Management Accounting for Costs & Control

VerifiedAdded on 2020/02/24

|10

|1673

|49

Report

AI Summary

This report covers various aspects of management accounting, including cost concepts, control mechanisms, and financial performance measurement. It discusses techniques such as activity-based costing, standard costing, and budgetary analysis, providing insights into how these methods can enhance business efficiency and decision-making. The report also includes practical examples and references to key literature in the field.

Accounting and Finance

Management Accounting for Costs & Control

1 | P a g e

Management Accounting for Costs & Control

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and Finance

Contents

Solution 1 - Management accounting..............................................................................................3

Solution 2 - Control.........................................................................................................................3

Solution 3 – Cost Concepts..............................................................................................................4

Solution 4 - Manufacturing statement and income statement.........................................................4

Solution 5 - Labour cost concepts...................................................................................................6

Solution 6 - Understanding the entries in the Materials Control account........................................6

Solution 7 - Understanding the entries in the Accrued Payroll account..........................................6

Solution 8 - Payroll entries..............................................................................................................7

Solution 9 - Activity Based Costing................................................................................................7

Solution 10 - Service department cost allocation............................................................................8

References......................................................................................................................................11

2 | P a g e

Contents

Solution 1 - Management accounting..............................................................................................3

Solution 2 - Control.........................................................................................................................3

Solution 3 – Cost Concepts..............................................................................................................4

Solution 4 - Manufacturing statement and income statement.........................................................4

Solution 5 - Labour cost concepts...................................................................................................6

Solution 6 - Understanding the entries in the Materials Control account........................................6

Solution 7 - Understanding the entries in the Accrued Payroll account..........................................6

Solution 8 - Payroll entries..............................................................................................................7

Solution 9 - Activity Based Costing................................................................................................7

Solution 10 - Service department cost allocation............................................................................8

References......................................................................................................................................11

2 | P a g e

Accounting and Finance

Solution 1 - Management accounting

The term Management Accounting has been coined in the recent past by the American Council

of productivity. The current Complex situations of the business enterprise created a huge

requirement of the concept of Management Accounting for the overall purpose of planning,

coordination other controlling function of business management. Management Accounting helps

in working out the detailed managerial aspect of accounting. The basic purpose of preparing the

reports of Management Accounting is bulleted as follows -

Measuring business performance - While utilising the effective tool and techniques of

budgetary analysis & standard costing it helps the management of the company to evaluate the

overall performance of the business enterprise. This helps the management in calculating the

deviation from the benchmark budgets and actual performance of the company.

Better planning and efficiency - Through various reports prepared using the techniques of

Management Accounting it not only improve the overall efficiency of business operations while

setting out targets in advance but also supports the management in planning the various business

operations for forecasting purpose (Zimmerman & Yahya-Zadeh, 2011).

Solution 2 - Control

Management Accounting implanted in the system of business organisation add to control and

monitor the financial activities associated with the Enterprise. There do exist various techniques

and tools that will comprehend the management in determining the cost of the business

organisation in advance. The actual cost incurred is then compared with the standard benchmark

cost to determine the variances if any. Generating variances will help the management in taking

appropriate action to enhance the overall efficiency and effectiveness of the business concern.

Standard costing and budgetary analysis control are the attractive techniques of Management

Accounting report that can be exercised control accounting. Further management can also use

methods of internal check, internal audit, and statutory audit as a part of management

accounting. These tools help the management in enforcing the objectives and plans in order to

establish coordination between standard performance and actual performance of the company.

3 | P a g e

Solution 1 - Management accounting

The term Management Accounting has been coined in the recent past by the American Council

of productivity. The current Complex situations of the business enterprise created a huge

requirement of the concept of Management Accounting for the overall purpose of planning,

coordination other controlling function of business management. Management Accounting helps

in working out the detailed managerial aspect of accounting. The basic purpose of preparing the

reports of Management Accounting is bulleted as follows -

Measuring business performance - While utilising the effective tool and techniques of

budgetary analysis & standard costing it helps the management of the company to evaluate the

overall performance of the business enterprise. This helps the management in calculating the

deviation from the benchmark budgets and actual performance of the company.

Better planning and efficiency - Through various reports prepared using the techniques of

Management Accounting it not only improve the overall efficiency of business operations while

setting out targets in advance but also supports the management in planning the various business

operations for forecasting purpose (Zimmerman & Yahya-Zadeh, 2011).

Solution 2 - Control

Management Accounting implanted in the system of business organisation add to control and

monitor the financial activities associated with the Enterprise. There do exist various techniques

and tools that will comprehend the management in determining the cost of the business

organisation in advance. The actual cost incurred is then compared with the standard benchmark

cost to determine the variances if any. Generating variances will help the management in taking

appropriate action to enhance the overall efficiency and effectiveness of the business concern.

Standard costing and budgetary analysis control are the attractive techniques of Management

Accounting report that can be exercised control accounting. Further management can also use

methods of internal check, internal audit, and statutory audit as a part of management

accounting. These tools help the management in enforcing the objectives and plans in order to

establish coordination between standard performance and actual performance of the company.

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting and Finance

Solution 3 – Cost Concepts

Product costing refers to accumulating total cost associated with the manufacturing of product

and delivering of services and then distributing among them. It works out as a key relevant tool

in formulating the strategic and operations decisions related to the company management. The

purpose and need for which the technique of product costing is been implanted in the business

organisation are detailed out as follows –

No. Purpose of Production costing Examples

1. For the financial and

management accounting

Performance analysis using the production

budgets

2. Making decision related to

expansion and contraction of

production capacity

Opportunity cost analysis tools

3. Taking make or Buy decision Product ranking table and comparison with the

market price

4. Evaluation total cost and total

revenue

Production cost sheet

4 | P a g e

Solution 3 – Cost Concepts

Product costing refers to accumulating total cost associated with the manufacturing of product

and delivering of services and then distributing among them. It works out as a key relevant tool

in formulating the strategic and operations decisions related to the company management. The

purpose and need for which the technique of product costing is been implanted in the business

organisation are detailed out as follows –

No. Purpose of Production costing Examples

1. For the financial and

management accounting

Performance analysis using the production

budgets

2. Making decision related to

expansion and contraction of

production capacity

Opportunity cost analysis tools

3. Taking make or Buy decision Product ranking table and comparison with the

market price

4. Evaluation total cost and total

revenue

Production cost sheet

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and Finance

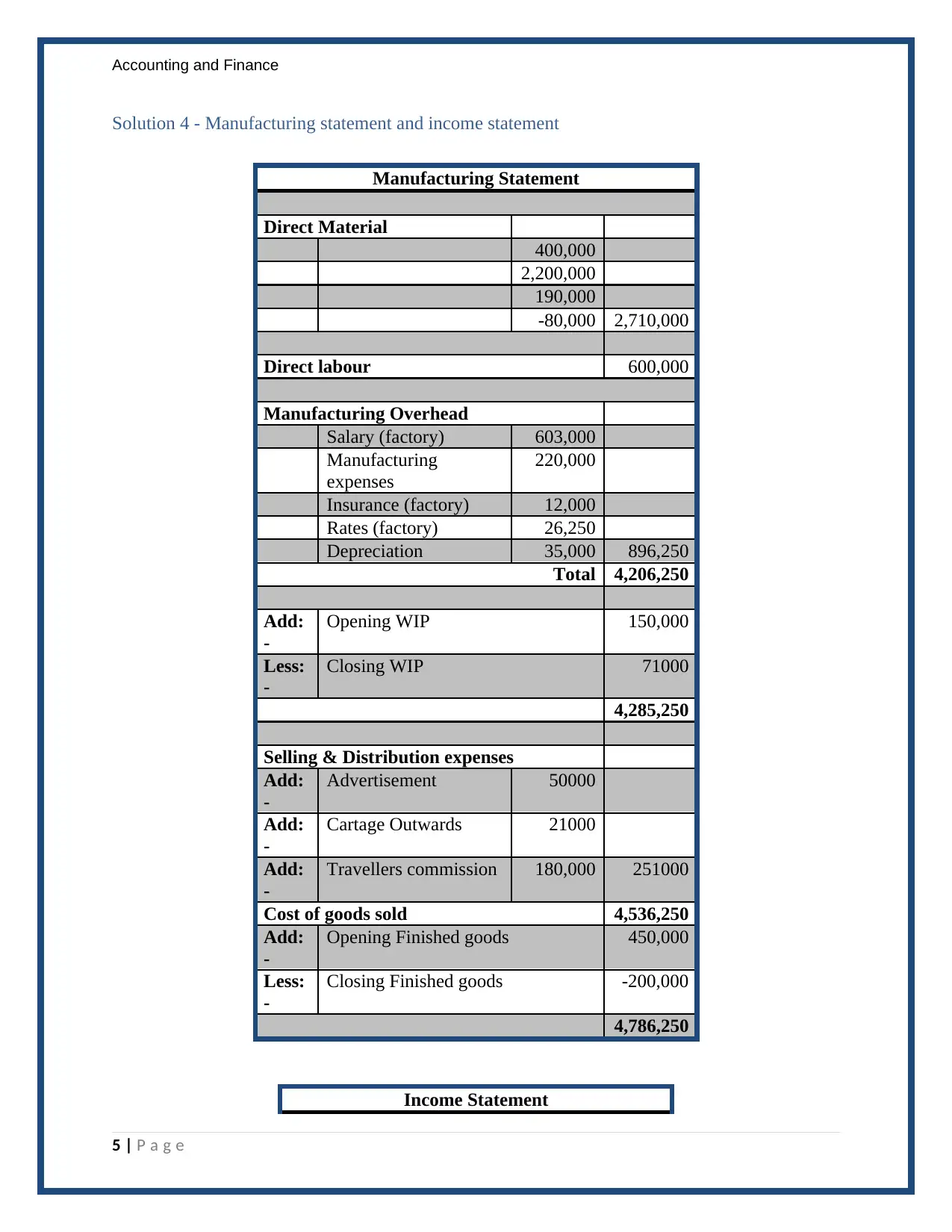

Solution 4 - Manufacturing statement and income statement

Income Statement

5 | P a g e

Manufacturing Statement

Direct Material

400,000

2,200,000

190,000

-80,000 2,710,000

Direct labour 600,000

Manufacturing Overhead

Salary (factory) 603,000

Manufacturing

expenses

220,000

Insurance (factory) 12,000

Rates (factory) 26,250

Depreciation 35,000 896,250

Total 4,206,250

Add:

-

Opening WIP 150,000

Less:

-

Closing WIP 71000

4,285,250

Selling & Distribution expenses

Add:

-

Advertisement 50000

Add:

-

Cartage Outwards 21000

Add:

-

Travellers commission 180,000 251000

Cost of goods sold 4,536,250

Add:

-

Opening Finished goods 450,000

Less:

-

Closing Finished goods -200,000

4,786,250

Solution 4 - Manufacturing statement and income statement

Income Statement

5 | P a g e

Manufacturing Statement

Direct Material

400,000

2,200,000

190,000

-80,000 2,710,000

Direct labour 600,000

Manufacturing Overhead

Salary (factory) 603,000

Manufacturing

expenses

220,000

Insurance (factory) 12,000

Rates (factory) 26,250

Depreciation 35,000 896,250

Total 4,206,250

Add:

-

Opening WIP 150,000

Less:

-

Closing WIP 71000

4,285,250

Selling & Distribution expenses

Add:

-

Advertisement 50000

Add:

-

Cartage Outwards 21000

Add:

-

Travellers commission 180,000 251000

Cost of goods sold 4,536,250

Add:

-

Opening Finished goods 450,000

Less:

-

Closing Finished goods -200,000

4,786,250

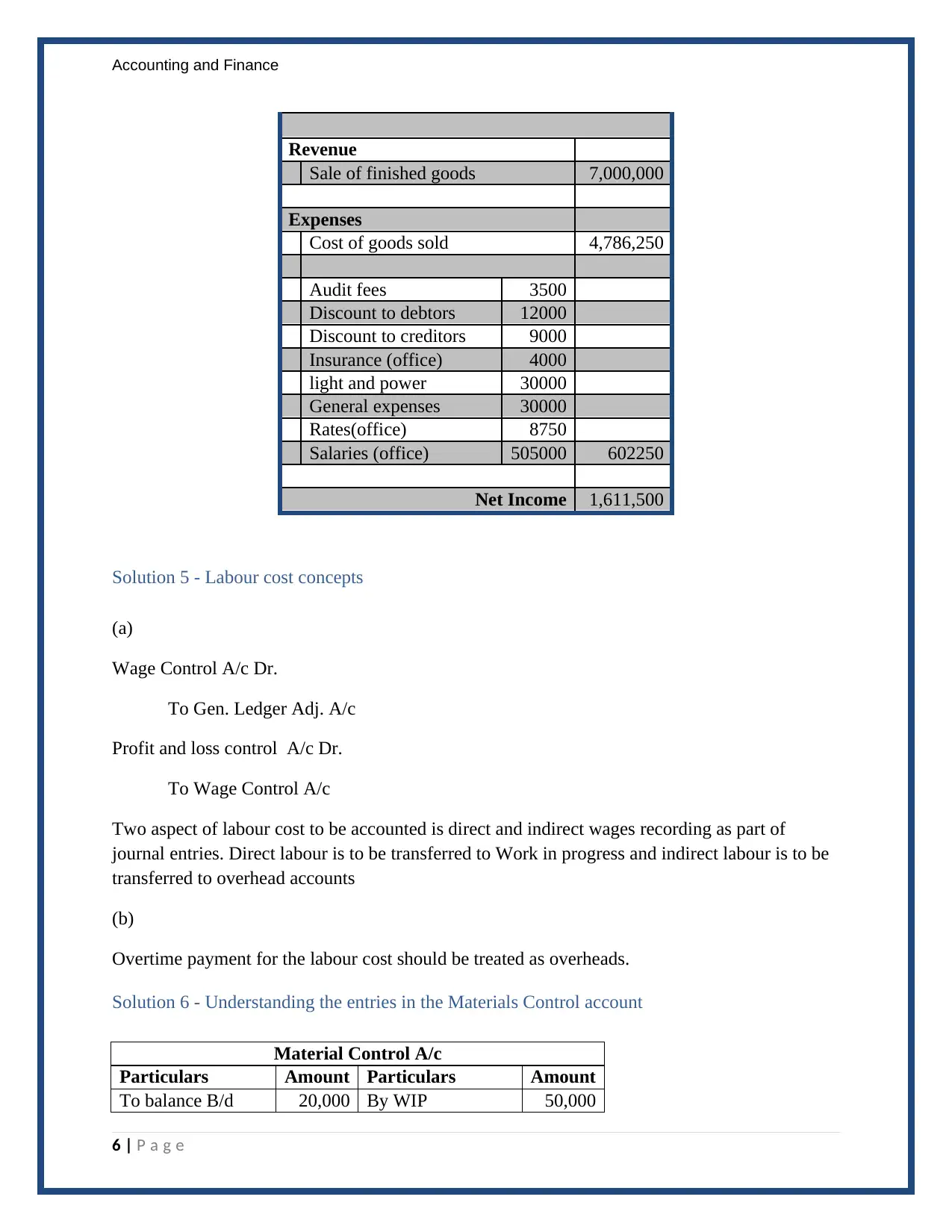

Accounting and Finance

Revenue

Sale of finished goods 7,000,000

Expenses

Cost of goods sold 4,786,250

Audit fees 3500

Discount to debtors 12000

Discount to creditors 9000

Insurance (office) 4000

light and power 30000

General expenses 30000

Rates(office) 8750

Salaries (office) 505000 602250

Net Income 1,611,500

Solution 5 - Labour cost concepts

(a)

Wage Control A/c Dr.

To Gen. Ledger Adj. A/c

Profit and loss control A/c Dr.

To Wage Control A/c

Two aspect of labour cost to be accounted is direct and indirect wages recording as part of

journal entries. Direct labour is to be transferred to Work in progress and indirect labour is to be

transferred to overhead accounts

(b)

Overtime payment for the labour cost should be treated as overheads.

Solution 6 - Understanding the entries in the Materials Control account

Material Control A/c

Particulars Amount Particulars Amount

To balance B/d 20,000 By WIP 50,000

6 | P a g e

Revenue

Sale of finished goods 7,000,000

Expenses

Cost of goods sold 4,786,250

Audit fees 3500

Discount to debtors 12000

Discount to creditors 9000

Insurance (office) 4000

light and power 30000

General expenses 30000

Rates(office) 8750

Salaries (office) 505000 602250

Net Income 1,611,500

Solution 5 - Labour cost concepts

(a)

Wage Control A/c Dr.

To Gen. Ledger Adj. A/c

Profit and loss control A/c Dr.

To Wage Control A/c

Two aspect of labour cost to be accounted is direct and indirect wages recording as part of

journal entries. Direct labour is to be transferred to Work in progress and indirect labour is to be

transferred to overhead accounts

(b)

Overtime payment for the labour cost should be treated as overheads.

Solution 6 - Understanding the entries in the Materials Control account

Material Control A/c

Particulars Amount Particulars Amount

To balance B/d 20,000 By WIP 50,000

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

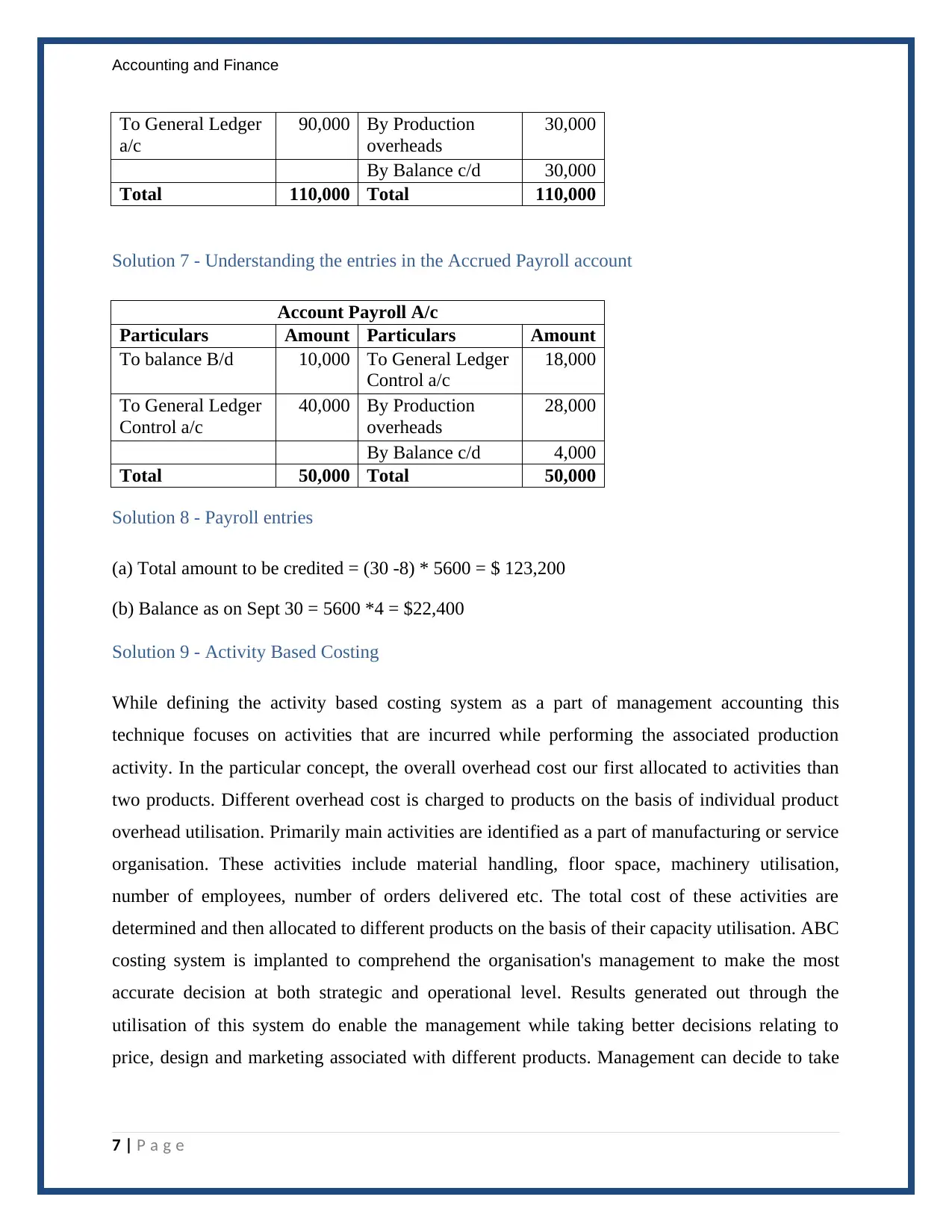

Accounting and Finance

To General Ledger

a/c

90,000 By Production

overheads

30,000

By Balance c/d 30,000

Total 110,000 Total 110,000

Solution 7 - Understanding the entries in the Accrued Payroll account

Account Payroll A/c

Particulars Amount Particulars Amount

To balance B/d 10,000 To General Ledger

Control a/c

18,000

To General Ledger

Control a/c

40,000 By Production

overheads

28,000

By Balance c/d 4,000

Total 50,000 Total 50,000

Solution 8 - Payroll entries

(a) Total amount to be credited = (30 -8) * 5600 = $ 123,200

(b) Balance as on Sept 30 = 5600 *4 = $22,400

Solution 9 - Activity Based Costing

While defining the activity based costing system as a part of management accounting this

technique focuses on activities that are incurred while performing the associated production

activity. In the particular concept, the overall overhead cost our first allocated to activities than

two products. Different overhead cost is charged to products on the basis of individual product

overhead utilisation. Primarily main activities are identified as a part of manufacturing or service

organisation. These activities include material handling, floor space, machinery utilisation,

number of employees, number of orders delivered etc. The total cost of these activities are

determined and then allocated to different products on the basis of their capacity utilisation. ABC

costing system is implanted to comprehend the organisation's management to make the most

accurate decision at both strategic and operational level. Results generated out through the

utilisation of this system do enable the management while taking better decisions relating to

price, design and marketing associated with different products. Management can decide to take

7 | P a g e

To General Ledger

a/c

90,000 By Production

overheads

30,000

By Balance c/d 30,000

Total 110,000 Total 110,000

Solution 7 - Understanding the entries in the Accrued Payroll account

Account Payroll A/c

Particulars Amount Particulars Amount

To balance B/d 10,000 To General Ledger

Control a/c

18,000

To General Ledger

Control a/c

40,000 By Production

overheads

28,000

By Balance c/d 4,000

Total 50,000 Total 50,000

Solution 8 - Payroll entries

(a) Total amount to be credited = (30 -8) * 5600 = $ 123,200

(b) Balance as on Sept 30 = 5600 *4 = $22,400

Solution 9 - Activity Based Costing

While defining the activity based costing system as a part of management accounting this

technique focuses on activities that are incurred while performing the associated production

activity. In the particular concept, the overall overhead cost our first allocated to activities than

two products. Different overhead cost is charged to products on the basis of individual product

overhead utilisation. Primarily main activities are identified as a part of manufacturing or service

organisation. These activities include material handling, floor space, machinery utilisation,

number of employees, number of orders delivered etc. The total cost of these activities are

determined and then allocated to different products on the basis of their capacity utilisation. ABC

costing system is implanted to comprehend the organisation's management to make the most

accurate decision at both strategic and operational level. Results generated out through the

utilisation of this system do enable the management while taking better decisions relating to

price, design and marketing associated with different products. Management can decide to take

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and Finance

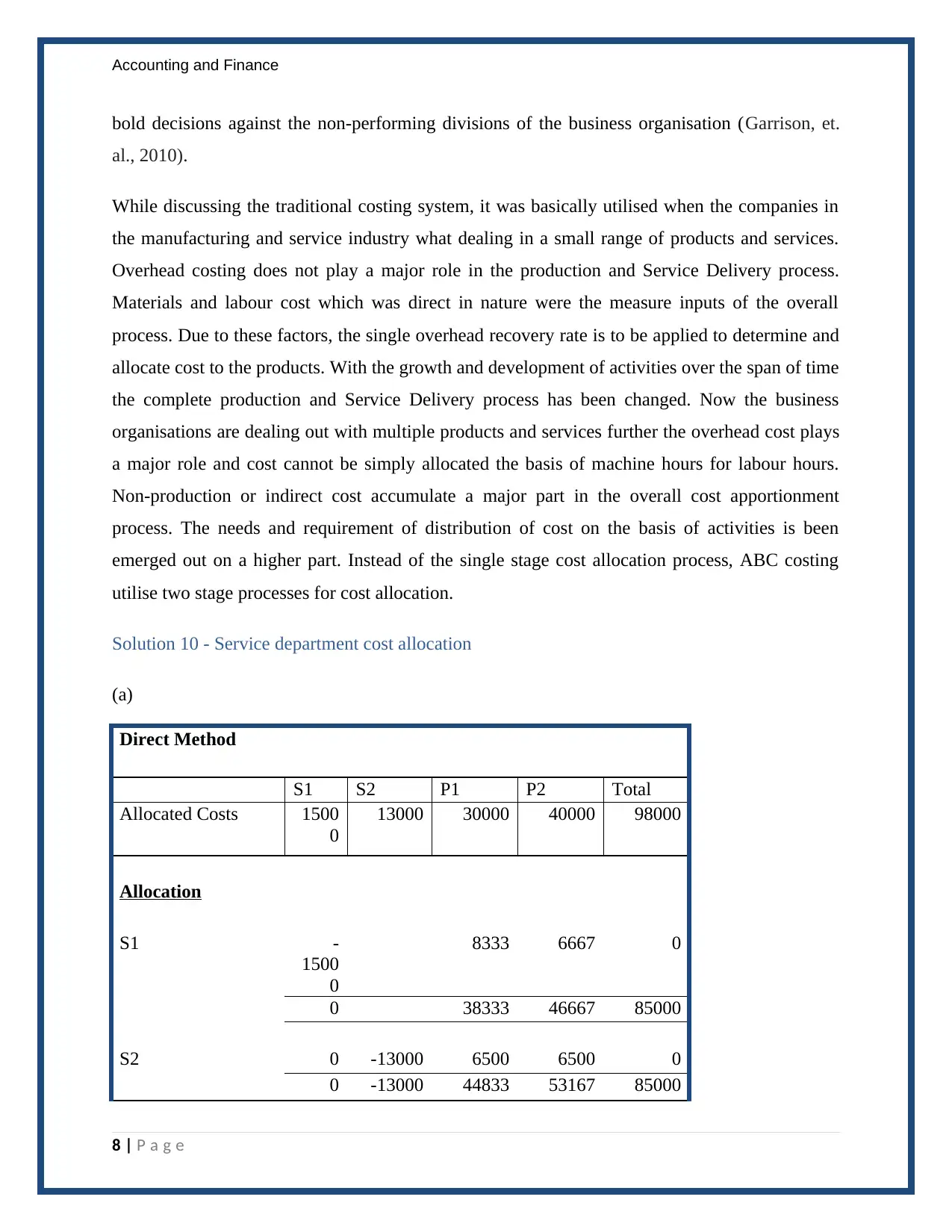

bold decisions against the non-performing divisions of the business organisation (Garrison, et.

al., 2010).

While discussing the traditional costing system, it was basically utilised when the companies in

the manufacturing and service industry what dealing in a small range of products and services.

Overhead costing does not play a major role in the production and Service Delivery process.

Materials and labour cost which was direct in nature were the measure inputs of the overall

process. Due to these factors, the single overhead recovery rate is to be applied to determine and

allocate cost to the products. With the growth and development of activities over the span of time

the complete production and Service Delivery process has been changed. Now the business

organisations are dealing out with multiple products and services further the overhead cost plays

a major role and cost cannot be simply allocated the basis of machine hours for labour hours.

Non-production or indirect cost accumulate a major part in the overall cost apportionment

process. The needs and requirement of distribution of cost on the basis of activities is been

emerged out on a higher part. Instead of the single stage cost allocation process, ABC costing

utilise two stage processes for cost allocation.

Solution 10 - Service department cost allocation

(a)

Direct Method

S1 S2 P1 P2 Total

Allocated Costs 1500

0

13000 30000 40000 98000

Allocation

S1 -

1500

0

8333 6667 0

0 38333 46667 85000

S2 0 -13000 6500 6500 0

0 -13000 44833 53167 85000

8 | P a g e

bold decisions against the non-performing divisions of the business organisation (Garrison, et.

al., 2010).

While discussing the traditional costing system, it was basically utilised when the companies in

the manufacturing and service industry what dealing in a small range of products and services.

Overhead costing does not play a major role in the production and Service Delivery process.

Materials and labour cost which was direct in nature were the measure inputs of the overall

process. Due to these factors, the single overhead recovery rate is to be applied to determine and

allocate cost to the products. With the growth and development of activities over the span of time

the complete production and Service Delivery process has been changed. Now the business

organisations are dealing out with multiple products and services further the overhead cost plays

a major role and cost cannot be simply allocated the basis of machine hours for labour hours.

Non-production or indirect cost accumulate a major part in the overall cost apportionment

process. The needs and requirement of distribution of cost on the basis of activities is been

emerged out on a higher part. Instead of the single stage cost allocation process, ABC costing

utilise two stage processes for cost allocation.

Solution 10 - Service department cost allocation

(a)

Direct Method

S1 S2 P1 P2 Total

Allocated Costs 1500

0

13000 30000 40000 98000

Allocation

S1 -

1500

0

8333 6667 0

0 38333 46667 85000

S2 0 -13000 6500 6500 0

0 -13000 44833 53167 85000

8 | P a g e

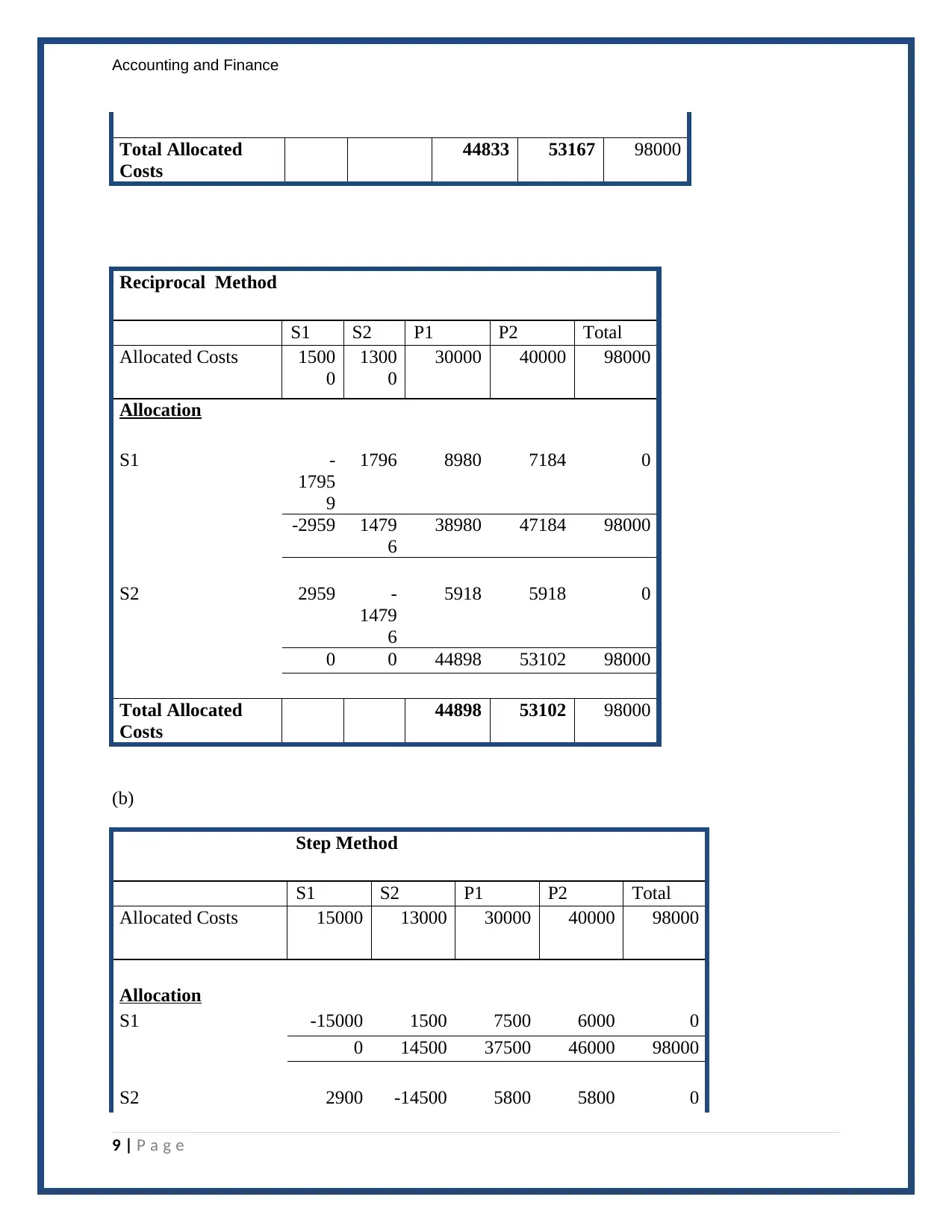

Accounting and Finance

Total Allocated

Costs

44833 53167 98000

Reciprocal Method

S1 S2 P1 P2 Total

Allocated Costs 1500

0

1300

0

30000 40000 98000

Allocation

S1 -

1795

9

1796 8980 7184 0

-2959 1479

6

38980 47184 98000

S2 2959 -

1479

6

5918 5918 0

0 0 44898 53102 98000

Total Allocated

Costs

44898 53102 98000

(b)

Step Method

S1 S2 P1 P2 Total

Allocated Costs 15000 13000 30000 40000 98000

Allocation

S1 -15000 1500 7500 6000 0

0 14500 37500 46000 98000

S2 2900 -14500 5800 5800 0

9 | P a g e

Total Allocated

Costs

44833 53167 98000

Reciprocal Method

S1 S2 P1 P2 Total

Allocated Costs 1500

0

1300

0

30000 40000 98000

Allocation

S1 -

1795

9

1796 8980 7184 0

-2959 1479

6

38980 47184 98000

S2 2959 -

1479

6

5918 5918 0

0 0 44898 53102 98000

Total Allocated

Costs

44898 53102 98000

(b)

Step Method

S1 S2 P1 P2 Total

Allocated Costs 15000 13000 30000 40000 98000

Allocation

S1 -15000 1500 7500 6000 0

0 14500 37500 46000 98000

S2 2900 -14500 5800 5800 0

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting and Finance

2900 0 43300 51800 98000

S1 -2900 290 1450 1160 0

0 290 44750 52960 98000

S2 58 -290 116 116 0

58 0 44866 53076 98000

S1 -58 6 29 23 0

0 6 44895 53099 98000

S2 1 -6 2 2 0

1 0 44897 53102 98000

S1 -1 0 1 0 0

0 0 44898 53102 98000

S2 0 0 0 0 0

0 0 44898 53102 98000

Total Allocated

Costs

44898 53102 98000

(c) Reciprocal Method

S1 X = 15,000 + 0.20 Y

S2 Y = 13,000 + 0.10 Y

X = 15,000 + 0.2 (13,000 +0.1 X)

X = 17,600 + 0.02 X

0.98 X = 17,600

X = $ 17959

Y = $ 14796

10 | P a g e

2900 0 43300 51800 98000

S1 -2900 290 1450 1160 0

0 290 44750 52960 98000

S2 58 -290 116 116 0

58 0 44866 53076 98000

S1 -58 6 29 23 0

0 6 44895 53099 98000

S2 1 -6 2 2 0

1 0 44897 53102 98000

S1 -1 0 1 0 0

0 0 44898 53102 98000

S2 0 0 0 0 0

0 0 44898 53102 98000

Total Allocated

Costs

44898 53102 98000

(c) Reciprocal Method

S1 X = 15,000 + 0.20 Y

S2 Y = 13,000 + 0.10 Y

X = 15,000 + 0.2 (13,000 +0.1 X)

X = 17,600 + 0.02 X

0.98 X = 17,600

X = $ 17959

Y = $ 14796

10 | P a g e

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.