Management Accounting for Costs and Control Assignment Analysis

VerifiedAdded on 2021/05/31

|26

|2430

|29

Homework Assignment

AI Summary

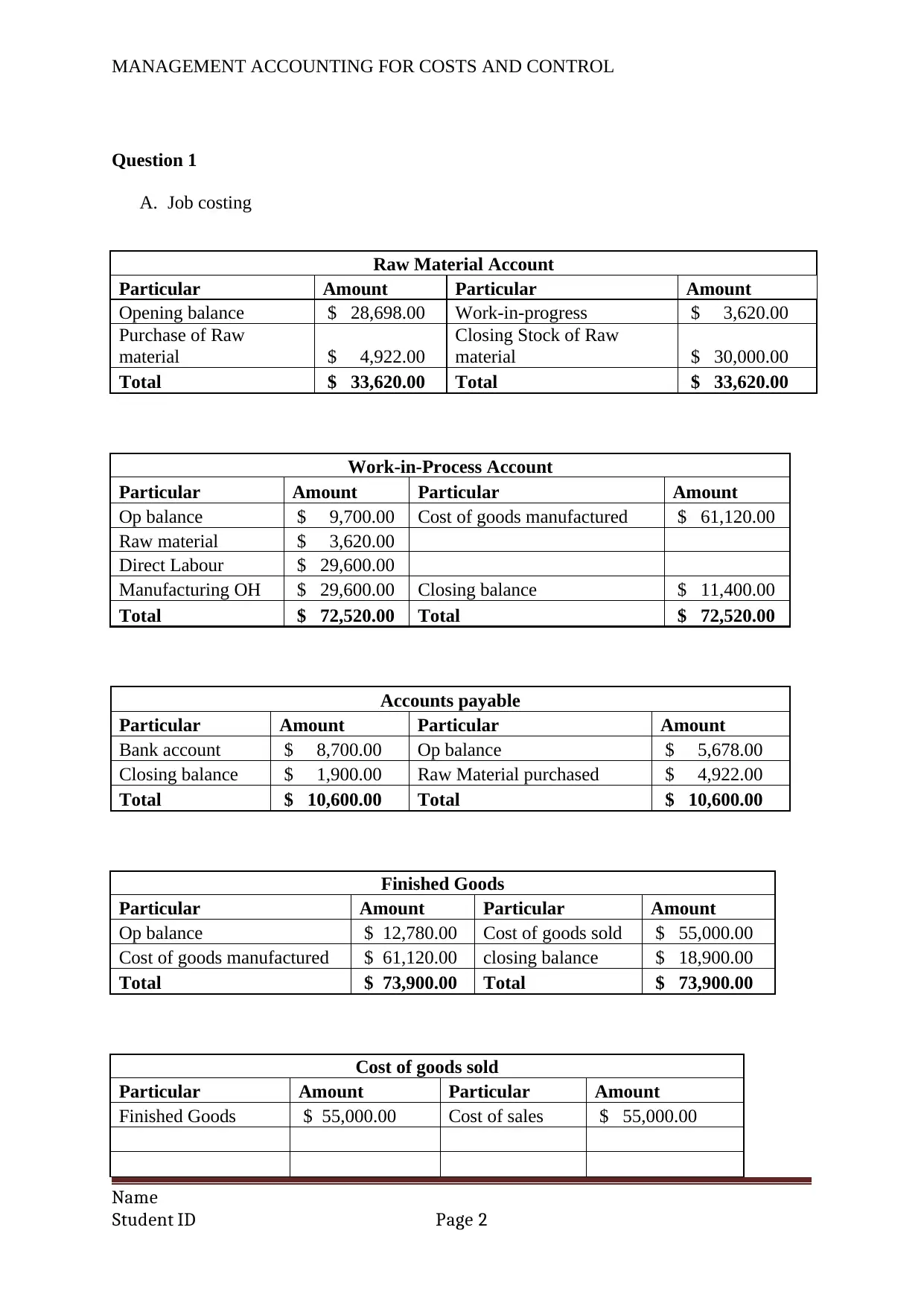

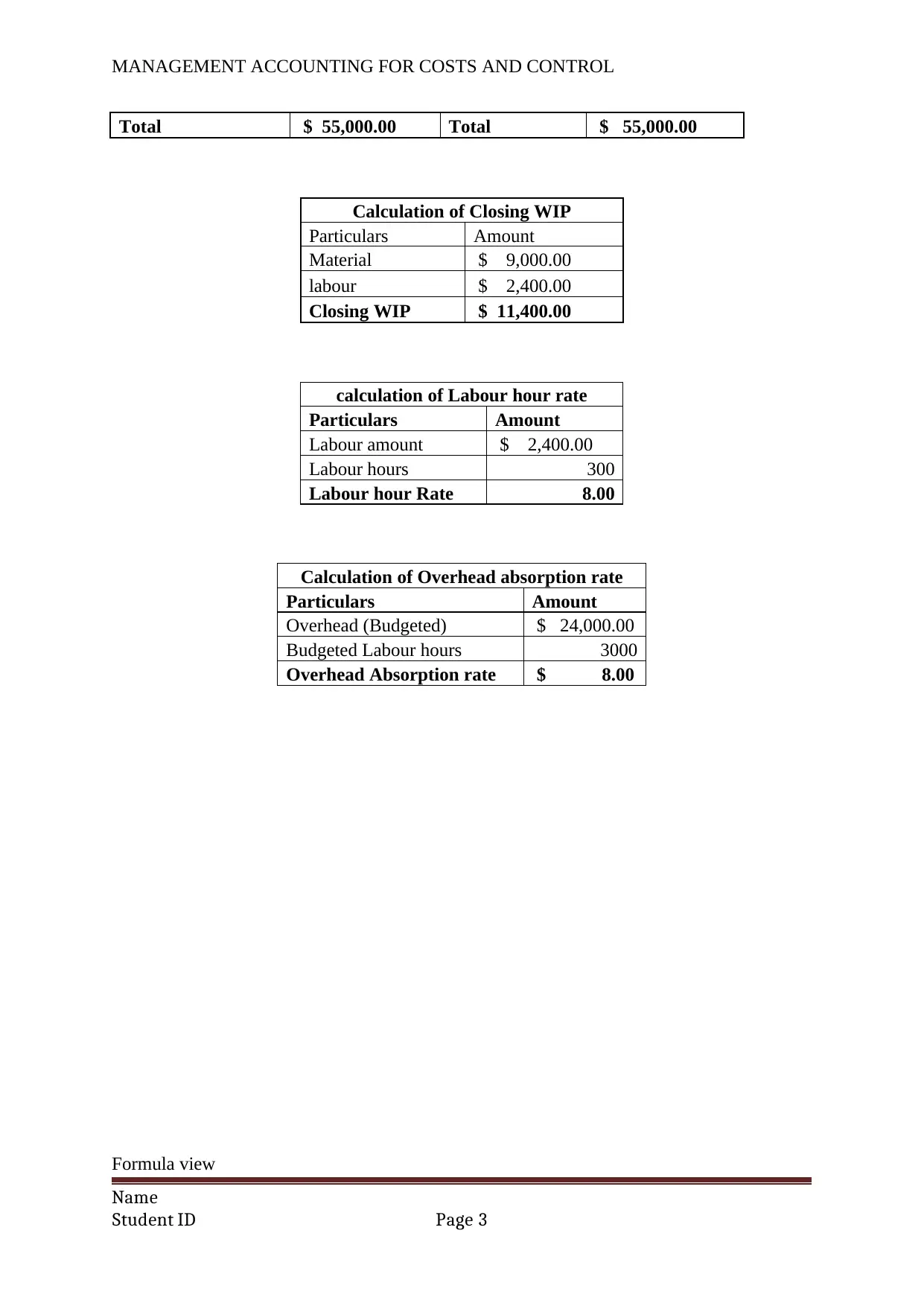

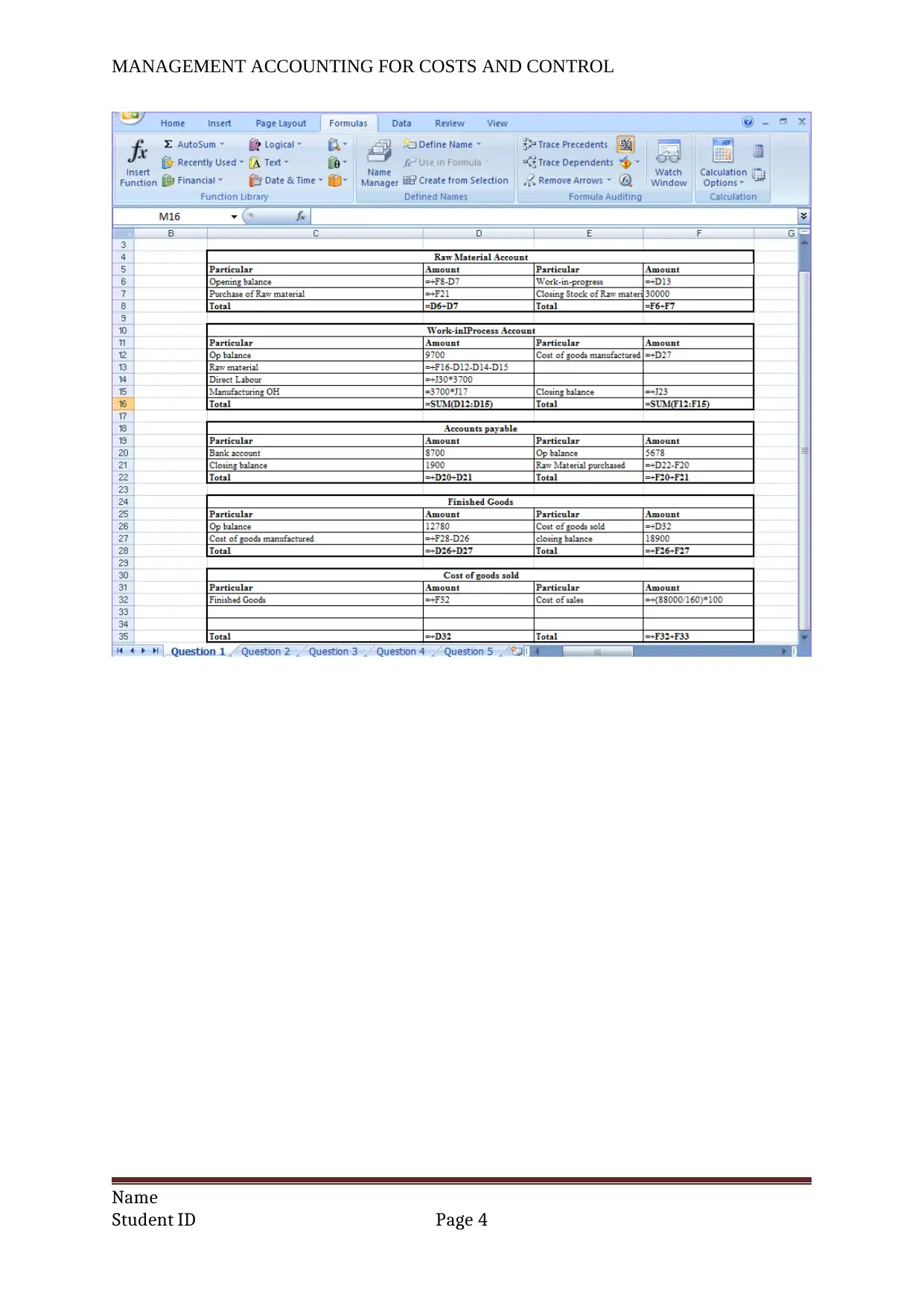

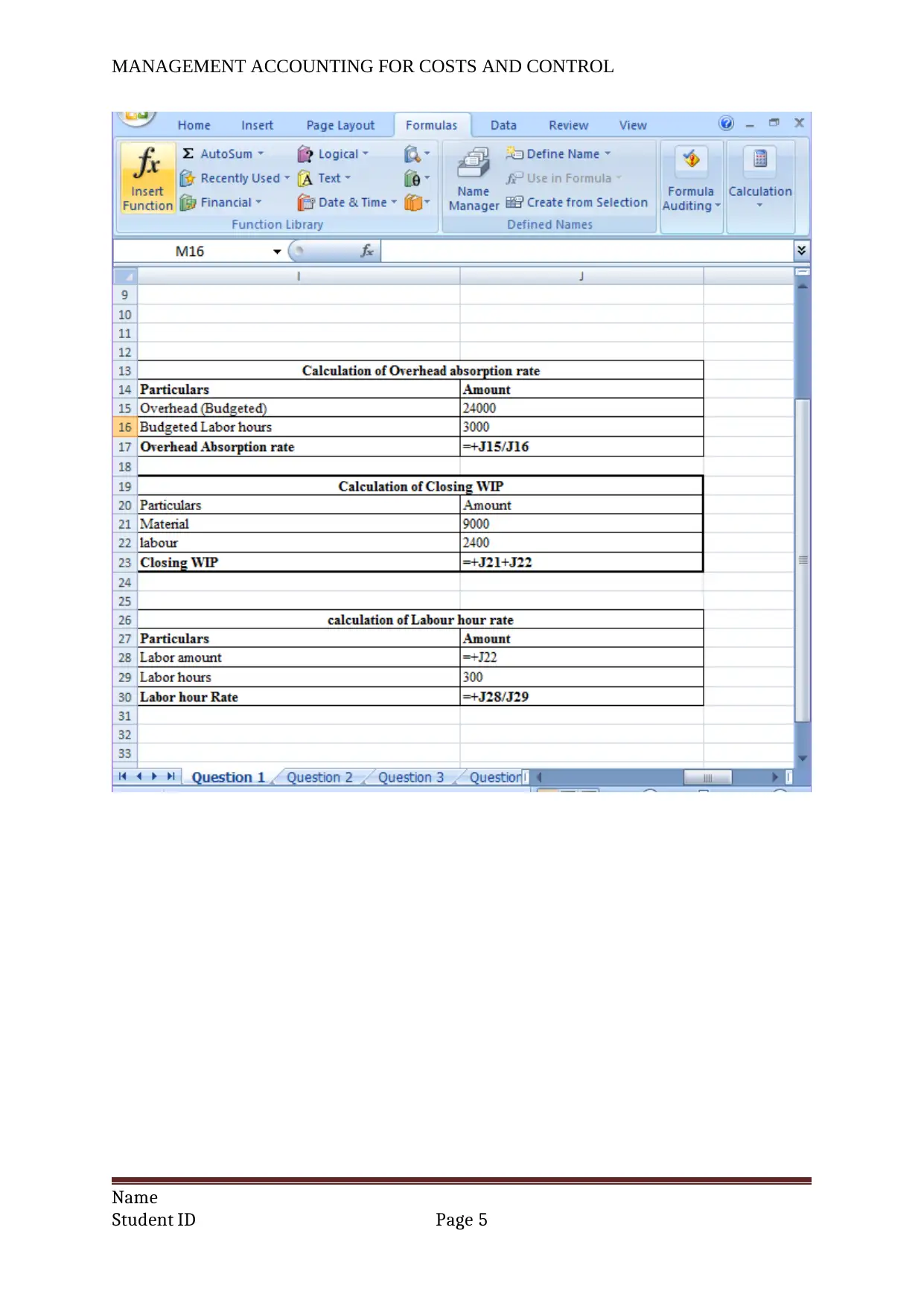

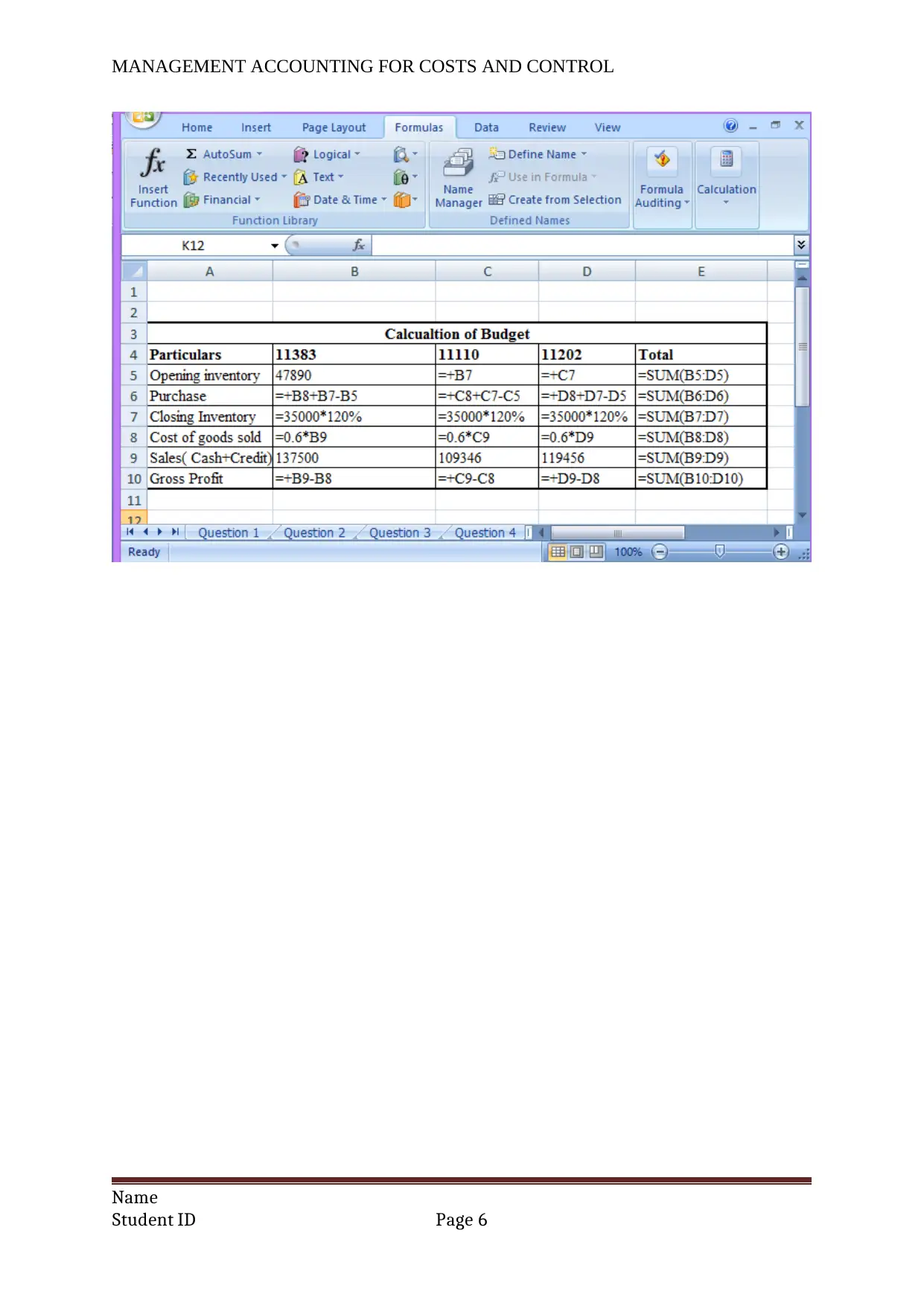

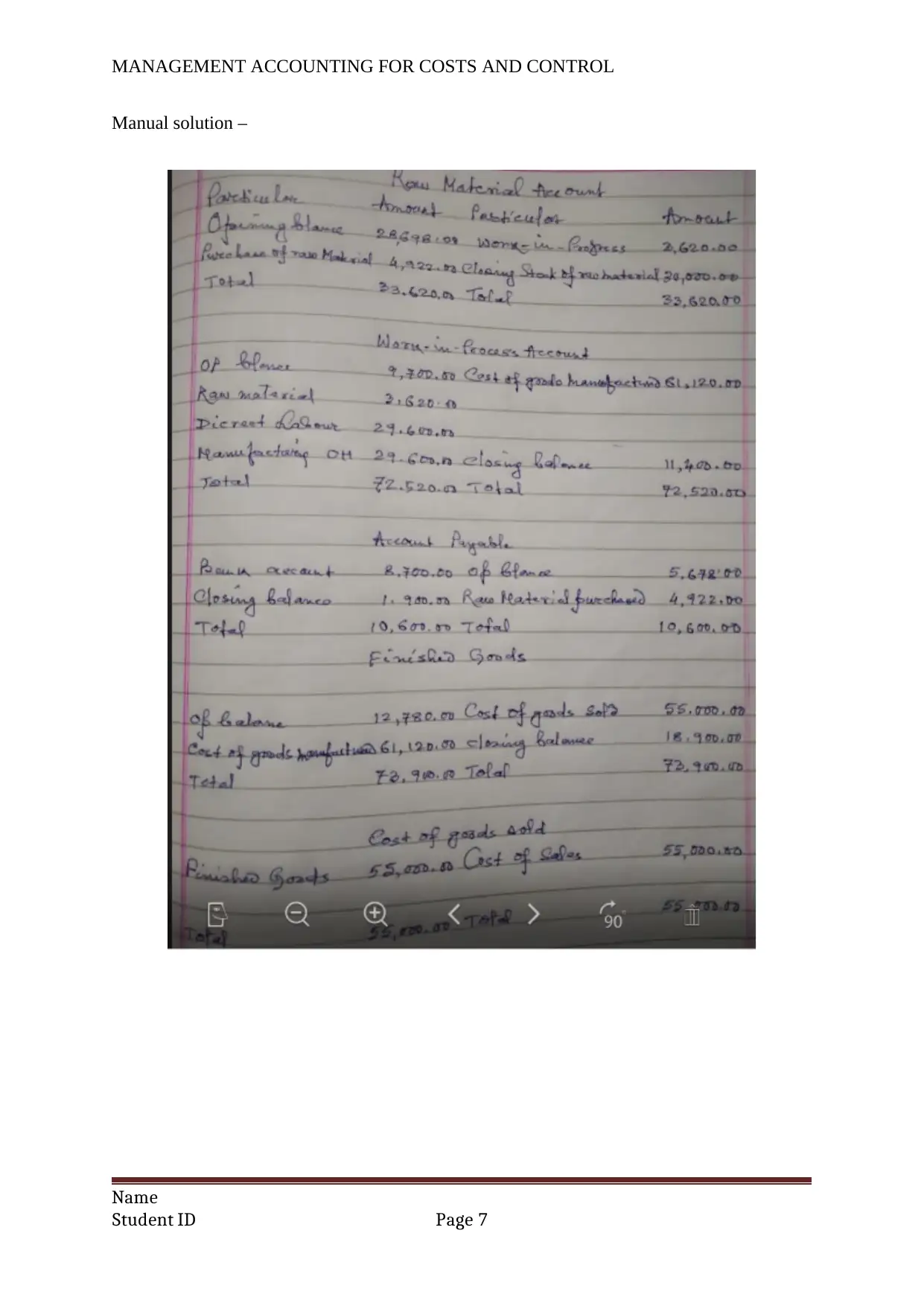

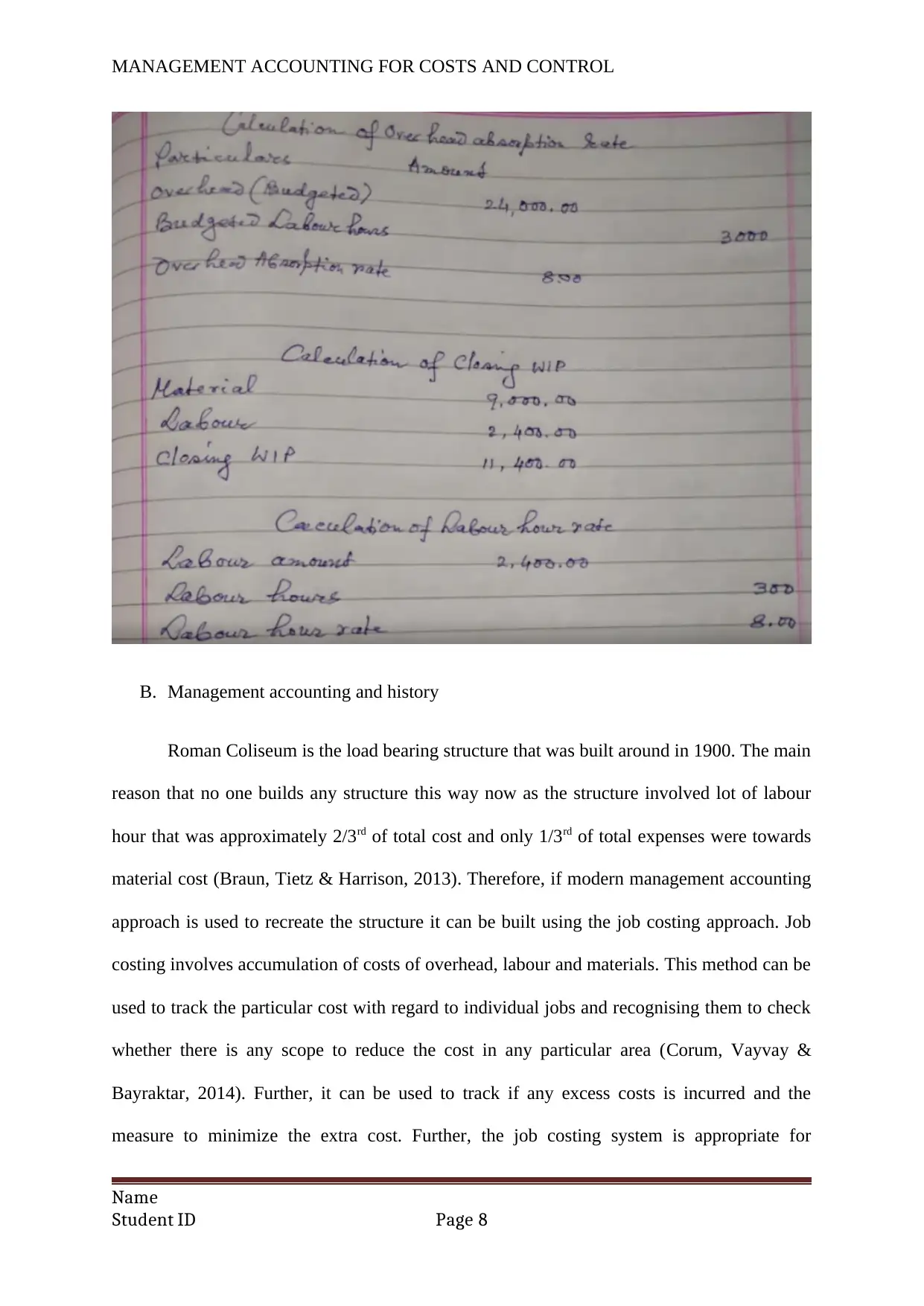

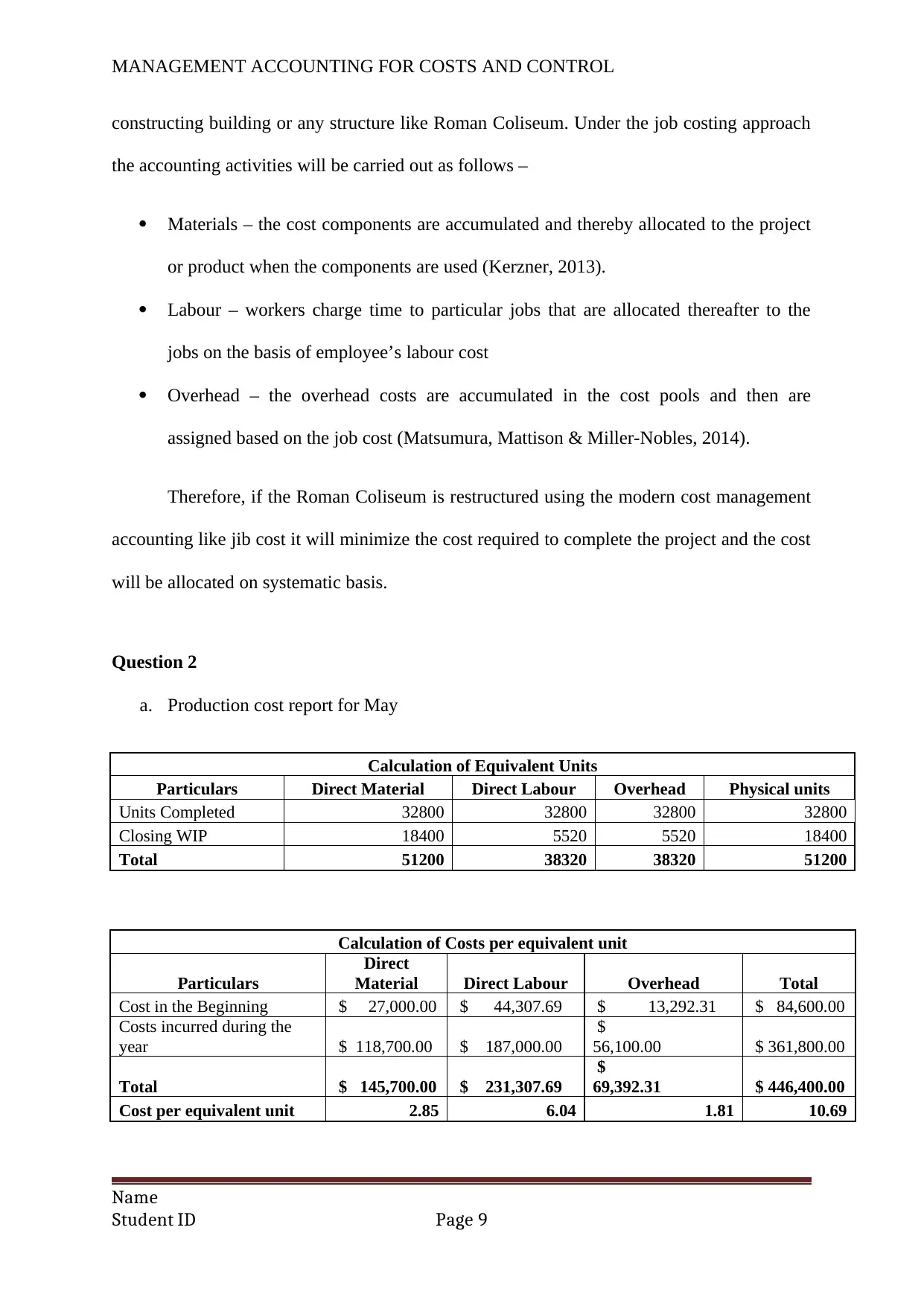

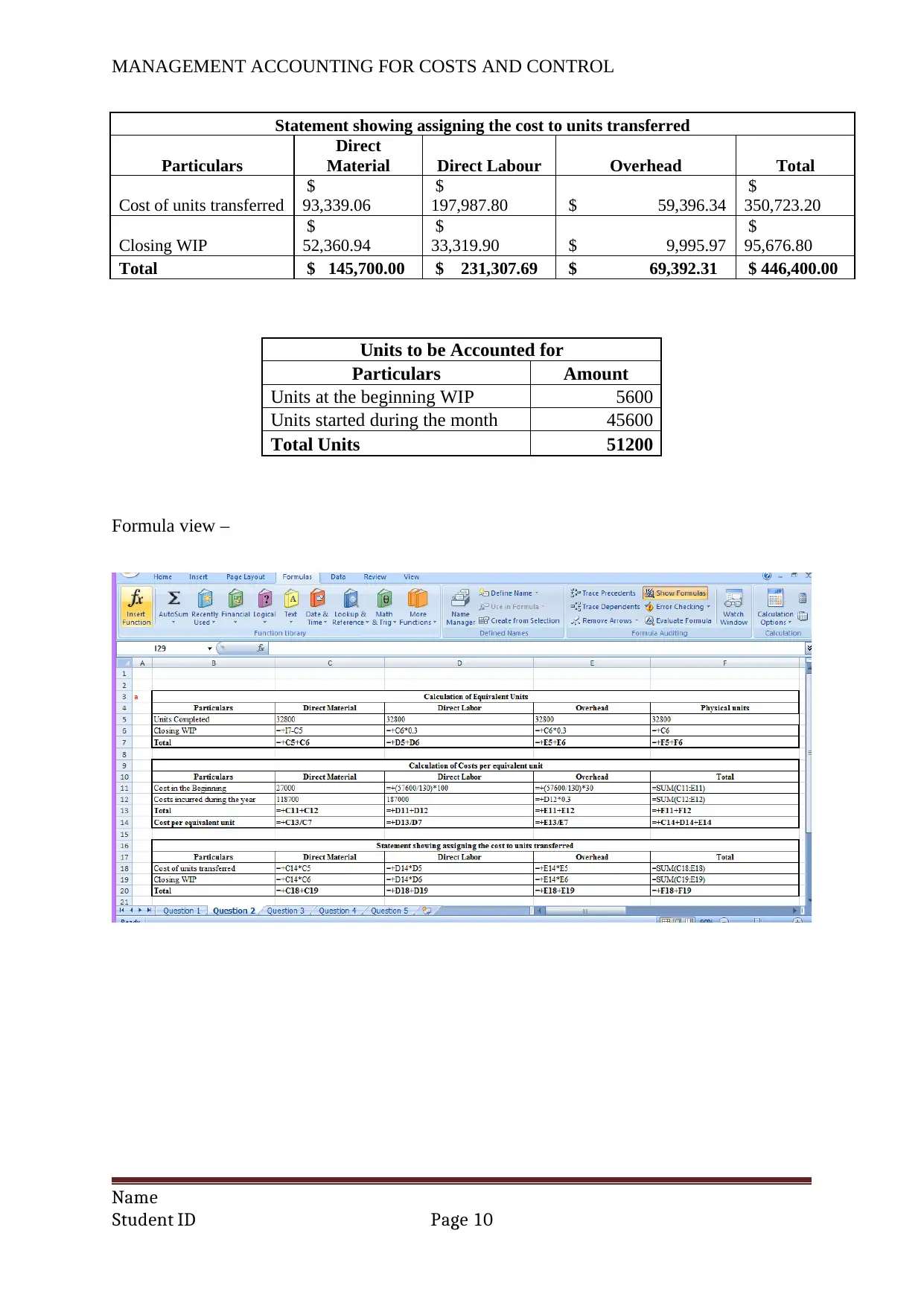

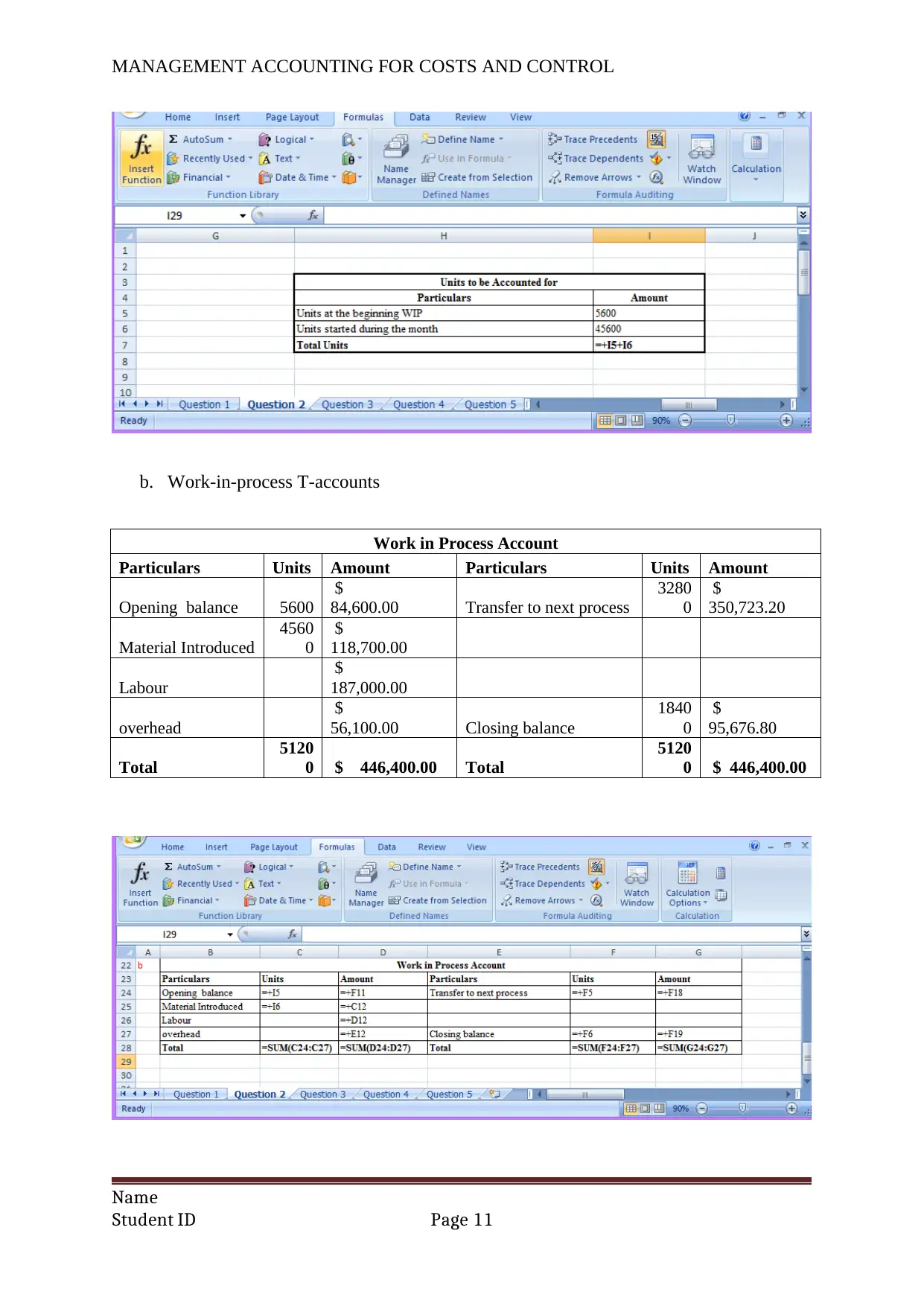

This document presents a comprehensive solution to a management accounting assignment, covering key areas such as job costing, production cost reports, and variance analysis. The solution begins with a detailed job costing problem, including the creation of raw material, work-in-process, accounts payable, finished goods, and cost of goods sold accounts, along with relevant calculations. The assignment then proceeds to a production cost report, calculating equivalent units and costs per equivalent unit, and assigning costs to units transferred and work-in-process. A profit analysis for different product grades is also included, determining the optimal course of action for further processing. Variance analysis is performed, calculating material price and usage variances, as well as labor rate variances. Finally, a budget is created, analyzing costs across different periods. The assignment incorporates formula views and manual solutions to aid understanding and provides a detailed discussion of variance analysis and budgeting processes. The document is a valuable resource for students studying management accounting.

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.