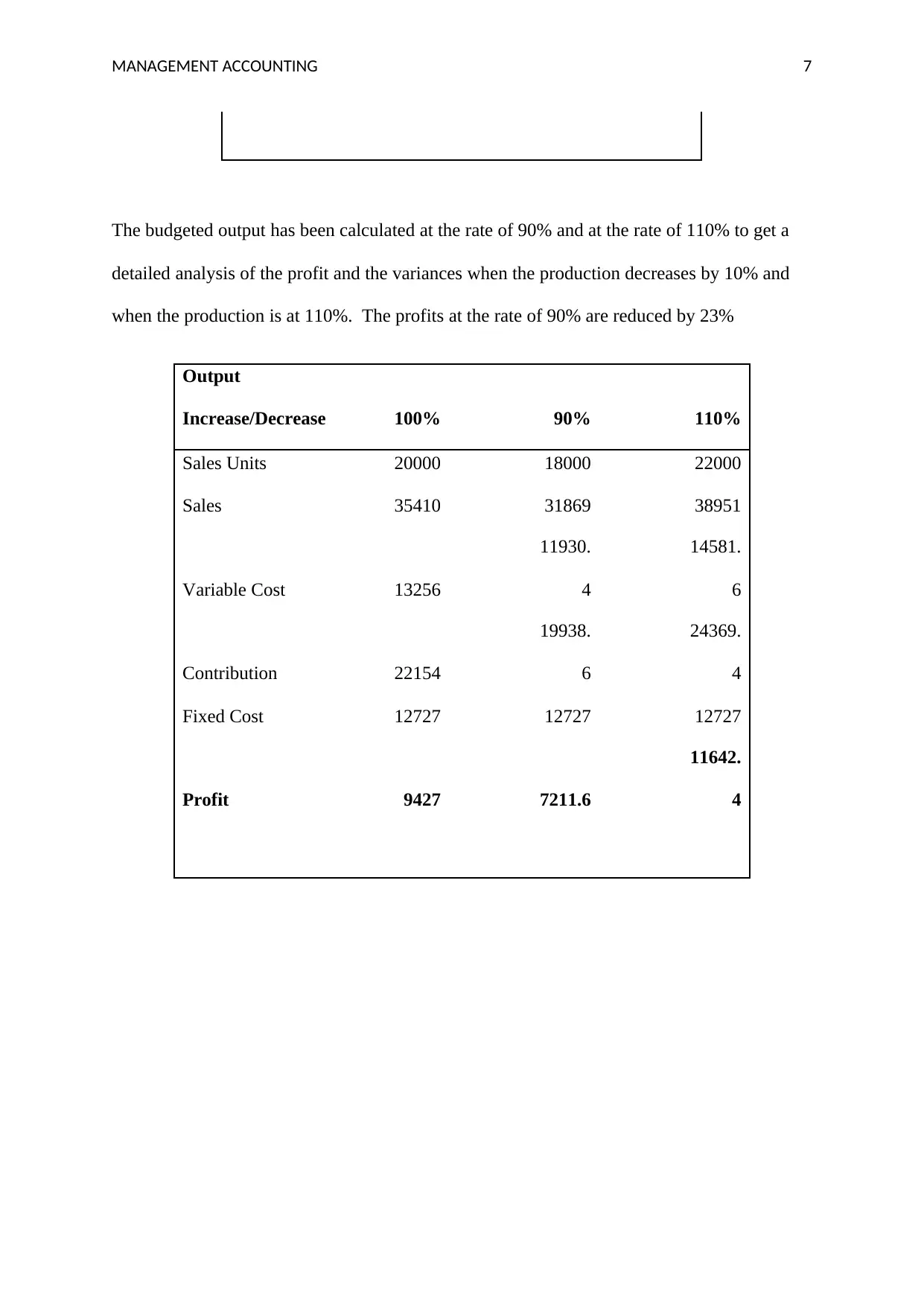

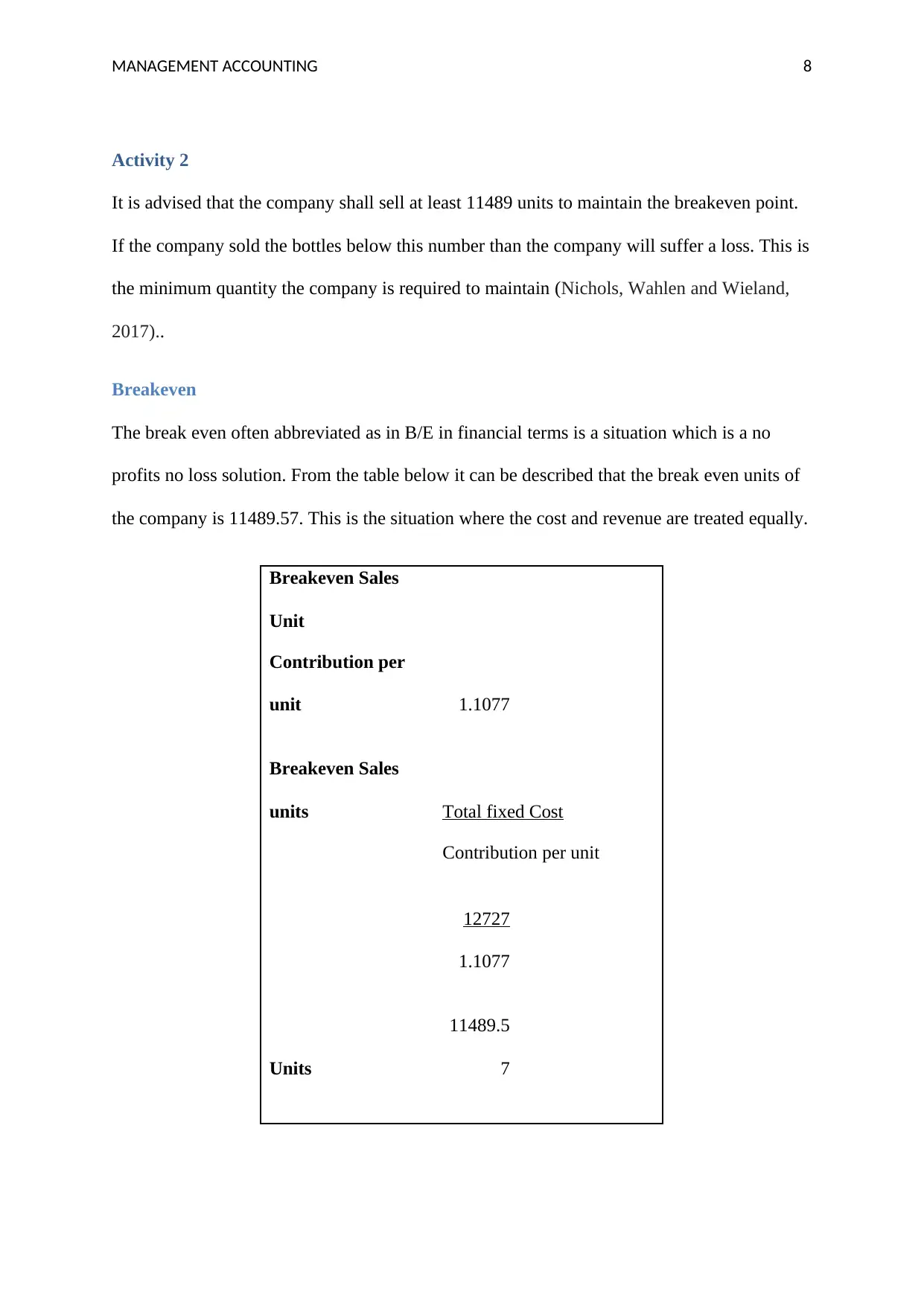

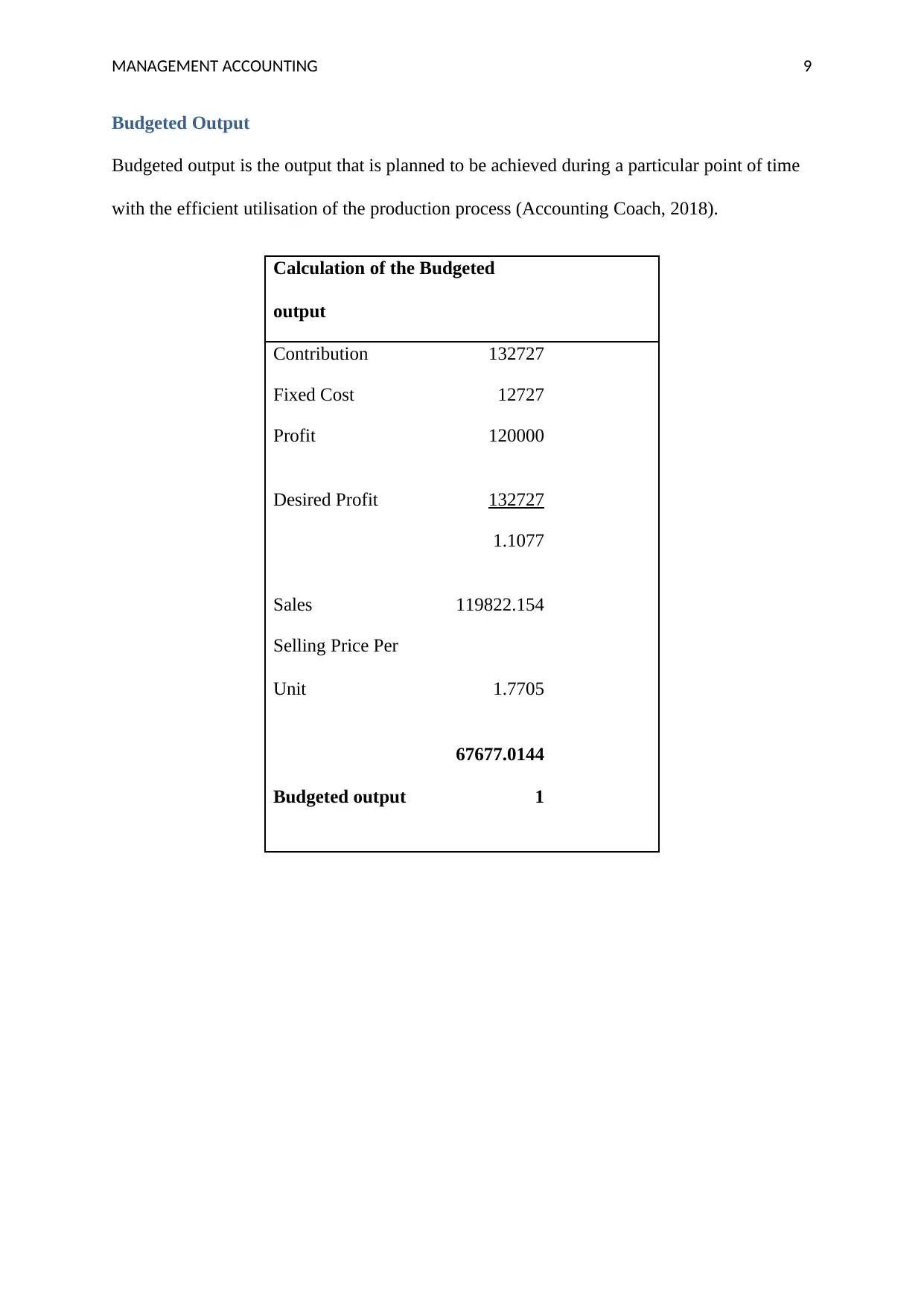

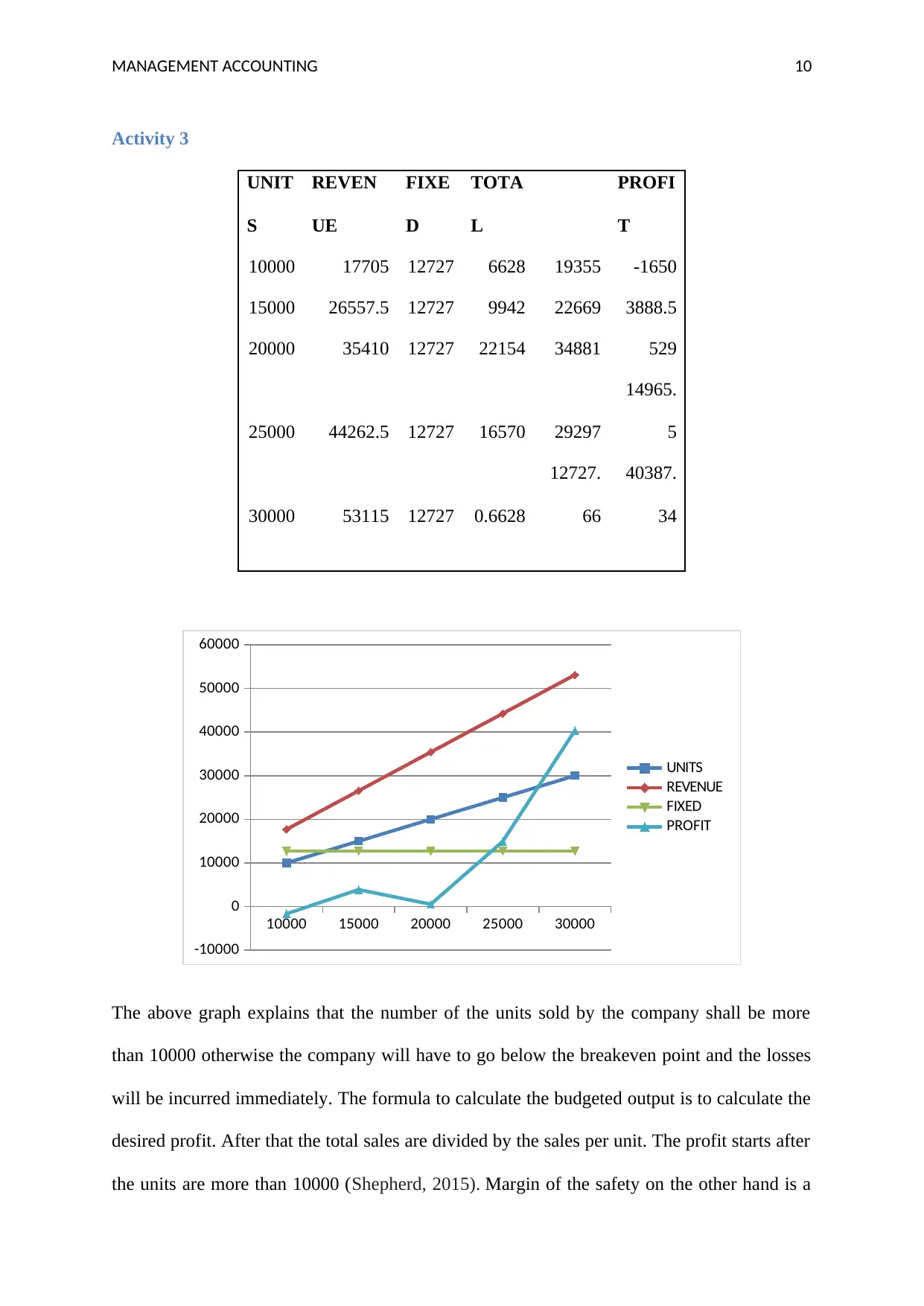

This management accounting report provides a detailed analysis of Coca-Cola's cost structure, including direct, indirect, fixed, variable, semi-variable, and stepped costs. It examines the company's cost per unit, breakeven point, and budgeted output, offering insights into profitability and cost management strategies. The report also calculates the margin of safety and advises on maintaining a budget for sustainable future periods, emphasizing the importance of reducing fixed costs to improve the margin of safety. The analysis includes calculations for various production scenarios and their impact on profit, concluding that the company should sell at least 11,489 units to maintain a breakeven point and achieve the desired profit.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.