Management Accounting: Cost Analysis & Profitability in BBQ Business

VerifiedAdded on 2023/06/06

|7

|1091

|387

Report

AI Summary

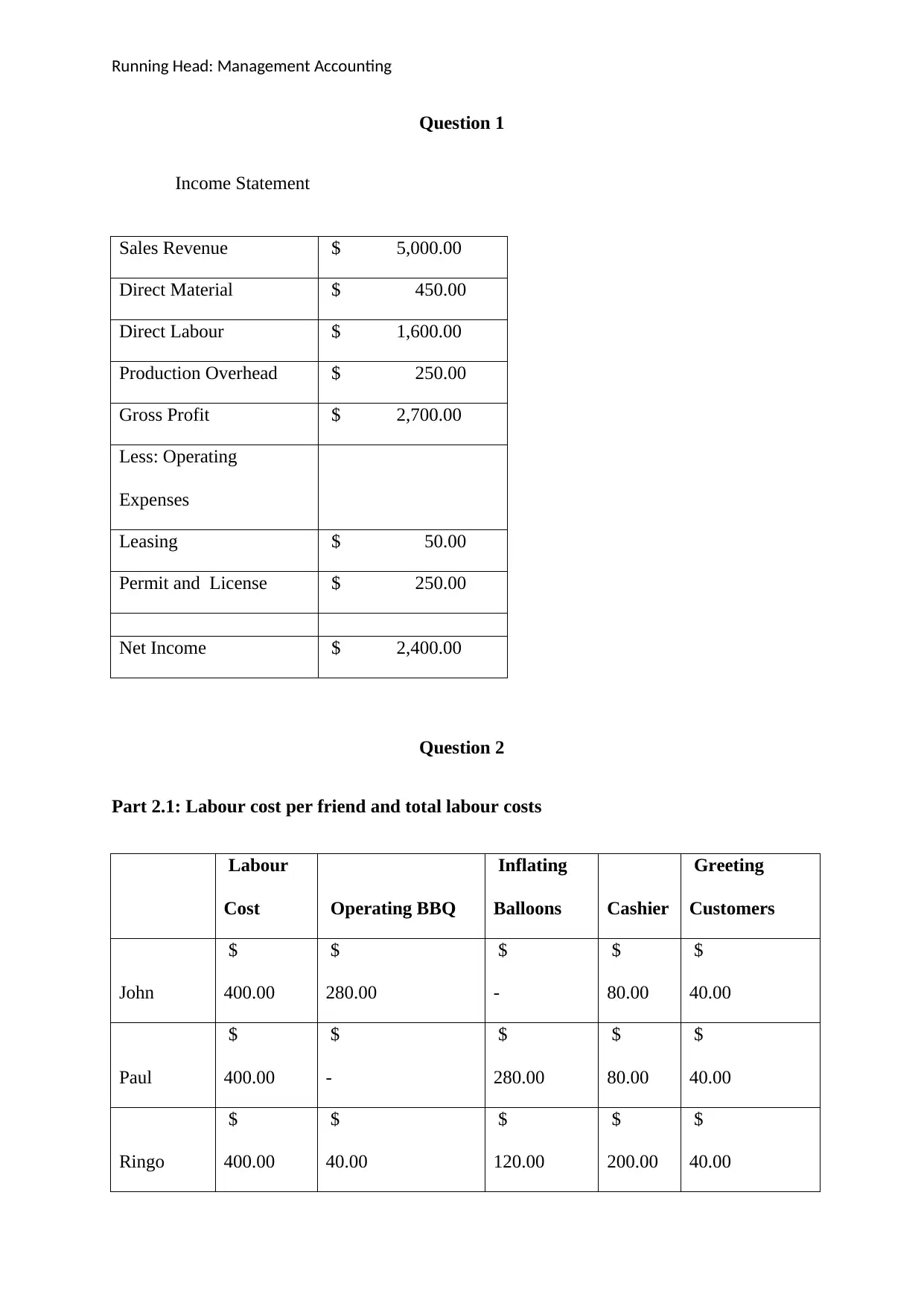

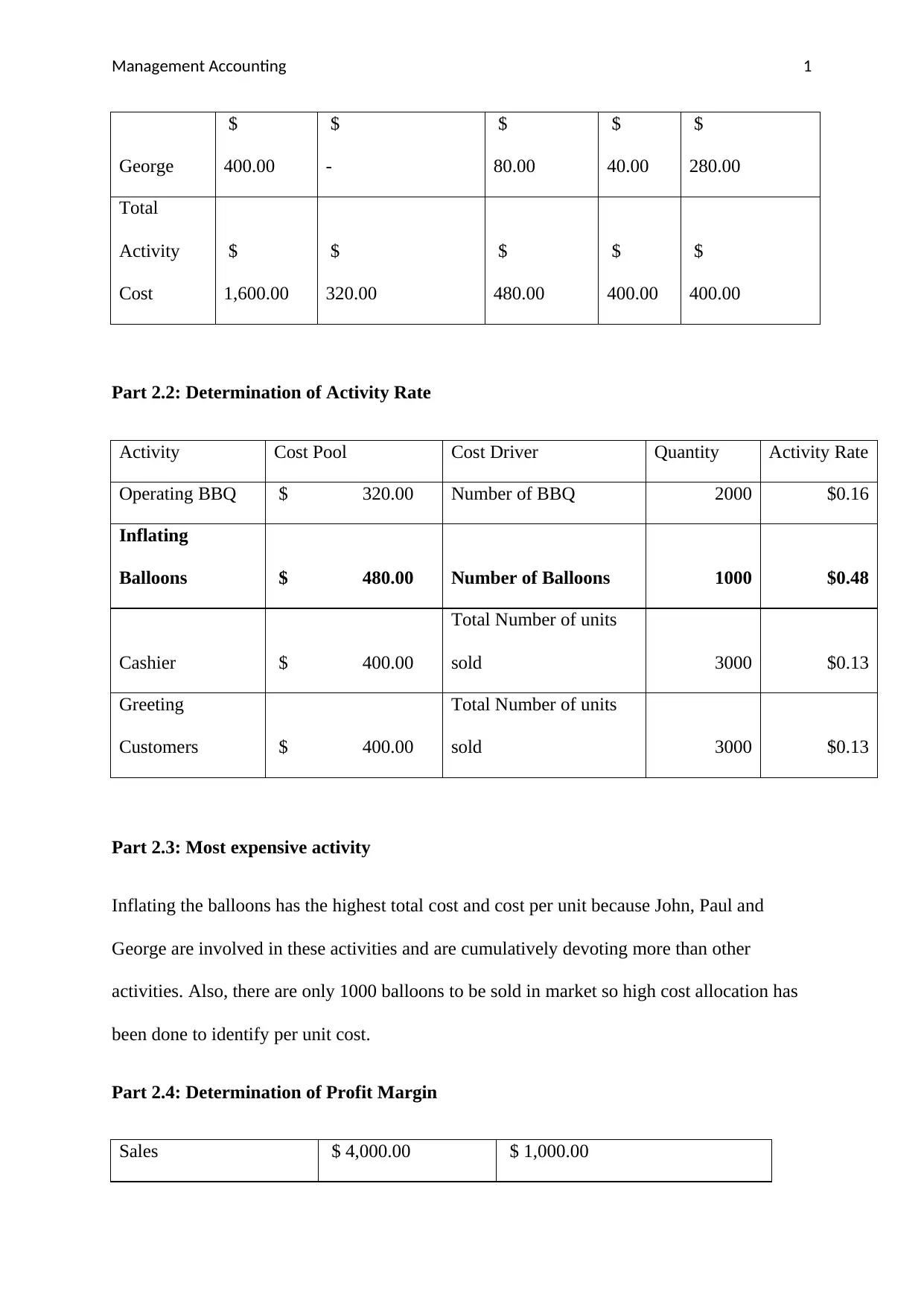

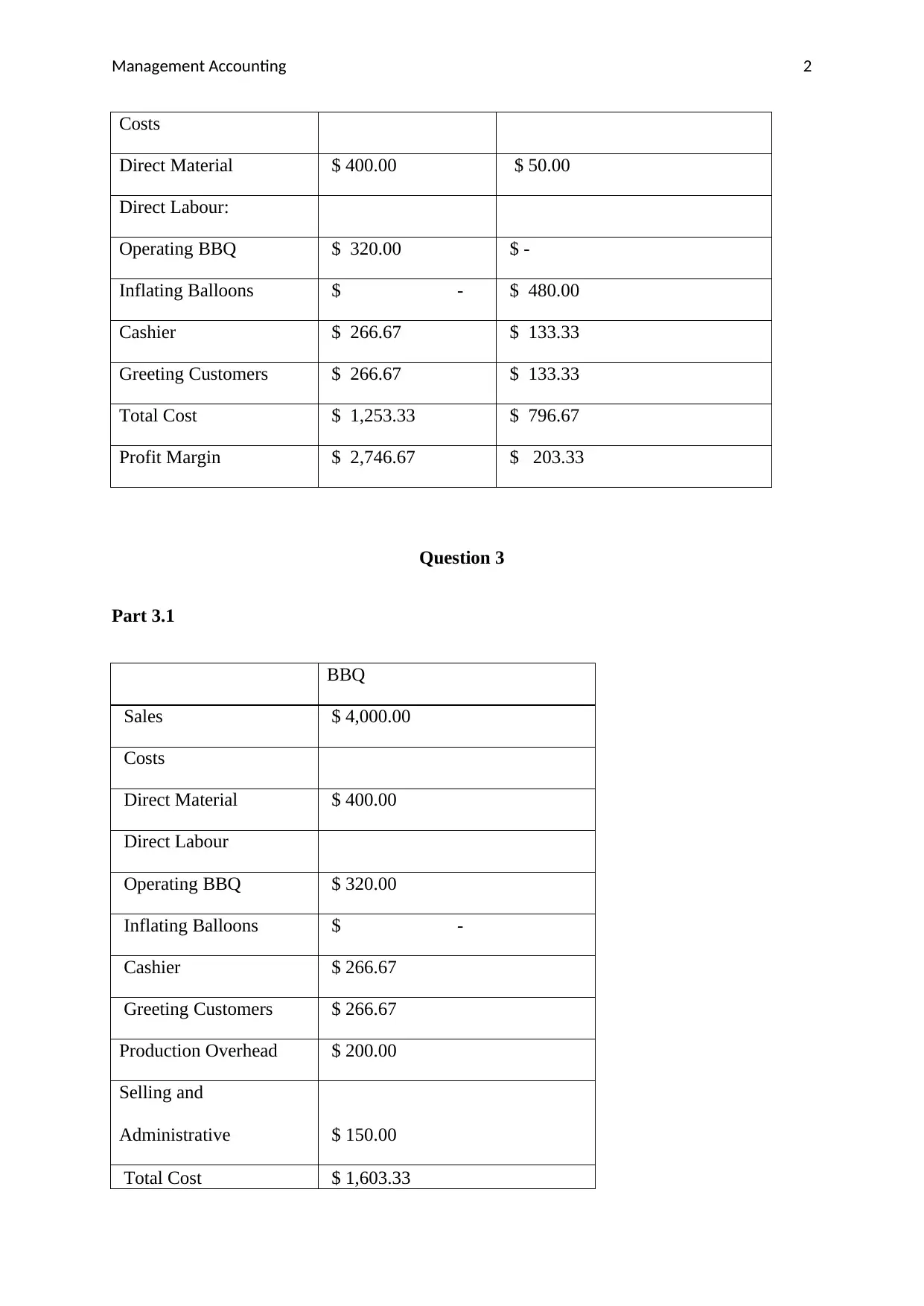

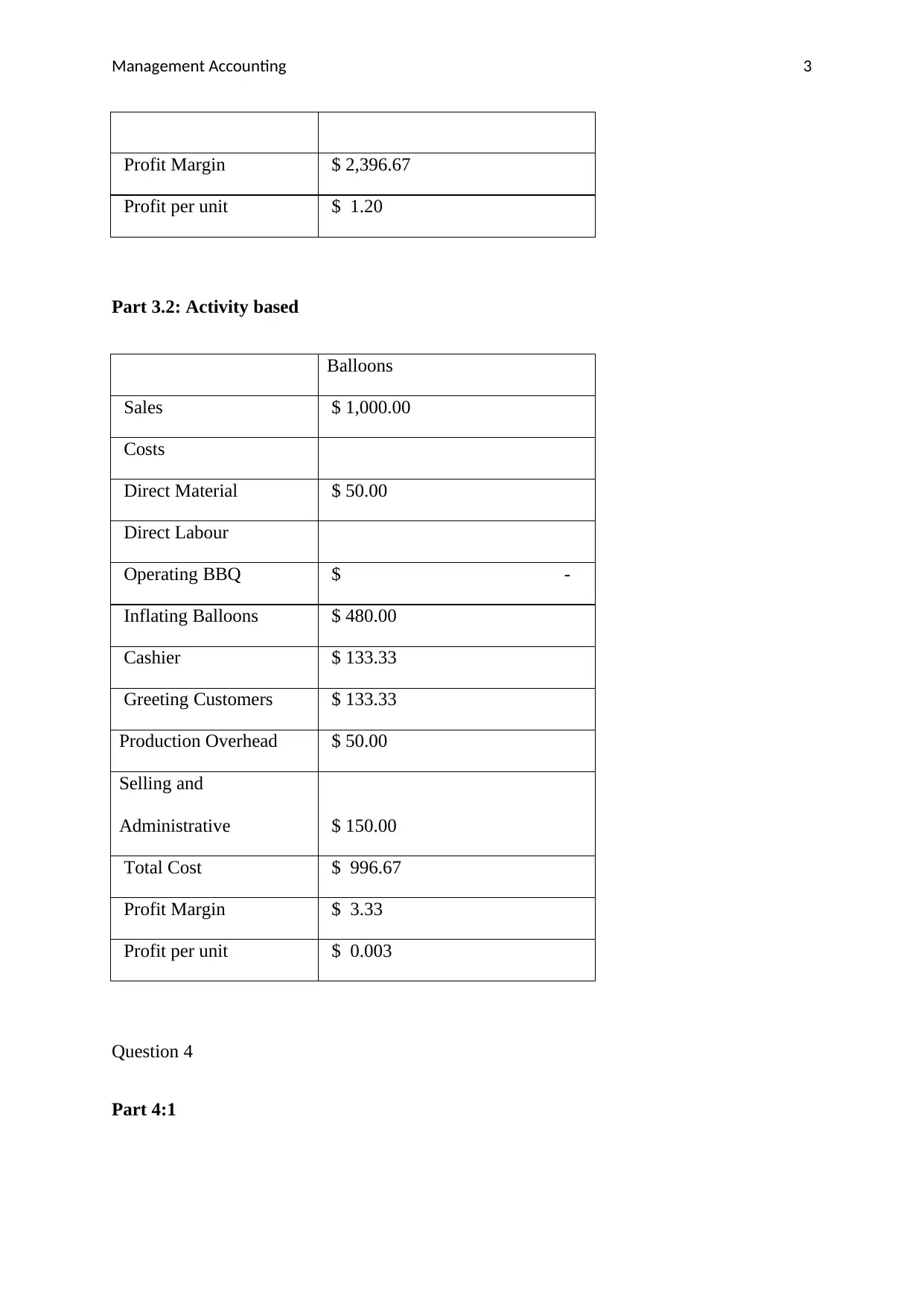

This report provides a detailed analysis of a BBQ and balloon business using management accounting principles. It includes an income statement, labor cost analysis, activity rate determination, and profitability analysis for both BBQ and balloon sales. The report uses activity-based costing (ABC) to allocate costs and evaluate the profitability of each product, revealing that BBQ sales are significantly more profitable than balloon sales. The analysis supports the argument that focusing resources on BBQ sales would lead to higher overall profitability for the firm. The report also discusses the fairness of income distribution among the firm's members, recommending pay based on time devoted to each activity and its complexity. The report concludes that the firm should focus on BBQ sales due to their higher profitability, supported by references to managerial accounting literature.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.