University Assignment: Management Accounting for Cost and Control

VerifiedAdded on 2020/02/24

|24

|1837

|33

Homework Assignment

AI Summary

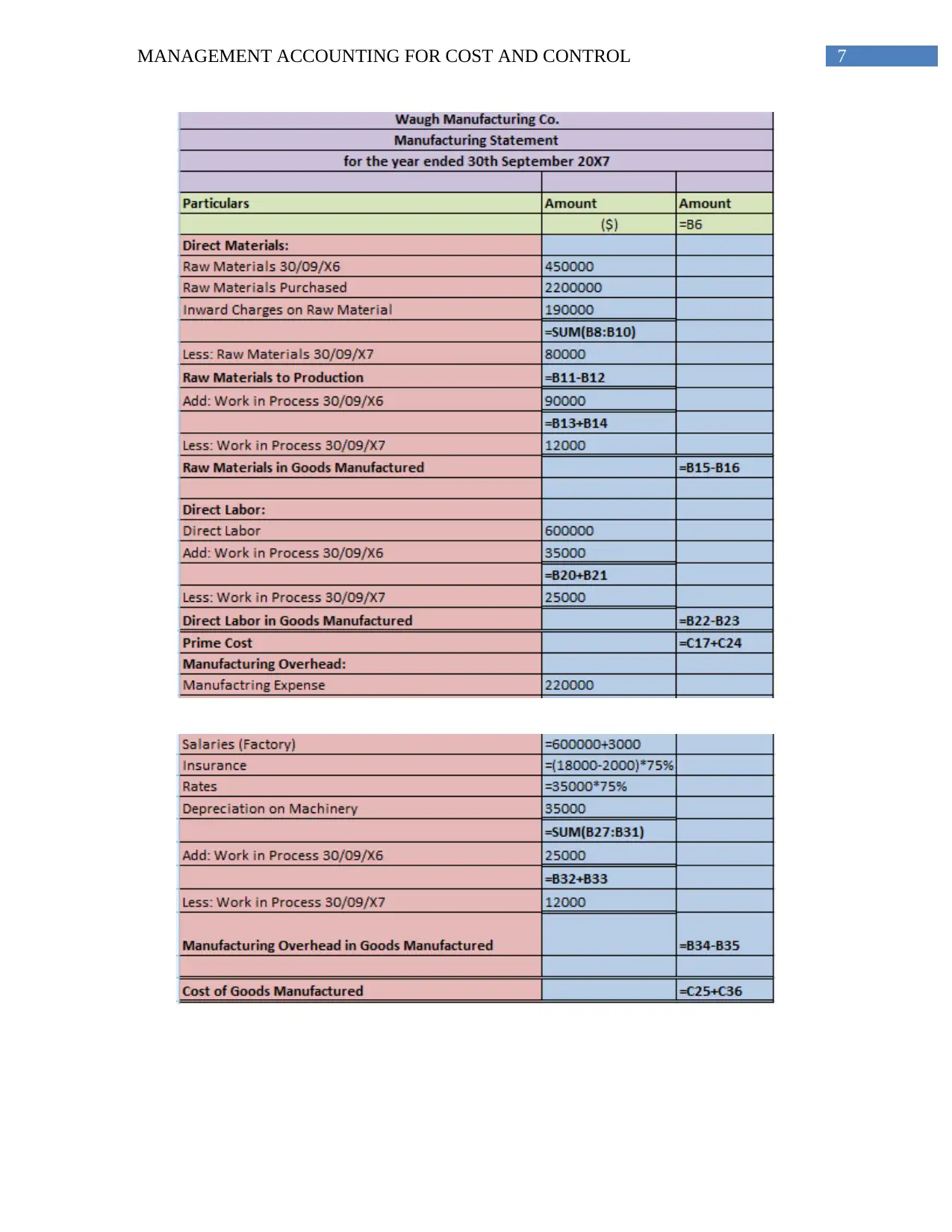

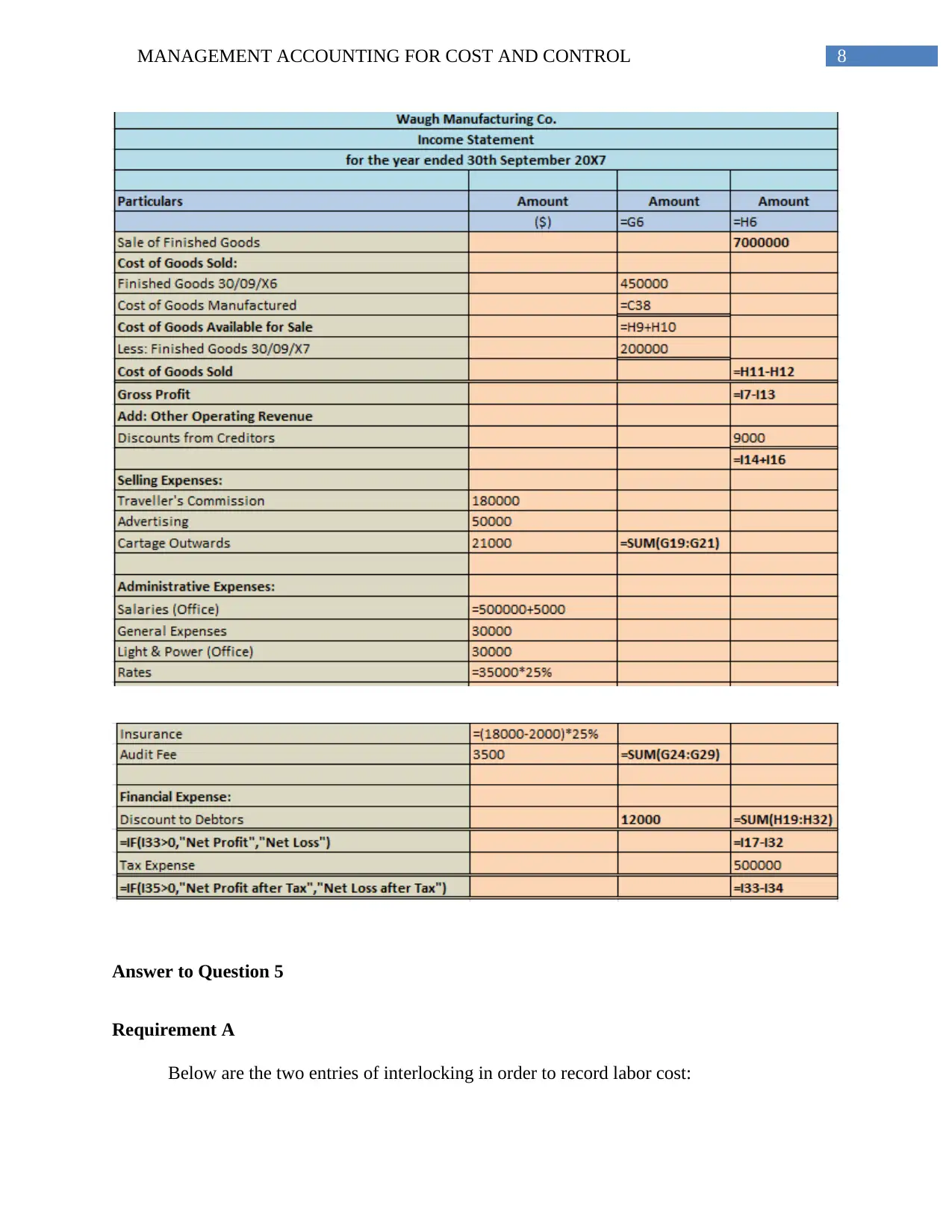

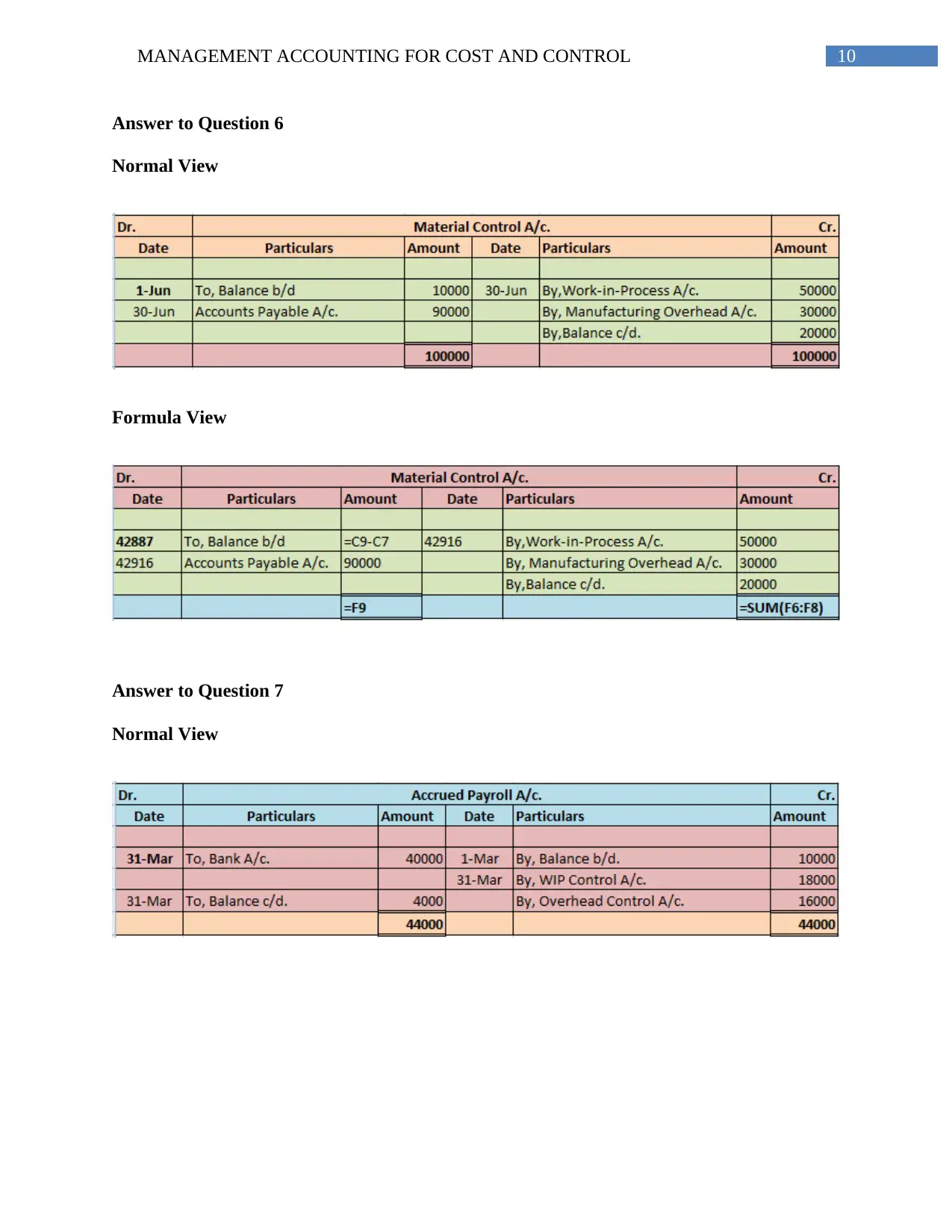

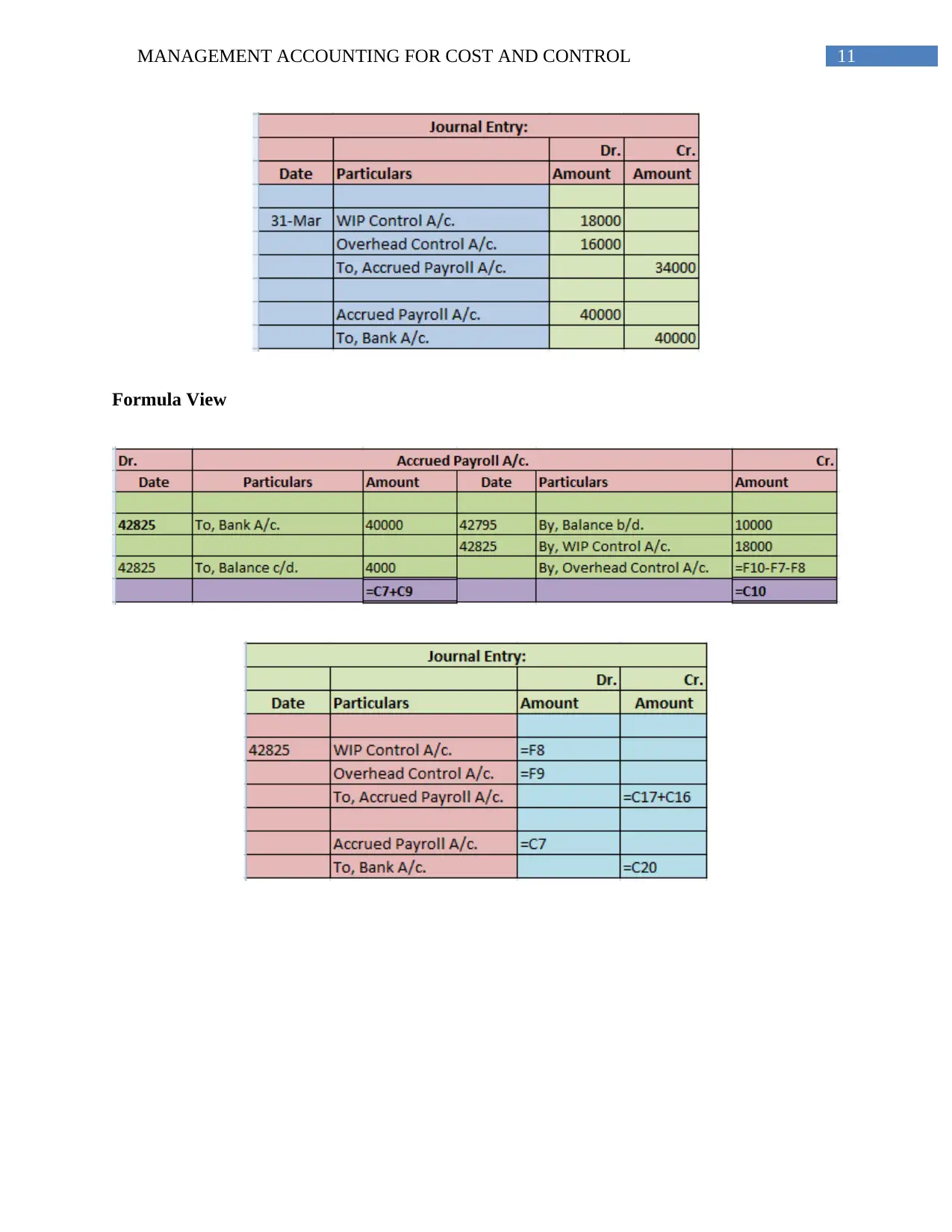

This assignment solution delves into the core principles of management accounting, focusing on cost and control. It provides detailed answers to questions covering various aspects, including the purposes of management accounting, the control function, product costing, and labor cost accounting. The solution explores the allocation of overhead expenses and contrasts traditional costing methods with activity-based costing, highlighting the advantages and disadvantages of each. The document also presents practical applications of overhead allocation, including the direct, step, and reciprocal service methods. Overall, the assignment offers a comprehensive analysis of management accounting concepts, providing a valuable resource for students seeking to understand and apply these principles.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.