Management Accounting Report: Eastern Engineering Co. Ltd Analysis

VerifiedAdded on 2022/11/30

|17

|4387

|61

Report

AI Summary

This management accounting report provides a comprehensive analysis of various aspects of management accounting, focusing on Eastern Engineering Co. Ltd. The report begins with an introduction to management accounting, its essential requirements, and a comparison with financial accounting. It then delves into different management accounting reporting methods, including performance reports, inventory reports, and cost accounting reports. The core of the report involves a detailed examination of costing techniques, specifically marginal and absorption costing, with calculations and income statement preparation. Furthermore, the report explores the advantages and disadvantages of planning tools used for budgetary control and concludes with a comparison of how organizations adapt management accounting systems. The report uses Eastern Engineering Co. Ltd as a case study to illustrate the practical application of these concepts.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirements of its systems.......................................1

P2 Different methods used for management accounting reporting.............................................4

TASK 2............................................................................................................................................5

P3 Calculation of cost using different costing techniques...........................................................5

........................................................................................................................................................10

TASK 3..........................................................................................................................................10

P4 Advantages and disadvantages of different planning tool used for budgetary control........10

TASK 4..........................................................................................................................................13

P5 Comparison of the way in which organisations are adapting management accounting

systems.......................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirements of its systems.......................................1

P2 Different methods used for management accounting reporting.............................................4

TASK 2............................................................................................................................................5

P3 Calculation of cost using different costing techniques...........................................................5

........................................................................................................................................................10

TASK 3..........................................................................................................................................10

P4 Advantages and disadvantages of different planning tool used for budgetary control........10

TASK 4..........................................................................................................................................13

P5 Comparison of the way in which organisations are adapting management accounting

systems.......................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is a branch of accounting that deals with locating, presenting, and evaluating

data for a variety of purposes, including , making decisions, maximising resource use, formulating

resources and preserving assets. It tends to deal with policy creation and plan formulation in order to

readily attain intended objectives. The company which was chosen in this assighnment is Eastern

Engineering Co. Ltd. on 6 July 1999 it is incorporated as manufacturing concern. In Uk It is established.

The definition of management accounting and the key needs of a management accounting system were

considered as part of this project. This paper also includes an explanation of several management

accounting reporting approaches. This project includes a cost analysis with supporting illustrations. The

advantages and disadvantages of planning tools for budgetary control are also examined in the relevant

assignment. This study also explains in full how management accounting is used to address difficulties

with financial concepts.

TASK 1

P.1 Explain management Accounting and give the essential requirement of different type of

management accounting system?

Management accounting: It is the process of analysing financial data collected from financial

statements in order to make key decisions that will allow a company to meet its organisational goals

within a certain time period.

Origin and evaluation of management accounting: At the time of industrial evaluation, this idea is

commonly introduced. Management accounting based on the concept of financial accounting is tends to

be created. Financial and cost accounting data are routinely used to generate management accounting

data. M.A. addresses both long-term and short-term planning.

Management accounting system: The following system cannot be implemented without financial

accounting system and cost. Companies use a variety of measures to assess their real and fair financial

situation in order to get a competitive advantage. Because the company Eastern engineering pvt ltd.

operates in the manufacturing industry, it is necessary to them to evaluate the benefits of various

systems so that they became capable to apply them properly in the business.

Difference B/w management & financial accounting

Management accounting Financial accounting

It reveals the information related to product, It reflects actual financial status of the company on

Management accounting is a branch of accounting that deals with locating, presenting, and evaluating

data for a variety of purposes, including , making decisions, maximising resource use, formulating

resources and preserving assets. It tends to deal with policy creation and plan formulation in order to

readily attain intended objectives. The company which was chosen in this assighnment is Eastern

Engineering Co. Ltd. on 6 July 1999 it is incorporated as manufacturing concern. In Uk It is established.

The definition of management accounting and the key needs of a management accounting system were

considered as part of this project. This paper also includes an explanation of several management

accounting reporting approaches. This project includes a cost analysis with supporting illustrations. The

advantages and disadvantages of planning tools for budgetary control are also examined in the relevant

assignment. This study also explains in full how management accounting is used to address difficulties

with financial concepts.

TASK 1

P.1 Explain management Accounting and give the essential requirement of different type of

management accounting system?

Management accounting: It is the process of analysing financial data collected from financial

statements in order to make key decisions that will allow a company to meet its organisational goals

within a certain time period.

Origin and evaluation of management accounting: At the time of industrial evaluation, this idea is

commonly introduced. Management accounting based on the concept of financial accounting is tends to

be created. Financial and cost accounting data are routinely used to generate management accounting

data. M.A. addresses both long-term and short-term planning.

Management accounting system: The following system cannot be implemented without financial

accounting system and cost. Companies use a variety of measures to assess their real and fair financial

situation in order to get a competitive advantage. Because the company Eastern engineering pvt ltd.

operates in the manufacturing industry, it is necessary to them to evaluate the benefits of various

systems so that they became capable to apply them properly in the business.

Difference B/w management & financial accounting

Management accounting Financial accounting

It reveals the information related to product, It reflects actual financial status of the company on

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

process, inventories, operational cost, job role etc. the basis of cash flow, p&L, balance sheet.

It is not concerned to legal constraits & generally

accepted principles.It can frame their own forms ,

rules and procedure as the information developed is

used internally only in this.

But it is governed by the principles of GAP

because to outsiders such as shareholders,

underwriters, financial institution, merchant

bankers, Qualified institution buyers etc it caters

important financial information.

Types of management accountingsystem

Cost Accounting System: this strategy facilitates the presentation of information about a company's costs

related with the production of various products & services. "the determination of actual cost, , budget,

standard cost, variance analysis, process activity and other associated activities." It is largely concerned

with acquiring, analysing, and presenting relevant cost data for the aim of interpreting and presenting

various types of management difficulties. It tends to be used in business to calculate the cost of items as

well as to services. It is also concerned with current expenses as well as cost estimation is to be incurred

in the near future.

Inventory management system: Its utilised to keep track of inventory data, which is useful for meeting

consumer demands. Different sorts of methods, such as Weighted Average, LIFO, HIFO and FIFO

approach, can be used to manage inventor.Various approaches are used by different organisations

depending on the nature of the business.. This is critical to its control since concerns such as

understocking and excess inventory tend to be reduced or eliminated with its support. It also aids in the

control of ordering costs and carrying cost by keeping inventory in shops in accordance with economic

order quantities. The right accounting system will require the company to decide regarding raw

materials, semi-finished goods, completed product and many other inventory-related considerations.

Price optimization system: As manufacturing company, Eastern engineering pvt ltd uses this strategy to

keep the cost of manufactured items at an optimal level, since it adds value by allowing them to analyse

the pricing that entities set for their products, as well as providing assurance that clients' expectations

are met or not. This approach must be followed by an entity in order to fulfil the goal, and only then will

it be feasible to fix the most appropriate price for a commodity or item, allowing the business to acquire

a competitive edge.

It is not concerned to legal constraits & generally

accepted principles.It can frame their own forms ,

rules and procedure as the information developed is

used internally only in this.

But it is governed by the principles of GAP

because to outsiders such as shareholders,

underwriters, financial institution, merchant

bankers, Qualified institution buyers etc it caters

important financial information.

Types of management accountingsystem

Cost Accounting System: this strategy facilitates the presentation of information about a company's costs

related with the production of various products & services. "the determination of actual cost, , budget,

standard cost, variance analysis, process activity and other associated activities." It is largely concerned

with acquiring, analysing, and presenting relevant cost data for the aim of interpreting and presenting

various types of management difficulties. It tends to be used in business to calculate the cost of items as

well as to services. It is also concerned with current expenses as well as cost estimation is to be incurred

in the near future.

Inventory management system: Its utilised to keep track of inventory data, which is useful for meeting

consumer demands. Different sorts of methods, such as Weighted Average, LIFO, HIFO and FIFO

approach, can be used to manage inventor.Various approaches are used by different organisations

depending on the nature of the business.. This is critical to its control since concerns such as

understocking and excess inventory tend to be reduced or eliminated with its support. It also aids in the

control of ordering costs and carrying cost by keeping inventory in shops in accordance with economic

order quantities. The right accounting system will require the company to decide regarding raw

materials, semi-finished goods, completed product and many other inventory-related considerations.

Price optimization system: As manufacturing company, Eastern engineering pvt ltd uses this strategy to

keep the cost of manufactured items at an optimal level, since it adds value by allowing them to analyse

the pricing that entities set for their products, as well as providing assurance that clients' expectations

are met or not. This approach must be followed by an entity in order to fulfil the goal, and only then will

it be feasible to fix the most appropriate price for a commodity or item, allowing the business to acquire

a competitive edge.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

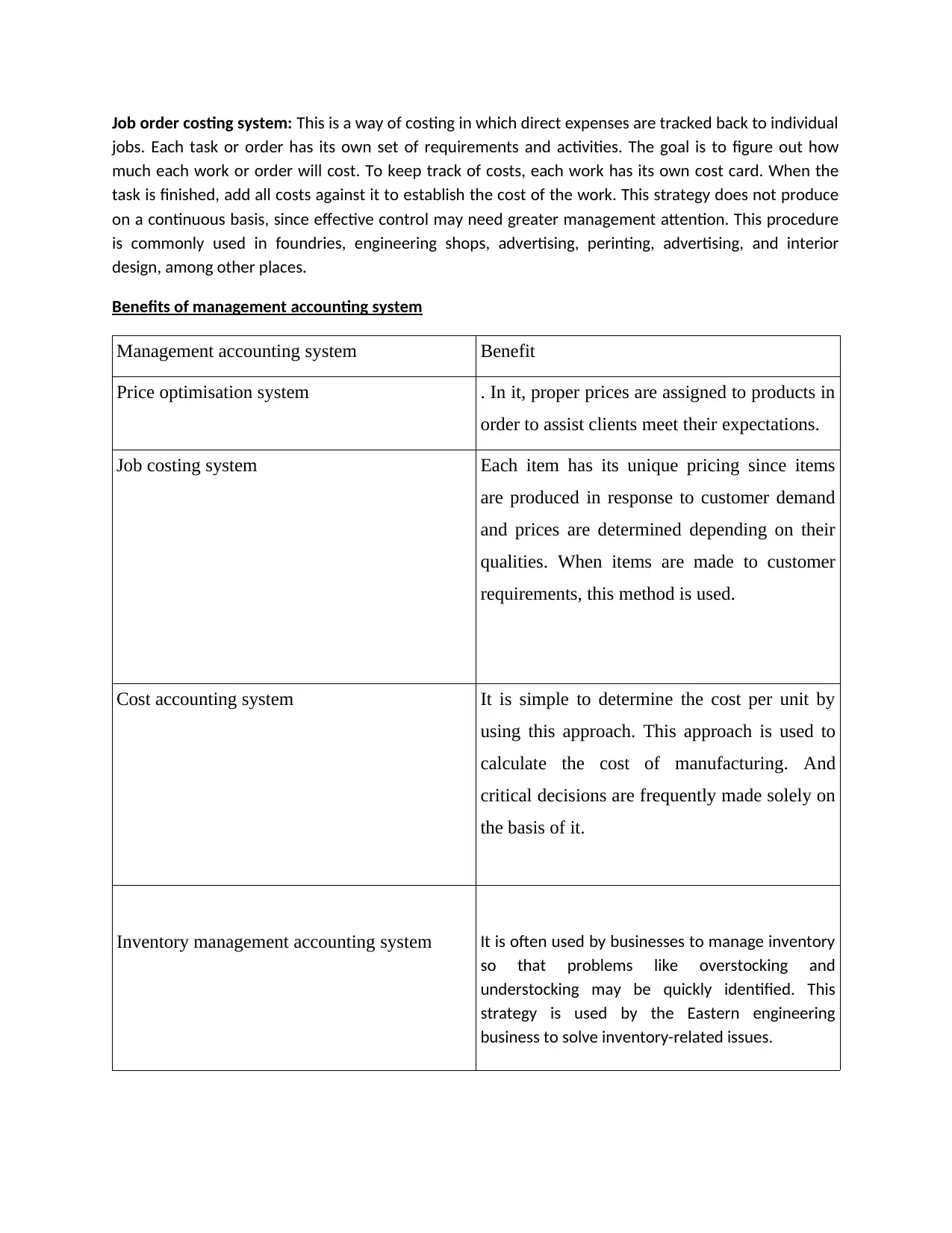

Job order costing system: This is a way of costing in which direct expenses are tracked back to individual

jobs. Each task or order has its own set of requirements and activities. The goal is to figure out how

much each work or order will cost. To keep track of costs, each work has its own cost card. When the

task is finished, add all costs against it to establish the cost of the work. This strategy does not produce

on a continuous basis, since effective control may need greater management attention. This procedure

is commonly used in foundries, engineering shops, advertising, perinting, advertising, and interior

design, among other places.

Benefits of management accounting system

Management accounting system Benefit

Price optimisation system . In it, proper prices are assigned to products in

order to assist clients meet their expectations.

Job costing system Each item has its unique pricing since items

are produced in response to customer demand

and prices are determined depending on their

qualities. When items are made to customer

requirements, this method is used.

Cost accounting system It is simple to determine the cost per unit by

using this approach. This approach is used to

calculate the cost of manufacturing. And

critical decisions are frequently made solely on

the basis of it.

Inventory management accounting system It is often used by businesses to manage inventory

so that problems like overstocking and

understocking may be quickly identified. This

strategy is used by the Eastern engineering

business to solve inventory-related issues.

jobs. Each task or order has its own set of requirements and activities. The goal is to figure out how

much each work or order will cost. To keep track of costs, each work has its own cost card. When the

task is finished, add all costs against it to establish the cost of the work. This strategy does not produce

on a continuous basis, since effective control may need greater management attention. This procedure

is commonly used in foundries, engineering shops, advertising, perinting, advertising, and interior

design, among other places.

Benefits of management accounting system

Management accounting system Benefit

Price optimisation system . In it, proper prices are assigned to products in

order to assist clients meet their expectations.

Job costing system Each item has its unique pricing since items

are produced in response to customer demand

and prices are determined depending on their

qualities. When items are made to customer

requirements, this method is used.

Cost accounting system It is simple to determine the cost per unit by

using this approach. This approach is used to

calculate the cost of manufacturing. And

critical decisions are frequently made solely on

the basis of it.

Inventory management accounting system It is often used by businesses to manage inventory

so that problems like overstocking and

understocking may be quickly identified. This

strategy is used by the Eastern engineering

business to solve inventory-related issues.

P.2 Explain different method used for management accounting reporting?

There are several approaches to generating management accounting reporting for a business in order to

track both non-financial & financial performance. IKEA will also compile its multiple accounting reports

using various accounting systems. The following is a list of some of the various reports or reporting

methods: -

Performance report - This form of report depicts actual performance of various aspects

that occur within the company or in some kind of research carried out by the employee..

This sort of report reveals the actual performance of multiple components that occur

inside the organisation or in some sort of employee research. The assignment discusses

the implications of the outcomes of a comparison of the real with the budgeted/standard.

There are several approaches to generating management accounting reporting for a

business in order to track both financial &non-financial performance. IKEA will also

prepare its various accounting reports using this tool. This could be used by company

management to assess the difference between the two statistics and between employee

outputs, as well as provide justification, and further that could be used by company

management to implement strategies that will eventually help to resolve these differences

and assist in achieving the set goals. IKEA is a small-scale furniture store. This is a

manufacturing company that uses such reports for two key reasons: employee

performance tracking and product quality assurance. The overall advantage of this

research can be seen in the way it operates, allowing employees to make good use of

keywords that help them produce better goods.

Inventory report –It is a data collection and reporting system for the quantities of raw

materials and finished items held in IKEA warehouses. A business may understand how

much inventory is already available and whether there is a need to purchase IKEA by

using an inventories report. As a result, the relevant firm must prepare inventory reports

in order to manage its products as well as raw material. Furthermore, the usage of

inventories reports help in the collection of data on a range of overheads in the inventory

There are several approaches to generating management accounting reporting for a business in order to

track both non-financial & financial performance. IKEA will also compile its multiple accounting reports

using various accounting systems. The following is a list of some of the various reports or reporting

methods: -

Performance report - This form of report depicts actual performance of various aspects

that occur within the company or in some kind of research carried out by the employee..

This sort of report reveals the actual performance of multiple components that occur

inside the organisation or in some sort of employee research. The assignment discusses

the implications of the outcomes of a comparison of the real with the budgeted/standard.

There are several approaches to generating management accounting reporting for a

business in order to track both financial &non-financial performance. IKEA will also

prepare its various accounting reports using this tool. This could be used by company

management to assess the difference between the two statistics and between employee

outputs, as well as provide justification, and further that could be used by company

management to implement strategies that will eventually help to resolve these differences

and assist in achieving the set goals. IKEA is a small-scale furniture store. This is a

manufacturing company that uses such reports for two key reasons: employee

performance tracking and product quality assurance. The overall advantage of this

research can be seen in the way it operates, allowing employees to make good use of

keywords that help them produce better goods.

Inventory report –It is a data collection and reporting system for the quantities of raw

materials and finished items held in IKEA warehouses. A business may understand how

much inventory is already available and whether there is a need to purchase IKEA by

using an inventories report. As a result, the relevant firm must prepare inventory reports

in order to manage its products as well as raw material. Furthermore, the usage of

inventories reports help in the collection of data on a range of overheads in the inventory

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

storage process. This, like IKEA, may generate a report on the management of raw

materials and ready-to-assemble furniture.

Account receivable ageing report – This section offers detailed information on debtors who

bought things on credit rather than cash. It Include collection related information, such as, the

name of the individual engaged, the date of credit purchase ,their address and phone number

and the date and amount of repayment details. This document is typically generated everyday

and reviewed once a month.

Cost accounting report -.This report includes the expenses of all operations performed

by the company in the manufacture of a certain product. et In the case of IKEA,

management team of entity uses this accounting report to track all expenditures

associated with the manufacture of its producct This research aids a company in

determining its possible expenses and earnings. process-costing & job order costing are

two approaches for generating cost accounting reports.

All costs incurred when doing a project must be considered when calculating the

expenses of a given task order. For example, IKEA management uses such a report to keep

track of all expenditures incurred when doing a given task of making furniture for a certain

sort of consumer. IKEA must transfer all expenses paid while conducting a procedure that

can be utilised to create a specific piece of furniture when using process costing. The major

goal of creating such reports is to help companies understand the total expenditures recouped

so that they can be tracked and examined more closely.

TASK 2

P.3 Calculate cost using appropriate technique of cost analysis to prepare an income statement using

marginal and absorption cost?

Cost represent the resources that have been sacrificed to attain a particular objective. In other

words cost is the amount of expenditure, actual or notional, incurred or attributable to a given

product or services. Cost is the amount of resources used for something which tends to be

measured in terms to money.

There are various type of cost that are incurred in business as these are explaining as follows:

materials and ready-to-assemble furniture.

Account receivable ageing report – This section offers detailed information on debtors who

bought things on credit rather than cash. It Include collection related information, such as, the

name of the individual engaged, the date of credit purchase ,their address and phone number

and the date and amount of repayment details. This document is typically generated everyday

and reviewed once a month.

Cost accounting report -.This report includes the expenses of all operations performed

by the company in the manufacture of a certain product. et In the case of IKEA,

management team of entity uses this accounting report to track all expenditures

associated with the manufacture of its producct This research aids a company in

determining its possible expenses and earnings. process-costing & job order costing are

two approaches for generating cost accounting reports.

All costs incurred when doing a project must be considered when calculating the

expenses of a given task order. For example, IKEA management uses such a report to keep

track of all expenditures incurred when doing a given task of making furniture for a certain

sort of consumer. IKEA must transfer all expenses paid while conducting a procedure that

can be utilised to create a specific piece of furniture when using process costing. The major

goal of creating such reports is to help companies understand the total expenditures recouped

so that they can be tracked and examined more closely.

TASK 2

P.3 Calculate cost using appropriate technique of cost analysis to prepare an income statement using

marginal and absorption cost?

Cost represent the resources that have been sacrificed to attain a particular objective. In other

words cost is the amount of expenditure, actual or notional, incurred or attributable to a given

product or services. Cost is the amount of resources used for something which tends to be

measured in terms to money.

There are various type of cost that are incurred in business as these are explaining as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct cost: Direct costs are those that can be clearly linked to a unit of operation. Direct

material, labour, and overhead costs can be assigned to a certain cost centre and charged

directly to that cost centre.

Indirect cost: Indirect costs are those that are not directly allocated to a cost centre and must

be recovered into cost units. As a result, all overhead costs are classified as indirect costs.

Fixed cost: it is a cost that tends to be unaffected by changes in the level of activity during a

given period of time as they are not change by variations in the volume of production.

There is an inverse relationship between volume and fixed cost per unit.

Variable cost: such type of cost are tends to vary in accordance with the level of activity

with in a relevant change and with in a given period of time. Direct material, direct labour

and direct expenses are tends to be vary in direct proportion to the level of activity. An

increase in the volume mean proportion increase in the total variable cost and decrease in

volume will leads to a proportionate decline in total variable cost. As they are constant per

unit but changes in totality.

Cost analysis: it is the process of apportionment of cost according to different activity as in

this identification; analysing, assessing and allocation are done to all the functional

department.

Marginal costing: In this technique only variable cost are considered for decision making .

An ascertainment is made for marginal cost and of the effect of change in volume/ type of

output over the profit. In this total cost are classified in two parts fixed and variable , but

only variable cost are charged to production.

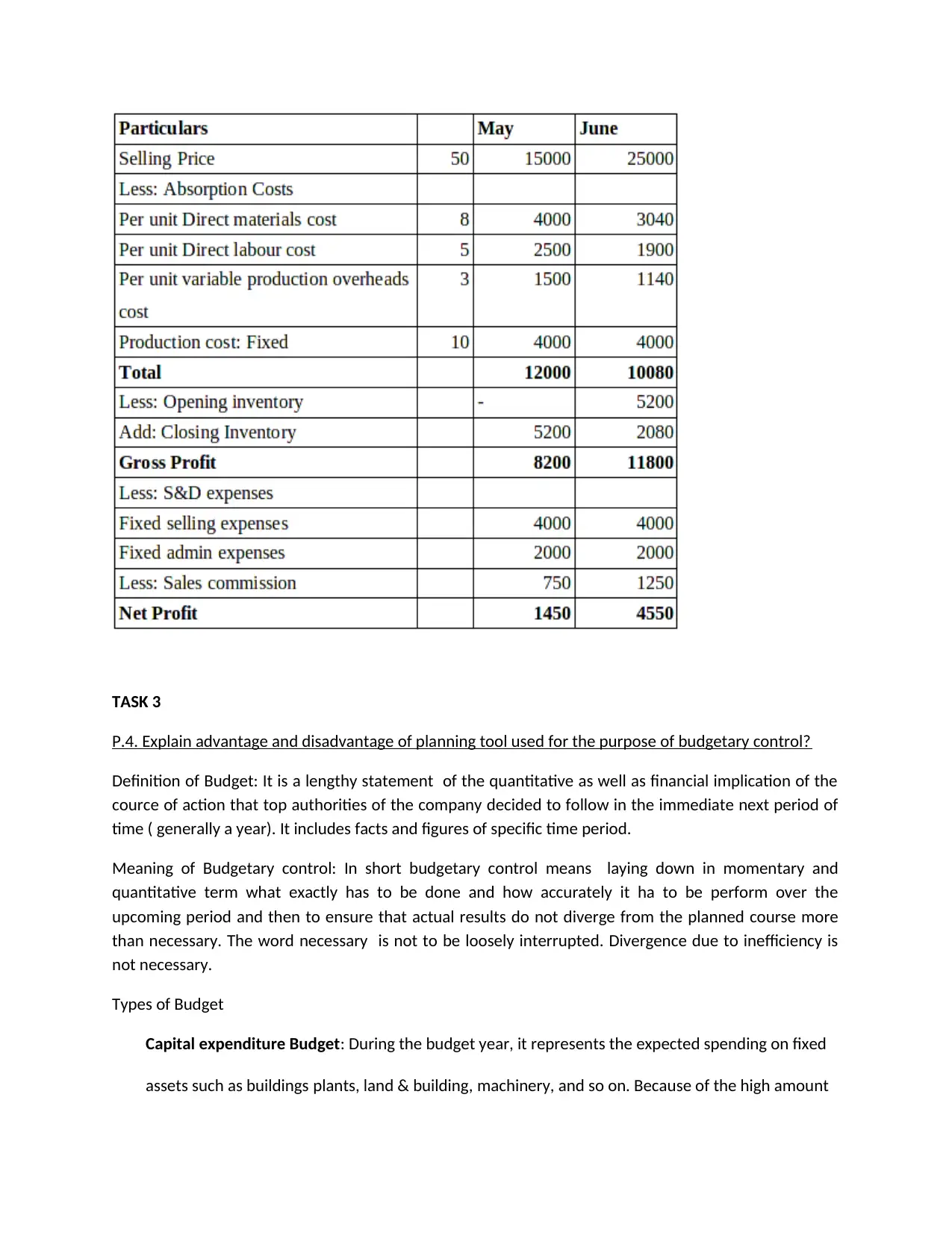

Absorption costing: It is a total cost technique. In this all cost fixed as well as variable are

tends to be charged to the production.

Standard costing: It is an accounting method in which predetermined costs are employed for

variance analysis and overall organisation control. It may be measured both monetarily &

quatitatively

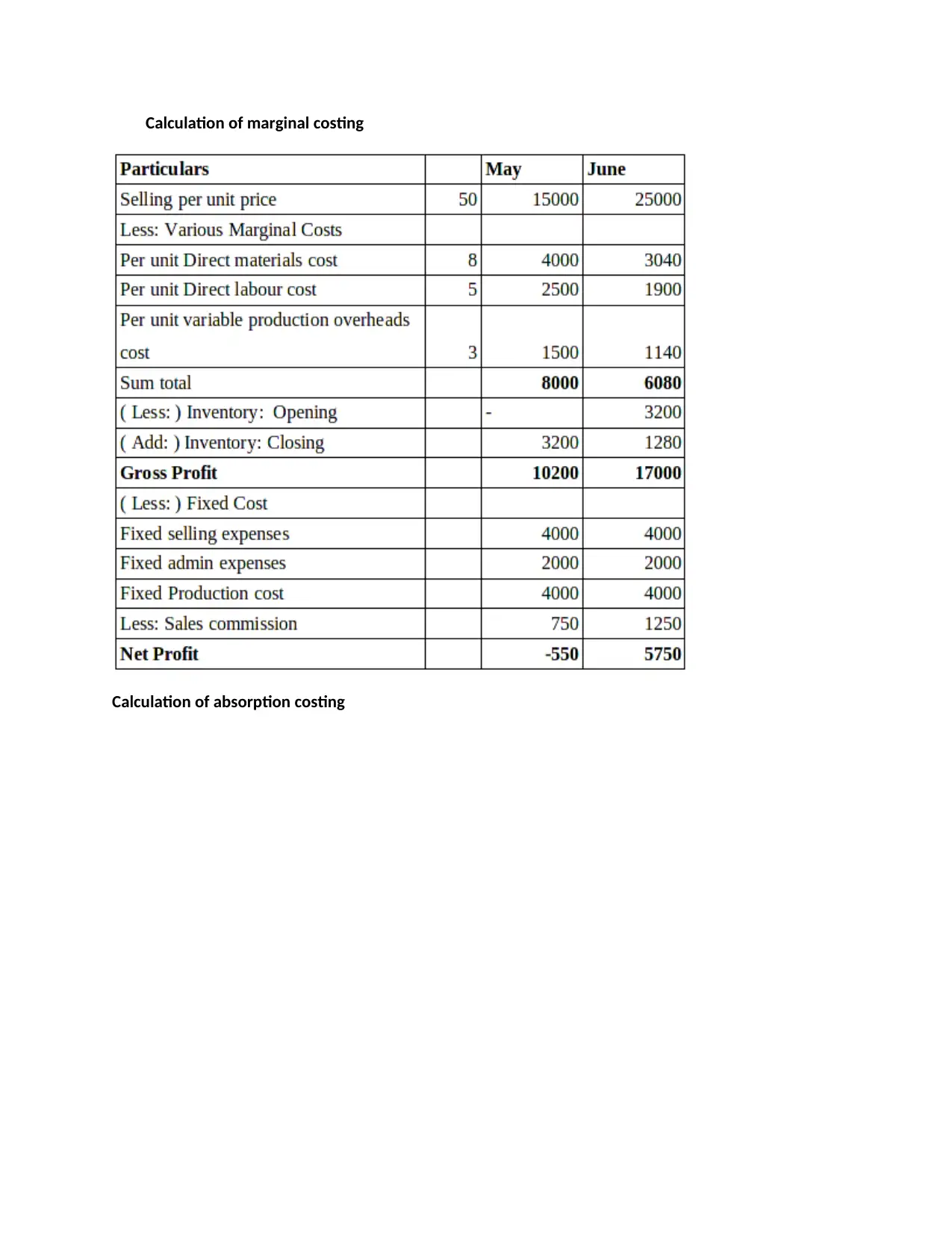

In order to create financial statements, a variety of approaches must be used. The system that

is used to report on the firm truly believes in it. As a result, P&L reports are frequently

generated using two separate methods: absorption and marginal costing. As a result, the net

profit value differs between the two ways. The reason for this is that different sorts of

activities, as well as material cost variations, are taken into account.

material, labour, and overhead costs can be assigned to a certain cost centre and charged

directly to that cost centre.

Indirect cost: Indirect costs are those that are not directly allocated to a cost centre and must

be recovered into cost units. As a result, all overhead costs are classified as indirect costs.

Fixed cost: it is a cost that tends to be unaffected by changes in the level of activity during a

given period of time as they are not change by variations in the volume of production.

There is an inverse relationship between volume and fixed cost per unit.

Variable cost: such type of cost are tends to vary in accordance with the level of activity

with in a relevant change and with in a given period of time. Direct material, direct labour

and direct expenses are tends to be vary in direct proportion to the level of activity. An

increase in the volume mean proportion increase in the total variable cost and decrease in

volume will leads to a proportionate decline in total variable cost. As they are constant per

unit but changes in totality.

Cost analysis: it is the process of apportionment of cost according to different activity as in

this identification; analysing, assessing and allocation are done to all the functional

department.

Marginal costing: In this technique only variable cost are considered for decision making .

An ascertainment is made for marginal cost and of the effect of change in volume/ type of

output over the profit. In this total cost are classified in two parts fixed and variable , but

only variable cost are charged to production.

Absorption costing: It is a total cost technique. In this all cost fixed as well as variable are

tends to be charged to the production.

Standard costing: It is an accounting method in which predetermined costs are employed for

variance analysis and overall organisation control. It may be measured both monetarily &

quatitatively

In order to create financial statements, a variety of approaches must be used. The system that

is used to report on the firm truly believes in it. As a result, P&L reports are frequently

generated using two separate methods: absorption and marginal costing. As a result, the net

profit value differs between the two ways. The reason for this is that different sorts of

activities, as well as material cost variations, are taken into account.

Calculation of marginal costing

Calculation of absorption costing

Calculation of absorption costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

P.4. Explain advantage and disadvantage of planning tool used for the purpose of budgetary control?

Definition of Budget: It is a lengthy statement of the quantitative as well as financial implication of the

cource of action that top authorities of the company decided to follow in the immediate next period of

time ( generally a year). It includes facts and figures of specific time period.

Meaning of Budgetary control: In short budgetary control means laying down in momentary and

quantitative term what exactly has to be done and how accurately it ha to be perform over the

upcoming period and then to ensure that actual results do not diverge from the planned course more

than necessary. The word necessary is not to be loosely interrupted. Divergence due to inefficiency is

not necessary.

Types of Budget

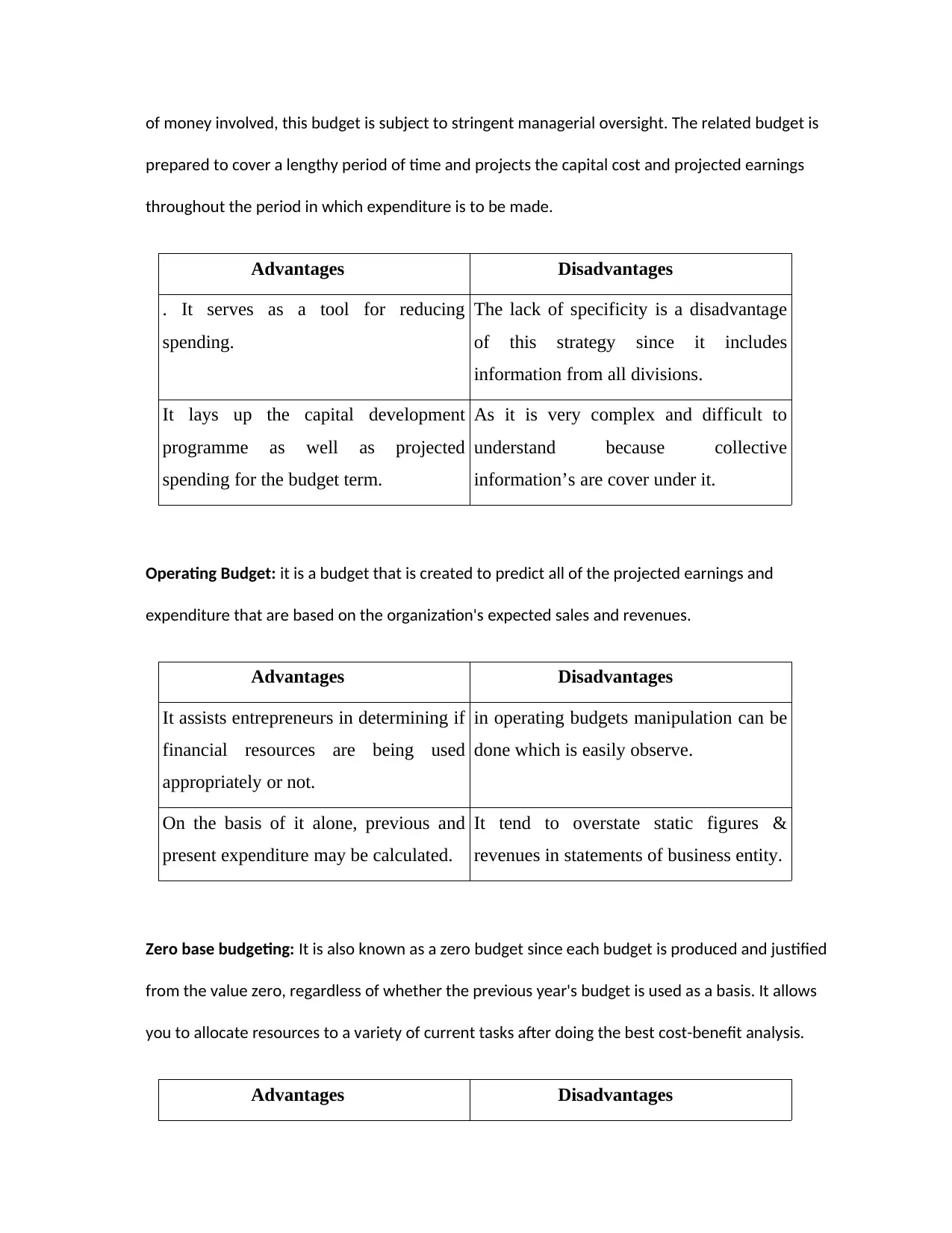

Capital expenditure Budget: During the budget year, it represents the expected spending on fixed

assets such as buildings plants, land & building, machinery, and so on. Because of the high amount

P.4. Explain advantage and disadvantage of planning tool used for the purpose of budgetary control?

Definition of Budget: It is a lengthy statement of the quantitative as well as financial implication of the

cource of action that top authorities of the company decided to follow in the immediate next period of

time ( generally a year). It includes facts and figures of specific time period.

Meaning of Budgetary control: In short budgetary control means laying down in momentary and

quantitative term what exactly has to be done and how accurately it ha to be perform over the

upcoming period and then to ensure that actual results do not diverge from the planned course more

than necessary. The word necessary is not to be loosely interrupted. Divergence due to inefficiency is

not necessary.

Types of Budget

Capital expenditure Budget: During the budget year, it represents the expected spending on fixed

assets such as buildings plants, land & building, machinery, and so on. Because of the high amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of money involved, this budget is subject to stringent managerial oversight. The related budget is

prepared to cover a lengthy period of time and projects the capital cost and projected earnings

throughout the period in which expenditure is to be made.

Advantages Disadvantages

. It serves as a tool for reducing

spending.

The lack of specificity is a disadvantage

of this strategy since it includes

information from all divisions.

It lays up the capital development

programme as well as projected

spending for the budget term.

As it is very complex and difficult to

understand because collective

information’s are cover under it.

Operating Budget: it is a budget that is created to predict all of the projected earnings and

expenditure that are based on the organization's expected sales and revenues.

Advantages Disadvantages

It assists entrepreneurs in determining if

financial resources are being used

appropriately or not.

in operating budgets manipulation can be

done which is easily observe.

On the basis of it alone, previous and

present expenditure may be calculated.

It tend to overstate static figures &

revenues in statements of business entity.

Zero base budgeting: It is also known as a zero budget since each budget is produced and justified

from the value zero, regardless of whether the previous year's budget is used as a basis. It allows

you to allocate resources to a variety of current tasks after doing the best cost-benefit analysis.

Advantages Disadvantages

prepared to cover a lengthy period of time and projects the capital cost and projected earnings

throughout the period in which expenditure is to be made.

Advantages Disadvantages

. It serves as a tool for reducing

spending.

The lack of specificity is a disadvantage

of this strategy since it includes

information from all divisions.

It lays up the capital development

programme as well as projected

spending for the budget term.

As it is very complex and difficult to

understand because collective

information’s are cover under it.

Operating Budget: it is a budget that is created to predict all of the projected earnings and

expenditure that are based on the organization's expected sales and revenues.

Advantages Disadvantages

It assists entrepreneurs in determining if

financial resources are being used

appropriately or not.

in operating budgets manipulation can be

done which is easily observe.

On the basis of it alone, previous and

present expenditure may be calculated.

It tend to overstate static figures &

revenues in statements of business entity.

Zero base budgeting: It is also known as a zero budget since each budget is produced and justified

from the value zero, regardless of whether the previous year's budget is used as a basis. It allows

you to allocate resources to a variety of current tasks after doing the best cost-benefit analysis.

Advantages Disadvantages

. It tends to provide systematic

approach for the evaluation of

different activities.

It aids in the discovery of

unnecessary expenditures and

their subsequent removal.

As compare to traditional

budgeting system it consume

more time.

Lot of paper work are involved in

this method and more personnel

are require to perform it which in

turn increases the cost.

TASK 4

P.5. Compare how organization are adapting management accounting system to respond to financial

problem?

Financial challenges develop in any organisation when funds are in limited supply or

enough capital is unavailable. It's critical for businesses to figure out what's causing these

financial problems. The following tools are used to determine the source of financial

troubles for this aim. Eastern Engineering Company has a number of financial issues,

including:

Late or delayed payment by their clients or from their customers.: Because

organisations provide credit to their consumers, difficulties with late payments by

customers/clients might emerge, resulting in a lack of financial resources and a deficit of

working capital, due to which effect negatively. As Eastern engineering offers credit to its

employees, it occasionally has concerns with late payments, which can cause company

difficulties due to a lack of financial resources. Which disrupts business operations and

makes it impossible for business to function smoothly owing to such financial concerns.

approach for the evaluation of

different activities.

It aids in the discovery of

unnecessary expenditures and

their subsequent removal.

As compare to traditional

budgeting system it consume

more time.

Lot of paper work are involved in

this method and more personnel

are require to perform it which in

turn increases the cost.

TASK 4

P.5. Compare how organization are adapting management accounting system to respond to financial

problem?

Financial challenges develop in any organisation when funds are in limited supply or

enough capital is unavailable. It's critical for businesses to figure out what's causing these

financial problems. The following tools are used to determine the source of financial

troubles for this aim. Eastern Engineering Company has a number of financial issues,

including:

Late or delayed payment by their clients or from their customers.: Because

organisations provide credit to their consumers, difficulties with late payments by

customers/clients might emerge, resulting in a lack of financial resources and a deficit of

working capital, due to which effect negatively. As Eastern engineering offers credit to its

employees, it occasionally has concerns with late payments, which can cause company

difficulties due to a lack of financial resources. Which disrupts business operations and

makes it impossible for business to function smoothly owing to such financial concerns.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.