Analysis of Management Accounting Principles, Systems, and Costing

VerifiedAdded on 2021/11/16

|9

|2550

|142

Report

AI Summary

This report delves into the multifaceted realm of management accounting, commencing with an explanation of its core principles. It elucidates the crucial role of management accounting and its systems within organizations, highlighting their advantages. The report then provides a comparative analysis of marginal and absorption costing systems, including their application in determining unit costs and preparing income statements. The report showcases the determination of unit costs and the preparation of income statements using both variable costing and absorption costing methods, further illustrating the practical application of these concepts. The report provides a clear understanding of how management accounting principles and systems contribute to effective decision-making and financial management within organizations. The report concludes with a reference list of sources used.

1

Table of content:

1. An explanation of management accounting principles 2

2. In an organisation, the role of management accounting and

management accounting systems, and their advantages

2

- Management accounting 2

- Management accounting system 4

3. A comparison of the marginal and absorption costing systems 5

4. Determine the unit cost of a product and prepare an income statement

using the variable costing and absorption costing system

7

Reference list 9

Table of content:

1. An explanation of management accounting principles 2

2. In an organisation, the role of management accounting and

management accounting systems, and their advantages

2

- Management accounting 2

- Management accounting system 4

3. A comparison of the marginal and absorption costing systems 5

4. Determine the unit cost of a product and prepare an income statement

using the variable costing and absorption costing system

7

Reference list 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

1. An explanation of management accounting principles:

Management accounting is at the center of good decision-making because it prioritizes the most

critical data and analysis in order to create and maintain meaning. The Principles serve as a

guide for best management accounting practices, ensuring that difficult decisions can be taken

that lead to long-term value creation.

There are four global principles related to management accounting that can be easily followed

by companies of all sizes, whether small, medium, or big, private or public.

- Influence: Influential knowledge can be gained by communication.Conversations are

central to management accounting. The Principles were built to assist organizations

break down silos and encourage integrated thinking, which leads to better decision-

making.

- Relevant: The information is relevant. Management accounting provides decision-

makers with timely access to relevant data. The Principles outline how to identify past,

present, and future information from internal and external sources, including financial

and non-financial data. This information covers social, environmental, and economic

issues.

- Analysis: The impact on valuation is analyzed. Management accounting links an

organization's strategy to its business model. This Principle assists organisations in

simulating different scenarios to understand better their effect on value creation and

preservation.

- Trust: Trust is built by stewardship. Accountability and scrutiny improve decision-

making objectivity. When short-term commercial interests are balanced against long-

term value for stakeholders, credibility and confidence are enhanced.

(CIMA, n.d.)

2. In an organisation, the role of management accounting and management accounting

systems, and their advantages:

Management accounting:

A management accountant's general responsibility is to supply reports for management

purposes. Planning, control, cost accounting, decision making, financial management, and

auditing are six distinct roles that can easily be defined.

❖ Planning:

Long term:

● Corporate and strategic strategy (more than 1 year).

● The strategic analysis unit receives data from the management accountant.

Short term:

● Often known as budgeting (less than 1 year).

● Budgets must be prepared by a management accountant.

❖ Control:

● Measure and correlate actual results to expected operations to identify variances

(differences), which also are investigated and reported to senior management.

● Accounting management are not in charge of punitive decisions.

❖ Cost accounting:

● Once was management Accountant's primary function.

1. An explanation of management accounting principles:

Management accounting is at the center of good decision-making because it prioritizes the most

critical data and analysis in order to create and maintain meaning. The Principles serve as a

guide for best management accounting practices, ensuring that difficult decisions can be taken

that lead to long-term value creation.

There are four global principles related to management accounting that can be easily followed

by companies of all sizes, whether small, medium, or big, private or public.

- Influence: Influential knowledge can be gained by communication.Conversations are

central to management accounting. The Principles were built to assist organizations

break down silos and encourage integrated thinking, which leads to better decision-

making.

- Relevant: The information is relevant. Management accounting provides decision-

makers with timely access to relevant data. The Principles outline how to identify past,

present, and future information from internal and external sources, including financial

and non-financial data. This information covers social, environmental, and economic

issues.

- Analysis: The impact on valuation is analyzed. Management accounting links an

organization's strategy to its business model. This Principle assists organisations in

simulating different scenarios to understand better their effect on value creation and

preservation.

- Trust: Trust is built by stewardship. Accountability and scrutiny improve decision-

making objectivity. When short-term commercial interests are balanced against long-

term value for stakeholders, credibility and confidence are enhanced.

(CIMA, n.d.)

2. In an organisation, the role of management accounting and management accounting

systems, and their advantages:

Management accounting:

A management accountant's general responsibility is to supply reports for management

purposes. Planning, control, cost accounting, decision making, financial management, and

auditing are six distinct roles that can easily be defined.

❖ Planning:

Long term:

● Corporate and strategic strategy (more than 1 year).

● The strategic analysis unit receives data from the management accountant.

Short term:

● Often known as budgeting (less than 1 year).

● Budgets must be prepared by a management accountant.

❖ Control:

● Measure and correlate actual results to expected operations to identify variances

(differences), which also are investigated and reported to senior management.

● Accounting management are not in charge of punitive decisions.

❖ Cost accounting:

● Once was management Accountant's primary function.

3

● Among functions are:

- The collection of a company's ongoing costs and revenues..

- A double-entry bookkeeping system is used to keep a record of them.

- The ‘books' must be balanced.

- The gathering of information.

● It also involves estimating the actual costs of goods and services for the

purposes of stock valuation, control, and decision making.

❖ Decision making:

● The supply of information for decision making is also one of Management

Accounting's primary functions.

● Rather than actual costs, decision-making information involves “anticipated/

expected future” costs.

- Decision on closure and shutdown.

- Decision making or buying.

- Decision on the price.

- Special orders.

❖ Financial management: Financial management, which is linked to management

accounting in general, has grown in importance in recent years. Even so, financial

accounting has almost become its own discipline. Its primary goal is to locate the funds

required to meet the entity's planning needs on a budget, to ensure that they are

accessible when required, and that they are used efficiently and effectively.

❖ Auditing:

● External audit:

- A component of the financial accounting function.

- Working for an outside entity.

● Internal audit:

- A component of the management accounting function

- The entity's employee

(Dyson, n.d.)

There are several objectives, however the main objective is to support an organization's

executive committee in making the most efficient informed choices. Management accounting's

role is to provide financial information to the management team in order for them to conduct

business and activities efficiently. The below is a comprehensive list of all management

accounting benefits.

- Making a Decision

- Organizing

- Keeping an eye on corporate processes

- Organization

- Financial data should be understood.

- Identifying and resolving business issues

- Strategic Management

(Toppr, n.d.)

● Among functions are:

- The collection of a company's ongoing costs and revenues..

- A double-entry bookkeeping system is used to keep a record of them.

- The ‘books' must be balanced.

- The gathering of information.

● It also involves estimating the actual costs of goods and services for the

purposes of stock valuation, control, and decision making.

❖ Decision making:

● The supply of information for decision making is also one of Management

Accounting's primary functions.

● Rather than actual costs, decision-making information involves “anticipated/

expected future” costs.

- Decision on closure and shutdown.

- Decision making or buying.

- Decision on the price.

- Special orders.

❖ Financial management: Financial management, which is linked to management

accounting in general, has grown in importance in recent years. Even so, financial

accounting has almost become its own discipline. Its primary goal is to locate the funds

required to meet the entity's planning needs on a budget, to ensure that they are

accessible when required, and that they are used efficiently and effectively.

❖ Auditing:

● External audit:

- A component of the financial accounting function.

- Working for an outside entity.

● Internal audit:

- A component of the management accounting function

- The entity's employee

(Dyson, n.d.)

There are several objectives, however the main objective is to support an organization's

executive committee in making the most efficient informed choices. Management accounting's

role is to provide financial information to the management team in order for them to conduct

business and activities efficiently. The below is a comprehensive list of all management

accounting benefits.

- Making a Decision

- Organizing

- Keeping an eye on corporate processes

- Organization

- Financial data should be understood.

- Identifying and resolving business issues

- Strategic Management

(Toppr, n.d.)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Management accounting system:

- Management accounting systems are used in businesses to keep track of the costs of

manufacturing goods and services. Four of the most prevalent systems are traditional

cost accounting, lean accounting, throughput accounting, and transfer pricing. All of

these management accounting systems provide a distinct method for companies to

monitor prices in order to deliver goods and service at the lowest price. Failure to follow

any system would lead in overpriced commodities and lower profit margins.

- Traditional management accounting systems report costs using job order or process

costing methods. This method, together with others, determines how a company

allocates direct materials, direct labor, and manufacturing overhead costs. Job order

costing is used for large projects where all costs can be quickly tracked down to

particular projects. In process costing, costs are allocated based on the number of

processes used to manufacture homogeneous products. These items are manufactured

in a continuous process and are hard to price separately.

- Lean accounting became a more revolutionary method in management accounting

systems. Lean accounting is an approach that provides a technique for reducing costs

by waste reduction rather than relying entirely on costs. Accountants in this system can

use near-real-time financial information for decision-making, value chain analysis, and

profitability measurement. Any unnecessary costs may be discarded and eliminated

from the system based on this information.

- Throughput accounting is not generally treated as a costing process in conventional

management accounting systems. Accountants focus on identifying the constraints of

the company's manufacturing structure. Constraints include insufficient levels of

materials, labor, or processing capability from the company's factories. More

throughputs may be used to increase production capacity, decreasing the cost per unit

produced by reducing these constraints. In most cases, this approach can be applied to

traditional job order or process costing systems.

- Transfer pricing is another common management accounting system. Using this

system, businesses will cost products as they move through different units. Each item

is transferred to a separate agency or process, each of which adds a minor portion to the

product's costs. Variable costs and opportunity costs are two types of costs that are often

applied to the transfer price. Opportunity costs represent the amount of money it will

cost the corporation to outsource output to another type. Other methods of transfer

pricing are also available. The system's flexibility in transfer pricing is often cited as an

advantage.

(Vitez, 2021)

- Internal management accounting systems are used to provide important information to

management for operational company decision-making. A manufacturing firm may use

these systems to help with costing and management of their activities. Management

accounting systems can assist a hospital with insurance billing and other internal

requirements. These systems vary based on the industries in which they are used, and

they support industry-specific functionalities and reports.

(What Is Management Accounting? | FreshBooks, n.d.)

Management accounting system:

- Management accounting systems are used in businesses to keep track of the costs of

manufacturing goods and services. Four of the most prevalent systems are traditional

cost accounting, lean accounting, throughput accounting, and transfer pricing. All of

these management accounting systems provide a distinct method for companies to

monitor prices in order to deliver goods and service at the lowest price. Failure to follow

any system would lead in overpriced commodities and lower profit margins.

- Traditional management accounting systems report costs using job order or process

costing methods. This method, together with others, determines how a company

allocates direct materials, direct labor, and manufacturing overhead costs. Job order

costing is used for large projects where all costs can be quickly tracked down to

particular projects. In process costing, costs are allocated based on the number of

processes used to manufacture homogeneous products. These items are manufactured

in a continuous process and are hard to price separately.

- Lean accounting became a more revolutionary method in management accounting

systems. Lean accounting is an approach that provides a technique for reducing costs

by waste reduction rather than relying entirely on costs. Accountants in this system can

use near-real-time financial information for decision-making, value chain analysis, and

profitability measurement. Any unnecessary costs may be discarded and eliminated

from the system based on this information.

- Throughput accounting is not generally treated as a costing process in conventional

management accounting systems. Accountants focus on identifying the constraints of

the company's manufacturing structure. Constraints include insufficient levels of

materials, labor, or processing capability from the company's factories. More

throughputs may be used to increase production capacity, decreasing the cost per unit

produced by reducing these constraints. In most cases, this approach can be applied to

traditional job order or process costing systems.

- Transfer pricing is another common management accounting system. Using this

system, businesses will cost products as they move through different units. Each item

is transferred to a separate agency or process, each of which adds a minor portion to the

product's costs. Variable costs and opportunity costs are two types of costs that are often

applied to the transfer price. Opportunity costs represent the amount of money it will

cost the corporation to outsource output to another type. Other methods of transfer

pricing are also available. The system's flexibility in transfer pricing is often cited as an

advantage.

(Vitez, 2021)

- Internal management accounting systems are used to provide important information to

management for operational company decision-making. A manufacturing firm may use

these systems to help with costing and management of their activities. Management

accounting systems can assist a hospital with insurance billing and other internal

requirements. These systems vary based on the industries in which they are used, and

they support industry-specific functionalities and reports.

(What Is Management Accounting? | FreshBooks, n.d.)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

- As the most valuable source of information, the management accounting system is

critical to achieving the organization's strategic objectives. As a result, any

inefficiencies or weaknesses in the system reduce efficiency and productivity, causing

plenty of problems within the enterprise. The management accounting system, as a

valuable subset of the system of financial and non-financial information, provides a

variety of types of information to users, especially managers, in any company.

(Ghanbari and Vaseli, 2015)

- The management accounting system can help to reduce different forms of waste,

manufacturing, defects, and other work, allowing employees to work more efficiently.

- Accounting systems ensure that management provides better and improved services to

consumers. The management accounting system's tools are accurate. Normally, this

process means that the data provided to management is precise and reliable.

(Accountlearning, n.d.)

3. A comparison of the marginal and absorption costing systems:

How are the terms in marginal cost related to cost of production the same as those that are

classified under the term absorption cost.

Absorption costing Marginal costing

Direct cost Variable cost

Direct materials Variable direct materials

Direct labour Variable direct labour

Direct expenses Variable direct expenses

Variable overhead

Indirect cost Fixed cost

Variable overhead fixe direct expenses

Fixed overheads Fixed overhead

- As the most valuable source of information, the management accounting system is

critical to achieving the organization's strategic objectives. As a result, any

inefficiencies or weaknesses in the system reduce efficiency and productivity, causing

plenty of problems within the enterprise. The management accounting system, as a

valuable subset of the system of financial and non-financial information, provides a

variety of types of information to users, especially managers, in any company.

(Ghanbari and Vaseli, 2015)

- The management accounting system can help to reduce different forms of waste,

manufacturing, defects, and other work, allowing employees to work more efficiently.

- Accounting systems ensure that management provides better and improved services to

consumers. The management accounting system's tools are accurate. Normally, this

process means that the data provided to management is precise and reliable.

(Accountlearning, n.d.)

3. A comparison of the marginal and absorption costing systems:

How are the terms in marginal cost related to cost of production the same as those that are

classified under the term absorption cost.

Absorption costing Marginal costing

Direct cost Variable cost

Direct materials Variable direct materials

Direct labour Variable direct labour

Direct expenses Variable direct expenses

Variable overhead

Indirect cost Fixed cost

Variable overhead fixe direct expenses

Fixed overheads Fixed overhead

6

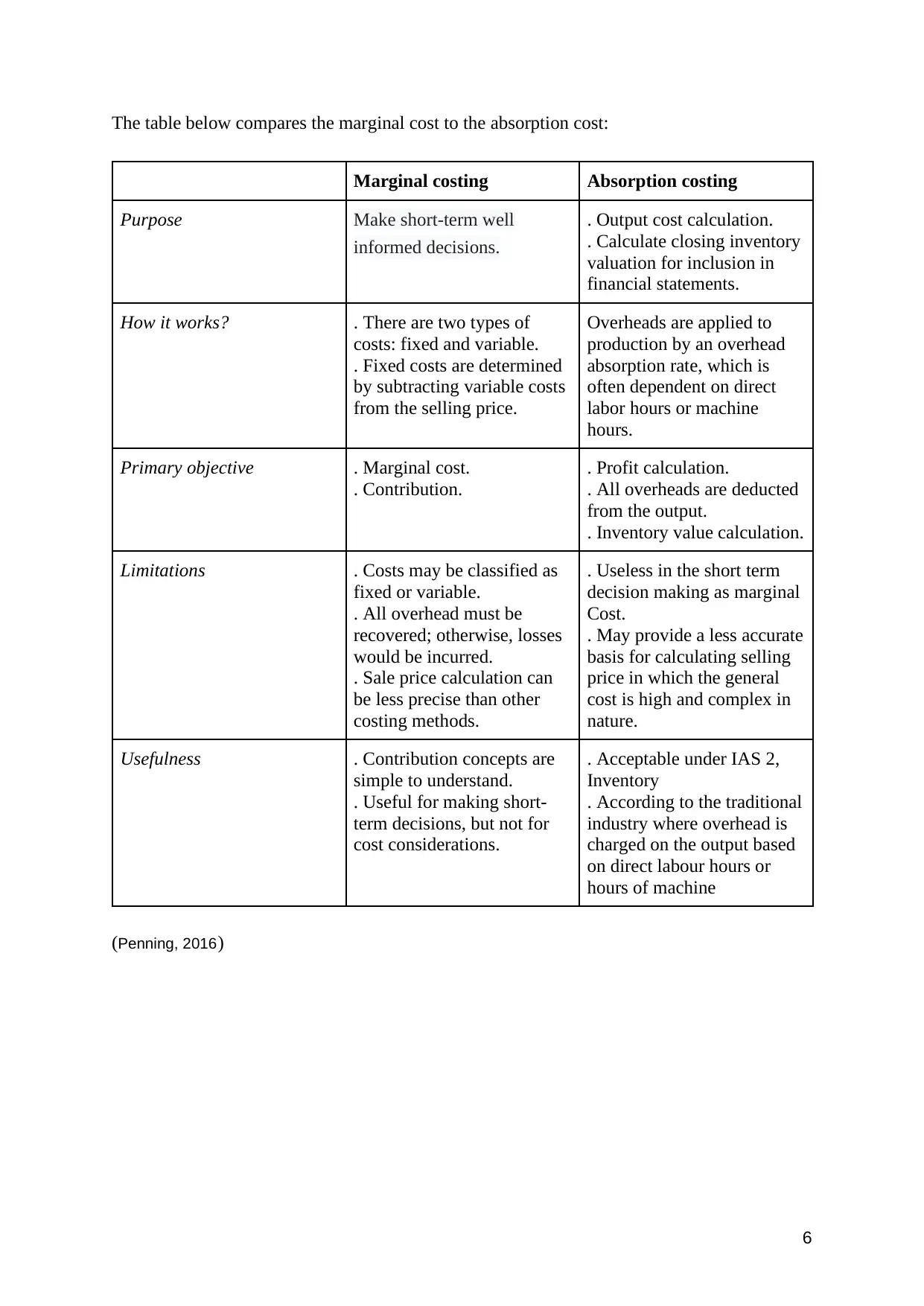

The table below compares the marginal cost to the absorption cost:

Marginal costing Absorption costing

Purpose Make short-term well

informed decisions.

. Output cost calculation.

. Calculate closing inventory

valuation for inclusion in

financial statements.

How it works? . There are two types of

costs: fixed and variable.

. Fixed costs are determined

by subtracting variable costs

from the selling price.

Overheads are applied to

production by an overhead

absorption rate, which is

often dependent on direct

labor hours or machine

hours.

Primary objective . Marginal cost.

. Contribution.

. Profit calculation.

. All overheads are deducted

from the output.

. Inventory value calculation.

Limitations . Costs may be classified as

fixed or variable.

. All overhead must be

recovered; otherwise, losses

would be incurred.

. Sale price calculation can

be less precise than other

costing methods.

. Useless in the short term

decision making as marginal

Cost.

. May provide a less accurate

basis for calculating selling

price in which the general

cost is high and complex in

nature.

Usefulness . Contribution concepts are

simple to understand.

. Useful for making short-

term decisions, but not for

cost considerations.

. Acceptable under IAS 2,

Inventory

. According to the traditional

industry where overhead is

charged on the output based

on direct labour hours or

hours of machine

(Penning, 2016)

The table below compares the marginal cost to the absorption cost:

Marginal costing Absorption costing

Purpose Make short-term well

informed decisions.

. Output cost calculation.

. Calculate closing inventory

valuation for inclusion in

financial statements.

How it works? . There are two types of

costs: fixed and variable.

. Fixed costs are determined

by subtracting variable costs

from the selling price.

Overheads are applied to

production by an overhead

absorption rate, which is

often dependent on direct

labor hours or machine

hours.

Primary objective . Marginal cost.

. Contribution.

. Profit calculation.

. All overheads are deducted

from the output.

. Inventory value calculation.

Limitations . Costs may be classified as

fixed or variable.

. All overhead must be

recovered; otherwise, losses

would be incurred.

. Sale price calculation can

be less precise than other

costing methods.

. Useless in the short term

decision making as marginal

Cost.

. May provide a less accurate

basis for calculating selling

price in which the general

cost is high and complex in

nature.

Usefulness . Contribution concepts are

simple to understand.

. Useful for making short-

term decisions, but not for

cost considerations.

. Acceptable under IAS 2,

Inventory

. According to the traditional

industry where overhead is

charged on the output based

on direct labour hours or

hours of machine

(Penning, 2016)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

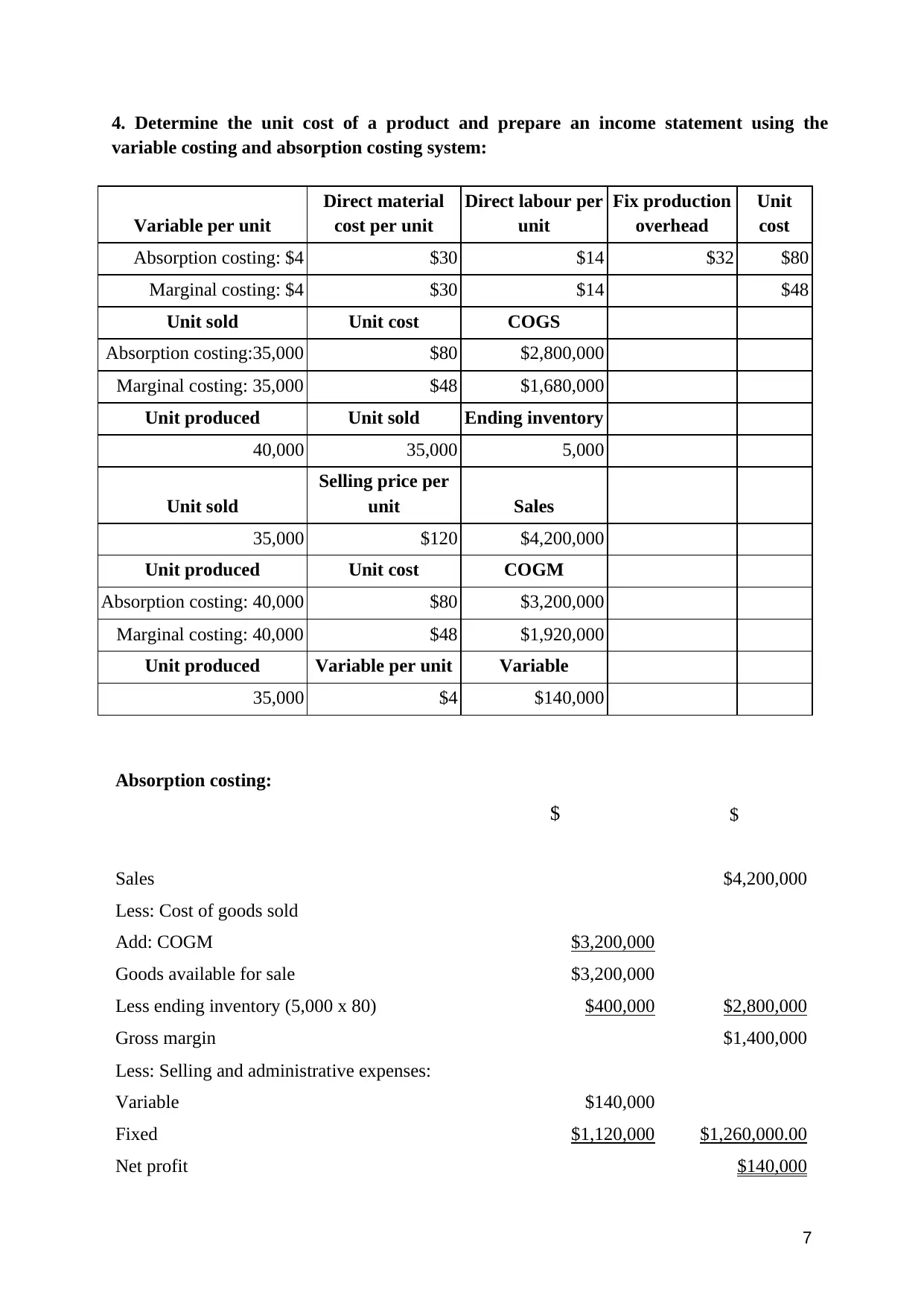

4. Determine the unit cost of a product and prepare an income statement using the

variable costing and absorption costing system:

Variable per unit

Direct material

cost per unit

Direct labour per

unit

Fix production

overhead

Unit

cost

Absorption costing: $4 $30 $14 $32 $80

Marginal costing: $4 $30 $14 $48

Unit sold Unit cost COGS

Absorption costing:35,000 $80 $2,800,000

Marginal costing: 35,000 $48 $1,680,000

Unit produced Unit sold Ending inventory

40,000 35,000 5,000

Unit sold

Selling price per

unit Sales

35,000 $120 $4,200,000

Unit produced Unit cost COGM

Absorption costing: 40,000 $80 $3,200,000

Marginal costing: 40,000 $48 $1,920,000

Unit produced Variable per unit Variable

35,000 $4 $140,000

Absorption costing:

$ $

Sales $4,200,000

Less: Cost of goods sold

Add: COGM $3,200,000

Goods available for sale $3,200,000

Less ending inventory (5,000 x 80) $400,000 $2,800,000

Gross margin $1,400,000

Less: Selling and administrative expenses:

Variable $140,000

Fixed $1,120,000 $1,260,000.00

Net profit $140,000

4. Determine the unit cost of a product and prepare an income statement using the

variable costing and absorption costing system:

Variable per unit

Direct material

cost per unit

Direct labour per

unit

Fix production

overhead

Unit

cost

Absorption costing: $4 $30 $14 $32 $80

Marginal costing: $4 $30 $14 $48

Unit sold Unit cost COGS

Absorption costing:35,000 $80 $2,800,000

Marginal costing: 35,000 $48 $1,680,000

Unit produced Unit sold Ending inventory

40,000 35,000 5,000

Unit sold

Selling price per

unit Sales

35,000 $120 $4,200,000

Unit produced Unit cost COGM

Absorption costing: 40,000 $80 $3,200,000

Marginal costing: 40,000 $48 $1,920,000

Unit produced Variable per unit Variable

35,000 $4 $140,000

Absorption costing:

$ $

Sales $4,200,000

Less: Cost of goods sold

Add: COGM $3,200,000

Goods available for sale $3,200,000

Less ending inventory (5,000 x 80) $400,000 $2,800,000

Gross margin $1,400,000

Less: Selling and administrative expenses:

Variable $140,000

Fixed $1,120,000 $1,260,000.00

Net profit $140,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

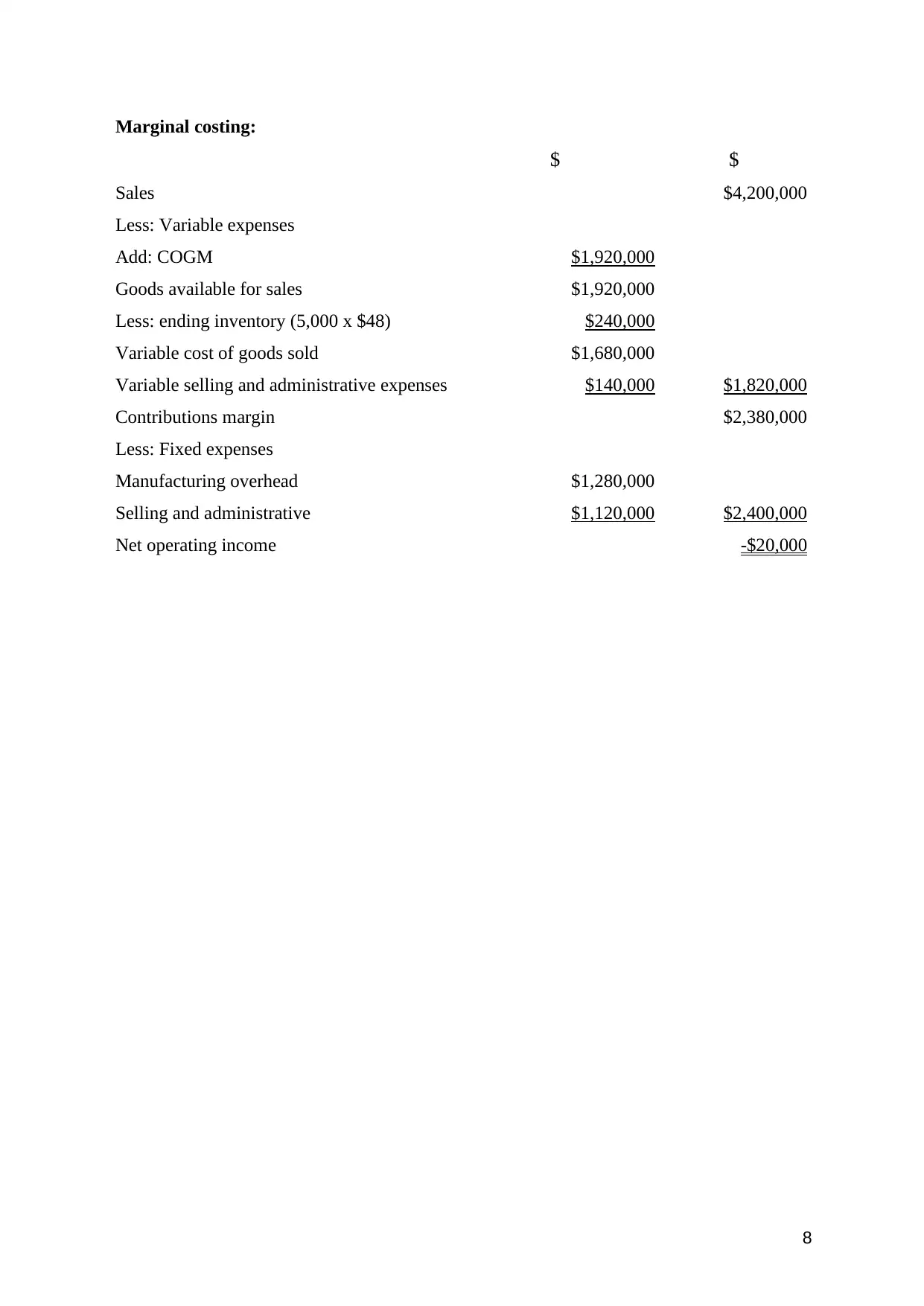

Marginal costing:

$ $

Sales $4,200,000

Less: Variable expenses

Add: COGM $1,920,000

Goods available for sales $1,920,000

Less: ending inventory (5,000 x $48) $240,000

Variable cost of goods sold $1,680,000

Variable selling and administrative expenses $140,000 $1,820,000

Contributions margin $2,380,000

Less: Fixed expenses

Manufacturing overhead $1,280,000

Selling and administrative $1,120,000 $2,400,000

Net operating income -$20,000

Marginal costing:

$ $

Sales $4,200,000

Less: Variable expenses

Add: COGM $1,920,000

Goods available for sales $1,920,000

Less: ending inventory (5,000 x $48) $240,000

Variable cost of goods sold $1,680,000

Variable selling and administrative expenses $140,000 $1,820,000

Contributions margin $2,380,000

Less: Fixed expenses

Manufacturing overhead $1,280,000

Selling and administrative $1,120,000 $2,400,000

Net operating income -$20,000

9

Reference list:

1. Accountlearning, n.d. Management Accounting | Advantages, Merits, Uses or Utility.

[online] Accountlearning.com. Available at:

<https://accountlearning.com/management-accounting-advantages-merits-uses-or-

utility/#:~:text=6.-

,Improvement%20of%20Efficiency,workers%20efficiency%20may%20be%20impro

ved.> [Accessed 30 April 2021].

2. CIMA, n.d. Global management accounting principles. [online] Cimaglobal.com.

Available at:

<https://www.cimaglobal.com/Documents/Employer%20docs/web%20pages%20201

6/global-management-accounting-principles.pdf> [Accessed 30 April 2021].

3. Dyson, J., n.d. Accounting for non-accounting students. 8th ed. [PDF] Pearson

education, p.274. Available at: <https://cdn.fbsbx.com/v/t59.2708-

21/33425409_783322745195093_5737467354107871232_n.pdf/Unit-10.-

Accounting-for-Non-Accounting-Students-8-edn.pdf?_nc_cat=102&ccb=1-

3&_nc_sid=0cab14&_nc_ohc=kZjOBOXGEesAX_l7_uR&_nc_ht=cdn.fbsbx.com&o

h=8433cc42b89ef822611fa1555981d073&oe=608BD7F2&dl=1> [Accessed 29 April

2021].

4. FreshBooks. n.d. What Is Management Accounting? | FreshBooks. [online] Available

at: <https://www.freshbooks.com/hub/accounting/management-

accounting#:~:text=estimated%20to%20be%3F-

,What%20Is%20a%20Management%20Accounting%20System%3F,and%20managin

g%20of%20their%20process.> [Accessed 7 May 2021].

5. Ghanbari, M. and Vaseli, S., 2015. The Role of Management Accounting in the

Organization. [online] Irjabs.com. Available at:

<https://irjabs.com/files_site/paperlist/r_2776_151211181647.pdf> [Accessed 30

April 2021].

6. Penning, A., 2016. Elements of costing tutorial. [PDF] p.207. Available at:

<https://www.osbornebooksshop.co.uk/files/acrt.pdf> [Accessed 25 April 2021].

7. Toppr. n.d. Meaning and Definition of Management Accounting. [online] Available

at: <https://www.toppr.com/guides/fundamentals-of-accounting/fundamentals-of-

cost-accounting/meaning-of-management-accounting/> [Accessed 30 April 2021].

8. Vitez, O., 2021. What are the Different Types of Management Accounting Systems?.

[online] Smart Capital Mind. Available at: <https://www.smartcapitalmind.com/what-

are-the-different-types-of-management-accounting-

systems.htm#:~:text=A%20few%20of%20the%20most,at%20the%20lowest%20cost

%20possible.> [Accessed 7 May 2021].

Reference list:

1. Accountlearning, n.d. Management Accounting | Advantages, Merits, Uses or Utility.

[online] Accountlearning.com. Available at:

<https://accountlearning.com/management-accounting-advantages-merits-uses-or-

utility/#:~:text=6.-

,Improvement%20of%20Efficiency,workers%20efficiency%20may%20be%20impro

ved.> [Accessed 30 April 2021].

2. CIMA, n.d. Global management accounting principles. [online] Cimaglobal.com.

Available at:

<https://www.cimaglobal.com/Documents/Employer%20docs/web%20pages%20201

6/global-management-accounting-principles.pdf> [Accessed 30 April 2021].

3. Dyson, J., n.d. Accounting for non-accounting students. 8th ed. [PDF] Pearson

education, p.274. Available at: <https://cdn.fbsbx.com/v/t59.2708-

21/33425409_783322745195093_5737467354107871232_n.pdf/Unit-10.-

Accounting-for-Non-Accounting-Students-8-edn.pdf?_nc_cat=102&ccb=1-

3&_nc_sid=0cab14&_nc_ohc=kZjOBOXGEesAX_l7_uR&_nc_ht=cdn.fbsbx.com&o

h=8433cc42b89ef822611fa1555981d073&oe=608BD7F2&dl=1> [Accessed 29 April

2021].

4. FreshBooks. n.d. What Is Management Accounting? | FreshBooks. [online] Available

at: <https://www.freshbooks.com/hub/accounting/management-

accounting#:~:text=estimated%20to%20be%3F-

,What%20Is%20a%20Management%20Accounting%20System%3F,and%20managin

g%20of%20their%20process.> [Accessed 7 May 2021].

5. Ghanbari, M. and Vaseli, S., 2015. The Role of Management Accounting in the

Organization. [online] Irjabs.com. Available at:

<https://irjabs.com/files_site/paperlist/r_2776_151211181647.pdf> [Accessed 30

April 2021].

6. Penning, A., 2016. Elements of costing tutorial. [PDF] p.207. Available at:

<https://www.osbornebooksshop.co.uk/files/acrt.pdf> [Accessed 25 April 2021].

7. Toppr. n.d. Meaning and Definition of Management Accounting. [online] Available

at: <https://www.toppr.com/guides/fundamentals-of-accounting/fundamentals-of-

cost-accounting/meaning-of-management-accounting/> [Accessed 30 April 2021].

8. Vitez, O., 2021. What are the Different Types of Management Accounting Systems?.

[online] Smart Capital Mind. Available at: <https://www.smartcapitalmind.com/what-

are-the-different-types-of-management-accounting-

systems.htm#:~:text=A%20few%20of%20the%20most,at%20the%20lowest%20cost

%20possible.> [Accessed 7 May 2021].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.