ACCT6004 Management Accounting Case Study: Costing & Profitability

VerifiedAdded on 2023/05/30

|25

|3789

|383

Case Study

AI Summary

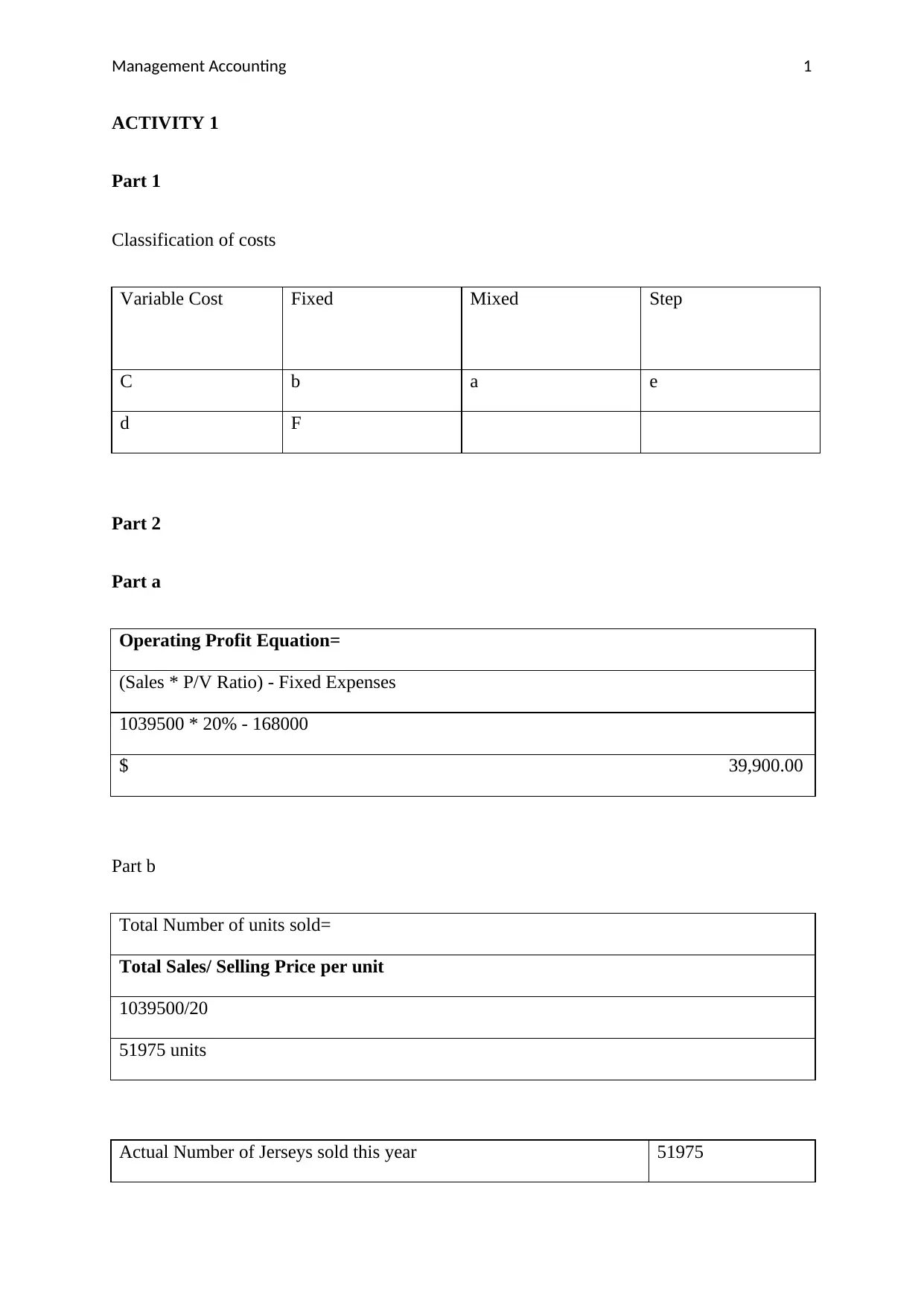

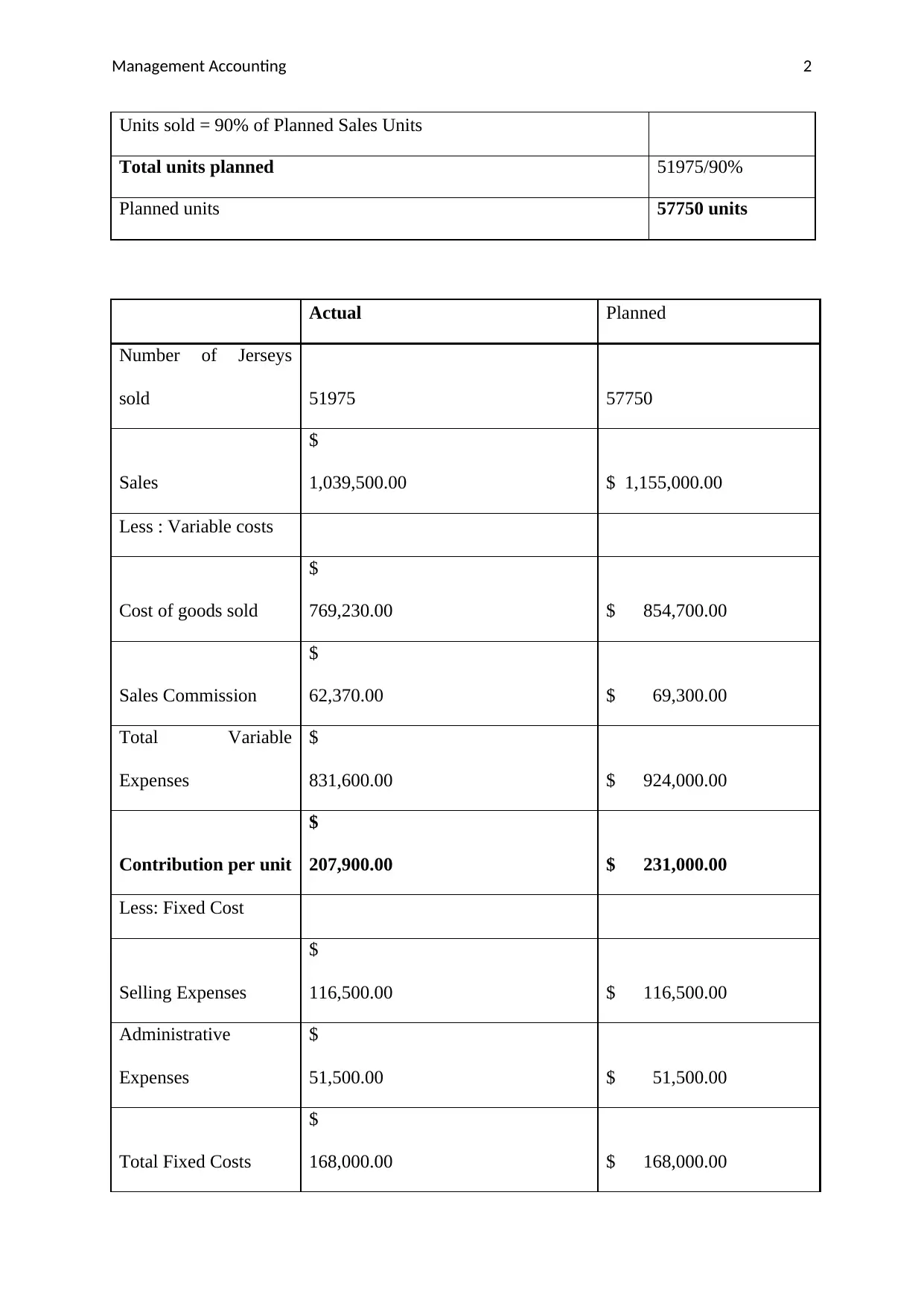

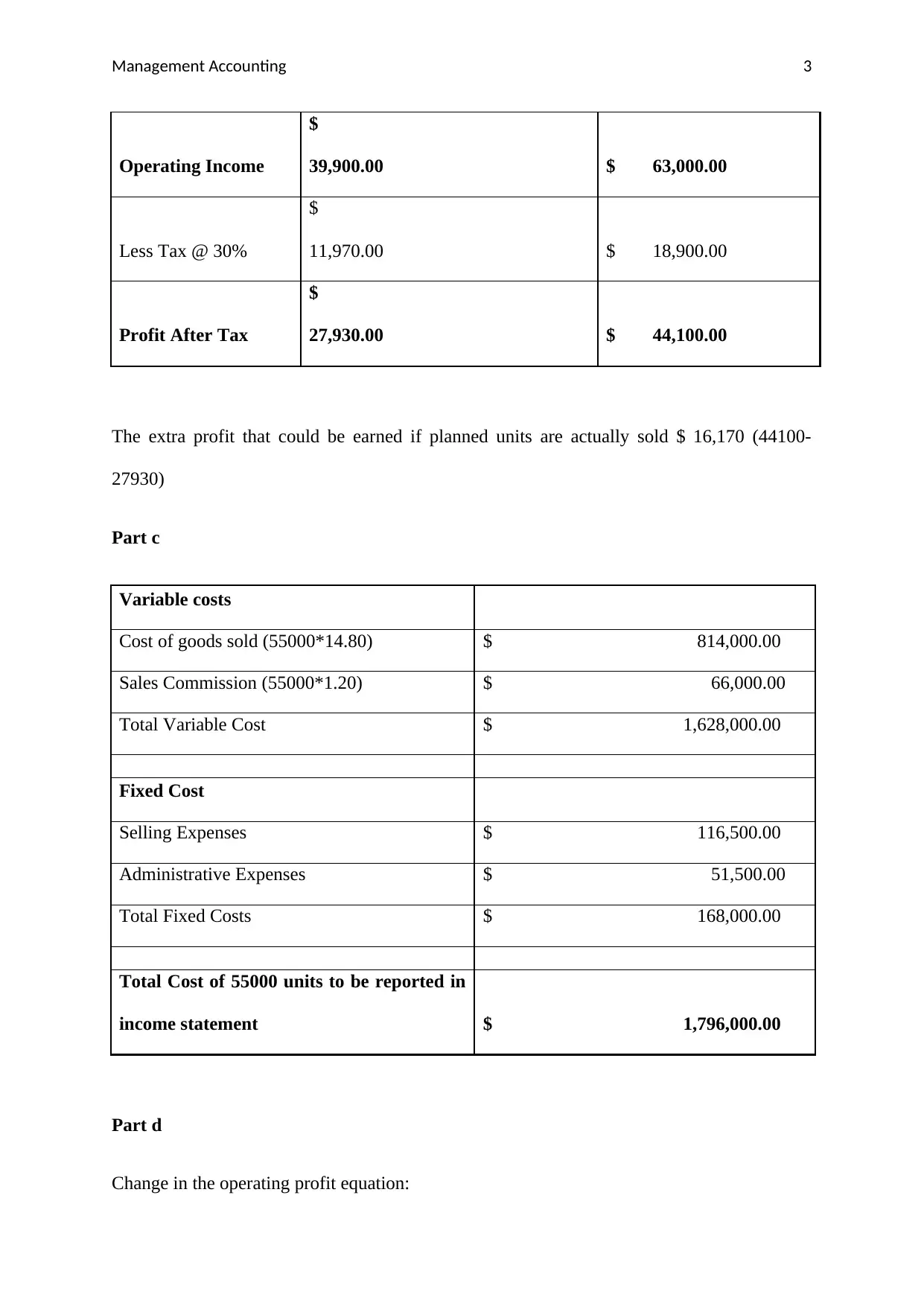

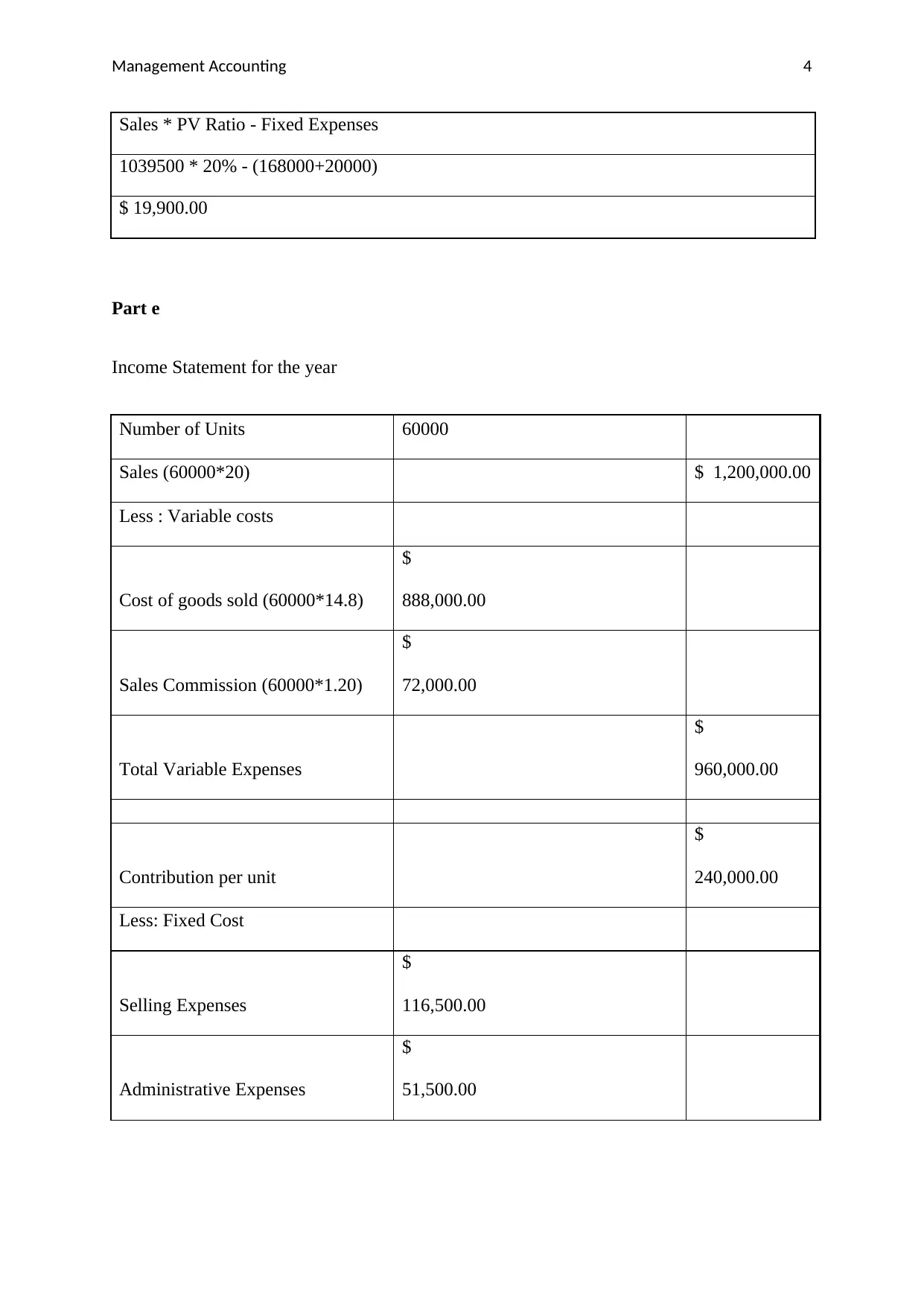

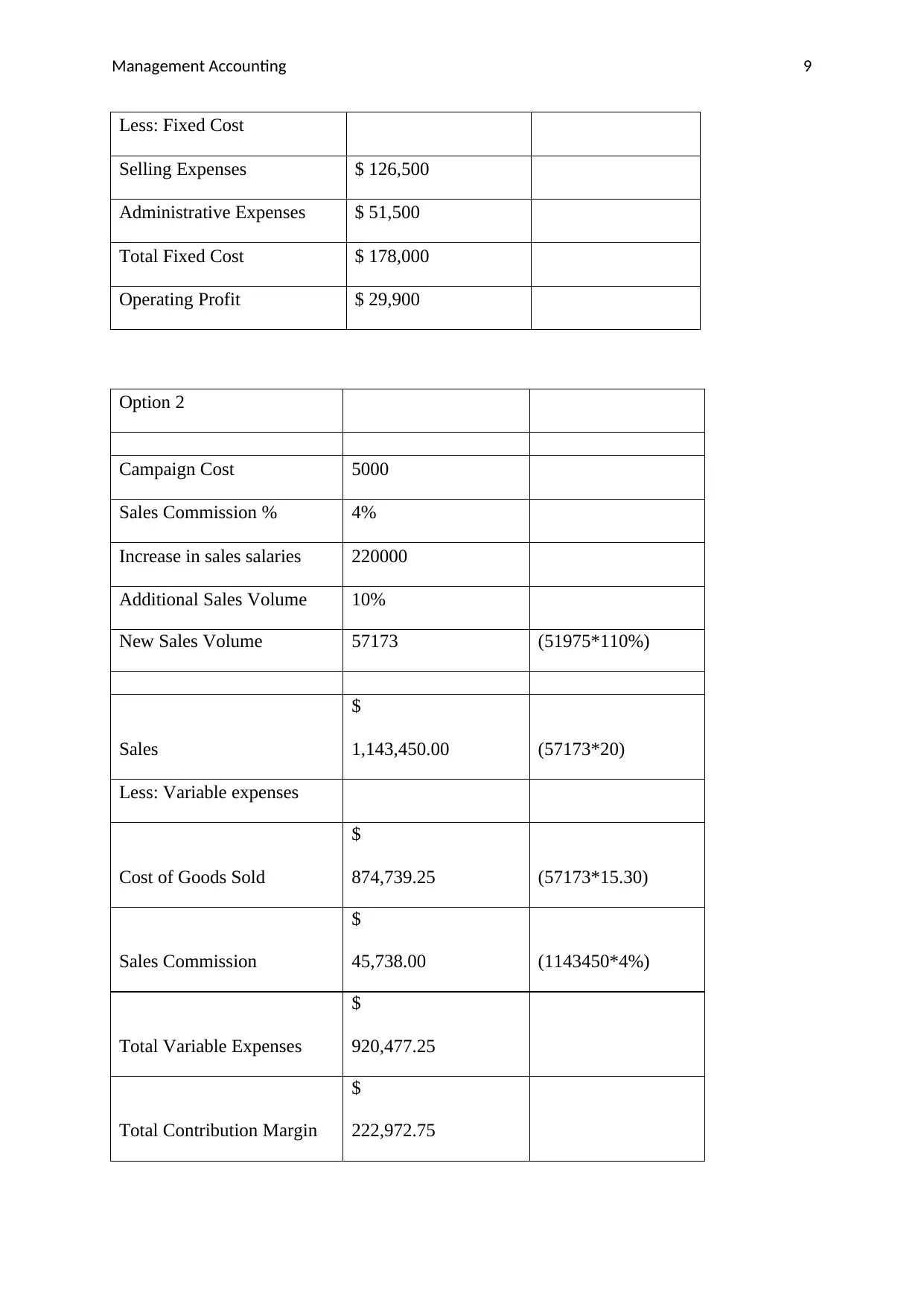

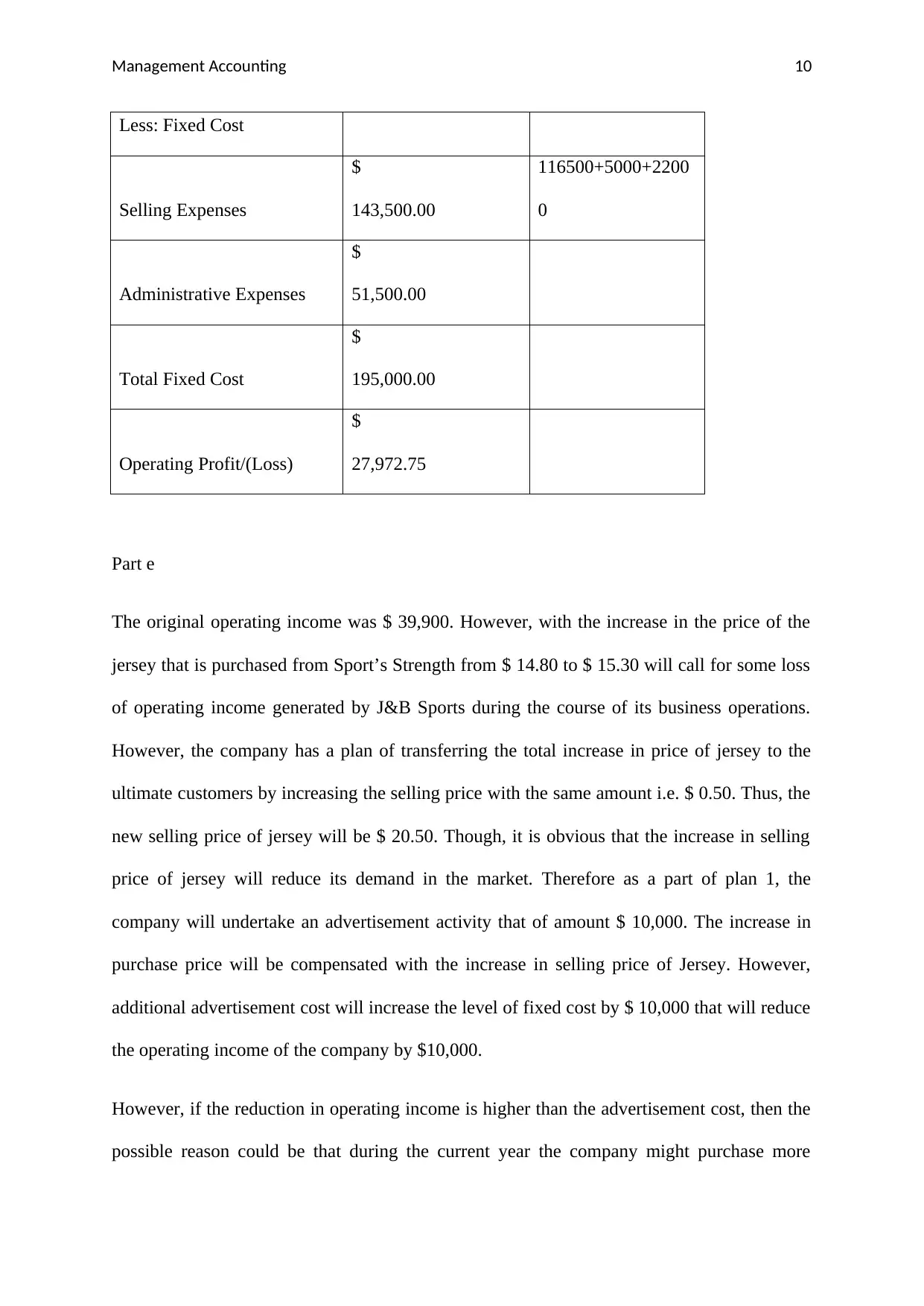

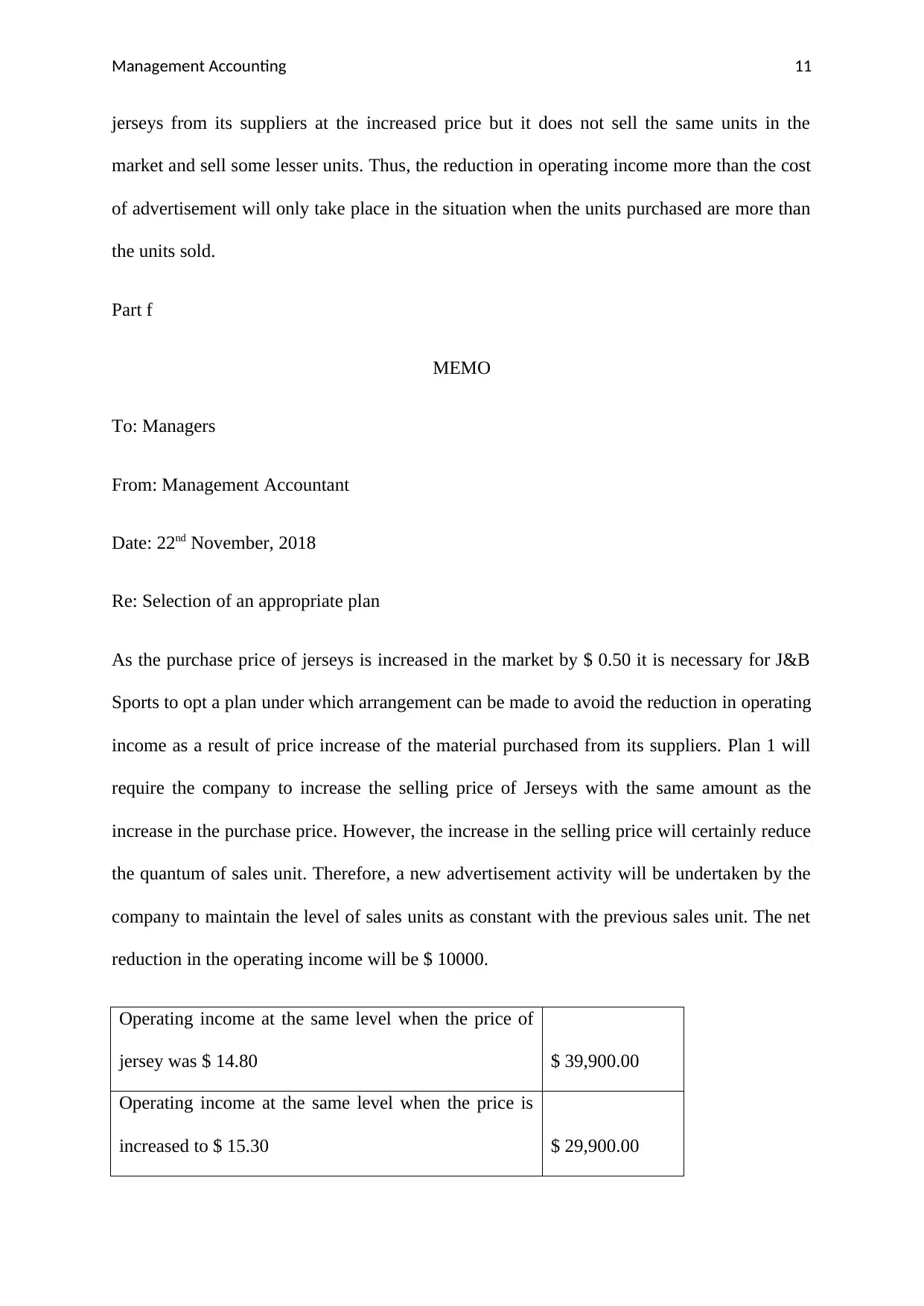

This document presents a comprehensive solution to a management accounting case study. It includes cost classifications (variable, fixed, mixed, and step costs), profit analysis using the operating profit equation, break-even point calculations, margin of safety analysis, and an evaluation of different strategic options involving pricing and advertising campaigns. The analysis extends to income statement preparation, cost of goods manufactured, and gross profit calculations under various scenarios. Recommendations are provided based on the financial analysis, focusing on maximizing profitability and optimizing cost management strategies. The document also highlights the importance of cost behavior and contribution margin analysis in making informed business decisions. This resource is ideal for students studying management accounting and seeking practical application of key concepts.

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.