Management Accounting for Cost and Control: In-Depth Analysis

VerifiedAdded on 2023/06/15

|16

|2063

|61

Report

AI Summary

This report provides a comprehensive overview of management accounting for cost and control, beginning with an explanation of Panopticism and its relevance to accounting practices. It details the functions of management accounting, including planning, controlling, and decision-making, and illustrates the use of checklists as a control device with the example of the Van Halen rock band. The report includes a manufacturing statement and income statement exercise, alongside discussions on perpetual inventory systems and overtime costs. It further contrasts traditional costing methods with activity-based costing (ABC), highlighting the advantages and disadvantages of each. Finally, the report concludes with a costing problem involving the allocation of service department costs.

Running head: MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Management Accounting for Cost and Control

Name of the Student

Name of the University

Name of the Author

Course ID

Management Accounting for Cost and Control

Name of the Student

Name of the University

Name of the Author

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................3

Answer to question 4:.................................................................................................................4

Answer to question 5:.................................................................................................................7

Answer to question A:................................................................................................................7

Answer to question B:................................................................................................................7

Answer to question 6:.................................................................................................................8

Answer to question 7:.................................................................................................................8

Answer to question 8:.................................................................................................................8

Answer to Part A:.......................................................................................................................8

Answer to part B:.......................................................................................................................9

Answer to Part C:.......................................................................................................................9

Answer to question 9:...............................................................................................................10

Answer to question 10:.............................................................................................................12

Reference List:.........................................................................................................................14

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................3

Answer to question 4:.................................................................................................................4

Answer to question 5:.................................................................................................................7

Answer to question A:................................................................................................................7

Answer to question B:................................................................................................................7

Answer to question 6:.................................................................................................................8

Answer to question 7:.................................................................................................................8

Answer to question 8:.................................................................................................................8

Answer to Part A:.......................................................................................................................8

Answer to part B:.......................................................................................................................9

Answer to Part C:.......................................................................................................................9

Answer to question 9:...............................................................................................................10

Answer to question 10:.............................................................................................................12

Reference List:.........................................................................................................................14

2MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Answer to question 1:

The term Panopticism is regarded as the social theory which is named after the French

philosopher Michel Foucault. The expression Panopticon can be defined as the experimental

laboratory of the power where an individual’s behaviour could be modified. The French

philosopher has viewed “panopticism” as the symbol of disciplinary society of surveillance.

Considering the example of Pannoticon it has increased the impact of surveillance in

the era of technology and it is regarded as the process of surveillance that possess the appeal

of culture (Salako & Yusuf, 2016). The growth in the visible data was given in the

organization and the individuals from the data mining tools. This has led to the development

of the surveillance of data which can address the mode of surveillance in indicating the

distant transactions source by taking account of the algorithmic manufacturing.

In respect to management accounting, Panopticism helps in maintaining the track of

accounting records together with the necessary figures (Lanen, 2016). Hence, Panopticism

assist in discovering the mistake and errors with adequate corrective measures to be taken for

modification to assure that the accounting process remains authentic.

Answer to question 2:

The functions of management accounting are as follows;

Planning: Planning as the function of management accounting refers to the short term and

long term formulation of plans and actions to attain a particular objective. A budget in the

financial planning illustrates how the resources are required to be acquired and used over the

specified period of time (Gitman et al., 2015). Management accounting is closely associated

with the planning since it helps in offering information for decision making and the overall

budget is developed around the accounting related reports.

Answer to question 1:

The term Panopticism is regarded as the social theory which is named after the French

philosopher Michel Foucault. The expression Panopticon can be defined as the experimental

laboratory of the power where an individual’s behaviour could be modified. The French

philosopher has viewed “panopticism” as the symbol of disciplinary society of surveillance.

Considering the example of Pannoticon it has increased the impact of surveillance in

the era of technology and it is regarded as the process of surveillance that possess the appeal

of culture (Salako & Yusuf, 2016). The growth in the visible data was given in the

organization and the individuals from the data mining tools. This has led to the development

of the surveillance of data which can address the mode of surveillance in indicating the

distant transactions source by taking account of the algorithmic manufacturing.

In respect to management accounting, Panopticism helps in maintaining the track of

accounting records together with the necessary figures (Lanen, 2016). Hence, Panopticism

assist in discovering the mistake and errors with adequate corrective measures to be taken for

modification to assure that the accounting process remains authentic.

Answer to question 2:

The functions of management accounting are as follows;

Planning: Planning as the function of management accounting refers to the short term and

long term formulation of plans and actions to attain a particular objective. A budget in the

financial planning illustrates how the resources are required to be acquired and used over the

specified period of time (Gitman et al., 2015). Management accounting is closely associated

with the planning since it helps in offering information for decision making and the overall

budget is developed around the accounting related reports.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Controlling: Controlling refers to the procedure of monitoring, measuring, assessing and

correcting the original results to make sure that the business enterprise goals and plans are

attained. The controlling functions of management accounting generates reports relating to

performance (Schaltegger & Zvezdov, 2015). These reports acts as the basis for taking into

the considerations the necessary actions of controlling operations.

Decision making: Decision making is regarded as the process of selecting among the

competing alternatives. Decision making forms the inherent part of each of the management

functions such as planning, organising and controlling. A manager would not be able to plan

without using the functions of control.

Answer to question 3:

Checklist can be defined as the list of all things that an individual is required to

consider or information that they want to discover or things an individual need to consider

somewhere to make sure that they do not forget anything (Schaltegger & Zvezdov, 2015).

According to Van Helen Rock Band checklist constitute the list of required things to

consider. They are helpful in imposing and controlling the control. As per the rock band, it is

regarded that checklist is vital tool of implementing control because it helps in making sure

that each person are engaged in the job are better able to understand the goals and complying

with the required process.

According to the statement by rock band they obtain advantage by using the checklist

because checklist as per the rock band is considered highly flexible to carry (Gitman et al.,

2015). The rock band with the help of checklist is better able to manage the consistency of

supply, inventories and they are usually considered as the element of time saving by adding

up the required records among the other things. As a result of this the checklist not only helps

in maintaining the necessary records but they are also needed for gaining success.

Controlling: Controlling refers to the procedure of monitoring, measuring, assessing and

correcting the original results to make sure that the business enterprise goals and plans are

attained. The controlling functions of management accounting generates reports relating to

performance (Schaltegger & Zvezdov, 2015). These reports acts as the basis for taking into

the considerations the necessary actions of controlling operations.

Decision making: Decision making is regarded as the process of selecting among the

competing alternatives. Decision making forms the inherent part of each of the management

functions such as planning, organising and controlling. A manager would not be able to plan

without using the functions of control.

Answer to question 3:

Checklist can be defined as the list of all things that an individual is required to

consider or information that they want to discover or things an individual need to consider

somewhere to make sure that they do not forget anything (Schaltegger & Zvezdov, 2015).

According to Van Helen Rock Band checklist constitute the list of required things to

consider. They are helpful in imposing and controlling the control. As per the rock band, it is

regarded that checklist is vital tool of implementing control because it helps in making sure

that each person are engaged in the job are better able to understand the goals and complying

with the required process.

According to the statement by rock band they obtain advantage by using the checklist

because checklist as per the rock band is considered highly flexible to carry (Gitman et al.,

2015). The rock band with the help of checklist is better able to manage the consistency of

supply, inventories and they are usually considered as the element of time saving by adding

up the required records among the other things. As a result of this the checklist not only helps

in maintaining the necessary records but they are also needed for gaining success.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING FOR COST AND CONTROL

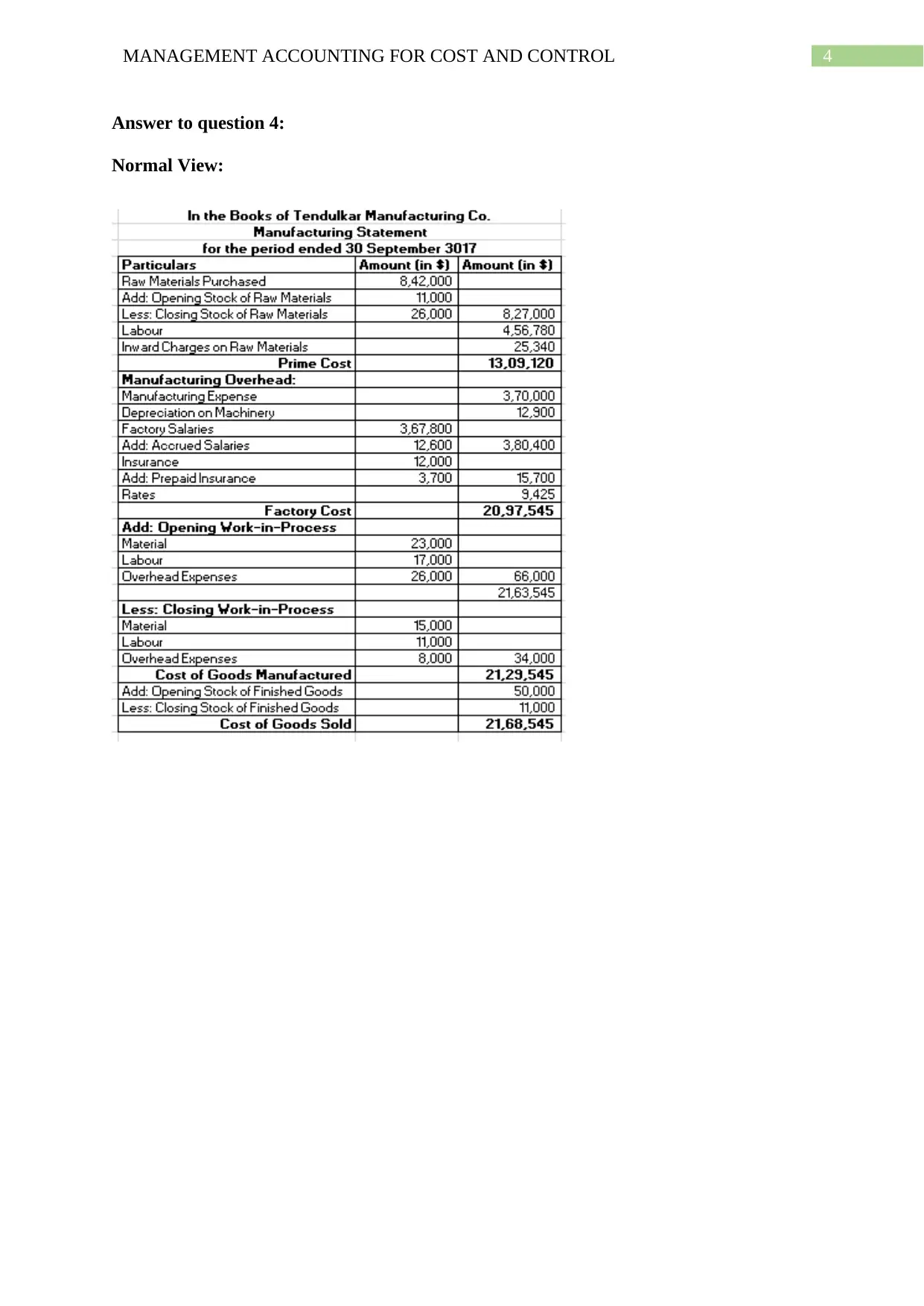

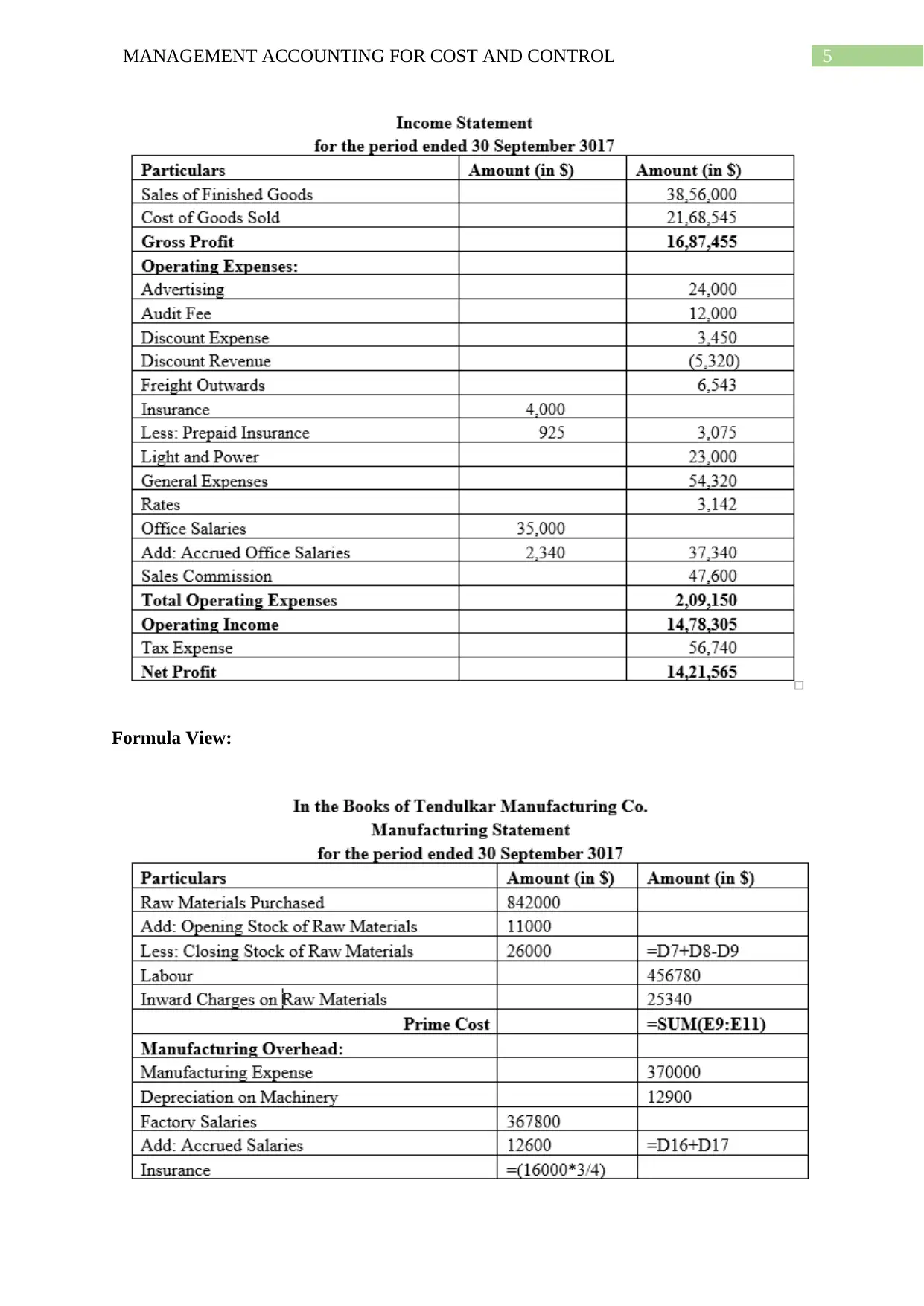

Answer to question 4:

Normal View:

Answer to question 4:

Normal View:

5MANAGEMENT ACCOUNTING FOR COST AND CONTROL

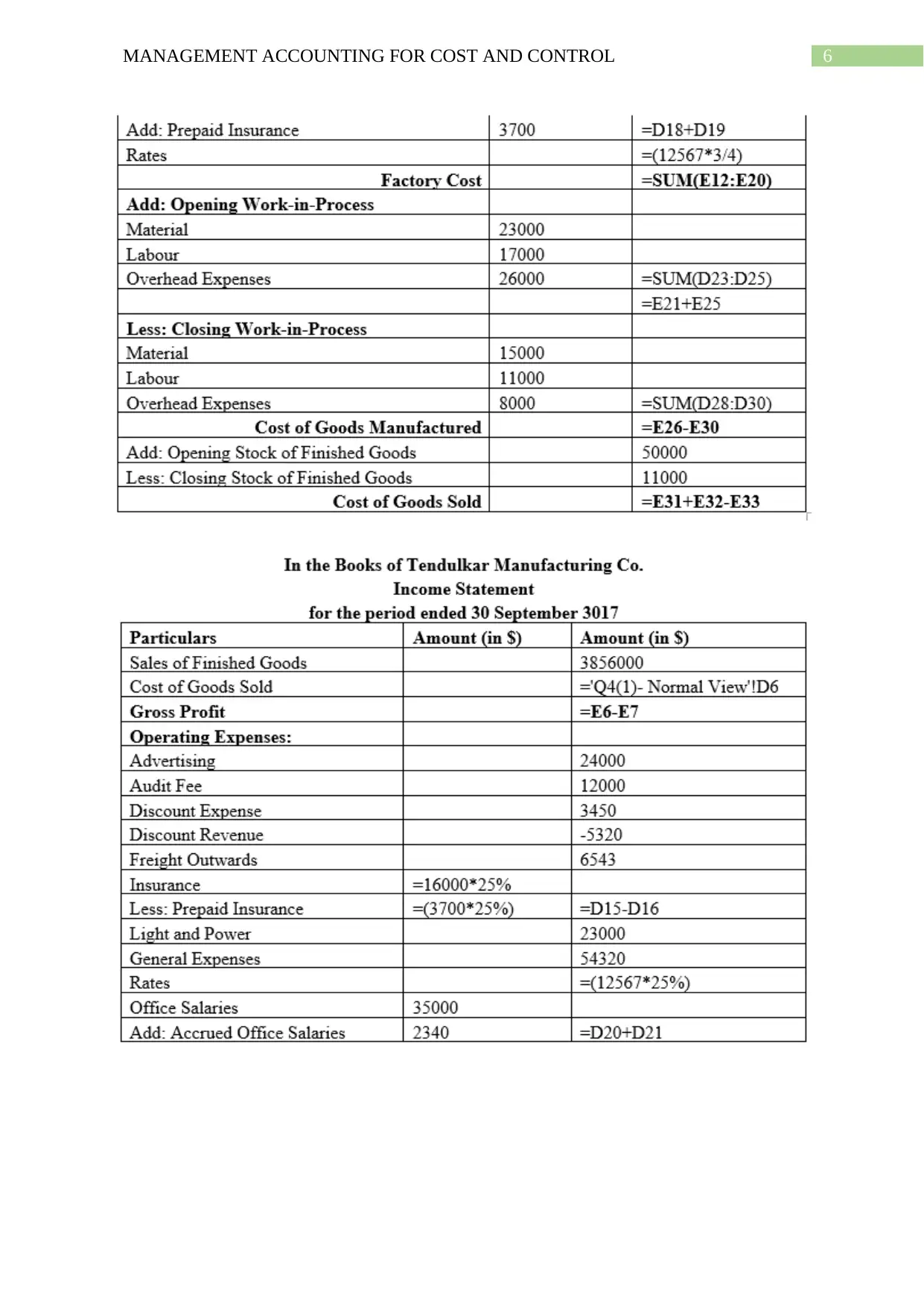

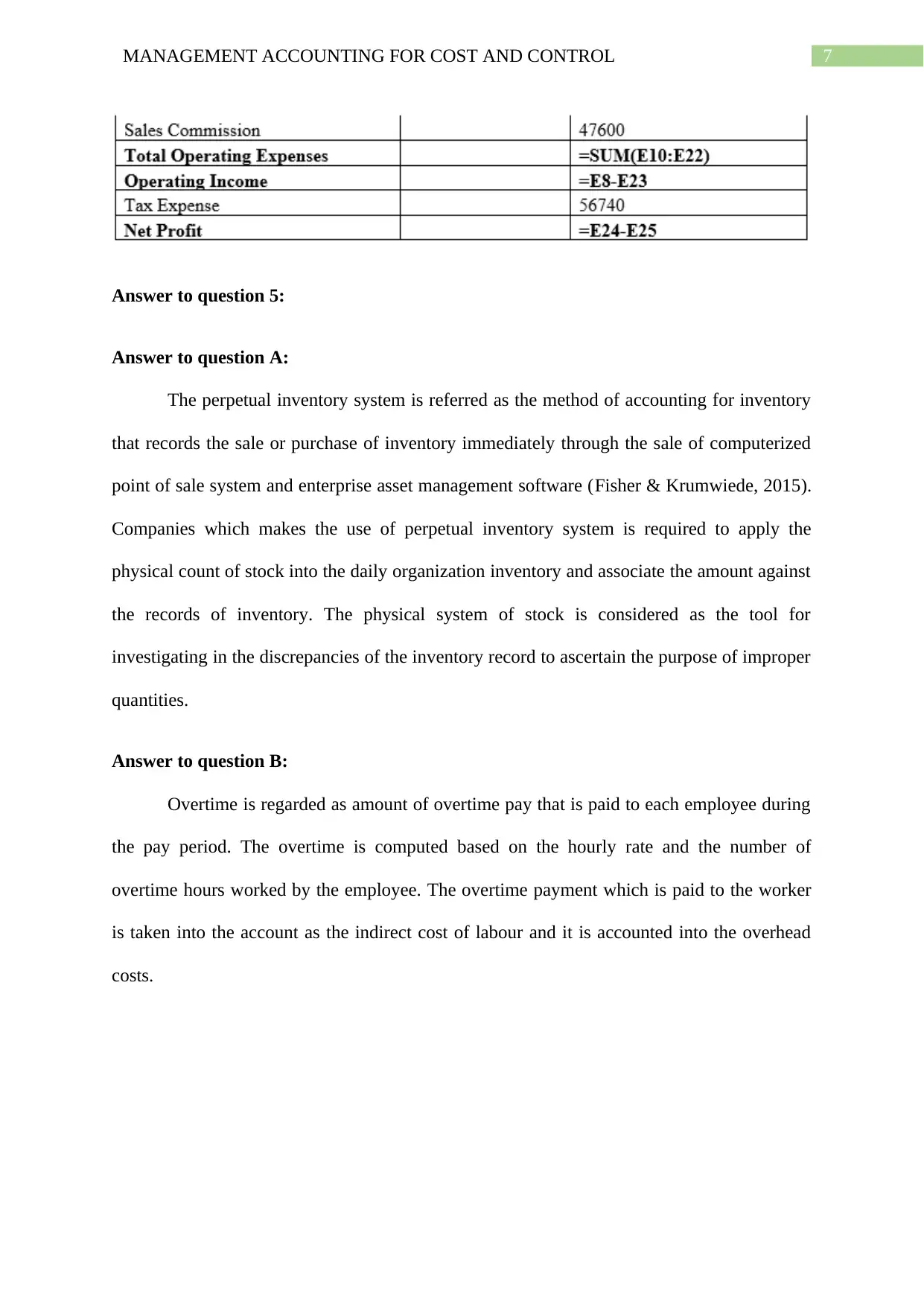

Formula View:

Formula View:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Answer to question 5:

Answer to question A:

The perpetual inventory system is referred as the method of accounting for inventory

that records the sale or purchase of inventory immediately through the sale of computerized

point of sale system and enterprise asset management software (Fisher & Krumwiede, 2015).

Companies which makes the use of perpetual inventory system is required to apply the

physical count of stock into the daily organization inventory and associate the amount against

the records of inventory. The physical system of stock is considered as the tool for

investigating in the discrepancies of the inventory record to ascertain the purpose of improper

quantities.

Answer to question B:

Overtime is regarded as amount of overtime pay that is paid to each employee during

the pay period. The overtime is computed based on the hourly rate and the number of

overtime hours worked by the employee. The overtime payment which is paid to the worker

is taken into the account as the indirect cost of labour and it is accounted into the overhead

costs.

Answer to question 5:

Answer to question A:

The perpetual inventory system is referred as the method of accounting for inventory

that records the sale or purchase of inventory immediately through the sale of computerized

point of sale system and enterprise asset management software (Fisher & Krumwiede, 2015).

Companies which makes the use of perpetual inventory system is required to apply the

physical count of stock into the daily organization inventory and associate the amount against

the records of inventory. The physical system of stock is considered as the tool for

investigating in the discrepancies of the inventory record to ascertain the purpose of improper

quantities.

Answer to question B:

Overtime is regarded as amount of overtime pay that is paid to each employee during

the pay period. The overtime is computed based on the hourly rate and the number of

overtime hours worked by the employee. The overtime payment which is paid to the worker

is taken into the account as the indirect cost of labour and it is accounted into the overhead

costs.

8MANAGEMENT ACCOUNTING FOR COST AND CONTROL

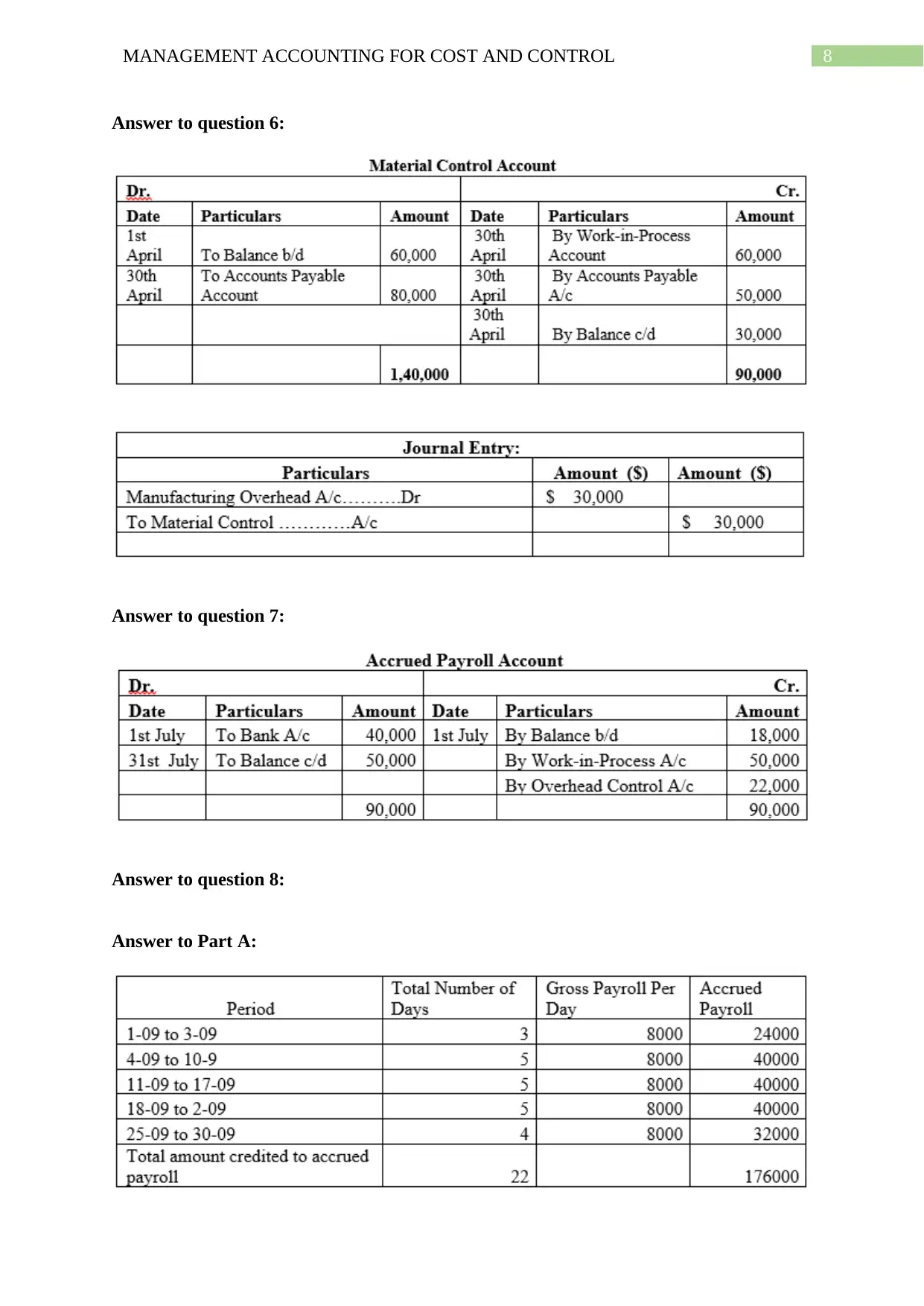

Answer to question 6:

Answer to question 7:

Answer to question 8:

Answer to Part A:

Answer to question 6:

Answer to question 7:

Answer to question 8:

Answer to Part A:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING FOR COST AND CONTROL

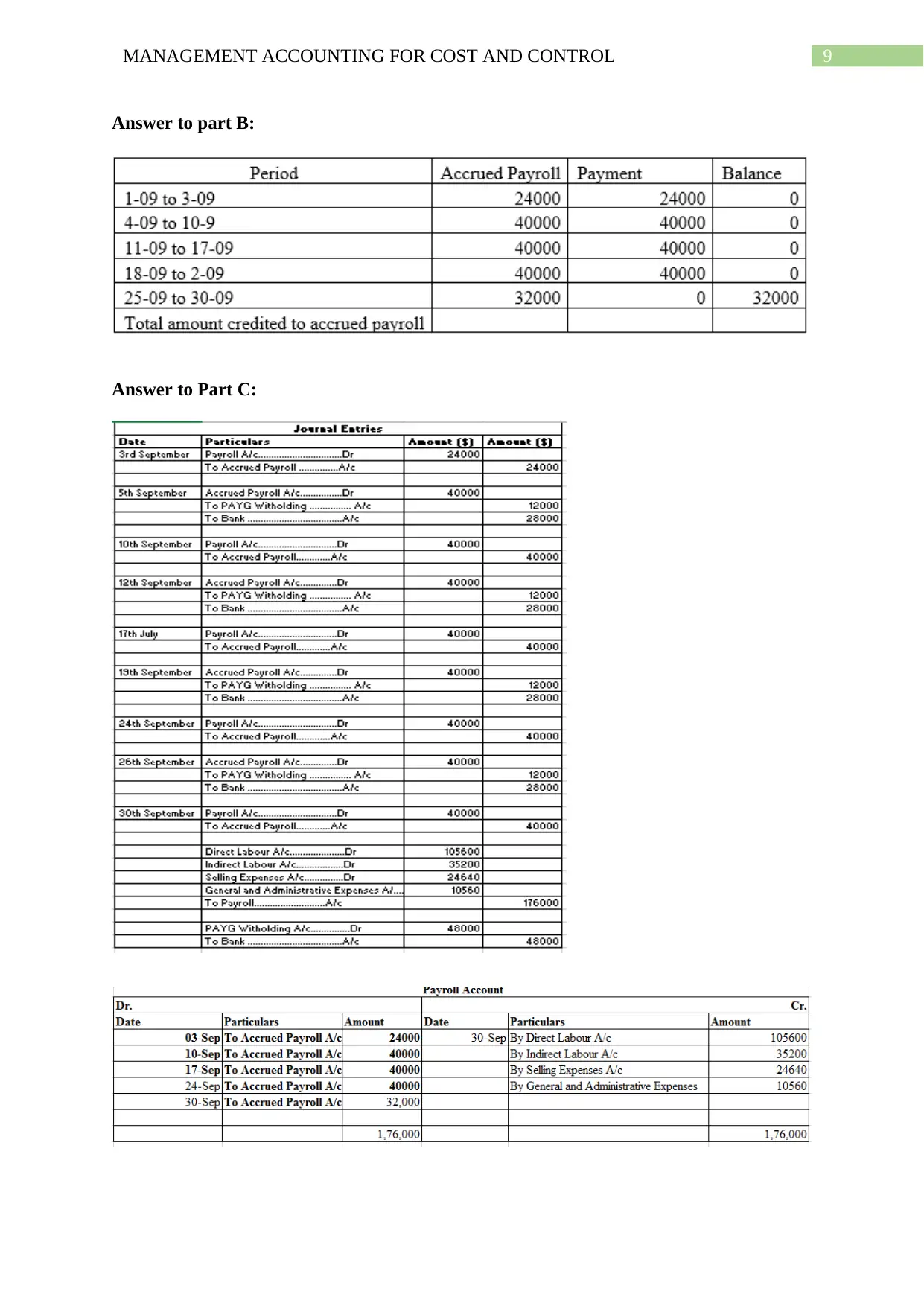

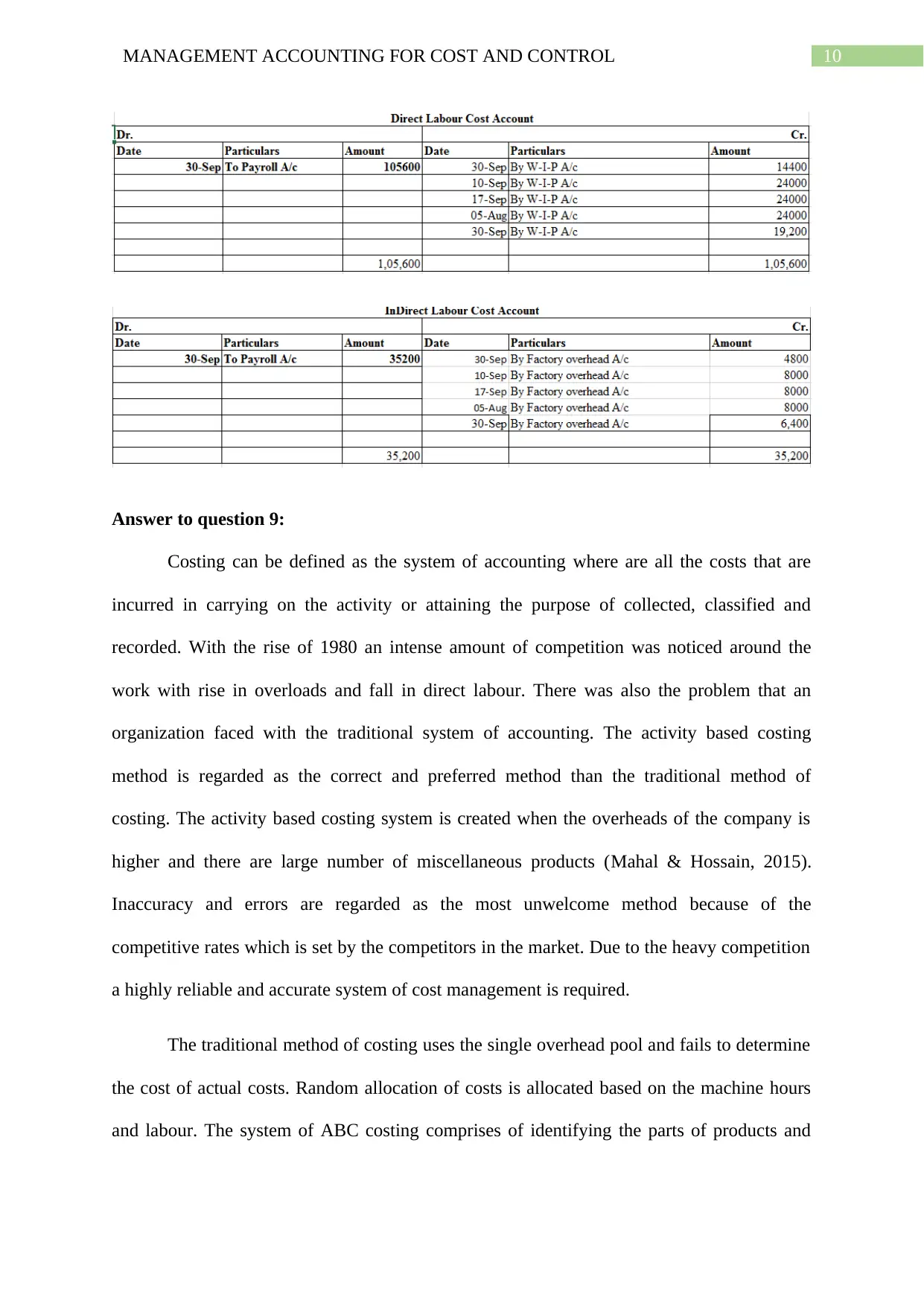

Answer to part B:

Answer to Part C:

Answer to part B:

Answer to Part C:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Answer to question 9:

Costing can be defined as the system of accounting where are all the costs that are

incurred in carrying on the activity or attaining the purpose of collected, classified and

recorded. With the rise of 1980 an intense amount of competition was noticed around the

work with rise in overloads and fall in direct labour. There was also the problem that an

organization faced with the traditional system of accounting. The activity based costing

method is regarded as the correct and preferred method than the traditional method of

costing. The activity based costing system is created when the overheads of the company is

higher and there are large number of miscellaneous products (Mahal & Hossain, 2015).

Inaccuracy and errors are regarded as the most unwelcome method because of the

competitive rates which is set by the competitors in the market. Due to the heavy competition

a highly reliable and accurate system of cost management is required.

The traditional method of costing uses the single overhead pool and fails to determine

the cost of actual costs. Random allocation of costs is allocated based on the machine hours

and labour. The system of ABC costing comprises of identifying the parts of products and

Answer to question 9:

Costing can be defined as the system of accounting where are all the costs that are

incurred in carrying on the activity or attaining the purpose of collected, classified and

recorded. With the rise of 1980 an intense amount of competition was noticed around the

work with rise in overloads and fall in direct labour. There was also the problem that an

organization faced with the traditional system of accounting. The activity based costing

method is regarded as the correct and preferred method than the traditional method of

costing. The activity based costing system is created when the overheads of the company is

higher and there are large number of miscellaneous products (Mahal & Hossain, 2015).

Inaccuracy and errors are regarded as the most unwelcome method because of the

competitive rates which is set by the competitors in the market. Due to the heavy competition

a highly reliable and accurate system of cost management is required.

The traditional method of costing uses the single overhead pool and fails to determine

the cost of actual costs. Random allocation of costs is allocated based on the machine hours

and labour. The system of ABC costing comprises of identifying the parts of products and

11MANAGEMENT ACCOUNTING FOR COST AND CONTROL

labour whereas the traditional method of cost accounting randomly accumulates the

expenditure, salaries and depreciation.

The targeted costs that is created on the activities are calculated through activity based

costing. The activity based costing is considered to be the advantageous since it helps in

simplifying the procedure of decision making and uses the concept of management that is

target oriented (Fisher & Krumwiede, 2015). The activity based costing system helps in

determining the performance and setting out the standards that assists the managers in using

the information for enabling comparative study.

In the traditional costing, an organization ascertains the cost of productions after the

production of budgets whereas under the activity based costing system the product value is

determined depending upon the feedback of customers (Otley, 2016). The activity based

costing helps in ascertaining whether the company is able to reduce or increase the cost of

activity to get the customers. The costing system helps in keeping up with the competitors

without making a sacrifice in the quality and quantity of products.

The activity based costing assist the company in developing the strategy long run

strategies and competitive advantage by emphasising on the activities. The activity based

costing system makes the use of cost recognition elements that is selected with direct costs

and costs related with products.

Though there are benefits for ABC system of costing but there are arguments against

the ABC system of costing in the areas of cost allocation. With the availability of data there

are certain costs that needs allocation to department and product allocation (Eldenburg et al.,

2016). This give rise to cost that may on certain occasion be considered possible.

Conclusively, the traditional system of costing is not as accurate as the ABC system of

labour whereas the traditional method of cost accounting randomly accumulates the

expenditure, salaries and depreciation.

The targeted costs that is created on the activities are calculated through activity based

costing. The activity based costing is considered to be the advantageous since it helps in

simplifying the procedure of decision making and uses the concept of management that is

target oriented (Fisher & Krumwiede, 2015). The activity based costing system helps in

determining the performance and setting out the standards that assists the managers in using

the information for enabling comparative study.

In the traditional costing, an organization ascertains the cost of productions after the

production of budgets whereas under the activity based costing system the product value is

determined depending upon the feedback of customers (Otley, 2016). The activity based

costing helps in ascertaining whether the company is able to reduce or increase the cost of

activity to get the customers. The costing system helps in keeping up with the competitors

without making a sacrifice in the quality and quantity of products.

The activity based costing assist the company in developing the strategy long run

strategies and competitive advantage by emphasising on the activities. The activity based

costing system makes the use of cost recognition elements that is selected with direct costs

and costs related with products.

Though there are benefits for ABC system of costing but there are arguments against

the ABC system of costing in the areas of cost allocation. With the availability of data there

are certain costs that needs allocation to department and product allocation (Eldenburg et al.,

2016). This give rise to cost that may on certain occasion be considered possible.

Conclusively, the traditional system of costing is not as accurate as the ABC system of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.