Management Accounting Assignment: Cost Analysis and Decisions

VerifiedAdded on 2019/11/12

|7

|1263

|121

Homework Assignment

AI Summary

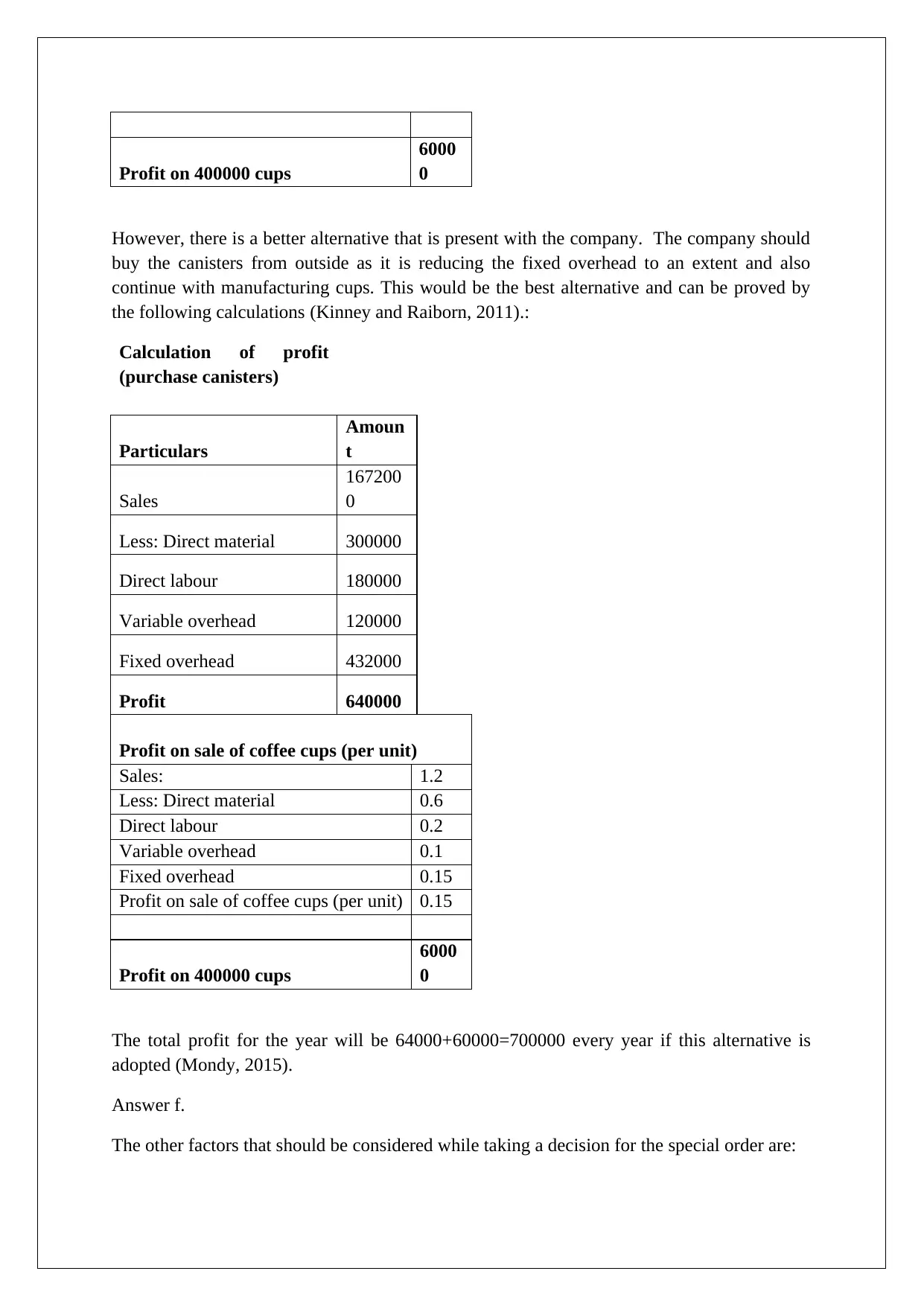

This document presents a comprehensive solution to a management accounting assignment, addressing various aspects of cost analysis and decision-making. The solution begins with calculating the cost per canister, followed by an analysis of the make-or-buy decision, considering both financial and non-financial factors. The analysis includes profit calculations under different scenarios, demonstrating the financial implications of each decision. The solution also explores the acceptance or rejection of a special order, calculating contribution margins to determine the impact on profitability. Furthermore, the assignment considers the importance of non-financial factors, such as customer satisfaction and long-term market competitiveness, in making strategic decisions. Finally, the solution examines the company's profitability under different production and purchasing scenarios, including the potential to sell coffee cups, and concludes with a discussion of additional factors to consider when evaluating a special order, such as product quality, timeliness, and potential impact on goodwill. The document includes references to relevant accounting and financial management literature.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.