Management Accounting Task 2 Report: Costing, Budgeting, and Analysis

VerifiedAdded on 2023/01/18

|16

|3451

|87

Report

AI Summary

This report delves into the core principles of management accounting, focusing on practical applications within a business context, using Prime Furniture as a case study. It begins by exploring different costing methods, including marginal and absorption costing, and demonstrates their impact on profit calculations through detailed financial analyses and reconciliation statements. The report then examines various planning tools for budgetary control, such as capital and operating budgets, and alternative methods like zero-based budgeting, along with their advantages and disadvantages. Furthermore, it discusses the behavioral implications of budgeting and explores pricing strategies. The report also includes PEST and SWOT analyses to assess the external and internal factors influencing the business. Overall, the report provides a comprehensive overview of management accounting practices, including costing, budgeting, and financial planning, providing valuable insights for business decision-making and strategic management.

Management Accounting

(Task-2)

(Task-2)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.................................................................................................................................3

TASK 2.................................................................................................................................................3

P3: Calculation of costs by using different costing methods..............................................................3

P4: Advantages and disadvantages of different planning tool used for budgetary control...............9

P5 Comparison of the way in which organisations are adapting management accounting systems

.........................................................................................................................................................13

CONCLUSION...................................................................................................................................14

REFERENCES....................................................................................................................................15

INTRODUCTION.................................................................................................................................3

TASK 2.................................................................................................................................................3

P3: Calculation of costs by using different costing methods..............................................................3

P4: Advantages and disadvantages of different planning tool used for budgetary control...............9

P5 Comparison of the way in which organisations are adapting management accounting systems

.........................................................................................................................................................13

CONCLUSION...................................................................................................................................14

REFERENCES....................................................................................................................................15

INTRODUCTION

Management accounting is the process of managing and maintaining books of

accounts with the purpose of making an effective decision and plans for the betterment of an

organisation (Bromwich and Scapens, 2016). For this, finance manager need to provide a

sufficient support by preparing final accounts such as profit and loss account, balance sheet,

cash flow statement etc. on timely basis. The present assignment report is based on Prime

furniture which is a growing East London based company now plans to start training course

for their new interns in November 2019. In this regards, different costing methods are studied

along with the planning tools to control budget. Along with this, role of management

accounting system in resolving financial issues are also discussed under this report.

TASK 2

P3: Calculation of costs by using different costing methods

Cost: It is defined as the amount measured in monetary terms consisting of different

factors such as efforts, time, resources utilised etc. to produce or manufacture something that

brings valuate outcome to an organisation in future period of time. It comprises of two types

which includes direct and indirect cost (Bryson, Crosby and Bloomberg, 2014). Direct cost

refers to the amount which is directly allocated to production activity whereas indirect cost

includes amount which is indirectly invested for the completed for particular project activity.

In the context of Prime furniture, huge amount is invested by production team to make their

desired project activities more successful by spending on purchasing raw materials, hiring

labour etc.

Marginal costing: It is a costing technique which focuses about just variable cost and

overlook fixed expense because of which it has other name i.e. variable costing technique.

Adopting such technique expands the figures of net benefit under the financial report

because of considering just variable cost because of which it is generally used by small and

medium sized manufacturing company such as Prime furniture.

Absorption costing: It is a method which considers both fixed and variable cost due to

which the net profit recorded under the financial statement are low in comparison with the net

profit comes under marginal costing method. It is used by large businesses who wants to

Management accounting is the process of managing and maintaining books of

accounts with the purpose of making an effective decision and plans for the betterment of an

organisation (Bromwich and Scapens, 2016). For this, finance manager need to provide a

sufficient support by preparing final accounts such as profit and loss account, balance sheet,

cash flow statement etc. on timely basis. The present assignment report is based on Prime

furniture which is a growing East London based company now plans to start training course

for their new interns in November 2019. In this regards, different costing methods are studied

along with the planning tools to control budget. Along with this, role of management

accounting system in resolving financial issues are also discussed under this report.

TASK 2

P3: Calculation of costs by using different costing methods

Cost: It is defined as the amount measured in monetary terms consisting of different

factors such as efforts, time, resources utilised etc. to produce or manufacture something that

brings valuate outcome to an organisation in future period of time. It comprises of two types

which includes direct and indirect cost (Bryson, Crosby and Bloomberg, 2014). Direct cost

refers to the amount which is directly allocated to production activity whereas indirect cost

includes amount which is indirectly invested for the completed for particular project activity.

In the context of Prime furniture, huge amount is invested by production team to make their

desired project activities more successful by spending on purchasing raw materials, hiring

labour etc.

Marginal costing: It is a costing technique which focuses about just variable cost and

overlook fixed expense because of which it has other name i.e. variable costing technique.

Adopting such technique expands the figures of net benefit under the financial report

because of considering just variable cost because of which it is generally used by small and

medium sized manufacturing company such as Prime furniture.

Absorption costing: It is a method which considers both fixed and variable cost due to

which the net profit recorded under the financial statement are low in comparison with the net

profit comes under marginal costing method. It is used by large businesses who wants to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

show actual financial position towards its shareholders with a motive to retain them with

company for longer duration (Englund and Gerdin, 2014).

Cost analysis: It is the procedure which is done to analyse the outcomes received after

investing amount in business activities. This will help manager of Prime furniture to make

decision regarding making further investment according to the possible outcomes.

Cost volume profit: It is a technique of cost accounting adopted by managers of Prime

furniture with a motive of evaluating the impact of variations in cost and volume on

organisational profit.

Flexible budgeting: It is kind of budget in which pre-determined amount may vary

according to the situations arises during future business activities. It reduces wastage of

resources utilised by Prime furniture by fluctuating the budget according to the possibilities

of receiving better outcomes (Honggowati and et.al., 2017).

Activity based costing: It is termed as technique which is adopted by Prime furniture

in order to allocate costs to different business activities on the basis of actual expenses taken

place during execution.

Role of costing in setting price: Costing plays an important role in manufacturing

furniture products by Prime furniture as it help them in determining the actual cost which is

incurred while conducting several business activities. Through thus, the manager can set a

price for its furniture after adding margin on it.

Inventory cost: It is the cost which is incurred to store and maintain the level of stock

in warehouses in order to meet clients requirements on time. It consists of two types which

includes:

Ordering cost: This is the cost which is incurred while creating and ordering raw

material for manufacturing furniture products from suppliers is called as ordering cost (Linoff

and Berry, 2011).

Carrying cost: It is another cost which also known as holding cost due to maintaining

adequate level of inventory in warehouses just to meet client’ s requirements.

Shortage cost: In this, cost take place when Prime furniture have faced shortage of

inventory with them.

company for longer duration (Englund and Gerdin, 2014).

Cost analysis: It is the procedure which is done to analyse the outcomes received after

investing amount in business activities. This will help manager of Prime furniture to make

decision regarding making further investment according to the possible outcomes.

Cost volume profit: It is a technique of cost accounting adopted by managers of Prime

furniture with a motive of evaluating the impact of variations in cost and volume on

organisational profit.

Flexible budgeting: It is kind of budget in which pre-determined amount may vary

according to the situations arises during future business activities. It reduces wastage of

resources utilised by Prime furniture by fluctuating the budget according to the possibilities

of receiving better outcomes (Honggowati and et.al., 2017).

Activity based costing: It is termed as technique which is adopted by Prime furniture

in order to allocate costs to different business activities on the basis of actual expenses taken

place during execution.

Role of costing in setting price: Costing plays an important role in manufacturing

furniture products by Prime furniture as it help them in determining the actual cost which is

incurred while conducting several business activities. Through thus, the manager can set a

price for its furniture after adding margin on it.

Inventory cost: It is the cost which is incurred to store and maintain the level of stock

in warehouses in order to meet clients requirements on time. It consists of two types which

includes:

Ordering cost: This is the cost which is incurred while creating and ordering raw

material for manufacturing furniture products from suppliers is called as ordering cost (Linoff

and Berry, 2011).

Carrying cost: It is another cost which also known as holding cost due to maintaining

adequate level of inventory in warehouses just to meet client’ s requirements.

Shortage cost: In this, cost take place when Prime furniture have faced shortage of

inventory with them.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

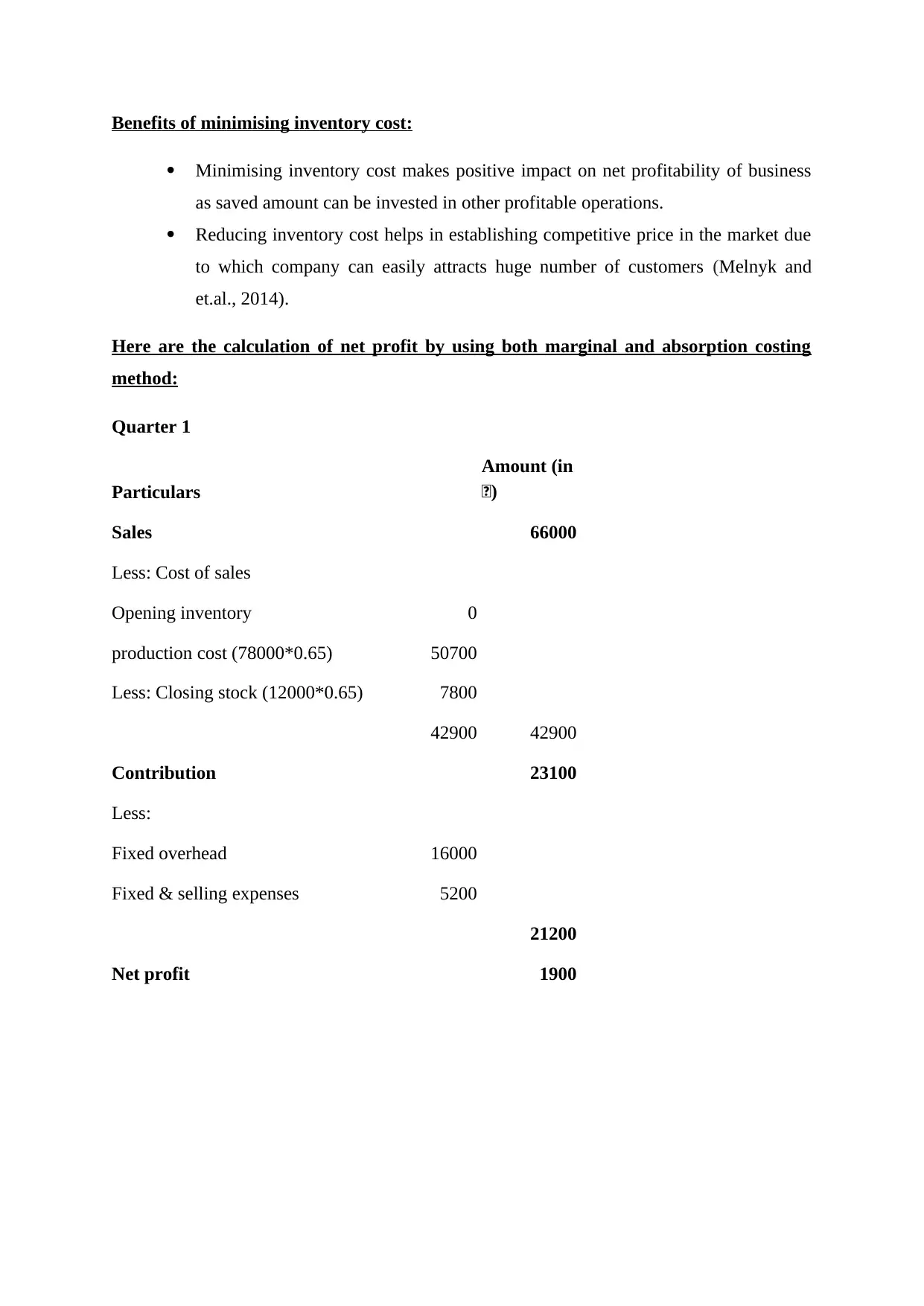

Benefits of minimising inventory cost:

Minimising inventory cost makes positive impact on net profitability of business

as saved amount can be invested in other profitable operations.

Reducing inventory cost helps in establishing competitive price in the market due

to which company can easily attracts huge number of customers (Melnyk and

et.al., 2014).

Here are the calculation of net profit by using both marginal and absorption costing

method:

Quarter 1

Particulars

Amount (in

£)

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock (12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 1900

Minimising inventory cost makes positive impact on net profitability of business

as saved amount can be invested in other profitable operations.

Reducing inventory cost helps in establishing competitive price in the market due

to which company can easily attracts huge number of customers (Melnyk and

et.al., 2014).

Here are the calculation of net profit by using both marginal and absorption costing

method:

Quarter 1

Particulars

Amount (in

£)

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock (12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 1900

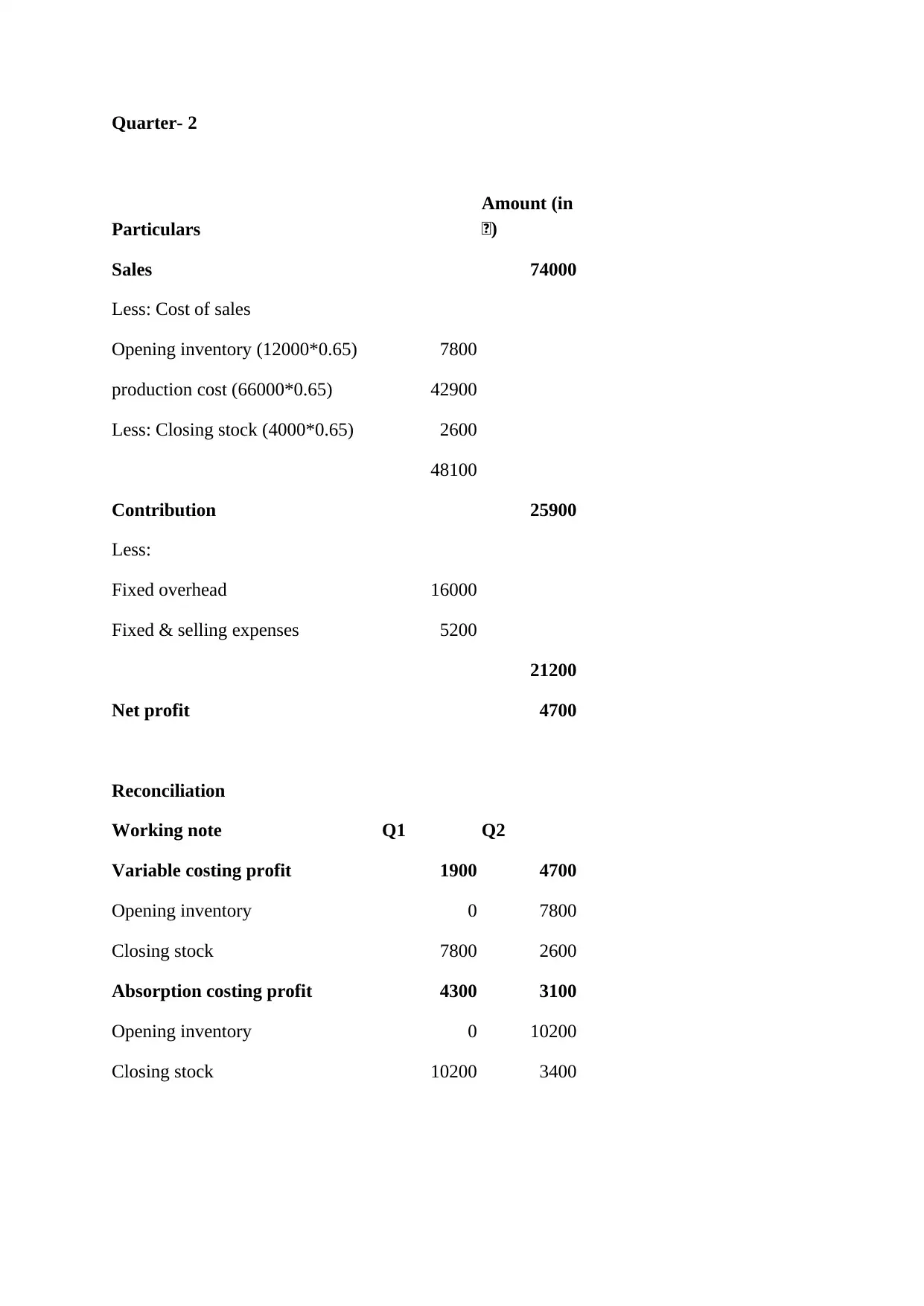

Quarter- 2

Particulars

Amount (in

£)

Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 4700

Reconciliation

Working note Q1 Q2

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Particulars

Amount (in

£)

Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 4700

Reconciliation

Working note Q1 Q2

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

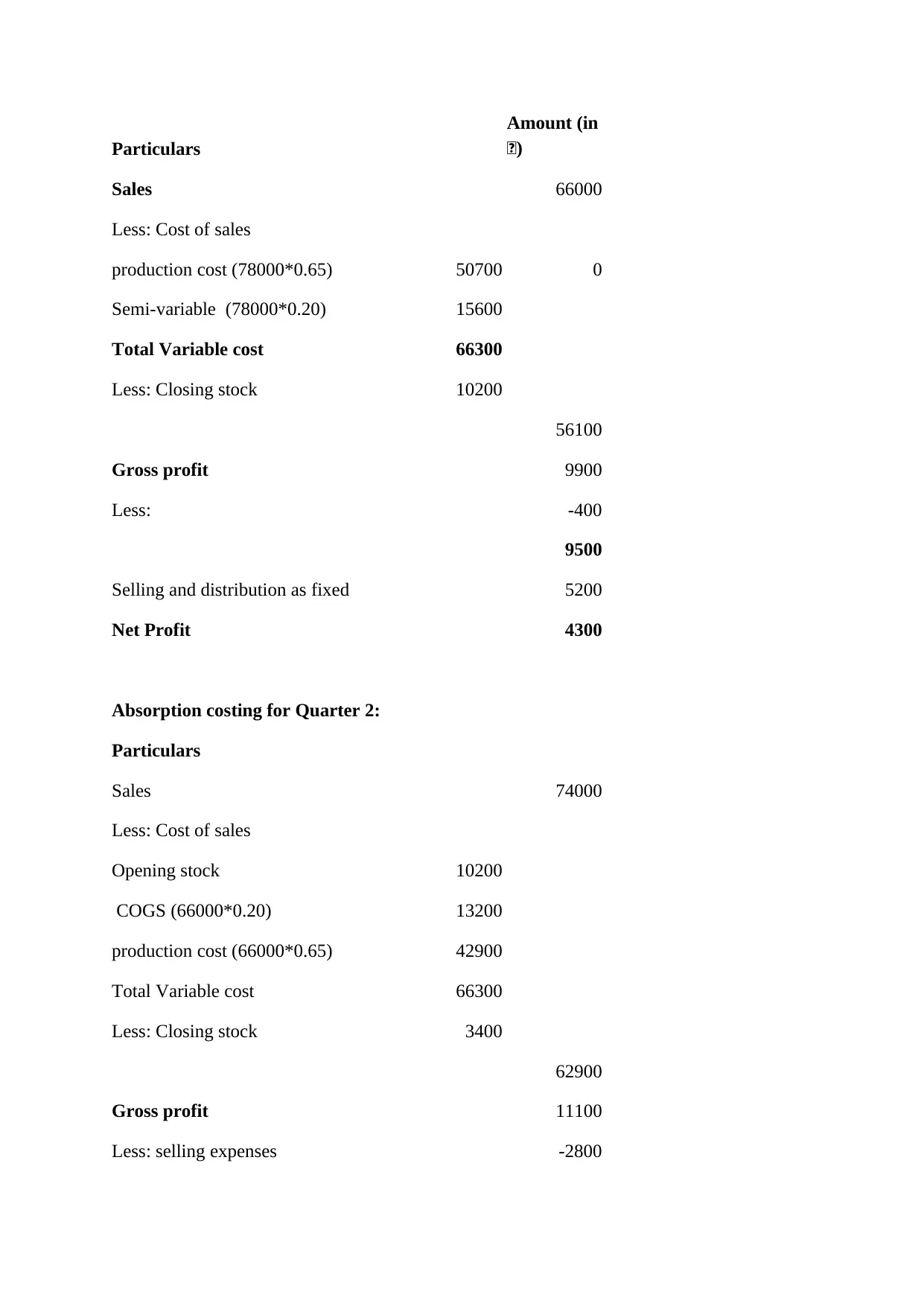

Absorption costing for Quarter 1:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars

Amount (in

£)

Sales 66000

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for Quarter 2:

Particulars

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

Amount (in

£)

Sales 66000

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for Quarter 2:

Particulars

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

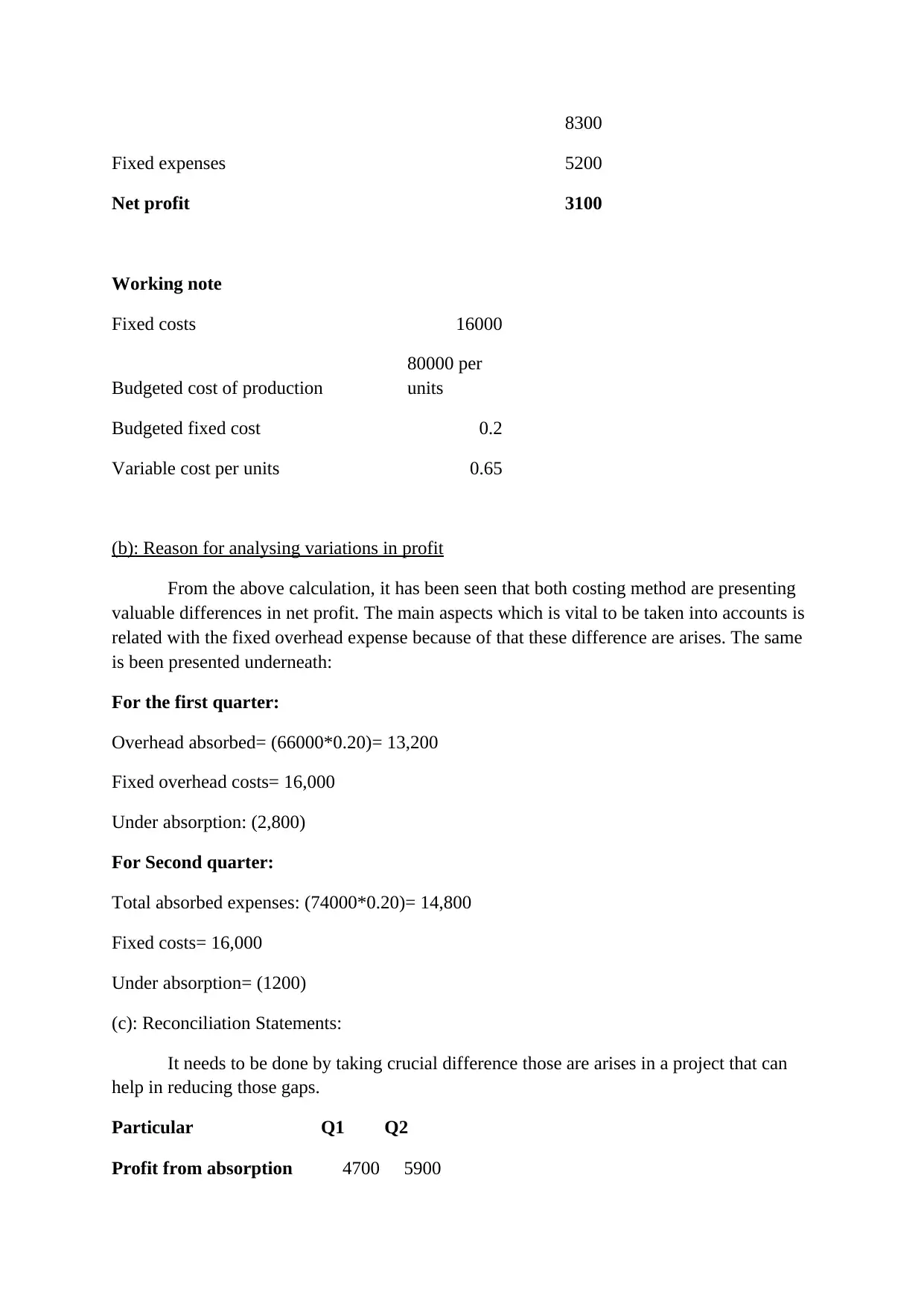

8300

Fixed expenses 5200

Net profit 3100

Working note

Fixed costs 16000

Budgeted cost of production

80000 per

units

Budgeted fixed cost 0.2

Variable cost per units 0.65

(b): Reason for analysing variations in profit

From the above calculation, it has been seen that both costing method are presenting

valuable differences in net profit. The main aspects which is vital to be taken into accounts is

related with the fixed overhead expense because of that these difference are arises. The same

is been presented underneath:

For the first quarter:

Overhead absorbed= (66000*0.20)= 13,200

Fixed overhead costs= 16,000

Under absorption: (2,800)

For Second quarter:

Total absorbed expenses: (74000*0.20)= 14,800

Fixed costs= 16,000

Under absorption= (1200)

(c): Reconciliation Statements:

It needs to be done by taking crucial difference those are arises in a project that can

help in reducing those gaps.

Particular Q1 Q2

Profit from absorption 4700 5900

Fixed expenses 5200

Net profit 3100

Working note

Fixed costs 16000

Budgeted cost of production

80000 per

units

Budgeted fixed cost 0.2

Variable cost per units 0.65

(b): Reason for analysing variations in profit

From the above calculation, it has been seen that both costing method are presenting

valuable differences in net profit. The main aspects which is vital to be taken into accounts is

related with the fixed overhead expense because of that these difference are arises. The same

is been presented underneath:

For the first quarter:

Overhead absorbed= (66000*0.20)= 13,200

Fixed overhead costs= 16,000

Under absorption: (2,800)

For Second quarter:

Total absorbed expenses: (74000*0.20)= 14,800

Fixed costs= 16,000

Under absorption= (1200)

(c): Reconciliation Statements:

It needs to be done by taking crucial difference those are arises in a project that can

help in reducing those gaps.

Particular Q1 Q2

Profit from absorption 4700 5900

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

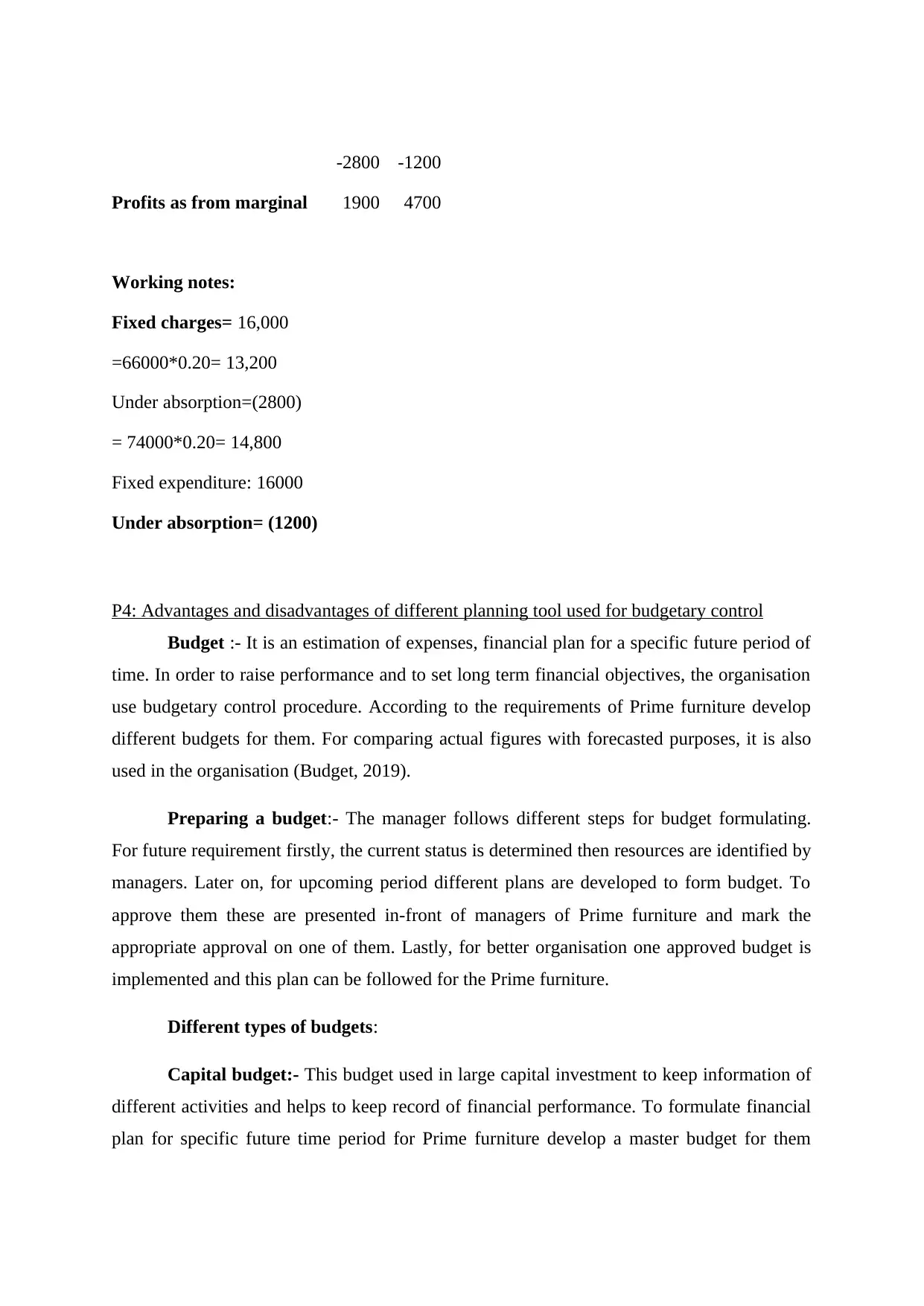

-2800 -1200

Profits as from marginal 1900 4700

Working notes:

Fixed charges= 16,000

=66000*0.20= 13,200

Under absorption=(2800)

= 74000*0.20= 14,800

Fixed expenditure: 16000

Under absorption= (1200)

P4: Advantages and disadvantages of different planning tool used for budgetary control

Budget :- It is an estimation of expenses, financial plan for a specific future period of

time. In order to raise performance and to set long term financial objectives, the organisation

use budgetary control procedure. According to the requirements of Prime furniture develop

different budgets for them. For comparing actual figures with forecasted purposes, it is also

used in the organisation (Budget, 2019).

Preparing a budget:- The manager follows different steps for budget formulating.

For future requirement firstly, the current status is determined then resources are identified by

managers. Later on, for upcoming period different plans are developed to form budget. To

approve them these are presented in-front of managers of Prime furniture and mark the

appropriate approval on one of them. Lastly, for better organisation one approved budget is

implemented and this plan can be followed for the Prime furniture.

Different types of budgets:

Capital budget:- This budget used in large capital investment to keep information of

different activities and helps to keep record of financial performance. To formulate financial

plan for specific future time period for Prime furniture develop a master budget for them

Profits as from marginal 1900 4700

Working notes:

Fixed charges= 16,000

=66000*0.20= 13,200

Under absorption=(2800)

= 74000*0.20= 14,800

Fixed expenditure: 16000

Under absorption= (1200)

P4: Advantages and disadvantages of different planning tool used for budgetary control

Budget :- It is an estimation of expenses, financial plan for a specific future period of

time. In order to raise performance and to set long term financial objectives, the organisation

use budgetary control procedure. According to the requirements of Prime furniture develop

different budgets for them. For comparing actual figures with forecasted purposes, it is also

used in the organisation (Budget, 2019).

Preparing a budget:- The manager follows different steps for budget formulating.

For future requirement firstly, the current status is determined then resources are identified by

managers. Later on, for upcoming period different plans are developed to form budget. To

approve them these are presented in-front of managers of Prime furniture and mark the

appropriate approval on one of them. Lastly, for better organisation one approved budget is

implemented and this plan can be followed for the Prime furniture.

Different types of budgets:

Capital budget:- This budget used in large capital investment to keep information of

different activities and helps to keep record of financial performance. To formulate financial

plan for specific future time period for Prime furniture develop a master budget for them

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Nørreklit, 2017). There are some advantages and disadvantages of the budget and they are

below:

Advantages :-

A larger number of monetary resources are invested, so this helps to keep the record

of all projects.

To determine financial performance of organisation, it provides high angle of the

business to the stakeholders.

Disadvantages :-

Due to its consist of clustered data of all departments, lack of specificity occur.

It is difficult to observe because of collective information at high level.

Operating budget:- This budget is used to calculate income and expenses which are based

on forecasted sales and revenues. To examine the monetary resources that are appropriately

undertaking or not, Prime furniture create this budget to help their top level of executives

(Quattrone, 2016). Few advantages and disadvantages are there which are as follows:-

Advantages:-

It provide long term financial obligations which allows to predict the cost and manage

the spending in short term.

This budget evaluated the past and present expenses.

Disadvantages :-

The revenues and figures can overstate of organisation.

Figures can manipulate easily.

Alternative method of budgeting:- The various alternative budgeting methods are there

which are as below.

Zero based budgeting:- This budgeting starts from zero. In this for a new period, all

expenses are justified. In order to reduce the cost of operations for Prime furniture by

justifying all the costs rerecorded in the books.

Advantage : To establish accuracy, a new budget is formulated at each accounting

year.

below:

Advantages :-

A larger number of monetary resources are invested, so this helps to keep the record

of all projects.

To determine financial performance of organisation, it provides high angle of the

business to the stakeholders.

Disadvantages :-

Due to its consist of clustered data of all departments, lack of specificity occur.

It is difficult to observe because of collective information at high level.

Operating budget:- This budget is used to calculate income and expenses which are based

on forecasted sales and revenues. To examine the monetary resources that are appropriately

undertaking or not, Prime furniture create this budget to help their top level of executives

(Quattrone, 2016). Few advantages and disadvantages are there which are as follows:-

Advantages:-

It provide long term financial obligations which allows to predict the cost and manage

the spending in short term.

This budget evaluated the past and present expenses.

Disadvantages :-

The revenues and figures can overstate of organisation.

Figures can manipulate easily.

Alternative method of budgeting:- The various alternative budgeting methods are there

which are as below.

Zero based budgeting:- This budgeting starts from zero. In this for a new period, all

expenses are justified. In order to reduce the cost of operations for Prime furniture by

justifying all the costs rerecorded in the books.

Advantage : To establish accuracy, a new budget is formulated at each accounting

year.

Disadvantage : In this, records can be biased by managers so it is not appropriate for

short term planning.

Cash only or traditional budgeting :- it is the inflows and outflows of cash receipt and

payment over a period of time and expected occur monthly and quarterly. To keep track

record of monetary resources of organisation, it is conducted by Prime furniture (Senftlechner

and Hiebl, 2015).

Advantage: It is used to identify the loss in company's financial statements.

Disadvantage: To deal credit transactions it limits the power of organisation.

Behavioural implications of budget :

It helps to improve communication among employees.

It consider actual data instead of budgeted figures .

Requires high monetary investment as the process of formulating budget is very

complex.

In this highly skilled managers are required to form budget for small companies.

Pricing strategies: organisation use different pricing strategies to set price for products.

Penetration : in this , the low prices are set at initial level that are going to be sold to

clients.

Premium : in this, high pricing is set by business that are sold to customers due to

high quality of products (Tucker and Lowe, 2014).

This is used by Ryder architecture to set prices for the constructed buildings.

Ways of competitors determine their prices :- Competitors of Ryder Prime

furniture such as Laz furniture determine their prices by analysing market situations.

Demand and supply considerations :- in order to achieve success, Prime furniture

required various demand and supply considerations and these are economic conditions,

market situations, social factors changes.

PEST analysis:

political:- the affect of unstable political situations on Prime furniture can result in

changes in government policies and cant alter their strategies according to it.

Economic :- Fluctuation in inflation and deflation rates can impact upon purchasing

power of clients.

short term planning.

Cash only or traditional budgeting :- it is the inflows and outflows of cash receipt and

payment over a period of time and expected occur monthly and quarterly. To keep track

record of monetary resources of organisation, it is conducted by Prime furniture (Senftlechner

and Hiebl, 2015).

Advantage: It is used to identify the loss in company's financial statements.

Disadvantage: To deal credit transactions it limits the power of organisation.

Behavioural implications of budget :

It helps to improve communication among employees.

It consider actual data instead of budgeted figures .

Requires high monetary investment as the process of formulating budget is very

complex.

In this highly skilled managers are required to form budget for small companies.

Pricing strategies: organisation use different pricing strategies to set price for products.

Penetration : in this , the low prices are set at initial level that are going to be sold to

clients.

Premium : in this, high pricing is set by business that are sold to customers due to

high quality of products (Tucker and Lowe, 2014).

This is used by Ryder architecture to set prices for the constructed buildings.

Ways of competitors determine their prices :- Competitors of Ryder Prime

furniture such as Laz furniture determine their prices by analysing market situations.

Demand and supply considerations :- in order to achieve success, Prime furniture

required various demand and supply considerations and these are economic conditions,

market situations, social factors changes.

PEST analysis:

political:- the affect of unstable political situations on Prime furniture can result in

changes in government policies and cant alter their strategies according to it.

Economic :- Fluctuation in inflation and deflation rates can impact upon purchasing

power of clients.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.