Management Accounting Report: Techniques of Cost Analysis, Oshodi PLC

VerifiedAdded on 2021/02/19

|20

|4859

|21

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on Oshodi PLC. It delves into various aspects, including different types of management accounting, methods of reporting, and the application of cost analysis techniques such as absorption and marginal costing. The report includes the calculation of income statements using both methods. Furthermore, it explores the advantages and disadvantages of planning tools used for budgetary control and examines how organizations adapt their management accounting systems to address financial issues. The report also covers cost accounting systems, inventory management, job costing, and price optimization, providing a holistic understanding of the subject matter. The report concludes with an overview of the impact of management accounting on decision-making within the organization.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1 Management accounting and essential requirements of different types of management

accounting...............................................................................................................................1

P2 Different methods for management accounting reporting................................................3

LO2..................................................................................................................................................4

P3 Calculate costs using appropriate techniques of cost analysis to prepare

an income statement using marginal and absorption costs...........................4

LO3..................................................................................................................................................8

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control....................................................................................................................8

LO4................................................................................................................................................11

P5 Compare how organisations are adapting management accounting systems to respond to

financial issues......................................................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

Books and journals...............................................................................................................15

Appendix........................................................................................................................................15

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1 Management accounting and essential requirements of different types of management

accounting...............................................................................................................................1

P2 Different methods for management accounting reporting................................................3

LO2..................................................................................................................................................4

P3 Calculate costs using appropriate techniques of cost analysis to prepare

an income statement using marginal and absorption costs...........................4

LO3..................................................................................................................................................8

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control....................................................................................................................8

LO4................................................................................................................................................11

P5 Compare how organisations are adapting management accounting systems to respond to

financial issues......................................................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

Books and journals...............................................................................................................15

Appendix........................................................................................................................................15

INTRODUCTION

Management accounting is a process of preparing financial report to assist the management team

to make policies to control business operations. Financial information helps in making strategic

decisions. It helps in evaluating the performance of the company by analysing previous year data

with the actual data. Present report is based on Oshodi PLC which is a juice manufacturing

company. Report contains the concept of management accounting, different types of

management accounting, methods of reporting. Report will include the techniques of cost

analysis i.e. absorption and marginal costing, calculation of income statement is presented by

both the methods. Further report also contains the how organisations adopt accounting systems to

respond to financial issues(Kaplan and Atkinson, 2015).

LO1

P1 Management accounting and essential requirements of different types of management

accounting.

It lays down the procedure for applying knowledge and professional expertise for

preparing the accounting plus financial information in a way assisting the management team to

formulate policies and to control the industrial operations of the firm. Process that helps the

mangers in making managerial decisions with the help of financial information and the

resources, management accounting is also referred as managerial accounting. Management

accounting is for the internal management team of the company and this difference makes it

stand apart from the financial accounting process. Finance administration discuss reports such as

financial statements, reports of the revenues and the other transactional reports with the

management accounting team of the organisation. Motive of management accounting is to take

exact and effective decision with help of statistical data to control the business enterprise.

Management accounting lays down the procedure for presenting financial data and the business

operations to help the management team to make decisions.

Types of management accounting system

Cost-accounting systems

Inventory management systems

Job-costing systems

price-optimising system

1

Management accounting is a process of preparing financial report to assist the management team

to make policies to control business operations. Financial information helps in making strategic

decisions. It helps in evaluating the performance of the company by analysing previous year data

with the actual data. Present report is based on Oshodi PLC which is a juice manufacturing

company. Report contains the concept of management accounting, different types of

management accounting, methods of reporting. Report will include the techniques of cost

analysis i.e. absorption and marginal costing, calculation of income statement is presented by

both the methods. Further report also contains the how organisations adopt accounting systems to

respond to financial issues(Kaplan and Atkinson, 2015).

LO1

P1 Management accounting and essential requirements of different types of management

accounting.

It lays down the procedure for applying knowledge and professional expertise for

preparing the accounting plus financial information in a way assisting the management team to

formulate policies and to control the industrial operations of the firm. Process that helps the

mangers in making managerial decisions with the help of financial information and the

resources, management accounting is also referred as managerial accounting. Management

accounting is for the internal management team of the company and this difference makes it

stand apart from the financial accounting process. Finance administration discuss reports such as

financial statements, reports of the revenues and the other transactional reports with the

management accounting team of the organisation. Motive of management accounting is to take

exact and effective decision with help of statistical data to control the business enterprise.

Management accounting lays down the procedure for presenting financial data and the business

operations to help the management team to make decisions.

Types of management accounting system

Cost-accounting systems

Inventory management systems

Job-costing systems

price-optimising system

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost Accounting System

Cost accounting is a branch of management accounting which is concerned with

classifying, allocating and recording the present and the future prospective costs. At the present

times it is considered to be the essential part of business management as the organisations are

highly benefited by applying cost accounting(Merchant and White, 2017). It helps the

organisation to classify its costs along with its recording. Management are able to classify its

costs into direct, prime, factory etc. Such allocation helps the organisation in controlling its costs

and to determine the profitability from the operations . Cost accounting also helps the

organisation to have a control over its various cost s such as material labour and other factory

overheads. It helps the organisation to set standards to increase its efficiency and to manage its

operations to achieve the set standards.

Inventory Management System

Inventory management helps the organisation to mange stocks of the business and

keeping the track records of the inventory of the business. Inventory management also helps the

company to be aware of its stock requirement and to order stocks on time without impacting the

production process. They have a major importance in the industries such as food and beverages,

health care etc. An active stock management system keeps the track records of the inventory fro

its entrance in the factory to the warehouse and from warehouse to the customers. Proper

inventory management system helps the company in keeping its business well maintained.

Updated records help the company to know its inventory requirements and to fulfil the

requirement on time without breaking the production process. Companies can maintain reorder

level, safety stock and to know the break even points.

Job Costing System

Job Costing helps the organisations to use cost records to know the profit margins of each

job and to compare it with budgeted profit margins. It is defined as the process of gathering

information about production and service activities and the costs connected with each activity. It

helps the organisation to know the reliability of the estimate made by it. The prices quoted

should be bale to acquire a reasonable profit for the company. It mainly helps the organisation in

maintaining three types of records such as direct materials to have the records of the

consumption of the materials, direct labour for getting the exact labour costings to the company

and the other overhead costs applied in manufacturing process(Schaltegger and Burritt, 2017).

2

Cost accounting is a branch of management accounting which is concerned with

classifying, allocating and recording the present and the future prospective costs. At the present

times it is considered to be the essential part of business management as the organisations are

highly benefited by applying cost accounting(Merchant and White, 2017). It helps the

organisation to classify its costs along with its recording. Management are able to classify its

costs into direct, prime, factory etc. Such allocation helps the organisation in controlling its costs

and to determine the profitability from the operations . Cost accounting also helps the

organisation to have a control over its various cost s such as material labour and other factory

overheads. It helps the organisation to set standards to increase its efficiency and to manage its

operations to achieve the set standards.

Inventory Management System

Inventory management helps the organisation to mange stocks of the business and

keeping the track records of the inventory of the business. Inventory management also helps the

company to be aware of its stock requirement and to order stocks on time without impacting the

production process. They have a major importance in the industries such as food and beverages,

health care etc. An active stock management system keeps the track records of the inventory fro

its entrance in the factory to the warehouse and from warehouse to the customers. Proper

inventory management system helps the company in keeping its business well maintained.

Updated records help the company to know its inventory requirements and to fulfil the

requirement on time without breaking the production process. Companies can maintain reorder

level, safety stock and to know the break even points.

Job Costing System

Job Costing helps the organisations to use cost records to know the profit margins of each

job and to compare it with budgeted profit margins. It is defined as the process of gathering

information about production and service activities and the costs connected with each activity. It

helps the organisation to know the reliability of the estimate made by it. The prices quoted

should be bale to acquire a reasonable profit for the company. It mainly helps the organisation in

maintaining three types of records such as direct materials to have the records of the

consumption of the materials, direct labour for getting the exact labour costings to the company

and the other overhead costs applied in manufacturing process(Schaltegger and Burritt, 2017).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Maas, Schaltegger and Crutzen, 2016)Price-optimising System

Price optimisation helps the organisation to analyse the variation in demands with the

change in prices of the products of the company. Then on the basis of the costs information

gathered and the available inventory level organisations make decisions on the prices that can

prevail in the market. It helps the company to determine its initial, promotional and the

discounted pricing policies. Price optimisation helps the company to know its standing in the

markets as well as the prices with which it can survive in the market. It tells the company about

the cost reduction or to improve the production process to match the pricing levels without

sacrificing profits of the company.

P2 Different methods for management accounting reporting.

Management accounting helps the Oshodi PLC in trimming its costs whit the help of

information provided by the managerial reports. Accounting reports also enable the organisation

to shred down its non rewarding product lines and to focus more on the goods which will offer

high financial returns to the Oshodi. Company may also generate reports considering its timely

requirements such as on quarterly, half yearly or on the annual basis(Maas, Schaltegger and

Crutzen, 2016).

Budget Reports

Budget reports helps the organisation to assess its efficiency and the performance of its

operations whether they are able to meet its set standards or the production is not declining.

Budgetary standards are set on the basis of the actual expenses occurred by the department and

the production level they were achieving at that costs levels in the prior years. It will also help

the company to change its budget reports if the expenses are going beyond the budgeted levels

even after making all the possible changes in the same budget. Budget reports also help the

organisation to trim its costs if the expenses are going beyond the attainable standards. Budgeted

reports help the managerial officials to analyse the performance of the workforce and to reward

them with incentives for meeting the targeted standards(Boučková, 2015).

Job Cost Reports

Job cost report helps the organisation to display its costs records over a specific process.

Reports are generally compared with the estimated revenue levels for evaluating the profitability

of the specific jobs. Job cost reports help the PLC to find out areas that give high returns and to

put extra efforts in enhancing those areas and ensure that the company does not waste its time on

3

Price optimisation helps the organisation to analyse the variation in demands with the

change in prices of the products of the company. Then on the basis of the costs information

gathered and the available inventory level organisations make decisions on the prices that can

prevail in the market. It helps the company to determine its initial, promotional and the

discounted pricing policies. Price optimisation helps the company to know its standing in the

markets as well as the prices with which it can survive in the market. It tells the company about

the cost reduction or to improve the production process to match the pricing levels without

sacrificing profits of the company.

P2 Different methods for management accounting reporting.

Management accounting helps the Oshodi PLC in trimming its costs whit the help of

information provided by the managerial reports. Accounting reports also enable the organisation

to shred down its non rewarding product lines and to focus more on the goods which will offer

high financial returns to the Oshodi. Company may also generate reports considering its timely

requirements such as on quarterly, half yearly or on the annual basis(Maas, Schaltegger and

Crutzen, 2016).

Budget Reports

Budget reports helps the organisation to assess its efficiency and the performance of its

operations whether they are able to meet its set standards or the production is not declining.

Budgetary standards are set on the basis of the actual expenses occurred by the department and

the production level they were achieving at that costs levels in the prior years. It will also help

the company to change its budget reports if the expenses are going beyond the budgeted levels

even after making all the possible changes in the same budget. Budget reports also help the

organisation to trim its costs if the expenses are going beyond the attainable standards. Budgeted

reports help the managerial officials to analyse the performance of the workforce and to reward

them with incentives for meeting the targeted standards(Boučková, 2015).

Job Cost Reports

Job cost report helps the organisation to display its costs records over a specific process.

Reports are generally compared with the estimated revenue levels for evaluating the profitability

of the specific jobs. Job cost reports help the PLC to find out areas that give high returns and to

put extra efforts in enhancing those areas and ensure that the company does not waste its time on

3

low returning jobs. It helps the organisation to control the costs of the ongoing project and to

make necessary changes by applying other cost-efficient methods to enable the organisation save

itself from the losses that could offer.

Performance Report

Oshodi generates its performance reports for reviewing the overall performance of the

PLC and the each employee working in the organisation. Performance reports enable the

managers to take decisions and to frame strategies to improve the future performance of the

company. Efficient employees are rewarded to perform even better and the inefficient employees

are trained and motivated to improve the performance. Performance report also helps the

organisation to know its efficiency in meeting the production levels to achieve its targets so that

the company can make necessary changes to improve the performance of the company as a

whole. Performance reports plays a vital role to detect the flaws and to implement new strategies

to achieve the target level(Chenhall and Moers, 2015).

Other Managerial Accounting Reports

There are other reports also that can be generated by the company as per requirement of

its business activities have a better monitoring and controlling the business operation. The

reports which also helps the PLC in analysing the existing business and its operational activities.

These reports can be prepared by the company itself or by the professionals working outside the

company and preparing reports as per the specific business requirement. Professionals possess

the knowledge and expertise to make reports and also also help the company to analyse its

impact. It also provides the company with the suggestive measures that can be used by the

company to improve its cost control measures along with the operations.

LO2

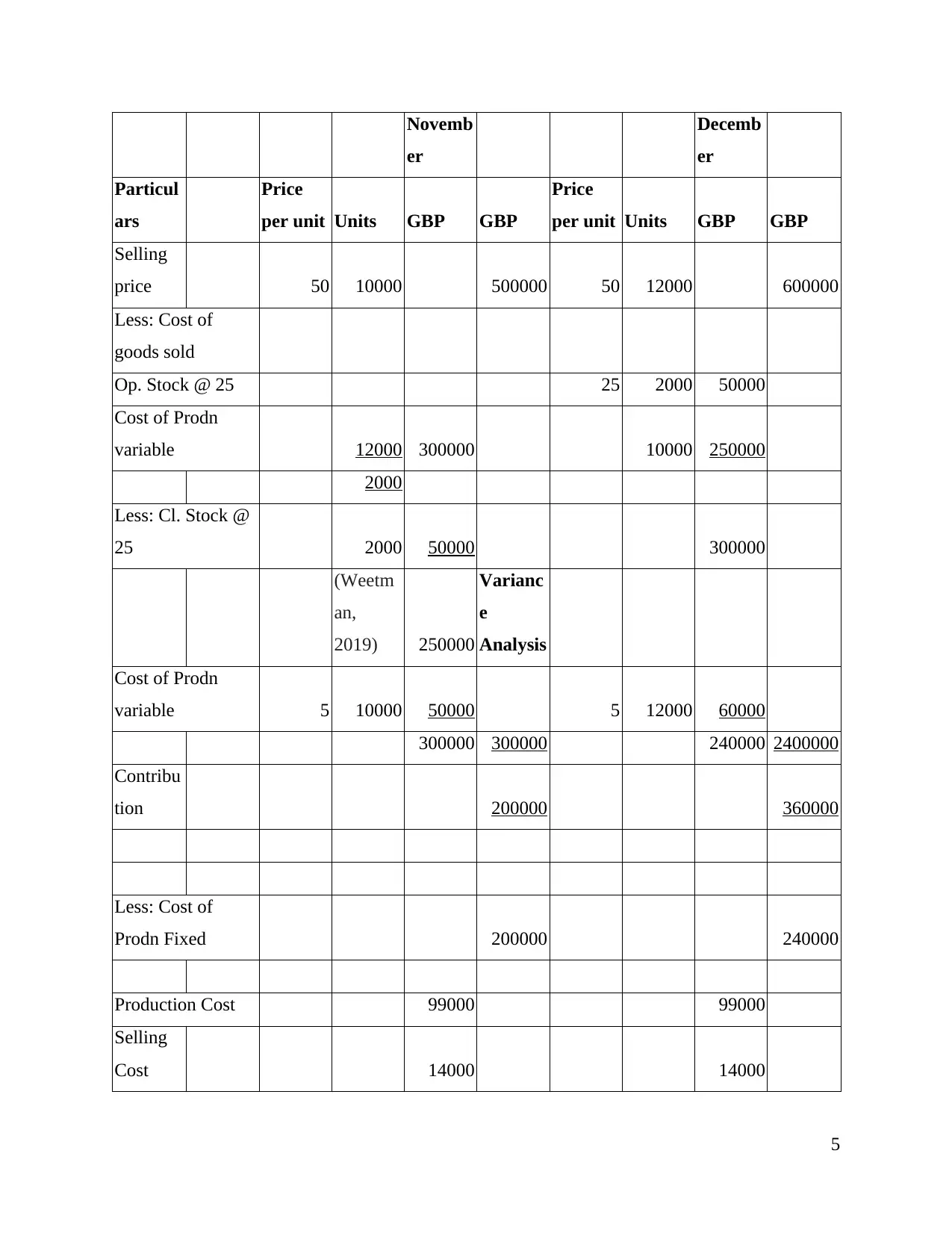

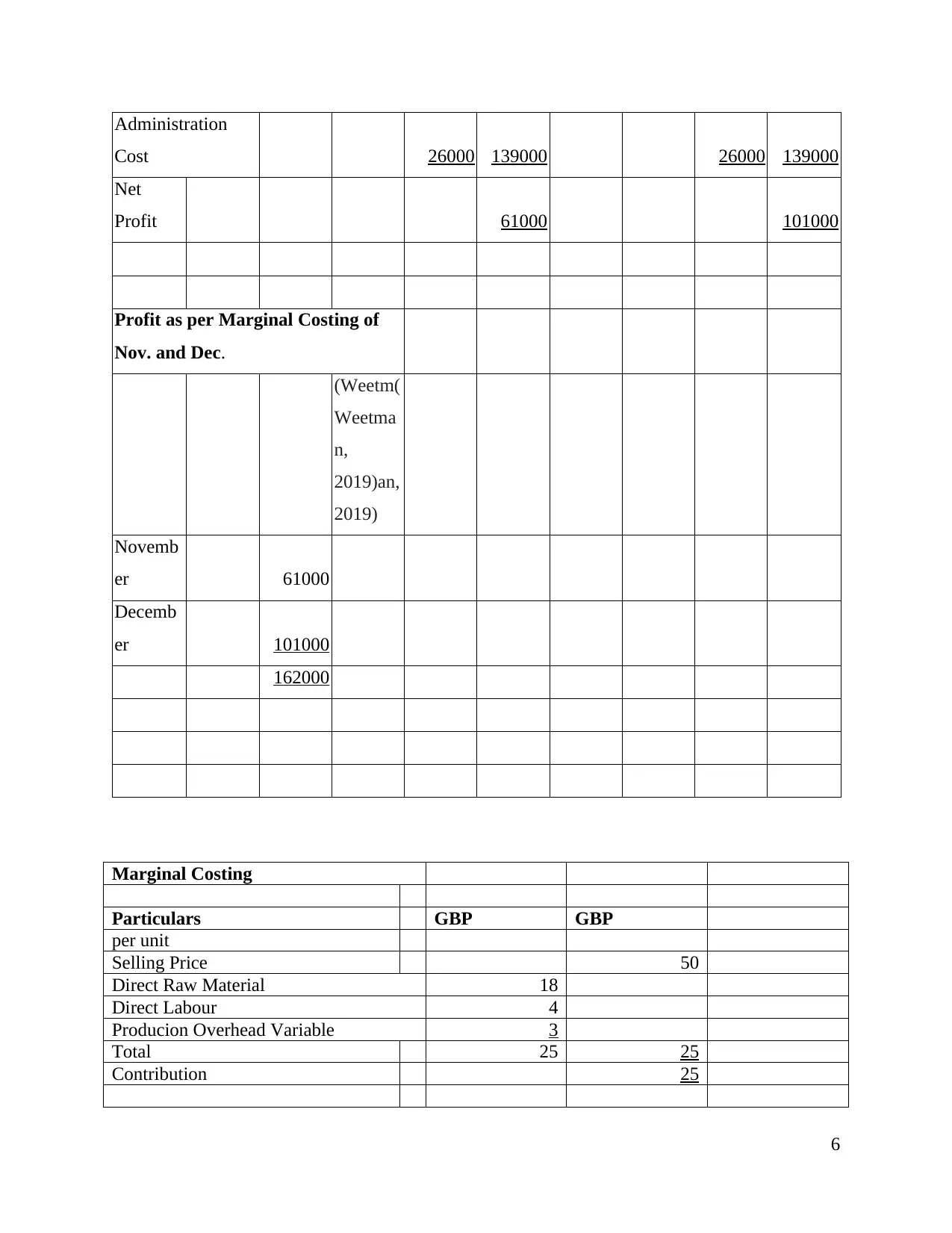

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

INCOME STATEMENTS USING MARGINAL COSTING

Marginal Costing

Profit or Loss statement of Oshodi PLC for November

and December

4

make necessary changes by applying other cost-efficient methods to enable the organisation save

itself from the losses that could offer.

Performance Report

Oshodi generates its performance reports for reviewing the overall performance of the

PLC and the each employee working in the organisation. Performance reports enable the

managers to take decisions and to frame strategies to improve the future performance of the

company. Efficient employees are rewarded to perform even better and the inefficient employees

are trained and motivated to improve the performance. Performance report also helps the

organisation to know its efficiency in meeting the production levels to achieve its targets so that

the company can make necessary changes to improve the performance of the company as a

whole. Performance reports plays a vital role to detect the flaws and to implement new strategies

to achieve the target level(Chenhall and Moers, 2015).

Other Managerial Accounting Reports

There are other reports also that can be generated by the company as per requirement of

its business activities have a better monitoring and controlling the business operation. The

reports which also helps the PLC in analysing the existing business and its operational activities.

These reports can be prepared by the company itself or by the professionals working outside the

company and preparing reports as per the specific business requirement. Professionals possess

the knowledge and expertise to make reports and also also help the company to analyse its

impact. It also provides the company with the suggestive measures that can be used by the

company to improve its cost control measures along with the operations.

LO2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

INCOME STATEMENTS USING MARGINAL COSTING

Marginal Costing

Profit or Loss statement of Oshodi PLC for November

and December

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Novemb

er

Decemb

er

Particul

ars

Price

per unit Units GBP GBP

Price

per unit Units GBP GBP

Selling

price 50 10000 500000 50 12000 600000

Less: Cost of

goods sold

Op. Stock @ 25 25 2000 50000

Cost of Prodn

variable 12000 300000 10000 250000

2000

Less: Cl. Stock @

25 2000 50000 300000

(Weetm

an,

2019) 250000

Varianc

e

Analysis

Cost of Prodn

variable 5 10000 50000 5 12000 60000

300000 300000 240000 2400000

Contribu

tion 200000 360000

Less: Cost of

Prodn Fixed 200000 240000

Production Cost 99000 99000

Selling

Cost 14000 14000

5

er

Decemb

er

Particul

ars

Price

per unit Units GBP GBP

Price

per unit Units GBP GBP

Selling

price 50 10000 500000 50 12000 600000

Less: Cost of

goods sold

Op. Stock @ 25 25 2000 50000

Cost of Prodn

variable 12000 300000 10000 250000

2000

Less: Cl. Stock @

25 2000 50000 300000

(Weetm

an,

2019) 250000

Varianc

e

Analysis

Cost of Prodn

variable 5 10000 50000 5 12000 60000

300000 300000 240000 2400000

Contribu

tion 200000 360000

Less: Cost of

Prodn Fixed 200000 240000

Production Cost 99000 99000

Selling

Cost 14000 14000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Administration

Cost 26000 139000 26000 139000

Net

Profit 61000 101000

Profit as per Marginal Costing of

Nov. and Dec.

(Weetm(

Weetma

n,

2019)an,

2019)

Novemb

er 61000

Decemb

er 101000

162000

Marginal Costing

Particulars GBP GBP

per unit

Selling Price 50

Direct Raw Material 18

Direct Labour 4

Producion Overhead Variable 3

Total 25 25

Contribution 25

6

Cost 26000 139000 26000 139000

Net

Profit 61000 101000

Profit as per Marginal Costing of

Nov. and Dec.

(Weetm(

Weetma

n,

2019)an,

2019)

Novemb

er 61000

Decemb

er 101000

162000

Marginal Costing

Particulars GBP GBP

per unit

Selling Price 50

Direct Raw Material 18

Direct Labour 4

Producion Overhead Variable 3

Total 25 25

Contribution 25

6

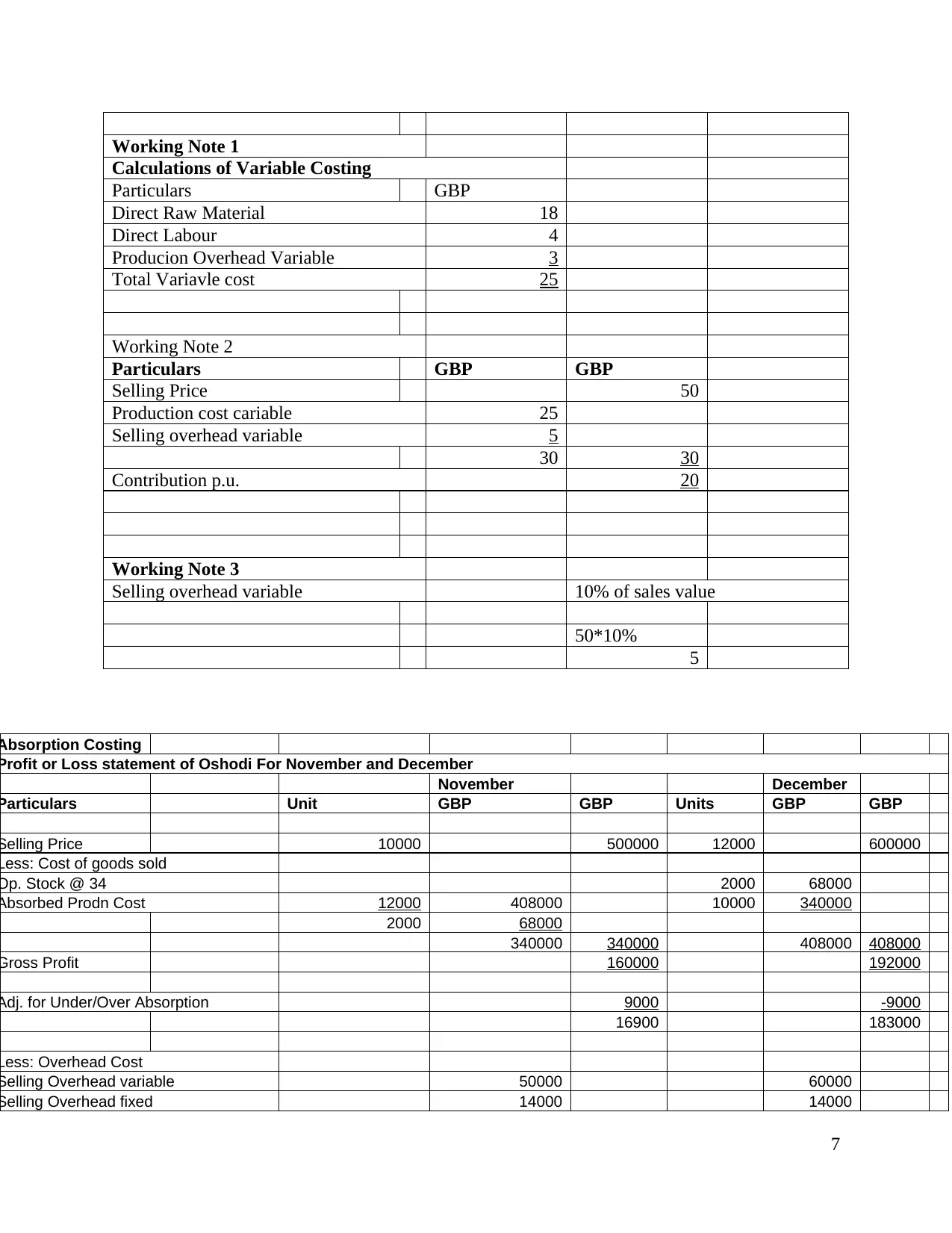

Working Note 1

Calculations of Variable Costing

Particulars GBP

Direct Raw Material 18

Direct Labour 4

Producion Overhead Variable 3

Total Variavle cost 25

Working Note 2

Particulars GBP GBP

Selling Price 50

Production cost cariable 25

Selling overhead variable 5

30 30

Contribution p.u. 20

Working Note 3

Selling overhead variable 10% of sales value

50*10%

5

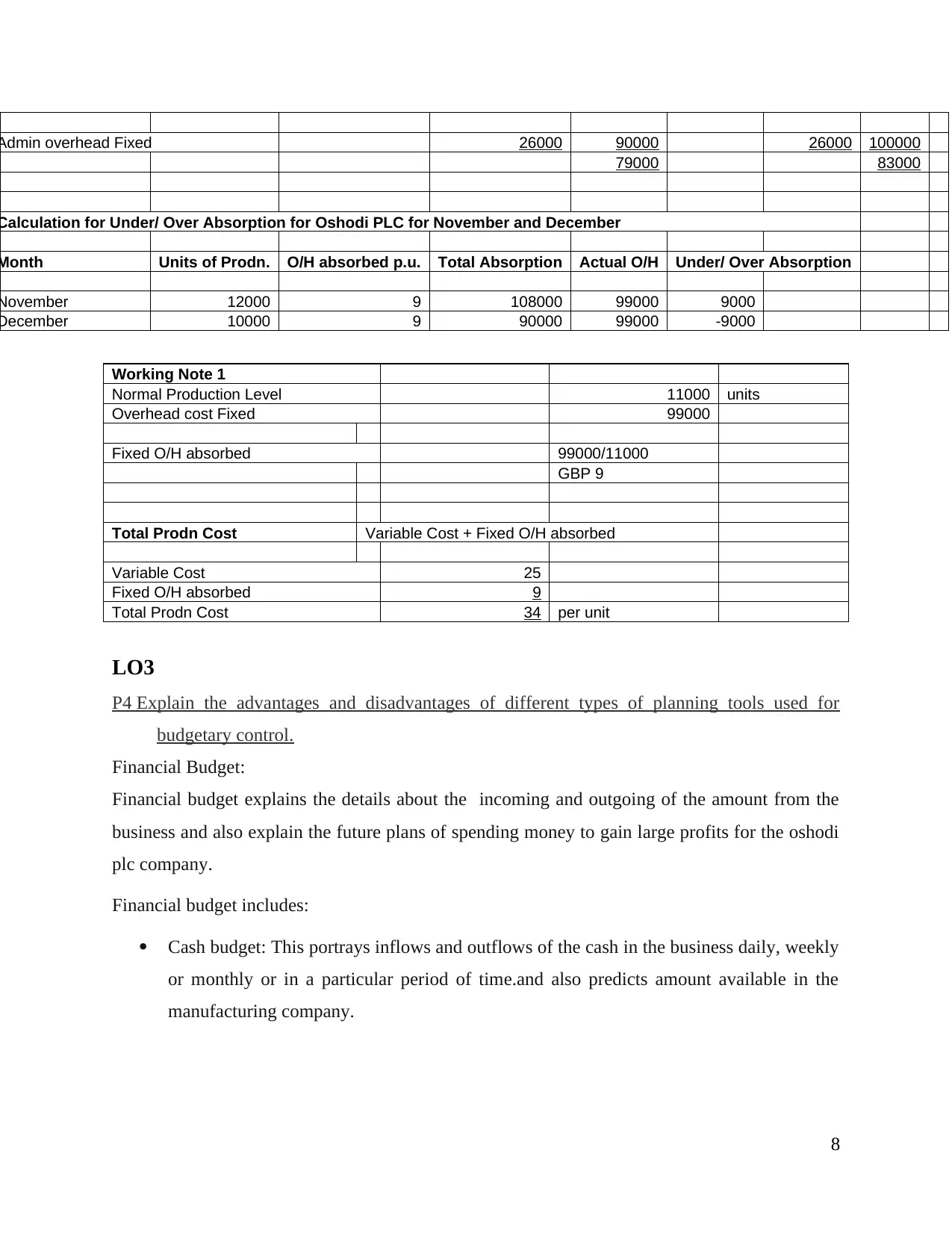

Absorption Costing

Profit or Loss statement of Oshodi For November and December

November December

Particulars Unit GBP GBP Units GBP GBP

Selling Price 10000 500000 12000 600000

Less: Cost of goods sold

Op. Stock @ 34 2000 68000

Absorbed Prodn Cost 12000 408000 10000 340000

2000 68000

340000 340000 408000 408000

Gross Profit 160000 192000

Adj. for Under/Over Absorption 9000 -9000

16900 183000

Less: Overhead Cost

Selling Overhead variable 50000 60000

Selling Overhead fixed 14000 14000

7

Calculations of Variable Costing

Particulars GBP

Direct Raw Material 18

Direct Labour 4

Producion Overhead Variable 3

Total Variavle cost 25

Working Note 2

Particulars GBP GBP

Selling Price 50

Production cost cariable 25

Selling overhead variable 5

30 30

Contribution p.u. 20

Working Note 3

Selling overhead variable 10% of sales value

50*10%

5

Absorption Costing

Profit or Loss statement of Oshodi For November and December

November December

Particulars Unit GBP GBP Units GBP GBP

Selling Price 10000 500000 12000 600000

Less: Cost of goods sold

Op. Stock @ 34 2000 68000

Absorbed Prodn Cost 12000 408000 10000 340000

2000 68000

340000 340000 408000 408000

Gross Profit 160000 192000

Adj. for Under/Over Absorption 9000 -9000

16900 183000

Less: Overhead Cost

Selling Overhead variable 50000 60000

Selling Overhead fixed 14000 14000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Admin overhead Fixed 26000 90000 26000 100000

79000 83000

Calculation for Under/ Over Absorption for Oshodi PLC for November and December

Month Units of Prodn. O/H absorbed p.u. Total Absorption Actual O/H Under/ Over Absorption

November 12000 9 108000 99000 9000

December 10000 9 90000 99000 -9000

Working Note 1

Normal Production Level 11000 units

Overhead cost Fixed 99000

Fixed O/H absorbed 99000/11000

GBP 9

Total Prodn Cost Variable Cost + Fixed O/H absorbed

Variable Cost 25

Fixed O/H absorbed 9

Total Prodn Cost 34 per unit

LO3

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.

Financial Budget:

Financial budget explains the details about the incoming and outgoing of the amount from the

business and also explain the future plans of spending money to gain large profits for the oshodi

plc company.

Financial budget includes:

Cash budget: This portrays inflows and outflows of the cash in the business daily, weekly

or monthly or in a particular period of time.and also predicts amount available in the

manufacturing company.

8

79000 83000

Calculation for Under/ Over Absorption for Oshodi PLC for November and December

Month Units of Prodn. O/H absorbed p.u. Total Absorption Actual O/H Under/ Over Absorption

November 12000 9 108000 99000 9000

December 10000 9 90000 99000 -9000

Working Note 1

Normal Production Level 11000 units

Overhead cost Fixed 99000

Fixed O/H absorbed 99000/11000

GBP 9

Total Prodn Cost Variable Cost + Fixed O/H absorbed

Variable Cost 25

Fixed O/H absorbed 9

Total Prodn Cost 34 per unit

LO3

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.

Financial Budget:

Financial budget explains the details about the incoming and outgoing of the amount from the

business and also explain the future plans of spending money to gain large profits for the oshodi

plc company.

Financial budget includes:

Cash budget: This portrays inflows and outflows of the cash in the business daily, weekly

or monthly or in a particular period of time.and also predicts amount available in the

manufacturing company.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Capital expenditure budget: This concentrates on the large investment on the fixed assets

of Such as, land buildings, vehicles or the new setups of the oshodi manufacturing

company of the jojo fruit juice.

The balance sheet budget: This includes liabilities, shares and the assets available in the

firm during the present period of accounting.

Advantages:

Financial budget carries all the details about incoming and outgoing money and the profit

margins of the company.

Financial budget provides ideas about further investment of the money and about

increasing the earnings from the jojo fruit juice.

Financial budget allows inflow and outflow of the cash that means it carries all the details

about available cash amount in the company which makes higher possibility to plan for

more profits and easy to recognise financial position of the company.

Disadvantages :

Business with Cash is quiet risky as it can be loose somewhere or there is a probability of

its stealing.

Financial capital expenses is the permanent investment and is an irreversible process, so

after investing money in permanent assets it cannot be used for further profits or sales.

Financial budget plan is time consuming process, as it needs an upgrade every now and

then as it is very short term process used on the regular days(Weetman, 2019).

Operating Budget:

Operation budget describes planning over a particular period of time such as annual or quarterly

etc. to portray sales and income of the business, actual and expected profit of the business.

Operating budget includes:

9

of Such as, land buildings, vehicles or the new setups of the oshodi manufacturing

company of the jojo fruit juice.

The balance sheet budget: This includes liabilities, shares and the assets available in the

firm during the present period of accounting.

Advantages:

Financial budget carries all the details about incoming and outgoing money and the profit

margins of the company.

Financial budget provides ideas about further investment of the money and about

increasing the earnings from the jojo fruit juice.

Financial budget allows inflow and outflow of the cash that means it carries all the details

about available cash amount in the company which makes higher possibility to plan for

more profits and easy to recognise financial position of the company.

Disadvantages :

Business with Cash is quiet risky as it can be loose somewhere or there is a probability of

its stealing.

Financial capital expenses is the permanent investment and is an irreversible process, so

after investing money in permanent assets it cannot be used for further profits or sales.

Financial budget plan is time consuming process, as it needs an upgrade every now and

then as it is very short term process used on the regular days(Weetman, 2019).

Operating Budget:

Operation budget describes planning over a particular period of time such as annual or quarterly

etc. to portray sales and income of the business, actual and expected profit of the business.

Operating budget includes:

9

The sales and revenue budget: This allocates the amount of money received by the normal

running of the business and determines the future economic positions of the oshodi PLC

manufacturing company.

The expense budget: This traces the expected expenses of the firm in a specific period of time

and also relates to approaching expenses of the business.

The project budget : This includes estimation of the amount authorised in a projects handled by

the oshodi plc company of jojo fruit juice.

Advantages:

Operating budget shape all the budget required for operating entire business which helps

in prediction of financial position of the company in the future.

It calculates the amount used for the production of jojo fruit juice and also calculate the

amount of the goods and services used for the production.

It also analyse profit margins of the business by calculating profit per each packet of juice

and also calculate no. of packets sold which helps in examining its demand and trends.

Disadvantages:

It is time consuming process, creating budget and detailing money inflows and outflows

of the company.

Operating budget varies directly with change in the sale volumes , income and even with

the change of goods and services.

It is short term process, needs updation after every short period of time(Suomala, Lyly-

Yrjänäinen, J., Laine and Mitchell, 2017).

static Budgets:

Static budget describes inflexible constant non changing budget with increase or decrease in

sales, income or other activities of the sale in the business.

Advantages:

10

running of the business and determines the future economic positions of the oshodi PLC

manufacturing company.

The expense budget: This traces the expected expenses of the firm in a specific period of time

and also relates to approaching expenses of the business.

The project budget : This includes estimation of the amount authorised in a projects handled by

the oshodi plc company of jojo fruit juice.

Advantages:

Operating budget shape all the budget required for operating entire business which helps

in prediction of financial position of the company in the future.

It calculates the amount used for the production of jojo fruit juice and also calculate the

amount of the goods and services used for the production.

It also analyse profit margins of the business by calculating profit per each packet of juice

and also calculate no. of packets sold which helps in examining its demand and trends.

Disadvantages:

It is time consuming process, creating budget and detailing money inflows and outflows

of the company.

Operating budget varies directly with change in the sale volumes , income and even with

the change of goods and services.

It is short term process, needs updation after every short period of time(Suomala, Lyly-

Yrjänäinen, J., Laine and Mitchell, 2017).

static Budgets:

Static budget describes inflexible constant non changing budget with increase or decrease in

sales, income or other activities of the sale in the business.

Advantages:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.