Management Accounting: Cost Analysis, CVP, and Decision Making

VerifiedAdded on 2023/06/18

|10

|1199

|185

Homework Assignment

AI Summary

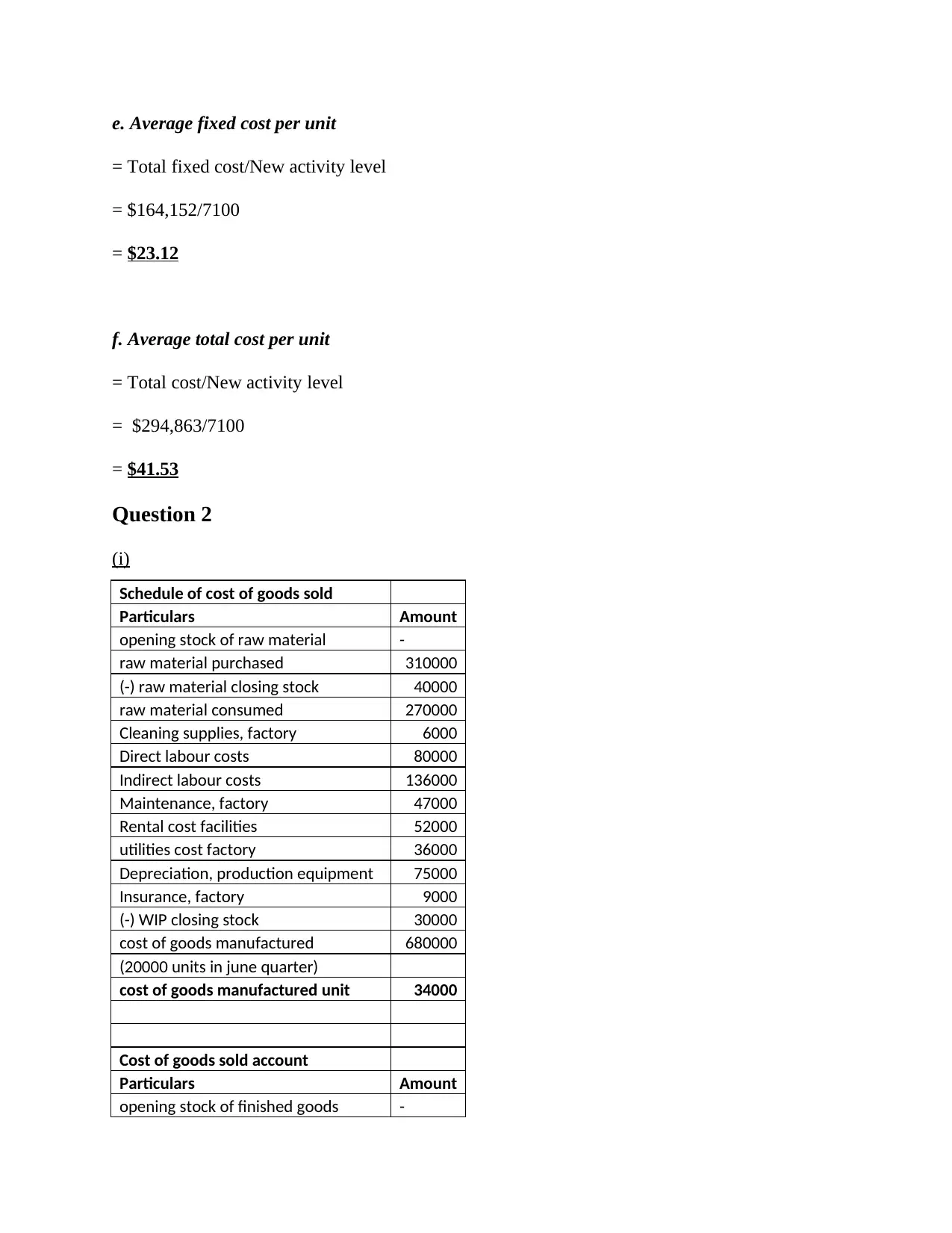

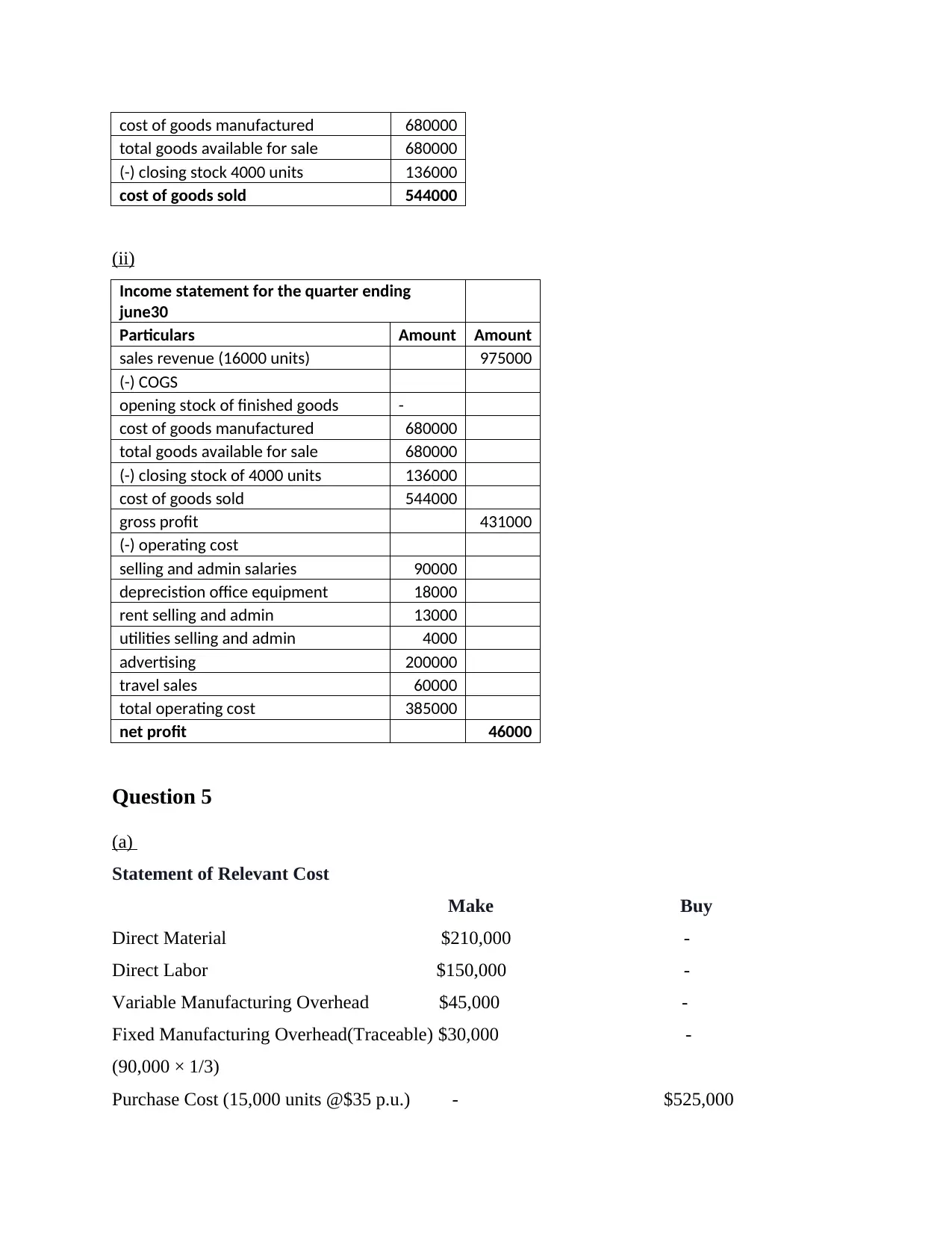

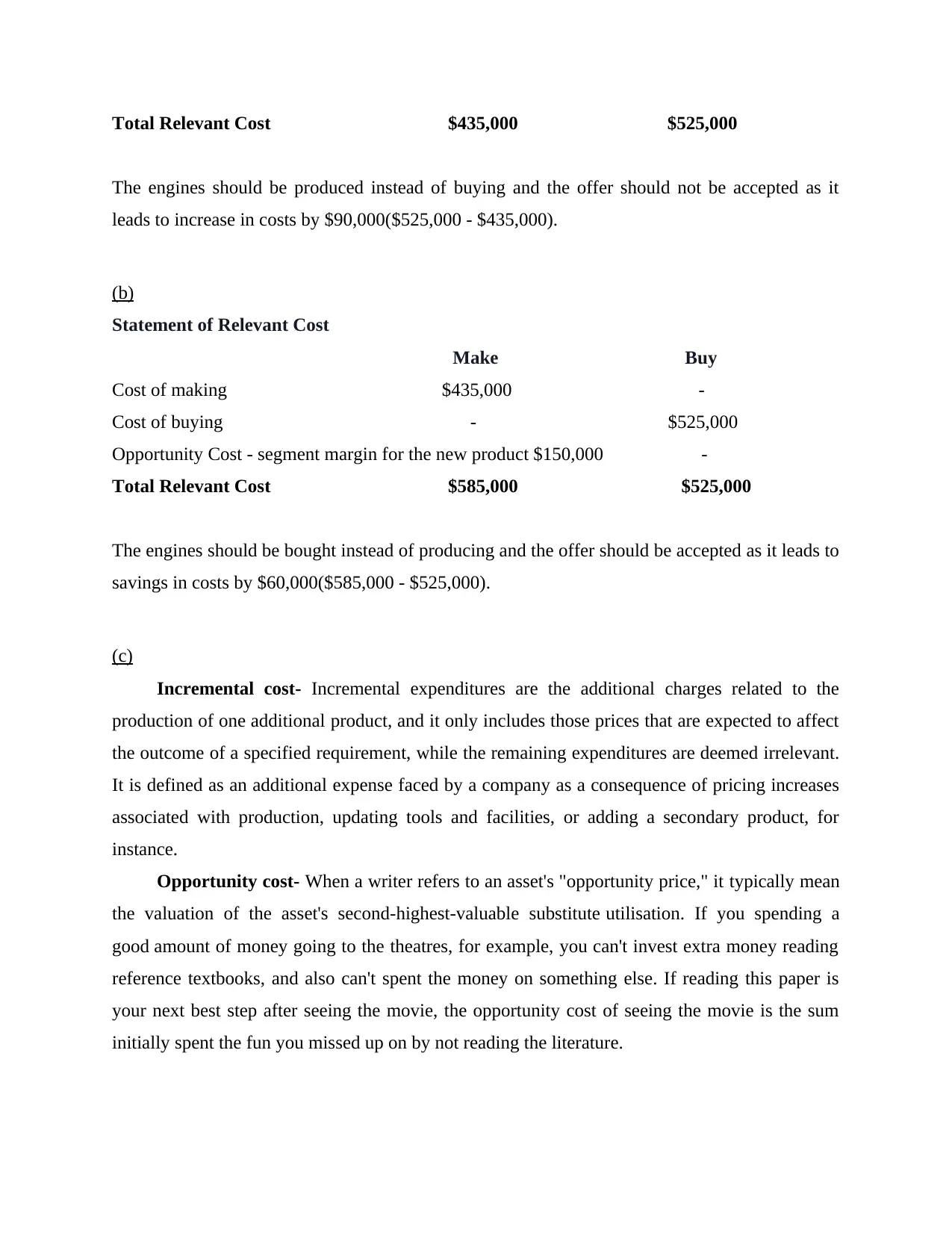

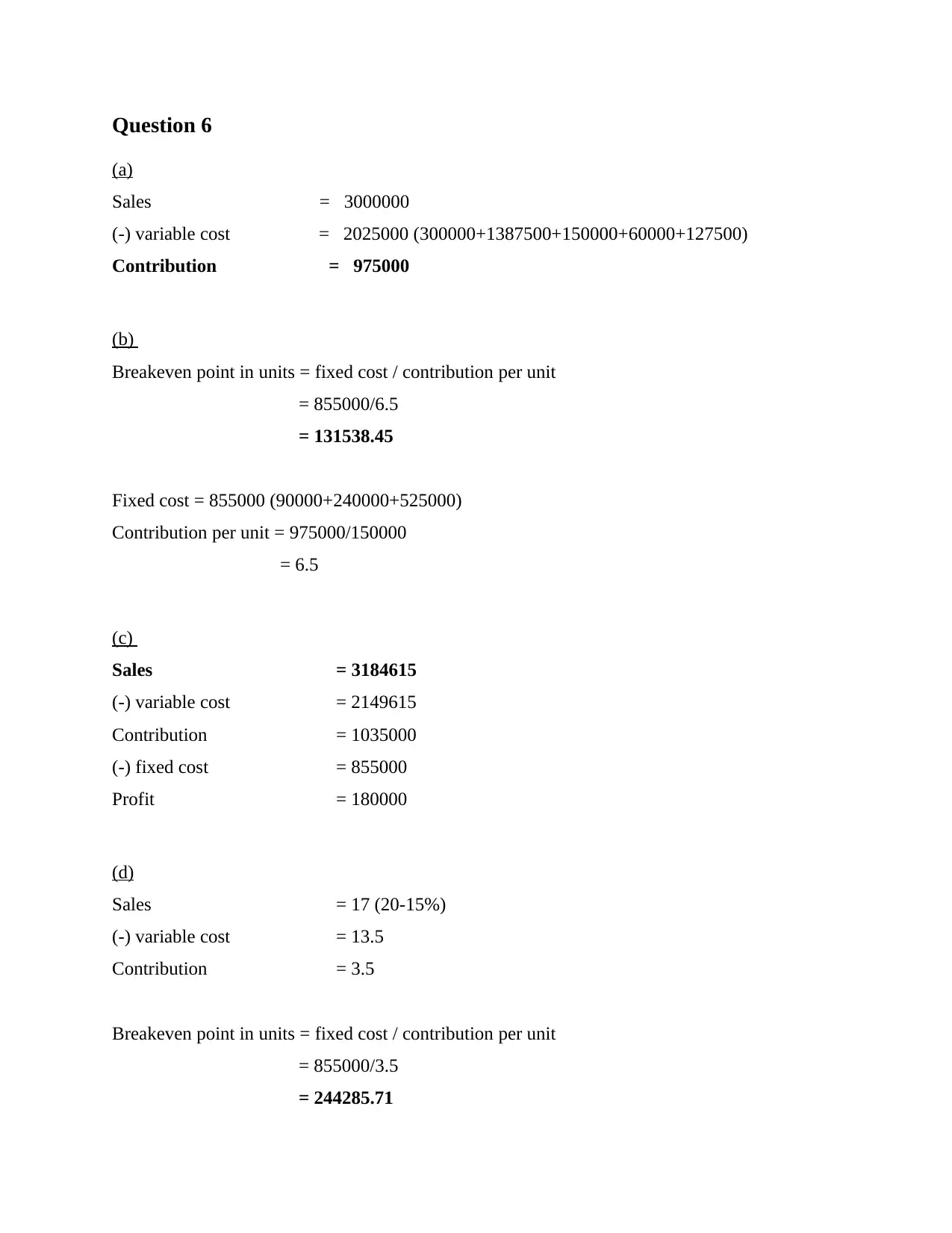

This assignment provides solutions to various management accounting problems. It includes calculating variable and fixed costs using the high-low method, preparing a schedule of cost of goods sold and an income statement, performing relevant cost analysis for make-or-buy decisions, and conducting cost-volume-profit (CVP) analysis to determine break-even points and profitability. The solutions demonstrate the application of management accounting principles in cost estimation, financial statement preparation, and decision-making scenarios.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.