Cost Volume Profit (CVP) Analysis Report: Azad Inc. Performance

VerifiedAdded on 2022/10/17

|8

|1286

|12

Report

AI Summary

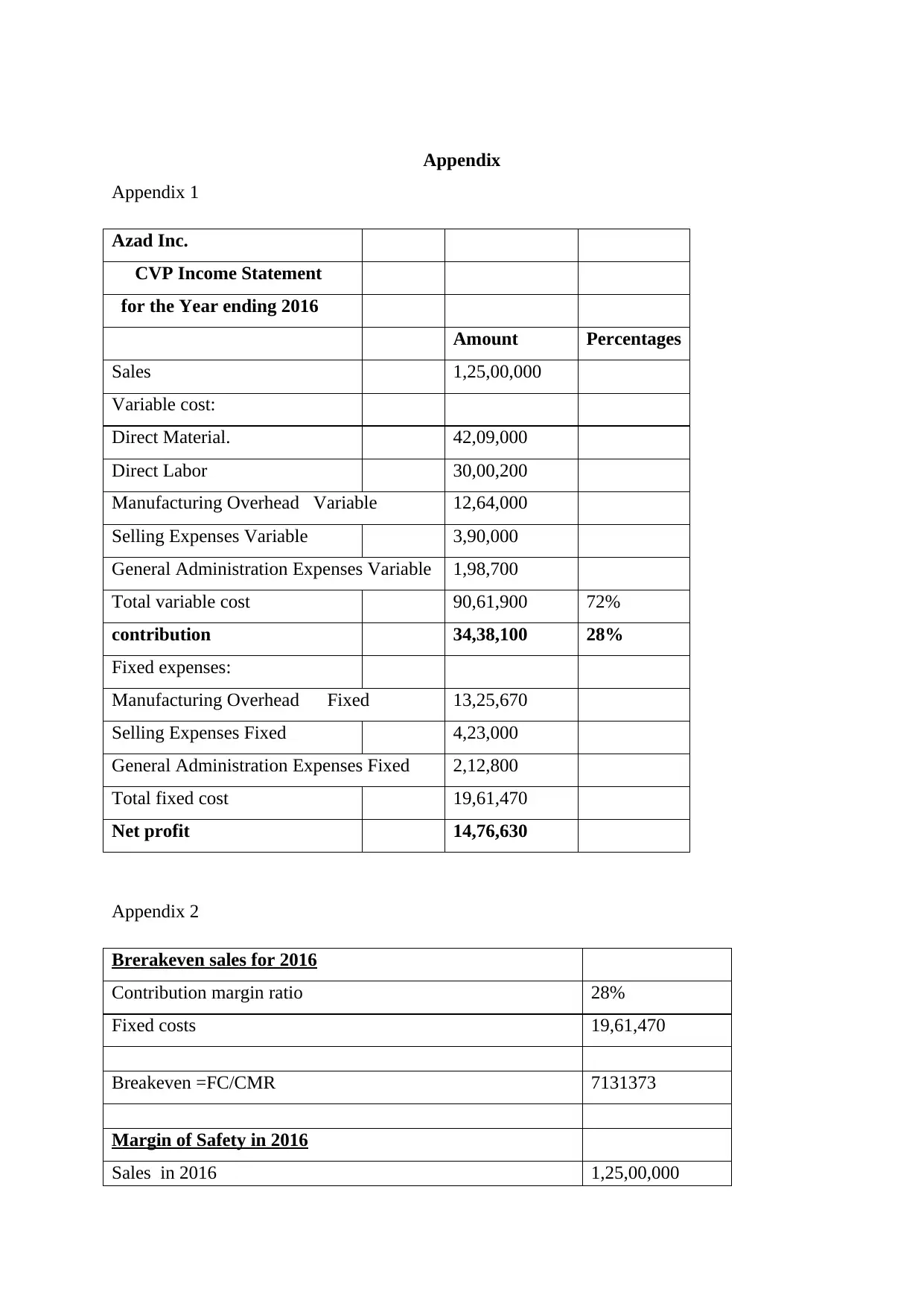

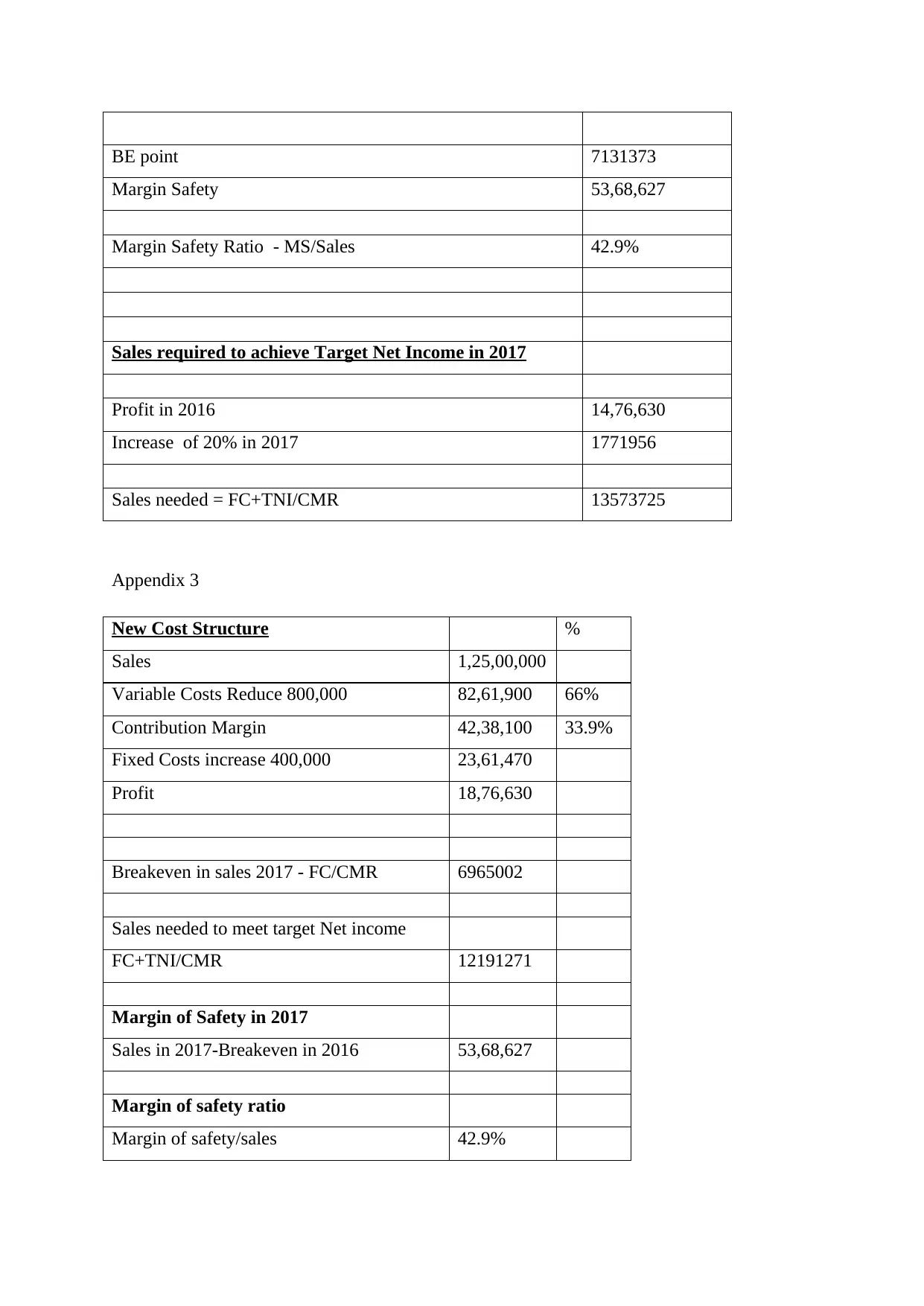

This report provides a comprehensive cost-volume-profit (CVP) analysis of Azad Inc.'s financial performance. The analysis begins with an executive summary and an introduction outlining the scope of the report. It includes the preparation of a CVP income statement, calculation of variable cost ratios, and contribution margins. The report also covers breakeven analysis, determining the breakeven sales and margin of safety, and assesses the impact of a proposed laser purchase on the company's financial metrics. The report concludes with an overview of the findings, highlighting the positive financial performance and the benefits of the laser purchase, supported by appendices that contain detailed financial data and calculations.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.