Management Accounting Project: Costing Systems and Analysis

VerifiedAdded on 2023/01/20

|15

|4419

|83

Project

AI Summary

This project report for HA2011 Management Accounting analyzes cost concepts, costing systems, and their application in a business context. Part A explores the value chain concept, its benefits, and its application to Caltex Australia, including its mission, vision, competitive strategy, and value chain model. Part B focuses on cost allocation, including estimated allocation rates, total overhead costs, and the amount of fixed and variable costs. Part C delves into cost pools, cost drivers, and allocation rates. The report examines the relevance and usefulness of the value chain concept in detail, providing calculations and interpretations to support its findings. The report aims to demonstrate an understanding of cost management principles and their impact on decision-making within an organization.

Running Head: Management Accounting

1

Project Report: Management Accounting

1

Project Report: Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

2

Contents

Part A................................................................................................................................3

a.Value chain concept...................................................................................................3

b.Company description.................................................................................................4

i.Mission and vision..................................................................................................4

ii.Competitive strategy:.............................................................................................5

iii.Value chain model................................................................................................5

iv.Value adding process............................................................................................6

v.Relevance and usefulness of value chain concept.................................................7

Part B................................................................................................................................7

a.Estimated allocation rate............................................................................................7

b.Total overhead cost allocated....................................................................................8

c.Total cost of job 20....................................................................................................8

d.Amount of fixed and variable cost in Oct..................................................................9

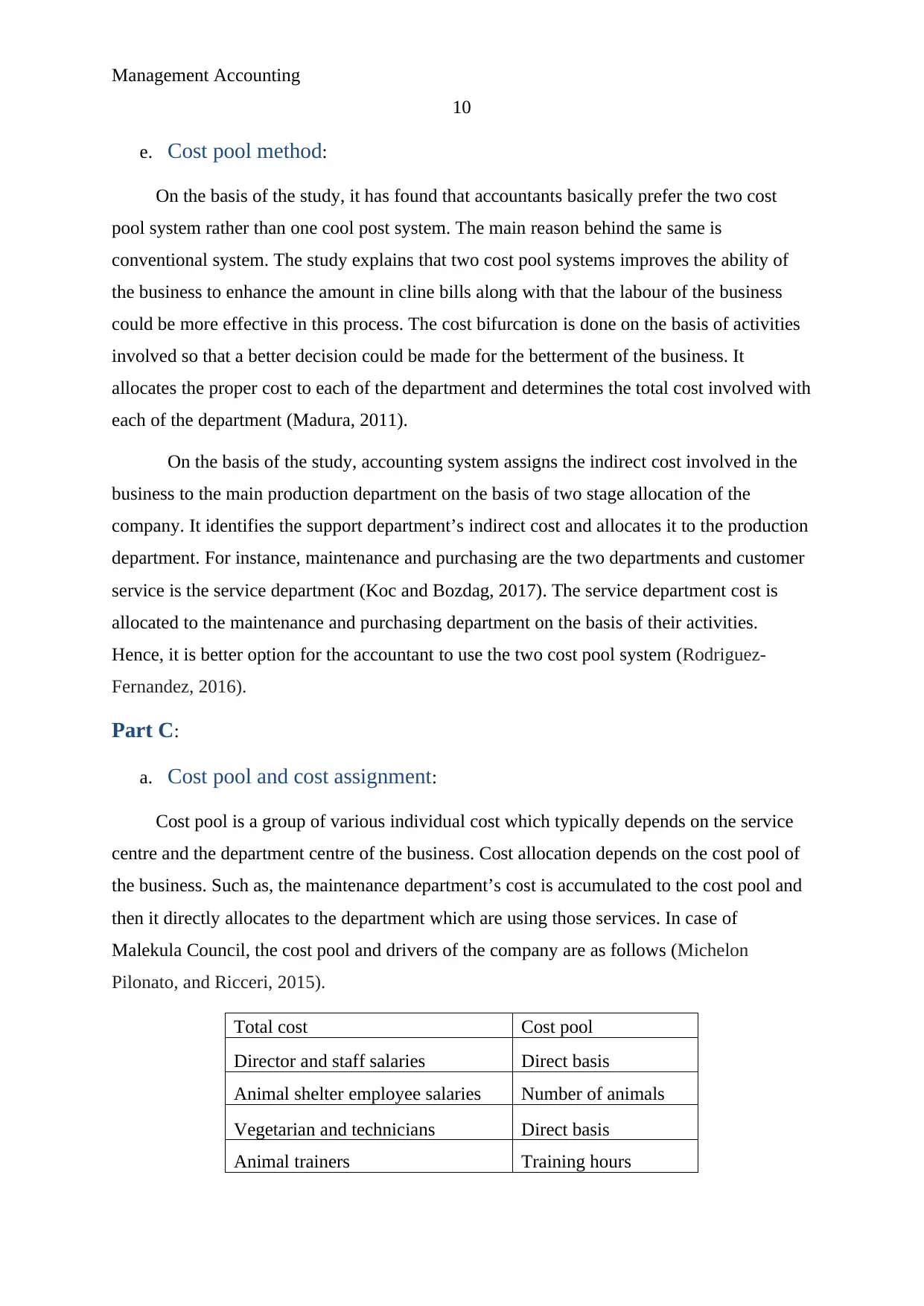

e.Cost pool method.......................................................................................................9

Part C..............................................................................................................................10

a.Cost pool and cost assignment.................................................................................10

b.Cost drivers for each cost pool................................................................................11

c.Allocation rate and interpretation............................................................................12

References.......................................................................................................................14

2

Contents

Part A................................................................................................................................3

a.Value chain concept...................................................................................................3

b.Company description.................................................................................................4

i.Mission and vision..................................................................................................4

ii.Competitive strategy:.............................................................................................5

iii.Value chain model................................................................................................5

iv.Value adding process............................................................................................6

v.Relevance and usefulness of value chain concept.................................................7

Part B................................................................................................................................7

a.Estimated allocation rate............................................................................................7

b.Total overhead cost allocated....................................................................................8

c.Total cost of job 20....................................................................................................8

d.Amount of fixed and variable cost in Oct..................................................................9

e.Cost pool method.......................................................................................................9

Part C..............................................................................................................................10

a.Cost pool and cost assignment.................................................................................10

b.Cost drivers for each cost pool................................................................................11

c.Allocation rate and interpretation............................................................................12

References.......................................................................................................................14

Management Accounting

3

Part A:

a. Value chain concept:

Value chain analysis is a strategic tool which is used in an organization to identify the

primary and secondary activities of the business in order to reach over the final product of the

company to evaluate the activities of the business. This process helps an organization to

reduce the overall associated cost with the production and service delivery of the company

and it also helps the company to improve the differentiation. The main goal of the value chain

analysis process is to identify the most valuable activities of the business and evaluate them

in order to set the competitive advantage of the company and improve the overall

performance of the company (Mihm, 2010). Below are the 2 main benefits of value chain

concepts which are used in an organization to improve the overall performance and set the

better position in the market:

i. Ensure value creates exceeds cost:

There are mainly 5 primary activities of an organization which defines about the main

operations of the business and associated with the management of cost and profit level of the

business. On the basis of evaluation over those 5 primary activities of the business, it

becomes easier for an organization to ensure about the exceed value of the business and the

cost to create the overall value of the business. The five value chain activities of the business

are as follows (Lang, and Stice-Lawrence, 2015).

Inbound logistics

Outbound logistics

Operations

Service

Marketing and sales (Madura, 2011)

These primary activities ensure that all the process of preparation and delivery of a

product or delivering a service are managed efficiently. It assures that the cost level of the

business could be reduced and it can set a better competitive advantage in the market

(Kozlowski, Searcy, and Bardecki, 2015).

ii. Gain competitive edge and boost profit:

3

Part A:

a. Value chain concept:

Value chain analysis is a strategic tool which is used in an organization to identify the

primary and secondary activities of the business in order to reach over the final product of the

company to evaluate the activities of the business. This process helps an organization to

reduce the overall associated cost with the production and service delivery of the company

and it also helps the company to improve the differentiation. The main goal of the value chain

analysis process is to identify the most valuable activities of the business and evaluate them

in order to set the competitive advantage of the company and improve the overall

performance of the company (Mihm, 2010). Below are the 2 main benefits of value chain

concepts which are used in an organization to improve the overall performance and set the

better position in the market:

i. Ensure value creates exceeds cost:

There are mainly 5 primary activities of an organization which defines about the main

operations of the business and associated with the management of cost and profit level of the

business. On the basis of evaluation over those 5 primary activities of the business, it

becomes easier for an organization to ensure about the exceed value of the business and the

cost to create the overall value of the business. The five value chain activities of the business

are as follows (Lang, and Stice-Lawrence, 2015).

Inbound logistics

Outbound logistics

Operations

Service

Marketing and sales (Madura, 2011)

These primary activities ensure that all the process of preparation and delivery of a

product or delivering a service are managed efficiently. It assures that the cost level of the

business could be reduced and it can set a better competitive advantage in the market

(Kozlowski, Searcy, and Bardecki, 2015).

ii. Gain competitive edge and boost profit:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting

4

Further, the value chain analysis also helps the business to gain a competitive

advantage and manage the profitability level of the business in the market. If an organization

could create an advantage in any of the below five activities then it becomes easier for the

business to capture the competitive advantage in the market and improve the overall

profitability level in the market.

Inbound logistics

Outbound logistics

Operations

Service

Marketing and sales

In order to capture a competitive state and advantage in the market, an organization

should map out all the activities within the main 5 value chain activities and improve the

efficiency level of the business in the market. It would help the business to meet the common

goal of the business (Lysons and Farrington, 2012).

b. Company description:

In the report, Caltex Australia has been chosen to identify the concept of value chain

and the importance of value chain analysis in an organization. Caltex Australia is a subsidiary

company of Woolworths limited. It is an Australian chain which operates under the

automotive and retains industry in the Australia. The main products of the business are petrol,

convenience and grocery. Company has been founded in the year of 1996 by the name of

Woolworths petrol. Later on, the company name changed to Caltex Woolworths in the year

of 2013.

i. Mission and vision:

Mission and vision statement of Caltex Australia has been studied further to understand

the main goal and aim of the company. Vision statement of company depicts that company’s

main vision is to be the leader in oil and refinery industry in Australia and company further

focused towards to be more admired and loved by the people, stakeholders and society

because of the performance and policies of the business (Our vision, 2019).

4

Further, the value chain analysis also helps the business to gain a competitive

advantage and manage the profitability level of the business in the market. If an organization

could create an advantage in any of the below five activities then it becomes easier for the

business to capture the competitive advantage in the market and improve the overall

profitability level in the market.

Inbound logistics

Outbound logistics

Operations

Service

Marketing and sales

In order to capture a competitive state and advantage in the market, an organization

should map out all the activities within the main 5 value chain activities and improve the

efficiency level of the business in the market. It would help the business to meet the common

goal of the business (Lysons and Farrington, 2012).

b. Company description:

In the report, Caltex Australia has been chosen to identify the concept of value chain

and the importance of value chain analysis in an organization. Caltex Australia is a subsidiary

company of Woolworths limited. It is an Australian chain which operates under the

automotive and retains industry in the Australia. The main products of the business are petrol,

convenience and grocery. Company has been founded in the year of 1996 by the name of

Woolworths petrol. Later on, the company name changed to Caltex Woolworths in the year

of 2013.

i. Mission and vision:

Mission and vision statement of Caltex Australia has been studied further to understand

the main goal and aim of the company. Vision statement of company depicts that company’s

main vision is to be the leader in oil and refinery industry in Australia and company further

focused towards to be more admired and loved by the people, stakeholders and society

because of the performance and policies of the business (Our vision, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

5

Further, the mission statement of company explains that the company wants to create a

universe whether all the excellent services are provided to the customers of the company. The

company wants to support and grow the employees and other stakeholders of the company.

Company is planning to invest in the infrastructure of the business in order to make it safer,

brighter, cleaner and more convenient to the environment of the company. The company

supports to the local initiatives and organizations to grow together and improve the education

and sport in the surrounding.

ii. Competitive strategy:

Caltex Australia has focused more towards the development of core competencies of

the company through differentiating the products of the company and become the cost leader

in the market. Caltex Australia is undergoing through a strategic shift away from the refining

business of the business which has basically contributed towards the unpredictable return and

disappointment of the business. The company is currently Australia’s leading fuel company

and the main competitive strength of the company is distribution of infrastructure that also

includes port terminals, airport terminals, inland terminals and pipelines. All of these

terminals are reliable delivery of fuel and enable efficient. The long term demand of transport

fuel remains favourable (Fuel and lubes, 2019). The demand of the business would grow

further in the market through offsetting the petrol prices in the market.

iii. Value chain model:

Caltex Australia has maintained and managed the value chain analysis model in an

efficient manner. The company has differentiated the primary and secondary activities of the

business in order to reach over the final goal of the company and evaluate the activities of the

business. This process has helped the business to reduce the overall associated cost with the

production and service delivery of the company and it also helps the company to improve the

differentiation. The main goal of the Caltex Australia behind the value chain analysis process

is to identify the most valuable activities of the business and evaluate them in order to set the

competitive advantage of the company and improve the overall performance of the company.

Below is the vale chain model of the business:

5

Further, the mission statement of company explains that the company wants to create a

universe whether all the excellent services are provided to the customers of the company. The

company wants to support and grow the employees and other stakeholders of the company.

Company is planning to invest in the infrastructure of the business in order to make it safer,

brighter, cleaner and more convenient to the environment of the company. The company

supports to the local initiatives and organizations to grow together and improve the education

and sport in the surrounding.

ii. Competitive strategy:

Caltex Australia has focused more towards the development of core competencies of

the company through differentiating the products of the company and become the cost leader

in the market. Caltex Australia is undergoing through a strategic shift away from the refining

business of the business which has basically contributed towards the unpredictable return and

disappointment of the business. The company is currently Australia’s leading fuel company

and the main competitive strength of the company is distribution of infrastructure that also

includes port terminals, airport terminals, inland terminals and pipelines. All of these

terminals are reliable delivery of fuel and enable efficient. The long term demand of transport

fuel remains favourable (Fuel and lubes, 2019). The demand of the business would grow

further in the market through offsetting the petrol prices in the market.

iii. Value chain model:

Caltex Australia has maintained and managed the value chain analysis model in an

efficient manner. The company has differentiated the primary and secondary activities of the

business in order to reach over the final goal of the company and evaluate the activities of the

business. This process has helped the business to reduce the overall associated cost with the

production and service delivery of the company and it also helps the company to improve the

differentiation. The main goal of the Caltex Australia behind the value chain analysis process

is to identify the most valuable activities of the business and evaluate them in order to set the

competitive advantage of the company and improve the overall performance of the company.

Below is the vale chain model of the business:

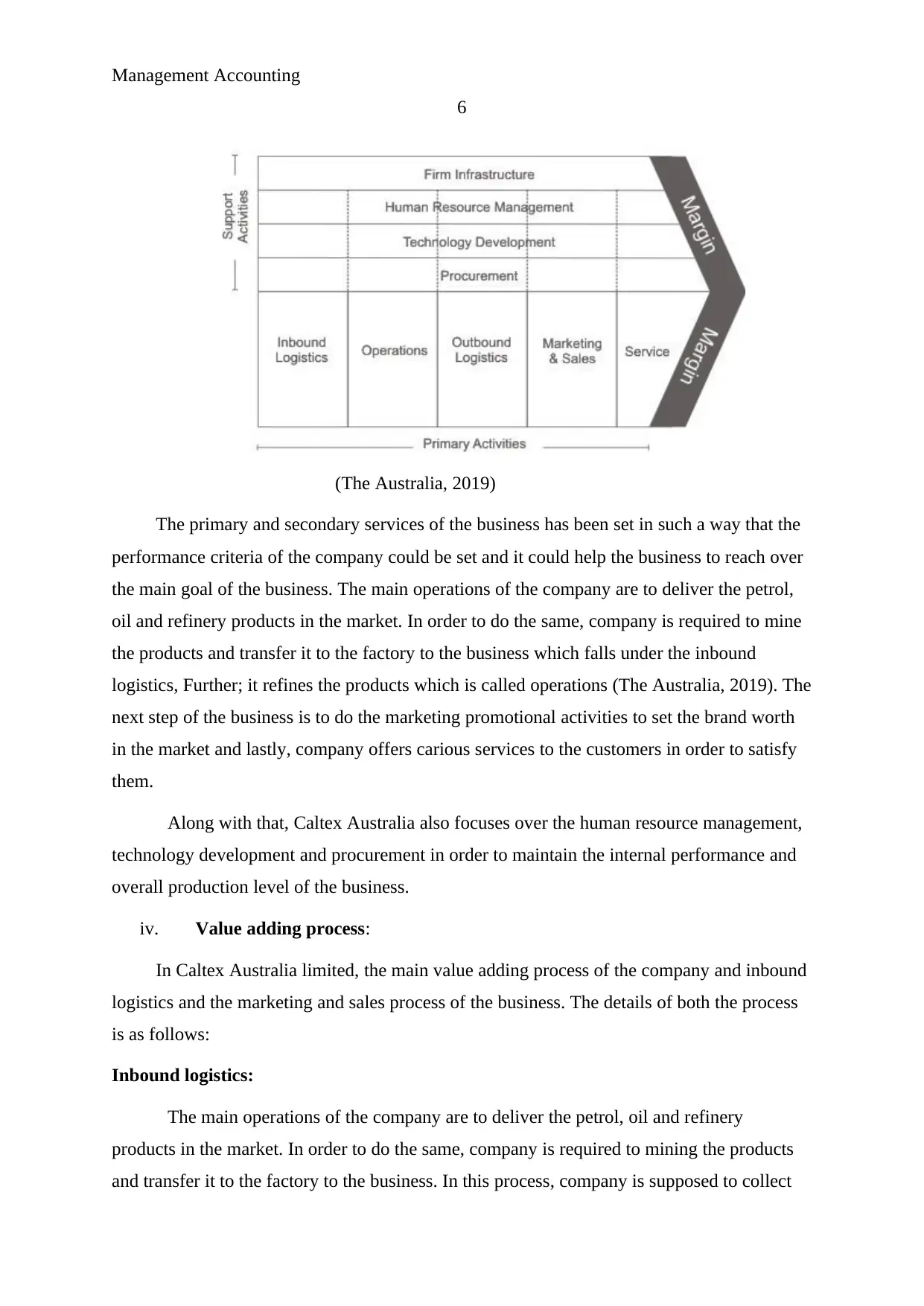

Management Accounting

6

(The Australia, 2019)

The primary and secondary services of the business has been set in such a way that the

performance criteria of the company could be set and it could help the business to reach over

the main goal of the business. The main operations of the company are to deliver the petrol,

oil and refinery products in the market. In order to do the same, company is required to mine

the products and transfer it to the factory to the business which falls under the inbound

logistics, Further; it refines the products which is called operations (The Australia, 2019). The

next step of the business is to do the marketing promotional activities to set the brand worth

in the market and lastly, company offers carious services to the customers in order to satisfy

them.

Along with that, Caltex Australia also focuses over the human resource management,

technology development and procurement in order to maintain the internal performance and

overall production level of the business.

iv. Value adding process:

In Caltex Australia limited, the main value adding process of the company and inbound

logistics and the marketing and sales process of the business. The details of both the process

is as follows:

Inbound logistics:

The main operations of the company are to deliver the petrol, oil and refinery

products in the market. In order to do the same, company is required to mining the products

and transfer it to the factory to the business. In this process, company is supposed to collect

6

(The Australia, 2019)

The primary and secondary services of the business has been set in such a way that the

performance criteria of the company could be set and it could help the business to reach over

the main goal of the business. The main operations of the company are to deliver the petrol,

oil and refinery products in the market. In order to do the same, company is required to mine

the products and transfer it to the factory to the business which falls under the inbound

logistics, Further; it refines the products which is called operations (The Australia, 2019). The

next step of the business is to do the marketing promotional activities to set the brand worth

in the market and lastly, company offers carious services to the customers in order to satisfy

them.

Along with that, Caltex Australia also focuses over the human resource management,

technology development and procurement in order to maintain the internal performance and

overall production level of the business.

iv. Value adding process:

In Caltex Australia limited, the main value adding process of the company and inbound

logistics and the marketing and sales process of the business. The details of both the process

is as follows:

Inbound logistics:

The main operations of the company are to deliver the petrol, oil and refinery

products in the market. In order to do the same, company is required to mining the products

and transfer it to the factory to the business. In this process, company is supposed to collect

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting

7

the raw materials from the mining and suppliers and transfer it to the factory to the company.

The process is called inbound logistics. Company has set proper logistics tactics in order to

manage the inbound logistics and reduce the extra cost of the business.

Marketing and sales:

Further, it has been found that there is huge competition for Caltex Australia in the

market. Hence, it becomes important for the business to check all the factors, in the market

and promote the product in the market. The Caltex Australia is using the various ways such

as TV media and newspaper to promote the products of the company and improve the sales

growth in the market (Sivula and Kantola, 2014).

v. Relevance and usefulness of value chain concept:

In order to examine the relevance and usefulness of value chain concept of the business,

various dimensions have been studied. on the basis of the study over Caltex Australia, it has

been found that value chain’s main aim is to ensure that all the activities of the company is

performed nicely so that the ultimate goal of the business could be reached. The Caltex

Australia is using inbound logistics, outbound logistics, Operations, Service and Marketing

and sales department and process in such a way that the main mission and vision of the

company could be achieved (Simatupang, Piboonrungroj and Williams, 2017).

The company had made changes into logistic process and marketing and sales process

in order to ensure that the value chain process relevancy could be improved in the business

and it becomes easier for the business to maintain the overall performance of the company.

Part B:

a. Estimated allocation rate:

Cost allocation is one of the important aspects of cost management in an organization.

It becomes important for production house to measure and analyze the fixed and variable

overhead cost related to the production of a particular in order to make better decision about

the performance and position of the company. The fixed overhead allocation and variable

overhead allocation of an organization depends on the cost drivers and cost pool of the

business.

Cost drivers are always set by the business on the basis of the involvement and

operations of each of the production and service department of the business. On the basis of

7

the raw materials from the mining and suppliers and transfer it to the factory to the company.

The process is called inbound logistics. Company has set proper logistics tactics in order to

manage the inbound logistics and reduce the extra cost of the business.

Marketing and sales:

Further, it has been found that there is huge competition for Caltex Australia in the

market. Hence, it becomes important for the business to check all the factors, in the market

and promote the product in the market. The Caltex Australia is using the various ways such

as TV media and newspaper to promote the products of the company and improve the sales

growth in the market (Sivula and Kantola, 2014).

v. Relevance and usefulness of value chain concept:

In order to examine the relevance and usefulness of value chain concept of the business,

various dimensions have been studied. on the basis of the study over Caltex Australia, it has

been found that value chain’s main aim is to ensure that all the activities of the company is

performed nicely so that the ultimate goal of the business could be reached. The Caltex

Australia is using inbound logistics, outbound logistics, Operations, Service and Marketing

and sales department and process in such a way that the main mission and vision of the

company could be achieved (Simatupang, Piboonrungroj and Williams, 2017).

The company had made changes into logistic process and marketing and sales process

in order to ensure that the value chain process relevancy could be improved in the business

and it becomes easier for the business to maintain the overall performance of the company.

Part B:

a. Estimated allocation rate:

Cost allocation is one of the important aspects of cost management in an organization.

It becomes important for production house to measure and analyze the fixed and variable

overhead cost related to the production of a particular in order to make better decision about

the performance and position of the company. The fixed overhead allocation and variable

overhead allocation of an organization depends on the cost drivers and cost pool of the

business.

Cost drivers are always set by the business on the basis of the involvement and

operations of each of the production and service department of the business. On the basis of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

8

the study over case, it has been observed that the allocation of the cost should be done on the

basis of cost drivers in order to reach over better outcome (Quattrone, 2016). The estimated

allocation rate of the company has been initially measured on the basis of total fixed

overhead and variable overhead of the business.

The allocation rate of an organization is the standard overhead amount. It amount is

applied in a production house on the basis of activity measurement. The main aim behind this

process is to ensure that the exact applied and occurred cost of the business could be

measured. The allocation rate of the business is as follows:

Particular Details Calculations

Variable rate 50% of direct labour cost <=750000/1500000*250 $ 125

Fixed variable rate

Fixed overhead / Direct

labour hours <=150000/250 $ 600

Total overhead cost

Fixed cost + variable

cost <=125+600 $ 725

b. Total overhead cost allocated:

Total overhead cost in an organization depicts about the total cost which has been

incurred in an organization at the time of producing a product or delivering a service. The

total overhead cost involves the fixed overhead cost as well as variable overhead cost. In the

given case, the below table has been presented to identify the total overhead cost incurred in

the company:

Particular Details Calculations

Variable rate 50% of direct labour cost <=750000/1500000*250 $ 125

Fixed variable rate

Fixed overhead / Direct

labour hours <=150000/250 $ 600

Total overhead cost

Fixed cost + variable

cost <=125+600 $ 725

(Messner, 2016)

8

the study over case, it has been observed that the allocation of the cost should be done on the

basis of cost drivers in order to reach over better outcome (Quattrone, 2016). The estimated

allocation rate of the company has been initially measured on the basis of total fixed

overhead and variable overhead of the business.

The allocation rate of an organization is the standard overhead amount. It amount is

applied in a production house on the basis of activity measurement. The main aim behind this

process is to ensure that the exact applied and occurred cost of the business could be

measured. The allocation rate of the business is as follows:

Particular Details Calculations

Variable rate 50% of direct labour cost <=750000/1500000*250 $ 125

Fixed variable rate

Fixed overhead / Direct

labour hours <=150000/250 $ 600

Total overhead cost

Fixed cost + variable

cost <=125+600 $ 725

b. Total overhead cost allocated:

Total overhead cost in an organization depicts about the total cost which has been

incurred in an organization at the time of producing a product or delivering a service. The

total overhead cost involves the fixed overhead cost as well as variable overhead cost. In the

given case, the below table has been presented to identify the total overhead cost incurred in

the company:

Particular Details Calculations

Variable rate 50% of direct labour cost <=750000/1500000*250 $ 125

Fixed variable rate

Fixed overhead / Direct

labour hours <=150000/250 $ 600

Total overhead cost

Fixed cost + variable

cost <=125+600 $ 725

(Messner, 2016)

Management Accounting

9

c. Total cost of job 20:

Total cost stands for the total amount which has been incurred in an organization while

the production of a product or because of different process applied while delivering the

services. It includes the total cost from getting the raw material in the business to deliver the

final product in the market. The total cost involves fixed cost, variable cost and semi variable

cost of the business. In case of the given case study found that there is various cost involved

with the production of a particular product.

In this section, the study has been conducted over the total cost involved in job 20 of

the business. The study brief that there are various cost such as fixed cost, variable cost and

semi variable cost are involved with the Job 20 of the company. The detail of the same is as

follows:

Particular Cost

Add: Direct labour cost $ 250

Variable overhead cost

(calculated) $ 125

Fixed overhead cost (calculated) $ 600

Total $ 975

Add: Opening WIP $ 3,500

Total cost for Job 20 $ 4,475

d. Amount of fixed and variable cost in Oct:

Further, the study has been done over the total fixed cost and variable cost of the

different jobs in the month of Oct. On the basis of the study, it has been found that there were

various cost involved in the production process of the business. In the case, the cost

evaluation has been done through allocating them in the variable cost and fixed cost. Also,

the cost drivers of the different cost have been taken into consideration.

Particular Amount

Fixed overhead allocation ($ 5725*48%) 2748

Variable overhead allocation ($ 5725 *

52%) 2977

9

c. Total cost of job 20:

Total cost stands for the total amount which has been incurred in an organization while

the production of a product or because of different process applied while delivering the

services. It includes the total cost from getting the raw material in the business to deliver the

final product in the market. The total cost involves fixed cost, variable cost and semi variable

cost of the business. In case of the given case study found that there is various cost involved

with the production of a particular product.

In this section, the study has been conducted over the total cost involved in job 20 of

the business. The study brief that there are various cost such as fixed cost, variable cost and

semi variable cost are involved with the Job 20 of the company. The detail of the same is as

follows:

Particular Cost

Add: Direct labour cost $ 250

Variable overhead cost

(calculated) $ 125

Fixed overhead cost (calculated) $ 600

Total $ 975

Add: Opening WIP $ 3,500

Total cost for Job 20 $ 4,475

d. Amount of fixed and variable cost in Oct:

Further, the study has been done over the total fixed cost and variable cost of the

different jobs in the month of Oct. On the basis of the study, it has been found that there were

various cost involved in the production process of the business. In the case, the cost

evaluation has been done through allocating them in the variable cost and fixed cost. Also,

the cost drivers of the different cost have been taken into consideration.

Particular Amount

Fixed overhead allocation ($ 5725*48%) 2748

Variable overhead allocation ($ 5725 *

52%) 2977

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting

10

e. Cost pool method:

On the basis of the study, it has found that accountants basically prefer the two cost

pool system rather than one cool post system. The main reason behind the same is

conventional system. The study explains that two cost pool systems improves the ability of

the business to enhance the amount in cline bills along with that the labour of the business

could be more effective in this process. The cost bifurcation is done on the basis of activities

involved so that a better decision could be made for the betterment of the business. It

allocates the proper cost to each of the department and determines the total cost involved with

each of the department (Madura, 2011).

On the basis of the study, accounting system assigns the indirect cost involved in the

business to the main production department on the basis of two stage allocation of the

company. It identifies the support department’s indirect cost and allocates it to the production

department. For instance, maintenance and purchasing are the two departments and customer

service is the service department (Koc and Bozdag, 2017). The service department cost is

allocated to the maintenance and purchasing department on the basis of their activities.

Hence, it is better option for the accountant to use the two cost pool system (Rodriguez-

Fernandez, 2016).

Part C:

a. Cost pool and cost assignment:

Cost pool is a group of various individual cost which typically depends on the service

centre and the department centre of the business. Cost allocation depends on the cost pool of

the business. Such as, the maintenance department’s cost is accumulated to the cost pool and

then it directly allocates to the department which are using those services. In case of

Malekula Council, the cost pool and drivers of the company are as follows (Michelon

Pilonato, and Ricceri, 2015).

Total cost Cost pool

Director and staff salaries Direct basis

Animal shelter employee salaries Number of animals

Vegetarian and technicians Direct basis

Animal trainers Training hours

10

e. Cost pool method:

On the basis of the study, it has found that accountants basically prefer the two cost

pool system rather than one cool post system. The main reason behind the same is

conventional system. The study explains that two cost pool systems improves the ability of

the business to enhance the amount in cline bills along with that the labour of the business

could be more effective in this process. The cost bifurcation is done on the basis of activities

involved so that a better decision could be made for the betterment of the business. It

allocates the proper cost to each of the department and determines the total cost involved with

each of the department (Madura, 2011).

On the basis of the study, accounting system assigns the indirect cost involved in the

business to the main production department on the basis of two stage allocation of the

company. It identifies the support department’s indirect cost and allocates it to the production

department. For instance, maintenance and purchasing are the two departments and customer

service is the service department (Koc and Bozdag, 2017). The service department cost is

allocated to the maintenance and purchasing department on the basis of their activities.

Hence, it is better option for the accountant to use the two cost pool system (Rodriguez-

Fernandez, 2016).

Part C:

a. Cost pool and cost assignment:

Cost pool is a group of various individual cost which typically depends on the service

centre and the department centre of the business. Cost allocation depends on the cost pool of

the business. Such as, the maintenance department’s cost is accumulated to the cost pool and

then it directly allocates to the department which are using those services. In case of

Malekula Council, the cost pool and drivers of the company are as follows (Michelon

Pilonato, and Ricceri, 2015).

Total cost Cost pool

Director and staff salaries Direct basis

Animal shelter employee salaries Number of animals

Vegetarian and technicians Direct basis

Animal trainers Training hours

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

11

food and supplies Apportionment basis

Building related costs Sq feet

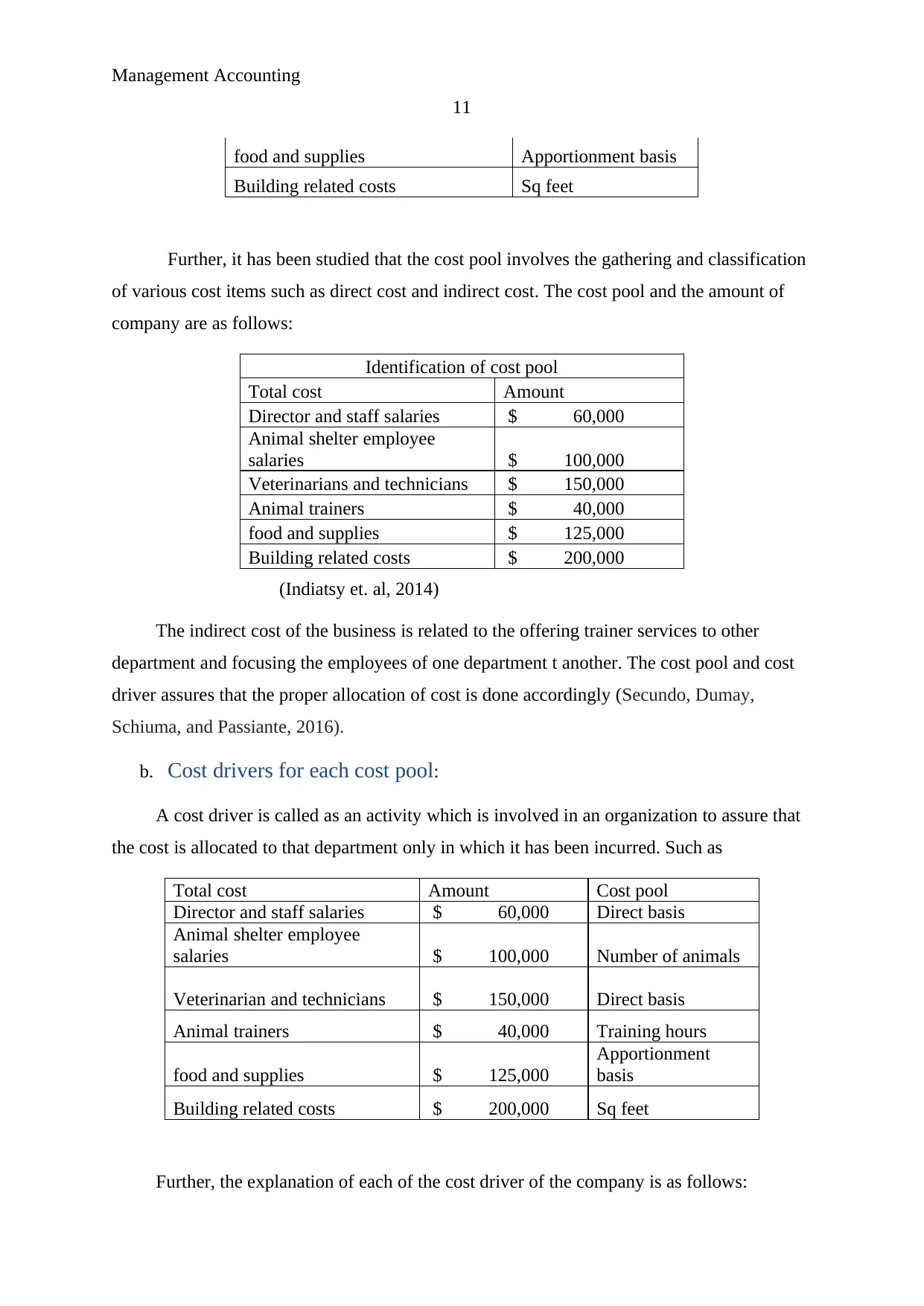

Further, it has been studied that the cost pool involves the gathering and classification

of various cost items such as direct cost and indirect cost. The cost pool and the amount of

company are as follows:

Identification of cost pool

Total cost Amount

Director and staff salaries $ 60,000

Animal shelter employee

salaries $ 100,000

Veterinarians and technicians $ 150,000

Animal trainers $ 40,000

food and supplies $ 125,000

Building related costs $ 200,000

(Indiatsy et. al, 2014)

The indirect cost of the business is related to the offering trainer services to other

department and focusing the employees of one department t another. The cost pool and cost

driver assures that the proper allocation of cost is done accordingly (Secundo, Dumay,

Schiuma, and Passiante, 2016).

b. Cost drivers for each cost pool:

A cost driver is called as an activity which is involved in an organization to assure that

the cost is allocated to that department only in which it has been incurred. Such as

Total cost Amount Cost pool

Director and staff salaries $ 60,000 Direct basis

Animal shelter employee

salaries $ 100,000 Number of animals

Veterinarian and technicians $ 150,000 Direct basis

Animal trainers $ 40,000 Training hours

food and supplies $ 125,000

Apportionment

basis

Building related costs $ 200,000 Sq feet

Further, the explanation of each of the cost driver of the company is as follows:

11

food and supplies Apportionment basis

Building related costs Sq feet

Further, it has been studied that the cost pool involves the gathering and classification

of various cost items such as direct cost and indirect cost. The cost pool and the amount of

company are as follows:

Identification of cost pool

Total cost Amount

Director and staff salaries $ 60,000

Animal shelter employee

salaries $ 100,000

Veterinarians and technicians $ 150,000

Animal trainers $ 40,000

food and supplies $ 125,000

Building related costs $ 200,000

(Indiatsy et. al, 2014)

The indirect cost of the business is related to the offering trainer services to other

department and focusing the employees of one department t another. The cost pool and cost

driver assures that the proper allocation of cost is done accordingly (Secundo, Dumay,

Schiuma, and Passiante, 2016).

b. Cost drivers for each cost pool:

A cost driver is called as an activity which is involved in an organization to assure that

the cost is allocated to that department only in which it has been incurred. Such as

Total cost Amount Cost pool

Director and staff salaries $ 60,000 Direct basis

Animal shelter employee

salaries $ 100,000 Number of animals

Veterinarian and technicians $ 150,000 Direct basis

Animal trainers $ 40,000 Training hours

food and supplies $ 125,000

Apportionment

basis

Building related costs $ 200,000 Sq feet

Further, the explanation of each of the cost driver of the company is as follows:

Management Accounting

12

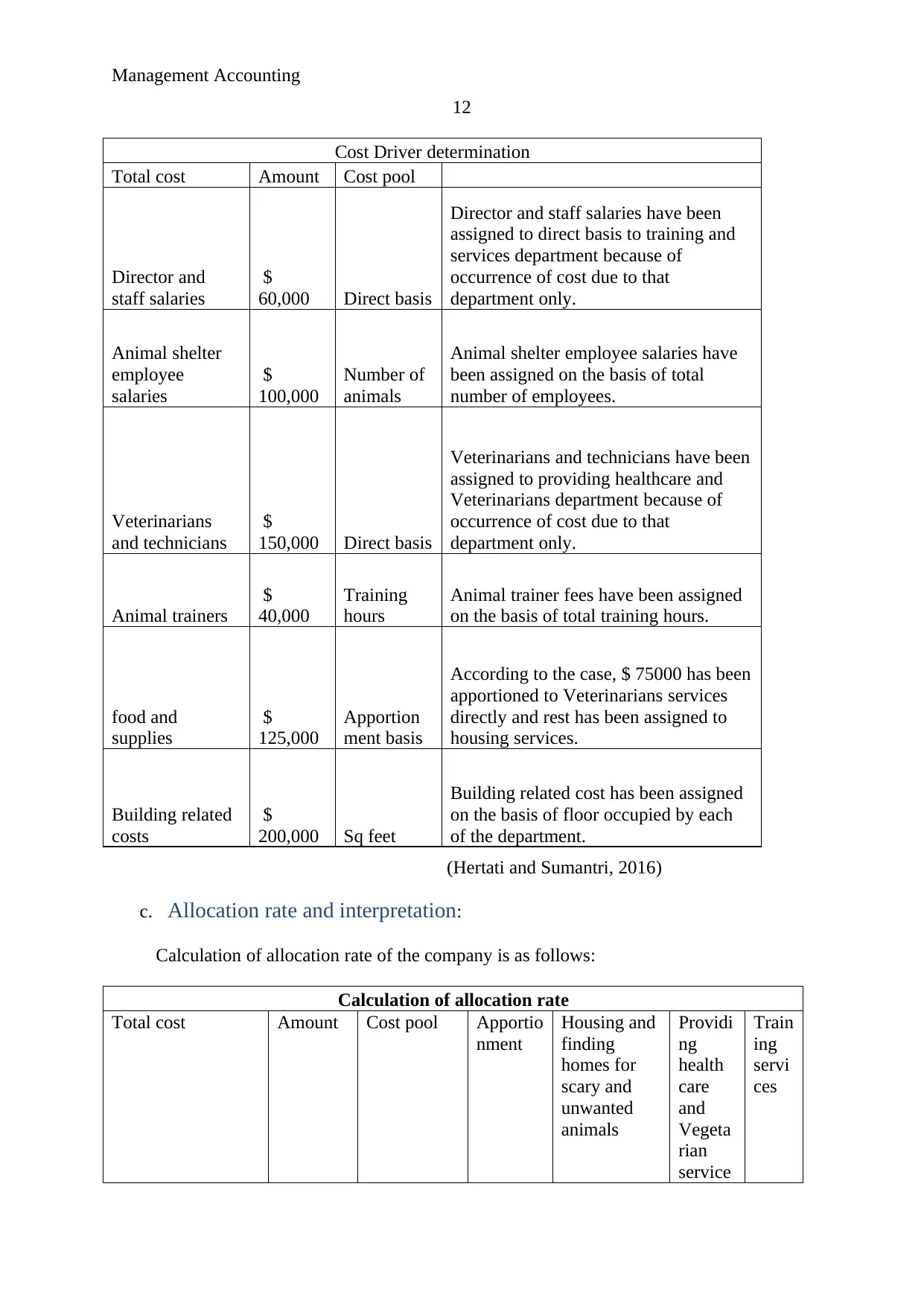

Cost Driver determination

Total cost Amount Cost pool

Director and

staff salaries

$

60,000 Direct basis

Director and staff salaries have been

assigned to direct basis to training and

services department because of

occurrence of cost due to that

department only.

Animal shelter

employee

salaries

$

100,000

Number of

animals

Animal shelter employee salaries have

been assigned on the basis of total

number of employees.

Veterinarians

and technicians

$

150,000 Direct basis

Veterinarians and technicians have been

assigned to providing healthcare and

Veterinarians department because of

occurrence of cost due to that

department only.

Animal trainers

$

40,000

Training

hours

Animal trainer fees have been assigned

on the basis of total training hours.

food and

supplies

$

125,000

Apportion

ment basis

According to the case, $ 75000 has been

apportioned to Veterinarians services

directly and rest has been assigned to

housing services.

Building related

costs

$

200,000 Sq feet

Building related cost has been assigned

on the basis of floor occupied by each

of the department.

(Hertati and Sumantri, 2016)

c. Allocation rate and interpretation:

Calculation of allocation rate of the company is as follows:

Calculation of allocation rate

Total cost Amount Cost pool Apportio

nment

Housing and

finding

homes for

scary and

unwanted

animals

Providi

ng

health

care

and

Vegeta

rian

service

Train

ing

servi

ces

12

Cost Driver determination

Total cost Amount Cost pool

Director and

staff salaries

$

60,000 Direct basis

Director and staff salaries have been

assigned to direct basis to training and

services department because of

occurrence of cost due to that

department only.

Animal shelter

employee

salaries

$

100,000

Number of

animals

Animal shelter employee salaries have

been assigned on the basis of total

number of employees.

Veterinarians

and technicians

$

150,000 Direct basis

Veterinarians and technicians have been

assigned to providing healthcare and

Veterinarians department because of

occurrence of cost due to that

department only.

Animal trainers

$

40,000

Training

hours

Animal trainer fees have been assigned

on the basis of total training hours.

food and

supplies

$

125,000

Apportion

ment basis

According to the case, $ 75000 has been

apportioned to Veterinarians services

directly and rest has been assigned to

housing services.

Building related

costs

$

200,000 Sq feet

Building related cost has been assigned

on the basis of floor occupied by each

of the department.

(Hertati and Sumantri, 2016)

c. Allocation rate and interpretation:

Calculation of allocation rate of the company is as follows:

Calculation of allocation rate

Total cost Amount Cost pool Apportio

nment

Housing and

finding

homes for

scary and

unwanted

animals

Providi

ng

health

care

and

Vegeta

rian

service

Train

ing

servi

ces

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.