Unit 5: Management Accounting Report: Decision Making

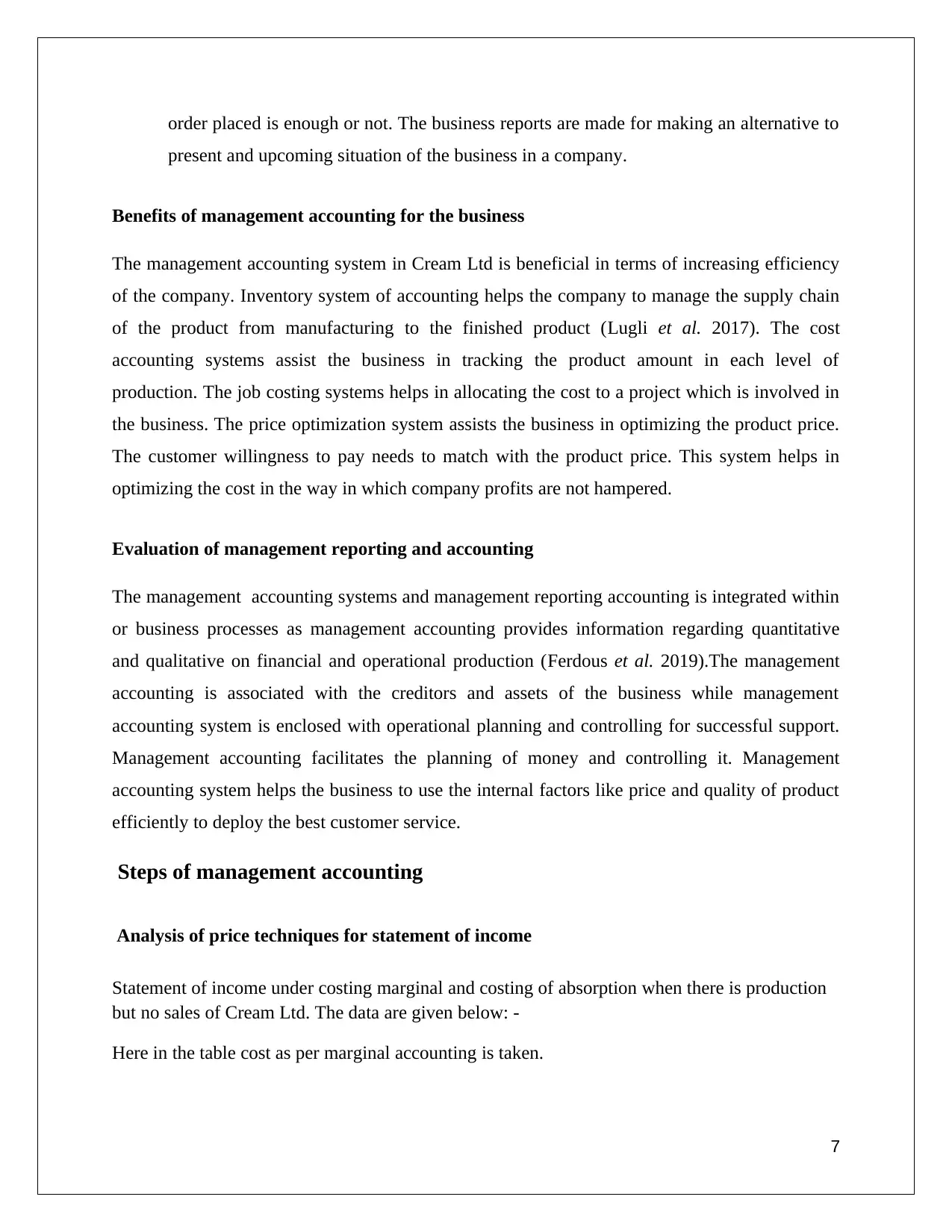

VerifiedAdded on 2021/04/05

|20

|5724

|146

Report

AI Summary

This report, prepared by a student, delves into the core concepts of management accounting within the context of Cream Ltd. It explores various types of management accounting systems, including inventory, cost, job costing, and price optimization, highlighting their benefits for business efficiency. The report also examines different methods of management reporting, such as budgets, variance analysis, and cost estimation, and their roles in financial planning and control. A significant portion of the report focuses on analyzing price techniques for statement of income, comparing marginal and absorption costing methods with detailed calculations and variance analysis. Furthermore, the report discusses the application of management accounting for financial reporting and outlines the steps involved in producing appropriate financial documents. The report concludes by addressing how management accounting tools can aid in responding to financial problems and contribute to an organization's sustainable success. The document is a valuable resource for students studying management accounting, providing insights into practical applications and theoretical frameworks.

Higher Nationals

Higher National Diploma in Business

Student Name Georgiana Aura Pavel ID HE0799

2

Unit Number and Title Unit 5 – Management Accounting

Academic Year 2019/2020 Cohort Sept 19 Term Block 3

Unit Leader Alfred Agyeman Assess

or

Joseph Olaniyan

Assignment Title Management Accounting Concepts and Techniques

in Decision Making

Issue Date 09/03/2020

Submission Start Date

(Formative)

27/04/2020

Submission Summative 08/05/2020

IV Name Seethalakshmy Nagarajan

IV Date 25/02/2020

Learners Declaration: I certify that the work submitted for this unit is my own

and the research sources are fully acknowledged.

Learners Name: Georgiana Aura Pavel

Date:23.05.2020

1

Higher National Diploma in Business

Student Name Georgiana Aura Pavel ID HE0799

2

Unit Number and Title Unit 5 – Management Accounting

Academic Year 2019/2020 Cohort Sept 19 Term Block 3

Unit Leader Alfred Agyeman Assess

or

Joseph Olaniyan

Assignment Title Management Accounting Concepts and Techniques

in Decision Making

Issue Date 09/03/2020

Submission Start Date

(Formative)

27/04/2020

Submission Summative 08/05/2020

IV Name Seethalakshmy Nagarajan

IV Date 25/02/2020

Learners Declaration: I certify that the work submitted for this unit is my own

and the research sources are fully acknowledged.

Learners Name: Georgiana Aura Pavel

Date:23.05.2020

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Please copy the above and insert into your assignment’s front page.

Academic Misconduct:

Any act of Academic Misconduct will be seriously dealt with according to the College’s

and awarding bodies’ regulations.

Academic misconduct includes, but is not limited to, the following: Verbatim (word

for word) quotation without clear acknowledgement, cutting and pasting from the

Internet without clear acknowledgement, collusion, inaccurate citation and failure to

acknowledge assistance.

Plagiarism is presenting someone’s work as your own. It includes copying information

directly from the web or books without referencing the material; submitting joint

coursework as an individual effort; copying another student’s coursework; stealing

coursework from another student and submitting it as your own work.

Suspected plagiarism, and any other cases of suspected academic misconduct, will

be investigated and if found to have occurred will be dealt with according to the

College procedure. (For further details please refer to 5o.i the Academic Misconduct

Policy and Procedure; 5o.ii Academic Misconduct Student Guide; Academic Good

Practice Handbook, all available on HELP.)

Please copy the above and insert into your assignment’s front page.

Academic Misconduct:

Any act of Academic Misconduct will be seriously dealt with according to the College’s

and awarding bodies’ regulations.

Academic misconduct includes, but is not limited to, the following: Verbatim (word

for word) quotation without clear acknowledgement, cutting and pasting from the

Internet without clear acknowledgement, collusion, inaccurate citation and failure to

acknowledge assistance.

Plagiarism is presenting someone’s work as your own. It includes copying information

directly from the web or books without referencing the material; submitting joint

coursework as an individual effort; copying another student’s coursework; stealing

coursework from another student and submitting it as your own work.

Suspected plagiarism, and any other cases of suspected academic misconduct, will

be investigated and if found to have occurred will be dealt with according to the

College procedure. (For further details please refer to 5o.i the Academic Misconduct

Policy and Procedure; 5o.ii Academic Misconduct Student Guide; Academic Good

Practice Handbook, all available on HELP.)

UNIT 5

MANAGEMENT ACCOUNTING

STUDENT NAME: GERGIANA AURA PAVEL

3

MANAGEMENT ACCOUNTING

STUDENT NAME: GERGIANA AURA PAVEL

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Table of Contents

Introduction......................................................................................................................................3

LO1: Discuss the MAS....................................................................................................................3

P1: Types of management accounting......................................................................................3

P2: Methods of management reporting...................................................................................4

Benefits ofmanagementaccounting for the business...............................................................5

Evaluation of management reportingand accounting............................................................5

LO2: Steps of management accounting...........................................................................................5

P3: Analysis of price techniques for statement of income......................................................5

Statementof income under costing marginal and costing of absorption when there is production

but no sales of Cream Ltd. The data are given below:-...............................................................5

Application of management accounting for reporting for financial.....................................9

Discuss the finance report of business activities....................................................................10

LO3: Tools for management accounting.......................................................................................10

P4: Advantages and disadvantages of planning tools...........................................................10

Analysis of tools and application on budgets.........................................................................11

LO4: Respond to financial problems.............................................................................................12

P5: Management responding to financial problems.............................................................12

Organisation sustainable success............................................................................................13

Conclusion.....................................................................................................................................14

Reference list.................................................................................................................................16

4

Introduction......................................................................................................................................3

LO1: Discuss the MAS....................................................................................................................3

P1: Types of management accounting......................................................................................3

P2: Methods of management reporting...................................................................................4

Benefits ofmanagementaccounting for the business...............................................................5

Evaluation of management reportingand accounting............................................................5

LO2: Steps of management accounting...........................................................................................5

P3: Analysis of price techniques for statement of income......................................................5

Statementof income under costing marginal and costing of absorption when there is production

but no sales of Cream Ltd. The data are given below:-...............................................................5

Application of management accounting for reporting for financial.....................................9

Discuss the finance report of business activities....................................................................10

LO3: Tools for management accounting.......................................................................................10

P4: Advantages and disadvantages of planning tools...........................................................10

Analysis of tools and application on budgets.........................................................................11

LO4: Respond to financial problems.............................................................................................12

P5: Management responding to financial problems.............................................................12

Organisation sustainable success............................................................................................13

Conclusion.....................................................................................................................................14

Reference list.................................................................................................................................16

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

In this study on accounting management of Cream ltd. the process of accounting management is

being elaborated. The requirement of different types of management accounting systems in

Cream ltd. is going to be explained. The discussion explains the management accounting system

and their application in the organisation. It also focuses on the accounting management system

and management accounting reporting. The study is based on understanding the integration with

the organisational processes. The study is on the understanding of management accounting

technique, calculation of the cost to prepare statement of income using absorption and cost of

marginal. The comparison will be done on organisation adaption to the management accounting

system to revert to issues of finance.

Discuss the MAS

Types of management accounting

The accounting process of Cream Ltd consists of management accounting and accounting of

cost which means analysing the cost of business and the operations to draw up reports of

finance internally, the account which the managers used, records which assists making of

decision process in attaining the organisational goals (van Helden et al. 2016). Different

types of MAS are:

1. Inventory system of accounting which facilitates stock placement in the company. This

system is vital to track the stocks in different locations and managing the supply network

effectively. It is present in all location to plan the production process and stock related

issues.

2. The cost accounting system is utilized to check stock manufacturing activities and for

recording inventories. This system is used by the top-level positions to track the stages of

inventory from manufacturing to finished product.

3. Job system costing is used to analyse the amount incurred in a product manufactured

with involvement in the business. This system is vital for industry construction and

mention to assigning a cost to the individual project of construction at the company.

5

In this study on accounting management of Cream ltd. the process of accounting management is

being elaborated. The requirement of different types of management accounting systems in

Cream ltd. is going to be explained. The discussion explains the management accounting system

and their application in the organisation. It also focuses on the accounting management system

and management accounting reporting. The study is based on understanding the integration with

the organisational processes. The study is on the understanding of management accounting

technique, calculation of the cost to prepare statement of income using absorption and cost of

marginal. The comparison will be done on organisation adaption to the management accounting

system to revert to issues of finance.

Discuss the MAS

Types of management accounting

The accounting process of Cream Ltd consists of management accounting and accounting of

cost which means analysing the cost of business and the operations to draw up reports of

finance internally, the account which the managers used, records which assists making of

decision process in attaining the organisational goals (van Helden et al. 2016). Different

types of MAS are:

1. Inventory system of accounting which facilitates stock placement in the company. This

system is vital to track the stocks in different locations and managing the supply network

effectively. It is present in all location to plan the production process and stock related

issues.

2. The cost accounting system is utilized to check stock manufacturing activities and for

recording inventories. This system is used by the top-level positions to track the stages of

inventory from manufacturing to finished product.

3. Job system costing is used to analyse the amount incurred in a product manufactured

with involvement in the business. This system is vital for industry construction and

mention to assigning a cost to the individual project of construction at the company.

5

4. Price system for optimisation is used to change the price in accordance with customer

willingness to pay. The company focuses on price optimizing critically as the need to sell

where the product can be easily purchased at given prices whether it is B2B or B2C.

Price optimizing system facilitates selling of a product in such price that company profits

goals are maintained and customer experience is also enhanced.

Methods of management reporting

Different types of methods used in management reporting like

Budgets are related to financial documents in cost allocations are mentioned for future

goals. The financial documents represent income and expenses of Cream ltd. The budget

is basically associated with forecasting the costs in present. Budgets consist of all

expenses like Direct overhead, labour expenses, and purchase of materials.

Variance analysis is used by the company to accumulate the cost involved and what was

estimated and look out for the difference and taking corrective measures for improving

the difference (Ittner et al. 2017). Cost estimation is done by the company for allocating

cost as per the requirement. Sometimes cost estimated exceeds the cost in that case

managers’ needs to check the reason and correct that accordingly.

Cost reports state that the determination of price in accordance with management

accounting. Labour cost, overhead cost, product cost all is taken into contemplation.

Total items are divided by the product cost for the calculation of the entire cost. This cost

report helps the manager to check the cost of the product and selling product price

(Owusu et al. 2016). This cost report assists in managing the plans of manager and limit

of incomes.

Execution reports are used to analyse the data of disbursing the plans with estimated

sums. After making the plan analysis is being done on the whole data. The performance

report is analysed each year, or some company does that quarterly. This data is utilized to

get prepared for the forthcoming call on production and changes (Ioppolo et al. 2019).

These reports are summarized by the accountants of the company and utilized

accordingly. Order place reports are made to place an order and to check whether the

6

willingness to pay. The company focuses on price optimizing critically as the need to sell

where the product can be easily purchased at given prices whether it is B2B or B2C.

Price optimizing system facilitates selling of a product in such price that company profits

goals are maintained and customer experience is also enhanced.

Methods of management reporting

Different types of methods used in management reporting like

Budgets are related to financial documents in cost allocations are mentioned for future

goals. The financial documents represent income and expenses of Cream ltd. The budget

is basically associated with forecasting the costs in present. Budgets consist of all

expenses like Direct overhead, labour expenses, and purchase of materials.

Variance analysis is used by the company to accumulate the cost involved and what was

estimated and look out for the difference and taking corrective measures for improving

the difference (Ittner et al. 2017). Cost estimation is done by the company for allocating

cost as per the requirement. Sometimes cost estimated exceeds the cost in that case

managers’ needs to check the reason and correct that accordingly.

Cost reports state that the determination of price in accordance with management

accounting. Labour cost, overhead cost, product cost all is taken into contemplation.

Total items are divided by the product cost for the calculation of the entire cost. This cost

report helps the manager to check the cost of the product and selling product price

(Owusu et al. 2016). This cost report assists in managing the plans of manager and limit

of incomes.

Execution reports are used to analyse the data of disbursing the plans with estimated

sums. After making the plan analysis is being done on the whole data. The performance

report is analysed each year, or some company does that quarterly. This data is utilized to

get prepared for the forthcoming call on production and changes (Ioppolo et al. 2019).

These reports are summarized by the accountants of the company and utilized

accordingly. Order place reports are made to place an order and to check whether the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

order placed is enough or not. The business reports are made for making an alternative to

present and upcoming situation of the business in a company.

Benefits of management accounting for the business

The management accounting system in Cream Ltd is beneficial in terms of increasing efficiency

of the company. Inventory system of accounting helps the company to manage the supply chain

of the product from manufacturing to the finished product (Lugli et al. 2017). The cost

accounting systems assist the business in tracking the product amount in each level of

production. The job costing systems helps in allocating the cost to a project which is involved in

the business. The price optimization system assists the business in optimizing the product price.

The customer willingness to pay needs to match with the product price. This system helps in

optimizing the cost in the way in which company profits are not hampered.

Evaluation of management reporting and accounting

The management accounting systems and management reporting accounting is integrated within

or business processes as management accounting provides information regarding quantitative

and qualitative on financial and operational production (Ferdous et al. 2019).The management

accounting is associated with the creditors and assets of the business while management

accounting system is enclosed with operational planning and controlling for successful support.

Management accounting facilitates the planning of money and controlling it. Management

accounting system helps the business to use the internal factors like price and quality of product

efficiently to deploy the best customer service.

Steps of management accounting

Analysis of price techniques for statement of income

Statement of income under costing marginal and costing of absorption when there is production

but no sales of Cream Ltd. The data are given below: -

Here in the table cost as per marginal accounting is taken.

7

present and upcoming situation of the business in a company.

Benefits of management accounting for the business

The management accounting system in Cream Ltd is beneficial in terms of increasing efficiency

of the company. Inventory system of accounting helps the company to manage the supply chain

of the product from manufacturing to the finished product (Lugli et al. 2017). The cost

accounting systems assist the business in tracking the product amount in each level of

production. The job costing systems helps in allocating the cost to a project which is involved in

the business. The price optimization system assists the business in optimizing the product price.

The customer willingness to pay needs to match with the product price. This system helps in

optimizing the cost in the way in which company profits are not hampered.

Evaluation of management reporting and accounting

The management accounting systems and management reporting accounting is integrated within

or business processes as management accounting provides information regarding quantitative

and qualitative on financial and operational production (Ferdous et al. 2019).The management

accounting is associated with the creditors and assets of the business while management

accounting system is enclosed with operational planning and controlling for successful support.

Management accounting facilitates the planning of money and controlling it. Management

accounting system helps the business to use the internal factors like price and quality of product

efficiently to deploy the best customer service.

Steps of management accounting

Analysis of price techniques for statement of income

Statement of income under costing marginal and costing of absorption when there is production

but no sales of Cream Ltd. The data are given below: -

Here in the table cost as per marginal accounting is taken.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Unit cost as per marginal

costing

Januar

y

Februar

y

Direct Material £5.00 £5.00

Direct Labour £3.00 £3.00

Variable Manufacturing

Overhead £2.00 £2.00

Total unit cost £10.00 £ 10.00

Figure 1: marginal costing

(Source: created by author)

Unit cost as per Absorption costing January February

Direct Material £5.00 £5.00

Direct Labor £3.00 £3.00

Variable Manufacturing Overhead £2.00 £2.00

Fixed Manufacturing Overhead £4.00 £4.00

Total unit cost £14.00 £14.00

8

costing

Januar

y

Februar

y

Direct Material £5.00 £5.00

Direct Labour £3.00 £3.00

Variable Manufacturing

Overhead £2.00 £2.00

Total unit cost £10.00 £ 10.00

Figure 1: marginal costing

(Source: created by author)

Unit cost as per Absorption costing January February

Direct Material £5.00 £5.00

Direct Labor £3.00 £3.00

Variable Manufacturing Overhead £2.00 £2.00

Fixed Manufacturing Overhead £4.00 £4.00

Total unit cost £14.00 £14.00

8

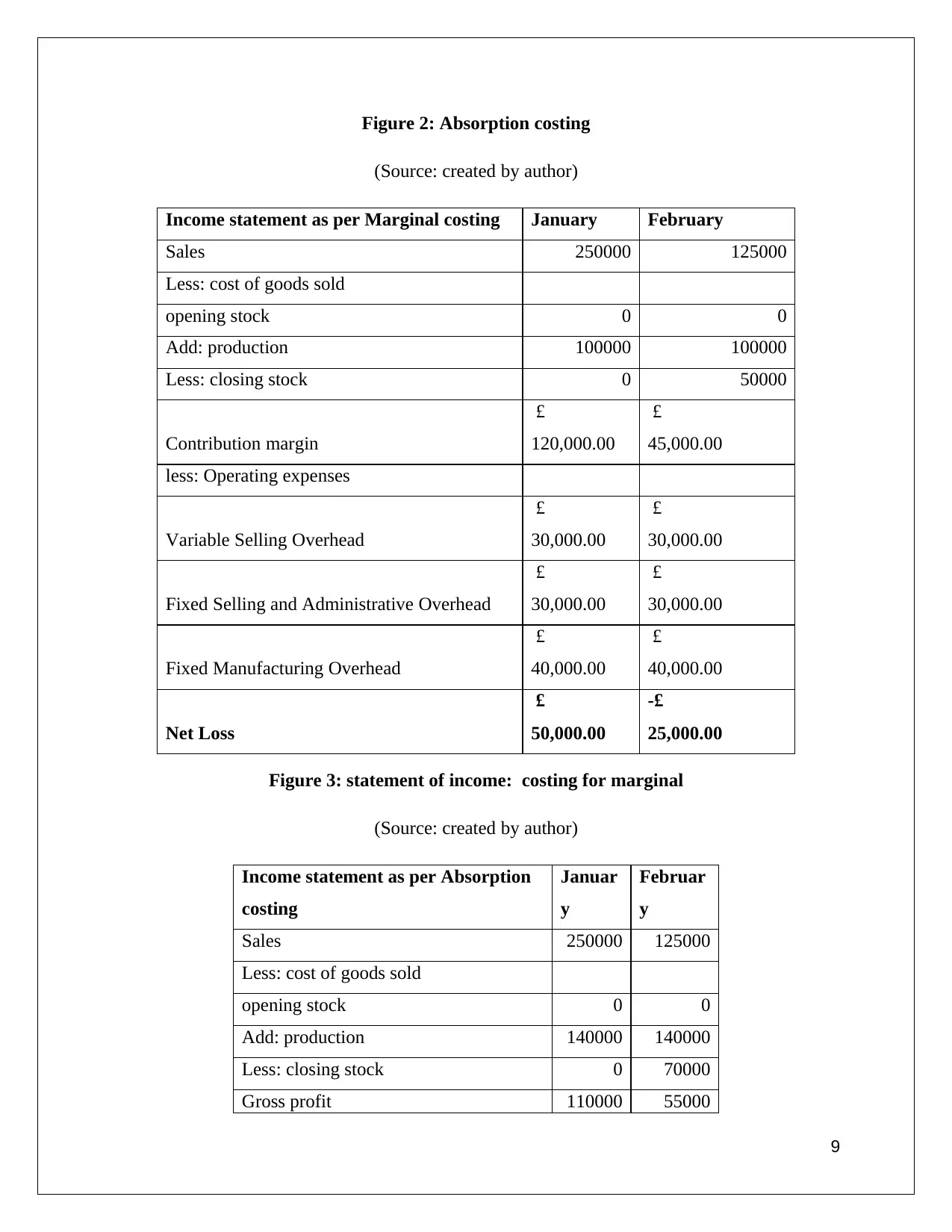

Figure 2: Absorption costing

(Source: created by author)

Income statement as per Marginal costing January February

Sales 250000 125000

Less: cost of goods sold

opening stock 0 0

Add: production 100000 100000

Less: closing stock 0 50000

Contribution margin

£

120,000.00

£

45,000.00

less: Operating expenses

Variable Selling Overhead

£

30,000.00

£

30,000.00

Fixed Selling and Administrative Overhead

£

30,000.00

£

30,000.00

Fixed Manufacturing Overhead

£

40,000.00

£

40,000.00

Net Loss

£

50,000.00

-£

25,000.00

Figure 3: statement of income: costing for marginal

(Source: created by author)

Income statement as per Absorption

costing

Januar

y

Februar

y

Sales 250000 125000

Less: cost of goods sold

opening stock 0 0

Add: production 140000 140000

Less: closing stock 0 70000

Gross profit 110000 55000

9

(Source: created by author)

Income statement as per Marginal costing January February

Sales 250000 125000

Less: cost of goods sold

opening stock 0 0

Add: production 100000 100000

Less: closing stock 0 50000

Contribution margin

£

120,000.00

£

45,000.00

less: Operating expenses

Variable Selling Overhead

£

30,000.00

£

30,000.00

Fixed Selling and Administrative Overhead

£

30,000.00

£

30,000.00

Fixed Manufacturing Overhead

£

40,000.00

£

40,000.00

Net Loss

£

50,000.00

-£

25,000.00

Figure 3: statement of income: costing for marginal

(Source: created by author)

Income statement as per Absorption

costing

Januar

y

Februar

y

Sales 250000 125000

Less: cost of goods sold

opening stock 0 0

Add: production 140000 140000

Less: closing stock 0 70000

Gross profit 110000 55000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

less: Operating expenses

Variable Selling Overhead 30000 30000

Fixed Selling and Administrative

Overhead 30000 30000

Net Loss 50000 -5000

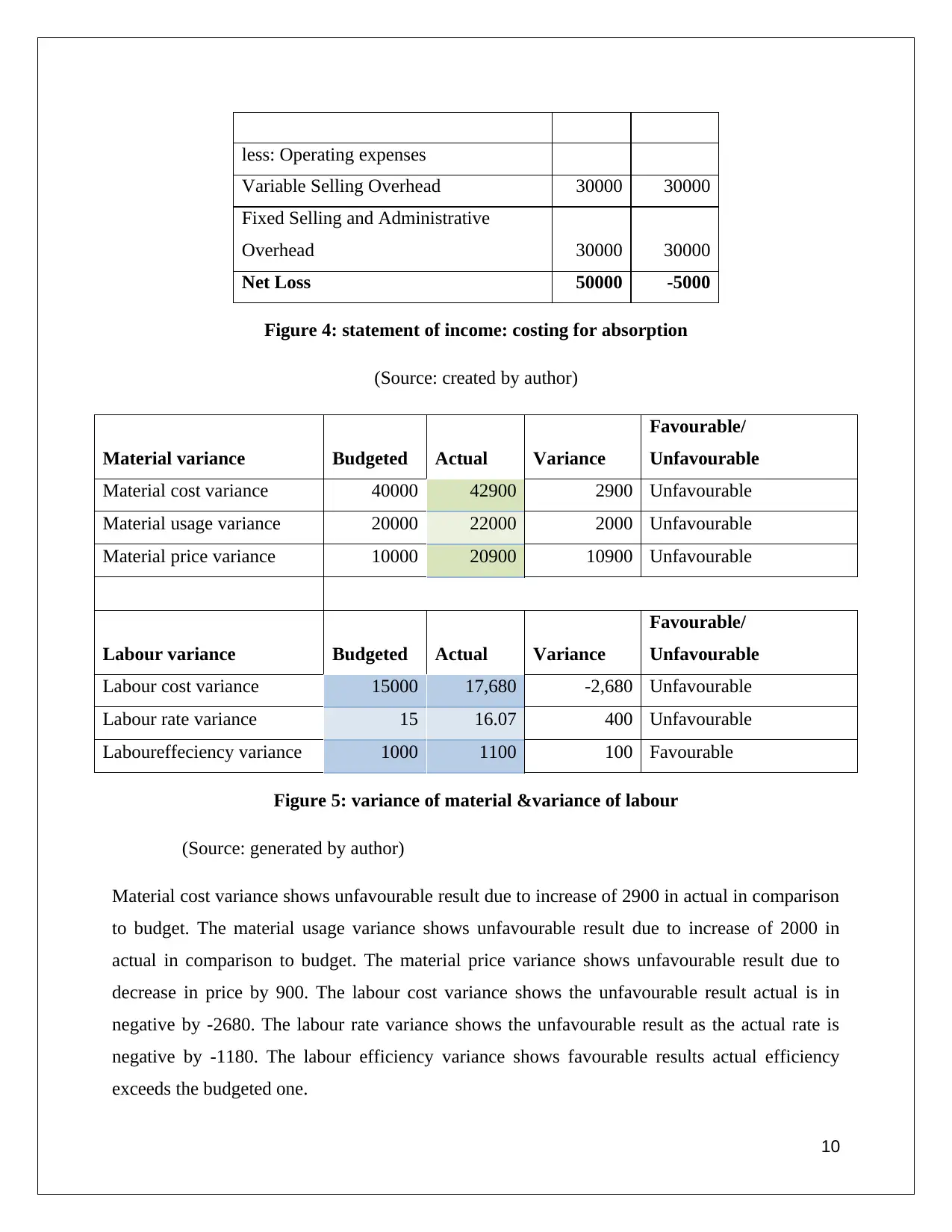

Figure 4: statement of income: costing for absorption

(Source: created by author)

Material variance Budgeted Actual Variance

Favourable/

Unfavourable

Material cost variance 40000 42900 2900 Unfavourable

Material usage variance 20000 22000 2000 Unfavourable

Material price variance 10000 20900 10900 Unfavourable

Labour variance Budgeted Actual Variance

Favourable/

Unfavourable

Labour cost variance 15000 17,680 -2,680 Unfavourable

Labour rate variance 15 16.07 400 Unfavourable

Laboureffeciency variance 1000 1100 100 Favourable

Figure 5: variance of material &variance of labour

(Source: generated by author)

Material cost variance shows unfavourable result due to increase of 2900 in actual in comparison

to budget. The material usage variance shows unfavourable result due to increase of 2000 in

actual in comparison to budget. The material price variance shows unfavourable result due to

decrease in price by 900. The labour cost variance shows the unfavourable result actual is in

negative by -2680. The labour rate variance shows the unfavourable result as the actual rate is

negative by -1180. The labour efficiency variance shows favourable results actual efficiency

exceeds the budgeted one.

10

Variable Selling Overhead 30000 30000

Fixed Selling and Administrative

Overhead 30000 30000

Net Loss 50000 -5000

Figure 4: statement of income: costing for absorption

(Source: created by author)

Material variance Budgeted Actual Variance

Favourable/

Unfavourable

Material cost variance 40000 42900 2900 Unfavourable

Material usage variance 20000 22000 2000 Unfavourable

Material price variance 10000 20900 10900 Unfavourable

Labour variance Budgeted Actual Variance

Favourable/

Unfavourable

Labour cost variance 15000 17,680 -2,680 Unfavourable

Labour rate variance 15 16.07 400 Unfavourable

Laboureffeciency variance 1000 1100 100 Favourable

Figure 5: variance of material &variance of labour

(Source: generated by author)

Material cost variance shows unfavourable result due to increase of 2900 in actual in comparison

to budget. The material usage variance shows unfavourable result due to increase of 2000 in

actual in comparison to budget. The material price variance shows unfavourable result due to

decrease in price by 900. The labour cost variance shows the unfavourable result actual is in

negative by -2680. The labour rate variance shows the unfavourable result as the actual rate is

negative by -1180. The labour efficiency variance shows favourable results actual efficiency

exceeds the budgeted one.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Application of management accounting for reporting for financial

The steps used by management accounting to produce appropriate financial reporting documents

are:-

Financial planning assists in making powerful financial planning which helps in meeting

organisation objectives (Sepasi et al. 2019). This tool technique is stated as the best

technique to achieve organisational objectives.

Statement of financial analysis helps in analysing the two important report of the

organisation that is the profit and loss and profit and balance sheet (Sepasi et al. 2019).

Henceforth this technique assistance can be known as growth of Creams Ltd. This

examination is done through ratio survey, common size statement and financial statements.

Cost accounting states the information related to product-wise, process-wise, department

wise and branch wise. The information of cost is compared with the pre-agreed one.

Fund flow analysis helps n tracking the fund flow from one period to another. The difference

between both the periods is ascertained while tracking. This analysis helps in checking

thoroughly funds are utilized properly or not in the given period.

Standard costing is termed as a predetermined cost. It provides a standard to compute the

performance. It is used to discover diversions if there is any.

Marginal costing steps are used to ascertain the price of selling, choosing the better sales

mix, using the scanty resources, and assisting in buying decision. This technique is built on a

variable cost, fixed cost, and contribution.

The budgetary control technique is associated with meeting future financial demands. It

helps in managing the financial perform in the business concern.

Revaluation accounting technique helps to revalue the assets of the company according to

requirement. It assists the company in ascertaining the capital employed.

Discuss the finance report of business activities

The financial reports like income statement, balance sheet, statement of stock holder’s equity,

cash flow statement and statement of comprehensive reports which play an vital step in making

decision, strategy making, success accomplishment and failure estimation in Cream Ltd. The

financial report helps in interpreting the range of the data by applying accuracy in financial

11

The steps used by management accounting to produce appropriate financial reporting documents

are:-

Financial planning assists in making powerful financial planning which helps in meeting

organisation objectives (Sepasi et al. 2019). This tool technique is stated as the best

technique to achieve organisational objectives.

Statement of financial analysis helps in analysing the two important report of the

organisation that is the profit and loss and profit and balance sheet (Sepasi et al. 2019).

Henceforth this technique assistance can be known as growth of Creams Ltd. This

examination is done through ratio survey, common size statement and financial statements.

Cost accounting states the information related to product-wise, process-wise, department

wise and branch wise. The information of cost is compared with the pre-agreed one.

Fund flow analysis helps n tracking the fund flow from one period to another. The difference

between both the periods is ascertained while tracking. This analysis helps in checking

thoroughly funds are utilized properly or not in the given period.

Standard costing is termed as a predetermined cost. It provides a standard to compute the

performance. It is used to discover diversions if there is any.

Marginal costing steps are used to ascertain the price of selling, choosing the better sales

mix, using the scanty resources, and assisting in buying decision. This technique is built on a

variable cost, fixed cost, and contribution.

The budgetary control technique is associated with meeting future financial demands. It

helps in managing the financial perform in the business concern.

Revaluation accounting technique helps to revalue the assets of the company according to

requirement. It assists the company in ascertaining the capital employed.

Discuss the finance report of business activities

The financial reports like income statement, balance sheet, statement of stock holder’s equity,

cash flow statement and statement of comprehensive reports which play an vital step in making

decision, strategy making, success accomplishment and failure estimation in Cream Ltd. The

financial report helps in interpreting the range of the data by applying accuracy in financial

11

transparency by showing the correct amount in the report of finance of the business. The tax

liability of the company should be correct in accordance with financial report no flaws should

exist (Cooper et al. 2017). The balance sheet of the business contains the assets and liability of

the organisation which help the business activities to work effectively using the assets of the

company properly. The statement of income of the business is a yardstick to measure the success

of the business workings for a specific period of time. The report of cash flow of the

businessstates the flow of fund inside the company and outside the company. It also states the

cash flows of the business activities outside and the speculations in a given period of time. The

statement cash flow is the most important financial report as it shows the flow of cash by which

the investors ascertain the state of the company.

Tools for management accounting

Advantages and disadvantages of planning tools

The positives and negatives of different types of tools of planning used for control of budgets are

Budget is a report which is prepared in each period which is presented by top position in

which allocation of funds is mentioned. The Advantages of the budget are it helps in the

bond building between all the departments of the Cream Ltd. It converts the strategy into

activity. It sates the revenue and expenses requirement for carrying out a plan. It provides

documentation of the activities which are going on in the organisation (Rikhardsson et al.

2018). The disadvantages of the budget are budget is followed rigidly which affects the

motivation of employees and which results in ineffective production. The rigid budget

structure will mitigate the innovation of ideas in the company.

Operational budgets: They are termed to be the plan of finances which is equipped with the

ability for meeting the obligations of debts along with sustainability over longer terms for the

company. In front of Creams Ltd., it can be sated advantageous through letting it know how

they are spending their money along with the area of cash management. However, use of

such tools can be disadvantages for the company also. Creams Ltd. is likely to face

inaccuracies within the financial budget which is likely to change on a frequent basis (Ittner

et al. 2017). In another direction, it can also be disadvantageous to Creams Ltd. through

12

liability of the company should be correct in accordance with financial report no flaws should

exist (Cooper et al. 2017). The balance sheet of the business contains the assets and liability of

the organisation which help the business activities to work effectively using the assets of the

company properly. The statement of income of the business is a yardstick to measure the success

of the business workings for a specific period of time. The report of cash flow of the

businessstates the flow of fund inside the company and outside the company. It also states the

cash flows of the business activities outside and the speculations in a given period of time. The

statement cash flow is the most important financial report as it shows the flow of cash by which

the investors ascertain the state of the company.

Tools for management accounting

Advantages and disadvantages of planning tools

The positives and negatives of different types of tools of planning used for control of budgets are

Budget is a report which is prepared in each period which is presented by top position in

which allocation of funds is mentioned. The Advantages of the budget are it helps in the

bond building between all the departments of the Cream Ltd. It converts the strategy into

activity. It sates the revenue and expenses requirement for carrying out a plan. It provides

documentation of the activities which are going on in the organisation (Rikhardsson et al.

2018). The disadvantages of the budget are budget is followed rigidly which affects the

motivation of employees and which results in ineffective production. The rigid budget

structure will mitigate the innovation of ideas in the company.

Operational budgets: They are termed to be the plan of finances which is equipped with the

ability for meeting the obligations of debts along with sustainability over longer terms for the

company. In front of Creams Ltd., it can be sated advantageous through letting it know how

they are spending their money along with the area of cash management. However, use of

such tools can be disadvantages for the company also. Creams Ltd. is likely to face

inaccuracies within the financial budget which is likely to change on a frequent basis (Ittner

et al. 2017). In another direction, it can also be disadvantageous to Creams Ltd. through

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.