Application of Accounting Techniques: Marginal & Absorption Costing

VerifiedAdded on 2024/05/14

|11

|380

|394

Presentation

AI Summary

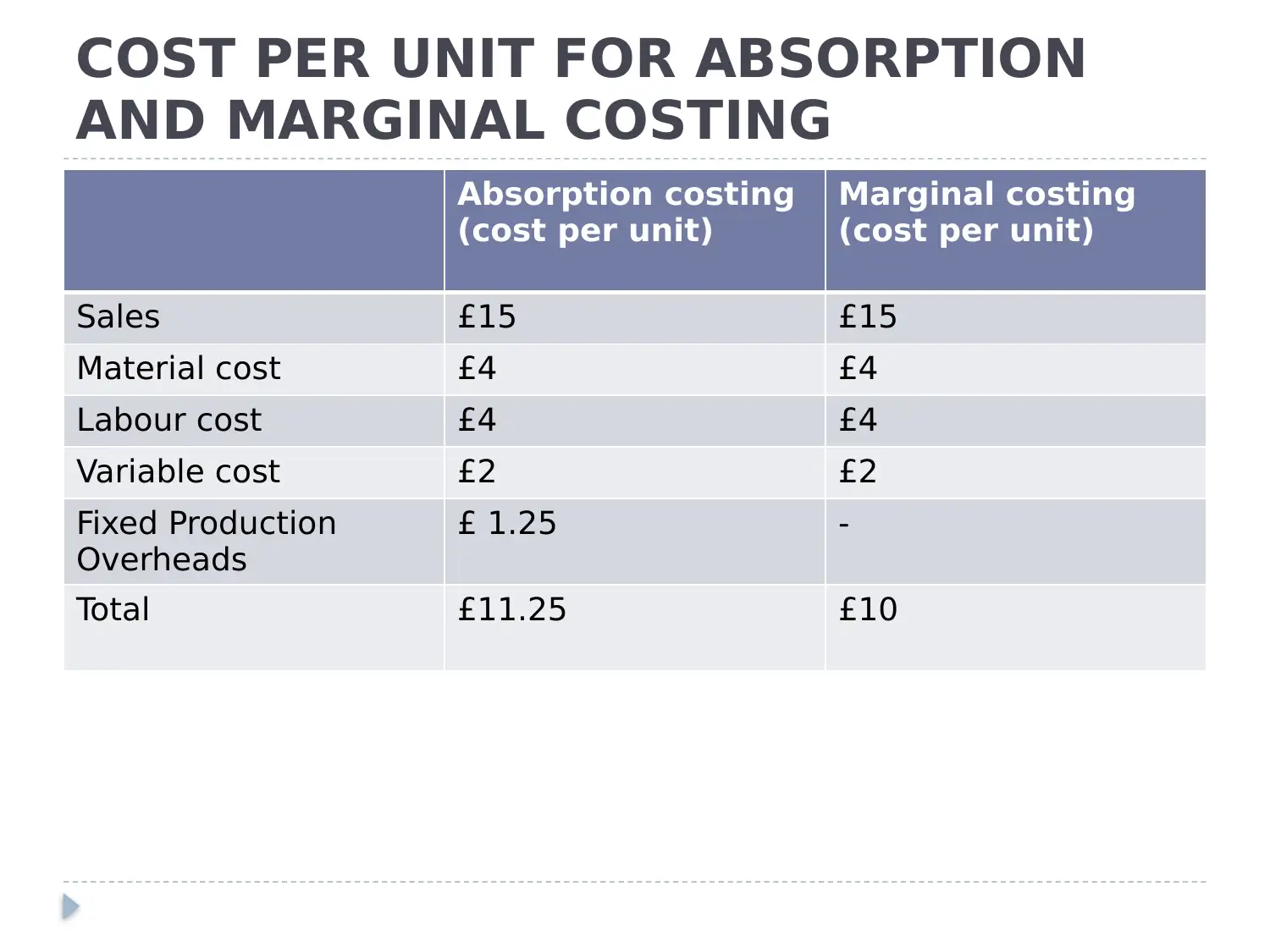

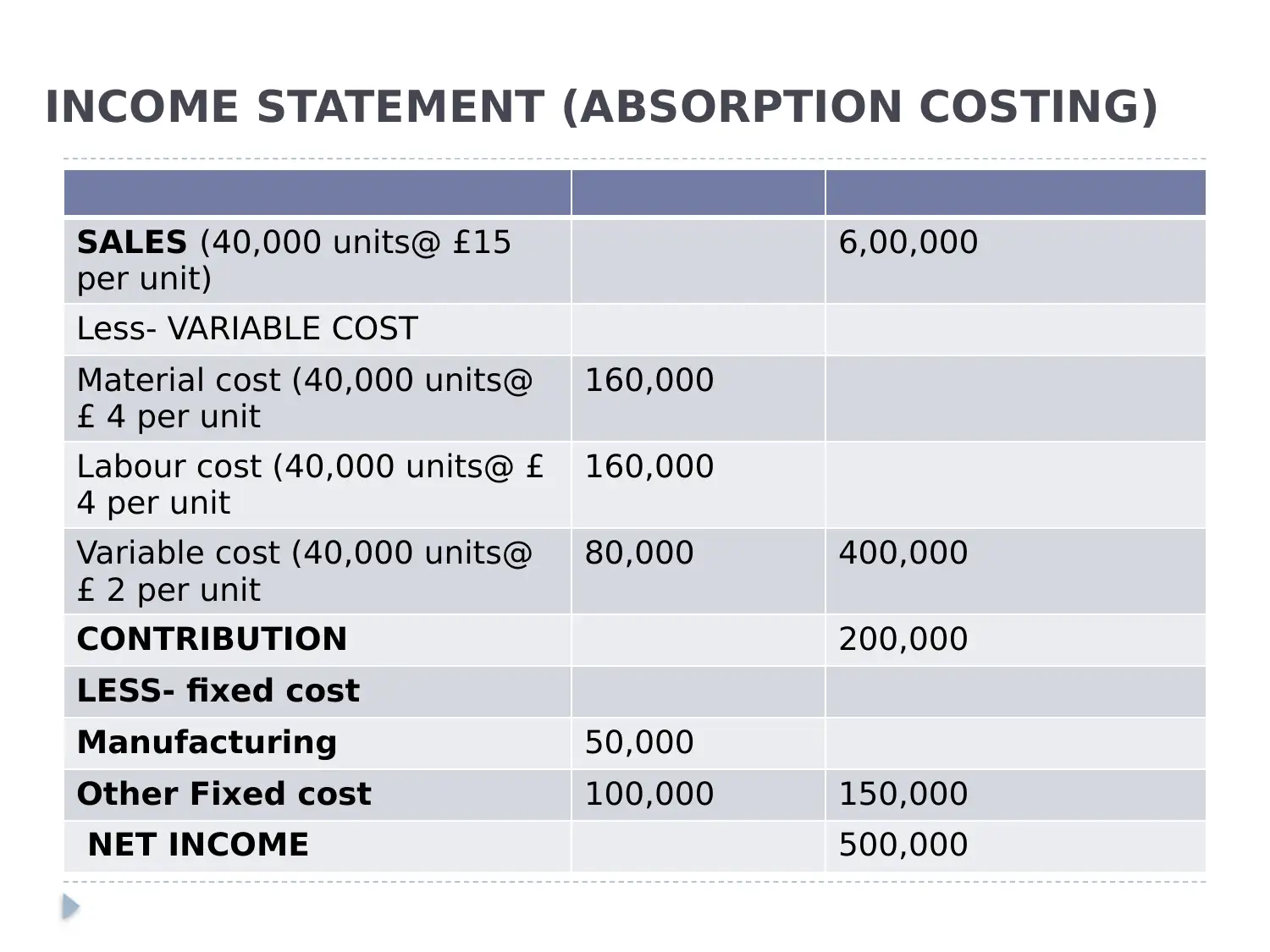

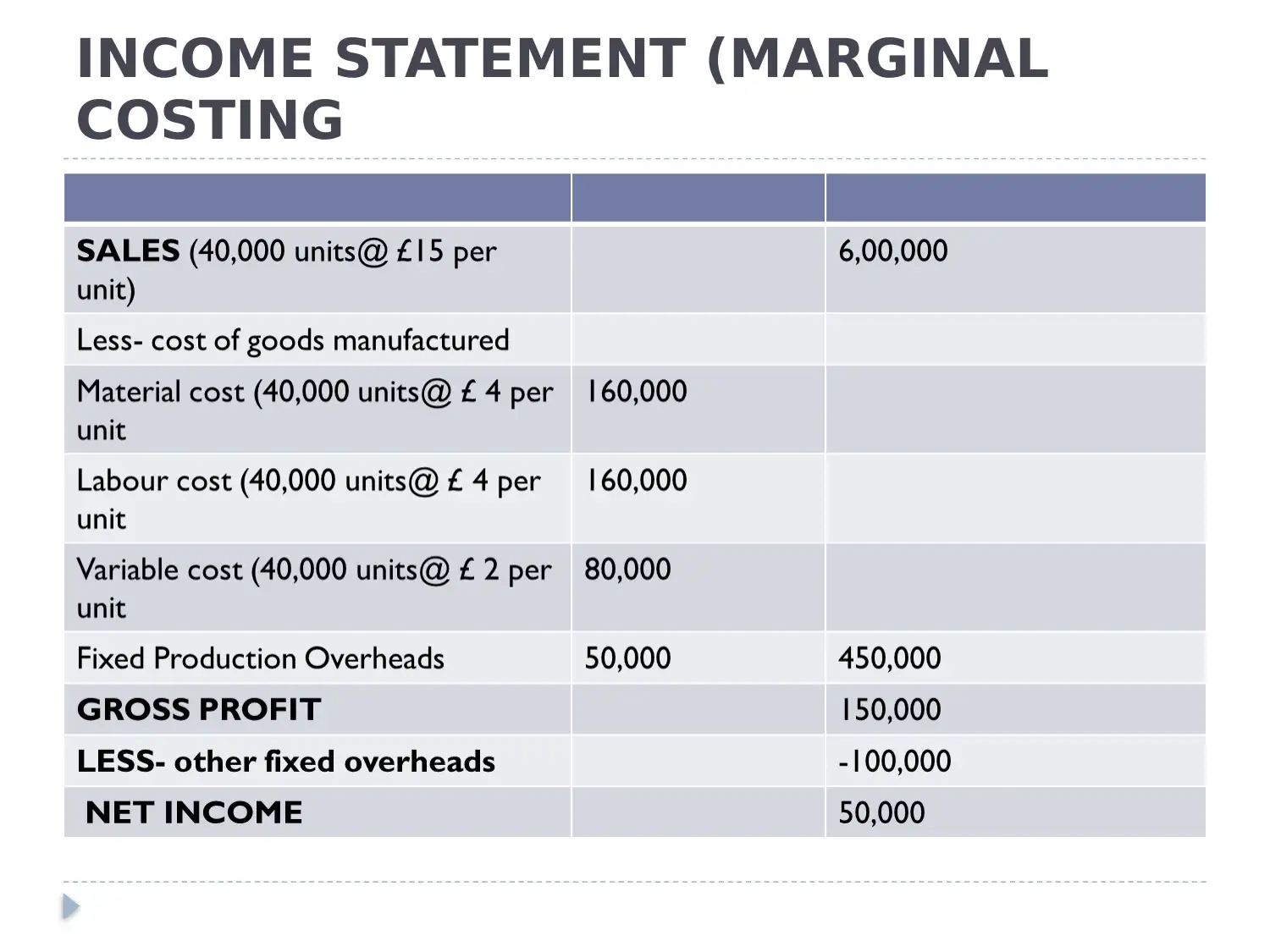

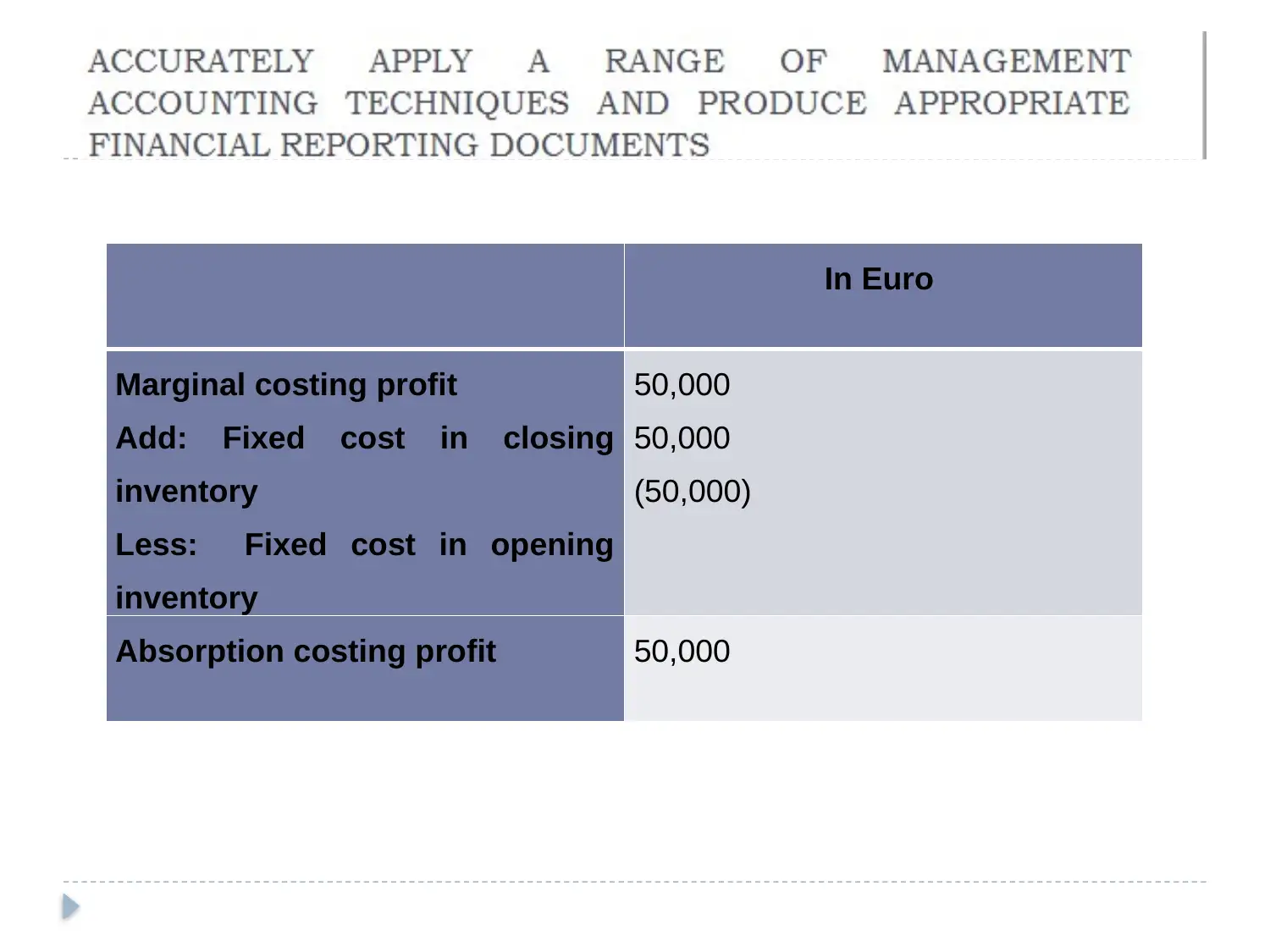

This presentation provides an understanding of the application of marginal and absorption costing methods for Conway Ltd. It differentiates between the two methods, highlighting that absorption costing doesn't distinguish between fixed and variable costs, while marginal costing treats them separately. The presentation includes calculations for cost per unit under both methods, followed by income statements prepared using each approach. The analysis demonstrates the calculation of net income using both absorption and marginal costing, ultimately revealing that Conway Ltd realizes the same profit under either method. The presentation concludes by emphasizing the insights gained into the different costing methods and their implications.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.