Management Accounting Analysis: Costing, Budgeting, and Variance

VerifiedAdded on 2020/01/28

|24

|6349

|83

Report

AI Summary

This report delves into the core principles of management accounting, offering a comprehensive analysis of cost behavior, profitability, and performance evaluation. The report begins by classifying costs into fixed, variable, and semi-variable categories for Columbus Ltd and Steel Ltd, followed by the computation of gross profits for both companies, demonstrating the application of marginal and absorption costing methods. The analysis extends to identifying different types of expenditure and constructing costing reports to evaluate performance indicators, emphasizing methods to reduce costs and enhance value and quality. Budgeting is explored, including its purpose, various methods, and a demonstration of flexible budgeting. Furthermore, the report incorporates variance analysis, evaluating Yuri Cutlery's budget and providing an operating statement and a memorandum report. The report highlights the importance of cost management tools in making effective decisions, managing financial prospects, and improving overall business efficiency.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................1

TASK 1: Analyze cost for Columbus Ltd.......................................................................................1

1.1 Classify costs into fixed, variable and semi variable.............................................................1

1.2 & 1.3 Computing gross profits for both Columbus Ltd and Steel Ltd..................................2

1.4 Identify the kinds of Expenditure..........................................................................................3

TASK 2: Costing reports for performance indicators......................................................................5

2.1 Cost of Production.................................................................................................................5

2.2 & 2.3 Performance indicators for improvement to reduce cost, enhance value and quality. 6

Task 3: Budgeting............................................................................................................................8

3.1 Purpose and nature of Budgeting...........................................................................................8

3.2 Budgeting methods................................................................................................................9

3.3 Demonstrating flexible budgeting.......................................................................................10

3.4 Flexible budget....................................................................................................................11

PART B (3.4).............................................................................................................................12

Task 4: Variance Analysis.............................................................................................................13

Part A) 4.1 Variance analysis of Yuri Cutlery budget...............................................................13

Part B) 4.2 Operating statement.................................................................................................14

4.3 Memorandum report............................................................................................................15

Conclusion.....................................................................................................................................17

References......................................................................................................................................18

Introduction......................................................................................................................................1

TASK 1: Analyze cost for Columbus Ltd.......................................................................................1

1.1 Classify costs into fixed, variable and semi variable.............................................................1

1.2 & 1.3 Computing gross profits for both Columbus Ltd and Steel Ltd..................................2

1.4 Identify the kinds of Expenditure..........................................................................................3

TASK 2: Costing reports for performance indicators......................................................................5

2.1 Cost of Production.................................................................................................................5

2.2 & 2.3 Performance indicators for improvement to reduce cost, enhance value and quality. 6

Task 3: Budgeting............................................................................................................................8

3.1 Purpose and nature of Budgeting...........................................................................................8

3.2 Budgeting methods................................................................................................................9

3.3 Demonstrating flexible budgeting.......................................................................................10

3.4 Flexible budget....................................................................................................................11

PART B (3.4).............................................................................................................................12

Task 4: Variance Analysis.............................................................................................................13

Part A) 4.1 Variance analysis of Yuri Cutlery budget...............................................................13

Part B) 4.2 Operating statement.................................................................................................14

4.3 Memorandum report............................................................................................................15

Conclusion.....................................................................................................................................17

References......................................................................................................................................18

INTRODUCTION

Looking at the present market conditions, the efficiency of enterprise depends upon the

ability of managers in understanding and applying the principles, approaches, methods of

modern management to carry out operations in ethical and reliable manner. However,

management accounting can be defined as the application of different principles of accounting

and financial management in order to create, procure, protect and enhance the value for money

of the associated stakeholders irrespective to the sector (Kaplanand Norton, 1993). The main

purpose of management accounting is to minimize the financial risks and uncertainties by

applying varied analytical tools and techniques.

In the current report, researcher focuses on cost information for both current and future of

the different business enterprises. Further, the main purpose of researcher behind carrying out

this study is to enhance understanding regarding how cost data is collected, compiled, analysed

and processed into information that is useful for business managers in making effective and

efficient decisions. Further, it consist of different costing and budgetary system and the cause of

resulting variances, together with the possible implications and potential measures undertaken by

managers of different organisations. However, in order to carry out financial aspects of different

operations in effective way it is important for the managers to have in-depth analysis of

management accounting.

TASK 1: ANALYZE COST FOR COLUMBUS LTD

1.1 Classify costs into fixed, variable and semi variable

Cost in general can be defined as the monetary measure of resources which are sacrificed

in order to achieve an objective. In context to a company, there are several costs associated with

it such as people employed, execution of operations, purchasing of raw materials etc. These

running or operating costs are defined as the accountants revenue expenditure which is important

for the company to incur for achieving desired results and outcomes (Hill, 2003). There are

different types of costs associated with the functioning of Columbus Ltd which are as follows:

On the basis of costing and pricing:

Direct costs:This type of costs can be defined as the combination of material, labour and

other overheads incurred or consumed in order to produce a particular unit of products

and services. Direct labour is the costs which is associated with the entire process of

production that company produces and for computing it managers undertake timesheet or

1

Looking at the present market conditions, the efficiency of enterprise depends upon the

ability of managers in understanding and applying the principles, approaches, methods of

modern management to carry out operations in ethical and reliable manner. However,

management accounting can be defined as the application of different principles of accounting

and financial management in order to create, procure, protect and enhance the value for money

of the associated stakeholders irrespective to the sector (Kaplanand Norton, 1993). The main

purpose of management accounting is to minimize the financial risks and uncertainties by

applying varied analytical tools and techniques.

In the current report, researcher focuses on cost information for both current and future of

the different business enterprises. Further, the main purpose of researcher behind carrying out

this study is to enhance understanding regarding how cost data is collected, compiled, analysed

and processed into information that is useful for business managers in making effective and

efficient decisions. Further, it consist of different costing and budgetary system and the cause of

resulting variances, together with the possible implications and potential measures undertaken by

managers of different organisations. However, in order to carry out financial aspects of different

operations in effective way it is important for the managers to have in-depth analysis of

management accounting.

TASK 1: ANALYZE COST FOR COLUMBUS LTD

1.1 Classify costs into fixed, variable and semi variable

Cost in general can be defined as the monetary measure of resources which are sacrificed

in order to achieve an objective. In context to a company, there are several costs associated with

it such as people employed, execution of operations, purchasing of raw materials etc. These

running or operating costs are defined as the accountants revenue expenditure which is important

for the company to incur for achieving desired results and outcomes (Hill, 2003). There are

different types of costs associated with the functioning of Columbus Ltd which are as follows:

On the basis of costing and pricing:

Direct costs:This type of costs can be defined as the combination of material, labour and

other overheads incurred or consumed in order to produce a particular unit of products

and services. Direct labour is the costs which is associated with the entire process of

production that company produces and for computing it managers undertake timesheet or

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

job cards on the basis of which remuneration is decided. Further, direct material is cost

that Columbus Ltd incur at time of purchasing raw materials which are used for

producing finished products. Lastly, direct overheads are those which are apart from

labour and material that Columbus Ltd has to incur in order to carry out production

process e.g. rent and equipment maintenance.

Indirect costs:This type of costs consist of materials and labour that are not directly made

used in producing a unit of products and services (Bevilacqua, Ciarapicaand Giacchetta,

2007). However, they are firstly charged to the cost centres and then split over the

products and services.

On the basis of behaviour:

Fixed costs: These are the costs which remains the same despite of change in level of

production. According to the given scenario, manufacturing costs can be defined as the

fixed costs for the Columbus Ltd.

Variable costs: these are the direct and indirect cost that changes with the alteration in

level of production. Herein, direct material cost refers to the variable costs for

theColumbus Ltd as it changes with the level of production.

Semi-variable costs:It is the combination of fixed and variable costs as in this, cost is

fixed at certain level of production or consumption and once the level is crossed it

becomes variable and increases with the level of production.

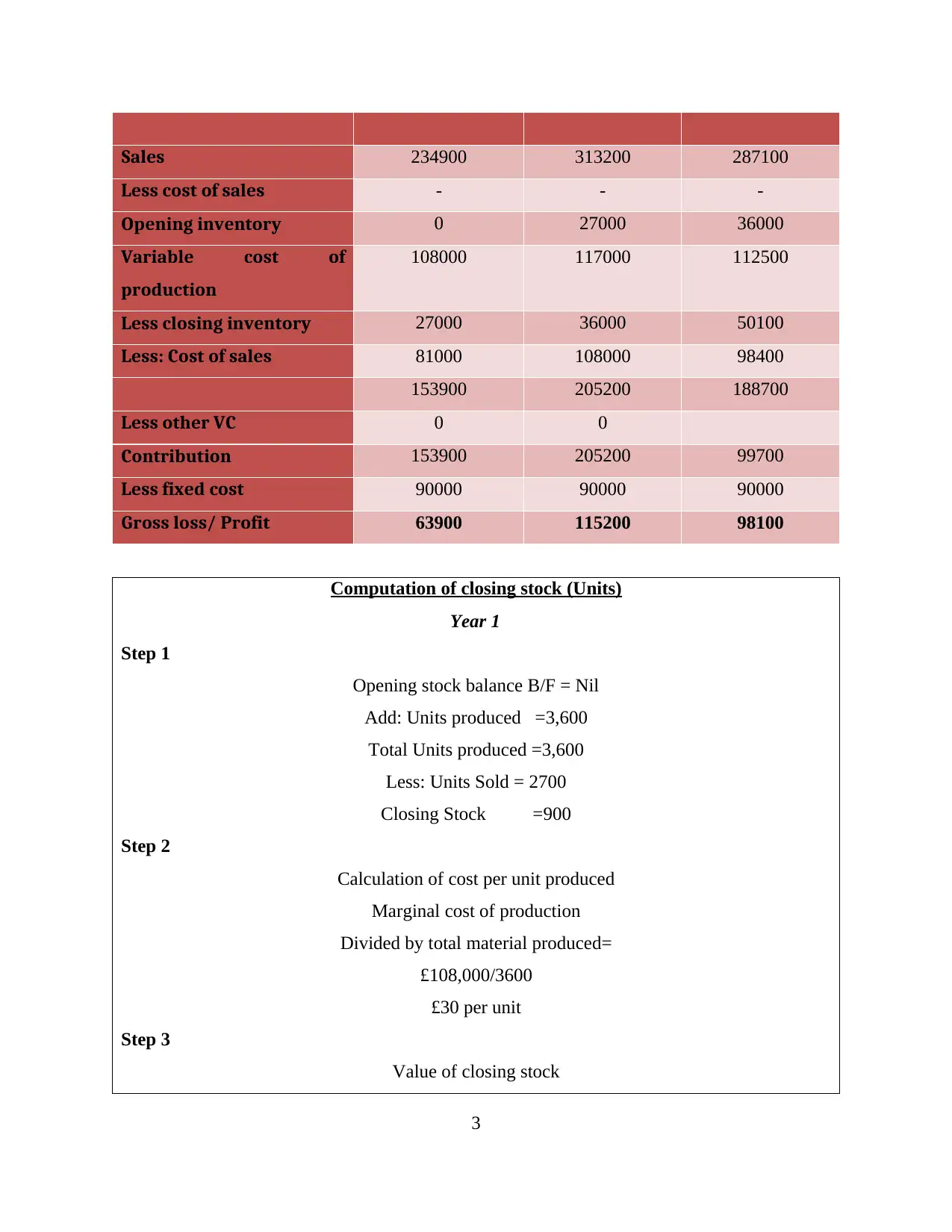

1.2 & 1.3 Computing gross profits for both Columbus Ltd and Steel Ltd

In general, marginal costs can be defined as the change in the total expenditure due to

increase in production units. However, in order to compute gross profit, cost management tools

is used by the mangers because it assist in analysing the expenditure and revenue information

which includes all the associated variable cost and provide contribution at the end. Further,

absorption cost is the expenditure that includes both variable and fixed expenses (Islam and

Dellaportas, 2011). However, the main aim of manager behind indulging absorption cost is that it

helps in controlling and managing the expenditure of the company in order to complete the

operations appropriately. Through the means of this, managers can easily make smart and

effective decisions regarding managing financial prospects of manufacturing unit.

Gross profit calculation of Columbus Ltd:

Particulars Year 1 Year 2 Year 3

2

that Columbus Ltd incur at time of purchasing raw materials which are used for

producing finished products. Lastly, direct overheads are those which are apart from

labour and material that Columbus Ltd has to incur in order to carry out production

process e.g. rent and equipment maintenance.

Indirect costs:This type of costs consist of materials and labour that are not directly made

used in producing a unit of products and services (Bevilacqua, Ciarapicaand Giacchetta,

2007). However, they are firstly charged to the cost centres and then split over the

products and services.

On the basis of behaviour:

Fixed costs: These are the costs which remains the same despite of change in level of

production. According to the given scenario, manufacturing costs can be defined as the

fixed costs for the Columbus Ltd.

Variable costs: these are the direct and indirect cost that changes with the alteration in

level of production. Herein, direct material cost refers to the variable costs for

theColumbus Ltd as it changes with the level of production.

Semi-variable costs:It is the combination of fixed and variable costs as in this, cost is

fixed at certain level of production or consumption and once the level is crossed it

becomes variable and increases with the level of production.

1.2 & 1.3 Computing gross profits for both Columbus Ltd and Steel Ltd

In general, marginal costs can be defined as the change in the total expenditure due to

increase in production units. However, in order to compute gross profit, cost management tools

is used by the mangers because it assist in analysing the expenditure and revenue information

which includes all the associated variable cost and provide contribution at the end. Further,

absorption cost is the expenditure that includes both variable and fixed expenses (Islam and

Dellaportas, 2011). However, the main aim of manager behind indulging absorption cost is that it

helps in controlling and managing the expenditure of the company in order to complete the

operations appropriately. Through the means of this, managers can easily make smart and

effective decisions regarding managing financial prospects of manufacturing unit.

Gross profit calculation of Columbus Ltd:

Particulars Year 1 Year 2 Year 3

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales 234900 313200 287100

Less cost of sales - - -

Opening inventory 0 27000 36000

Variable cost of

production

108000 117000 112500

Less closing inventory 27000 36000 50100

Less: Cost of sales 81000 108000 98400

153900 205200 188700

Less other VC 0 0

Contribution 153900 205200 99700

Less fixed cost 90000 90000 90000

Gross loss/ Profit 63900 115200 98100

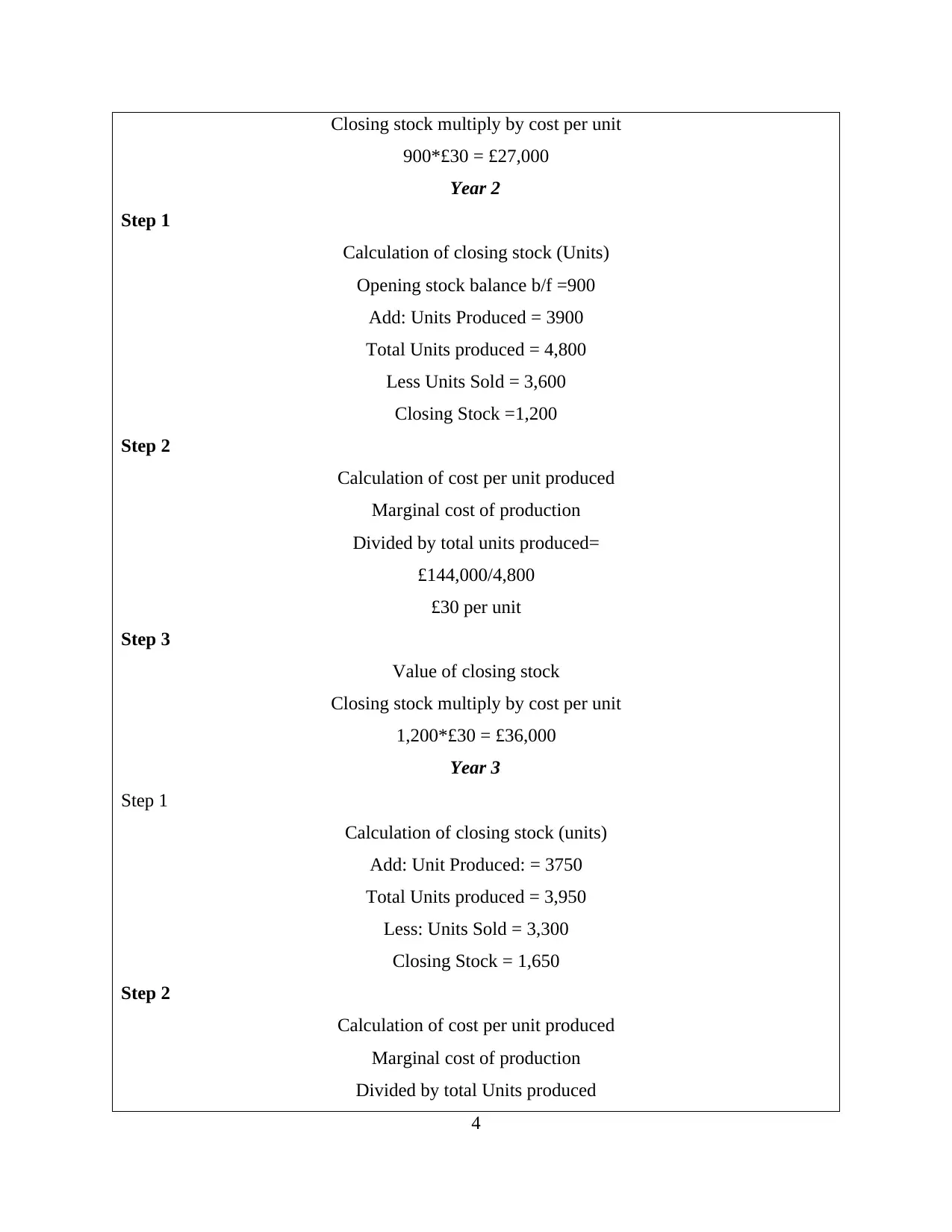

Computation of closing stock (Units)

Year 1

Step 1

Opening stock balance B/F = Nil

Add: Units produced =3,600

Total Units produced =3,600

Less: Units Sold = 2700

Closing Stock =900

Step 2

Calculation of cost per unit produced

Marginal cost of production

Divided by total material produced=

£108,000/3600

£30 per unit

Step 3

Value of closing stock

3

Less cost of sales - - -

Opening inventory 0 27000 36000

Variable cost of

production

108000 117000 112500

Less closing inventory 27000 36000 50100

Less: Cost of sales 81000 108000 98400

153900 205200 188700

Less other VC 0 0

Contribution 153900 205200 99700

Less fixed cost 90000 90000 90000

Gross loss/ Profit 63900 115200 98100

Computation of closing stock (Units)

Year 1

Step 1

Opening stock balance B/F = Nil

Add: Units produced =3,600

Total Units produced =3,600

Less: Units Sold = 2700

Closing Stock =900

Step 2

Calculation of cost per unit produced

Marginal cost of production

Divided by total material produced=

£108,000/3600

£30 per unit

Step 3

Value of closing stock

3

Closing stock multiply by cost per unit

900*£30 = £27,000

Year 2

Step 1

Calculation of closing stock (Units)

Opening stock balance b/f =900

Add: Units Produced = 3900

Total Units produced = 4,800

Less Units Sold = 3,600

Closing Stock =1,200

Step 2

Calculation of cost per unit produced

Marginal cost of production

Divided by total units produced=

£144,000/4,800

£30 per unit

Step 3

Value of closing stock

Closing stock multiply by cost per unit

1,200*£30 = £36,000

Year 3

Step 1

Calculation of closing stock (units)

Add: Unit Produced: = 3750

Total Units produced = 3,950

Less: Units Sold = 3,300

Closing Stock = 1,650

Step 2

Calculation of cost per unit produced

Marginal cost of production

Divided by total Units produced

4

900*£30 = £27,000

Year 2

Step 1

Calculation of closing stock (Units)

Opening stock balance b/f =900

Add: Units Produced = 3900

Total Units produced = 4,800

Less Units Sold = 3,600

Closing Stock =1,200

Step 2

Calculation of cost per unit produced

Marginal cost of production

Divided by total units produced=

£144,000/4,800

£30 per unit

Step 3

Value of closing stock

Closing stock multiply by cost per unit

1,200*£30 = £36,000

Year 3

Step 1

Calculation of closing stock (units)

Add: Unit Produced: = 3750

Total Units produced = 3,950

Less: Units Sold = 3,300

Closing Stock = 1,650

Step 2

Calculation of cost per unit produced

Marginal cost of production

Divided by total Units produced

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

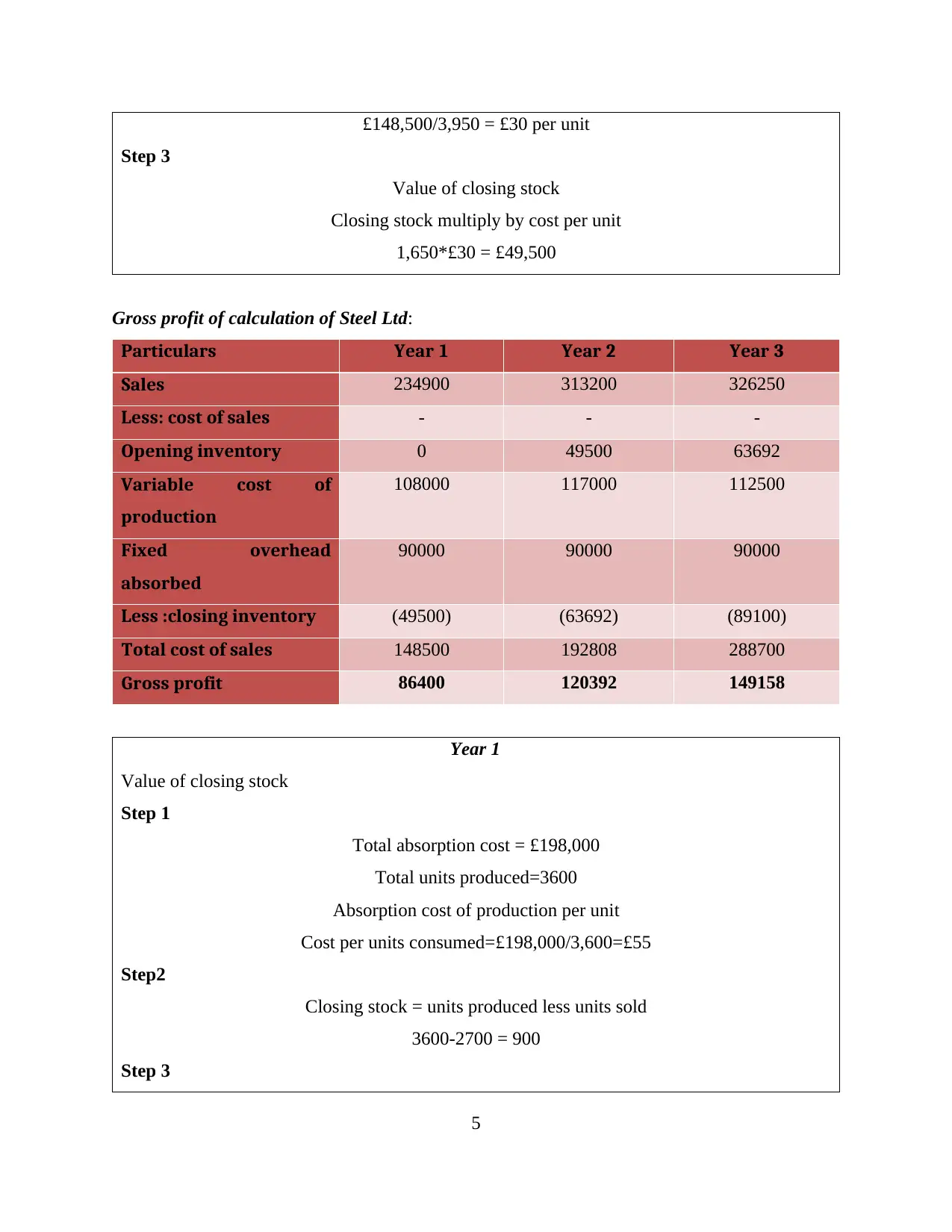

£148,500/3,950 = £30 per unit

Step 3

Value of closing stock

Closing stock multiply by cost per unit

1,650*£30 = £49,500

Gross profit of calculation of Steel Ltd:

Particulars Year 1 Year 2 Year 3

Sales 234900 313200 326250

Less: cost of sales - - -

Opening inventory 0 49500 63692

Variable cost of

production

108000 117000 112500

Fixed overhead

absorbed

90000 90000 90000

Less :closing inventory (49500) (63692) (89100)

Total cost of sales 148500 192808 288700

Gross profit 86400 120392 149158

Year 1

Value of closing stock

Step 1

Total absorption cost = £198,000

Total units produced=3600

Absorption cost of production per unit

Cost per units consumed=£198,000/3,600=£55

Step2

Closing stock = units produced less units sold

3600-2700 = 900

Step 3

5

Step 3

Value of closing stock

Closing stock multiply by cost per unit

1,650*£30 = £49,500

Gross profit of calculation of Steel Ltd:

Particulars Year 1 Year 2 Year 3

Sales 234900 313200 326250

Less: cost of sales - - -

Opening inventory 0 49500 63692

Variable cost of

production

108000 117000 112500

Fixed overhead

absorbed

90000 90000 90000

Less :closing inventory (49500) (63692) (89100)

Total cost of sales 148500 192808 288700

Gross profit 86400 120392 149158

Year 1

Value of closing stock

Step 1

Total absorption cost = £198,000

Total units produced=3600

Absorption cost of production per unit

Cost per units consumed=£198,000/3,600=£55

Step2

Closing stock = units produced less units sold

3600-2700 = 900

Step 3

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

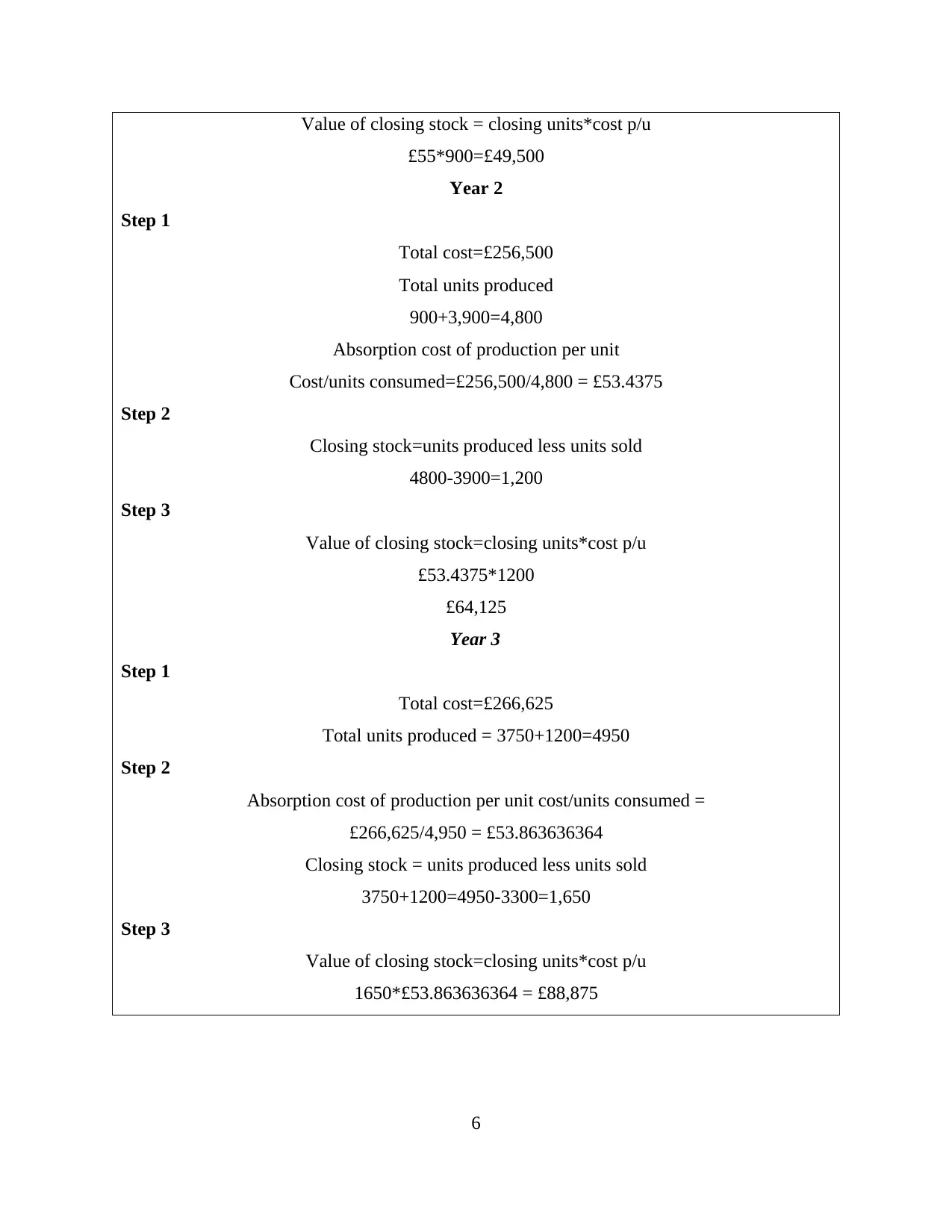

Value of closing stock = closing units*cost p/u

£55*900=£49,500

Year 2

Step 1

Total cost=£256,500

Total units produced

900+3,900=4,800

Absorption cost of production per unit

Cost/units consumed=£256,500/4,800 = £53.4375

Step 2

Closing stock=units produced less units sold

4800-3900=1,200

Step 3

Value of closing stock=closing units*cost p/u

£53.4375*1200

£64,125

Year 3

Step 1

Total cost=£266,625

Total units produced = 3750+1200=4950

Step 2

Absorption cost of production per unit cost/units consumed =

£266,625/4,950 = £53.863636364

Closing stock = units produced less units sold

3750+1200=4950-3300=1,650

Step 3

Value of closing stock=closing units*cost p/u

1650*£53.863636364 = £88,875

6

£55*900=£49,500

Year 2

Step 1

Total cost=£256,500

Total units produced

900+3,900=4,800

Absorption cost of production per unit

Cost/units consumed=£256,500/4,800 = £53.4375

Step 2

Closing stock=units produced less units sold

4800-3900=1,200

Step 3

Value of closing stock=closing units*cost p/u

£53.4375*1200

£64,125

Year 3

Step 1

Total cost=£266,625

Total units produced = 3750+1200=4950

Step 2

Absorption cost of production per unit cost/units consumed =

£266,625/4,950 = £53.863636364

Closing stock = units produced less units sold

3750+1200=4950-3300=1,650

Step 3

Value of closing stock=closing units*cost p/u

1650*£53.863636364 = £88,875

6

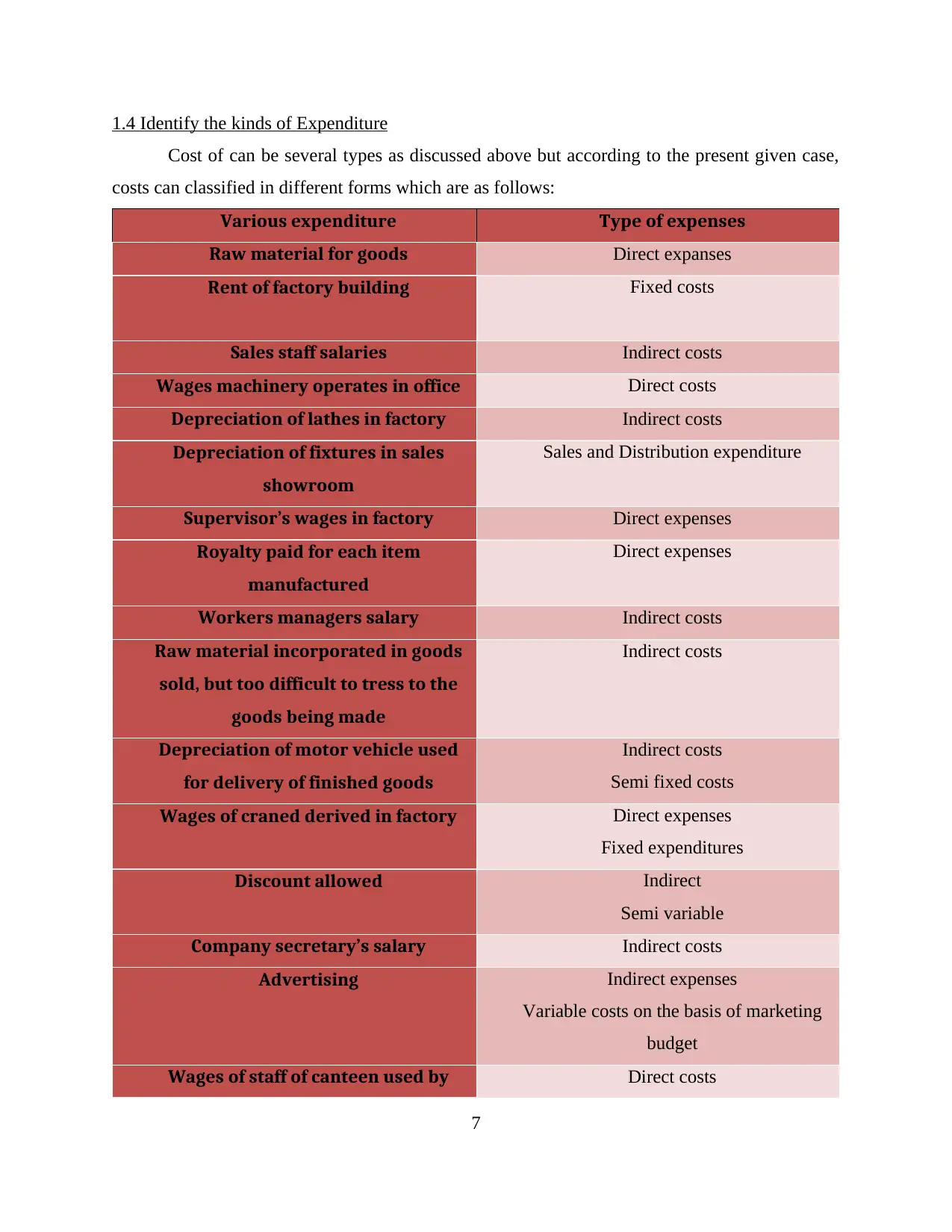

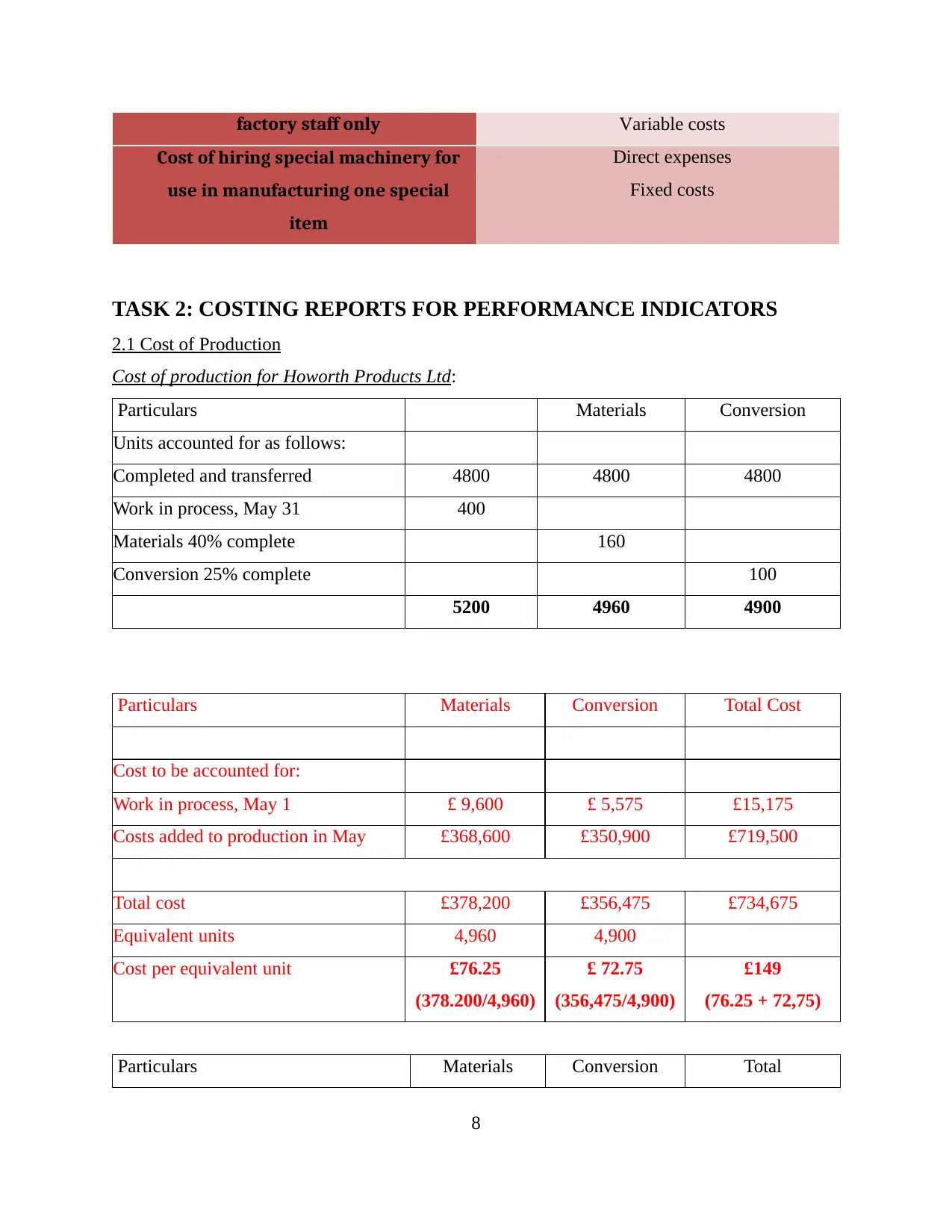

1.4 Identify the kinds of Expenditure

Cost of can be several types as discussed above but according to the present given case,

costs can classified in different forms which are as follows:

Various expenditure Type of expenses

Raw material for goods Direct expanses

Rent of factory building Fixed costs

Sales staff salaries Indirect costs

Wages machinery operates in office Direct costs

Depreciation of lathes in factory Indirect costs

Depreciation of fixtures in sales

showroom

Sales and Distribution expenditure

Supervisor’s wages in factory Direct expenses

Royalty paid for each item

manufactured

Direct expenses

Workers managers salary Indirect costs

Raw material incorporated in goods

sold, but too difficult to tress to the

goods being made

Indirect costs

Depreciation of motor vehicle used

for delivery of finished goods

Indirect costs

Semi fixed costs

Wages of craned derived in factory Direct expenses

Fixed expenditures

Discount allowed Indirect

Semi variable

Company secretary’s salary Indirect costs

Advertising Indirect expenses

Variable costs on the basis of marketing

budget

Wages of staff of canteen used by Direct costs

7

Cost of can be several types as discussed above but according to the present given case,

costs can classified in different forms which are as follows:

Various expenditure Type of expenses

Raw material for goods Direct expanses

Rent of factory building Fixed costs

Sales staff salaries Indirect costs

Wages machinery operates in office Direct costs

Depreciation of lathes in factory Indirect costs

Depreciation of fixtures in sales

showroom

Sales and Distribution expenditure

Supervisor’s wages in factory Direct expenses

Royalty paid for each item

manufactured

Direct expenses

Workers managers salary Indirect costs

Raw material incorporated in goods

sold, but too difficult to tress to the

goods being made

Indirect costs

Depreciation of motor vehicle used

for delivery of finished goods

Indirect costs

Semi fixed costs

Wages of craned derived in factory Direct expenses

Fixed expenditures

Discount allowed Indirect

Semi variable

Company secretary’s salary Indirect costs

Advertising Indirect expenses

Variable costs on the basis of marketing

budget

Wages of staff of canteen used by Direct costs

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

factory staff only Variable costs

Cost of hiring special machinery for

use in manufacturing one special

item

Direct expenses

Fixed costs

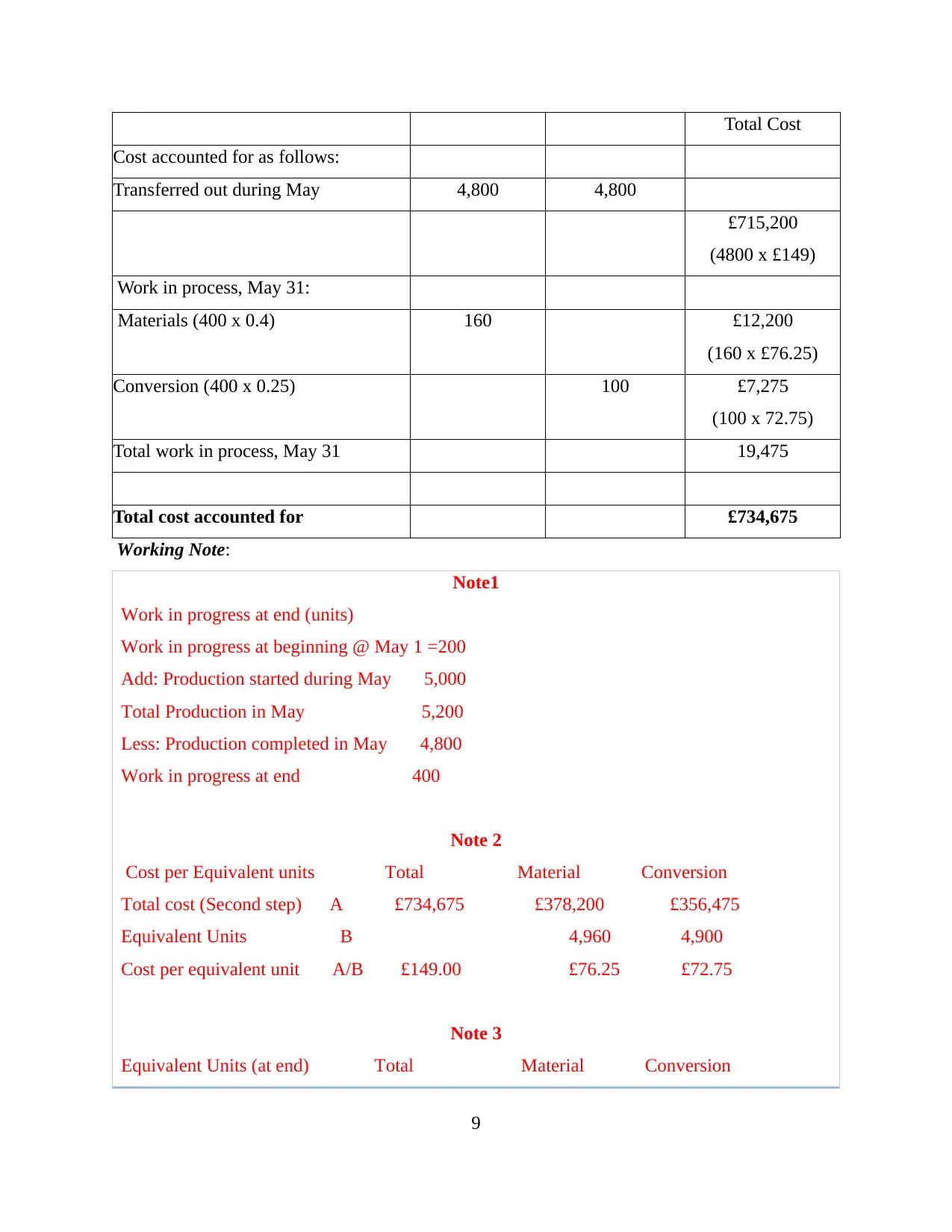

TASK 2: COSTING REPORTS FOR PERFORMANCE INDICATORS

2.1 Cost of Production

Cost of production for Howorth Products Ltd:

Particulars Materials Conversion

Units accounted for as follows:

Completed and transferred 4800 4800 4800

Work in process, May 31 400

Materials 40% complete 160

Conversion 25% complete 100

5200 4960 4900

Particulars Materials Conversion Total Cost

Cost to be accounted for:

Work in process, May 1 £ 9,600 £ 5,575 £15,175

Costs added to production in May £368,600 £350,900 £719,500

Total cost £378,200 £356,475 £734,675

Equivalent units 4,960 4,900

Cost per equivalent unit £76.25

(378.200/4,960)

£ 72.75

(356,475/4,900)

£149

(76.25 + 72,75)

Particulars Materials Conversion Total

8

Cost of hiring special machinery for

use in manufacturing one special

item

Direct expenses

Fixed costs

TASK 2: COSTING REPORTS FOR PERFORMANCE INDICATORS

2.1 Cost of Production

Cost of production for Howorth Products Ltd:

Particulars Materials Conversion

Units accounted for as follows:

Completed and transferred 4800 4800 4800

Work in process, May 31 400

Materials 40% complete 160

Conversion 25% complete 100

5200 4960 4900

Particulars Materials Conversion Total Cost

Cost to be accounted for:

Work in process, May 1 £ 9,600 £ 5,575 £15,175

Costs added to production in May £368,600 £350,900 £719,500

Total cost £378,200 £356,475 £734,675

Equivalent units 4,960 4,900

Cost per equivalent unit £76.25

(378.200/4,960)

£ 72.75

(356,475/4,900)

£149

(76.25 + 72,75)

Particulars Materials Conversion Total

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total Cost

Cost accounted for as follows:

Transferred out during May 4,800 4,800

£715,200

(4800 x £149)

Work in process, May 31:

Materials (400 x 0.4) 160 £12,200

(160 x £76.25)

Conversion (400 x 0.25) 100 £7,275

(100 x 72.75)

Total work in process, May 31 19,475

Total cost accounted for £734,675

Working Note:

Note1

Work in progress at end (units)

Work in progress at beginning @ May 1 =200

Add: Production started during May 5,000

Total Production in May 5,200

Less: Production completed in May 4,800

Work in progress at end 400

Note 2

Cost per Equivalent units Total Material Conversion

Total cost (Second step) A £734,675 £378,200 £356,475

Equivalent Units B 4,960 4,900

Cost per equivalent unit A/B £149.00 £76.25 £72.75

Note 3

Equivalent Units (at end) Total Material Conversion

9

Cost accounted for as follows:

Transferred out during May 4,800 4,800

£715,200

(4800 x £149)

Work in process, May 31:

Materials (400 x 0.4) 160 £12,200

(160 x £76.25)

Conversion (400 x 0.25) 100 £7,275

(100 x 72.75)

Total work in process, May 31 19,475

Total cost accounted for £734,675

Working Note:

Note1

Work in progress at end (units)

Work in progress at beginning @ May 1 =200

Add: Production started during May 5,000

Total Production in May 5,200

Less: Production completed in May 4,800

Work in progress at end 400

Note 2

Cost per Equivalent units Total Material Conversion

Total cost (Second step) A £734,675 £378,200 £356,475

Equivalent Units B 4,960 4,900

Cost per equivalent unit A/B £149.00 £76.25 £72.75

Note 3

Equivalent Units (at end) Total Material Conversion

9

400 - -

Material(40% complete) 400*40% 160 -

Conversion(25%complete)400*25% - 100

Total unit 160 100

Note 4

Equivalent unit costs(Total) Material Conversion

Cost per unit multiply by equivalent units

Material (£76.25*160) Note 2*Note3 £12,200 -

Conversion(£72.75*100) Note 2*Note3 - £7,275

Note 5

Total Cost Accounted:

Effective units Materials Conversion Effective rate P/U Total cost

£ £

4,800 4,800 4,800 149.00 715,200

- 160 - 76.25 12,200

- - 100 72.75 7,275

Total 4,960 4,900 734,675

From the above computation of production cost for Howorth Products Ltd it has been

analysed that the materials and conversion work in progress are 70% and 45% respectively that

has been completed during the month of May. However, production manager of Howorth

Products Ltd expected to produce 5000 units at the beginning of the month but was only able to

produce 4800 units during the course of month. Henceforth, it can be said that, cost of

unproduced 200 units will not be counted within the month of May which leads the cited firm to

incur total costs of £734675.

2.2 & 2.3 Performance indicators for improvement to reduce cost, enhance value and quality

It is essential for a firm to evaluate its performance at constant basis so as to identify and

ensure that its operations are functioning as per the competitive market. However, performance

indicators is considered asthe important tool for analysing the current position of business

10

Material(40% complete) 400*40% 160 -

Conversion(25%complete)400*25% - 100

Total unit 160 100

Note 4

Equivalent unit costs(Total) Material Conversion

Cost per unit multiply by equivalent units

Material (£76.25*160) Note 2*Note3 £12,200 -

Conversion(£72.75*100) Note 2*Note3 - £7,275

Note 5

Total Cost Accounted:

Effective units Materials Conversion Effective rate P/U Total cost

£ £

4,800 4,800 4,800 149.00 715,200

- 160 - 76.25 12,200

- - 100 72.75 7,275

Total 4,960 4,900 734,675

From the above computation of production cost for Howorth Products Ltd it has been

analysed that the materials and conversion work in progress are 70% and 45% respectively that

has been completed during the month of May. However, production manager of Howorth

Products Ltd expected to produce 5000 units at the beginning of the month but was only able to

produce 4800 units during the course of month. Henceforth, it can be said that, cost of

unproduced 200 units will not be counted within the month of May which leads the cited firm to

incur total costs of £734675.

2.2 & 2.3 Performance indicators for improvement to reduce cost, enhance value and quality

It is essential for a firm to evaluate its performance at constant basis so as to identify and

ensure that its operations are functioning as per the competitive market. However, performance

indicators is considered asthe important tool for analysing the current position of business

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.