Management Accounting Assignment: Cost Analysis and Reporting

VerifiedAdded on 2019/12/03

|20

|5365

|224

Homework Assignment

AI Summary

This management accounting assignment provides a comprehensive analysis of costing and budgeting techniques. The solution begins with an introduction to different cost classifications (direct, indirect, function, nature, and behavior) and proceeds to compute the total and unit cost of a job using job costing. The assignment then demonstrates the application of absorption costing, including the allocation of overhead costs and the computation of cost per unit. A detailed analysis of cost data is performed using various techniques. The assignment further includes the preparation and analysis of routine cost reports, the use of performance indicators to identify potential business improvements, and recommendations for cost reduction and value enhancement. Budgeting processes are explained, with the selection of appropriate methods and preparation of production, material purchase, and cash budgets. Finally, variance analysis is conducted, identifying potential causes and recommending corrective actions, along with the preparation of a reconciliation operating statement and a management report.

Management

accounting

accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................4

1.1 Different types of classification of cost.................................................................................4

1.2 Computation of total cost and unit cost of job 444 by making use of job costing................5

1.3 Computation of cost of exquisite by making use of absorption costing technique...............5

1.4 Analysis of cost data of exquisite using appropriate techniques...........................................7

Task 2...............................................................................................................................................8

2.1 Preparation and analysis of routine cost reports....................................................................8

2.2 Use of performance indicators in order to identify potential improvements in business....10

2.3 Recommendation for cost reduction and value enhancement for business.........................10

Task 3.............................................................................................................................................11

3.1 Explanation of purpose and nature of the budgeting process..............................................11

3.2 Selection of appropriate budgeting methods in accordance with the needs of organization

...................................................................................................................................................12

3.3 Preparation of production and material purchase budget....................................................12

3.4 Preparation of cash budget...................................................................................................13

Task 4.............................................................................................................................................16

4.1 Computation of variances along with the identification of possible causes and

recommendation for corrective actions......................................................................................16

4.2 Preparation of reconciliation operating statement...............................................................17

4.3 Management report in accordance with the identified responsibility centres.....................17

Conclusion.....................................................................................................................................18

References......................................................................................................................................19

2

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................4

1.1 Different types of classification of cost.................................................................................4

1.2 Computation of total cost and unit cost of job 444 by making use of job costing................5

1.3 Computation of cost of exquisite by making use of absorption costing technique...............5

1.4 Analysis of cost data of exquisite using appropriate techniques...........................................7

Task 2...............................................................................................................................................8

2.1 Preparation and analysis of routine cost reports....................................................................8

2.2 Use of performance indicators in order to identify potential improvements in business....10

2.3 Recommendation for cost reduction and value enhancement for business.........................10

Task 3.............................................................................................................................................11

3.1 Explanation of purpose and nature of the budgeting process..............................................11

3.2 Selection of appropriate budgeting methods in accordance with the needs of organization

...................................................................................................................................................12

3.3 Preparation of production and material purchase budget....................................................12

3.4 Preparation of cash budget...................................................................................................13

Task 4.............................................................................................................................................16

4.1 Computation of variances along with the identification of possible causes and

recommendation for corrective actions......................................................................................16

4.2 Preparation of reconciliation operating statement...............................................................17

4.3 Management report in accordance with the identified responsibility centres.....................17

Conclusion.....................................................................................................................................18

References......................................................................................................................................19

2

INDEX OF TABLES

Table 1: Computation of cost of Job 444.........................................................................................5

Table 2: Computation of total cost of exquisite...............................................................................5

Table 3: Allocation of cost of support departments on the basis of machine hours........................6

Table 4: Allocation Criteria of cost.................................................................................................6

Table 5: Units to be produced.........................................................................................................6

Table 6: Statement showing computation of exquisite....................................................................7

Table 7: Statement showing computation of exquisite....................................................................7

Table 8: Routine cost report of September......................................................................................8

Table 9: Computation of standard budget at 1900 units..................................................................8

Table 10: Production budget of Jeffrey and Son's smake..............................................................13

Table 11: Material purchase budget of Jeffrey and Son's smake...................................................13

Table 12: Cash budget of Jeffrey and Son's...................................................................................13

Table 17: Computation of variances of Jeffrey and Son's smake..................................................16

Table 18: Reconciliation operating statement of Jeffrey and Son's smake...................................17

3

Table 1: Computation of cost of Job 444.........................................................................................5

Table 2: Computation of total cost of exquisite...............................................................................5

Table 3: Allocation of cost of support departments on the basis of machine hours........................6

Table 4: Allocation Criteria of cost.................................................................................................6

Table 5: Units to be produced.........................................................................................................6

Table 6: Statement showing computation of exquisite....................................................................7

Table 7: Statement showing computation of exquisite....................................................................7

Table 8: Routine cost report of September......................................................................................8

Table 9: Computation of standard budget at 1900 units..................................................................8

Table 10: Production budget of Jeffrey and Son's smake..............................................................13

Table 11: Material purchase budget of Jeffrey and Son's smake...................................................13

Table 12: Cash budget of Jeffrey and Son's...................................................................................13

Table 17: Computation of variances of Jeffrey and Son's smake..................................................16

Table 18: Reconciliation operating statement of Jeffrey and Son's smake...................................17

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is field of accounting which combines norms of costing and

budgeting. By making use of these techniques, organization can determine cost of their

production and operational activities in order to make viable decisions. For this aspect, they are

required to record their cost and expenses by making use of appropriate costing technique

(Banks, 2008). These techniques assist organization in making reduction in their costs in order to

enhance their profitability. Present study is based on the practical and theoretical description of

various costing techniques. For this aspect, different types of cost and budgets will be explained

along with its practical applicability in the given case scenario. In addition to this, cost report

will be prepared in order to analyse information of business and making viable decisions.

TASK 1

1.1 Different types of classification of cost

Cost can be termed as expense incurred by an organization for the completion of business

activities. Cost of business can be classified on the basis of following elements:

Elements- Element factor classifies cost into direct and indirect cost. Direct costs are

expenses incurred for the production activities of business. Example of direct cost is material,

labour, lighting and heating etc (Burns, Hopper and Yazdifar, 2004). Further, indirect cost is

incurred for smooth run of production activities. Example of indirect cost is lubricating oil, small

tools etc.

Function- Classification of cost can also be done on the basis of various functions and

activities. Common classification of costs are Administration, Distribution, Finance, Production,

Quality Check, Research and Development and selling.

Nature- On the basis of nature of expense, cost can be classified into material, labour and

overhead expenses (Zawawi and Hoque, 2010). Material expenses are incurred for the purchase

of raw material, labour expenses are made for the payment of wage rate to the human resources

and overhead expenses are related to the other costs of business organization.

Behaviour- By considering the behavior factor, cost can be classified into fixed, variable

and semi variable cost. Fixed costs are those expenses which does not fluctuate with the change

4

Management accounting is field of accounting which combines norms of costing and

budgeting. By making use of these techniques, organization can determine cost of their

production and operational activities in order to make viable decisions. For this aspect, they are

required to record their cost and expenses by making use of appropriate costing technique

(Banks, 2008). These techniques assist organization in making reduction in their costs in order to

enhance their profitability. Present study is based on the practical and theoretical description of

various costing techniques. For this aspect, different types of cost and budgets will be explained

along with its practical applicability in the given case scenario. In addition to this, cost report

will be prepared in order to analyse information of business and making viable decisions.

TASK 1

1.1 Different types of classification of cost

Cost can be termed as expense incurred by an organization for the completion of business

activities. Cost of business can be classified on the basis of following elements:

Elements- Element factor classifies cost into direct and indirect cost. Direct costs are

expenses incurred for the production activities of business. Example of direct cost is material,

labour, lighting and heating etc (Burns, Hopper and Yazdifar, 2004). Further, indirect cost is

incurred for smooth run of production activities. Example of indirect cost is lubricating oil, small

tools etc.

Function- Classification of cost can also be done on the basis of various functions and

activities. Common classification of costs are Administration, Distribution, Finance, Production,

Quality Check, Research and Development and selling.

Nature- On the basis of nature of expense, cost can be classified into material, labour and

overhead expenses (Zawawi and Hoque, 2010). Material expenses are incurred for the purchase

of raw material, labour expenses are made for the payment of wage rate to the human resources

and overhead expenses are related to the other costs of business organization.

Behaviour- By considering the behavior factor, cost can be classified into fixed, variable

and semi variable cost. Fixed costs are those expenses which does not fluctuate with the change

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

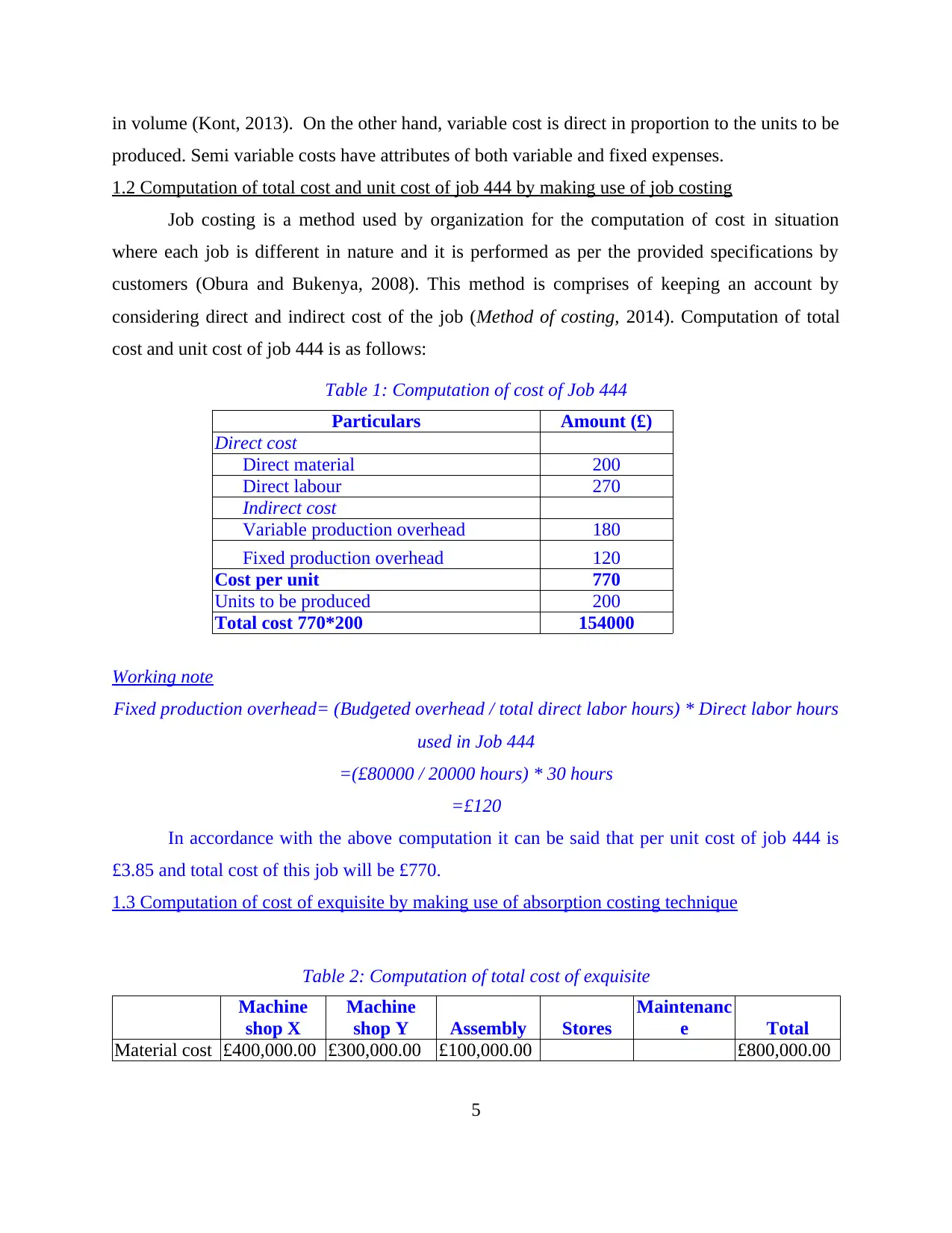

in volume (Kont, 2013). On the other hand, variable cost is direct in proportion to the units to be

produced. Semi variable costs have attributes of both variable and fixed expenses.

1.2 Computation of total cost and unit cost of job 444 by making use of job costing

Job costing is a method used by organization for the computation of cost in situation

where each job is different in nature and it is performed as per the provided specifications by

customers (Obura and Bukenya, 2008). This method is comprises of keeping an account by

considering direct and indirect cost of the job (Method of costing, 2014). Computation of total

cost and unit cost of job 444 is as follows:

Table 1: Computation of cost of Job 444

Particulars Amount (£)

Direct cost

Direct material 200

Direct labour 270

Indirect cost

Variable production overhead 180

Fixed production overhead 120

Cost per unit 770

Units to be produced 200

Total cost 770*200 154000

Working note

Fixed production overhead= (Budgeted overhead / total direct labor hours) * Direct labor hours

used in Job 444

=(£80000 / 20000 hours) * 30 hours

=£120

In accordance with the above computation it can be said that per unit cost of job 444 is

£3.85 and total cost of this job will be £770.

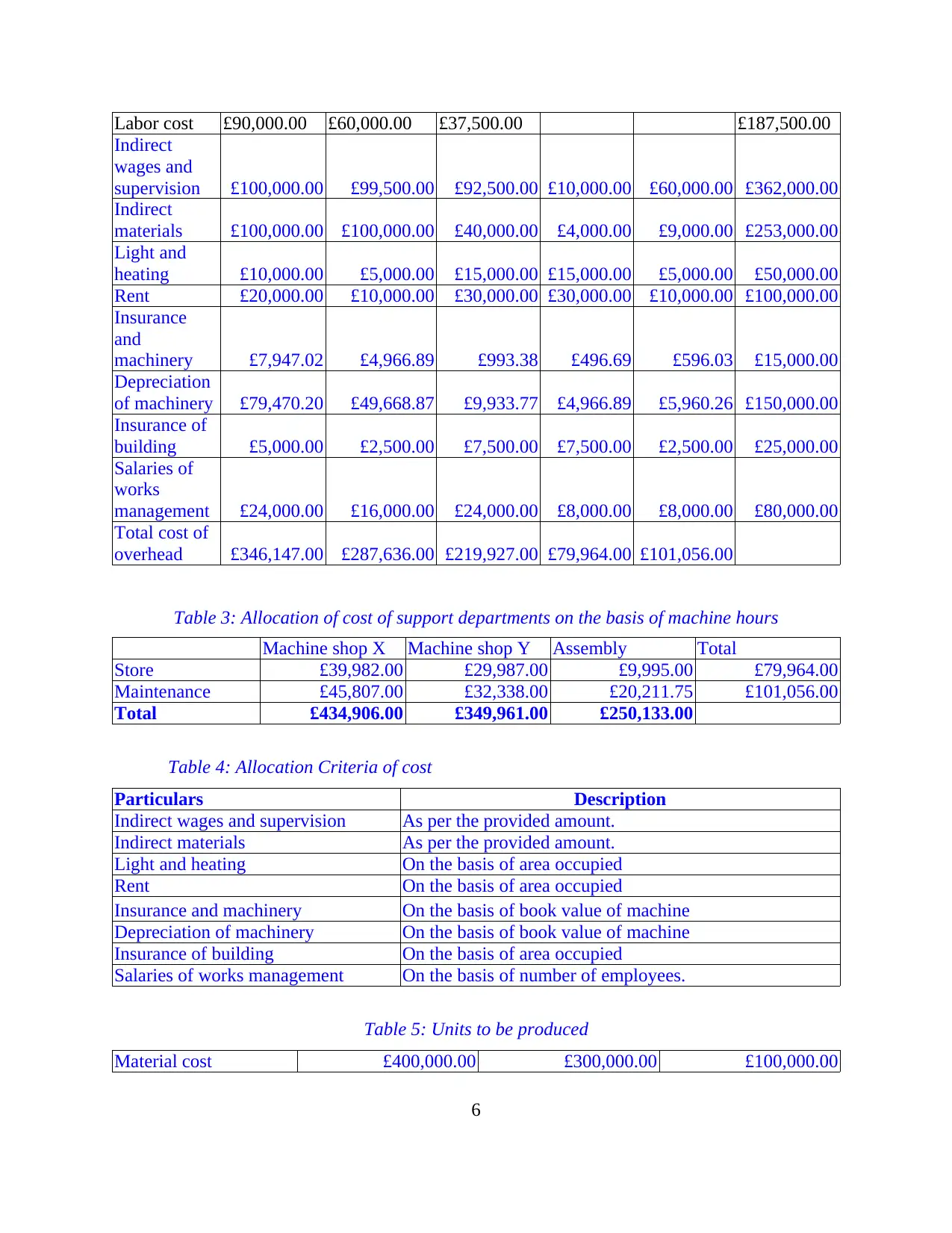

1.3 Computation of cost of exquisite by making use of absorption costing technique

Table 2: Computation of total cost of exquisite

Machine

shop X

Machine

shop Y Assembly Stores

Maintenanc

e Total

Material cost £400,000.00 £300,000.00 £100,000.00 £800,000.00

5

produced. Semi variable costs have attributes of both variable and fixed expenses.

1.2 Computation of total cost and unit cost of job 444 by making use of job costing

Job costing is a method used by organization for the computation of cost in situation

where each job is different in nature and it is performed as per the provided specifications by

customers (Obura and Bukenya, 2008). This method is comprises of keeping an account by

considering direct and indirect cost of the job (Method of costing, 2014). Computation of total

cost and unit cost of job 444 is as follows:

Table 1: Computation of cost of Job 444

Particulars Amount (£)

Direct cost

Direct material 200

Direct labour 270

Indirect cost

Variable production overhead 180

Fixed production overhead 120

Cost per unit 770

Units to be produced 200

Total cost 770*200 154000

Working note

Fixed production overhead= (Budgeted overhead / total direct labor hours) * Direct labor hours

used in Job 444

=(£80000 / 20000 hours) * 30 hours

=£120

In accordance with the above computation it can be said that per unit cost of job 444 is

£3.85 and total cost of this job will be £770.

1.3 Computation of cost of exquisite by making use of absorption costing technique

Table 2: Computation of total cost of exquisite

Machine

shop X

Machine

shop Y Assembly Stores

Maintenanc

e Total

Material cost £400,000.00 £300,000.00 £100,000.00 £800,000.00

5

Labor cost £90,000.00 £60,000.00 £37,500.00 £187,500.00

Indirect

wages and

supervision £100,000.00 £99,500.00 £92,500.00 £10,000.00 £60,000.00 £362,000.00

Indirect

materials £100,000.00 £100,000.00 £40,000.00 £4,000.00 £9,000.00 £253,000.00

Light and

heating £10,000.00 £5,000.00 £15,000.00 £15,000.00 £5,000.00 £50,000.00

Rent £20,000.00 £10,000.00 £30,000.00 £30,000.00 £10,000.00 £100,000.00

Insurance

and

machinery £7,947.02 £4,966.89 £993.38 £496.69 £596.03 £15,000.00

Depreciation

of machinery £79,470.20 £49,668.87 £9,933.77 £4,966.89 £5,960.26 £150,000.00

Insurance of

building £5,000.00 £2,500.00 £7,500.00 £7,500.00 £2,500.00 £25,000.00

Salaries of

works

management £24,000.00 £16,000.00 £24,000.00 £8,000.00 £8,000.00 £80,000.00

Total cost of

overhead £346,147.00 £287,636.00 £219,927.00 £79,964.00 £101,056.00

Table 3: Allocation of cost of support departments on the basis of machine hours

Machine shop X Machine shop Y Assembly Total

Store £39,982.00 £29,987.00 £9,995.00 £79,964.00

Maintenance £45,807.00 £32,338.00 £20,211.75 £101,056.00

Total £434,906.00 £349,961.00 £250,133.00

Table 4: Allocation Criteria of cost

Particulars Description

Indirect wages and supervision As per the provided amount.

Indirect materials As per the provided amount.

Light and heating On the basis of area occupied

Rent On the basis of area occupied

Insurance and machinery On the basis of book value of machine

Depreciation of machinery On the basis of book value of machine

Insurance of building On the basis of area occupied

Salaries of works management On the basis of number of employees.

Table 5: Units to be produced

Material cost £400,000.00 £300,000.00 £100,000.00

6

Indirect

wages and

supervision £100,000.00 £99,500.00 £92,500.00 £10,000.00 £60,000.00 £362,000.00

Indirect

materials £100,000.00 £100,000.00 £40,000.00 £4,000.00 £9,000.00 £253,000.00

Light and

heating £10,000.00 £5,000.00 £15,000.00 £15,000.00 £5,000.00 £50,000.00

Rent £20,000.00 £10,000.00 £30,000.00 £30,000.00 £10,000.00 £100,000.00

Insurance

and

machinery £7,947.02 £4,966.89 £993.38 £496.69 £596.03 £15,000.00

Depreciation

of machinery £79,470.20 £49,668.87 £9,933.77 £4,966.89 £5,960.26 £150,000.00

Insurance of

building £5,000.00 £2,500.00 £7,500.00 £7,500.00 £2,500.00 £25,000.00

Salaries of

works

management £24,000.00 £16,000.00 £24,000.00 £8,000.00 £8,000.00 £80,000.00

Total cost of

overhead £346,147.00 £287,636.00 £219,927.00 £79,964.00 £101,056.00

Table 3: Allocation of cost of support departments on the basis of machine hours

Machine shop X Machine shop Y Assembly Total

Store £39,982.00 £29,987.00 £9,995.00 £79,964.00

Maintenance £45,807.00 £32,338.00 £20,211.75 £101,056.00

Total £434,906.00 £349,961.00 £250,133.00

Table 4: Allocation Criteria of cost

Particulars Description

Indirect wages and supervision As per the provided amount.

Indirect materials As per the provided amount.

Light and heating On the basis of area occupied

Rent On the basis of area occupied

Insurance and machinery On the basis of book value of machine

Depreciation of machinery On the basis of book value of machine

Insurance of building On the basis of area occupied

Salaries of works management On the basis of number of employees.

Table 5: Units to be produced

Material cost £400,000.00 £300,000.00 £100,000.00

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

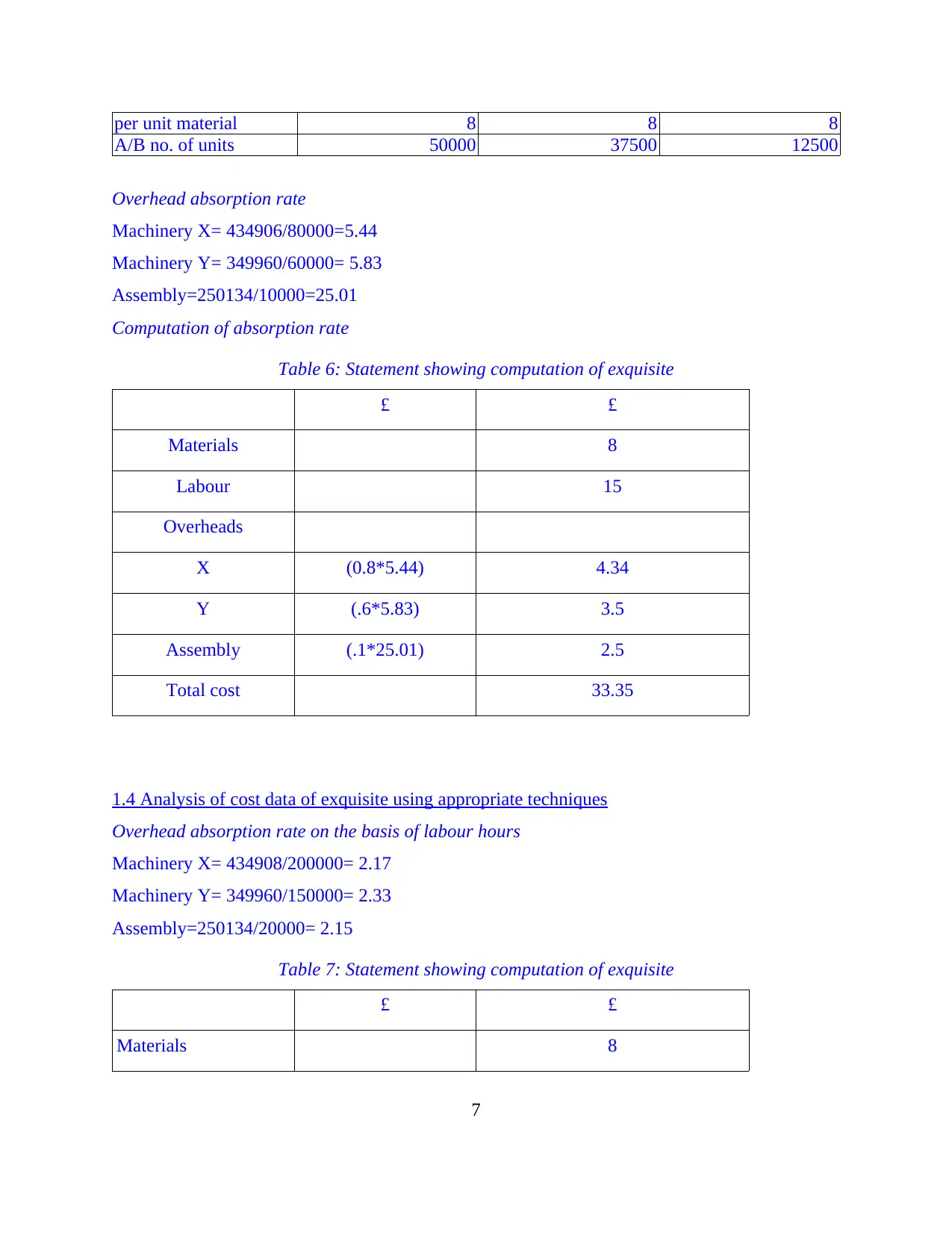

per unit material 8 8 8

A/B no. of units 50000 37500 12500

Overhead absorption rate

Machinery X= 434906/80000=5.44

Machinery Y= 349960/60000= 5.83

Assembly=250134/10000=25.01

Computation of absorption rate

Table 6: Statement showing computation of exquisite

£ £

Materials 8

Labour 15

Overheads

X (0.8*5.44) 4.34

Y (.6*5.83) 3.5

Assembly (.1*25.01) 2.5

Total cost 33.35

1.4 Analysis of cost data of exquisite using appropriate techniques

Overhead absorption rate on the basis of labour hours

Machinery X= 434908/200000= 2.17

Machinery Y= 349960/150000= 2.33

Assembly=250134/20000= 2.15

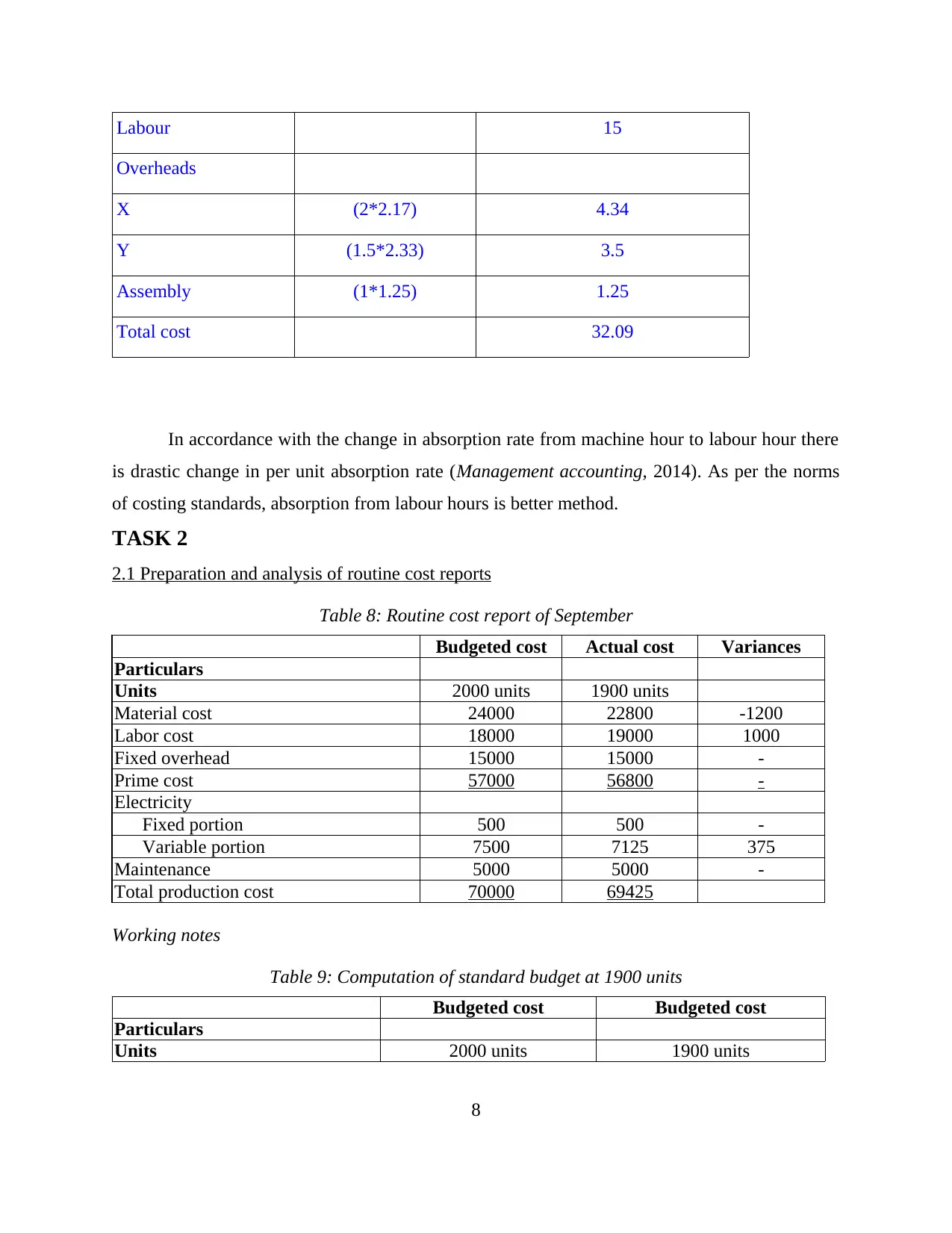

Table 7: Statement showing computation of exquisite

£ £

Materials 8

7

A/B no. of units 50000 37500 12500

Overhead absorption rate

Machinery X= 434906/80000=5.44

Machinery Y= 349960/60000= 5.83

Assembly=250134/10000=25.01

Computation of absorption rate

Table 6: Statement showing computation of exquisite

£ £

Materials 8

Labour 15

Overheads

X (0.8*5.44) 4.34

Y (.6*5.83) 3.5

Assembly (.1*25.01) 2.5

Total cost 33.35

1.4 Analysis of cost data of exquisite using appropriate techniques

Overhead absorption rate on the basis of labour hours

Machinery X= 434908/200000= 2.17

Machinery Y= 349960/150000= 2.33

Assembly=250134/20000= 2.15

Table 7: Statement showing computation of exquisite

£ £

Materials 8

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Labour 15

Overheads

X (2*2.17) 4.34

Y (1.5*2.33) 3.5

Assembly (1*1.25) 1.25

Total cost 32.09

In accordance with the change in absorption rate from machine hour to labour hour there

is drastic change in per unit absorption rate (Management accounting, 2014). As per the norms

of costing standards, absorption from labour hours is better method.

TASK 2

2.1 Preparation and analysis of routine cost reports

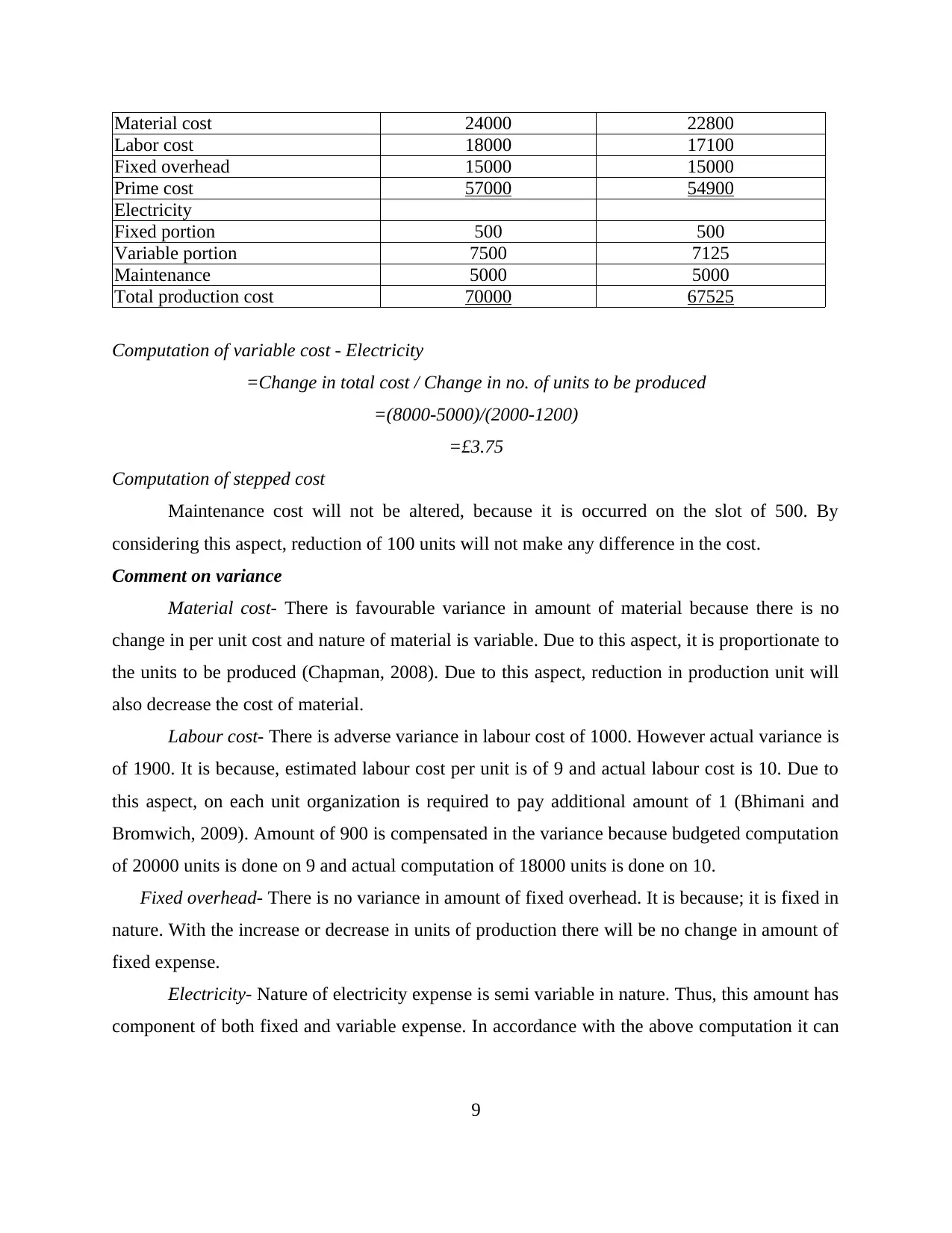

Table 8: Routine cost report of September

Budgeted cost Actual cost Variances

Particulars

Units 2000 units 1900 units

Material cost 24000 22800 -1200

Labor cost 18000 19000 1000

Fixed overhead 15000 15000 -

Prime cost 57000 56800 -

Electricity

Fixed portion 500 500 -

Variable portion 7500 7125 375

Maintenance 5000 5000 -

Total production cost 70000 69425

Working notes

Table 9: Computation of standard budget at 1900 units

Budgeted cost Budgeted cost

Particulars

Units 2000 units 1900 units

8

Overheads

X (2*2.17) 4.34

Y (1.5*2.33) 3.5

Assembly (1*1.25) 1.25

Total cost 32.09

In accordance with the change in absorption rate from machine hour to labour hour there

is drastic change in per unit absorption rate (Management accounting, 2014). As per the norms

of costing standards, absorption from labour hours is better method.

TASK 2

2.1 Preparation and analysis of routine cost reports

Table 8: Routine cost report of September

Budgeted cost Actual cost Variances

Particulars

Units 2000 units 1900 units

Material cost 24000 22800 -1200

Labor cost 18000 19000 1000

Fixed overhead 15000 15000 -

Prime cost 57000 56800 -

Electricity

Fixed portion 500 500 -

Variable portion 7500 7125 375

Maintenance 5000 5000 -

Total production cost 70000 69425

Working notes

Table 9: Computation of standard budget at 1900 units

Budgeted cost Budgeted cost

Particulars

Units 2000 units 1900 units

8

Material cost 24000 22800

Labor cost 18000 17100

Fixed overhead 15000 15000

Prime cost 57000 54900

Electricity

Fixed portion 500 500

Variable portion 7500 7125

Maintenance 5000 5000

Total production cost 70000 67525

Computation of variable cost - Electricity

=Change in total cost / Change in no. of units to be produced

=(8000-5000)/(2000-1200)

=£3.75

Computation of stepped cost

Maintenance cost will not be altered, because it is occurred on the slot of 500. By

considering this aspect, reduction of 100 units will not make any difference in the cost.

Comment on variance

Material cost- There is favourable variance in amount of material because there is no

change in per unit cost and nature of material is variable. Due to this aspect, it is proportionate to

the units to be produced (Chapman, 2008). Due to this aspect, reduction in production unit will

also decrease the cost of material.

Labour cost- There is adverse variance in labour cost of 1000. However actual variance is

of 1900. It is because, estimated labour cost per unit is of 9 and actual labour cost is 10. Due to

this aspect, on each unit organization is required to pay additional amount of 1 (Bhimani and

Bromwich, 2009). Amount of 900 is compensated in the variance because budgeted computation

of 20000 units is done on 9 and actual computation of 18000 units is done on 10.

Fixed overhead- There is no variance in amount of fixed overhead. It is because; it is fixed in

nature. With the increase or decrease in units of production there will be no change in amount of

fixed expense.

Electricity- Nature of electricity expense is semi variable in nature. Thus, this amount has

component of both fixed and variable expense. In accordance with the above computation it can

9

Labor cost 18000 17100

Fixed overhead 15000 15000

Prime cost 57000 54900

Electricity

Fixed portion 500 500

Variable portion 7500 7125

Maintenance 5000 5000

Total production cost 70000 67525

Computation of variable cost - Electricity

=Change in total cost / Change in no. of units to be produced

=(8000-5000)/(2000-1200)

=£3.75

Computation of stepped cost

Maintenance cost will not be altered, because it is occurred on the slot of 500. By

considering this aspect, reduction of 100 units will not make any difference in the cost.

Comment on variance

Material cost- There is favourable variance in amount of material because there is no

change in per unit cost and nature of material is variable. Due to this aspect, it is proportionate to

the units to be produced (Chapman, 2008). Due to this aspect, reduction in production unit will

also decrease the cost of material.

Labour cost- There is adverse variance in labour cost of 1000. However actual variance is

of 1900. It is because, estimated labour cost per unit is of 9 and actual labour cost is 10. Due to

this aspect, on each unit organization is required to pay additional amount of 1 (Bhimani and

Bromwich, 2009). Amount of 900 is compensated in the variance because budgeted computation

of 20000 units is done on 9 and actual computation of 18000 units is done on 10.

Fixed overhead- There is no variance in amount of fixed overhead. It is because; it is fixed in

nature. With the increase or decrease in units of production there will be no change in amount of

fixed expense.

Electricity- Nature of electricity expense is semi variable in nature. Thus, this amount has

component of both fixed and variable expense. In accordance with the above computation it can

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

be noticed that there is no change in fixed portion (Lucey, 2002). Further, amount of variable

portion is decreased proportionately.

Maintenance- Maintenance charges are stepped cost. It increased with the increase in slot

of 500. By considering this aspect, there will not be any change in amount of maintenance cost.

It is because; reduction of 100 units will not make any difference in the cost.

2.2 Use of performance indicators in order to identify potential improvements in business

By making use of enumerated performance indicators management of Jeffrey and Son's smake

can identify scope of potential improvement in their business-

Financial statements- Through analysis of this statement, change in financial position

can be noticed by management of Jeffrey and Son's smake. In situation where there is decrease in

amount of sales and profitability or increase in amount of cost then organization is required to

make changes in their operational strategies (Keown, 2005). These statements will provide

description of change in all financial values in an accounting year. By considering this

information, organization can identify the areas where there is increase in the amount of cost.

Quality of product and services- By the assessment of quality of product and services

areas of improvement can be identified (Key Performance Indicators, 2014). This aspect can be

done by monitoring of operational activities in business. This assessment will provide

information of loopholes in operating performance due to which quality of the product is

adversely affected.

Customer satisfaction- Further, potential improvement can be identified through

considering reviews of the customers (Jiambalvo, 2001). By considering their feedback and

complaints, management of Jeffrey and Son's smake can make improvement in their production

process in order to enhance their level of satisfaction.

2.3 Recommendation for cost reduction and value enhancement for business

By making use of following techniques, management of Jeffrey and Son's smake can achieve

their objective of cost reduction and value enhancement for business-

Just in time system and economic order quantity- By making use of these techniques,

organization can make reduction in their storage and carrying cost. As per this approach,

management of Jeffrey and Son's smake will purchase raw material as per the demand in the

10

portion is decreased proportionately.

Maintenance- Maintenance charges are stepped cost. It increased with the increase in slot

of 500. By considering this aspect, there will not be any change in amount of maintenance cost.

It is because; reduction of 100 units will not make any difference in the cost.

2.2 Use of performance indicators in order to identify potential improvements in business

By making use of enumerated performance indicators management of Jeffrey and Son's smake

can identify scope of potential improvement in their business-

Financial statements- Through analysis of this statement, change in financial position

can be noticed by management of Jeffrey and Son's smake. In situation where there is decrease in

amount of sales and profitability or increase in amount of cost then organization is required to

make changes in their operational strategies (Keown, 2005). These statements will provide

description of change in all financial values in an accounting year. By considering this

information, organization can identify the areas where there is increase in the amount of cost.

Quality of product and services- By the assessment of quality of product and services

areas of improvement can be identified (Key Performance Indicators, 2014). This aspect can be

done by monitoring of operational activities in business. This assessment will provide

information of loopholes in operating performance due to which quality of the product is

adversely affected.

Customer satisfaction- Further, potential improvement can be identified through

considering reviews of the customers (Jiambalvo, 2001). By considering their feedback and

complaints, management of Jeffrey and Son's smake can make improvement in their production

process in order to enhance their level of satisfaction.

2.3 Recommendation for cost reduction and value enhancement for business

By making use of following techniques, management of Jeffrey and Son's smake can achieve

their objective of cost reduction and value enhancement for business-

Just in time system and economic order quantity- By making use of these techniques,

organization can make reduction in their storage and carrying cost. As per this approach,

management of Jeffrey and Son's smake will purchase raw material as per the demand in the

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

market. With this applicability of this approach, there is reduction in the unwanted inventory of

business.

Total quality management- This tool makes qualitative improvement in the operational

activities of business. Total quality management approach is based on the improvement in

overall production process by resolving loop holes (Vanderbeck, 2012). By this implementation

of this approach, organization can enhance the productivity and quality of production in order to

satisfy needs of customers in an effective manner.

Kaizen costing- Similar to the TQM approach, Kaizen costing is also mainly focused on

making continuous betterment in the overall functioning of the business organization. This

technique motivate employees to accomplish operational tasks with the perfection (Vance,

2002). With this motive, it makes drastic reduction in the wastage by making prevention of

enumerated aspects- Decrements in valuation because of high waiting time, Inappropriate

allocation of human resources, Production more than requirement, Increase in faulty production

units, Holding high inventory, Non-economical processing for value addition and Poor strategies

for transportation

Management audits- Through this technique, organization can monitor the performance

of employees in order to assure standard outcome. Management audits in timely manner will

influence employees to provide standard performance in order to attain quality remark. For this

aspect, management of Jeffrey and Son's smake can also make provision of surprise audit in their

business strategies.

TASK 3

3.1 Explanation of purpose and nature of the budgeting process

Purpose of budgeting process

Budgets can be defined as statements prepared for the forecasting of future operational

activities. Main objective of budgeting process is make estimation of future expenses and

revenue, in order to allocate resources in an optimum manner (Vaivio, 2008). With these

statements, profit of business is determined. On the basis of these statements, decisions are made

by managerial persons. In addition to this, budgeting helps in making comparison of actual

performance with the standard performance.

Nature of budgeting process

11

business.

Total quality management- This tool makes qualitative improvement in the operational

activities of business. Total quality management approach is based on the improvement in

overall production process by resolving loop holes (Vanderbeck, 2012). By this implementation

of this approach, organization can enhance the productivity and quality of production in order to

satisfy needs of customers in an effective manner.

Kaizen costing- Similar to the TQM approach, Kaizen costing is also mainly focused on

making continuous betterment in the overall functioning of the business organization. This

technique motivate employees to accomplish operational tasks with the perfection (Vance,

2002). With this motive, it makes drastic reduction in the wastage by making prevention of

enumerated aspects- Decrements in valuation because of high waiting time, Inappropriate

allocation of human resources, Production more than requirement, Increase in faulty production

units, Holding high inventory, Non-economical processing for value addition and Poor strategies

for transportation

Management audits- Through this technique, organization can monitor the performance

of employees in order to assure standard outcome. Management audits in timely manner will

influence employees to provide standard performance in order to attain quality remark. For this

aspect, management of Jeffrey and Son's smake can also make provision of surprise audit in their

business strategies.

TASK 3

3.1 Explanation of purpose and nature of the budgeting process

Purpose of budgeting process

Budgets can be defined as statements prepared for the forecasting of future operational

activities. Main objective of budgeting process is make estimation of future expenses and

revenue, in order to allocate resources in an optimum manner (Vaivio, 2008). With these

statements, profit of business is determined. On the basis of these statements, decisions are made

by managerial persons. In addition to this, budgeting helps in making comparison of actual

performance with the standard performance.

Nature of budgeting process

11

Estimation in budgetary statements is made in accordance with the actual values of last

accounting period. With this estimation, computation of possible amount of cash is done from

the sales and other activities of business. For this aspect, various expenses such as material,

labour and production expenses (Statements on Management Accounting, 2015). Amount of

expenditure is deducted from the estimated amount of profits in order to determine proposes

deficit or surplus from operating activities. This budget is reviewed by senior manager and it is

submitted to the board of directors for practical applicability.

3.2 Selection of appropriate budgeting methods in accordance with the needs of organization

Preparation of budgets can be done by various methods in accordance with the needs and

requirements of the commercial entity. Description of various budgeting methods is enumerated

below:

Operational budgets- In this method, budgets are prepared by considering separate

operational activities of business such as production, selling and distribution etc (Vanderbeck,

2012). These budgets are prepared on periodical basis that can be annual, monthly or quarterly.

On the basis of these budgets, strategies are implemented by business organization.

Zero based budgeting- This method of budget is selected in situation where there is previous

base for preparation of budget. This situation is arises mainly when there is drastic change in

market situations or there is development of new product (Vance, 2002). In this method, there

are no measures of forecasted thus there is high possibility of variances.

Incremental budgeting- This method is selected for the computation of budget in situation

when there are minor changes in environment. This the traditional technique for budgeting

because in this method budgets are prepared by considering previous financial information.

In accordance with the above description, most suitable method of preparation of budget

for Jeffrey and Son's smake is operational budgeting. It is because, in this technique different

statements are prepared for forecasting by considering operating activities of business.

3.3 Preparation of production and material purchase budget

12

accounting period. With this estimation, computation of possible amount of cash is done from

the sales and other activities of business. For this aspect, various expenses such as material,

labour and production expenses (Statements on Management Accounting, 2015). Amount of

expenditure is deducted from the estimated amount of profits in order to determine proposes

deficit or surplus from operating activities. This budget is reviewed by senior manager and it is

submitted to the board of directors for practical applicability.

3.2 Selection of appropriate budgeting methods in accordance with the needs of organization

Preparation of budgets can be done by various methods in accordance with the needs and

requirements of the commercial entity. Description of various budgeting methods is enumerated

below:

Operational budgets- In this method, budgets are prepared by considering separate

operational activities of business such as production, selling and distribution etc (Vanderbeck,

2012). These budgets are prepared on periodical basis that can be annual, monthly or quarterly.

On the basis of these budgets, strategies are implemented by business organization.

Zero based budgeting- This method of budget is selected in situation where there is previous

base for preparation of budget. This situation is arises mainly when there is drastic change in

market situations or there is development of new product (Vance, 2002). In this method, there

are no measures of forecasted thus there is high possibility of variances.

Incremental budgeting- This method is selected for the computation of budget in situation

when there are minor changes in environment. This the traditional technique for budgeting

because in this method budgets are prepared by considering previous financial information.

In accordance with the above description, most suitable method of preparation of budget

for Jeffrey and Son's smake is operational budgeting. It is because, in this technique different

statements are prepared for forecasting by considering operating activities of business.

3.3 Preparation of production and material purchase budget

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.