Management Accounting Report: Planning Tools and Financial Reporting

VerifiedAdded on 2023/01/11

|22

|6302

|52

Report

AI Summary

This report provides a comprehensive overview of management accounting, exploring various systems and techniques. It begins by defining management accounting and outlining its essential requirements, including different management styles, organizational structures, and the importance of information. The report then delves into different management accounting reporting methods, such as debtors/accounts receivable aging reports, departmental reports, and performance reports. It further examines the benefits and applications of specific systems like cost accounting, job costing, and inventory management within the context of Cream Ltd. The core of the report involves calculating costs using marginal and absorption costing methods to prepare income statements for Cream Ltd. It then explores the use of planning tools, particularly for budgetary control, discussing their advantages and disadvantages. Finally, the report analyzes how organizations can use management accounting to respond to financial problems, comparing different approaches and evaluating how these can lead to sustainable success. The report includes detailed calculations, financial statements, and practical applications, making it a valuable resource for understanding management accounting principles and their practical implementation.

MANAGEMENT

ACCOUNTING

| P a g e

ACCOUNTING

| P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

LO1. Demonstrate an understanding of management accounting systems.....................................4

P1. Explain management accounting and give the essential requirements of different types of

management accounting systems.................................................................................................4

P2. Explain different methods used for management accounting reporting................................6

M1. Evaluate the benefits of management accounting systems and their application within an

organizational context..................................................................................................................7

LO2. Explain the use of planning tools used in Management Accounting.....................................8

P3. Calculate costs using appropriate techniques of cost analysis to prepare income statement

using marginal and absorption costs............................................................................................8

M2. Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents...................................................................................................11

LO3. Explain the use of planning tools used in Management Accounting...................................12

P4. Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.......................................................................................................................12

M3. Analyze the use of different planning tools and their application for preparing budgets

and forecasts..............................................................................................................................15

LO4. Compare ways in which organizations could use Management Accounting to respond to

Financial Problems........................................................................................................................16

P5. Compare how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................16

M4. Analyze how, in responding to financial problems, management accounting can lead

organizations to sustainable success..........................................................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

| P a g e

INTRODUCTION...........................................................................................................................3

LO1. Demonstrate an understanding of management accounting systems.....................................4

P1. Explain management accounting and give the essential requirements of different types of

management accounting systems.................................................................................................4

P2. Explain different methods used for management accounting reporting................................6

M1. Evaluate the benefits of management accounting systems and their application within an

organizational context..................................................................................................................7

LO2. Explain the use of planning tools used in Management Accounting.....................................8

P3. Calculate costs using appropriate techniques of cost analysis to prepare income statement

using marginal and absorption costs............................................................................................8

M2. Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents...................................................................................................11

LO3. Explain the use of planning tools used in Management Accounting...................................12

P4. Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.......................................................................................................................12

M3. Analyze the use of different planning tools and their application for preparing budgets

and forecasts..............................................................................................................................15

LO4. Compare ways in which organizations could use Management Accounting to respond to

Financial Problems........................................................................................................................16

P5. Compare how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................16

M4. Analyze how, in responding to financial problems, management accounting can lead

organizations to sustainable success..........................................................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

| P a g e

| P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The Management accounting is an arrangement of bookkeeping that causes the board to play out their

capacities all the more productively. At the end of the day, the term the executives bookkeeping is utilized

to give bookkeeping data to the board exercises, for example, arranging, association, administration,

control and dynamic, and so on. Along these lines, the administration account is centered on improving

the productivity of the administration. It does this by furnishing various degrees of the board with the data

required for good dynamic.

This task report dependent on better comprehension of the idea Management bookkeeping; the different

fundamental apparatuses of the executives bookkeeping strategies will investigate the extent of this most

recent money related idea. Estimation of pay proclamation through negligible and retention costing

techniques will upgrade the fundamental contrast among two and furthermore uncovers the purpose for

distinction in both net benefit figure. The chosen organization for this particular project is Cream

Ltd. which sells ice creams, doughnuts and waffles.

| P a g e

The Management accounting is an arrangement of bookkeeping that causes the board to play out their

capacities all the more productively. At the end of the day, the term the executives bookkeeping is utilized

to give bookkeeping data to the board exercises, for example, arranging, association, administration,

control and dynamic, and so on. Along these lines, the administration account is centered on improving

the productivity of the administration. It does this by furnishing various degrees of the board with the data

required for good dynamic.

This task report dependent on better comprehension of the idea Management bookkeeping; the different

fundamental apparatuses of the executives bookkeeping strategies will investigate the extent of this most

recent money related idea. Estimation of pay proclamation through negligible and retention costing

techniques will upgrade the fundamental contrast among two and furthermore uncovers the purpose for

distinction in both net benefit figure. The chosen organization for this particular project is Cream

Ltd. which sells ice creams, doughnuts and waffles.

| P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO1. Demonstrate an understanding of management accounting systems

P1. Explain management accounting and give the essential requirements of

different types of management accounting systems

Management accounting: In management accounting or managerial accounting, managers use provisions

of accounting information to better inform themselves before making decisions in the affairs of their

organizations, which assist in the performance of their management and control functions; calculating

techniques to provide effective accounting information for business managers inside the company. For

financial accounting this includes management planning, adjustments between departments, corporate

budgets used for control activities, direct cost accounting, standard cost calculations, and more. It is being

reorganized under Management Information System (MIS) with the introduction of computers (Kaplan

and Atkinson, 2015).

Benefits of management accounting to an organization:

Management accounting has many benefits. Through an effective management accounting system, it is

possible to enhance the overall performance of the company (Burns and Vaivio, 2001). These benefits are

discussed below:

Advanced technology and features:

Cost Transparency

Flexibility and independence

Marginal Cost

Company efficiency

Bar of profitability

Different types of management accounting:

Managerial accountant uses different types of management accounting techniques to solve financial

problems of an organization; these techniques are discussed below:

Cost accounting system: The cost accounting system is only a part of the full accounting system. This

method is established to obtain cost related information. With this help the cost of product services and

various processes can be controlled. At present, cost accounting has become so important that it is not

possible to develop in this era of competition. Every producer must have knowledge about cost

| P a g e

P1. Explain management accounting and give the essential requirements of

different types of management accounting systems

Management accounting: In management accounting or managerial accounting, managers use provisions

of accounting information to better inform themselves before making decisions in the affairs of their

organizations, which assist in the performance of their management and control functions; calculating

techniques to provide effective accounting information for business managers inside the company. For

financial accounting this includes management planning, adjustments between departments, corporate

budgets used for control activities, direct cost accounting, standard cost calculations, and more. It is being

reorganized under Management Information System (MIS) with the introduction of computers (Kaplan

and Atkinson, 2015).

Benefits of management accounting to an organization:

Management accounting has many benefits. Through an effective management accounting system, it is

possible to enhance the overall performance of the company (Burns and Vaivio, 2001). These benefits are

discussed below:

Advanced technology and features:

Cost Transparency

Flexibility and independence

Marginal Cost

Company efficiency

Bar of profitability

Different types of management accounting:

Managerial accountant uses different types of management accounting techniques to solve financial

problems of an organization; these techniques are discussed below:

Cost accounting system: The cost accounting system is only a part of the full accounting system. This

method is established to obtain cost related information. With this help the cost of product services and

various processes can be controlled. At present, cost accounting has become so important that it is not

possible to develop in this era of competition. Every producer must have knowledge about cost

| P a g e

accounting and must keep the cost accounts systematically in order to maintain his accountability, as a

result of which he can make maximum profit on the goods he produces in the era of competition.

Job costing system: A job costing system includes the way to collect cost data associated with a

particular production or administration operation. This data may be required to present cost data to a

customer under an agreement in which expenses are reimbursed. Likewise, the data is useful for

determining the accuracy of an organization's scoreboard, which should include an option to provide cost

estimates that take reasonable advantage into account. The data can be used in the same way to calculate

the deductible costs for manufactured products (Horngren, Sundem, Elliott and Philbrick, 2002).

Inventory management system: An inventory management system is the combination of innovation

(equipment and programming) and methods and strategies that monitor the monitoring and support of

uploaded items, regardless of organizational resources, raw materials and a supply of these or complete

items suitable for transmission to final or final buyers.

Price optimization: The price optimization system is a scientific project that reveals how demand

changes at different levels of value and subsequently combines this information with cost data and

inventory levels to suggest costs which will improve the benefits. Presentation allows organizations to use

evaluation as a dramatic, often unusual, benefit change. Value optimization models can be used to

customize customer portfolio estimates by replicating the way focused customers manage value changes

with information-based scenarios. Given the multidimensional nature of predicting large numbers of

things in extremely powerful economic conditions, the emergence of results and knowledge helps drive

demand, generate and maintain demand creation of evaluation and promotion procedures, control of stock

levels and improvement of customer loyalty.

Explain the essential requirements associated with different management accounting systems

The main aim of the management accounting information is to use internal information’s available

through various accounting documents to support managerial accountants. Some of the essential

requirements associated with different management accounting systems have been discussed below:

1) Management style: Management style is the strategy adopted by manager or leader according to

essential requirement and situation face by business. Different circumstances require applying different

management style.

2) Organization structure: Organization structure refers to the arrangement of interrelations and

functions throughout the organization. The organization's management is determined overall based on the

| P a g e

result of which he can make maximum profit on the goods he produces in the era of competition.

Job costing system: A job costing system includes the way to collect cost data associated with a

particular production or administration operation. This data may be required to present cost data to a

customer under an agreement in which expenses are reimbursed. Likewise, the data is useful for

determining the accuracy of an organization's scoreboard, which should include an option to provide cost

estimates that take reasonable advantage into account. The data can be used in the same way to calculate

the deductible costs for manufactured products (Horngren, Sundem, Elliott and Philbrick, 2002).

Inventory management system: An inventory management system is the combination of innovation

(equipment and programming) and methods and strategies that monitor the monitoring and support of

uploaded items, regardless of organizational resources, raw materials and a supply of these or complete

items suitable for transmission to final or final buyers.

Price optimization: The price optimization system is a scientific project that reveals how demand

changes at different levels of value and subsequently combines this information with cost data and

inventory levels to suggest costs which will improve the benefits. Presentation allows organizations to use

evaluation as a dramatic, often unusual, benefit change. Value optimization models can be used to

customize customer portfolio estimates by replicating the way focused customers manage value changes

with information-based scenarios. Given the multidimensional nature of predicting large numbers of

things in extremely powerful economic conditions, the emergence of results and knowledge helps drive

demand, generate and maintain demand creation of evaluation and promotion procedures, control of stock

levels and improvement of customer loyalty.

Explain the essential requirements associated with different management accounting systems

The main aim of the management accounting information is to use internal information’s available

through various accounting documents to support managerial accountants. Some of the essential

requirements associated with different management accounting systems have been discussed below:

1) Management style: Management style is the strategy adopted by manager or leader according to

essential requirement and situation face by business. Different circumstances require applying different

management style.

2) Organization structure: Organization structure refers to the arrangement of interrelations and

functions throughout the organization. The organization's management is determined overall based on the

| P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organization's structure. The entire organizational system of an organization is the organization structure

that displays the relationships of the employees working in it.

3) Information: Information for management is mainly obtained from financial accounting and cost

accounting which helps managers to make budget, assess profit, determine value, decide capital

expenditure, etc. The administration must choose which data to use. Who requests the data and how it

will be necessary to negotiate the choice. As a result of these studies, data is collected. Source: Another

important fact is where the data will be collected. This can come from internal or external sources.

It is measured solely on light. Allocator: Not all policy data. Distinguish the law and provide another way;

Cc Accuracy: The amount of data is data. It gives any idea an idea. A policy that can recover the burden

of common law from the fact that stocking does not result (Bromwich and Bhimani, 2005).

P2. Explain different methods used for management accounting reporting

Management accounting reporting: The head of the company, from time to time, faces the problem of the

profitability of the company and decides for itself the question: is it profitable and should it continue. To

find answers to them, manager is engaged in the creation of cost and sales prices of goods, budget

planning, scheduling of responsibility centers, analysis of external environment and many other functions

designed to provide complete and transparent control over the organization; this practice is known as

management accounting reporting (Libby and Waterhouse, 1996).

Different methods of management accounting reports:

Management accounting reporting is not the concept which can apply by organization individually; it

requires application of different reporting methods according to requirements. These methods are

discussed below:

Debtors/Accounts receivable aging reports: Accounts receivable aging (sometimes called an account

receivable reconciliation) is the process of categorizing the amount owed by all customers, including the

period of time the unpaid balance is due (unpaid), thus your age, or Consider this information "old age"

(Hansen, Mowen and Guan, 2007). The standard categories for this type of report are:

Departmental reports: These reports are generated by different departments of the company according

to various product segments. This report consists of revenue and expenses of each department separately

and also shows any increase or decrease in total sales compare to previous session.

| P a g e

that displays the relationships of the employees working in it.

3) Information: Information for management is mainly obtained from financial accounting and cost

accounting which helps managers to make budget, assess profit, determine value, decide capital

expenditure, etc. The administration must choose which data to use. Who requests the data and how it

will be necessary to negotiate the choice. As a result of these studies, data is collected. Source: Another

important fact is where the data will be collected. This can come from internal or external sources.

It is measured solely on light. Allocator: Not all policy data. Distinguish the law and provide another way;

Cc Accuracy: The amount of data is data. It gives any idea an idea. A policy that can recover the burden

of common law from the fact that stocking does not result (Bromwich and Bhimani, 2005).

P2. Explain different methods used for management accounting reporting

Management accounting reporting: The head of the company, from time to time, faces the problem of the

profitability of the company and decides for itself the question: is it profitable and should it continue. To

find answers to them, manager is engaged in the creation of cost and sales prices of goods, budget

planning, scheduling of responsibility centers, analysis of external environment and many other functions

designed to provide complete and transparent control over the organization; this practice is known as

management accounting reporting (Libby and Waterhouse, 1996).

Different methods of management accounting reports:

Management accounting reporting is not the concept which can apply by organization individually; it

requires application of different reporting methods according to requirements. These methods are

discussed below:

Debtors/Accounts receivable aging reports: Accounts receivable aging (sometimes called an account

receivable reconciliation) is the process of categorizing the amount owed by all customers, including the

period of time the unpaid balance is due (unpaid), thus your age, or Consider this information "old age"

(Hansen, Mowen and Guan, 2007). The standard categories for this type of report are:

Departmental reports: These reports are generated by different departments of the company according

to various product segments. This report consists of revenue and expenses of each department separately

and also shows any increase or decrease in total sales compare to previous session.

| P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance reports: These reports uses financial KPIs that are ration analyses to compare its present

performance by taking either its own previous year report or by considering competitors performance

report.

Operating budget report: This budget report is based on the estimation cost of operating overheads and

expenses required for running the business. Working capital expenditures are considered in such type of

report of an organization.

M1. Evaluate the benefits of management accounting systems and their

application within an organizational context

Cost accounting system:

Benefit: Cost bookkeeping can be increasingly adaptable and explicit, particularly as far as cost sharing

and rundown estimating. Tragically, this review chance that expands multifaceted nature is getting

progressively costly and its viability is constrained to the ability and accuracy of the organization's

experts.

Application: Cost accounting can be applied in Creams Ltd. for the estimation of cost control, inventory,

and profits throughout the year.

Job costing system:

Benefit: The cost is collected by number in the package to determine the unit cost for each item; the cores

are separated by numbers. Common designs are average incubation costs for manufacturing plants that

produce residency packages, roll production lines, heating products, and components in pharmaceutical

companies.

Application: It applied by Creams Ltd. usually done within the factory. Each function behaves as a

separate entity, and the associated costs are recorded separately. This type of cost is suitable for printers,

machine tool makers, job casting, furniture manufacturing etc.

Inventory management system:

Benefit: The significance of stock administration, particularly for internet business and online deals logos,

can't be satisfactorily affirmed. Appropriate stock following permits the logo to finish arranges on

schedule and accurately. Record the executives is required to develop in organizations as the business

grows. With a vital arrangement that smoothes out the venture the executives and the board procedure,

| P a g e

performance by taking either its own previous year report or by considering competitors performance

report.

Operating budget report: This budget report is based on the estimation cost of operating overheads and

expenses required for running the business. Working capital expenditures are considered in such type of

report of an organization.

M1. Evaluate the benefits of management accounting systems and their

application within an organizational context

Cost accounting system:

Benefit: Cost bookkeeping can be increasingly adaptable and explicit, particularly as far as cost sharing

and rundown estimating. Tragically, this review chance that expands multifaceted nature is getting

progressively costly and its viability is constrained to the ability and accuracy of the organization's

experts.

Application: Cost accounting can be applied in Creams Ltd. for the estimation of cost control, inventory,

and profits throughout the year.

Job costing system:

Benefit: The cost is collected by number in the package to determine the unit cost for each item; the cores

are separated by numbers. Common designs are average incubation costs for manufacturing plants that

produce residency packages, roll production lines, heating products, and components in pharmaceutical

companies.

Application: It applied by Creams Ltd. usually done within the factory. Each function behaves as a

separate entity, and the associated costs are recorded separately. This type of cost is suitable for printers,

machine tool makers, job casting, furniture manufacturing etc.

Inventory management system:

Benefit: The significance of stock administration, particularly for internet business and online deals logos,

can't be satisfactorily affirmed. Appropriate stock following permits the logo to finish arranges on

schedule and accurately. Record the executives is required to develop in organizations as the business

grows. With a vital arrangement that smoothes out the venture the executives and the board procedure,

| P a g e

remembering continuous information for stock terms and conditions, organizations can recover the

advantages of stock administration.

Application: Creams Ltd can apply this techniques to reach at Economic Order Quantity (EOQ) which is

optimized cost paid by company to manage inventories.

LO2. Explain the use of planning tools used in Management Accounting

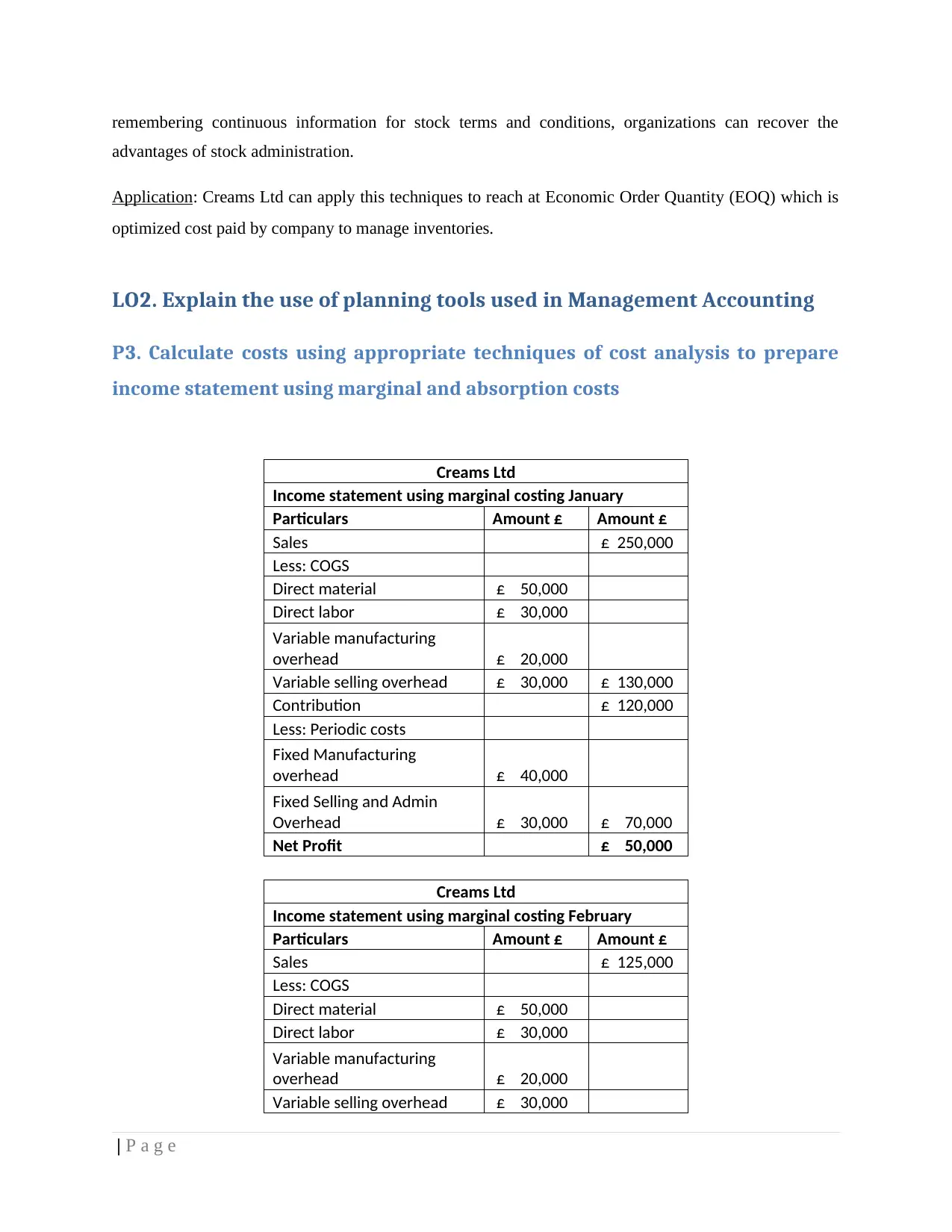

P3. Calculate costs using appropriate techniques of cost analysis to prepare

income statement using marginal and absorption costs

Creams Ltd

Income statement using marginal costing January

Particulars Amount £ Amount £

Sales £ 250,000

Less: COGS

Direct material £ 50,000

Direct labor £ 30,000

Variable manufacturing

overhead £ 20,000

Variable selling overhead £ 30,000 £ 130,000

Contribution £ 120,000

Less: Periodic costs

Fixed Manufacturing

overhead £ 40,000

Fixed Selling and Admin

Overhead £ 30,000 £ 70,000

Net Profit £ 50,000

Creams Ltd

Income statement using marginal costing February

Particulars Amount £ Amount £

Sales £ 125,000

Less: COGS

Direct material £ 50,000

Direct labor £ 30,000

Variable manufacturing

overhead £ 20,000

Variable selling overhead £ 30,000

| P a g e

advantages of stock administration.

Application: Creams Ltd can apply this techniques to reach at Economic Order Quantity (EOQ) which is

optimized cost paid by company to manage inventories.

LO2. Explain the use of planning tools used in Management Accounting

P3. Calculate costs using appropriate techniques of cost analysis to prepare

income statement using marginal and absorption costs

Creams Ltd

Income statement using marginal costing January

Particulars Amount £ Amount £

Sales £ 250,000

Less: COGS

Direct material £ 50,000

Direct labor £ 30,000

Variable manufacturing

overhead £ 20,000

Variable selling overhead £ 30,000 £ 130,000

Contribution £ 120,000

Less: Periodic costs

Fixed Manufacturing

overhead £ 40,000

Fixed Selling and Admin

Overhead £ 30,000 £ 70,000

Net Profit £ 50,000

Creams Ltd

Income statement using marginal costing February

Particulars Amount £ Amount £

Sales £ 125,000

Less: COGS

Direct material £ 50,000

Direct labor £ 30,000

Variable manufacturing

overhead £ 20,000

Variable selling overhead £ 30,000

| P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

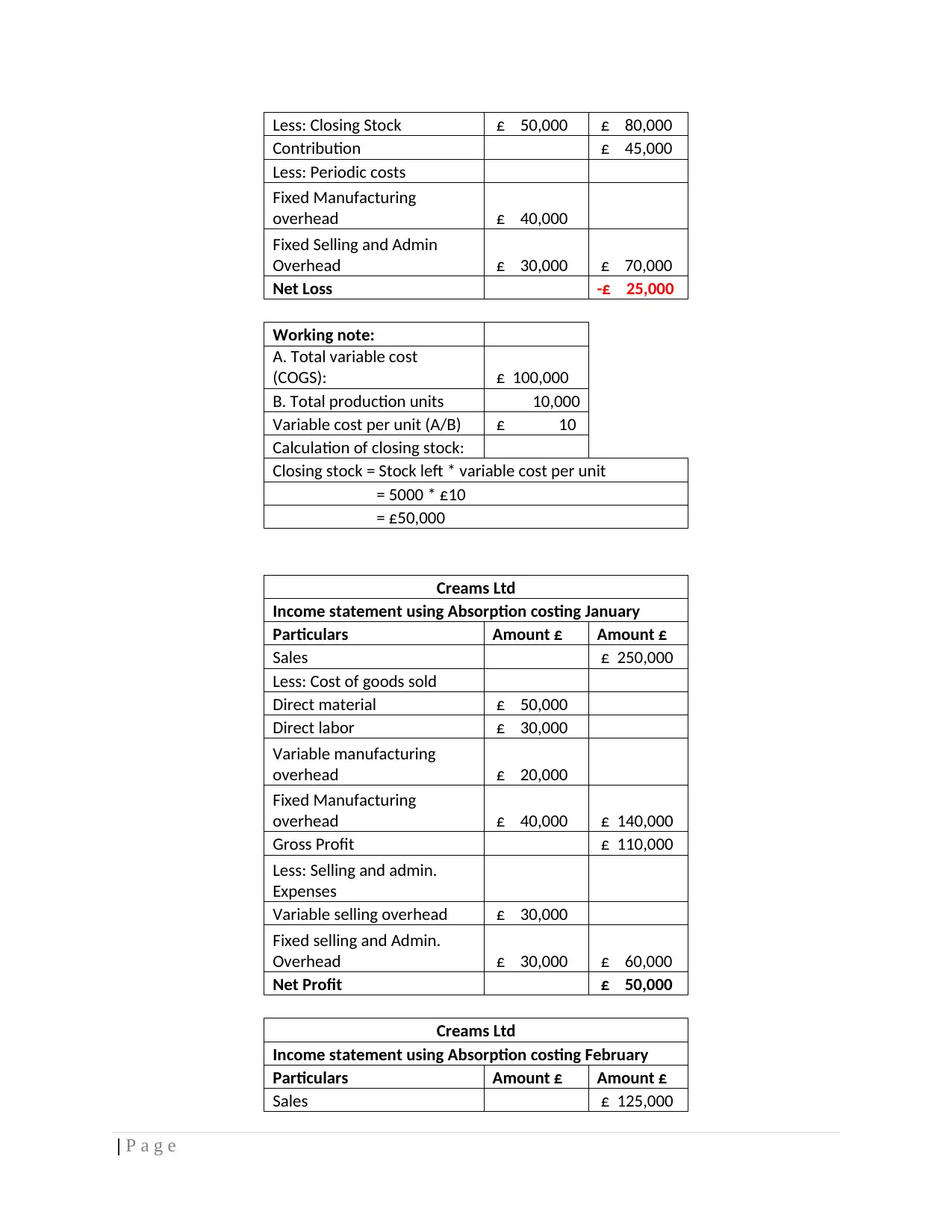

Less: Closing Stock £ 50,000 £ 80,000

Contribution £ 45,000

Less: Periodic costs

Fixed Manufacturing

overhead £ 40,000

Fixed Selling and Admin

Overhead £ 30,000 £ 70,000

Net Loss -£ 25,000

Working note:

A. Total variable cost

(COGS): £ 100,000

B. Total production units 10,000

Variable cost per unit (A/B) £ 10

Calculation of closing stock:

Closing stock = Stock left * variable cost per unit

= 5000 * £10

= £50,000

Creams Ltd

Income statement using Absorption costing January

Particulars Amount £ Amount £

Sales £ 250,000

Less: Cost of goods sold

Direct material £ 50,000

Direct labor £ 30,000

Variable manufacturing

overhead £ 20,000

Fixed Manufacturing

overhead £ 40,000 £ 140,000

Gross Profit £ 110,000

Less: Selling and admin.

Expenses

Variable selling overhead £ 30,000

Fixed selling and Admin.

Overhead £ 30,000 £ 60,000

Net Profit £ 50,000

Creams Ltd

Income statement using Absorption costing February

Particulars Amount £ Amount £

Sales £ 125,000

| P a g e

Contribution £ 45,000

Less: Periodic costs

Fixed Manufacturing

overhead £ 40,000

Fixed Selling and Admin

Overhead £ 30,000 £ 70,000

Net Loss -£ 25,000

Working note:

A. Total variable cost

(COGS): £ 100,000

B. Total production units 10,000

Variable cost per unit (A/B) £ 10

Calculation of closing stock:

Closing stock = Stock left * variable cost per unit

= 5000 * £10

= £50,000

Creams Ltd

Income statement using Absorption costing January

Particulars Amount £ Amount £

Sales £ 250,000

Less: Cost of goods sold

Direct material £ 50,000

Direct labor £ 30,000

Variable manufacturing

overhead £ 20,000

Fixed Manufacturing

overhead £ 40,000 £ 140,000

Gross Profit £ 110,000

Less: Selling and admin.

Expenses

Variable selling overhead £ 30,000

Fixed selling and Admin.

Overhead £ 30,000 £ 60,000

Net Profit £ 50,000

Creams Ltd

Income statement using Absorption costing February

Particulars Amount £ Amount £

Sales £ 125,000

| P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

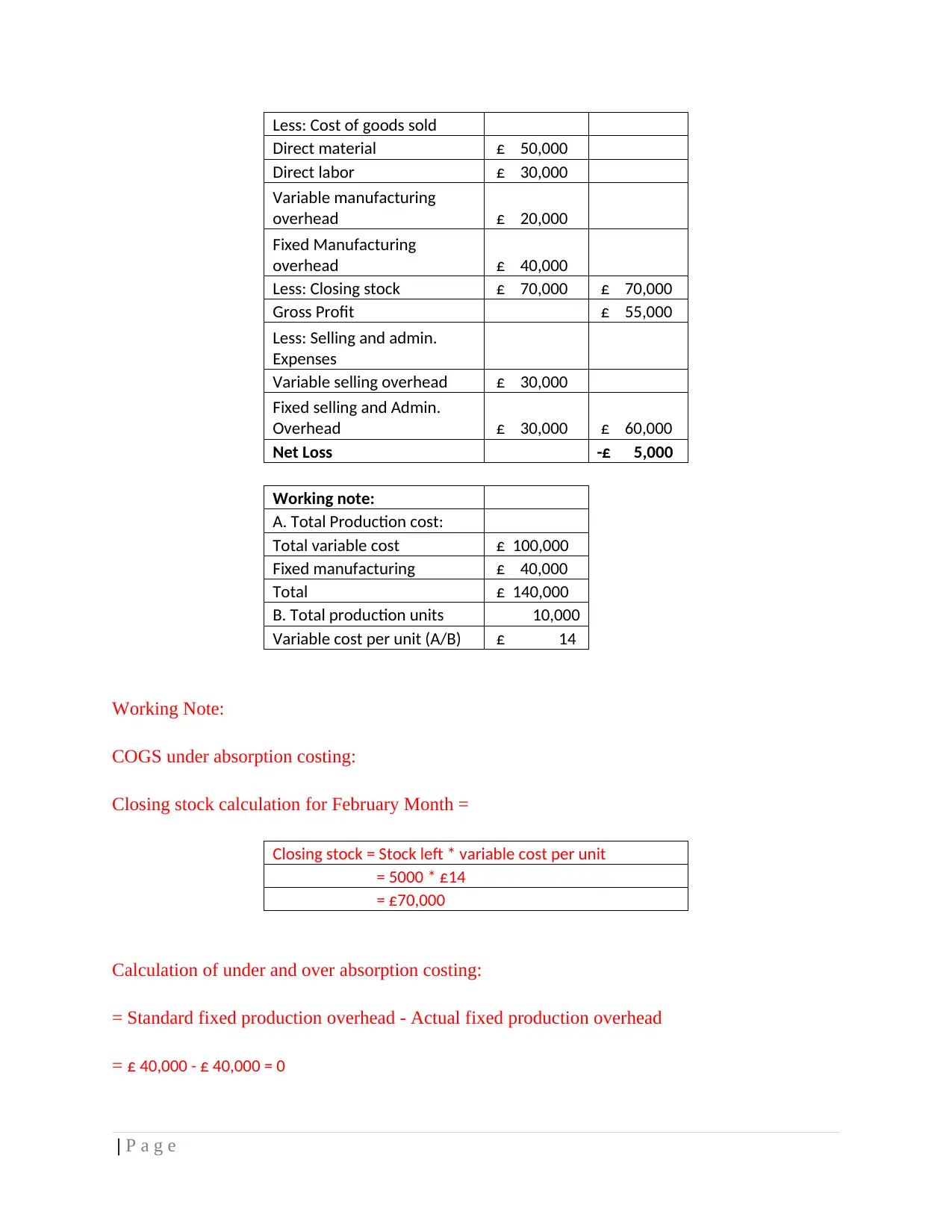

Less: Cost of goods sold

Direct material £ 50,000

Direct labor £ 30,000

Variable manufacturing

overhead £ 20,000

Fixed Manufacturing

overhead £ 40,000

Less: Closing stock £ 70,000 £ 70,000

Gross Profit £ 55,000

Less: Selling and admin.

Expenses

Variable selling overhead £ 30,000

Fixed selling and Admin.

Overhead £ 30,000 £ 60,000

Net Loss -£ 5,000

Working note:

A. Total Production cost:

Total variable cost £ 100,000

Fixed manufacturing £ 40,000

Total £ 140,000

B. Total production units 10,000

Variable cost per unit (A/B) £ 14

Working Note:

COGS under absorption costing:

Closing stock calculation for February Month =

Closing stock = Stock left * variable cost per unit

= 5000 * £14

= £70,000

Calculation of under and over absorption costing:

= Standard fixed production overhead - Actual fixed production overhead

= £ 40,000 - £ 40,000 = 0

| P a g e

Direct material £ 50,000

Direct labor £ 30,000

Variable manufacturing

overhead £ 20,000

Fixed Manufacturing

overhead £ 40,000

Less: Closing stock £ 70,000 £ 70,000

Gross Profit £ 55,000

Less: Selling and admin.

Expenses

Variable selling overhead £ 30,000

Fixed selling and Admin.

Overhead £ 30,000 £ 60,000

Net Loss -£ 5,000

Working note:

A. Total Production cost:

Total variable cost £ 100,000

Fixed manufacturing £ 40,000

Total £ 140,000

B. Total production units 10,000

Variable cost per unit (A/B) £ 14

Working Note:

COGS under absorption costing:

Closing stock calculation for February Month =

Closing stock = Stock left * variable cost per unit

= 5000 * £14

= £70,000

Calculation of under and over absorption costing:

= Standard fixed production overhead - Actual fixed production overhead

= £ 40,000 - £ 40,000 = 0

| P a g e

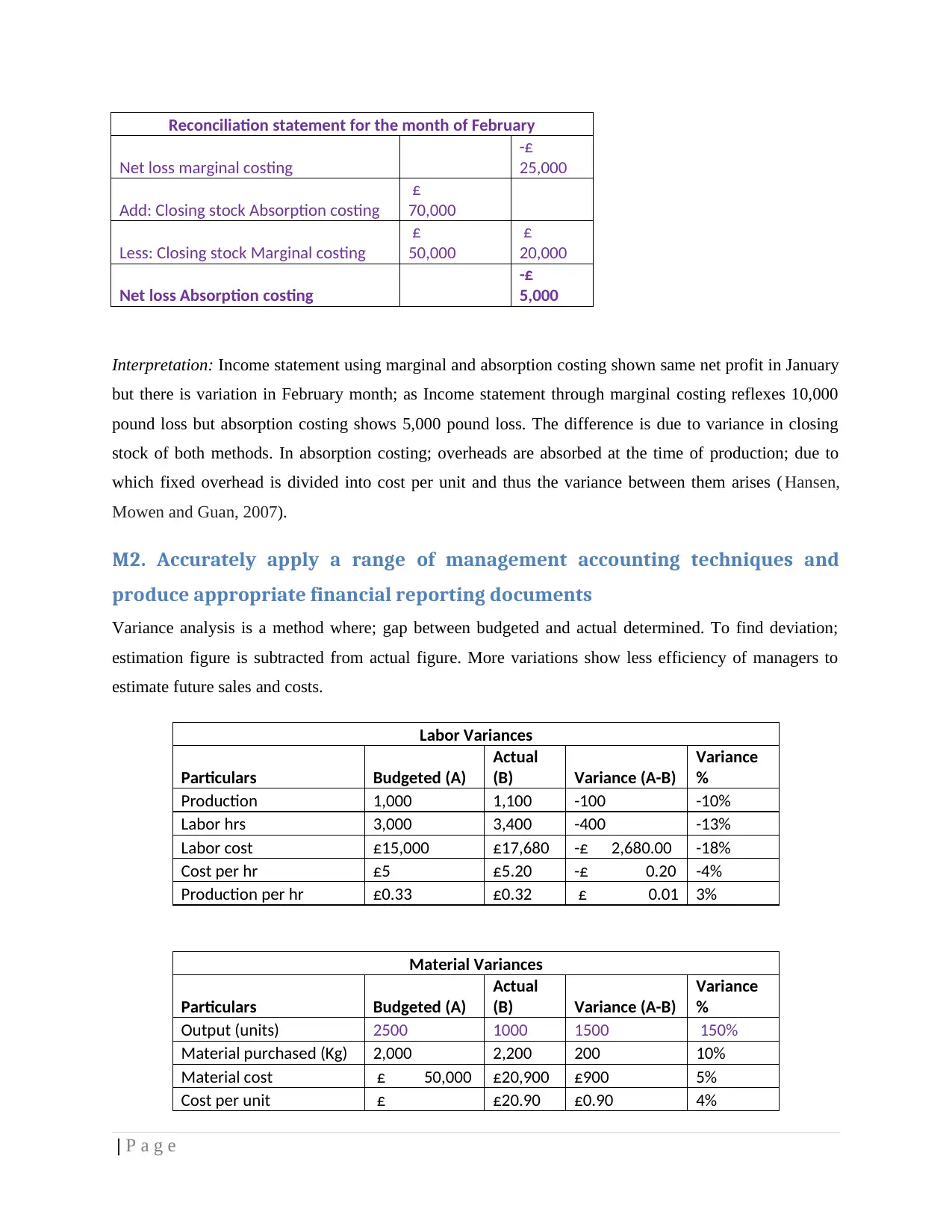

Reconciliation statement for the month of February

Net loss marginal costing

-£

25,000

Add: Closing stock Absorption costing

£

70,000

Less: Closing stock Marginal costing

£

50,000

£

20,000

Net loss Absorption costing

-£

5,000

Interpretation: Income statement using marginal and absorption costing shown same net profit in January

but there is variation in February month; as Income statement through marginal costing reflexes 10,000

pound loss but absorption costing shows 5,000 pound loss. The difference is due to variance in closing

stock of both methods. In absorption costing; overheads are absorbed at the time of production; due to

which fixed overhead is divided into cost per unit and thus the variance between them arises ( Hansen,

Mowen and Guan, 2007).

M2. Accurately apply a range of management accounting techniques and

produce appropriate financial reporting documents

Variance analysis is a method where; gap between budgeted and actual determined. To find deviation;

estimation figure is subtracted from actual figure. More variations show less efficiency of managers to

estimate future sales and costs.

Labor Variances

Particulars Budgeted (A)

Actual

(B) Variance (A-B)

Variance

%

Production 1,000 1,100 -100 -10%

Labor hrs 3,000 3,400 -400 -13%

Labor cost £15,000 £17,680 -£ 2,680.00 -18%

Cost per hr £5 £5.20 -£ 0.20 -4%

Production per hr £0.33 £0.32 £ 0.01 3%

Material Variances

Particulars Budgeted (A)

Actual

(B) Variance (A-B)

Variance

%

Output (units) 2500 1000 1500 150%

Material purchased (Kg) 2,000 2,200 200 10%

Material cost £ 50,000 £20,900 £900 5%

Cost per unit £ £20.90 £0.90 4%

| P a g e

Net loss marginal costing

-£

25,000

Add: Closing stock Absorption costing

£

70,000

Less: Closing stock Marginal costing

£

50,000

£

20,000

Net loss Absorption costing

-£

5,000

Interpretation: Income statement using marginal and absorption costing shown same net profit in January

but there is variation in February month; as Income statement through marginal costing reflexes 10,000

pound loss but absorption costing shows 5,000 pound loss. The difference is due to variance in closing

stock of both methods. In absorption costing; overheads are absorbed at the time of production; due to

which fixed overhead is divided into cost per unit and thus the variance between them arises ( Hansen,

Mowen and Guan, 2007).

M2. Accurately apply a range of management accounting techniques and

produce appropriate financial reporting documents

Variance analysis is a method where; gap between budgeted and actual determined. To find deviation;

estimation figure is subtracted from actual figure. More variations show less efficiency of managers to

estimate future sales and costs.

Labor Variances

Particulars Budgeted (A)

Actual

(B) Variance (A-B)

Variance

%

Production 1,000 1,100 -100 -10%

Labor hrs 3,000 3,400 -400 -13%

Labor cost £15,000 £17,680 -£ 2,680.00 -18%

Cost per hr £5 £5.20 -£ 0.20 -4%

Production per hr £0.33 £0.32 £ 0.01 3%

Material Variances

Particulars Budgeted (A)

Actual

(B) Variance (A-B)

Variance

%

Output (units) 2500 1000 1500 150%

Material purchased (Kg) 2,000 2,200 200 10%

Material cost £ 50,000 £20,900 £900 5%

Cost per unit £ £20.90 £0.90 4%

| P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.