King's Own Institute ACC200 Management Accounting Assignment Analysis

VerifiedAdded on 2022/08/27

|12

|2803

|46

Homework Assignment

AI Summary

This assignment solution for ACC200 Introduction to Management Accounting, completed at King's Own Institute, analyzes the product costing of Kona and Malaysian coffee using both traditional and activity-based costing methods. The solution begins by determining the predetermined overhead rate using direct labor cost and then calculates product costs and selling prices. It then develops product costs using activity-based costing and compares the results with the traditional costing system, explaining the differences in cost allocation and overhead assignment. The analysis includes a detailed comparison of the two costing methods, examining cost pools, applied rates, suitability, benefits, cost assignment, and focus. Finally, the assignment provides recommendations for pricing the two products based on the analysis, considering the impact of different costing methods on pricing strategies. The solution demonstrates a clear understanding of management accounting principles, cost allocation, and pricing decisions.

Running head: INTRODUCTION TO MANAGEMENT ACCOUNTING

Introduction to Management Accounting

Name of the Student:

Name of the University:

Author Note

Introduction to Management Accounting

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INTRODUCTION TO MANAGEMENT ACCOUNTING

Table of Contents

1a) Determining the company’s predetermined overhead rate using direct labour cost as the

single customer:.........................................................................................................................2

1b) Determining the product cost and selling price of 1 kg of Kona Coffee and 1kg of

Malaysian coffee:.......................................................................................................................3

2) Developing new product cost using activity-based costing for 1kg of Kona Coffee and 1kg

of Malaysian coffee:...................................................................................................................3

3a) Comparing the cost of the product calculated in requirement 1 and 2, providing

explanation as to why the product cost using the traditional costing system are different from

ABC method:.............................................................................................................................5

3b) Making relevant recommendations for pricing of the two products based on the analysis:8

References and Bibliography:..................................................................................................10

Table of Contents

1a) Determining the company’s predetermined overhead rate using direct labour cost as the

single customer:.........................................................................................................................2

1b) Determining the product cost and selling price of 1 kg of Kona Coffee and 1kg of

Malaysian coffee:.......................................................................................................................3

2) Developing new product cost using activity-based costing for 1kg of Kona Coffee and 1kg

of Malaysian coffee:...................................................................................................................3

3a) Comparing the cost of the product calculated in requirement 1 and 2, providing

explanation as to why the product cost using the traditional costing system are different from

ABC method:.............................................................................................................................5

3b) Making relevant recommendations for pricing of the two products based on the analysis:8

References and Bibliography:..................................................................................................10

2INTRODUCTION TO MANAGEMENT ACCOUNTING

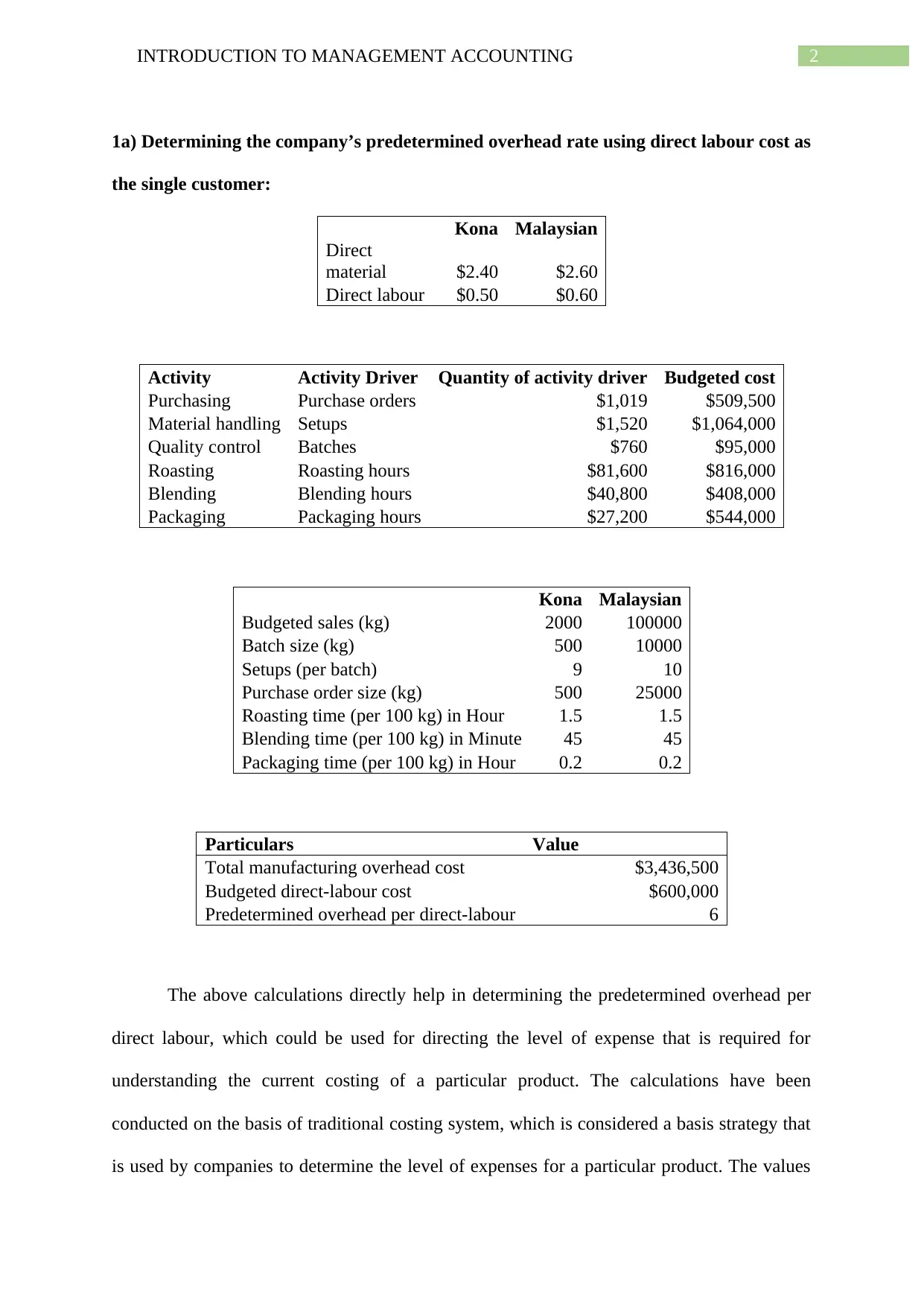

1a) Determining the company’s predetermined overhead rate using direct labour cost as

the single customer:

Kona Malaysian

Direct

material $2.40 $2.60

Direct labour $0.50 $0.60

Activity Activity Driver Quantity of activity driver Budgeted cost

Purchasing Purchase orders $1,019 $509,500

Material handling Setups $1,520 $1,064,000

Quality control Batches $760 $95,000

Roasting Roasting hours $81,600 $816,000

Blending Blending hours $40,800 $408,000

Packaging Packaging hours $27,200 $544,000

Kona Malaysian

Budgeted sales (kg) 2000 100000

Batch size (kg) 500 10000

Setups (per batch) 9 10

Purchase order size (kg) 500 25000

Roasting time (per 100 kg) in Hour 1.5 1.5

Blending time (per 100 kg) in Minute 45 45

Packaging time (per 100 kg) in Hour 0.2 0.2

Particulars Value

Total manufacturing overhead cost $3,436,500

Budgeted direct-labour cost $600,000

Predetermined overhead per direct-labour 6

The above calculations directly help in determining the predetermined overhead per

direct labour, which could be used for directing the level of expense that is required for

understanding the current costing of a particular product. The calculations have been

conducted on the basis of traditional costing system, which is considered a basis strategy that

is used by companies to determine the level of expenses for a particular product. The values

1a) Determining the company’s predetermined overhead rate using direct labour cost as

the single customer:

Kona Malaysian

Direct

material $2.40 $2.60

Direct labour $0.50 $0.60

Activity Activity Driver Quantity of activity driver Budgeted cost

Purchasing Purchase orders $1,019 $509,500

Material handling Setups $1,520 $1,064,000

Quality control Batches $760 $95,000

Roasting Roasting hours $81,600 $816,000

Blending Blending hours $40,800 $408,000

Packaging Packaging hours $27,200 $544,000

Kona Malaysian

Budgeted sales (kg) 2000 100000

Batch size (kg) 500 10000

Setups (per batch) 9 10

Purchase order size (kg) 500 25000

Roasting time (per 100 kg) in Hour 1.5 1.5

Blending time (per 100 kg) in Minute 45 45

Packaging time (per 100 kg) in Hour 0.2 0.2

Particulars Value

Total manufacturing overhead cost $3,436,500

Budgeted direct-labour cost $600,000

Predetermined overhead per direct-labour 6

The above calculations directly help in determining the predetermined overhead per

direct labour, which could be used for directing the level of expense that is required for

understanding the current costing of a particular product. The calculations have been

conducted on the basis of traditional costing system, which is considered a basis strategy that

is used by companies to determine the level of expenses for a particular product. The values

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INTRODUCTION TO MANAGEMENT ACCOUNTING

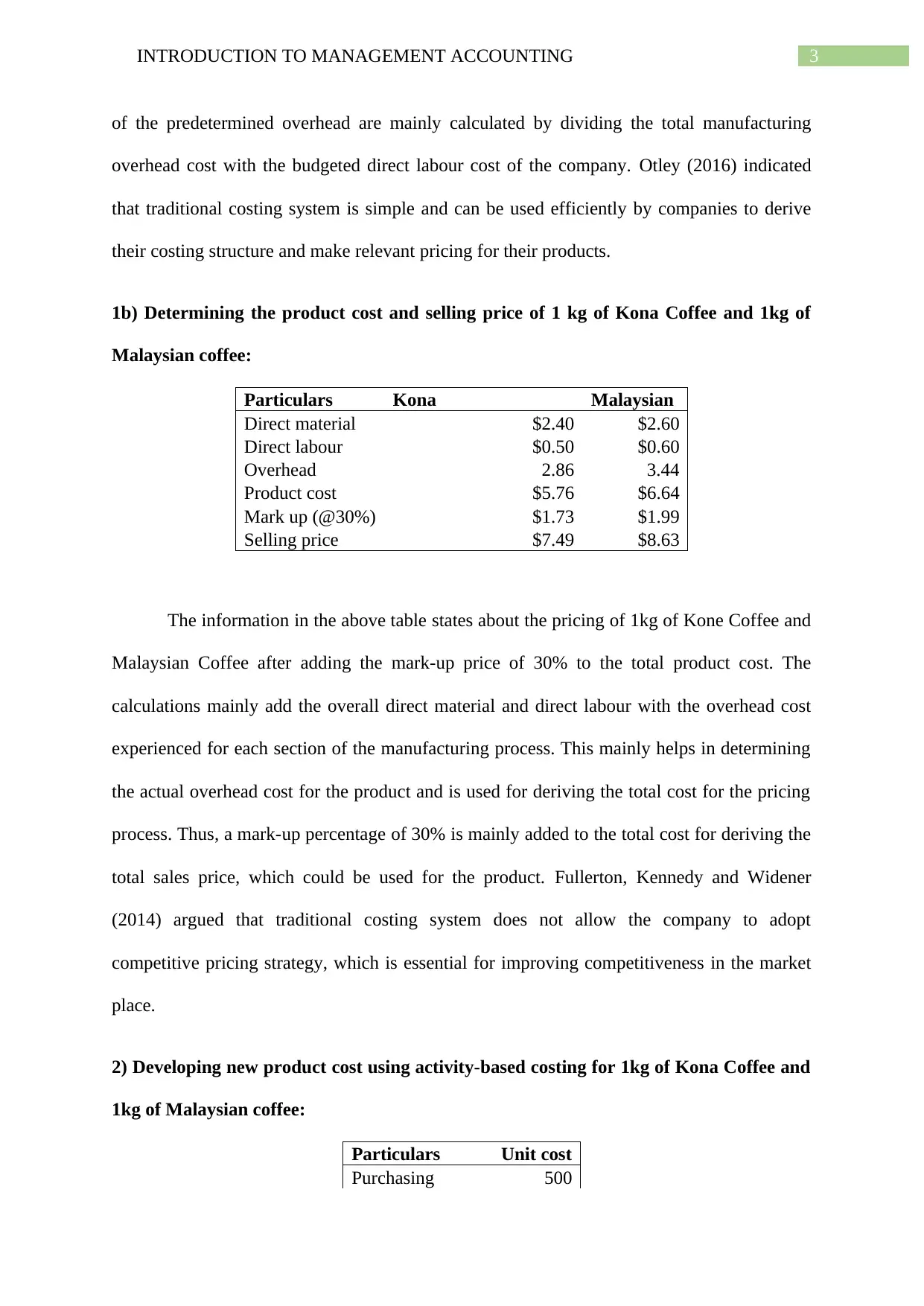

of the predetermined overhead are mainly calculated by dividing the total manufacturing

overhead cost with the budgeted direct labour cost of the company. Otley (2016) indicated

that traditional costing system is simple and can be used efficiently by companies to derive

their costing structure and make relevant pricing for their products.

1b) Determining the product cost and selling price of 1 kg of Kona Coffee and 1kg of

Malaysian coffee:

Particulars Kona Malaysian

Direct material $2.40 $2.60

Direct labour $0.50 $0.60

Overhead 2.86 3.44

Product cost $5.76 $6.64

Mark up (@30%) $1.73 $1.99

Selling price $7.49 $8.63

The information in the above table states about the pricing of 1kg of Kone Coffee and

Malaysian Coffee after adding the mark-up price of 30% to the total product cost. The

calculations mainly add the overall direct material and direct labour with the overhead cost

experienced for each section of the manufacturing process. This mainly helps in determining

the actual overhead cost for the product and is used for deriving the total cost for the pricing

process. Thus, a mark-up percentage of 30% is mainly added to the total cost for deriving the

total sales price, which could be used for the product. Fullerton, Kennedy and Widener

(2014) argued that traditional costing system does not allow the company to adopt

competitive pricing strategy, which is essential for improving competitiveness in the market

place.

2) Developing new product cost using activity-based costing for 1kg of Kona Coffee and

1kg of Malaysian coffee:

Particulars Unit cost

Purchasing 500

of the predetermined overhead are mainly calculated by dividing the total manufacturing

overhead cost with the budgeted direct labour cost of the company. Otley (2016) indicated

that traditional costing system is simple and can be used efficiently by companies to derive

their costing structure and make relevant pricing for their products.

1b) Determining the product cost and selling price of 1 kg of Kona Coffee and 1kg of

Malaysian coffee:

Particulars Kona Malaysian

Direct material $2.40 $2.60

Direct labour $0.50 $0.60

Overhead 2.86 3.44

Product cost $5.76 $6.64

Mark up (@30%) $1.73 $1.99

Selling price $7.49 $8.63

The information in the above table states about the pricing of 1kg of Kone Coffee and

Malaysian Coffee after adding the mark-up price of 30% to the total product cost. The

calculations mainly add the overall direct material and direct labour with the overhead cost

experienced for each section of the manufacturing process. This mainly helps in determining

the actual overhead cost for the product and is used for deriving the total cost for the pricing

process. Thus, a mark-up percentage of 30% is mainly added to the total cost for deriving the

total sales price, which could be used for the product. Fullerton, Kennedy and Widener

(2014) argued that traditional costing system does not allow the company to adopt

competitive pricing strategy, which is essential for improving competitiveness in the market

place.

2) Developing new product cost using activity-based costing for 1kg of Kona Coffee and

1kg of Malaysian coffee:

Particulars Unit cost

Purchasing 500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INTRODUCTION TO MANAGEMENT ACCOUNTING

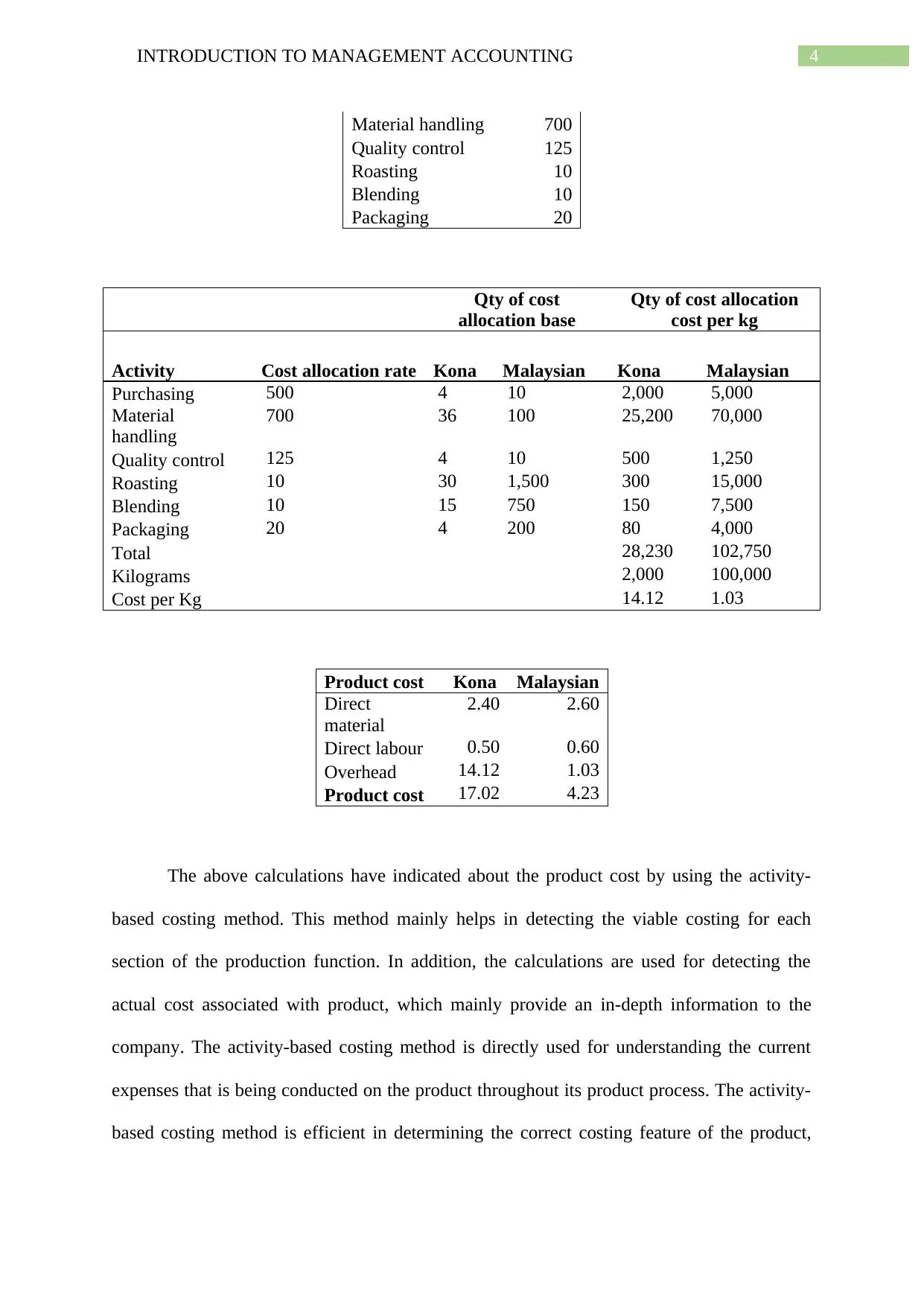

Material handling 700

Quality control 125

Roasting 10

Blending 10

Packaging 20

Qty of cost

allocation base

Qty of cost allocation

cost per kg

Activity Cost allocation rate Kona Malaysian Kona Malaysian

Purchasing 500 4 10 2,000 5,000

Material

handling

700 36 100 25,200 70,000

Quality control 125 4 10 500 1,250

Roasting 10 30 1,500 300 15,000

Blending 10 15 750 150 7,500

Packaging 20 4 200 80 4,000

Total 28,230 102,750

Kilograms 2,000 100,000

Cost per Kg 14.12 1.03

Product cost Kona Malaysian

Direct

material

2.40 2.60

Direct labour 0.50 0.60

Overhead 14.12 1.03

Product cost 17.02 4.23

The above calculations have indicated about the product cost by using the activity-

based costing method. This method mainly helps in detecting the viable costing for each

section of the production function. In addition, the calculations are used for detecting the

actual cost associated with product, which mainly provide an in-depth information to the

company. The activity-based costing method is directly used for understanding the current

expenses that is being conducted on the product throughout its product process. The activity-

based costing method is efficient in determining the correct costing feature of the product,

Material handling 700

Quality control 125

Roasting 10

Blending 10

Packaging 20

Qty of cost

allocation base

Qty of cost allocation

cost per kg

Activity Cost allocation rate Kona Malaysian Kona Malaysian

Purchasing 500 4 10 2,000 5,000

Material

handling

700 36 100 25,200 70,000

Quality control 125 4 10 500 1,250

Roasting 10 30 1,500 300 15,000

Blending 10 15 750 150 7,500

Packaging 20 4 200 80 4,000

Total 28,230 102,750

Kilograms 2,000 100,000

Cost per Kg 14.12 1.03

Product cost Kona Malaysian

Direct

material

2.40 2.60

Direct labour 0.50 0.60

Overhead 14.12 1.03

Product cost 17.02 4.23

The above calculations have indicated about the product cost by using the activity-

based costing method. This method mainly helps in detecting the viable costing for each

section of the production function. In addition, the calculations are used for detecting the

actual cost associated with product, which mainly provide an in-depth information to the

company. The activity-based costing method is directly used for understanding the current

expenses that is being conducted on the product throughout its product process. The activity-

based costing method is efficient in determining the correct costing feature of the product,

5INTRODUCTION TO MANAGEMENT ACCOUNTING

which allow the management to make relevant pricing decisions and increase their

competitive edge against competitors in the market (Maas, Schaltegger and Crutzen 2016).

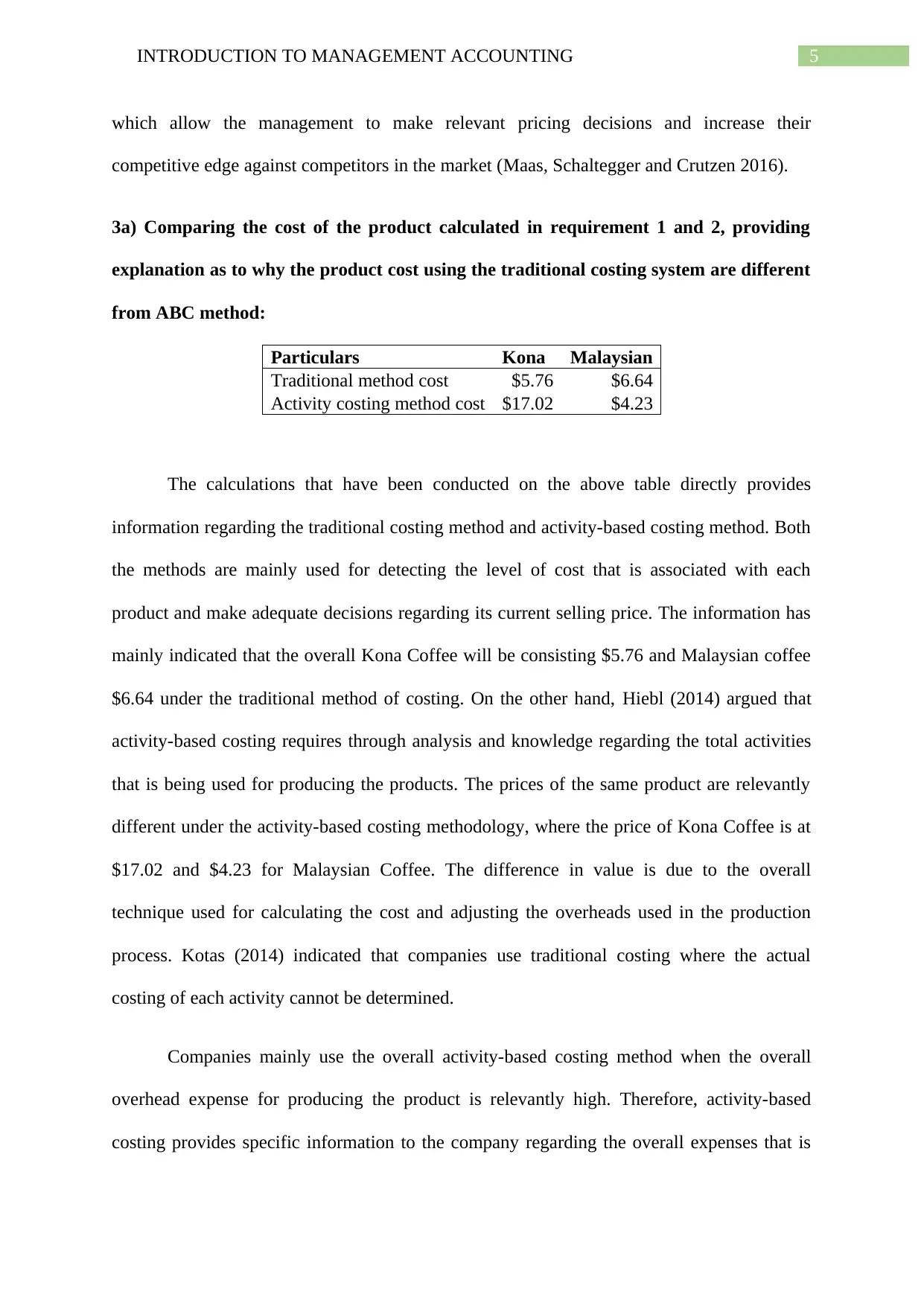

3a) Comparing the cost of the product calculated in requirement 1 and 2, providing

explanation as to why the product cost using the traditional costing system are different

from ABC method:

Particulars Kona Malaysian

Traditional method cost $5.76 $6.64

Activity costing method cost $17.02 $4.23

The calculations that have been conducted on the above table directly provides

information regarding the traditional costing method and activity-based costing method. Both

the methods are mainly used for detecting the level of cost that is associated with each

product and make adequate decisions regarding its current selling price. The information has

mainly indicated that the overall Kona Coffee will be consisting $5.76 and Malaysian coffee

$6.64 under the traditional method of costing. On the other hand, Hiebl (2014) argued that

activity-based costing requires through analysis and knowledge regarding the total activities

that is being used for producing the products. The prices of the same product are relevantly

different under the activity-based costing methodology, where the price of Kona Coffee is at

$17.02 and $4.23 for Malaysian Coffee. The difference in value is due to the overall

technique used for calculating the cost and adjusting the overheads used in the production

process. Kotas (2014) indicated that companies use traditional costing where the actual

costing of each activity cannot be determined.

Companies mainly use the overall activity-based costing method when the overall

overhead expense for producing the product is relevantly high. Therefore, activity-based

costing provides specific information to the company regarding the overall expenses that is

which allow the management to make relevant pricing decisions and increase their

competitive edge against competitors in the market (Maas, Schaltegger and Crutzen 2016).

3a) Comparing the cost of the product calculated in requirement 1 and 2, providing

explanation as to why the product cost using the traditional costing system are different

from ABC method:

Particulars Kona Malaysian

Traditional method cost $5.76 $6.64

Activity costing method cost $17.02 $4.23

The calculations that have been conducted on the above table directly provides

information regarding the traditional costing method and activity-based costing method. Both

the methods are mainly used for detecting the level of cost that is associated with each

product and make adequate decisions regarding its current selling price. The information has

mainly indicated that the overall Kona Coffee will be consisting $5.76 and Malaysian coffee

$6.64 under the traditional method of costing. On the other hand, Hiebl (2014) argued that

activity-based costing requires through analysis and knowledge regarding the total activities

that is being used for producing the products. The prices of the same product are relevantly

different under the activity-based costing methodology, where the price of Kona Coffee is at

$17.02 and $4.23 for Malaysian Coffee. The difference in value is due to the overall

technique used for calculating the cost and adjusting the overheads used in the production

process. Kotas (2014) indicated that companies use traditional costing where the actual

costing of each activity cannot be determined.

Companies mainly use the overall activity-based costing method when the overall

overhead expense for producing the product is relevantly high. Therefore, activity-based

costing provides specific information to the company regarding the overall expenses that is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INTRODUCTION TO MANAGEMENT ACCOUNTING

being associated with each of the product. The elaboration on the difference between the

overall traditional costing method and activity-based costing method are depicted as follows.

Cost pools:

One of the major differences between traditional costing method and activity-based

costing method is the cost pools, which is used for calculating the overall expenses associated

with each product. The traditional method would mainly utilise one or limited number of cost

pools for determining the expenses incurred for producing a particular product. The cost

pools are not distinguished in different segments under the traditional costing method. On the

other hand, the activity-based costing method uses many forms of cost pools for detecting the

accurate level of costing for the product. The combination of different cost pools associated

with the overhead cost would eventually help in detecting the actual level for the product.

Hence, many cost pools are used in ABC method in contrast to traditional costing method

(Lavia and Hiebl 2014).

Applied rate:

The second difference is between the two method is the applied rate system, which is

used for assigning the relevant level of cost associated with the production process. The

traditional costing system us uses volume-based cost drivers, as it measures the total level of

cost for the products produced by the company. Hence, the measure would mainly neglect the

factor of different activities and non-financial measures that is used for producing the

productivity. Hence, the activity-based costing method focuses only of activity and non-

financial factors while deriving the overall cost for the product. This information would

mainly help the company understand the actual lengths taken by the production process to

produce the overall product (Renz and Herman 2016).

being associated with each of the product. The elaboration on the difference between the

overall traditional costing method and activity-based costing method are depicted as follows.

Cost pools:

One of the major differences between traditional costing method and activity-based

costing method is the cost pools, which is used for calculating the overall expenses associated

with each product. The traditional method would mainly utilise one or limited number of cost

pools for determining the expenses incurred for producing a particular product. The cost

pools are not distinguished in different segments under the traditional costing method. On the

other hand, the activity-based costing method uses many forms of cost pools for detecting the

accurate level of costing for the product. The combination of different cost pools associated

with the overhead cost would eventually help in detecting the actual level for the product.

Hence, many cost pools are used in ABC method in contrast to traditional costing method

(Lavia and Hiebl 2014).

Applied rate:

The second difference is between the two method is the applied rate system, which is

used for assigning the relevant level of cost associated with the production process. The

traditional costing system us uses volume-based cost drivers, as it measures the total level of

cost for the products produced by the company. Hence, the measure would mainly neglect the

factor of different activities and non-financial measures that is used for producing the

productivity. Hence, the activity-based costing method focuses only of activity and non-

financial factors while deriving the overall cost for the product. This information would

mainly help the company understand the actual lengths taken by the production process to

produce the overall product (Renz and Herman 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTRODUCTION TO MANAGEMENT ACCOUNTING

Costing method Suited:

Both the method is mainly suited for different companies having different

requirements for their production process. Consequently, traditional costing method would

eventually help the organization that is most suited to labour intensive and low overhead

companies, as it will not have a negative impact on the overall costing measures while

detecting the total cost for the product. However, the companies use activity based costing

only when their operations fall under the following categories capital intensive, product

diverse, variation in production runs, high overhead costing, and diverse operating activities

directly utilize activity based costing system. Therefore, organizations need to identify the

relevant level of operations that needs to be conducted in the production process. This would

eventually help in determining whether the overall costing method can be used for detecting

the actual cost for the product (Cooper, Ezzamel and Qu 2017).

Benefits:

The difference between traditional costing system and activity based costing system

can be for the evaluated on the basis of benefits that is provided to the organisation. The

traditional costing system direct is considered to be simple and inexpensive which provides

and ultra-benefit to the organisation by reducing the level of expenses in code in maintaining

overall costing system. However, the benefits provided by activity based costing are more

attractive to an organisation as it helps in accurately detecting the product cost, possible

elimination of non-value added activities and determining the appropriate competitive pricing

structure that could be used to improve their overall competitiveness in the market. Hence,

the operations of the organisation determine the relevant benefits it could provide to the

management (Tucker and Lowe 2014).

Cost assignment:

Costing method Suited:

Both the method is mainly suited for different companies having different

requirements for their production process. Consequently, traditional costing method would

eventually help the organization that is most suited to labour intensive and low overhead

companies, as it will not have a negative impact on the overall costing measures while

detecting the total cost for the product. However, the companies use activity based costing

only when their operations fall under the following categories capital intensive, product

diverse, variation in production runs, high overhead costing, and diverse operating activities

directly utilize activity based costing system. Therefore, organizations need to identify the

relevant level of operations that needs to be conducted in the production process. This would

eventually help in determining whether the overall costing method can be used for detecting

the actual cost for the product (Cooper, Ezzamel and Qu 2017).

Benefits:

The difference between traditional costing system and activity based costing system

can be for the evaluated on the basis of benefits that is provided to the organisation. The

traditional costing system direct is considered to be simple and inexpensive which provides

and ultra-benefit to the organisation by reducing the level of expenses in code in maintaining

overall costing system. However, the benefits provided by activity based costing are more

attractive to an organisation as it helps in accurately detecting the product cost, possible

elimination of non-value added activities and determining the appropriate competitive pricing

structure that could be used to improve their overall competitiveness in the market. Hence,

the operations of the organisation determine the relevant benefits it could provide to the

management (Tucker and Lowe 2014).

Cost assignment:

8INTRODUCTION TO MANAGEMENT ACCOUNTING

Cost assignment method is segregated in two distinctive conditions that can be used

by the organisation to suit their costing needs. The traditional costing system directly

allocates the overhead cost first to department and second to the product or services, that is

being produced by the organisation. This type of allocation of overhead cost directly helps in

segregating the expenses without determining any kind of activity leading towards the overall

production process. However, with the help of activity based costing system companies are

able to assign its overhead cost first to the activity cost pools that is associated with the

production process and after that the product of services are included. This type of costing

method directly helps in determining the accurate level of expenses that is associated with the

production process of an organisation (Schaltegger and Burritt 2017).

Focus:

The focus of the costing system is also an essential component, which distinguishes

between traditional costing system and activity based costing system. The traditional costing

system relatively focuses on managing cost on functional departments or responsibility

centers, which could eventually help in detecting the costing structure of the organization.

Hence, the activity based costing focuses on activities processes and solutions a cross

functional problems of the production system. This would eventually help in understanding

the actual values associated with the production process (Quattrone 2016).

3b) Making relevant recommendations for pricing of the two products based on the

analysis:

Particulars Kona Malaysian

Traditional method price $7.49 $8.63

Traditional method cost $5.76 $6.64

Activity costing method price

$22.1

2 $5.50

Activity costing method cost

$17.0

2 $4.23

Cost assignment method is segregated in two distinctive conditions that can be used

by the organisation to suit their costing needs. The traditional costing system directly

allocates the overhead cost first to department and second to the product or services, that is

being produced by the organisation. This type of allocation of overhead cost directly helps in

segregating the expenses without determining any kind of activity leading towards the overall

production process. However, with the help of activity based costing system companies are

able to assign its overhead cost first to the activity cost pools that is associated with the

production process and after that the product of services are included. This type of costing

method directly helps in determining the accurate level of expenses that is associated with the

production process of an organisation (Schaltegger and Burritt 2017).

Focus:

The focus of the costing system is also an essential component, which distinguishes

between traditional costing system and activity based costing system. The traditional costing

system relatively focuses on managing cost on functional departments or responsibility

centers, which could eventually help in detecting the costing structure of the organization.

Hence, the activity based costing focuses on activities processes and solutions a cross

functional problems of the production system. This would eventually help in understanding

the actual values associated with the production process (Quattrone 2016).

3b) Making relevant recommendations for pricing of the two products based on the

analysis:

Particulars Kona Malaysian

Traditional method price $7.49 $8.63

Traditional method cost $5.76 $6.64

Activity costing method price

$22.1

2 $5.50

Activity costing method cost

$17.0

2 $4.23

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INTRODUCTION TO MANAGEMENT ACCOUNTING

The above table portrays the information regarding the traditional costing method and

activity-based costing method, which could help in determining the accurate level of prices

for the similar production process. The price comparisons between the traditional costing

activity-based costing method is relevantly different, which mainly alters the perception of

the company regarding their current cost structure and pricing strategy. Therefore, with the

help of traditional costing method only normal costing measures are taken into consideration,

which does not relate to the actual activity used for producing the activity. On the other hand,

the overall activity-based costing measure has indicated a cost price, which is higher for

Kona, while lower for Malaysian. This input would mainly help the company understand the

different level of activities that is being conducted for the production of coffee under different

process. Thus, activity-based costing measure is providing higher input regarding the actual

costing of the product at the end of the process, which is essential for making pricing

decisions for the management. Thus, pricing of the both the products needs to be conducted

on the basis of activity costing method, as it is the correct method for deriving the actual cost

for the product.

The above table portrays the information regarding the traditional costing method and

activity-based costing method, which could help in determining the accurate level of prices

for the similar production process. The price comparisons between the traditional costing

activity-based costing method is relevantly different, which mainly alters the perception of

the company regarding their current cost structure and pricing strategy. Therefore, with the

help of traditional costing method only normal costing measures are taken into consideration,

which does not relate to the actual activity used for producing the activity. On the other hand,

the overall activity-based costing measure has indicated a cost price, which is higher for

Kona, while lower for Malaysian. This input would mainly help the company understand the

different level of activities that is being conducted for the production of coffee under different

process. Thus, activity-based costing measure is providing higher input regarding the actual

costing of the product at the end of the process, which is essential for making pricing

decisions for the management. Thus, pricing of the both the products needs to be conducted

on the basis of activity costing method, as it is the correct method for deriving the actual cost

for the product.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INTRODUCTION TO MANAGEMENT ACCOUNTING

References and Bibliography:

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research, 31, pp.1-9.

Cooper, D.J., Ezzamel, M. and Qu, S.Q., 2017. Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research, 34(2), pp.991-1025.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), pp.414-428.

Hiebl, M.R., 2014. Upper echelons theory in management accounting and control

research. Journal of Management Control, 24(3), pp.223-240.

Kokubu, K. and Kitada, H., 2015. Material flow cost accounting and existing management

perspectives. Journal of Cleaner Production, 108, pp.1279-1288.

Kotas, R., 2014. Management accounting for hotels and restaurants. Routledge.

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and medium-sized

enterprises: current knowledge and avenues for further research. Journal of Management

Accounting Research, 27(1), pp.81-119.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, pp.237-248.

Nitzl, C., 2016. The use of partial least squares structural equation modelling (PLS-SEM) in

management accounting research: Directions for future theory development. Journal of

Accounting Literature, 37, pp.19-35.

References and Bibliography:

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research, 31, pp.1-9.

Cooper, D.J., Ezzamel, M. and Qu, S.Q., 2017. Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research, 34(2), pp.991-1025.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), pp.414-428.

Hiebl, M.R., 2014. Upper echelons theory in management accounting and control

research. Journal of Management Control, 24(3), pp.223-240.

Kokubu, K. and Kitada, H., 2015. Material flow cost accounting and existing management

perspectives. Journal of Cleaner Production, 108, pp.1279-1288.

Kotas, R., 2014. Management accounting for hotels and restaurants. Routledge.

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and medium-sized

enterprises: current knowledge and avenues for further research. Journal of Management

Accounting Research, 27(1), pp.81-119.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, pp.237-248.

Nitzl, C., 2016. The use of partial least squares structural equation modelling (PLS-SEM) in

management accounting research: Directions for future theory development. Journal of

Accounting Literature, 37, pp.19-35.

11INTRODUCTION TO MANAGEMENT ACCOUNTING

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research, 31, pp.118-122.

Renz, D.O. and Herman, R.D. eds., 2016. The Jossey-Bass handbook of nonprofit leadership

and management. John Wiley & Sons.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Senftlechner, D. and Hiebl, M.R., 2015. Management accounting and management control in

family businesses: Past accomplishments and future opportunities. Journal of Accounting &

Organizational Change, 11(4), pp.573-606.

Shields, M.D., 2015. Established management accounting knowledge. Journal of

Management Accounting Research, 27(1), pp.123-132.

Tucker, B.P. and Lowe, A.D., 2014. Practitioners are from Mars; academics are from

Venus?: An investigation of the research-practice gap in management

accounting. Accounting, Auditing & Accountability Journal, 27(3), pp.394-425.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research, 31, pp.118-122.

Renz, D.O. and Herman, R.D. eds., 2016. The Jossey-Bass handbook of nonprofit leadership

and management. John Wiley & Sons.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Senftlechner, D. and Hiebl, M.R., 2015. Management accounting and management control in

family businesses: Past accomplishments and future opportunities. Journal of Accounting &

Organizational Change, 11(4), pp.573-606.

Shields, M.D., 2015. Established management accounting knowledge. Journal of

Management Accounting Research, 27(1), pp.123-132.

Tucker, B.P. and Lowe, A.D., 2014. Practitioners are from Mars; academics are from

Venus?: An investigation of the research-practice gap in management

accounting. Accounting, Auditing & Accountability Journal, 27(3), pp.394-425.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.