Report on Management Accounting for Creams Ltd: Analysis

VerifiedAdded on 2023/01/12

|18

|4136

|66

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application to Creams Ltd., a company specializing in ice-creams, doughnuts, and waffles. The report begins by defining management accounting and its role in providing insights for business decision-making. It then delves into various systems of management accounting, including cost accounting, inventory management, job costing, and price optimization, outlining their essential requirements and benefits. The report also explores different methods for management accounting reports, such as budget reports, accounts receivable aging reports, sales reports, and performance reports, explaining their purpose and how Creams Ltd. can utilize them. Furthermore, the report examines cost calculation techniques, including marginal costing and absorption costing, highlighting their advantages and disadvantages. It also discusses planning tools, their merits and demerits, and how organizations can use them to analyze and solve financial problems. The report concludes with a comparison of how different organizations use management accounting data to address financial challenges and evaluates the effectiveness of planning tools in this context.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

P1: Systems of management accounting.................................................................................................3

M1: Benefits of systems of management accounting..............................................................................4

P2: Methods for reports of management accounting.............................................................................4

M2: Application of techniques of management accounting....................................................................5

D1: Critical evaluation of systems of management accounting...............................................................6

TASK 2..........................................................................................................................................................6

P3: Cost calculation with use of techniques............................................................................................6

M2: Application of management accounting techniques......................................................................11

D2: Producing of financial reports.........................................................................................................12

TASK 3........................................................................................................................................................12

P4: Merits and Demerits of planning tools............................................................................................12

M3: Analysis tools’ usage......................................................................................................................13

TASK 4........................................................................................................................................................14

P5: Comparison between organizations................................................................................................14

M4: Analysis of use of management accounting by organizations........................................................15

D3: Evaluation of planning tools for solving financial problems............................................................15

CONCLUSION.............................................................................................................................................16

REFERENCES..............................................................................................................................................17

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

P1: Systems of management accounting.................................................................................................3

M1: Benefits of systems of management accounting..............................................................................4

P2: Methods for reports of management accounting.............................................................................4

M2: Application of techniques of management accounting....................................................................5

D1: Critical evaluation of systems of management accounting...............................................................6

TASK 2..........................................................................................................................................................6

P3: Cost calculation with use of techniques............................................................................................6

M2: Application of management accounting techniques......................................................................11

D2: Producing of financial reports.........................................................................................................12

TASK 3........................................................................................................................................................12

P4: Merits and Demerits of planning tools............................................................................................12

M3: Analysis tools’ usage......................................................................................................................13

TASK 4........................................................................................................................................................14

P5: Comparison between organizations................................................................................................14

M4: Analysis of use of management accounting by organizations........................................................15

D3: Evaluation of planning tools for solving financial problems............................................................15

CONCLUSION.............................................................................................................................................16

REFERENCES..............................................................................................................................................17

INTRODUCTION

Management accounting refers to using financial data, facts, figures and information for

analysis and interpretation of financial statements of a company by the management

(Aggelopoulos and Georgopoulos, 2017). It helps managers a lot in getting deep insights into the

business and taking the required decisions for its benefit in the long-run. If the managers use this

data efficiently and effectively then it can benefit the organization a lot in the long-run. Properly

applying its strategies and techniques can lead a firm towards sustainable success in the future

and it can easily get ahead of the competition in the market. This report is based on Creams Ltd.,

a company which specializes in selling ice-creams, doughnuts and waffles. This project will

focus on systems of management accounting, applying a range of its techniques, explaining the

tools used for planning. Additionally, detailed analysis will be done on comparison of ways in

which organizations can use its data to respond to financial problems.

TASK 1

P1: Systems of management accounting

The use of various techniques for financial data and information for getting useful

insights about the business of company is known as management accounting. Creams Ltd.’s

managers can use it so that they can easily interpret their financial information.

There are different types of systems in management accounting which are explained as

follows-

Cost accounting system- It refers to a framework which is used by the firms in order to

find out details about their costs and use different techniques for reduction of cost. Creams Ltd.

can make use of this system so that it can identify its costs, excessive overheads and try to reduce

them so that its profits can be maximized.

Essential requirements- A good cost accounting system must be simple and practical to

use. It must help in identifying and segregating the costs in a company according to its various

products. It must display the required accuracy for getting the desired results in the context of the

organization. Thus, overall it must be able to provide managers the required information relevant

to them.

Inventory management system- It is a framework which can be utilized by

organizations by applying its various approaches such as LIFO, FIFO and Weighted Average

Cost to control, manage and track the inventory level in the organization (Alfian, 2017). Creams

Ltd. can make use of this system so that proper tracking of its stock level is done.

Management accounting refers to using financial data, facts, figures and information for

analysis and interpretation of financial statements of a company by the management

(Aggelopoulos and Georgopoulos, 2017). It helps managers a lot in getting deep insights into the

business and taking the required decisions for its benefit in the long-run. If the managers use this

data efficiently and effectively then it can benefit the organization a lot in the long-run. Properly

applying its strategies and techniques can lead a firm towards sustainable success in the future

and it can easily get ahead of the competition in the market. This report is based on Creams Ltd.,

a company which specializes in selling ice-creams, doughnuts and waffles. This project will

focus on systems of management accounting, applying a range of its techniques, explaining the

tools used for planning. Additionally, detailed analysis will be done on comparison of ways in

which organizations can use its data to respond to financial problems.

TASK 1

P1: Systems of management accounting

The use of various techniques for financial data and information for getting useful

insights about the business of company is known as management accounting. Creams Ltd.’s

managers can use it so that they can easily interpret their financial information.

There are different types of systems in management accounting which are explained as

follows-

Cost accounting system- It refers to a framework which is used by the firms in order to

find out details about their costs and use different techniques for reduction of cost. Creams Ltd.

can make use of this system so that it can identify its costs, excessive overheads and try to reduce

them so that its profits can be maximized.

Essential requirements- A good cost accounting system must be simple and practical to

use. It must help in identifying and segregating the costs in a company according to its various

products. It must display the required accuracy for getting the desired results in the context of the

organization. Thus, overall it must be able to provide managers the required information relevant

to them.

Inventory management system- It is a framework which can be utilized by

organizations by applying its various approaches such as LIFO, FIFO and Weighted Average

Cost to control, manage and track the inventory level in the organization (Alfian, 2017). Creams

Ltd. can make use of this system so that proper tracking of its stock level is done.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Essential requirements- A good inventory management system should track stock level

of the organization and should manage it effectively and efficiently. Also, it should be able to

effectively review the requirements of the firm.

Job costing system- It is a highly useful management accounting system for the

manufacturing firms (Bentley, 2018). As Creams Ltd. manufactures ice-creams, doughnuts and

waffles it can use this system effectively and efficiently so that orders can be properly managed

so that mismanagement does not occurs in the operations of company.

Essential requirements- A good system must be able to segregate the orders and

manage them according to their date of completion. Also it must be able to track the progress of

orders and the cost incurred in completing them. This will help in reducing the extra costs

incurred in completing orders and maximization of profits.

Price optimization system- It is useful when the company has to select a pricing strategy

relevant to the product. Creams Ltd. can utilize it to set price according to demand levels in the

market which can help it in setting of right price so that maximum profit can be earned from the

product. It is useful in changing strategies according to dynamic situations in the market.

Essential requirements- A good price optimization system should help in dealing with

the trends in the market. Also it must be able to adjust the price according to changes in market

so that it benefits the company the most in such a scenario.

M1: Benefits of systems of management accounting

Advantages are offered by management accounting systems to Creams Ltd. Cost

accounting system helps it in finding and avoiding the extra costs. Inventory management system

helps in tracking the stock levels, Job costing system helps in managing the orders. Price

optimization system helps in setting an appropriate price according to conditions in the market.

Thus it is up to the management of the company to use these systems effectively and efficiently

so as to bring the required smoothness in the operations and functioning of the firm. All these

systems can be applied within the organizational context which will lead to smooth functioning

of the processes of the organization.

P2: Methods for reports of management accounting

Creams Ltd. can use reports of managerial accounting so as to interpret and analyze the

overall performance in the company. It is to check whether it is up to the mark or not. The

methods which it can use are as follows-

Budget Reports- They help the small businesses in setting and managing the budgets for

monitoring and controlling the performance of their business (Curry, 2020). It can be used for

comparison purposes so that performance of current year with the previous year and to compare

of the organization and should manage it effectively and efficiently. Also, it should be able to

effectively review the requirements of the firm.

Job costing system- It is a highly useful management accounting system for the

manufacturing firms (Bentley, 2018). As Creams Ltd. manufactures ice-creams, doughnuts and

waffles it can use this system effectively and efficiently so that orders can be properly managed

so that mismanagement does not occurs in the operations of company.

Essential requirements- A good system must be able to segregate the orders and

manage them according to their date of completion. Also it must be able to track the progress of

orders and the cost incurred in completing them. This will help in reducing the extra costs

incurred in completing orders and maximization of profits.

Price optimization system- It is useful when the company has to select a pricing strategy

relevant to the product. Creams Ltd. can utilize it to set price according to demand levels in the

market which can help it in setting of right price so that maximum profit can be earned from the

product. It is useful in changing strategies according to dynamic situations in the market.

Essential requirements- A good price optimization system should help in dealing with

the trends in the market. Also it must be able to adjust the price according to changes in market

so that it benefits the company the most in such a scenario.

M1: Benefits of systems of management accounting

Advantages are offered by management accounting systems to Creams Ltd. Cost

accounting system helps it in finding and avoiding the extra costs. Inventory management system

helps in tracking the stock levels, Job costing system helps in managing the orders. Price

optimization system helps in setting an appropriate price according to conditions in the market.

Thus it is up to the management of the company to use these systems effectively and efficiently

so as to bring the required smoothness in the operations and functioning of the firm. All these

systems can be applied within the organizational context which will lead to smooth functioning

of the processes of the organization.

P2: Methods for reports of management accounting

Creams Ltd. can use reports of managerial accounting so as to interpret and analyze the

overall performance in the company. It is to check whether it is up to the mark or not. The

methods which it can use are as follows-

Budget Reports- They help the small businesses in setting and managing the budgets for

monitoring and controlling the performance of their business (Curry, 2020). It can be used for

comparison purposes so that performance of current year with the previous year and to compare

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

performance with the established standards of the industry. This helps in finding out deviations

and variations so that they can be rectified quickly for optimizing the performance of the

company in the short-run as well as the long-run. Creams Ltd. can use it to check and monitor its

performance.

Accounts Receivable Aging Reports- Accounts receivables aging reports are used by

companies to check their cash flow from their debtors (Eisenberg, 2017). Managers of Creams

Ltd. can use these reports to check the cash flow, credit policy and identify those debtors whose

debts are due since a long time. It also helps the organization in making a list of receivables

according to their due date of payment. Also, potential bad debts can be easily identified by the

management so that a provision can be created for them for the future.

Sales Reports- Sales reports can be used by managers to monitor the level of sales in the

company (Su and et.al., 2016). Management of Creams Ltd. can use them for comparison and

analysis purpose to see whether there has been an increase or decrease in sales compared to the

previous year. This helps in comparing the own sales of organization with that of the

competitors. If the sales revenue has decreased and deviations and variations are found in sales

then the reasons for the same can be identified so that quick rectifying actions are taken to

increase the revenue. Forecasting of sales for the next year can be done using them which

enhances the company to set up relevant standards for the sales department to achieve the targets

of performance.

Performance Reports- Performance reports can be used by managers to analyze the

overall performance of operations in a business enterprise (Gao, Gao and Wang, 2017). The

managers of Creams Ltd. can use these reports to check, control and monitor the performance of

different departments of the enterprise such as production, marketing, finance, HR etc. Standards

and metrics need to be used for measurement so that comparison is done effectively and

efficiently relevant to the context of the organization’s business operations and mode of

functioning. This helps in preparing an overall report on the working of an organization during a

specific time period which is mostly a year. The performance can thereby be monitored and

compared with that of the other competitors so as to see whether the firm is ahead of them or

behind them. Suitable action can then be taken on the basis of findings.

Thus, Management accounting reporting is all about preparation of various reports so that

analysis and interpretation can be performed within an organization. The reasons why they are

produced and used by businesses is that they help in raising the overall efficiency and

effectiveness of processes and also allows for making specific strategies within the context of an

organization.

M2: Application of techniques of management accounting

They can be used by management of Creams Ltd. effectively and efficiently to get the

best performance out of the employees and optimizing the processes. Also, a lot of help is

and variations so that they can be rectified quickly for optimizing the performance of the

company in the short-run as well as the long-run. Creams Ltd. can use it to check and monitor its

performance.

Accounts Receivable Aging Reports- Accounts receivables aging reports are used by

companies to check their cash flow from their debtors (Eisenberg, 2017). Managers of Creams

Ltd. can use these reports to check the cash flow, credit policy and identify those debtors whose

debts are due since a long time. It also helps the organization in making a list of receivables

according to their due date of payment. Also, potential bad debts can be easily identified by the

management so that a provision can be created for them for the future.

Sales Reports- Sales reports can be used by managers to monitor the level of sales in the

company (Su and et.al., 2016). Management of Creams Ltd. can use them for comparison and

analysis purpose to see whether there has been an increase or decrease in sales compared to the

previous year. This helps in comparing the own sales of organization with that of the

competitors. If the sales revenue has decreased and deviations and variations are found in sales

then the reasons for the same can be identified so that quick rectifying actions are taken to

increase the revenue. Forecasting of sales for the next year can be done using them which

enhances the company to set up relevant standards for the sales department to achieve the targets

of performance.

Performance Reports- Performance reports can be used by managers to analyze the

overall performance of operations in a business enterprise (Gao, Gao and Wang, 2017). The

managers of Creams Ltd. can use these reports to check, control and monitor the performance of

different departments of the enterprise such as production, marketing, finance, HR etc. Standards

and metrics need to be used for measurement so that comparison is done effectively and

efficiently relevant to the context of the organization’s business operations and mode of

functioning. This helps in preparing an overall report on the working of an organization during a

specific time period which is mostly a year. The performance can thereby be monitored and

compared with that of the other competitors so as to see whether the firm is ahead of them or

behind them. Suitable action can then be taken on the basis of findings.

Thus, Management accounting reporting is all about preparation of various reports so that

analysis and interpretation can be performed within an organization. The reasons why they are

produced and used by businesses is that they help in raising the overall efficiency and

effectiveness of processes and also allows for making specific strategies within the context of an

organization.

M2: Application of techniques of management accounting

They can be used by management of Creams Ltd. effectively and efficiently to get the

best performance out of the employees and optimizing the processes. Also, a lot of help is

provided to the managers in analysis and decision-making. Right decisions can be taken by the

mangers of the organization if they use these techniques appropriately. This leads to their overall

effectiveness and the company can touch new heights of success in the future leaving behind its

various competitors and maximizing its profits.

D1: Critical evaluation of systems of management accounting

The systems of managerial accounting can be used effectively and efficiently by

managers of Creams Ltd. They can do so by properly integrating these systems into various

organizational processes which helps not just in monitoring the performance of employees and

workers in these processes but also enhances the improvements that need to be done for bringing

more efficiency in the overall system of enterprise. Thus they help the mangers in taking the

right decisions at the appropriate time.

TASK 2

P3: Cost calculation with use of techniques

There are different types of costs which are prevalent in the context of an organization

(Huang, 2016). The detailed explanation of these costs in relation with Creams Ltd. is provided

as follows-

Fixed costs- These are constant costs which do not change at all even after a change in

the level of output in the company. In Creams Ltd. examples of these costs are rent, fixed

manufacturing costs etc. Change in the level of production in the company does not have an

impact on them.

Semi-variable costs- These are costs in which certain element is fixed while other is

variable in nature (Seppänen, 2016). In Creams Ltd. examples of these costs are repairs, monthly

telephone bills, and indirect labor costs. They are impacted by a change in the level of production

of goods in the company.

Variable costs- These costs are the ones in which can impact the level of output (Jamal,

Tayles and Grant, 2019). In Creams Ltd. examples of these costs are office expenses, variable

manufacturing costs, electricity bill etc. Change in the level of production impacts these costs.

Techniques used for calculation of costs-

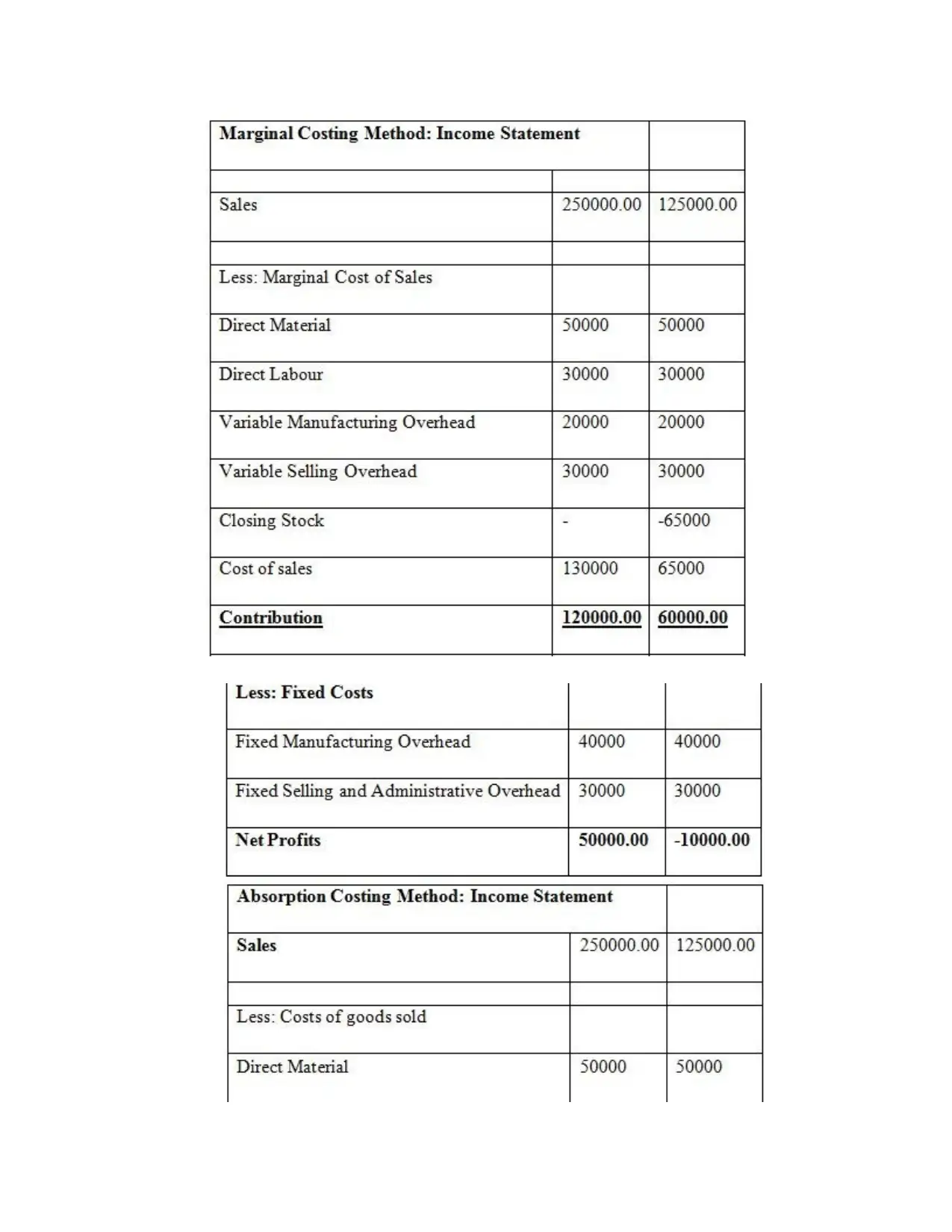

Marginal costing-

It is a technique in which calculation of break-even point is faciliated. Creams Ltd. makes

use of this technique.

mangers of the organization if they use these techniques appropriately. This leads to their overall

effectiveness and the company can touch new heights of success in the future leaving behind its

various competitors and maximizing its profits.

D1: Critical evaluation of systems of management accounting

The systems of managerial accounting can be used effectively and efficiently by

managers of Creams Ltd. They can do so by properly integrating these systems into various

organizational processes which helps not just in monitoring the performance of employees and

workers in these processes but also enhances the improvements that need to be done for bringing

more efficiency in the overall system of enterprise. Thus they help the mangers in taking the

right decisions at the appropriate time.

TASK 2

P3: Cost calculation with use of techniques

There are different types of costs which are prevalent in the context of an organization

(Huang, 2016). The detailed explanation of these costs in relation with Creams Ltd. is provided

as follows-

Fixed costs- These are constant costs which do not change at all even after a change in

the level of output in the company. In Creams Ltd. examples of these costs are rent, fixed

manufacturing costs etc. Change in the level of production in the company does not have an

impact on them.

Semi-variable costs- These are costs in which certain element is fixed while other is

variable in nature (Seppänen, 2016). In Creams Ltd. examples of these costs are repairs, monthly

telephone bills, and indirect labor costs. They are impacted by a change in the level of production

of goods in the company.

Variable costs- These costs are the ones in which can impact the level of output (Jamal,

Tayles and Grant, 2019). In Creams Ltd. examples of these costs are office expenses, variable

manufacturing costs, electricity bill etc. Change in the level of production impacts these costs.

Techniques used for calculation of costs-

Marginal costing-

It is a technique in which calculation of break-even point is faciliated. Creams Ltd. makes

use of this technique.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantages-

The effects of production and sales policy and can be effectively implemented in this

technique.

It eliminates the large balances which are left in the overhead accounts thus resulting in

more efficiency in costing operations of the company.

Disadvantages-

It understates various elements of business which can provide misleading results and

underestimation of financial conclusions derived using this technique of calculation of

costs.

Fixed overhead application is dependent on actual data and not on the estimates as

provided in the marginal costing approach. Thus it may result either in under-absorption

or the over-absorption of the overheads of the company which can impact the profits.

Absorption costing-

It is an approach of calculation of costs which helps firms by determining costs (Kramer,

Maas and Van Rinsum, 2016). It is a technique which helps in absorption of various

overheads of the organization. It also accounts for overheads which is something that the

marginal costing technique does not take into consideration.

Advantages-

It is simple to use and inexpensive to apply to the operations and functions of the

company.

There is no need to separate the fixed and variable costs in this technique as it is required

in marginal costing. This leads to accuracy in calculations and final results which can be

sued for analysis and interpretation of performance.

Disadvantages-

Fixed costs are period costs and whether related with manufacturing or selling or

administration produce no future benefits and thus must not be included in the cost of the

product or inventory.

Apportionment of overhead costs in absorption costing technique is done using arbitrary

methods and thus this sometimes produces inaccurate results.

The effects of production and sales policy and can be effectively implemented in this

technique.

It eliminates the large balances which are left in the overhead accounts thus resulting in

more efficiency in costing operations of the company.

Disadvantages-

It understates various elements of business which can provide misleading results and

underestimation of financial conclusions derived using this technique of calculation of

costs.

Fixed overhead application is dependent on actual data and not on the estimates as

provided in the marginal costing approach. Thus it may result either in under-absorption

or the over-absorption of the overheads of the company which can impact the profits.

Absorption costing-

It is an approach of calculation of costs which helps firms by determining costs (Kramer,

Maas and Van Rinsum, 2016). It is a technique which helps in absorption of various

overheads of the organization. It also accounts for overheads which is something that the

marginal costing technique does not take into consideration.

Advantages-

It is simple to use and inexpensive to apply to the operations and functions of the

company.

There is no need to separate the fixed and variable costs in this technique as it is required

in marginal costing. This leads to accuracy in calculations and final results which can be

sued for analysis and interpretation of performance.

Disadvantages-

Fixed costs are period costs and whether related with manufacturing or selling or

administration produce no future benefits and thus must not be included in the cost of the

product or inventory.

Apportionment of overhead costs in absorption costing technique is done using arbitrary

methods and thus this sometimes produces inaccurate results.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

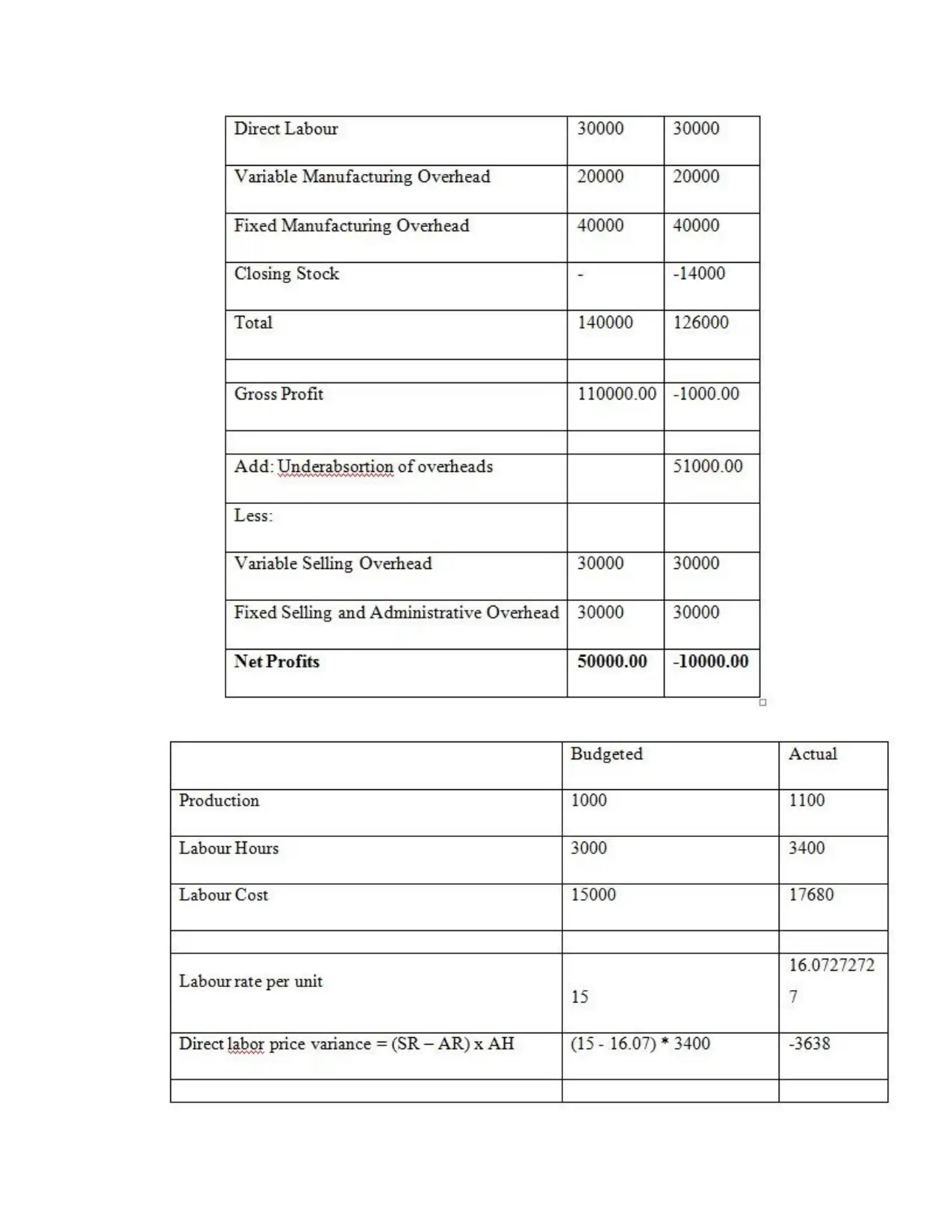

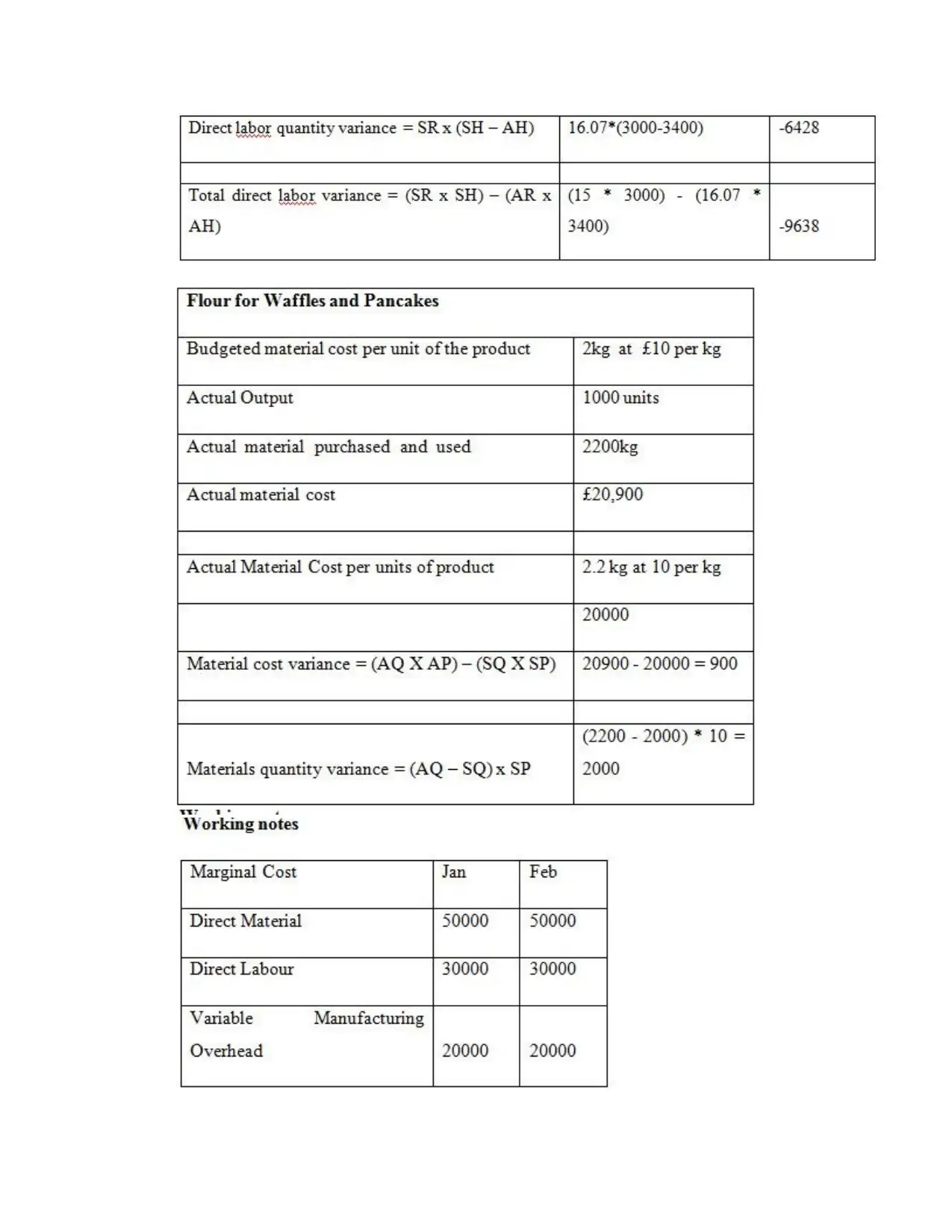

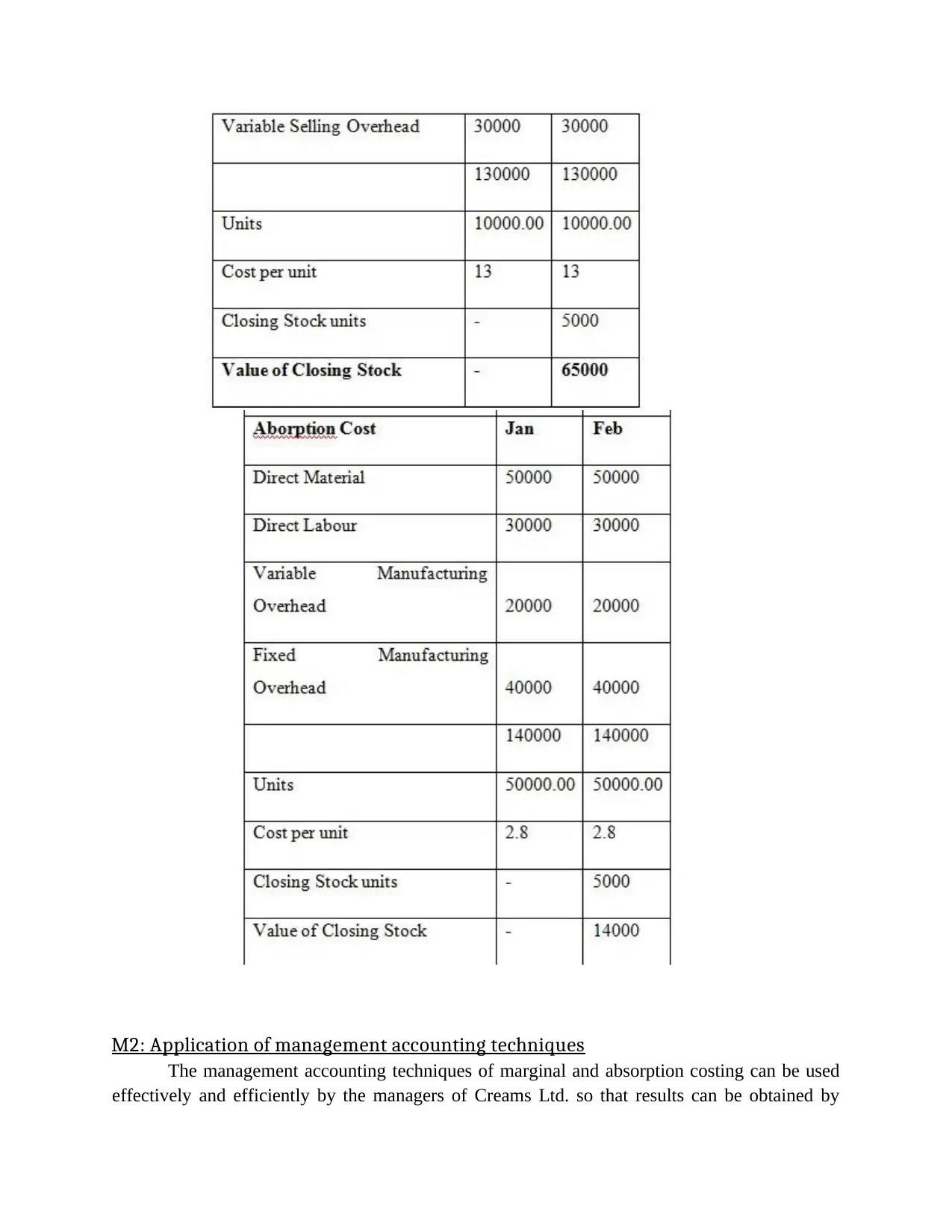

M2: Application of management accounting techniques

The management accounting techniques of marginal and absorption costing can be used

effectively and efficiently by the managers of Creams Ltd. so that results can be obtained by

The management accounting techniques of marginal and absorption costing can be used

effectively and efficiently by the managers of Creams Ltd. so that results can be obtained by

their application. The use of these techniques not only helps in finding out profits but also helps

in finding out ways to reduce the extra costs being incurred so that profits can be maximized and

goals and objectives of company can be realized. Thus they are analytical and interpretative in

nature which enhances the abilities and competencies of managers in finding out rational

solutions to the problems incurred.

D2: Producing of financial reports

Financial reports can be prepared on the basis of analysis and interpretation of data

provided in the financial statements and other accounts of the company. Managers of Creams

Ltd. can use these reports for checking the accuracy of calculations. Also these reports are

important in the context of business to draw conclusions and recommendations on the basis of

insights and information provided by them. This helps in development of competencies in a firm

which is always ready to improve in a dynamic business environment which will ensure that it

attains sustainable success in the future.

TASK 3

P4: Merits and Demerits of planning tools

Different types of planning tools can be used by the management of the organizations to

plan, cooperate and coordinate effectively for the future (Machete, F. and et.al., 2016). Various

goals and objectives can be set by the companies for the future which they need to achieve for

sustainable growth. Creams Ltd. uses the following tools explained as follows-

Cash budget-

It is used by organizations in order to forecast their cash revenues and expenditures

during a particular period of time (Ng, 2018). It can be used by managers of Creams Ltd. to

manage their cash operations.

Advantages-

Cash budget can be used to limit the spending of cash on non-essential items in the

organization. This helps in preventing overspending.

Cash budget helps in properly maintaing the cash and other cash equivalents thus

resulting in maintaining of liquidity position of the firm.

Disadvantages-

Cash budget leads to rigidity in cash operations of the company which can reduce its

financial flexibility.

If prepared inaccurately a cash budget can be harmful for the prospects of the company

both in the short-run and the long-run because of the wrong analysis and interpretation.

Operating budget-

in finding out ways to reduce the extra costs being incurred so that profits can be maximized and

goals and objectives of company can be realized. Thus they are analytical and interpretative in

nature which enhances the abilities and competencies of managers in finding out rational

solutions to the problems incurred.

D2: Producing of financial reports

Financial reports can be prepared on the basis of analysis and interpretation of data

provided in the financial statements and other accounts of the company. Managers of Creams

Ltd. can use these reports for checking the accuracy of calculations. Also these reports are

important in the context of business to draw conclusions and recommendations on the basis of

insights and information provided by them. This helps in development of competencies in a firm

which is always ready to improve in a dynamic business environment which will ensure that it

attains sustainable success in the future.

TASK 3

P4: Merits and Demerits of planning tools

Different types of planning tools can be used by the management of the organizations to

plan, cooperate and coordinate effectively for the future (Machete, F. and et.al., 2016). Various

goals and objectives can be set by the companies for the future which they need to achieve for

sustainable growth. Creams Ltd. uses the following tools explained as follows-

Cash budget-

It is used by organizations in order to forecast their cash revenues and expenditures

during a particular period of time (Ng, 2018). It can be used by managers of Creams Ltd. to

manage their cash operations.

Advantages-

Cash budget can be used to limit the spending of cash on non-essential items in the

organization. This helps in preventing overspending.

Cash budget helps in properly maintaing the cash and other cash equivalents thus

resulting in maintaining of liquidity position of the firm.

Disadvantages-

Cash budget leads to rigidity in cash operations of the company which can reduce its

financial flexibility.

If prepared inaccurately a cash budget can be harmful for the prospects of the company

both in the short-run and the long-run because of the wrong analysis and interpretation.

Operating budget-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.