HA2011 Management Accounting: Costing Systems, Analysis & Decisions

VerifiedAdded on 2023/03/23

|13

|4110

|61

Report

AI Summary

This management accounting report delves into the application of cost concepts across various costing systems, justifying the selection of these systems, and critically evaluating accounting information for informed decision-making and the attainment of business objectives. It includes a value chain analysis of Reliance Worldwide Corporation, identifying value-adding activities such as sales, marketing, and technology development. The report links theoretical concepts with real-world scenarios, emphasizing the importance of sales and marketing in generating revenue and the role of technology in enhancing efficiency across the value chain. This document is available on Desklib, a platform offering a wide array of study tools and resources for students.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Table of Contents

Question 1:.........................................................................................................................2

Requirement a:...............................................................................................................2

Requirement b:...............................................................................................................3

Part i:..........................................................................................................................3

Part ii:..........................................................................................................................3

Part iii:.........................................................................................................................4

Part iv:.........................................................................................................................5

Part v:.........................................................................................................................6

Question 2:.........................................................................................................................7

Requirement a:...............................................................................................................7

Requirement b:...............................................................................................................7

Requirement c:...............................................................................................................7

Requirement d:...............................................................................................................7

Requirement e:...............................................................................................................8

Question 3:.........................................................................................................................8

Requirement a:...............................................................................................................8

Requirement b:...............................................................................................................8

Requirement c:...............................................................................................................9

References:......................................................................................................................11

Table of Contents

Question 1:.........................................................................................................................2

Requirement a:...............................................................................................................2

Requirement b:...............................................................................................................3

Part i:..........................................................................................................................3

Part ii:..........................................................................................................................3

Part iii:.........................................................................................................................4

Part iv:.........................................................................................................................5

Part v:.........................................................................................................................6

Question 2:.........................................................................................................................7

Requirement a:...............................................................................................................7

Requirement b:...............................................................................................................7

Requirement c:...............................................................................................................7

Requirement d:...............................................................................................................7

Requirement e:...............................................................................................................8

Question 3:.........................................................................................................................8

Requirement a:...............................................................................................................8

Requirement b:...............................................................................................................8

Requirement c:...............................................................................................................9

References:......................................................................................................................11

2MANAGEMENT ACCOUNTING

Question 1:

Requirement a:

A value chain could be defined as a business model, which explains the entire

group of activities required to develop a product or service. For organisations

manufacturing products, value chain includes the steps, which involve bringing a

product from conception to distribution like procurement of raw materials, marketing

activities and manufacturing functions (Bettis et al. 2014). Value chain analysis is

conducted by analysing the detailed processes involved in each step of the business.

The objective of this analysis is to raise the efficiency of production in order to ensure

delivery of maximum value for the organisation at the lowest possible cost.

Owing to the growing competition for unbeatable prices, customer loyalty and

exceptional products, it is necessary for the business organisations to investigate value

continuously that they develop for retaining their competitive edge in the market

(Bornemann and Wiedenhofer 2014). With the help of value chain, an organisation

could discern certain business areas, which are inefficient and accordingly, strategies

could be implemented that would optimise the procedures for maximum profitability and

efficiency. Along with ensuring the seamlessness and efficiency of production

mechanism, it is crucial for an organisation to ensure the security and confidence of its

customers for maintaining their loyalty as well. Value chain analysis assists in

maintaining customer loyalty as well.

There are two ways through which the value chain concept provides benefit to

the business organisations and they are demonstrated briefly as follows:

Identification of sources pertaining to competitive advantage:

With the help of conduction of value chain analysis, it becomes possible for any

business organisation during the planning process to identify the probable sources of

competitive advantage. The organisation is an accumulation of various activities, which

share association to a certain extent. It is not possible for any organisation to trade all

activities in the outside market (Darmawan, Putra and Wiguna 2014). According to the

approach of the value chain, an organisation could take into account such activities as

the sources of economic rent. The activities could act in the form of impediments to the

new entrants or they could cause cost drawbacks to the customers.

Enhanced flow of information materials and finances:

With the help of enhanced information flow, it becomes possible for the

organisation to detect as well as exploit new opportunities along with minimisation of

external threats. The continual evaluation of the value chain could lead to timely fill of

significant gaps, which might influence the productivity of an organisation. Moreover,

when an organisation makes sound enforcement of the value chain analysis, material

and product flow could be enhanced owing to improved sales and demand forecasting.

Furthermore, there could be enhancement in inventory management as well, as delays

could be reduced by tracking activities across the supply chain (El-Sayed, Dickson and

El-Naggar 2015).

The modern customers provide increased importance to quick response along

with convenient access to the significant product-related information. The unanticipated

interruption in the flow of information could have impact on the relationship between the

suppliers and the customers. With the help of value chain analysis and by implementing

Question 1:

Requirement a:

A value chain could be defined as a business model, which explains the entire

group of activities required to develop a product or service. For organisations

manufacturing products, value chain includes the steps, which involve bringing a

product from conception to distribution like procurement of raw materials, marketing

activities and manufacturing functions (Bettis et al. 2014). Value chain analysis is

conducted by analysing the detailed processes involved in each step of the business.

The objective of this analysis is to raise the efficiency of production in order to ensure

delivery of maximum value for the organisation at the lowest possible cost.

Owing to the growing competition for unbeatable prices, customer loyalty and

exceptional products, it is necessary for the business organisations to investigate value

continuously that they develop for retaining their competitive edge in the market

(Bornemann and Wiedenhofer 2014). With the help of value chain, an organisation

could discern certain business areas, which are inefficient and accordingly, strategies

could be implemented that would optimise the procedures for maximum profitability and

efficiency. Along with ensuring the seamlessness and efficiency of production

mechanism, it is crucial for an organisation to ensure the security and confidence of its

customers for maintaining their loyalty as well. Value chain analysis assists in

maintaining customer loyalty as well.

There are two ways through which the value chain concept provides benefit to

the business organisations and they are demonstrated briefly as follows:

Identification of sources pertaining to competitive advantage:

With the help of conduction of value chain analysis, it becomes possible for any

business organisation during the planning process to identify the probable sources of

competitive advantage. The organisation is an accumulation of various activities, which

share association to a certain extent. It is not possible for any organisation to trade all

activities in the outside market (Darmawan, Putra and Wiguna 2014). According to the

approach of the value chain, an organisation could take into account such activities as

the sources of economic rent. The activities could act in the form of impediments to the

new entrants or they could cause cost drawbacks to the customers.

Enhanced flow of information materials and finances:

With the help of enhanced information flow, it becomes possible for the

organisation to detect as well as exploit new opportunities along with minimisation of

external threats. The continual evaluation of the value chain could lead to timely fill of

significant gaps, which might influence the productivity of an organisation. Moreover,

when an organisation makes sound enforcement of the value chain analysis, material

and product flow could be enhanced owing to improved sales and demand forecasting.

Furthermore, there could be enhancement in inventory management as well, as delays

could be reduced by tracking activities across the supply chain (El-Sayed, Dickson and

El-Naggar 2015).

The modern customers provide increased importance to quick response along

with convenient access to the significant product-related information. The unanticipated

interruption in the flow of information could have impact on the relationship between the

suppliers and the customers. With the help of value chain analysis and by implementing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

the same, an organisation could identify and eliminate the bottlenecks to the flow of

information (Harding 2017).

Requirement b:

For this section, Reliance Worldwide Corporation is an Australian organisation,

which is involved in producing materials in order to plumb solutions as well as water

control systems. The organisation has presence in UK, USA and other parts of Europe.

In addition, there is export of plumbing products to few Asian nations.

Part i:

Reliance Worldwide Corporation is involved in exporting plumbing products to

few Asian nations (Rwc.com 2019). The organisation provides a group of values in

order to control pressure, temperature, thermostatic and isolating water for industrial

and domestic pipelines. It holds above 700 patents on plumbing solutions, since the

organisation is operating in the sector for above 100 years. Furthermore, the business

of the organisation offers other ancillary as well as conventional plumbing fittings to the

Australian customers.

The mission statement of an organisation describes the major priorities of an

organisation (Jenkins and Williamson 2015). Reliance Worldwide Corporation intends to

be the most increasingly valued business in the eyes of the customers it serves, the

community where it operates and the committed and loyal colleagues and shareholders.

On the other hand, the objective of Reliance Worldwide Corporation is to maintain the

loyal customers by providing superior quality products to its customers at competitive

prices. At the time of offering the products, the organisation takes into consideration

significant issues like hygiene, health, animal welfare, safety and support to the

community welfare and environmental protection.

Part ii:

One of the significant advantages of Reliance Worldwide Corporation is its vast

range of products, which assists in valve control, the innovation in plumbing fittings like

push-to-connect fittings as well as conventional products in plumbing fittings. The

business has delivered plumbing solution to the Australian customers for above 67

years with different kinds of pipe fittings and valves. The organisation is involved in

offering different products such as controlling valve for hot water as well as cold water.

In addition, the instant fittings of socket for copper, flex and other pipes have assisted in

the generation of unique competitive edge over its rivals. As a result, this product results

in creation of value for both industrial and domestic customers through minimisation of

the installation time and labour cost in terms of fitting two pipes. Moreover, this product

possesses the ability of offering a solution in order to minimise the installation cost and

thus, this cost leadership and differentiation strategy of the organisation has assisted in

gaining competitive edge in the market.

It is possible for the retail customers to fit the water pipes in their houses with

bare hands with the usage of push-to-connect fittings. Along with this, Reliance

Worldwide Corporation has strong channel of distribution in USA by entering into long-

term contract with Lowe’s Companies Inc. Reliance Worldwide Corporation has entered

the European market owing to the uncertainties in the US taxation regulations

the same, an organisation could identify and eliminate the bottlenecks to the flow of

information (Harding 2017).

Requirement b:

For this section, Reliance Worldwide Corporation is an Australian organisation,

which is involved in producing materials in order to plumb solutions as well as water

control systems. The organisation has presence in UK, USA and other parts of Europe.

In addition, there is export of plumbing products to few Asian nations.

Part i:

Reliance Worldwide Corporation is involved in exporting plumbing products to

few Asian nations (Rwc.com 2019). The organisation provides a group of values in

order to control pressure, temperature, thermostatic and isolating water for industrial

and domestic pipelines. It holds above 700 patents on plumbing solutions, since the

organisation is operating in the sector for above 100 years. Furthermore, the business

of the organisation offers other ancillary as well as conventional plumbing fittings to the

Australian customers.

The mission statement of an organisation describes the major priorities of an

organisation (Jenkins and Williamson 2015). Reliance Worldwide Corporation intends to

be the most increasingly valued business in the eyes of the customers it serves, the

community where it operates and the committed and loyal colleagues and shareholders.

On the other hand, the objective of Reliance Worldwide Corporation is to maintain the

loyal customers by providing superior quality products to its customers at competitive

prices. At the time of offering the products, the organisation takes into consideration

significant issues like hygiene, health, animal welfare, safety and support to the

community welfare and environmental protection.

Part ii:

One of the significant advantages of Reliance Worldwide Corporation is its vast

range of products, which assists in valve control, the innovation in plumbing fittings like

push-to-connect fittings as well as conventional products in plumbing fittings. The

business has delivered plumbing solution to the Australian customers for above 67

years with different kinds of pipe fittings and valves. The organisation is involved in

offering different products such as controlling valve for hot water as well as cold water.

In addition, the instant fittings of socket for copper, flex and other pipes have assisted in

the generation of unique competitive edge over its rivals. As a result, this product results

in creation of value for both industrial and domestic customers through minimisation of

the installation time and labour cost in terms of fitting two pipes. Moreover, this product

possesses the ability of offering a solution in order to minimise the installation cost and

thus, this cost leadership and differentiation strategy of the organisation has assisted in

gaining competitive edge in the market.

It is possible for the retail customers to fit the water pipes in their houses with

bare hands with the usage of push-to-connect fittings. Along with this, Reliance

Worldwide Corporation has strong channel of distribution in USA by entering into long-

term contract with Lowe’s Companies Inc. Reliance Worldwide Corporation has entered

the European market owing to the uncertainties in the US taxation regulations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

Administrative, Finance infrastructureLegal, Accounting, Financial Management

Human Resource ManagementPersonnel, Key Recruitment, Training, Staff Planning

Product and Technology DevelopmentProduct and Process Design, Production Engineering, Market Testing

ProcurementSupplier Management, Subcontracting, Funding, Specification

Inbound Logistics

Quality control, receiving, raw material control, supply schedules

Operations

Packaging, manufacturing, production control, maintenance, quality control

Outbound Logistics

Customer management, order taking, sales analysis, promotion, market research

Sales and Marketing

Finished goods, order handling, dispatch, delivery, invoicing

Servicing

Warranty, maintenance, training and education services

Support Activites

Primary Activities

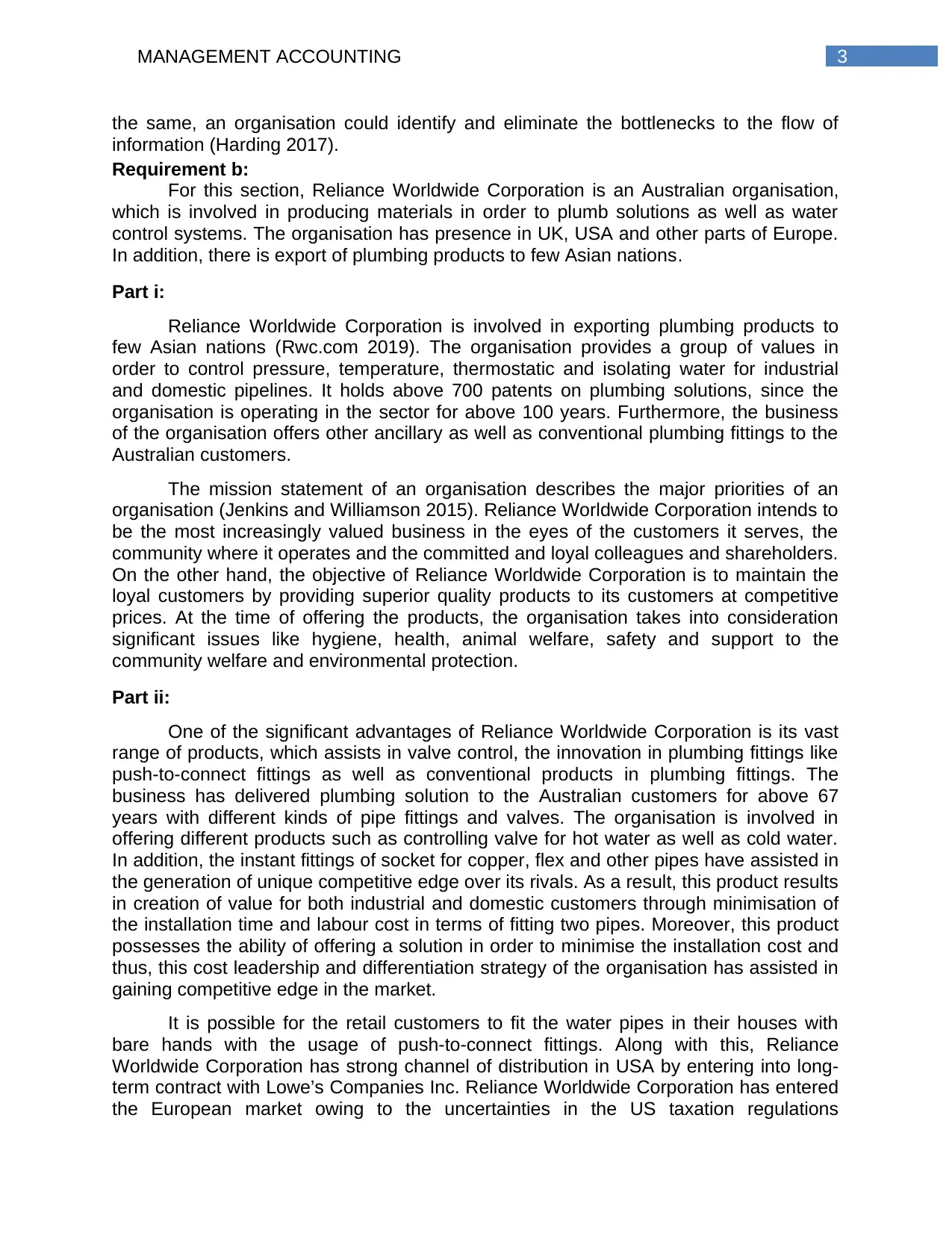

(Rwc.com 2019). The marketing strategy of the organisation in entering a new rich

community is timed perfectly in order to increase the overall market share. It is involved

in offering integrated solutions to the customers through the sale of meters, backflow

valves and mains. In addition, it produces conventional fittings of brass plumbing in

Australia via screwed, compression and capillary design. The industrial solution of the

organisation has gathered the marketing policy to sell the products via Tubefit in

Australia and Titon in New Zealand.

Part iii:

Figure 1: Value chain model of Reliance Worldwide Corporation

Pr

ofi

t

m

ar

gi

n

Administrative, Finance infrastructureLegal, Accounting, Financial Management

Human Resource ManagementPersonnel, Key Recruitment, Training, Staff Planning

Product and Technology DevelopmentProduct and Process Design, Production Engineering, Market Testing

ProcurementSupplier Management, Subcontracting, Funding, Specification

Inbound Logistics

Quality control, receiving, raw material control, supply schedules

Operations

Packaging, manufacturing, production control, maintenance, quality control

Outbound Logistics

Customer management, order taking, sales analysis, promotion, market research

Sales and Marketing

Finished goods, order handling, dispatch, delivery, invoicing

Servicing

Warranty, maintenance, training and education services

Support Activites

Primary Activities

(Rwc.com 2019). The marketing strategy of the organisation in entering a new rich

community is timed perfectly in order to increase the overall market share. It is involved

in offering integrated solutions to the customers through the sale of meters, backflow

valves and mains. In addition, it produces conventional fittings of brass plumbing in

Australia via screwed, compression and capillary design. The industrial solution of the

organisation has gathered the marketing policy to sell the products via Tubefit in

Australia and Titon in New Zealand.

Part iii:

Figure 1: Value chain model of Reliance Worldwide Corporation

Pr

ofi

t

m

ar

gi

n

5MANAGEMENT ACCOUNTING

(Source: Rwc.com 2019)

Part iv:

The two value-adding activities that have been chosen from the value chain

model of Reliance Worldwide Corporation mainly include sales and marketing from

primary activities and technology from the secondary activities. The brief evaluation of

these activities in the context of the concerned organisation is provided as follows:

Sales and marketing:

In this stage, it is necessary for Reliance Worldwide Corporation to shed light on

the advantages and points of differentiation of the provided products for persuading the

customers to show the superiority of its products compared to those of the competitors

(Jung 2014). Thus, providing superior quality products at reasonable prices and

differentiated features could not form value until the organisation decides to spend on

sales and marketing activities. The roles of the marketers and the sales agents are

deemed to be a crucial aspect in this case.

Some instances of sales and marketing activities in Reliance Worldwide

Corporation constitute of sales force, promotional activities, selection of channels,

advertising, developing and quoting relations with the members of the channels. The

organisation could utilise the approach of marketing funnel so that it could structure its

sales and marketing activities accordingly (Mohajeri et al. 2014). The marketing policies

could be either pull or push in nature based on the objectives, competitive landscape,

current market standing and brand identity of Reliance Worldwide Corporation.

When marketing policies are integrated effectively and wisely, it becomes

possible for Reliance Worldwide Corporation to develop its brand equity and thus, it

could withstand the ongoing competition in the market (Lasserre 2017). However, the

organisations needs to avoid making any kind of false commitments regarding its

product features that could not be fulfilled from the end of the production department.

This signifies the requirement of assuring coordination among the various activities of

the value chain.

Product and technology development:

In the contemporary and technological advanced era, almost the entire activities

in the value chain rely on technological support. The technological integration in

distribution, production, human resource activities and marketing need Reliance

Worldwide Corporation to recognise the significance of technology development

(Morden 2016). This could be segregated into activities relating to process and product

technology development. Some instances include primarily customer services

supported by technology, automation software, data analytics and product design

research. The research and development department of the organisation is categorised

under this category.

Therefore, it is essential for Reliance Worldwide Corporation to use its

competitive advantage on activities where it needs to access to the scarce or rare

resources. This might constitute of assets, intellectual capital, distribution network or

(Source: Rwc.com 2019)

Part iv:

The two value-adding activities that have been chosen from the value chain

model of Reliance Worldwide Corporation mainly include sales and marketing from

primary activities and technology from the secondary activities. The brief evaluation of

these activities in the context of the concerned organisation is provided as follows:

Sales and marketing:

In this stage, it is necessary for Reliance Worldwide Corporation to shed light on

the advantages and points of differentiation of the provided products for persuading the

customers to show the superiority of its products compared to those of the competitors

(Jung 2014). Thus, providing superior quality products at reasonable prices and

differentiated features could not form value until the organisation decides to spend on

sales and marketing activities. The roles of the marketers and the sales agents are

deemed to be a crucial aspect in this case.

Some instances of sales and marketing activities in Reliance Worldwide

Corporation constitute of sales force, promotional activities, selection of channels,

advertising, developing and quoting relations with the members of the channels. The

organisation could utilise the approach of marketing funnel so that it could structure its

sales and marketing activities accordingly (Mohajeri et al. 2014). The marketing policies

could be either pull or push in nature based on the objectives, competitive landscape,

current market standing and brand identity of Reliance Worldwide Corporation.

When marketing policies are integrated effectively and wisely, it becomes

possible for Reliance Worldwide Corporation to develop its brand equity and thus, it

could withstand the ongoing competition in the market (Lasserre 2017). However, the

organisations needs to avoid making any kind of false commitments regarding its

product features that could not be fulfilled from the end of the production department.

This signifies the requirement of assuring coordination among the various activities of

the value chain.

Product and technology development:

In the contemporary and technological advanced era, almost the entire activities

in the value chain rely on technological support. The technological integration in

distribution, production, human resource activities and marketing need Reliance

Worldwide Corporation to recognise the significance of technology development

(Morden 2016). This could be segregated into activities relating to process and product

technology development. Some instances include primarily customer services

supported by technology, automation software, data analytics and product design

research. The research and development department of the organisation is categorised

under this category.

Therefore, it is essential for Reliance Worldwide Corporation to use its

competitive advantage on activities where it needs to access to the scarce or rare

resources. This might constitute of assets, intellectual capital, distribution network or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

skills (Mudambi and Puck 2016). With the aid of value chain analysis, it would be

possible for Reliance Worldwide Corporation to detect those activities and areas for

obtaining a significant competitive advantage over the rivals. The business

organisations such as Sharp and Toshiba made huge investment in research and

development activities within their network pertaining to the value chain (Sharma, Moon

and Strohbehn 2014).

Reliance Worldwide Corporation could either utilise operations, marketing and

other pertinent value chain activities for obtaining the cost advantages or it could utilise

human resources, infrastructure, technology, service or other pertinent activities for

setting strong base of differentiation. From the broader perspective, it is possible to

group sources of competitive advantage into differentiation and cost (Ansoff et al. 2018).

Therefore, Reliance Worldwide Corporation could obtain competitive edge from one or

more sources based on the breadth and depth of value chain analysis.

Part v:

Since two value-adding processes are chosen from the value chain model of

Reliance Worldwide Corporation, the theoretical concept about these processes would

be linked with the real life scenario. In theory, it has been learned that in marketing and

sales activity of the value chain model that products manufactured do not mean

automatically that there are individuals to buy the same. This is the area, in which sales

and marketing play a significant role in generation of sales. The marketers and the sales

agents need to ensure the awareness of the products among the potential customers

willing to buy them seriously (Brewer, Garrison and Noreen 2015). The activities related

to sales and marketing would provide means through which the buyers could purchase

the products along with inducing them to conduct the same. The examples constitute of

promotion, advertising, sales force, channel relations, channel selection, pricing and

quoting. The marketing funnel is a sound approach for structuring the entire marketing

process. Some instances of sales and marketing activities in Reliance Worldwide

Corporation constitute of sales force, promotional activities, selection of channels,

advertising, developing and quoting relations with the members of the channels. The

organisation could utilise the approach of marketing funnel so that it could structure its

sales and marketing activities accordingly.

In theory, idea has been developed that the array of technology used in majority

of the organisation is considerably wide. The activities associated with technology

development could be classified into efforts for enhancing the product and the entire

process. Some examples include accounting automation software, research pertaining

to product design, telecommunications technology as well as customer servicing

procedures (Robson 2015). In case of Reliance Worldwide Corporation, some instances

include primarily customer services supported by technology, automation software, data

analytics and product design research. The research and development department of

the organisation is categorised under this category.

With the help of enhanced information flow, it becomes possible for the

organisation to detect as well as exploit new opportunities along with minimisation of

external threats. The continual evaluation of the value chain could lead to timely fill of

skills (Mudambi and Puck 2016). With the aid of value chain analysis, it would be

possible for Reliance Worldwide Corporation to detect those activities and areas for

obtaining a significant competitive advantage over the rivals. The business

organisations such as Sharp and Toshiba made huge investment in research and

development activities within their network pertaining to the value chain (Sharma, Moon

and Strohbehn 2014).

Reliance Worldwide Corporation could either utilise operations, marketing and

other pertinent value chain activities for obtaining the cost advantages or it could utilise

human resources, infrastructure, technology, service or other pertinent activities for

setting strong base of differentiation. From the broader perspective, it is possible to

group sources of competitive advantage into differentiation and cost (Ansoff et al. 2018).

Therefore, Reliance Worldwide Corporation could obtain competitive edge from one or

more sources based on the breadth and depth of value chain analysis.

Part v:

Since two value-adding processes are chosen from the value chain model of

Reliance Worldwide Corporation, the theoretical concept about these processes would

be linked with the real life scenario. In theory, it has been learned that in marketing and

sales activity of the value chain model that products manufactured do not mean

automatically that there are individuals to buy the same. This is the area, in which sales

and marketing play a significant role in generation of sales. The marketers and the sales

agents need to ensure the awareness of the products among the potential customers

willing to buy them seriously (Brewer, Garrison and Noreen 2015). The activities related

to sales and marketing would provide means through which the buyers could purchase

the products along with inducing them to conduct the same. The examples constitute of

promotion, advertising, sales force, channel relations, channel selection, pricing and

quoting. The marketing funnel is a sound approach for structuring the entire marketing

process. Some instances of sales and marketing activities in Reliance Worldwide

Corporation constitute of sales force, promotional activities, selection of channels,

advertising, developing and quoting relations with the members of the channels. The

organisation could utilise the approach of marketing funnel so that it could structure its

sales and marketing activities accordingly.

In theory, idea has been developed that the array of technology used in majority

of the organisation is considerably wide. The activities associated with technology

development could be classified into efforts for enhancing the product and the entire

process. Some examples include accounting automation software, research pertaining

to product design, telecommunications technology as well as customer servicing

procedures (Robson 2015). In case of Reliance Worldwide Corporation, some instances

include primarily customer services supported by technology, automation software, data

analytics and product design research. The research and development department of

the organisation is categorised under this category.

With the help of enhanced information flow, it becomes possible for the

organisation to detect as well as exploit new opportunities along with minimisation of

external threats. The continual evaluation of the value chain could lead to timely fill of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

significant gaps, which might influence the productivity of an organisation. Moreover,

when an organisation makes sound enforcement of the value chain analysis, material

and product flow could be enhanced owing to improved sales and demand forecasting.

Furthermore, there could be enhancement in inventory management as well, as delays

could be reduced by tracking activities across the supply chain

Question 2:

Requirement a:

Particulars Details Values

Estimated variable overhead A $ 150,000

Estimated direct labour cost B $ 75,000

Fixed overhead C $ 120,000

Direct labour hours D 3,000

Variable overhead rate as

percentage of direct labour cost E=A/B 200%

Fixed overhead rate F=C/D $ 40

Requirement b:

Particulars Details Values

Variable overhead rate A 200%

Direct labour cost B $ 250

Fixed overhead rate C $ 40

Direct labour hours D 10

Overhead cost allocated to Job 20 E=(AxB)+(CxD) $ 900

Requirement c:

Particulars Details Values

Equipment and supplies cost A $ 1,000

Direct labour cost B $ 250

Overhead applied C $ 900

Total cost of Job 20 D=A+B+C $ 2,150

Requirement d:

Particulars Details Values

Total direct labour cost A $ 5,725

Variable overhead rate B 200%

Total direct labour hours C 229

Fixed overhead rate D $ 40

Allocation of variable overhead E=AxB $ 11,450

Allocation of fixed overhead F=CxD $ 9,160

significant gaps, which might influence the productivity of an organisation. Moreover,

when an organisation makes sound enforcement of the value chain analysis, material

and product flow could be enhanced owing to improved sales and demand forecasting.

Furthermore, there could be enhancement in inventory management as well, as delays

could be reduced by tracking activities across the supply chain

Question 2:

Requirement a:

Particulars Details Values

Estimated variable overhead A $ 150,000

Estimated direct labour cost B $ 75,000

Fixed overhead C $ 120,000

Direct labour hours D 3,000

Variable overhead rate as

percentage of direct labour cost E=A/B 200%

Fixed overhead rate F=C/D $ 40

Requirement b:

Particulars Details Values

Variable overhead rate A 200%

Direct labour cost B $ 250

Fixed overhead rate C $ 40

Direct labour hours D 10

Overhead cost allocated to Job 20 E=(AxB)+(CxD) $ 900

Requirement c:

Particulars Details Values

Equipment and supplies cost A $ 1,000

Direct labour cost B $ 250

Overhead applied C $ 900

Total cost of Job 20 D=A+B+C $ 2,150

Requirement d:

Particulars Details Values

Total direct labour cost A $ 5,725

Variable overhead rate B 200%

Total direct labour hours C 229

Fixed overhead rate D $ 40

Allocation of variable overhead E=AxB $ 11,450

Allocation of fixed overhead F=CxD $ 9,160

8MANAGEMENT ACCOUNTING

Total overhead allocation G=E+F $ 20,610

Requirement e:

The accountant of Prime Personal Trainers needs to use two cost pools rather

than one for enhancing the accuracy of product cost information. The bases of

allocation utilised for each department would be more realistic in signifying the

association between the product and the overhead expenses rather than utilising a

single plant-wide rate (Otley 2016). On the other hand, the use of departmental

overhead rates needs the distribution of overhead costs to the departments, the

assignment of support department expenses to the production departments and the

accumulation of cost driver data from the end of the production departments. Although

this approach provides more valuable information compared to the single cost pool, it is

expensive and it might provide some misleading information as well. However, despite

this loophole, the method is still deemed to be useful for better cost allocation and

accurate product costing (Quattrone 2016).

The method would make a difference because the usage of activities is different

for each overhead activity (Kaplan and Atkinson 2015). This method would make

difference, since the allocation of overhead is made based on direct labour hours or

direct labour cost. Hence, if there is usage of more equipment, it would result in lower

usage of labour and the overhead allocation would be lower, which would lead to lower

cost.

Question 3:

Requirement a:

In the words of Langfield-Smith et al. (2017), cost pool denotes the collection of

individual costs into a class based on department or cost centre. The same is used in

order to assign costs to the cost units. From the case information of Malekula Council, it

could be witnessed that the organisation is involved in providing three kinds of services

and they mainly include the following:

Housing services to the stray animals

Animal training services

Animal healthcare services

Therefore, the costs could be categorised into three cost pools depending on their

cost objects. These cost pools mainly include training costs, animal shelter costs and

healthcare service costs.

Requirement b:

When indirect expenses are collected together, they are identified in the form of

overhead expenses. All these cost elements rely on particular activities, which are

termed as cost drivers (Lavia López and Hiebl 2014). By evaluating the cost structure of

Malekula Council along with its cost objects, certain cost drivers are identified, which

are demonstrated briefly as follows:

Cost Pool Cost Driver

Total overhead allocation G=E+F $ 20,610

Requirement e:

The accountant of Prime Personal Trainers needs to use two cost pools rather

than one for enhancing the accuracy of product cost information. The bases of

allocation utilised for each department would be more realistic in signifying the

association between the product and the overhead expenses rather than utilising a

single plant-wide rate (Otley 2016). On the other hand, the use of departmental

overhead rates needs the distribution of overhead costs to the departments, the

assignment of support department expenses to the production departments and the

accumulation of cost driver data from the end of the production departments. Although

this approach provides more valuable information compared to the single cost pool, it is

expensive and it might provide some misleading information as well. However, despite

this loophole, the method is still deemed to be useful for better cost allocation and

accurate product costing (Quattrone 2016).

The method would make a difference because the usage of activities is different

for each overhead activity (Kaplan and Atkinson 2015). This method would make

difference, since the allocation of overhead is made based on direct labour hours or

direct labour cost. Hence, if there is usage of more equipment, it would result in lower

usage of labour and the overhead allocation would be lower, which would lead to lower

cost.

Question 3:

Requirement a:

In the words of Langfield-Smith et al. (2017), cost pool denotes the collection of

individual costs into a class based on department or cost centre. The same is used in

order to assign costs to the cost units. From the case information of Malekula Council, it

could be witnessed that the organisation is involved in providing three kinds of services

and they mainly include the following:

Housing services to the stray animals

Animal training services

Animal healthcare services

Therefore, the costs could be categorised into three cost pools depending on their

cost objects. These cost pools mainly include training costs, animal shelter costs and

healthcare service costs.

Requirement b:

When indirect expenses are collected together, they are identified in the form of

overhead expenses. All these cost elements rely on particular activities, which are

termed as cost drivers (Lavia López and Hiebl 2014). By evaluating the cost structure of

Malekula Council along with its cost objects, certain cost drivers are identified, which

are demonstrated briefly as follows:

Cost Pool Cost Driver

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

Animal shelter costs Number of animal days

Training costs Number of training classes

attended

Healthcare service costs Number of animal visits

Requirement c:

Statement showing assignment of cost to different cost pools

Elements of costs Basis of Allocation Shelter Costs Training costs Health care

service

costs

Animal shelter

employees salaries

Actual $ 100,000

Veternarians and

technicians salaries

Actual $

150,000

Animal trainers' salaries 50% for Training

and rest for the

sheltered animals

$ 20,000 $

20,000

Food and supplies 75000 for health

care and the rest for

the shelter

$ 50,000 $

75,000

Building related costs Area occupied

(5:3:2)

$ 100,000 $

60,000

$

40,000

Director and

administration staff's

salary

Respective

departments' staff's

salary (12:2:15)

$ 24,828 $

4,138

$

31,034

Total costs assigned

each cost pool

$ 294,828 $

84,138

$

296,034

Cost Pool Activity Driver Number of activity Cost

of

each

cost

pool

Cost per unit

of activity

Shelter Costs Number of

animal days 27,375

Animal days $

294,82

8

$

10.77

per

anim

al

Animal shelter costs Number of animal days

Training costs Number of training classes

attended

Healthcare service costs Number of animal visits

Requirement c:

Statement showing assignment of cost to different cost pools

Elements of costs Basis of Allocation Shelter Costs Training costs Health care

service

costs

Animal shelter

employees salaries

Actual $ 100,000

Veternarians and

technicians salaries

Actual $

150,000

Animal trainers' salaries 50% for Training

and rest for the

sheltered animals

$ 20,000 $

20,000

Food and supplies 75000 for health

care and the rest for

the shelter

$ 50,000 $

75,000

Building related costs Area occupied

(5:3:2)

$ 100,000 $

60,000

$

40,000

Director and

administration staff's

salary

Respective

departments' staff's

salary (12:2:15)

$ 24,828 $

4,138

$

31,034

Total costs assigned

each cost pool

$ 294,828 $

84,138

$

296,034

Cost Pool Activity Driver Number of activity Cost

of

each

cost

pool

Cost per unit

of activity

Shelter Costs Number of

animal days 27,375

Animal days $

294,82

8

$

10.77

per

anim

al

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

day

Training costs Number of

Training class

attended

1,250

Individual

classes

$

84,138

$

67.31

per

indivi

dual

class

Health care

service costs

Number of

Animal Visit 5,000

Animal

visits

$

296,03

4

$

59.21

per

anim

al

visit

day

Training costs Number of

Training class

attended

1,250

Individual

classes

$

84,138

$

67.31

per

indivi

dual

class

Health care

service costs

Number of

Animal Visit 5,000

Animal

visits

$

296,03

4

$

59.21

per

anim

al

visit

11MANAGEMENT ACCOUNTING

References:

Ansoff, H.I., Kipley, D., Lewis, A.O., Helm-Stevens, R. and Ansoff, R., 2018. Implanting

strategic management. Springer.

Bettis, R., Gambardella, A., Helfat, C. and Mitchell, W., 2014. Quantitative empirical

analysis in strategic management. Strategic Management Journal, 35(7), pp.949-953.

Bornemann, M. and Wiedenhofer, R., 2014. Intellectual capital in education: a value

chain perspective. Journal of Intellectual Capital, 15(3), pp.451-470.

Brewer, P.C., Garrison, R.H. and Noreen, E.W., 2015. Introduction to managerial

accounting. McGraw-Hill Education.

Darmawan, M.A., Putra, M.P.I.F. and Wiguna, B., 2014. Value chain analysis for green

productivity improvement in the natural rubber supply chain: a case study. Journal of

Cleaner Production, 85, pp.201-211.

El-Sayed, A.F.M., Dickson, M.W. and El-Naggar, G.O., 2015. Value chain analysis of

the aquaculture feed sector in Egypt. Aquaculture, 437, pp.92-101.

Harding, S., 2017. MBA management models. Routledge.

Hopper, T. and Bui, B., 2016. Has management accounting research been

critical?. Management Accounting Research, 31, pp.10-30.

Jenkins, W. and Williamson, D., 2015. Strategic management and business analysis.

Routledge.

Jung, S.C., 2014. The analysis of strategic management of samsung electronics

company through the generic value chain model. International Journal of Software

Engineering and Its Applications, 8(12), pp.133-142

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI

Learning.

Langfield-Smith, K., Smith, D., Andon, P., Hilton, R. and Thorne, H., 2017. Management

accounting: Information for creating and managing value. McGraw-Hill Education

Australia.

Lasserre, P., 2017. Global strategic management. Macmillan International Higher

Education.

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and medium-

sized enterprises: current knowledge and avenues for further research. Journal of

Management Accounting Research, 27(1), pp.81-119.

Messner, M., 2016. Does industry matter? How industry context shapes management

accounting practice. Management Accounting Research, 31, pp.103-111.

Mohajeri, B., Nyberg, T., Karjalainen, J., Tukiainen, T., Nelson, M., Shang, X. and

Xiong, G., 2014, October. The impact of social manufacturing on the value chain model

in the apparel industry. In Proceedings of 2014 IEEE International Conference on

Service Operations and Logistics, and Informatics (pp. 378-381). Ieee.

Morden, T., 2016. Principles of strategic management. Routledge.

Mudambi, R. and Puck, J., 2016. A global value chain analysis of the ‘regional

strategy’perspective. Journal of Management Studies, 53(6), pp.1076-1093.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

References:

Ansoff, H.I., Kipley, D., Lewis, A.O., Helm-Stevens, R. and Ansoff, R., 2018. Implanting

strategic management. Springer.

Bettis, R., Gambardella, A., Helfat, C. and Mitchell, W., 2014. Quantitative empirical

analysis in strategic management. Strategic Management Journal, 35(7), pp.949-953.

Bornemann, M. and Wiedenhofer, R., 2014. Intellectual capital in education: a value

chain perspective. Journal of Intellectual Capital, 15(3), pp.451-470.

Brewer, P.C., Garrison, R.H. and Noreen, E.W., 2015. Introduction to managerial

accounting. McGraw-Hill Education.

Darmawan, M.A., Putra, M.P.I.F. and Wiguna, B., 2014. Value chain analysis for green

productivity improvement in the natural rubber supply chain: a case study. Journal of

Cleaner Production, 85, pp.201-211.

El-Sayed, A.F.M., Dickson, M.W. and El-Naggar, G.O., 2015. Value chain analysis of

the aquaculture feed sector in Egypt. Aquaculture, 437, pp.92-101.

Harding, S., 2017. MBA management models. Routledge.

Hopper, T. and Bui, B., 2016. Has management accounting research been

critical?. Management Accounting Research, 31, pp.10-30.

Jenkins, W. and Williamson, D., 2015. Strategic management and business analysis.

Routledge.

Jung, S.C., 2014. The analysis of strategic management of samsung electronics

company through the generic value chain model. International Journal of Software

Engineering and Its Applications, 8(12), pp.133-142

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI

Learning.

Langfield-Smith, K., Smith, D., Andon, P., Hilton, R. and Thorne, H., 2017. Management

accounting: Information for creating and managing value. McGraw-Hill Education

Australia.

Lasserre, P., 2017. Global strategic management. Macmillan International Higher

Education.

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and medium-

sized enterprises: current knowledge and avenues for further research. Journal of

Management Accounting Research, 27(1), pp.81-119.

Messner, M., 2016. Does industry matter? How industry context shapes management

accounting practice. Management Accounting Research, 31, pp.103-111.

Mohajeri, B., Nyberg, T., Karjalainen, J., Tukiainen, T., Nelson, M., Shang, X. and

Xiong, G., 2014, October. The impact of social manufacturing on the value chain model

in the apparel industry. In Proceedings of 2014 IEEE International Conference on

Service Operations and Logistics, and Informatics (pp. 378-381). Ieee.

Morden, T., 2016. Principles of strategic management. Routledge.

Mudambi, R. and Puck, J., 2016. A global value chain analysis of the ‘regional

strategy’perspective. Journal of Management Studies, 53(6), pp.1076-1093.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.