ACFI2003 Management Accounting Assignment: Cost Analysis and Methods

VerifiedAdded on 2022/09/03

|6

|730

|14

Homework Assignment

AI Summary

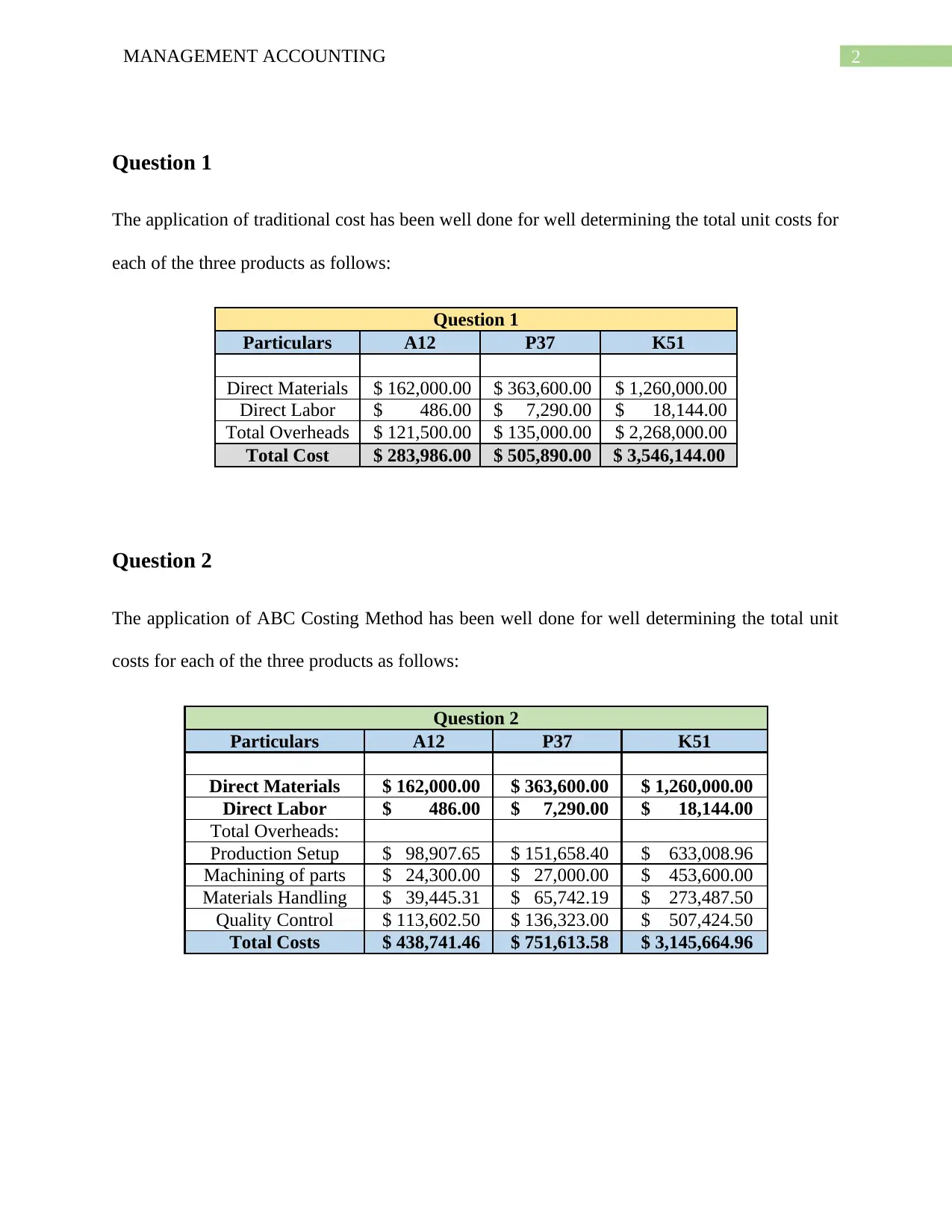

This assignment analyzes the application of traditional and Activity-Based Costing (ABC) methods for a manufacturing company, Newcastle Industrial Manufacturers (NIM), which produces three parts: A-12, P-37, and K-51. The assignment provides a comparison of unit costs calculated using both methods, including direct materials, direct labor, and overhead. It highlights the advantages and disadvantages of ABC costing, emphasizing its ability to allocate overhead more precisely and provide a more accurate view of product margins. The analysis also explores the context of NIM's challenges in meeting competitor pricing for the K-51 part and the need to set premium prices for the more complex A-12 and P-37 parts, reflecting the importance of accurate costing in strategic decision-making. The assignment concludes by referencing key academic sources to support the analysis.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.