Comprehensive Report: Management Accounting Costing and Budgeting

VerifiedAdded on 2019/12/04

|18

|5191

|40

Report

AI Summary

This report delves into the core aspects of management accounting, focusing on costing and budgeting techniques within the context of a food service company, Waitrose. The report begins by classifying different types of costs based on their nature, behavior, and elements. It then explores various costing methods, including job, unit, and absorption costing, and demonstrates how to calculate costs using appropriate techniques. The report also covers the preparation and analysis of routine cost reports, the use of performance indicators to identify potential improvements, and suggestions for cost reduction and value enhancement. Furthermore, it examines the purpose and nature of the budgeting process, selecting suitable budgeting methods, preparing budgets (including a cash budget), and calculating and analyzing variances to propose corrective actions. Finally, the report provides a reconciliation of the operating statement and reporting findings to management.

Management Accounting: Costing and

Budgeting

Budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

1.1 Classifying different types of cost.........................................................................................4

1.2 Using different costing methods............................................................................................5

1.3 Calculating costs using appropriate techniques.....................................................................6

1.4 Analysing costs data using appropriate techniques...............................................................8

2.1 Preparing and analysing routine cost reports.........................................................................8

2.2 Using performance indicators to identify potential improvement.........................................9

2.3 Suggesting improvements to reduce cost, enhance value and quality.................................10

TASK 2..........................................................................................................................................11

3.1 Purpose and nature of budgeting process.............................................................................11

3.2 Selecting appropriate budgeting methods for organization and its needs............................11

3.3 Preparing budgets according to the chosen budgeting method............................................12

3.4 Preparing cash budget..........................................................................................................13

4.1 Calculating variances, its causes and corrective actions......................................................14

4.2 Preparing a reconcile operating statement..........................................................................15

4.3 Reporting of findings to the management with identified responsibility centres...............16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

2

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

1.1 Classifying different types of cost.........................................................................................4

1.2 Using different costing methods............................................................................................5

1.3 Calculating costs using appropriate techniques.....................................................................6

1.4 Analysing costs data using appropriate techniques...............................................................8

2.1 Preparing and analysing routine cost reports.........................................................................8

2.2 Using performance indicators to identify potential improvement.........................................9

2.3 Suggesting improvements to reduce cost, enhance value and quality.................................10

TASK 2..........................................................................................................................................11

3.1 Purpose and nature of budgeting process.............................................................................11

3.2 Selecting appropriate budgeting methods for organization and its needs............................11

3.3 Preparing budgets according to the chosen budgeting method............................................12

3.4 Preparing cash budget..........................................................................................................13

4.1 Calculating variances, its causes and corrective actions......................................................14

4.2 Preparing a reconcile operating statement..........................................................................15

4.3 Reporting of findings to the management with identified responsibility centres...............16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

2

INDEX OF TABLES

Table 1: Job cost..............................................................................................................................5

Table 2: Unit cost.............................................................................................................................5

Table 3: Absorption cost..................................................................................................................6

Table 4: OAR...................................................................................................................................7

Table 5: Costing basis of labour hour..............................................................................................8

Table 6: Cost data............................................................................................................................8

Table 7: Variances...........................................................................................................................9

Table 8: Production budget............................................................................................................12

Table 9: Material usage budget......................................................................................................13

Table 10: Cash budget...................................................................................................................13

Table 11: Variances analysis.........................................................................................................14

Table 12: Reconcile operating statement.......................................................................................15

3

Table 1: Job cost..............................................................................................................................5

Table 2: Unit cost.............................................................................................................................5

Table 3: Absorption cost..................................................................................................................6

Table 4: OAR...................................................................................................................................7

Table 5: Costing basis of labour hour..............................................................................................8

Table 6: Cost data............................................................................................................................8

Table 7: Variances...........................................................................................................................9

Table 8: Production budget............................................................................................................12

Table 9: Material usage budget......................................................................................................13

Table 10: Cash budget...................................................................................................................13

Table 11: Variances analysis.........................................................................................................14

Table 12: Reconcile operating statement.......................................................................................15

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the most imperative aspect of business as it facilities control

in the organization with the help of budgeting and costing techniques. Several aspects are

associated with management accounting such as budgetary control, interim reporting and

taxation as well as office services. Present report is based on Waitrose that deals in food services

in the supermarket along with online shopping. It is the sixth largest grocery retailer in the UK

which caters the need of large number of buyers. Furthermore, report covers different types of

cost and its methods for calculating appropriate selling price for the products and services.

Similarly, use of performance indicators for potential improvements in corporation has also been

explained. Apart from this, purpose and nature of budgeting process have also been described.

TASK 1

1.1 Classifying different types of cost

There are different types of cost which are based on the nature, behaviour and elements

of business. It affects sales price of products and services (Costing methods, 2015). These are as

follows-

On the basis of nature

According to the nature of business, cost is classified into different aspects like material,

labour and overhead. Here, raw material of food products depends upon the volume of

production (Bellah and et. al., 2013). On the other hand, labour cost is based on the productivity

of corporation. In addition to this, overhead consists of the costs such as fuel, water etc. used for

producing products.

On the basis of behaviour

In accordance with the behaviour, cost is segregated into different parts such as fixed,

variable and semi-variable. Fixed remains constant throughout the production cycle and does not

fluctuate as per the volume of output (Bonazzi and Iotti, 2014). However, variable cost tends to

change as per the output's volume. In addition to this, semi-variable cost is partly fixed and

partly variable. For this, the most effective example can be quoted of Telephone expenses. Here,

Waitrose needs to pay fixed amount of bill for phone expenses whether that is in use or not.

On the basis of element

4

Management accounting is the most imperative aspect of business as it facilities control

in the organization with the help of budgeting and costing techniques. Several aspects are

associated with management accounting such as budgetary control, interim reporting and

taxation as well as office services. Present report is based on Waitrose that deals in food services

in the supermarket along with online shopping. It is the sixth largest grocery retailer in the UK

which caters the need of large number of buyers. Furthermore, report covers different types of

cost and its methods for calculating appropriate selling price for the products and services.

Similarly, use of performance indicators for potential improvements in corporation has also been

explained. Apart from this, purpose and nature of budgeting process have also been described.

TASK 1

1.1 Classifying different types of cost

There are different types of cost which are based on the nature, behaviour and elements

of business. It affects sales price of products and services (Costing methods, 2015). These are as

follows-

On the basis of nature

According to the nature of business, cost is classified into different aspects like material,

labour and overhead. Here, raw material of food products depends upon the volume of

production (Bellah and et. al., 2013). On the other hand, labour cost is based on the productivity

of corporation. In addition to this, overhead consists of the costs such as fuel, water etc. used for

producing products.

On the basis of behaviour

In accordance with the behaviour, cost is segregated into different parts such as fixed,

variable and semi-variable. Fixed remains constant throughout the production cycle and does not

fluctuate as per the volume of output (Bonazzi and Iotti, 2014). However, variable cost tends to

change as per the output's volume. In addition to this, semi-variable cost is partly fixed and

partly variable. For this, the most effective example can be quoted of Telephone expenses. Here,

Waitrose needs to pay fixed amount of bill for phone expenses whether that is in use or not.

On the basis of element

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

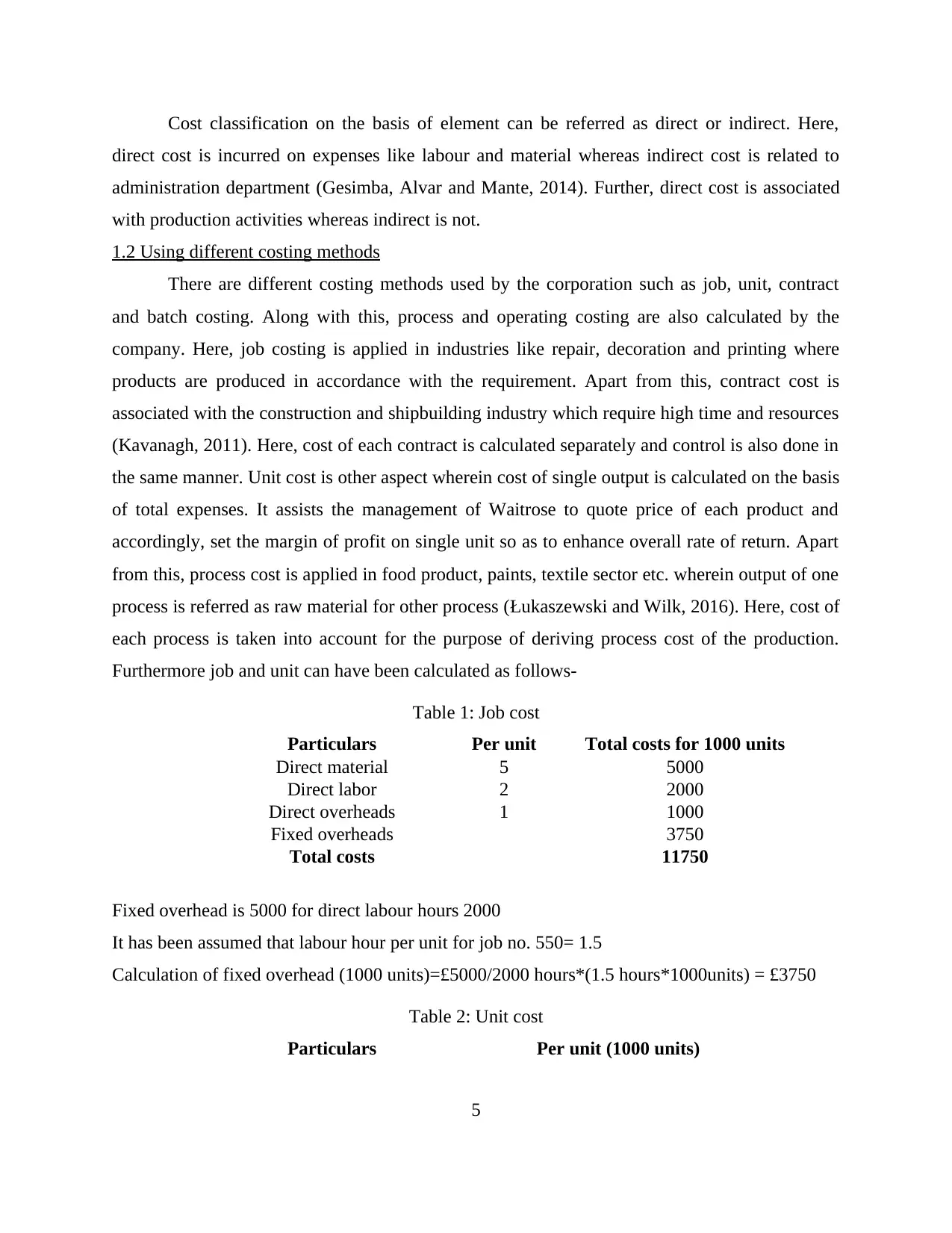

Cost classification on the basis of element can be referred as direct or indirect. Here,

direct cost is incurred on expenses like labour and material whereas indirect cost is related to

administration department (Gesimba, Alvar and Mante, 2014). Further, direct cost is associated

with production activities whereas indirect is not.

1.2 Using different costing methods

There are different costing methods used by the corporation such as job, unit, contract

and batch costing. Along with this, process and operating costing are also calculated by the

company. Here, job costing is applied in industries like repair, decoration and printing where

products are produced in accordance with the requirement. Apart from this, contract cost is

associated with the construction and shipbuilding industry which require high time and resources

(Kavanagh, 2011). Here, cost of each contract is calculated separately and control is also done in

the same manner. Unit cost is other aspect wherein cost of single output is calculated on the basis

of total expenses. It assists the management of Waitrose to quote price of each product and

accordingly, set the margin of profit on single unit so as to enhance overall rate of return. Apart

from this, process cost is applied in food product, paints, textile sector etc. wherein output of one

process is referred as raw material for other process (Łukaszewski and Wilk, 2016). Here, cost of

each process is taken into account for the purpose of deriving process cost of the production.

Furthermore job and unit can have been calculated as follows-

Table 1: Job cost

Particulars Per unit Total costs for 1000 units

Direct material 5 5000

Direct labor 2 2000

Direct overheads 1 1000

Fixed overheads 3750

Total costs 11750

Fixed overhead is 5000 for direct labour hours 2000

It has been assumed that labour hour per unit for job no. 550= 1.5

Calculation of fixed overhead (1000 units)=£5000/2000 hours*(1.5 hours*1000units) = £3750

Table 2: Unit cost

Particulars Per unit (1000 units)

5

direct cost is incurred on expenses like labour and material whereas indirect cost is related to

administration department (Gesimba, Alvar and Mante, 2014). Further, direct cost is associated

with production activities whereas indirect is not.

1.2 Using different costing methods

There are different costing methods used by the corporation such as job, unit, contract

and batch costing. Along with this, process and operating costing are also calculated by the

company. Here, job costing is applied in industries like repair, decoration and printing where

products are produced in accordance with the requirement. Apart from this, contract cost is

associated with the construction and shipbuilding industry which require high time and resources

(Kavanagh, 2011). Here, cost of each contract is calculated separately and control is also done in

the same manner. Unit cost is other aspect wherein cost of single output is calculated on the basis

of total expenses. It assists the management of Waitrose to quote price of each product and

accordingly, set the margin of profit on single unit so as to enhance overall rate of return. Apart

from this, process cost is applied in food product, paints, textile sector etc. wherein output of one

process is referred as raw material for other process (Łukaszewski and Wilk, 2016). Here, cost of

each process is taken into account for the purpose of deriving process cost of the production.

Furthermore job and unit can have been calculated as follows-

Table 1: Job cost

Particulars Per unit Total costs for 1000 units

Direct material 5 5000

Direct labor 2 2000

Direct overheads 1 1000

Fixed overheads 3750

Total costs 11750

Fixed overhead is 5000 for direct labour hours 2000

It has been assumed that labour hour per unit for job no. 550= 1.5

Calculation of fixed overhead (1000 units)=£5000/2000 hours*(1.5 hours*1000units) = £3750

Table 2: Unit cost

Particulars Per unit (1000 units)

5

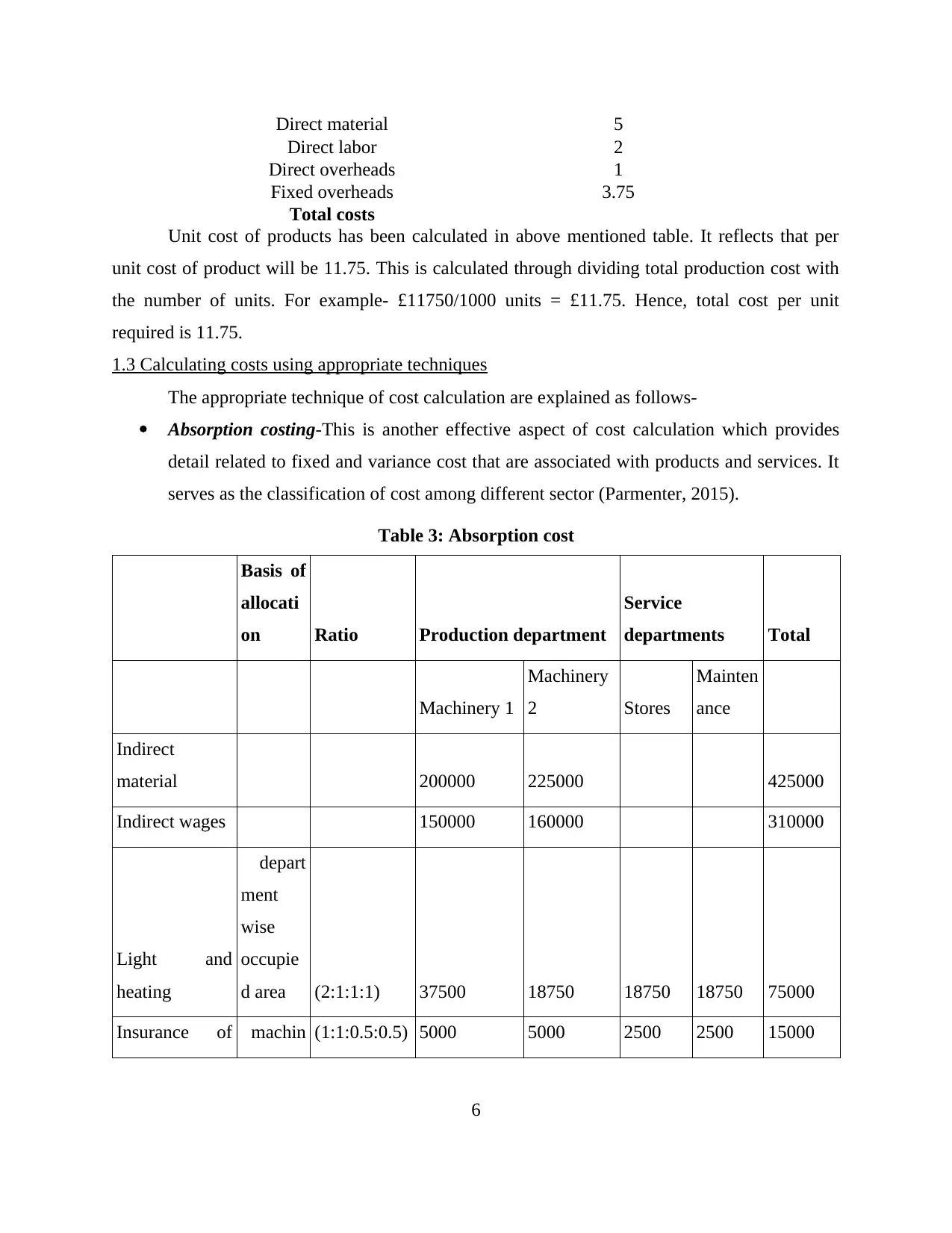

Direct material 5

Direct labor 2

Direct overheads 1

Fixed overheads 3.75

Total costs

Unit cost of products has been calculated in above mentioned table. It reflects that per

unit cost of product will be 11.75. This is calculated through dividing total production cost with

the number of units. For example- £11750/1000 units = £11.75. Hence, total cost per unit

required is 11.75.

1.3 Calculating costs using appropriate techniques

The appropriate technique of cost calculation are explained as follows-

Absorption costing-This is another effective aspect of cost calculation which provides

detail related to fixed and variance cost that are associated with products and services. It

serves as the classification of cost among different sector (Parmenter, 2015).

Table 3: Absorption cost

Basis of

allocati

on Ratio Production department

Service

departments Total

Machinery 1

Machinery

2 Stores

Mainten

ance

Indirect

material 200000 225000 425000

Indirect wages 150000 160000 310000

Light and

heating

depart

ment

wise

occupie

d area (2:1:1:1) 37500 18750 18750 18750 75000

Insurance of machin (1:1:0.5:0.5) 5000 5000 2500 2500 15000

6

Direct labor 2

Direct overheads 1

Fixed overheads 3.75

Total costs

Unit cost of products has been calculated in above mentioned table. It reflects that per

unit cost of product will be 11.75. This is calculated through dividing total production cost with

the number of units. For example- £11750/1000 units = £11.75. Hence, total cost per unit

required is 11.75.

1.3 Calculating costs using appropriate techniques

The appropriate technique of cost calculation are explained as follows-

Absorption costing-This is another effective aspect of cost calculation which provides

detail related to fixed and variance cost that are associated with products and services. It

serves as the classification of cost among different sector (Parmenter, 2015).

Table 3: Absorption cost

Basis of

allocati

on Ratio Production department

Service

departments Total

Machinery 1

Machinery

2 Stores

Mainten

ance

Indirect

material 200000 225000 425000

Indirect wages 150000 160000 310000

Light and

heating

depart

ment

wise

occupie

d area (2:1:1:1) 37500 18750 18750 18750 75000

Insurance of machin (1:1:0.5:0.5) 5000 5000 2500 2500 15000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

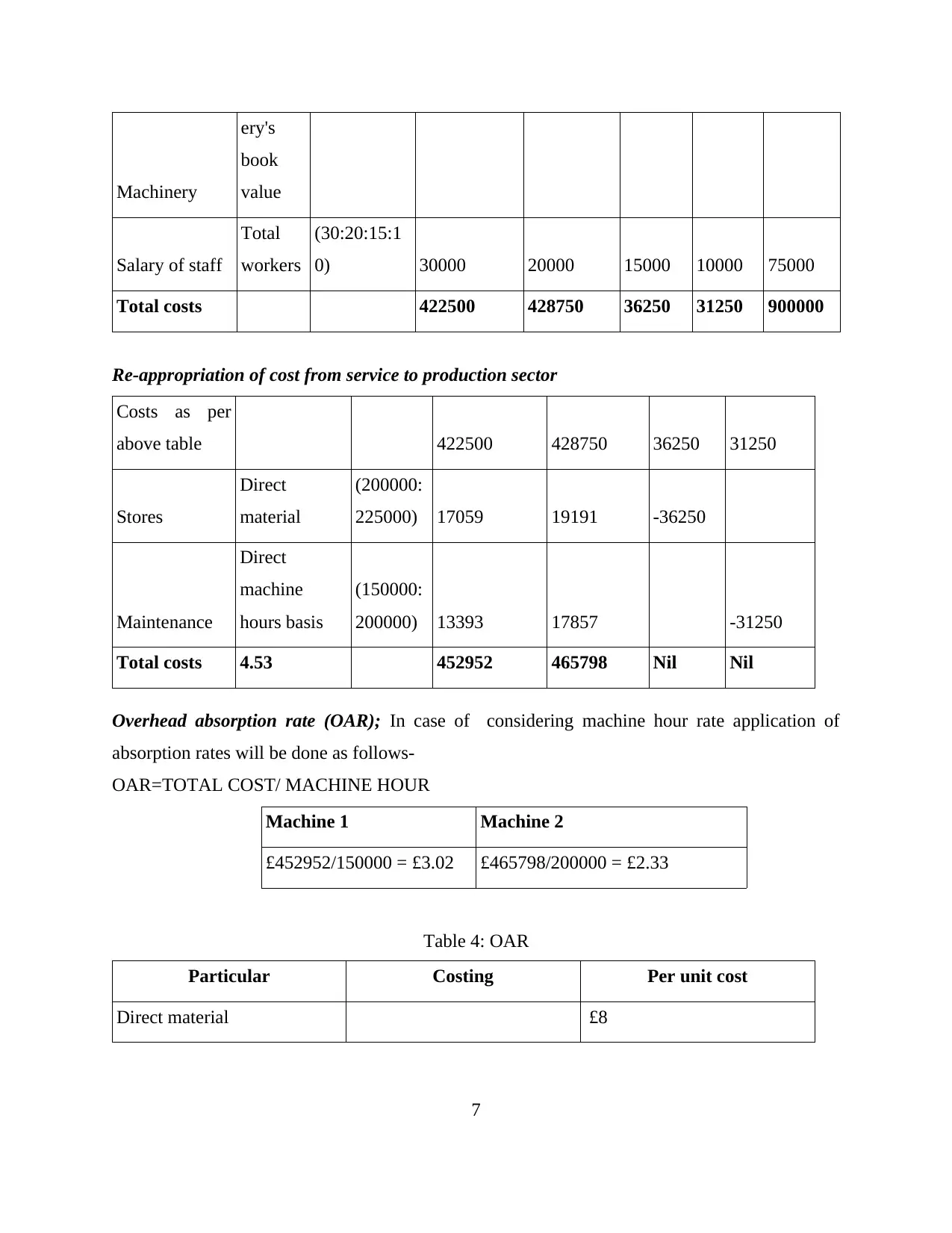

Machinery

ery's

book

value

Salary of staff

Total

workers

(30:20:15:1

0) 30000 20000 15000 10000 75000

Total costs 422500 428750 36250 31250 900000

Re-appropriation of cost from service to production sector

Costs as per

above table 422500 428750 36250 31250

Stores

Direct

material

(200000:

225000) 17059 19191 -36250

Maintenance

Direct

machine

hours basis

(150000:

200000) 13393 17857 -31250

Total costs 4.53 452952 465798 Nil Nil

Overhead absorption rate (OAR); In case of considering machine hour rate application of

absorption rates will be done as follows-

OAR=TOTAL COST/ MACHINE HOUR

Machine 1 Machine 2

£452952/150000 = £3.02 £465798/200000 = £2.33

Table 4: OAR

Particular Costing Per unit cost

Direct material £8

7

ery's

book

value

Salary of staff

Total

workers

(30:20:15:1

0) 30000 20000 15000 10000 75000

Total costs 422500 428750 36250 31250 900000

Re-appropriation of cost from service to production sector

Costs as per

above table 422500 428750 36250 31250

Stores

Direct

material

(200000:

225000) 17059 19191 -36250

Maintenance

Direct

machine

hours basis

(150000:

200000) 13393 17857 -31250

Total costs 4.53 452952 465798 Nil Nil

Overhead absorption rate (OAR); In case of considering machine hour rate application of

absorption rates will be done as follows-

OAR=TOTAL COST/ MACHINE HOUR

Machine 1 Machine 2

£452952/150000 = £3.02 £465798/200000 = £2.33

Table 4: OAR

Particular Costing Per unit cost

Direct material £8

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

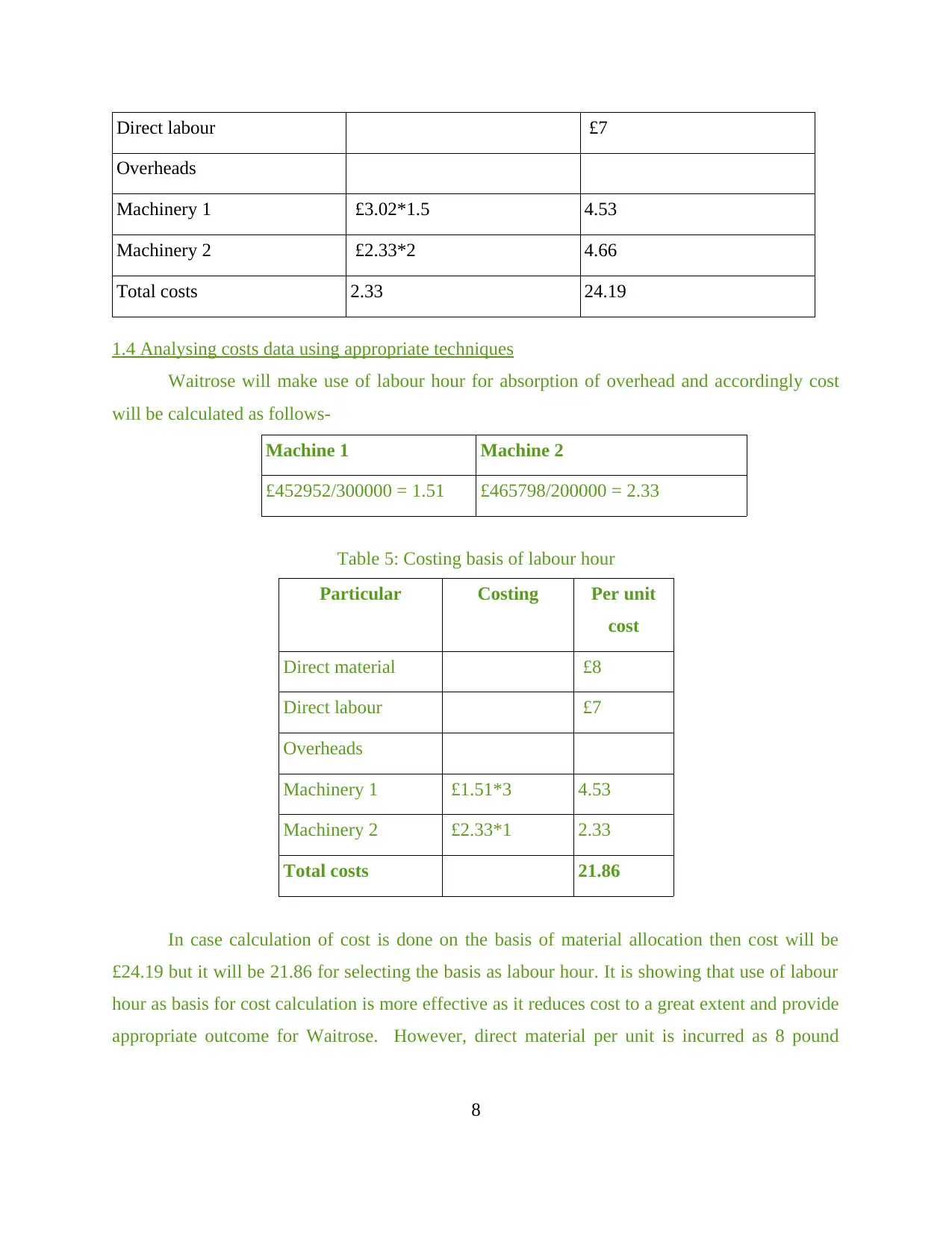

Direct labour £7

Overheads

Machinery 1 £3.02*1.5 4.53

Machinery 2 £2.33*2 4.66

Total costs 2.33 24.19

1.4 Analysing costs data using appropriate techniques

Waitrose will make use of labour hour for absorption of overhead and accordingly cost

will be calculated as follows-

Machine 1 Machine 2

£452952/300000 = 1.51 £465798/200000 = 2.33

Table 5: Costing basis of labour hour

Particular Costing Per unit

cost

Direct material £8

Direct labour £7

Overheads

Machinery 1 £1.51*3 4.53

Machinery 2 £2.33*1 2.33

Total costs 21.86

In case calculation of cost is done on the basis of material allocation then cost will be

£24.19 but it will be 21.86 for selecting the basis as labour hour. It is showing that use of labour

hour as basis for cost calculation is more effective as it reduces cost to a great extent and provide

appropriate outcome for Waitrose. However, direct material per unit is incurred as 8 pound

8

Overheads

Machinery 1 £3.02*1.5 4.53

Machinery 2 £2.33*2 4.66

Total costs 2.33 24.19

1.4 Analysing costs data using appropriate techniques

Waitrose will make use of labour hour for absorption of overhead and accordingly cost

will be calculated as follows-

Machine 1 Machine 2

£452952/300000 = 1.51 £465798/200000 = 2.33

Table 5: Costing basis of labour hour

Particular Costing Per unit

cost

Direct material £8

Direct labour £7

Overheads

Machinery 1 £1.51*3 4.53

Machinery 2 £2.33*1 2.33

Total costs 21.86

In case calculation of cost is done on the basis of material allocation then cost will be

£24.19 but it will be 21.86 for selecting the basis as labour hour. It is showing that use of labour

hour as basis for cost calculation is more effective as it reduces cost to a great extent and provide

appropriate outcome for Waitrose. However, direct material per unit is incurred as 8 pound

8

where as direct labour was 7. It serves as the direct or indirect cost which can be varied in

accordance with volume of production. It affect cost of production per unit and accordingly firm

increase pricing scenario also. Furthermore, overhead consists of expenses incurred from

machinery 1 and machinery 2 where it has been found that first machinery has cost of per unit

4.53. In addition to this, second one incurred 2.33. Accordingly total cost is 21.83 and here

management of corporation can margin of profitability in accordance with selected pricing

strategy.

2.1 Preparing and analysing routine cost reports

Routine cost report consists of detail information related to cost of production lot and

benefits derived from the same. It can be done as follows-

Table 6: Cost data

Particular Units/ cost per unit

Production 2500 units

Material price £15 per unit

Labour rate £10 per unit

Overhead rate £8 per unit

Fixed cost £10000

Table 7: Variances

Particular Expected Actual (2500 units) Variance

Direct material 35000 37500 -2500

Direct labour 26000 25000 1000

Direct overhead 19500 20000 -500

Fixed overheads 10000 10000 0

Total costs 90500 92500 -2000

The above mentioned table reflects that there is negative variance with regard to direct

material. It is showing that corporation is not working in accordance with set budge (Shelby,

2013)t. In fact there is significant difference in the actual and expected output. The above table is

showing that expected amount of direct material will be 35000 but it is 37500. It can be seen that

9

accordance with volume of production. It affect cost of production per unit and accordingly firm

increase pricing scenario also. Furthermore, overhead consists of expenses incurred from

machinery 1 and machinery 2 where it has been found that first machinery has cost of per unit

4.53. In addition to this, second one incurred 2.33. Accordingly total cost is 21.83 and here

management of corporation can margin of profitability in accordance with selected pricing

strategy.

2.1 Preparing and analysing routine cost reports

Routine cost report consists of detail information related to cost of production lot and

benefits derived from the same. It can be done as follows-

Table 6: Cost data

Particular Units/ cost per unit

Production 2500 units

Material price £15 per unit

Labour rate £10 per unit

Overhead rate £8 per unit

Fixed cost £10000

Table 7: Variances

Particular Expected Actual (2500 units) Variance

Direct material 35000 37500 -2500

Direct labour 26000 25000 1000

Direct overhead 19500 20000 -500

Fixed overheads 10000 10000 0

Total costs 90500 92500 -2000

The above mentioned table reflects that there is negative variance with regard to direct

material. It is showing that corporation is not working in accordance with set budge (Shelby,

2013)t. In fact there is significant difference in the actual and expected output. The above table is

showing that expected amount of direct material will be 35000 but it is 37500. It can be seen that

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

variance of 2500 exist in the direct material. O the other hand, it was expected that 26000 will

be incurred on direct labour but actual expenses on labour was 25000. Owing to this, there is

positive variance that corporation is using its resources effectively. Apart from this, direct

overhead was assumed to be 19500 but in real it was 20000. It reflects that negative variance of

500 has been derived. Therefore, Waitrose should focus upon budgeting policies in order to

anticipate future performance.

2.2 Using performance indicators to identify potential improvement

Performance indicators play an important role in the organization because of their

assistance in potential improvement. There are several performance indicators associated with

Waitrose which are explained as follows- Profitability-It is the most important element which defines that how organization is

performing in particular financial year (Chapman, Hopwood and Shields, 2011). In case,

if profit ratio of Waitorse was high in 2015 but low in 2016 then it depicts that

corporation is not performing in a right manner. It requires to reduce the cost of

production and perform other necessary improvements in its production cycle. Sales turnover-This is another imperative aspect which reflects that whether company is

gaining profit or not (Elmassri and Harris, 2011). For instance: if sales turnover is

increasing then it will reflect positive situation for corporation. It aids to cater the need of

management in an effectual manner because market share will also be increased with the

same. Quality of products and services- Good quality of products and services generally

increases customer base (Debarshi, 2011). It assists the corporation to meet the

expectations of buyers and deliver good quality of services among them. Furthermore, it

is very important for the organization to carry out its business in an ethical manner.

Cost reduction-Overall reduction in the cost is also an important performance indicator

which sheds light on the low price of product and services (Macintosh and Quattrone,

2010). On the other hand, if cost of production increases then it reflects that management

of Waitrose is not implementing effective practices in the production process.

10

be incurred on direct labour but actual expenses on labour was 25000. Owing to this, there is

positive variance that corporation is using its resources effectively. Apart from this, direct

overhead was assumed to be 19500 but in real it was 20000. It reflects that negative variance of

500 has been derived. Therefore, Waitrose should focus upon budgeting policies in order to

anticipate future performance.

2.2 Using performance indicators to identify potential improvement

Performance indicators play an important role in the organization because of their

assistance in potential improvement. There are several performance indicators associated with

Waitrose which are explained as follows- Profitability-It is the most important element which defines that how organization is

performing in particular financial year (Chapman, Hopwood and Shields, 2011). In case,

if profit ratio of Waitorse was high in 2015 but low in 2016 then it depicts that

corporation is not performing in a right manner. It requires to reduce the cost of

production and perform other necessary improvements in its production cycle. Sales turnover-This is another imperative aspect which reflects that whether company is

gaining profit or not (Elmassri and Harris, 2011). For instance: if sales turnover is

increasing then it will reflect positive situation for corporation. It aids to cater the need of

management in an effectual manner because market share will also be increased with the

same. Quality of products and services- Good quality of products and services generally

increases customer base (Debarshi, 2011). It assists the corporation to meet the

expectations of buyers and deliver good quality of services among them. Furthermore, it

is very important for the organization to carry out its business in an ethical manner.

Cost reduction-Overall reduction in the cost is also an important performance indicator

which sheds light on the low price of product and services (Macintosh and Quattrone,

2010). On the other hand, if cost of production increases then it reflects that management

of Waitrose is not implementing effective practices in the production process.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.3 Suggesting improvements to reduce cost, enhance value and quality

Waitrose can use different alternatives for reducing cost associated with the production

process. It is helpful for management to enhance profitability and offer product to the customers

in relatively low prices- Material management- Effective management of material is helpful to reduce the cost

because most of the times, storage cost is increased to a great extent. Owing to this,

effective methods like LIFO and FIFO can be used so as to ensure optimum utilization of

limited resources (Bhaird, 2010). Cost control- Under this, workforce must be trained to use different aspects for reducing

the overall cost (Thomas, 2010). It proves to be effective in meeting objectives of the

company in order to quote right price of products and services. Monitoring and controlling- Monitoring and controlling are very important for

management as thereby, wastage of material will be reduced and recycling of same can

be ensured.

Enhance value and quality

For enhancing value and quality, Waitrose should provide training to its personnel in an

effectual manner. However, suggestions can be taken from workforce also so as to maintain

quality standards. Such standards must be in accordance with the demand of buyers which leads

to meet their expectations effectively (McKevitt and Davis, 2013). Similarly, innovation and

creativity must be ensured at workplace with involvement of highly skilled personnel. However,

competitor’s analysis can be done for offering better quality which in turn create good image of

corporation in the marketplace.

TASK 2

3.1 Purpose and nature of budgeting process

Budget is the process of anticipating expenses of company for future time span and

taking corrective action for well being of corporation. The basic aim of preparing budget is to

reduce uncertainty associated with business. It assists organization to go in upward direction so

as to increase overall rate of return (Bellah and et. al., 2013). With the help of budgeting

technique corporation can easily control overall expenses incurred on production activities which

leads to ensure higher rate of return and low cost of production. Furthermore, budgeting process

11

Waitrose can use different alternatives for reducing cost associated with the production

process. It is helpful for management to enhance profitability and offer product to the customers

in relatively low prices- Material management- Effective management of material is helpful to reduce the cost

because most of the times, storage cost is increased to a great extent. Owing to this,

effective methods like LIFO and FIFO can be used so as to ensure optimum utilization of

limited resources (Bhaird, 2010). Cost control- Under this, workforce must be trained to use different aspects for reducing

the overall cost (Thomas, 2010). It proves to be effective in meeting objectives of the

company in order to quote right price of products and services. Monitoring and controlling- Monitoring and controlling are very important for

management as thereby, wastage of material will be reduced and recycling of same can

be ensured.

Enhance value and quality

For enhancing value and quality, Waitrose should provide training to its personnel in an

effectual manner. However, suggestions can be taken from workforce also so as to maintain

quality standards. Such standards must be in accordance with the demand of buyers which leads

to meet their expectations effectively (McKevitt and Davis, 2013). Similarly, innovation and

creativity must be ensured at workplace with involvement of highly skilled personnel. However,

competitor’s analysis can be done for offering better quality which in turn create good image of

corporation in the marketplace.

TASK 2

3.1 Purpose and nature of budgeting process

Budget is the process of anticipating expenses of company for future time span and

taking corrective action for well being of corporation. The basic aim of preparing budget is to

reduce uncertainty associated with business. It assists organization to go in upward direction so

as to increase overall rate of return (Bellah and et. al., 2013). With the help of budgeting

technique corporation can easily control overall expenses incurred on production activities which

leads to ensure higher rate of return and low cost of production. Furthermore, budgeting process

11

facilitates to allocate financial resources in right business activities in order to get competitive

edge. Apart from this, budgeting process tend to allocate budget for current business activities as

well as future strategies of organization which tend to create its unique identity in the

marketplace (Bonazzi and Iotti, 2014).

Furthermore, process of budgeting start with setting objectives. Here, management of

Waitrose set objectives by collecting data of internal and external environment of business.

Furthermore, expectations of managers are discussed in formal meeting so they can easily

accomplish set objectives of organization (Gesimba, Alvar and Mante, 2014). After

reconciliation of objectives in accordance with expectations, budget is created by financial

personnel of organization. After completion of budget, outcome are monitored along with

variance analysis. This assists organization to reduce overall gap between actual ads expected

outcome. In addition to this, adjustment is done in the light of expectation or set gaols.

3.2 Selecting appropriate budgeting methods for organization and its needs

In order to have sustainable development, it is significant for management of Waitrose to

ensure about selection of budgeting methods. It is also necessary for decision makers to design

and select budget methods as per the organizational needs. In addition to this, the Zero base

budgeting method can also be one of most suitable aspect for the organization (Kavanagh,

2011). In this, management needs to provide justification for all expenses in the budget process

so that goals can be accomplished in desired form. It is a budget that starts from baseline and

every function of organisation is analyzed according to organizational need. Cost of operational

activities also need to be evaluated for further developments. In order to expand business

effectively at international level the business firm requires low cost and high budget for

investment (Łukaszewski and Wilk, 2016).

In this regard, the management of Waitrose also requires optimum allocation and

utilization of sources so that needs of business units can be accomplished in most suitable

manner (Shelby, 2013). With an assistance of Zero base budgeting the top level authorities can

design strategic goals which can be applied for success of budgeting process. Specific functional

areas also need to be designed in desired form for better satisfaction.

As per consideration of traditional method of budgeting the management also requires

identification of previous year sales and expenditures (Elmassri and Harris, 2011). It can be

12

edge. Apart from this, budgeting process tend to allocate budget for current business activities as

well as future strategies of organization which tend to create its unique identity in the

marketplace (Bonazzi and Iotti, 2014).

Furthermore, process of budgeting start with setting objectives. Here, management of

Waitrose set objectives by collecting data of internal and external environment of business.

Furthermore, expectations of managers are discussed in formal meeting so they can easily

accomplish set objectives of organization (Gesimba, Alvar and Mante, 2014). After

reconciliation of objectives in accordance with expectations, budget is created by financial

personnel of organization. After completion of budget, outcome are monitored along with

variance analysis. This assists organization to reduce overall gap between actual ads expected

outcome. In addition to this, adjustment is done in the light of expectation or set gaols.

3.2 Selecting appropriate budgeting methods for organization and its needs

In order to have sustainable development, it is significant for management of Waitrose to

ensure about selection of budgeting methods. It is also necessary for decision makers to design

and select budget methods as per the organizational needs. In addition to this, the Zero base

budgeting method can also be one of most suitable aspect for the organization (Kavanagh,

2011). In this, management needs to provide justification for all expenses in the budget process

so that goals can be accomplished in desired form. It is a budget that starts from baseline and

every function of organisation is analyzed according to organizational need. Cost of operational

activities also need to be evaluated for further developments. In order to expand business

effectively at international level the business firm requires low cost and high budget for

investment (Łukaszewski and Wilk, 2016).

In this regard, the management of Waitrose also requires optimum allocation and

utilization of sources so that needs of business units can be accomplished in most suitable

manner (Shelby, 2013). With an assistance of Zero base budgeting the top level authorities can

design strategic goals which can be applied for success of budgeting process. Specific functional

areas also need to be designed in desired form for better satisfaction.

As per consideration of traditional method of budgeting the management also requires

identification of previous year sales and expenditures (Elmassri and Harris, 2011). It can be

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.