University Management Accounting Report: Costing Techniques Analysis

VerifiedAdded on 2022/11/24

|11

|1497

|174

Report

AI Summary

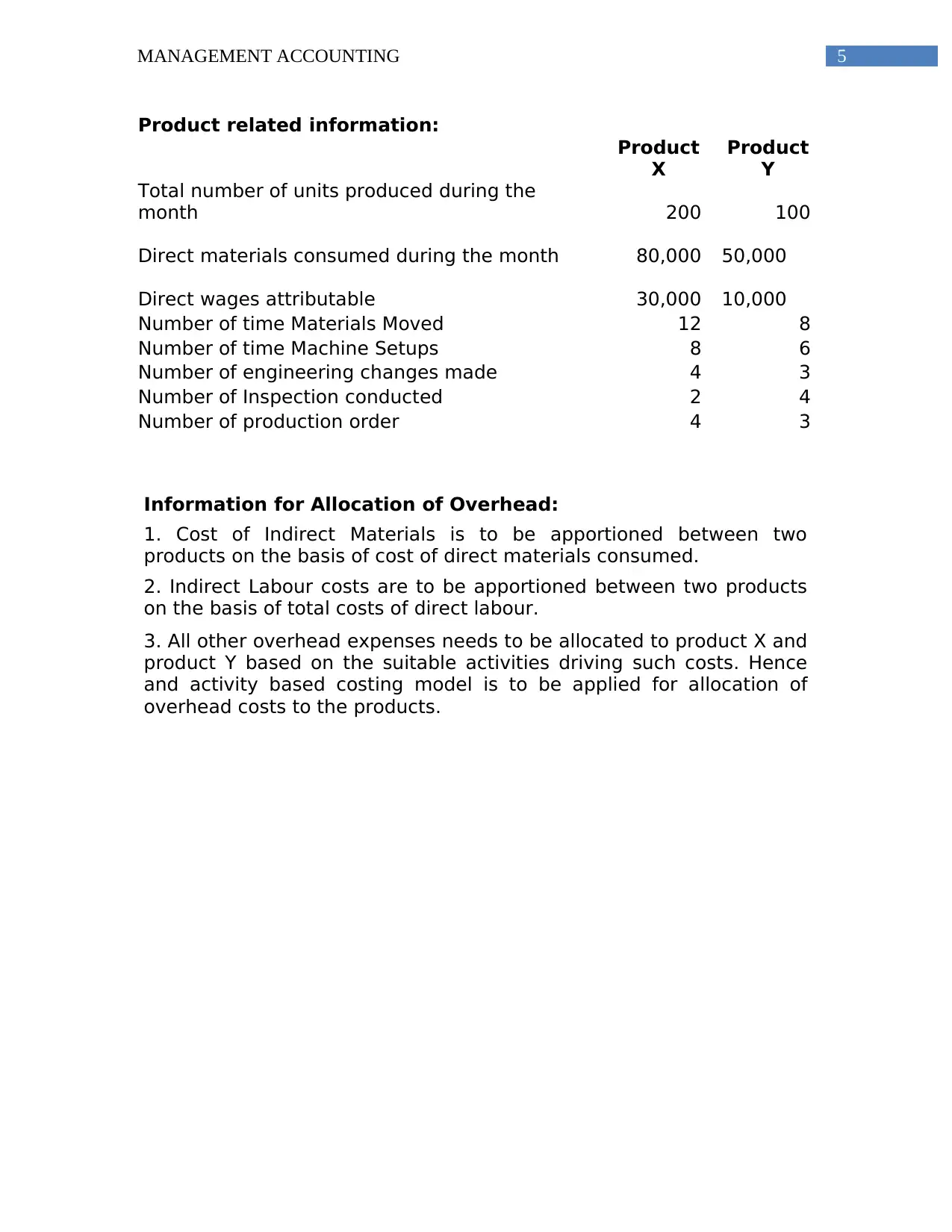

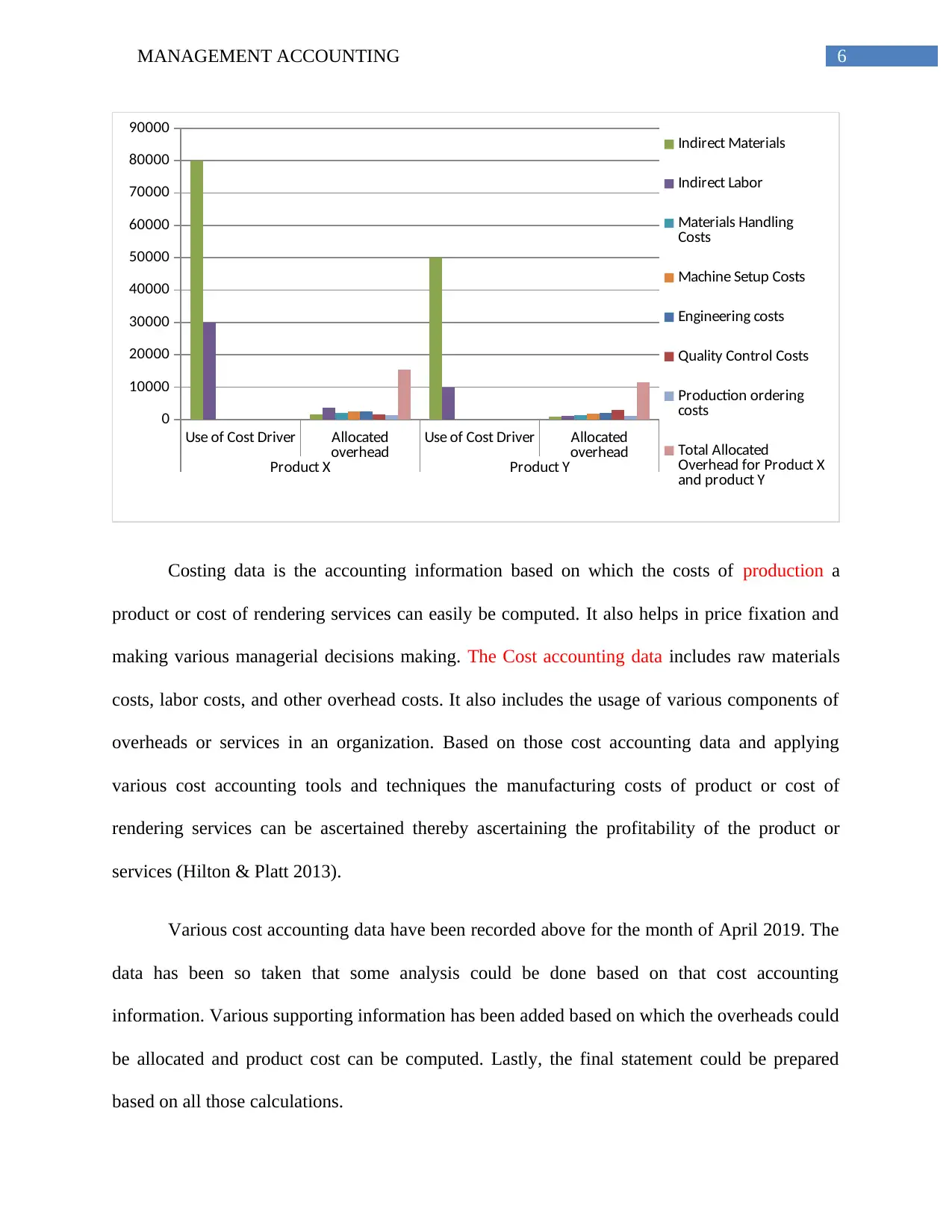

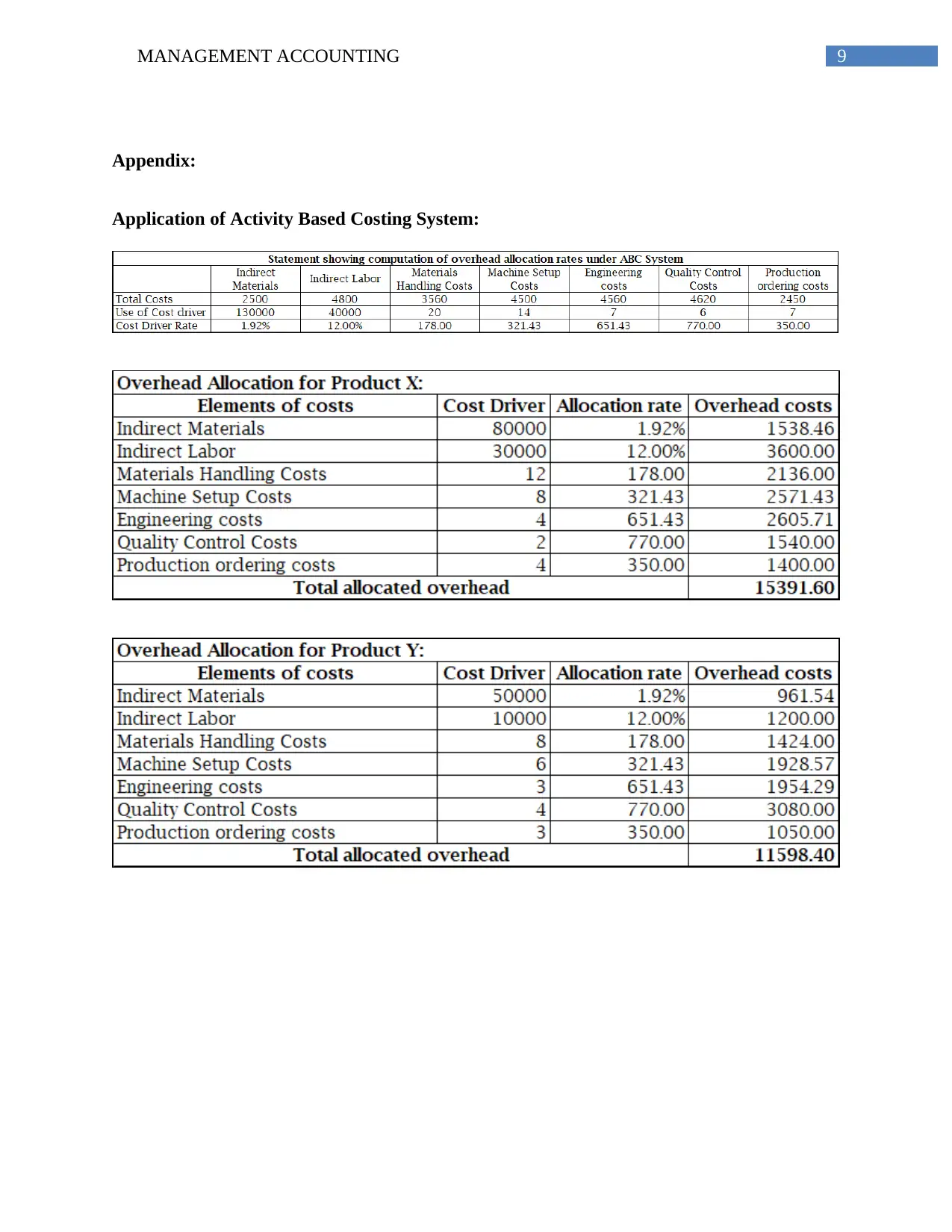

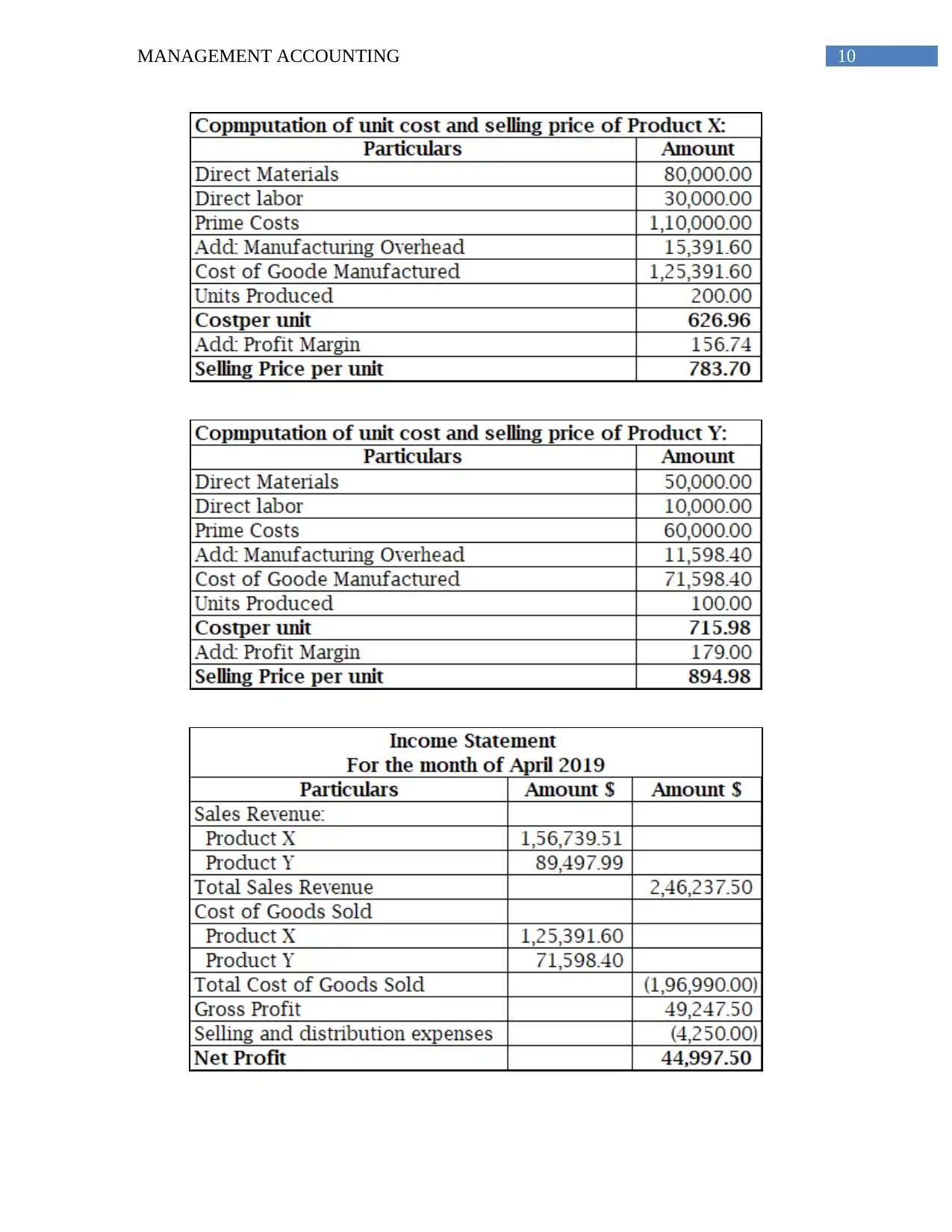

This report, prepared for a Management Accounting course, delves into the application of various costing techniques within a business context. It begins by introducing the concept of job costing, highlighting its relevance in organizations with unique, customized projects, and discussing its limitations. The report then presents quantitative and qualitative costing data, providing a practical example to illustrate cost accounting principles. An in-depth analysis of the Activity-Based Costing (ABC) model follows, demonstrating its effectiveness in allocating overhead costs. The report concludes with recommendations for improving managerial decision-making processes, emphasizing the importance of understanding and effectively implementing costing techniques for better cost management and profitability.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.