Management Accounting: Costing, Budgeting, and Inventory Analysis

VerifiedAdded on 2020/06/06

|17

|3923

|62

Report

AI Summary

This report delves into the fundamentals of management accounting, crucial for organizational growth and decision-making. It explores cost classification, differentiating between fixed, variable, and semi-variable costs, along with other classification methods. The report includes calculations of costs at various production levels and their graphical analysis. Inventory valuation methods, specifically FIFO, LIFO, and the average inventory method, are examined with detailed calculations. A January month report is prepared using these inventory methods. Furthermore, the report discusses diverse performance indicators, emphasizing cost reduction and value enhancement within an organization. The second part of the report focuses on budgeting, including its objectives and the process of budget preparation, followed by the preparation of different budgets and a cash budget. The final section covers the computation of budgeted statements.

Management Accounting:

Costing and Budgeting

Costing and Budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Q1................................................................................................................................................1

a). Cost classification into Fixed, variable and semi-variable costs:..........................................1

b). Explain other ways of classifying costs:................................................................................2

Q2. ..............................................................................................................................................3

A). Calculation of costs at various level:....................................................................................3

B). Analysis the cost via graphs..................................................................................................4

Q3 Calculation of inventory by using FIFO,LIFO and average inventory method:...................4

Q4 Preparation of January month report through using inventory methods:..............................6

Q5. ..............................................................................................................................................6

a). Diverse performance indicators:............................................................................................6

b).................................................................................................................................................7

1. To reduce costs:.......................................................................................................................7

2. To enhance value:...................................................................................................................7

TASK 2............................................................................................................................................8

Q6................................................................................................................................................8

a). Budget:...................................................................................................................................8

B). Objectives of budget formulation:........................................................................................8

c). Process of budget preparation:...............................................................................................8

Q7: Preparation of different budgets...........................................................................................9

Q8.Cash Budget .......................................................................................................................10

TASK 3..........................................................................................................................................10

Q9. Computation of budgeted statements.................................................................................10

Q10............................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Q1................................................................................................................................................1

a). Cost classification into Fixed, variable and semi-variable costs:..........................................1

b). Explain other ways of classifying costs:................................................................................2

Q2. ..............................................................................................................................................3

A). Calculation of costs at various level:....................................................................................3

B). Analysis the cost via graphs..................................................................................................4

Q3 Calculation of inventory by using FIFO,LIFO and average inventory method:...................4

Q4 Preparation of January month report through using inventory methods:..............................6

Q5. ..............................................................................................................................................6

a). Diverse performance indicators:............................................................................................6

b).................................................................................................................................................7

1. To reduce costs:.......................................................................................................................7

2. To enhance value:...................................................................................................................7

TASK 2............................................................................................................................................8

Q6................................................................................................................................................8

a). Budget:...................................................................................................................................8

B). Objectives of budget formulation:........................................................................................8

c). Process of budget preparation:...............................................................................................8

Q7: Preparation of different budgets...........................................................................................9

Q8.Cash Budget .......................................................................................................................10

TASK 3..........................................................................................................................................10

Q9. Computation of budgeted statements.................................................................................10

Q10............................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting tools are an essential aspect for growing the firm's development

and likewise support firm's management. In order to make decision for short term as well as long

term, managers should need to prepare management reports and accounts to get accurate result

and provide financial and statistical information (Renz, 2016). The main aim of this report is to

know that how management accounting uses financial data in order to making planning,

monitoring and control of the finance within organisation. Therefore it is necessary to introduce

the fundamentals of management accounting which applies within the organisation in order to

operate business environment. Therefore the methods and techniques and tools should need to be

implemented in order to control the usage of finance which help an organisation to face the

financial problems (Suomala, Lyly-Yrjänäinen and Lukka, 2014).

TASK 1

Q1

a). Cost classification into Fixed, variable and semi-variable costs:

Cost: This is the main aspect for producing a good. If the management of the smart look

Ltd effectively implement management accounting tools in a firm the company could get the

sustainable development in the firm. Cost is divided into three parts which are namely: fixed,

variable and semi-variable costs.

Costs are divided into two parts; direct and indirect costs. Direct costs are those which are

directly connected to producing of units. While indirect costs are those which are ultimately not

related to the cost of production but indirectly contribute to the costs of production (Ward,

2012).

Cost are namely divided as follows:

Fixed costs Variable costs Semi-variable costs

This is the cost that constantly

fixed irrespective of change in

the output or sales revenue.

These are optimum used if

production is highly produced.

This is the cost which vary as

per the change in the cost of

production. This makes does

not effect on the cost of

production as this change with

A semi- variable costs are

those which are half variable

and half fixed. However, there

is a need to apportioned these

costs that are totally used by

1

Management accounting tools are an essential aspect for growing the firm's development

and likewise support firm's management. In order to make decision for short term as well as long

term, managers should need to prepare management reports and accounts to get accurate result

and provide financial and statistical information (Renz, 2016). The main aim of this report is to

know that how management accounting uses financial data in order to making planning,

monitoring and control of the finance within organisation. Therefore it is necessary to introduce

the fundamentals of management accounting which applies within the organisation in order to

operate business environment. Therefore the methods and techniques and tools should need to be

implemented in order to control the usage of finance which help an organisation to face the

financial problems (Suomala, Lyly-Yrjänäinen and Lukka, 2014).

TASK 1

Q1

a). Cost classification into Fixed, variable and semi-variable costs:

Cost: This is the main aspect for producing a good. If the management of the smart look

Ltd effectively implement management accounting tools in a firm the company could get the

sustainable development in the firm. Cost is divided into three parts which are namely: fixed,

variable and semi-variable costs.

Costs are divided into two parts; direct and indirect costs. Direct costs are those which are

directly connected to producing of units. While indirect costs are those which are ultimately not

related to the cost of production but indirectly contribute to the costs of production (Ward,

2012).

Cost are namely divided as follows:

Fixed costs Variable costs Semi-variable costs

This is the cost that constantly

fixed irrespective of change in

the output or sales revenue.

These are optimum used if

production is highly produced.

This is the cost which vary as

per the change in the cost of

production. This makes does

not effect on the cost of

production as this change with

A semi- variable costs are

those which are half variable

and half fixed. However, there

is a need to apportioned these

costs that are totally used by

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Such activity will make per

unit cost of production lower

that will ultimately helps the

firm to get the competitive

advantage over the firm

(Quagli, 2011). product costs

are used by the firm Under this

case, factory rent, factory

supervisors' wages (considered

only paid at a flat rate),

telephone expenses which are

paid at flat rate, office rates,

delivery drivers' pay which are

paid at flat rate these are

considered as the fixed costs.

the vary in the production units

in the firm. Direct material,

direct labours, and direct

overheads are the main costs

which are considered as the

production costs. These are the

costs which very with the

change in the production.

Under the given case, material

for cloths, power for sewing

machines in the factory,

factory supervisor which are

related to the manufacturing

based bonus (Otley and

Emmanuel, 2013). Packaging

materials, telephone expenses

charged on an amount per call.

Delivery drivers expenses

which are related to the bonus

package delivered.

the company in order to gain

objectives. This costs is

likewise known as

miscellaneous costs and semi

fixed costs. Under this report,

factory heating is the semi

variable costs. Hence, the

company needs to apply

certain management

accounting tools that can be

used by the firm in order to

make certain cost related

strategy.

b). Explain other ways of classifying costs:

Apart from fixed, variable and semi-variable costs, costs can be segregated into various ways.

However, cost classification is a common process under which company group or divides costs

in an effective manner. This is to be noted that many of the time similar cost can not be

segregated. This is to be mentioned that many of the time similar cost could be segregated in

various ways henceforth, costs is categorise in diverse manner. Some of the following ways

which are mentioned hereunder:

Quality of Expense: Cost are divided into raw material, labour and various expenses.

Relation to cost objects: This are related to categorization is assisted in connection with the cost

components with the cost object. The classification is via into direct and indirect costs.

2

unit cost of production lower

that will ultimately helps the

firm to get the competitive

advantage over the firm

(Quagli, 2011). product costs

are used by the firm Under this

case, factory rent, factory

supervisors' wages (considered

only paid at a flat rate),

telephone expenses which are

paid at flat rate, office rates,

delivery drivers' pay which are

paid at flat rate these are

considered as the fixed costs.

the vary in the production units

in the firm. Direct material,

direct labours, and direct

overheads are the main costs

which are considered as the

production costs. These are the

costs which very with the

change in the production.

Under the given case, material

for cloths, power for sewing

machines in the factory,

factory supervisor which are

related to the manufacturing

based bonus (Otley and

Emmanuel, 2013). Packaging

materials, telephone expenses

charged on an amount per call.

Delivery drivers expenses

which are related to the bonus

package delivered.

the company in order to gain

objectives. This costs is

likewise known as

miscellaneous costs and semi

fixed costs. Under this report,

factory heating is the semi

variable costs. Hence, the

company needs to apply

certain management

accounting tools that can be

used by the firm in order to

make certain cost related

strategy.

b). Explain other ways of classifying costs:

Apart from fixed, variable and semi-variable costs, costs can be segregated into various ways.

However, cost classification is a common process under which company group or divides costs

in an effective manner. This is to be noted that many of the time similar cost can not be

segregated. This is to be mentioned that many of the time similar cost could be segregated in

various ways henceforth, costs is categorise in diverse manner. Some of the following ways

which are mentioned hereunder:

Quality of Expense: Cost are divided into raw material, labour and various expenses.

Relation to cost objects: This are related to categorization is assisted in connection with the cost

components with the cost object. The classification is via into direct and indirect costs.

2

Purpose: Cost can be divided into various purposes.

Components of Production costs,

Relation to time,

Avoidable and unavoidable

Manageable and unmanageable

Real and notional costs

Relevant costs

Sunk costs

Q2.

A). Calculation of costs at various level:

Total cost of the product is considered the variable and fixed costs. However ,variable

costs is the cost which changes as per the change in the production. Although, this can go with

zero, if nothing produced. Henceforth, this depends on the production of goods (Macintosh and

Quattrone, 2010). Smart look Ltd needs to manufacture their units and for that, these are required

to know the whole manufacturing costs that are incurred for producing of goods. Smart look Ltd

wants to know the total cost in a diverse units.

Particular 15000 units 20000 units 25000 units

Material cost (P.U @

£5)

75000 100000 125000

Labour cost (P.U @

£6)

90000 120000 150000

Total variable cost £11 165000 220000 275000

Total fixed cost 50000 50000 50000

Total cost 215000 270000 325000

Per Unit cost £ 14.33 £13.5 £13

From this table, it has been shown that smart look Ltd cost of production is diverse at

diverse manufacturing level. In the initial stage, firm manufacture 15000 units and for producing

such units, company total cost is computed £215000 which changed with the change in the units

3

Components of Production costs,

Relation to time,

Avoidable and unavoidable

Manageable and unmanageable

Real and notional costs

Relevant costs

Sunk costs

Q2.

A). Calculation of costs at various level:

Total cost of the product is considered the variable and fixed costs. However ,variable

costs is the cost which changes as per the change in the production. Although, this can go with

zero, if nothing produced. Henceforth, this depends on the production of goods (Macintosh and

Quattrone, 2010). Smart look Ltd needs to manufacture their units and for that, these are required

to know the whole manufacturing costs that are incurred for producing of goods. Smart look Ltd

wants to know the total cost in a diverse units.

Particular 15000 units 20000 units 25000 units

Material cost (P.U @

£5)

75000 100000 125000

Labour cost (P.U @

£6)

90000 120000 150000

Total variable cost £11 165000 220000 275000

Total fixed cost 50000 50000 50000

Total cost 215000 270000 325000

Per Unit cost £ 14.33 £13.5 £13

From this table, it has been shown that smart look Ltd cost of production is diverse at

diverse manufacturing level. In the initial stage, firm manufacture 15000 units and for producing

such units, company total cost is computed £215000 which changed with the change in the units

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of production, for producing 20000 units, the total cost is calculated as £270000. while

producing 250000 units, the total cost is reached to £325000.

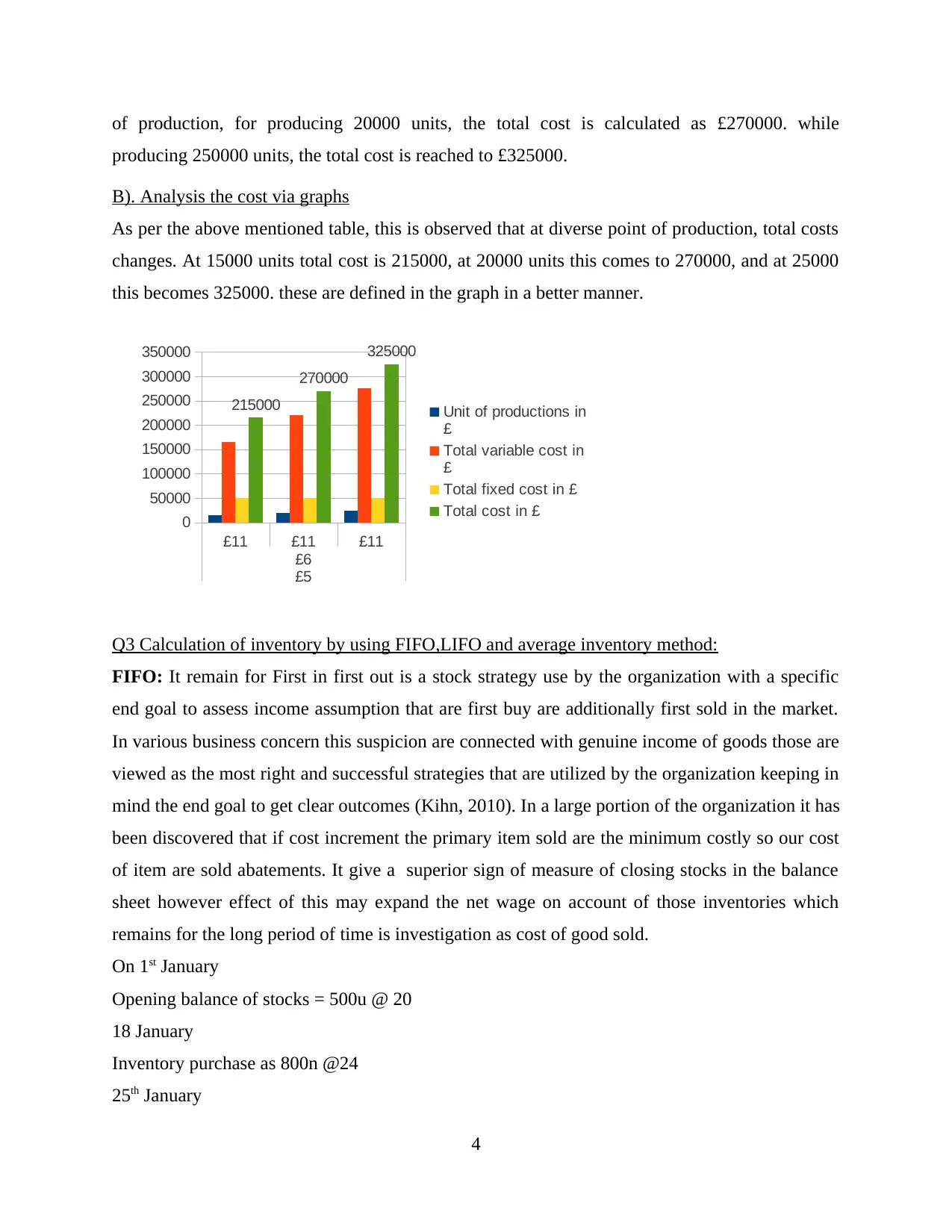

B). Analysis the cost via graphs

As per the above mentioned table, this is observed that at diverse point of production, total costs

changes. At 15000 units total cost is 215000, at 20000 units this comes to 270000, and at 25000

this becomes 325000. these are defined in the graph in a better manner.

£11 £11 £11

£6

£5

0

50000

100000

150000

200000

250000

300000

350000

215000

270000

325000

Unit of productions in

£

Total variable cost in

£

Total fixed cost in £

Total cost in £

Q3 Calculation of inventory by using FIFO,LIFO and average inventory method:

FIFO: It remain for First in first out is a stock strategy use by the organization with a specific

end goal to assess income assumption that are first buy are additionally first sold in the market.

In various business concern this suspicion are connected with genuine income of goods those are

viewed as the most right and successful strategies that are utilized by the organization keeping in

mind the end goal to get clear outcomes (Kihn, 2010). In a large portion of the organization it has

been discovered that if cost increment the primary item sold are the minimum costly so our cost

of item are sold abatements. It give a superior sign of measure of closing stocks in the balance

sheet however effect of this may expand the net wage on account of those inventories which

remains for the long period of time is investigation as cost of good sold.

On 1st January

Opening balance of stocks = 500u @ 20

18 January

Inventory purchase as 800n @24

25th January

4

producing 250000 units, the total cost is reached to £325000.

B). Analysis the cost via graphs

As per the above mentioned table, this is observed that at diverse point of production, total costs

changes. At 15000 units total cost is 215000, at 20000 units this comes to 270000, and at 25000

this becomes 325000. these are defined in the graph in a better manner.

£11 £11 £11

£6

£5

0

50000

100000

150000

200000

250000

300000

350000

215000

270000

325000

Unit of productions in

£

Total variable cost in

£

Total fixed cost in £

Total cost in £

Q3 Calculation of inventory by using FIFO,LIFO and average inventory method:

FIFO: It remain for First in first out is a stock strategy use by the organization with a specific

end goal to assess income assumption that are first buy are additionally first sold in the market.

In various business concern this suspicion are connected with genuine income of goods those are

viewed as the most right and successful strategies that are utilized by the organization keeping in

mind the end goal to get clear outcomes (Kihn, 2010). In a large portion of the organization it has

been discovered that if cost increment the primary item sold are the minimum costly so our cost

of item are sold abatements. It give a superior sign of measure of closing stocks in the balance

sheet however effect of this may expand the net wage on account of those inventories which

remains for the long period of time is investigation as cost of good sold.

On 1st January

Opening balance of stocks = 500u @ 20

18 January

Inventory purchase as 800n @24

25th January

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

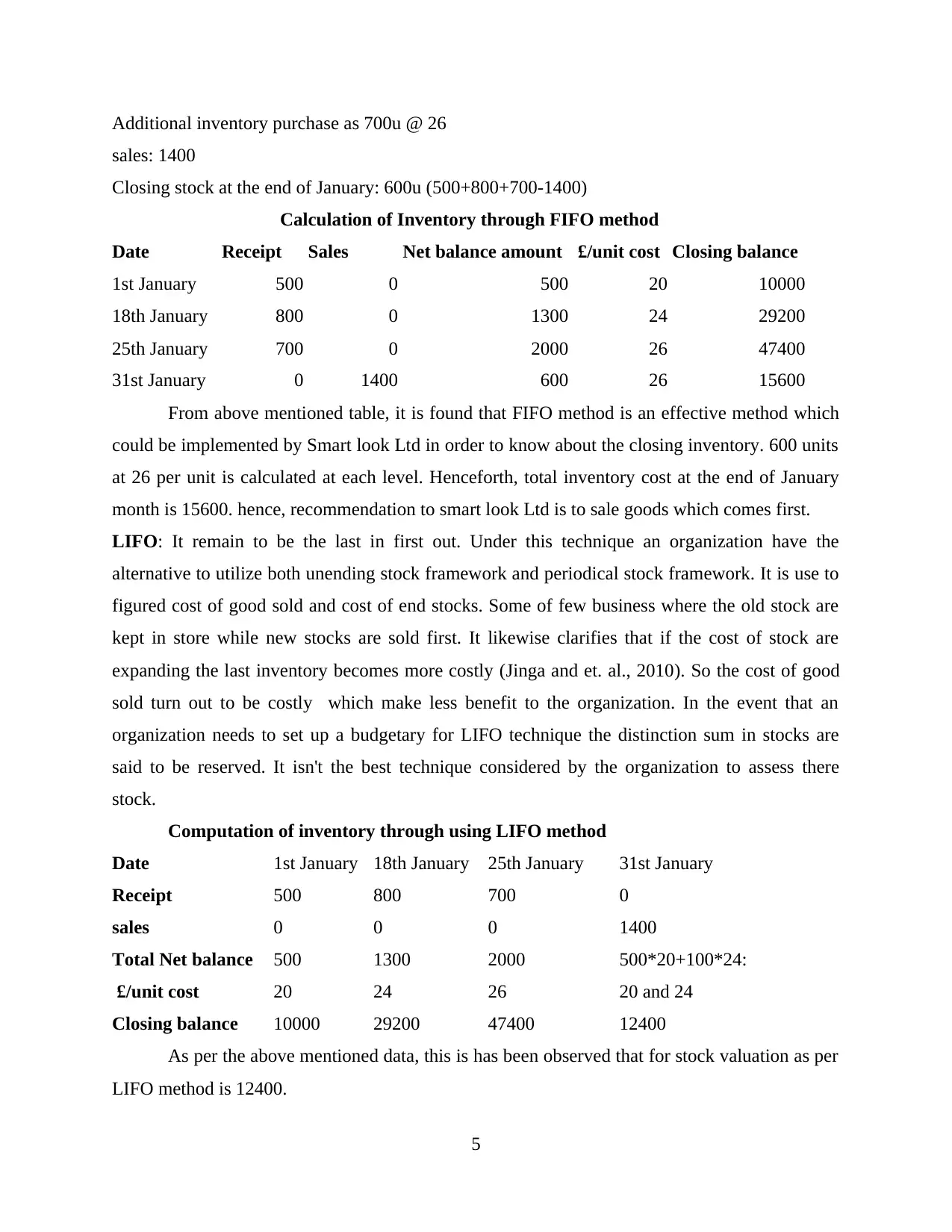

Additional inventory purchase as 700u @ 26

sales: 1400

Closing stock at the end of January: 600u (500+800+700-1400)

Calculation of Inventory through FIFO method

Date Receipt Sales Net balance amount £/unit cost Closing balance

1st January 500 0 500 20 10000

18th January 800 0 1300 24 29200

25th January 700 0 2000 26 47400

31st January 0 1400 600 26 15600

From above mentioned table, it is found that FIFO method is an effective method which

could be implemented by Smart look Ltd in order to know about the closing inventory. 600 units

at 26 per unit is calculated at each level. Henceforth, total inventory cost at the end of January

month is 15600. hence, recommendation to smart look Ltd is to sale goods which comes first.

LIFO: It remain to be the last in first out. Under this technique an organization have the

alternative to utilize both unending stock framework and periodical stock framework. It is use to

figured cost of good sold and cost of end stocks. Some of few business where the old stock are

kept in store while new stocks are sold first. It likewise clarifies that if the cost of stock are

expanding the last inventory becomes more costly (Jinga and et. al., 2010). So the cost of good

sold turn out to be costly which make less benefit to the organization. In the event that an

organization needs to set up a budgetary for LIFO technique the distinction sum in stocks are

said to be reserved. It isn't the best technique considered by the organization to assess there

stock.

Computation of inventory through using LIFO method

Date 1st January 18th January 25th January 31st January

Receipt 500 800 700 0

sales 0 0 0 1400

Total Net balance 500 1300 2000 500*20+100*24:

£/unit cost 20 24 26 20 and 24

Closing balance 10000 29200 47400 12400

As per the above mentioned data, this is has been observed that for stock valuation as per

LIFO method is 12400.

5

sales: 1400

Closing stock at the end of January: 600u (500+800+700-1400)

Calculation of Inventory through FIFO method

Date Receipt Sales Net balance amount £/unit cost Closing balance

1st January 500 0 500 20 10000

18th January 800 0 1300 24 29200

25th January 700 0 2000 26 47400

31st January 0 1400 600 26 15600

From above mentioned table, it is found that FIFO method is an effective method which

could be implemented by Smart look Ltd in order to know about the closing inventory. 600 units

at 26 per unit is calculated at each level. Henceforth, total inventory cost at the end of January

month is 15600. hence, recommendation to smart look Ltd is to sale goods which comes first.

LIFO: It remain to be the last in first out. Under this technique an organization have the

alternative to utilize both unending stock framework and periodical stock framework. It is use to

figured cost of good sold and cost of end stocks. Some of few business where the old stock are

kept in store while new stocks are sold first. It likewise clarifies that if the cost of stock are

expanding the last inventory becomes more costly (Jinga and et. al., 2010). So the cost of good

sold turn out to be costly which make less benefit to the organization. In the event that an

organization needs to set up a budgetary for LIFO technique the distinction sum in stocks are

said to be reserved. It isn't the best technique considered by the organization to assess there

stock.

Computation of inventory through using LIFO method

Date 1st January 18th January 25th January 31st January

Receipt 500 800 700 0

sales 0 0 0 1400

Total Net balance 500 1300 2000 500*20+100*24:

£/unit cost 20 24 26 20 and 24

Closing balance 10000 29200 47400 12400

As per the above mentioned data, this is has been observed that for stock valuation as per

LIFO method is 12400.

5

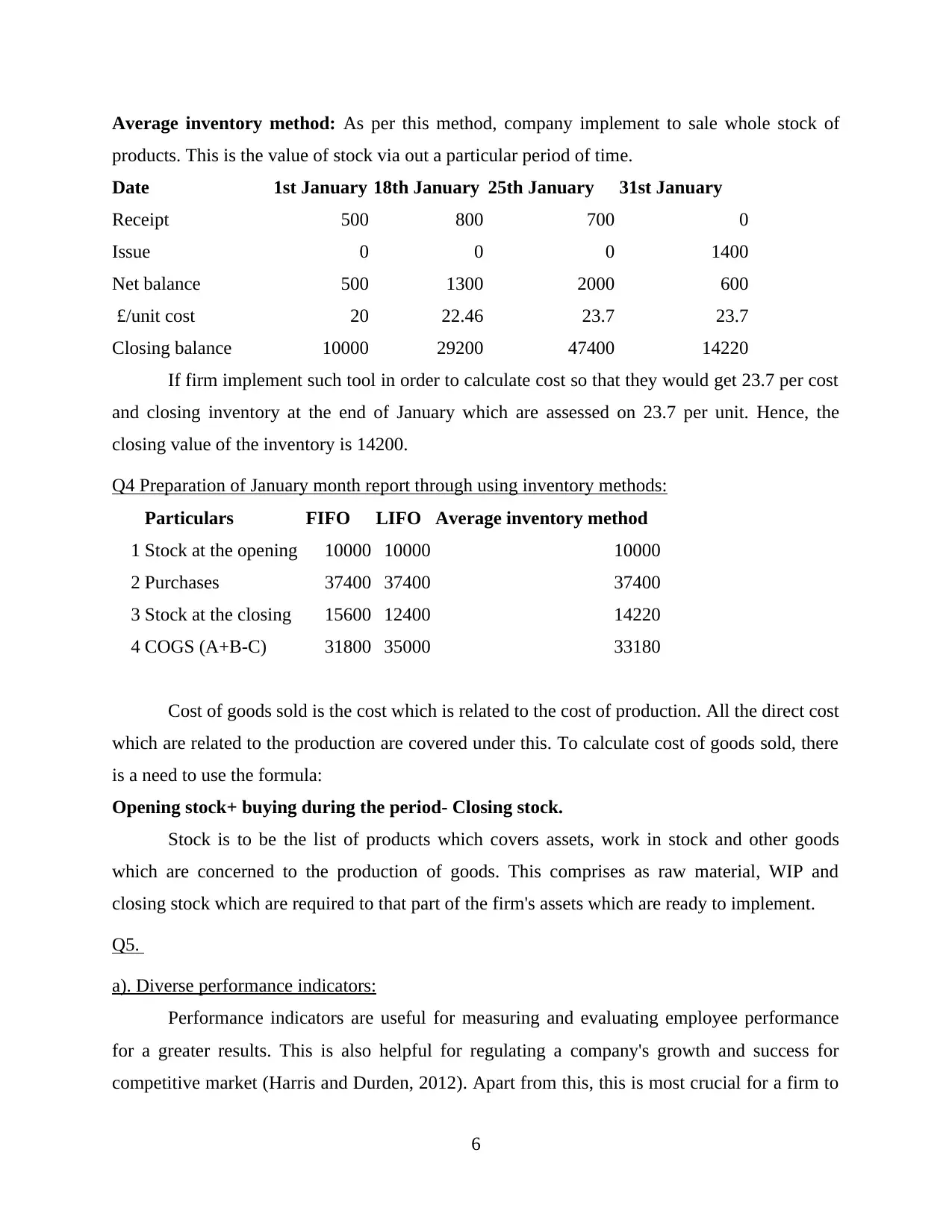

Average inventory method: As per this method, company implement to sale whole stock of

products. This is the value of stock via out a particular period of time.

Date 1st January 18th January 25th January 31st January

Receipt 500 800 700 0

Issue 0 0 0 1400

Net balance 500 1300 2000 600

£/unit cost 20 22.46 23.7 23.7

Closing balance 10000 29200 47400 14220

If firm implement such tool in order to calculate cost so that they would get 23.7 per cost

and closing inventory at the end of January which are assessed on 23.7 per unit. Hence, the

closing value of the inventory is 14200.

Q4 Preparation of January month report through using inventory methods:

Particulars FIFO LIFO Average inventory method

1 Stock at the opening 10000 10000 10000

2 Purchases 37400 37400 37400

3 Stock at the closing 15600 12400 14220

4 COGS (A+B-C) 31800 35000 33180

Cost of goods sold is the cost which is related to the cost of production. All the direct cost

which are related to the production are covered under this. To calculate cost of goods sold, there

is a need to use the formula:

Opening stock+ buying during the period- Closing stock.

Stock is to be the list of products which covers assets, work in stock and other goods

which are concerned to the production of goods. This comprises as raw material, WIP and

closing stock which are required to that part of the firm's assets which are ready to implement.

Q5.

a). Diverse performance indicators:

Performance indicators are useful for measuring and evaluating employee performance

for a greater results. This is also helpful for regulating a company's growth and success for

competitive market (Harris and Durden, 2012). Apart from this, this is most crucial for a firm to

6

products. This is the value of stock via out a particular period of time.

Date 1st January 18th January 25th January 31st January

Receipt 500 800 700 0

Issue 0 0 0 1400

Net balance 500 1300 2000 600

£/unit cost 20 22.46 23.7 23.7

Closing balance 10000 29200 47400 14220

If firm implement such tool in order to calculate cost so that they would get 23.7 per cost

and closing inventory at the end of January which are assessed on 23.7 per unit. Hence, the

closing value of the inventory is 14200.

Q4 Preparation of January month report through using inventory methods:

Particulars FIFO LIFO Average inventory method

1 Stock at the opening 10000 10000 10000

2 Purchases 37400 37400 37400

3 Stock at the closing 15600 12400 14220

4 COGS (A+B-C) 31800 35000 33180

Cost of goods sold is the cost which is related to the cost of production. All the direct cost

which are related to the production are covered under this. To calculate cost of goods sold, there

is a need to use the formula:

Opening stock+ buying during the period- Closing stock.

Stock is to be the list of products which covers assets, work in stock and other goods

which are concerned to the production of goods. This comprises as raw material, WIP and

closing stock which are required to that part of the firm's assets which are ready to implement.

Q5.

a). Diverse performance indicators:

Performance indicators are useful for measuring and evaluating employee performance

for a greater results. This is also helpful for regulating a company's growth and success for

competitive market (Harris and Durden, 2012). Apart from this, this is most crucial for a firm to

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

determine the key components that are covered in its performance. This covers requirement of

productivity measurement and such kind of techniques are implemented under this. There are

followings tools which are accountable for analysing performance of employees under a firm.

These are mentioned hereunder:

Customer experiences:- customers are the major tool who supports the firm for

identifying its success. A firm is likewise assess its performance level by taking

feedbacks from customers feedbacks. This assists managers to address whether they are

meeting market demands and trends.

Supplier and product quality:- If a firm supplies value added goods to its buyers and if

such buyers would satisfy their needs then the company would able to make certain

assumptions effectively (Faÿ, Introna and Puyou, 2010).

Soundness of operations:- This is an ethical accountability of the higher authorities which

aims to enhance its operations in an effective manner. Such would assist the firm to

expand the area of production materials or products.

Reducing maintenance budgeting:- there are so many avoidable expenses which occurs

during production. Which gives adverse impacts on the firm performance. There is a need

to make plan by which such kinds of costs eliminates in an effective manner (Zainun

Tuanmat and Smith, 2011).

b).

1. To reduce costs:

Cost is the main tool for making the product. However, management of the Smart Look

Ltd eliminate wastage costs which helps the firm in order to make optimise the profits.

Regarding such process, management implement various diverse process which ultimately used

for maximising the profits and minimising the costs of the cost of production. Although, this can

be said that the company is always implementing diverse tools that could totally helpful for

reducing the costs of production while making product (Bodie, Kane and Marcus, 2014). These

tools are used by the firm in order to reduce costs which are usually connected with the

manufacturing process covers the following:

1. Enhanced strategies and processes: Taking a fresh, strategic approach to processes is the

first steps for determining various ways to reduce costs throughout the production process. This

permits an advance manner for evaluating staff, resources and various processes.

7

productivity measurement and such kind of techniques are implemented under this. There are

followings tools which are accountable for analysing performance of employees under a firm.

These are mentioned hereunder:

Customer experiences:- customers are the major tool who supports the firm for

identifying its success. A firm is likewise assess its performance level by taking

feedbacks from customers feedbacks. This assists managers to address whether they are

meeting market demands and trends.

Supplier and product quality:- If a firm supplies value added goods to its buyers and if

such buyers would satisfy their needs then the company would able to make certain

assumptions effectively (Faÿ, Introna and Puyou, 2010).

Soundness of operations:- This is an ethical accountability of the higher authorities which

aims to enhance its operations in an effective manner. Such would assist the firm to

expand the area of production materials or products.

Reducing maintenance budgeting:- there are so many avoidable expenses which occurs

during production. Which gives adverse impacts on the firm performance. There is a need

to make plan by which such kinds of costs eliminates in an effective manner (Zainun

Tuanmat and Smith, 2011).

b).

1. To reduce costs:

Cost is the main tool for making the product. However, management of the Smart Look

Ltd eliminate wastage costs which helps the firm in order to make optimise the profits.

Regarding such process, management implement various diverse process which ultimately used

for maximising the profits and minimising the costs of the cost of production. Although, this can

be said that the company is always implementing diverse tools that could totally helpful for

reducing the costs of production while making product (Bodie, Kane and Marcus, 2014). These

tools are used by the firm in order to reduce costs which are usually connected with the

manufacturing process covers the following:

1. Enhanced strategies and processes: Taking a fresh, strategic approach to processes is the

first steps for determining various ways to reduce costs throughout the production process. This

permits an advance manner for evaluating staff, resources and various processes.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Enhanced Customer understanding and services: The quality system assist the

management to limit the costs with the help of rendering a great understanding of customer

needs.

2. To enhance value:

Within a firm, this has been observed that the owners of the firm are facing diverse

problems for providing great quality of product to its customers. However, few of them could

achieve success for getting set of targets. As, they are the risk taker. For enhancing value of the

firm, management is requires to follow its pre-set objectives and frame a plan. Few of them are

as follows:

Find out mistakes: the senior manager are accountable to analysis the performance in order to

know whether it is going in the right ways for gaining their pre-set targets.

Development of training: Management needs to give more attention in terms of money and time

in order to make training program more effective and efficient.

TASK 2

Q6

a). Budget:

This is the estimation of whole income which a firm is generate and expenditure are done

at the given period of time (Callahan, Stetz and Brooks, 2011). The main objective of budget is

to incorporate an entire framework for making efficient implementation of funds. There are

various types of budgets which can be used by the firm for making efficient operations.

Zero base budgeting: this is the method under which a firm manage their expenses. This

always starts with the base. That is the reason, this is called zero base budgeting.

Flexible budget: This is the budget which changes according to the activities. This is

totally different from the static budget as these remains constant .

B). Objectives of budget formulation:

This is observed that divers firms uses budgets in an effective manner that are to be

evaluated with the actual outcome and then the firm compare them so that the if any deviation

occurs, will eliminates effectively. Budget assist the firm for making effective strategies as per

the budgeted plan.

8

management to limit the costs with the help of rendering a great understanding of customer

needs.

2. To enhance value:

Within a firm, this has been observed that the owners of the firm are facing diverse

problems for providing great quality of product to its customers. However, few of them could

achieve success for getting set of targets. As, they are the risk taker. For enhancing value of the

firm, management is requires to follow its pre-set objectives and frame a plan. Few of them are

as follows:

Find out mistakes: the senior manager are accountable to analysis the performance in order to

know whether it is going in the right ways for gaining their pre-set targets.

Development of training: Management needs to give more attention in terms of money and time

in order to make training program more effective and efficient.

TASK 2

Q6

a). Budget:

This is the estimation of whole income which a firm is generate and expenditure are done

at the given period of time (Callahan, Stetz and Brooks, 2011). The main objective of budget is

to incorporate an entire framework for making efficient implementation of funds. There are

various types of budgets which can be used by the firm for making efficient operations.

Zero base budgeting: this is the method under which a firm manage their expenses. This

always starts with the base. That is the reason, this is called zero base budgeting.

Flexible budget: This is the budget which changes according to the activities. This is

totally different from the static budget as these remains constant .

B). Objectives of budget formulation:

This is observed that divers firms uses budgets in an effective manner that are to be

evaluated with the actual outcome and then the firm compare them so that the if any deviation

occurs, will eliminates effectively. Budget assist the firm for making effective strategies as per

the budgeted plan.

8

c). Process of budget preparation:

Budget preparation is the main tool which are used by the firm for estimating inflows and

outflows for a given period of time. There are diverse methods which are used for preparation of

budgets:

Zero-based Budgeting: This is the performance of budgeting under which whole

distribution for each advance time (Baldvinsdottir, Mitchell and Nørreklit, 2010). This

emerge from zero base and whole role is analysed.

Fixed budget: This is the budget which remains constant and does not change with the

change in the other factors. Usually, this kind of budget is avoided by many firms as this

is fixed and does not change.

Variable budget: This is the budget which change as per the change in the production.

This is the most effective budget and change as per the change in the cost (Bennett,

Schaltegger and Zvezdov, 2011).

Q7: Preparation of different budgets

a) Sales budget of smart look Ltd

Month Forecasting sales in Units Sales in Units Total sales

April 2000 30 £60000

May 1500 30 £45000

June 2500 30 £75000

Total 6000 30 180000

From the above sales budget, it has been found that being actual sales units remain the

same as 30 units they are getting profit total profit of 180000. In the month of June they are

receiving maximum profit with the forecasted unit of 2500.

b) Production Budget:

Months April May June

Estimated sales 2000 1500 2500

Add: Closing units 150 250 100

Less: Opening units 100 150 250

Total production in units 2050 1600 2350

9

Budget preparation is the main tool which are used by the firm for estimating inflows and

outflows for a given period of time. There are diverse methods which are used for preparation of

budgets:

Zero-based Budgeting: This is the performance of budgeting under which whole

distribution for each advance time (Baldvinsdottir, Mitchell and Nørreklit, 2010). This

emerge from zero base and whole role is analysed.

Fixed budget: This is the budget which remains constant and does not change with the

change in the other factors. Usually, this kind of budget is avoided by many firms as this

is fixed and does not change.

Variable budget: This is the budget which change as per the change in the production.

This is the most effective budget and change as per the change in the cost (Bennett,

Schaltegger and Zvezdov, 2011).

Q7: Preparation of different budgets

a) Sales budget of smart look Ltd

Month Forecasting sales in Units Sales in Units Total sales

April 2000 30 £60000

May 1500 30 £45000

June 2500 30 £75000

Total 6000 30 180000

From the above sales budget, it has been found that being actual sales units remain the

same as 30 units they are getting profit total profit of 180000. In the month of June they are

receiving maximum profit with the forecasted unit of 2500.

b) Production Budget:

Months April May June

Estimated sales 2000 1500 2500

Add: Closing units 150 250 100

Less: Opening units 100 150 250

Total production in units 2050 1600 2350

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.