Management Accounting Report: Cost Analysis and Planning

VerifiedAdded on 2020/10/22

|12

|3593

|125

Report

AI Summary

This report delves into the core principles of management accounting, emphasizing its significance in organizational decision-making and financial planning. It begins by differentiating management accounting from financial accounting, highlighting their distinct objectives, scope, and application. The report then explores various cost evaluation methods, including marginal costing and absorption costing, providing detailed calculations and comparisons to illustrate their impact on profit analysis. Furthermore, it examines different types of budgets used in budgetary control, along with their advantages, and elucidates the budget preparation process. The report also underscores the importance of budgeting as a vital tool for planning and control, offering insights into the implications of management accounting systems in addressing financial problems and conflicts. Through comprehensive analysis and practical examples, the report aims to provide a thorough understanding of management accounting concepts and their practical applications in business environments.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) Explain the management accounting and the requirement of management accounting

system..........................................................................................................................................1

b) Presenting financial information.............................................................................................3

TASK 2............................................................................................................................................4

Cost evaluation methods.............................................................................................................4

TASK 3............................................................................................................................................6

a) Different kind of budgets and their advantages......................................................................6

b) The budget preparation process containing purpose of price and different costing system...7

c) Importance of budget as a tool for planing and control process.............................................8

TASK 4............................................................................................................................................8

Implication of management accounting system subject to respond financial problems and

conflicts.......................................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) Explain the management accounting and the requirement of management accounting

system..........................................................................................................................................1

b) Presenting financial information.............................................................................................3

TASK 2............................................................................................................................................4

Cost evaluation methods.............................................................................................................4

TASK 3............................................................................................................................................6

a) Different kind of budgets and their advantages......................................................................6

b) The budget preparation process containing purpose of price and different costing system...7

c) Importance of budget as a tool for planing and control process.............................................8

TASK 4............................................................................................................................................8

Implication of management accounting system subject to respond financial problems and

conflicts.......................................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Managerial accounting is becoming prior requirement of business entities and

organisations. Management accounting is adopted by organisation in terms of taking important

decisions and managing information in effective manner. Assisting decision making process and

analysing the plans is the main objective of management accounting. This report defines the

meaning of management accounting and types of management accounting system. Cost

evaluation methods are analysed in respect of evaluation profit (Wickramasinghe and

Alawattage, 2012). Type of budgets and planning tools are defined which are used in capital

budgeting. TECH UK limited organisation is used to define the meaning of management

accounting. Implication of management accounting system subject to respond financial problems

defined in this report.

TASK 1

a) Explain the management accounting and the requirement of management accounting system

I. Difference between management accounting and financial accounting

Basis of difference Management accounting Financial accounting

Objective Assisting managers and

accountants to make strategies and

business plans and make smooth

the decision making process.

Analysing, defining and presenting

the financial position of organisation

to managers is the main objective of

financial accounting.

Scope Business and organisation adopt the

management accounting system as

per their needs and suitability.

Wide scope found of financial

accounting in terms of managing

finance department of organisation.

Need It is not mandatory for

organisations to maintain

management accounting.

It is mandatory for organisation to

follow the rules and guidelines in

terms of keeping financial records.

Guidelines and

regulations

There are no specific rules and

legislations are made for maintain

and keeping management records

Rules and policies produced by

GAAP, IFRS and IAS are needed to

follow.

Review and control No any review and control required Financial accounts and records are

1

Managerial accounting is becoming prior requirement of business entities and

organisations. Management accounting is adopted by organisation in terms of taking important

decisions and managing information in effective manner. Assisting decision making process and

analysing the plans is the main objective of management accounting. This report defines the

meaning of management accounting and types of management accounting system. Cost

evaluation methods are analysed in respect of evaluation profit (Wickramasinghe and

Alawattage, 2012). Type of budgets and planning tools are defined which are used in capital

budgeting. TECH UK limited organisation is used to define the meaning of management

accounting. Implication of management accounting system subject to respond financial problems

defined in this report.

TASK 1

a) Explain the management accounting and the requirement of management accounting system

I. Difference between management accounting and financial accounting

Basis of difference Management accounting Financial accounting

Objective Assisting managers and

accountants to make strategies and

business plans and make smooth

the decision making process.

Analysing, defining and presenting

the financial position of organisation

to managers is the main objective of

financial accounting.

Scope Business and organisation adopt the

management accounting system as

per their needs and suitability.

Wide scope found of financial

accounting in terms of managing

finance department of organisation.

Need It is not mandatory for

organisations to maintain

management accounting.

It is mandatory for organisation to

follow the rules and guidelines in

terms of keeping financial records.

Guidelines and

regulations

There are no specific rules and

legislations are made for maintain

and keeping management records

Rules and policies produced by

GAAP, IFRS and IAS are needed to

follow.

Review and control No any review and control required Financial accounts and records are

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

for management accounting, it

depends upon organisational needs.

audited properly by auditors with

proper legal structure and guidelines.

Period There is no specific timeline

decided for management

accounting.

Financial accounts are made

quarterly, half yearly and annual

basis.

II. Importance of management accounting information as a decision making tool

Management accounting is basically used as a decision making tool which assist

managers and accountants for effective and better forecasting. For successful image of business

and organisation it is required to make effective. It provides a descriptive and in-depth

knowledge of business operations and management functions. With the effective use of

management accounting it become easy for managers to identify key performance indicators for

all the departments. This is mainly associated with collecting information, comparison and

making the plans in effective manner are analysed in this context.

III. Cost accounting system

This is one of the important element of business comes under management accounting.

Analysing the cost increasing factor and adopting tools to control cost is the main objective of

cost accounting system. This is a system which is majorly used by organisation to control the

cost and maximising profitability. Type of cost accounting systems and methods are used under

cost accounting system. Unit costing, process costing are some essential accounting system in

terms of analysing the cost and maximising profitability (Weygandt, Kimmel and Kieso, 2015).

IV. Inventory management system

This is one of the essential aspect in terms of managing the functions and management of

inventories. it is required for organisation and departments to manage and control the inventories

level for better execution of production and manufacturing process. It is a process of managing

the inventories and parts with the help of computer programs and software. Inventory

management system helps to track the level of stock, sales, order, purchase and delivery system.

In large organisations it helps to manufactures and creating work order, bill of material and other

production related documents.

V. Job costing system

2

depends upon organisational needs.

audited properly by auditors with

proper legal structure and guidelines.

Period There is no specific timeline

decided for management

accounting.

Financial accounts are made

quarterly, half yearly and annual

basis.

II. Importance of management accounting information as a decision making tool

Management accounting is basically used as a decision making tool which assist

managers and accountants for effective and better forecasting. For successful image of business

and organisation it is required to make effective. It provides a descriptive and in-depth

knowledge of business operations and management functions. With the effective use of

management accounting it become easy for managers to identify key performance indicators for

all the departments. This is mainly associated with collecting information, comparison and

making the plans in effective manner are analysed in this context.

III. Cost accounting system

This is one of the important element of business comes under management accounting.

Analysing the cost increasing factor and adopting tools to control cost is the main objective of

cost accounting system. This is a system which is majorly used by organisation to control the

cost and maximising profitability. Type of cost accounting systems and methods are used under

cost accounting system. Unit costing, process costing are some essential accounting system in

terms of analysing the cost and maximising profitability (Weygandt, Kimmel and Kieso, 2015).

IV. Inventory management system

This is one of the essential aspect in terms of managing the functions and management of

inventories. it is required for organisation and departments to manage and control the inventories

level for better execution of production and manufacturing process. It is a process of managing

the inventories and parts with the help of computer programs and software. Inventory

management system helps to track the level of stock, sales, order, purchase and delivery system.

In large organisations it helps to manufactures and creating work order, bill of material and other

production related documents.

V. Job costing system

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing system helps to analyse the cost of diverse sections and department with in

the organisation. This is the system which helps to analyse the different sectional cost at various

level such as production and manufacturing level, work in progress and finished goods stage.

Products are effectively bifurcated in separate section and cost evaluation become

more convenient. Manufacturing cost to analyse the an individual products or batch are defined

in this context.

b) Presenting financial information

I. Various type of managerial accounting reports

There are type of management accounting reports are produced to make decision making

process more fluent and flexible. These information helps to analyse the important decision and

make strategies.

Performance reports: these are the reports which helps to analyse the performance of

manpower and the strength of organisation. There is an individual performance and the

strength is evaluated by tracking the performance records for a specific time duration and

period. In large organisation these reports remain associated with analysing the

performance of individual sections and divisions.

Demand reports: these are the reports which helps to analyse the requirement of

inventors and level of stock in terms of managing the production and manufacturing

process. It helps to formulate the essential information and aspects in terms of managing

the requirement level as scheduled and pre-recorded as per the report (Moser, 2012).

Inventory management reports: this reports contains the information and data related

to raw materiel consumed during the year, work in progress, finish good products and

analysing the production requirement of organisation. There is a brief information such as

opening stock, closing stock and identifying the future requirement of business in terms

of improving the complete growth and effective of organisation.

Job cost reports: these are the reports which remain essential for analysing the cost of

individual sections and departments of organisation. In large business and manufacturing

organisations process of manufacturing remain bifurcated in several parts, individual cost

records are maintained by accountants and the departments. In the end of year all the

departmental and job costs are consolidated in single format to analyse overall cost of

operation.

3

the organisation. This is the system which helps to analyse the different sectional cost at various

level such as production and manufacturing level, work in progress and finished goods stage.

Products are effectively bifurcated in separate section and cost evaluation become

more convenient. Manufacturing cost to analyse the an individual products or batch are defined

in this context.

b) Presenting financial information

I. Various type of managerial accounting reports

There are type of management accounting reports are produced to make decision making

process more fluent and flexible. These information helps to analyse the important decision and

make strategies.

Performance reports: these are the reports which helps to analyse the performance of

manpower and the strength of organisation. There is an individual performance and the

strength is evaluated by tracking the performance records for a specific time duration and

period. In large organisation these reports remain associated with analysing the

performance of individual sections and divisions.

Demand reports: these are the reports which helps to analyse the requirement of

inventors and level of stock in terms of managing the production and manufacturing

process. It helps to formulate the essential information and aspects in terms of managing

the requirement level as scheduled and pre-recorded as per the report (Moser, 2012).

Inventory management reports: this reports contains the information and data related

to raw materiel consumed during the year, work in progress, finish good products and

analysing the production requirement of organisation. There is a brief information such as

opening stock, closing stock and identifying the future requirement of business in terms

of improving the complete growth and effective of organisation.

Job cost reports: these are the reports which remain essential for analysing the cost of

individual sections and departments of organisation. In large business and manufacturing

organisations process of manufacturing remain bifurcated in several parts, individual cost

records are maintained by accountants and the departments. In the end of year all the

departmental and job costs are consolidated in single format to analyse overall cost of

operation.

3

Operational budget reports: these are the reports which helps to analyse the cost of

operations and management in terms of defining the operational cost. With the help of

operational budget reports managers become able to make budget for future events and

operational activities. By making effective operating budge reports cost can be easily

control which helps to enhance profitability.

Schedule reports: timeline is one of the essential element of organisation in terms of

getting the desired advantages in time. These majorly helps to sort out the plans and

complex business situations and assist operations and management to complete task and

project before time and on the given deadline (Leitner, 2013).

II. Importance of presenting information in systematic manner

It is require to present financial information in effective manner so that it become eligible

to sort out the plans and objectives. These information not only assist the organisational structure

to achieve the core competence but also helps to enhance profitability of organisation. There are

some rules and legislations are made in terms of presenting and making reports and present them

in specific format. There are rules and regulations terms of GAAP which helps to associate with

reporting related to financial information and analysing the profitability. There are some

reporting standards also followed by organisations to make reporting structure viable and

voidable. Management accounting system does not contains the rules and legislations but the the

methods and tools used under management accounting are required to follow in system and

ethical manner. An effective reporting structure helps make the business functions in effective

manner so that organisation be able to make viability in legal terms.

TASK 2

Cost evaluation methods

Marginal costing: this is the costing system which helps to determine the cost of

production and manufacturing cost on the basis of variable cost. There are some essential aspects

are considered in terms of analysing the profitability and sustainability of organisation. This is

also a part of the unit cost. This costing also remain help in decision making process and also

helps to sort out the plan for a specific time duration and period. The cost is incurred in majorly

three forms such as direct material, direct labour and direct expenses. As per this costing if sales

increased then profitability also increase (Lavia López and Hiebl, 2014). As per decision making

4

operations and management in terms of defining the operational cost. With the help of

operational budget reports managers become able to make budget for future events and

operational activities. By making effective operating budge reports cost can be easily

control which helps to enhance profitability.

Schedule reports: timeline is one of the essential element of organisation in terms of

getting the desired advantages in time. These majorly helps to sort out the plans and

complex business situations and assist operations and management to complete task and

project before time and on the given deadline (Leitner, 2013).

II. Importance of presenting information in systematic manner

It is require to present financial information in effective manner so that it become eligible

to sort out the plans and objectives. These information not only assist the organisational structure

to achieve the core competence but also helps to enhance profitability of organisation. There are

some rules and legislations are made in terms of presenting and making reports and present them

in specific format. There are rules and regulations terms of GAAP which helps to associate with

reporting related to financial information and analysing the profitability. There are some

reporting standards also followed by organisations to make reporting structure viable and

voidable. Management accounting system does not contains the rules and legislations but the the

methods and tools used under management accounting are required to follow in system and

ethical manner. An effective reporting structure helps make the business functions in effective

manner so that organisation be able to make viability in legal terms.

TASK 2

Cost evaluation methods

Marginal costing: this is the costing system which helps to determine the cost of

production and manufacturing cost on the basis of variable cost. There are some essential aspects

are considered in terms of analysing the profitability and sustainability of organisation. This is

also a part of the unit cost. This costing also remain help in decision making process and also

helps to sort out the plan for a specific time duration and period. The cost is incurred in majorly

three forms such as direct material, direct labour and direct expenses. As per this costing if sales

increased then profitability also increase (Lavia López and Hiebl, 2014). As per decision making

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

perspective marginal costing plays vital role in organisational context. This costing method is

also called as period cost method.

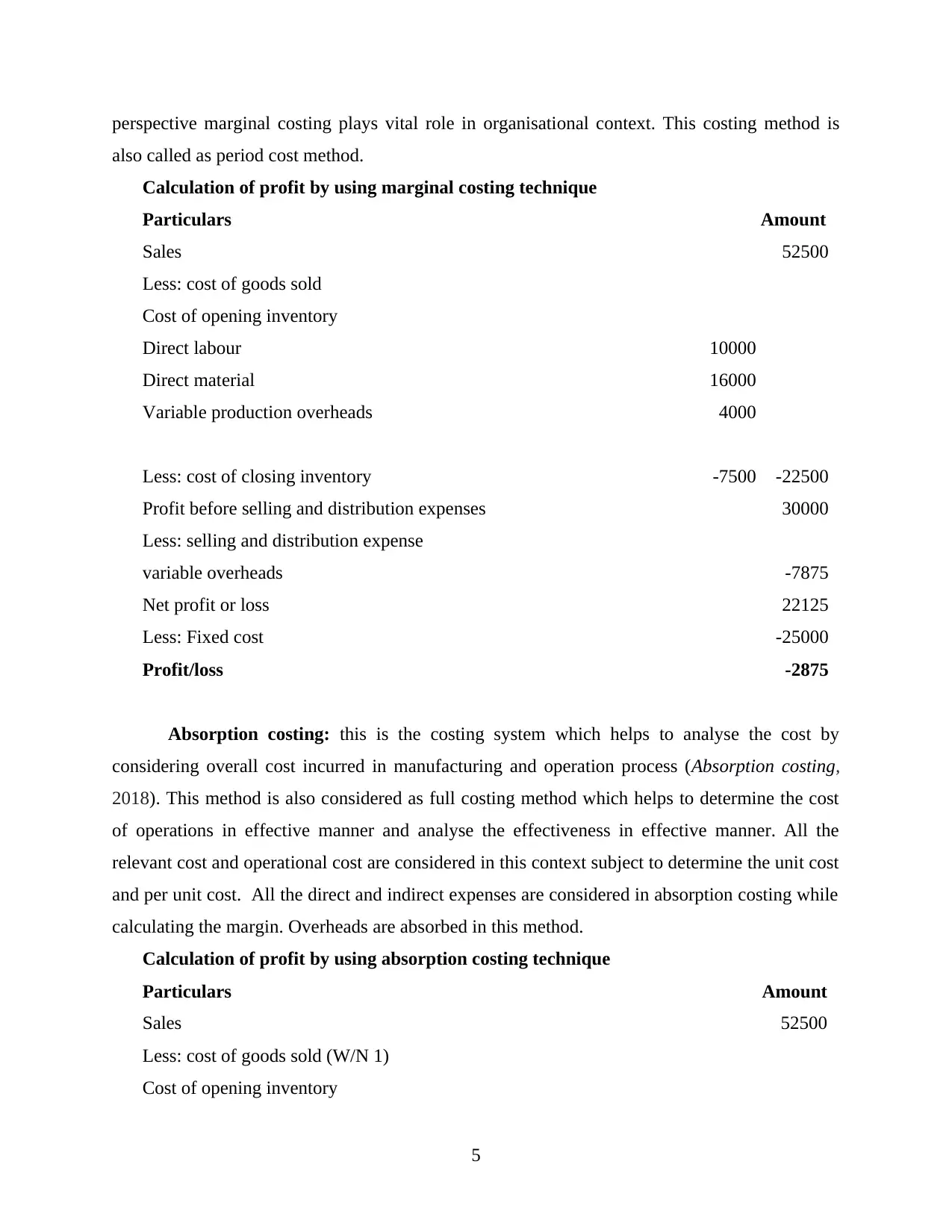

Calculation of profit by using marginal costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold

Cost of opening inventory

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Less: cost of closing inventory -7500 -22500

Profit before selling and distribution expenses 30000

Less: selling and distribution expense

variable overheads -7875

Net profit or loss 22125

Less: Fixed cost -25000

Profit/loss -2875

Absorption costing: this is the costing system which helps to analyse the cost by

considering overall cost incurred in manufacturing and operation process (Absorption costing,

2018). This method is also considered as full costing method which helps to determine the cost

of operations in effective manner and analyse the effectiveness in effective manner. All the

relevant cost and operational cost are considered in this context subject to determine the unit cost

and per unit cost. All the direct and indirect expenses are considered in absorption costing while

calculating the margin. Overheads are absorbed in this method.

Calculation of profit by using absorption costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold (W/N 1)

Cost of opening inventory

5

also called as period cost method.

Calculation of profit by using marginal costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold

Cost of opening inventory

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Less: cost of closing inventory -7500 -22500

Profit before selling and distribution expenses 30000

Less: selling and distribution expense

variable overheads -7875

Net profit or loss 22125

Less: Fixed cost -25000

Profit/loss -2875

Absorption costing: this is the costing system which helps to analyse the cost by

considering overall cost incurred in manufacturing and operation process (Absorption costing,

2018). This method is also considered as full costing method which helps to determine the cost

of operations in effective manner and analyse the effectiveness in effective manner. All the

relevant cost and operational cost are considered in this context subject to determine the unit cost

and per unit cost. All the direct and indirect expenses are considered in absorption costing while

calculating the margin. Overheads are absorbed in this method.

Calculation of profit by using absorption costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold (W/N 1)

Cost of opening inventory

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Fixed overheads 10000

Less: cost of closing inventory -10000 -30000

Profit before deduction fixed overheads and selling and distribution

expenses 22500

Less: under/over absorption -5000

17500

Less: selling and distribution expense

fixed overheads -10000

variable overheads -7875

Net profit or loss -375

Working Notes:

1. Calculation of cost of goods sold under absorption costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Fixed overheads (2000*5) 10000

Less: cost of closing inventory (500*20) -10000

Cost of goods sold 30000

2. Calculation of selling and distribution expenses

Particulars Details Amount

fixed overheads 10000

variable overheads (52500*15%) 7875

Total selling and distribution expenses 17875

3. Calculation of cost of goods sold under marginal costing technique

Particulars Details Amount

Cost of opening inventory -

6

Direct material 16000

Variable production overheads 4000

Fixed overheads 10000

Less: cost of closing inventory -10000 -30000

Profit before deduction fixed overheads and selling and distribution

expenses 22500

Less: under/over absorption -5000

17500

Less: selling and distribution expense

fixed overheads -10000

variable overheads -7875

Net profit or loss -375

Working Notes:

1. Calculation of cost of goods sold under absorption costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Fixed overheads (2000*5) 10000

Less: cost of closing inventory (500*20) -10000

Cost of goods sold 30000

2. Calculation of selling and distribution expenses

Particulars Details Amount

fixed overheads 10000

variable overheads (52500*15%) 7875

Total selling and distribution expenses 17875

3. Calculation of cost of goods sold under marginal costing technique

Particulars Details Amount

Cost of opening inventory -

6

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Less: cost of closing inventory (500*15) 7500

Cost of goods sold 22500

TASK 3

a) Different kind of budgets and their advantages

There are type of budgets are used in budgetary control process. There are planning tools

are also analysed in budgetary control which make cost control process in more effective

manner.

Operational budget: this budget helps to determine the operational cost to be incurred

for subsiding year. Total expected revenues and expenditure are considered this budget (Hilton

and Platt, 2013).

Advantages: operational cost can be easily controlled and comprised with the

help of making operational budget.

Disadvantage: there is a lack of accurate information found in terms of making

operational budget.

Cash budget: this budget helps to determine the requirement of cash for upcoming

events and activities in terms of executing functions and operations in effective manner.

Analysation of cash budget is based upon cash flow from operation activities, financial activities

and investing activities.

Advantages: this helps to analyse the total cash inflow and total cash out flow

during the year or for a specific time duration. The are essential aspects are considered subject to

analyse the cost (Eierle and Schultze, 2013).

Disadvantage: it becomes difficult for managers to adjust the amount of cash

generated after preparing cash budget.

Rolling budget: this is the budget which helps to determine the additional requirement in

terms of incremental cost and information.

Advantages: the changes be able to determine at initial stage and it become

helpful for organisation.

7

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Less: cost of closing inventory (500*15) 7500

Cost of goods sold 22500

TASK 3

a) Different kind of budgets and their advantages

There are type of budgets are used in budgetary control process. There are planning tools

are also analysed in budgetary control which make cost control process in more effective

manner.

Operational budget: this budget helps to determine the operational cost to be incurred

for subsiding year. Total expected revenues and expenditure are considered this budget (Hilton

and Platt, 2013).

Advantages: operational cost can be easily controlled and comprised with the

help of making operational budget.

Disadvantage: there is a lack of accurate information found in terms of making

operational budget.

Cash budget: this budget helps to determine the requirement of cash for upcoming

events and activities in terms of executing functions and operations in effective manner.

Analysation of cash budget is based upon cash flow from operation activities, financial activities

and investing activities.

Advantages: this helps to analyse the total cash inflow and total cash out flow

during the year or for a specific time duration. The are essential aspects are considered subject to

analyse the cost (Eierle and Schultze, 2013).

Disadvantage: it becomes difficult for managers to adjust the amount of cash

generated after preparing cash budget.

Rolling budget: this is the budget which helps to determine the additional requirement in

terms of incremental cost and information.

Advantages: the changes be able to determine at initial stage and it become

helpful for organisation.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Disadvantage: it become difficult for managers and accountants to analyse the

additional incremental requirement of budget.

Fixed budget: this budget can not be changed and remain non flexible for subsiding

years. A financial plan is proposed to change for a specific time duration.

Advantages: For small business this budget remain essential and effective.

Disadvantage: it does not contains the accuracy for unpredictable activities.

Flexible budget: there are type of project analysed in terms of products and services.

Changes can be easily adopted in this budget.

Advantages: it helps to bifurcate the cost as per seasonal basis and include

changes on regular basis.

Disadvantage: it become difficult for managers and accountants to track the

expenses and cost of organisation.

b) The budget preparation process containing purpose of price and different costing system

Budgeting process mainly associated in major steps such as

Preparing and analysing the budget assumptions

Defining the requirement of funds

Analysing the cost points and evaluating the cost centre

Creating the package of budget

Sustain forecast of revenue

Analyse the departmental budgets

Validate compensation and analyse the validation

Validate bonus plans are analysed in terms of determine the project requirement

Sustain the capital budget appeal

Update and modify the budget

Review and Issue the budget

c) Importance of budget as a tool for planing and control process

There are type of planning tools are used and methods are used to control the cost and

increase the amount in effective manner. There are type of methods are also used which are

defined as follows:

8

additional incremental requirement of budget.

Fixed budget: this budget can not be changed and remain non flexible for subsiding

years. A financial plan is proposed to change for a specific time duration.

Advantages: For small business this budget remain essential and effective.

Disadvantage: it does not contains the accuracy for unpredictable activities.

Flexible budget: there are type of project analysed in terms of products and services.

Changes can be easily adopted in this budget.

Advantages: it helps to bifurcate the cost as per seasonal basis and include

changes on regular basis.

Disadvantage: it become difficult for managers and accountants to track the

expenses and cost of organisation.

b) The budget preparation process containing purpose of price and different costing system

Budgeting process mainly associated in major steps such as

Preparing and analysing the budget assumptions

Defining the requirement of funds

Analysing the cost points and evaluating the cost centre

Creating the package of budget

Sustain forecast of revenue

Analyse the departmental budgets

Validate compensation and analyse the validation

Validate bonus plans are analysed in terms of determine the project requirement

Sustain the capital budget appeal

Update and modify the budget

Review and Issue the budget

c) Importance of budget as a tool for planing and control process

There are type of planning tools are used and methods are used to control the cost and

increase the amount in effective manner. There are type of methods are also used which are

defined as follows:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price skimming: it helps to enhance the sales graph of organisation and increase the sale

of new products. It is considered as a strategy with the help of this method price of the products

are analysed on the basis of demand of products and services (Christ, 2014).

Cost plus pricing: this method helps to decide the price of products after considering the

additional cost incurred to manufacture and produce products. Direct labour, direct cost and

charges are incurred in while calculating profit margin upon products and services.

Full costing pricing: this method helps to define the cost of products and services by

considering all the direct and indirect cost. Price of products and services get higher by

implementation of this method.

Economic pricing: this pricing method is mainly used to define the cost and set the price

at very low at their different products.

TASK 4

Implication of management accounting system subject to respond financial problems and

conflicts

As per above case scenario of TECH UK Ltd, there is a loss of £1.5 million in their

accounts are and it is analysed that the organisation is ready to evaluate and bifurcate the

business in effective manner. There are ways analysed in terms of evaluate this financial problem

and find out the ways to adopt management accounting system with in the organisation. There is

a method helps to determine the financial problem and analysis the financial problem of

organisation.

Balance scorecard method:

it is one of the essential element in terms of operating and deal with financial problem

and helps to make effective financial plans and strategies. It provides a schedule to make time

line and structure for better assessment of project and task (Becker, Ulrich and Staffel, 2011).

This approach is mainly works around following elements which are defined as follows:

Financial: this helps to define the financial requirement and find out the possible ways to

arrange financial resources. This is one of the essential aspect in terms of utilisation and

implication of financial resources in effective manner.

Customer: it is required to analyse the market share and number of customers in

organisational context. Information related to stakeholders, customer and perception of customer

plays vital role.

9

of new products. It is considered as a strategy with the help of this method price of the products

are analysed on the basis of demand of products and services (Christ, 2014).

Cost plus pricing: this method helps to decide the price of products after considering the

additional cost incurred to manufacture and produce products. Direct labour, direct cost and

charges are incurred in while calculating profit margin upon products and services.

Full costing pricing: this method helps to define the cost of products and services by

considering all the direct and indirect cost. Price of products and services get higher by

implementation of this method.

Economic pricing: this pricing method is mainly used to define the cost and set the price

at very low at their different products.

TASK 4

Implication of management accounting system subject to respond financial problems and

conflicts

As per above case scenario of TECH UK Ltd, there is a loss of £1.5 million in their

accounts are and it is analysed that the organisation is ready to evaluate and bifurcate the

business in effective manner. There are ways analysed in terms of evaluate this financial problem

and find out the ways to adopt management accounting system with in the organisation. There is

a method helps to determine the financial problem and analysis the financial problem of

organisation.

Balance scorecard method:

it is one of the essential element in terms of operating and deal with financial problem

and helps to make effective financial plans and strategies. It provides a schedule to make time

line and structure for better assessment of project and task (Becker, Ulrich and Staffel, 2011).

This approach is mainly works around following elements which are defined as follows:

Financial: this helps to define the financial requirement and find out the possible ways to

arrange financial resources. This is one of the essential aspect in terms of utilisation and

implication of financial resources in effective manner.

Customer: it is required to analyse the market share and number of customers in

organisational context. Information related to stakeholders, customer and perception of customer

plays vital role.

9

Internal process: this step helps to sort out the issues and conflicting which remain

associated with quality and good services. Increased quality and effective services helps to

improve the internal management and control.

Organisational volume: this is the last step which helps to examine the effectiveness of

approach in terms of attaining the aim and opportunities. Analysing the performance of

organisation as strong capital and quality of good and services (Akbar, 2010).

CONCLUSION

This report is prepared to analyse effectiveness of management accounting in

organisational context. There are type of accounting system and reports are defined in this

context which help in decision making process. Marginal and absorption costing method

discussed in terms of analysing the profitability of products and services. This is one of the

essential method which helps to consolidate the information and requirement of business in

effective manner so that decision making process become flexible. There are type of budgets and

planning tools are described which are used in budgetary control. Importance of management

accounting system to respond financial problems are also defined in this context.

10

associated with quality and good services. Increased quality and effective services helps to

improve the internal management and control.

Organisational volume: this is the last step which helps to examine the effectiveness of

approach in terms of attaining the aim and opportunities. Analysing the performance of

organisation as strong capital and quality of good and services (Akbar, 2010).

CONCLUSION

This report is prepared to analyse effectiveness of management accounting in

organisational context. There are type of accounting system and reports are defined in this

context which help in decision making process. Marginal and absorption costing method

discussed in terms of analysing the profitability of products and services. This is one of the

essential method which helps to consolidate the information and requirement of business in

effective manner so that decision making process become flexible. There are type of budgets and

planning tools are described which are used in budgetary control. Importance of management

accounting system to respond financial problems are also defined in this context.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.