Comparing Costing Techniques: A Management Accounting Assignment

VerifiedAdded on 2023/01/19

|7

|838

|71

Homework Assignment

AI Summary

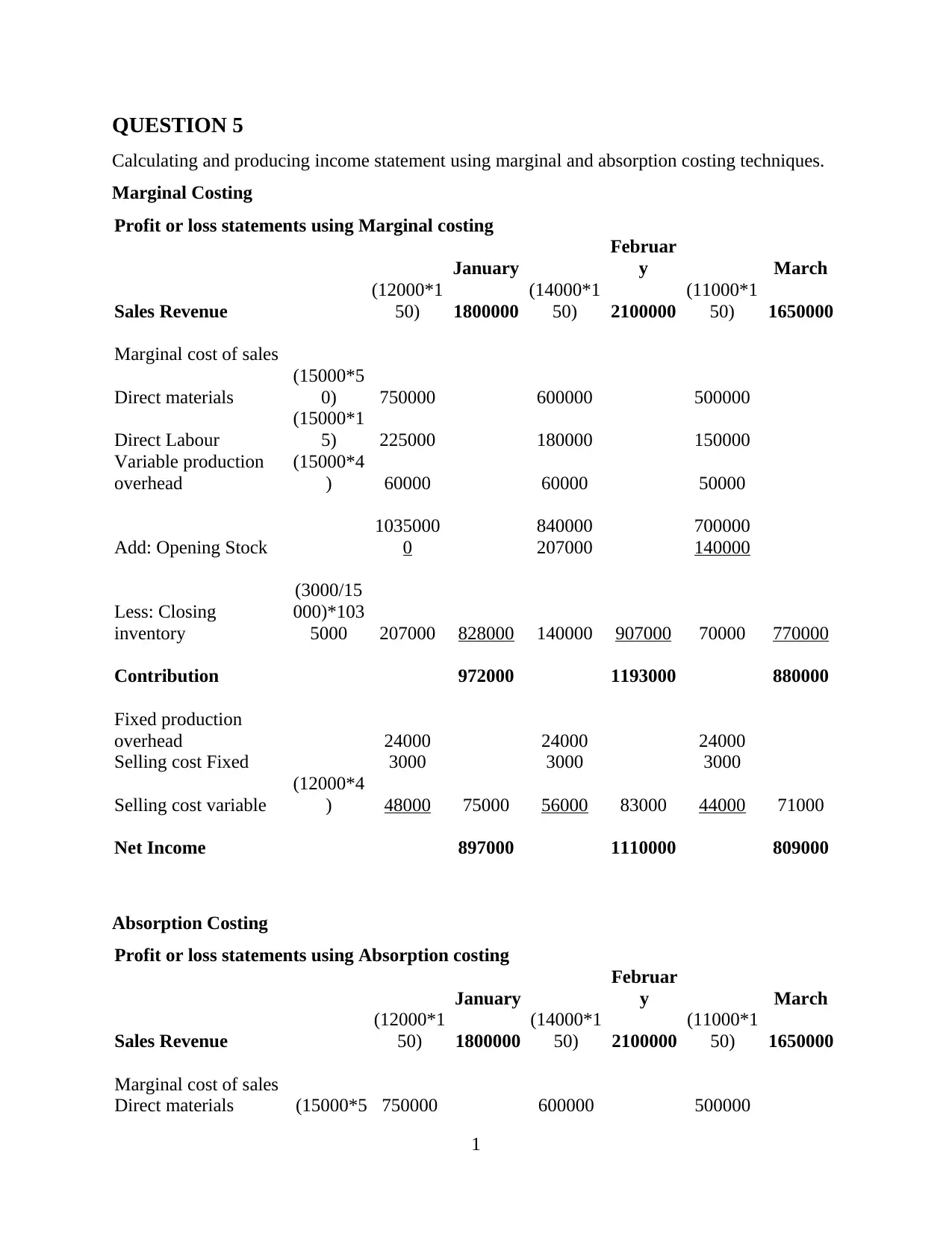

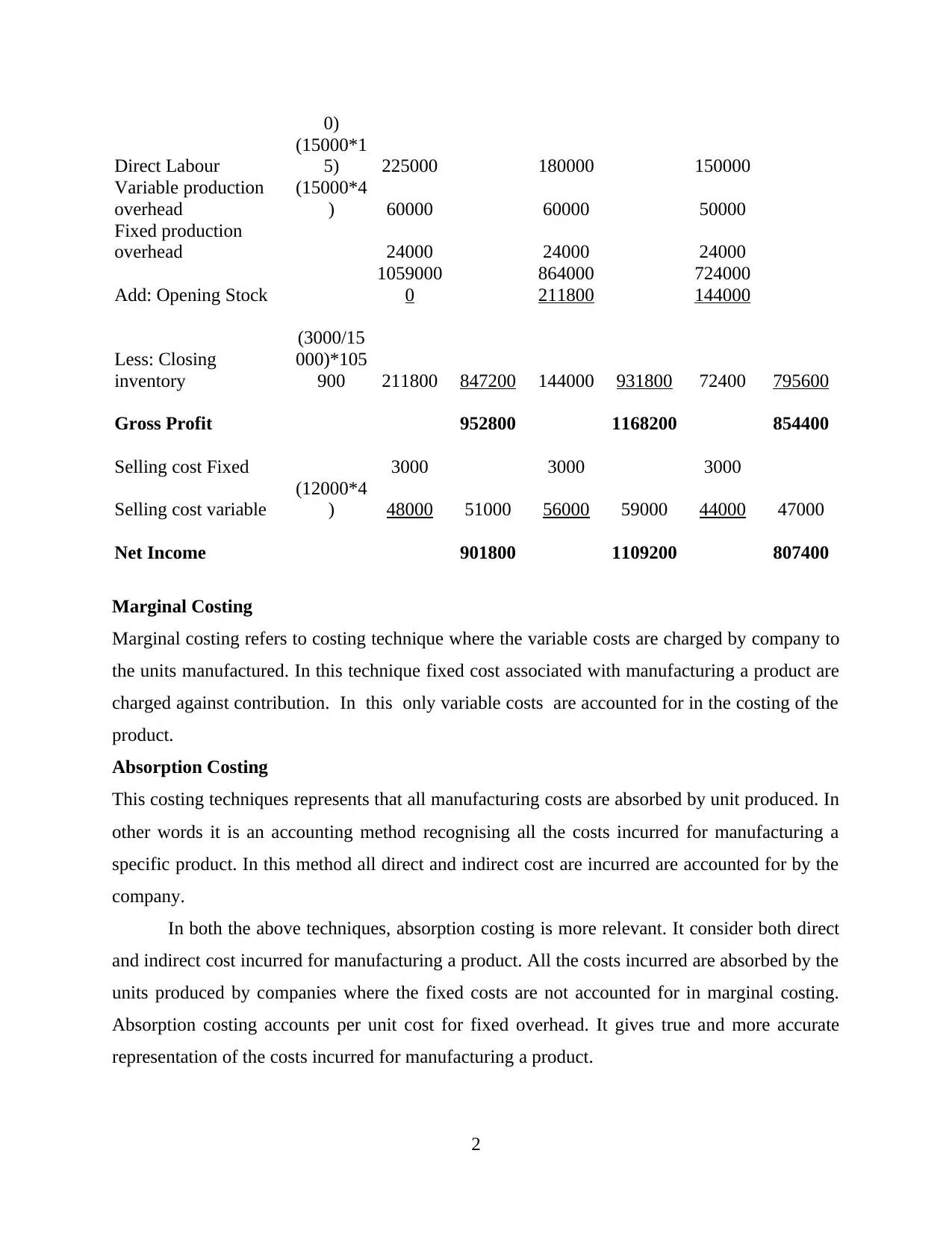

This assignment solution provides a detailed analysis of management accounting principles, specifically focusing on costing techniques, break-even analysis, and net profit calculations. The solution includes calculations and comparisons between marginal and absorption costing methods, presenting profit or loss statements for different periods. It then proceeds to calculate the break-even point, explaining its significance in management decision-making and pricing strategies. Finally, the assignment concludes with the calculation of net profit, emphasizing its importance for assessing a company's financial performance and health, as well as its implications for investors and business strategies. The document includes formulas and explanations to support the calculations and analyses.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.